News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Thurly

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

New Alzheimer's Research

They test an acute model. Thoughts?

http://www.neurobiologyofaging.org/article/S0197-4580(16)30087-2/fulltext?elsca1=etoc&elsca2=email&elsca3=0197-4580_201609_45__&elsca4=Neurology|Geriatric Medicine

Abstract

In Alzheimer's disease (AD), cognitive deficits and psychological symptoms are associated with an early deregulation of the hypothalamic-pituitary-adrenal axis. Here, in an acute model of AD, we investigated if antiglucocorticoid strategies with selective glucocorticoid receptor (GR) modulators (CORT108297 and CORT113176) that combine antagonistic and agonistic GR properties could offer an interesting therapeutic approach in the future. We confirm the expected properties of the nonselective GR antagonist (mifepristone) because in addition to restoring basal circulating glucocorticoids levels, mifepristone totally reverses synaptic deficits and hippocampal apoptosis processes. However, mifepristone only partially reverses cognitive deficit, effects of the hippocampal amyloidogenic pathway, and neuroinflammatory processes, suggesting limits in its efficacy. By contrast, selective GR modulators CORT108297 and CORT113176 at a dose of 20 and 10 mg/kg, respectively, reverse hippocampal amyloid-ß peptide generation, neuroinflammation, and apoptotic processes, restore the hippocampal levels of synaptic markers, re-establish basal plasma levels of glucocorticoids, and improve cognitive function. In conclusion, selective GR modulators are particularly attractive and may pave the way to new strategies for AD treatment.

QED, I'm afraid. GLTA — exit on any bounce, if you can.

Alan Leong's latest:

http://alanhobbes.blogspot.co.uk/search?q=Corcept

PG,

I have to use the public board, I don't have a subscription account at IHub.

I haven't been following PPHM too too closely lately. These guys chronically disappoint, IMO. I have major trust issues with them. It's hard to trust the science when you don't trust management.

On top of that, I've been doing well with the two positions I currently hold and don't want to trade out of them until they've run their course.

Best,

LM

Corcept Therapeutics Announces Poster Presentations on Mifepristone

for the Treatment of Patients with Cushing’s Syndrome

at the 27th Annual American Association of Clinical Endocrinologists

Press Release delivered via email

MENLO PARK, Calif. (May 14, 2015) -- Corcept Therapeutics Incorporated (NASDAQ: CORT), a pharmaceutical company engaged in the discovery, development and commercialization of drugs for the treatment of severe metabolic, oncologic and psychiatric disorders, today announced that four posters about mifepristone will be presented at the 24th annual American Association of Clinical Endocrinologists (AACE) being held at the Music City Convention Center in Nashville, TN from May 13 – 17, 2015.

“We are pleased that physicians have taken a strong interest in mifepristone and its potential to treat patients with Cushing’s syndrome,” said Joseph K. Belanoff, M.D., Corcept’s Chief Executive Officer.

In addition to presentation of the four abstracts described below, AACE attendees will have the opportunity to attend a “Product Theatre” talk by Ty Carroll, M.D., whose topic will be “Not-So-Subclinical Cushing’s Syndrome.” Corcept is a sponsor of Dr. Carroll’s presentation.

Friday, May 15, 2015

Poster #131: “Resistant metabolic abnormalities prompting Cushing’s syndrome work-up and treatment with mifepristone”

Douglas Beatty, M.D., Rachel Bunta, Dat Nguyen, PharmD

Poster # 840: “Mifepristone re-established glycemic control in a Cushing’s syndrome patient that relapsed after a 21 month interruption”

Todd Frieze, M.D., James Smith, Ph. D.

Product Theater: “Not-So-Subclinical Cushing’s Syndrome”

Ty Carroll, M.D.

Saturday, May 16, 2015

Late-Breaking Poster: “Use of mifepristone in an ectopic Cushing’s syndrome patient pending tumor localization”

Adeela Ansari, M.D., Precious Lim, Ph.D., Dat Nguyen, PharmD

Late-Breaking Poster: “Improved response to octreotide LAR for ectopic Cushing’s syndrome during mifepristone therapy: A case study”

Andreas Moraitis, M.D., Richard Auchus, M.D.

I asked Corcept about the two patients that were partial responders (at least 30% reduction of target tumors' "longest diameter" total) and got the following reply:

. . . of the two responders, both were breast cancer patients (1 was triple negative breast cancer, 1 was classified as metastatic breast cancer).

CORCEPT THERAPEUTICS’ MIFEPRISTONE COMBINED WITH ERIBULIN TO IMPROVE ANTITUMOR ACTIVITY IN PATIENTS WITH TRIPLE-NEGATIVE BREAST CANCER

http://www.marketwatch.com/story/corcept-therapeutics-mifepristone-combined-with-eribulin-to-improve-antitumor-activity-in-patients-with-triple-negative-breast-cancer-2015-05-13

Patients with metastatic breast cancer (five with triple-negative breast cancer) were treated with mifepristone and eribulin at three different dose levels. The study consisted of seven patients with GR-positive tumors, three patients with GR-negative tumors and three patients with unknown GR status. Two partial responses have been observed, both in patients with GR-positive cancer.

The study title shows it includes patients who do not have triple negative breast cancer:

Mifepristone and Eribulin in Patients With Metastatic Triple Negative Breast Cancer or Other Specified Solid Tumors

https://clinicaltrials.gov/ct2/show/NCT02014337?term=Triple+Negative+Breast+Cancer+mifepristone&rank=1

In fact, the study accepts Breast Cancer, Ovarian Epithelial Cancer Recurrent, Sarcoma, Non-small Cell Lung Cancer, Carcinoma, Transitional Cell, Prostate Cancer, Prostatic Neoplasms

From the title of the press release, one would assume that of the two partial responses, at least one of them was in TNBC, but it's not entirely clear from the text.

What's clear is that both patients had GR-positive tumors and advanced disease.

From the press release: An additional 20 patients with GR-positive metastatic TNBC will be enrolled into the study’s efficacy phase.

Adjusting for CORT's 1 off expense Q1, net revenue increased 36.6% (would have been $12.3M ex-expense). CORT guides a similar Q/Q rate of uptake going forward.

On the phone call referenced in my last post, Robb (CORT CFO) said he hadn't heard Alan shut down BioWatch News. He had great respect for Alan and his research. He said, in his opinion the analyst that now best gets CORT is the MD that comes from FBR.

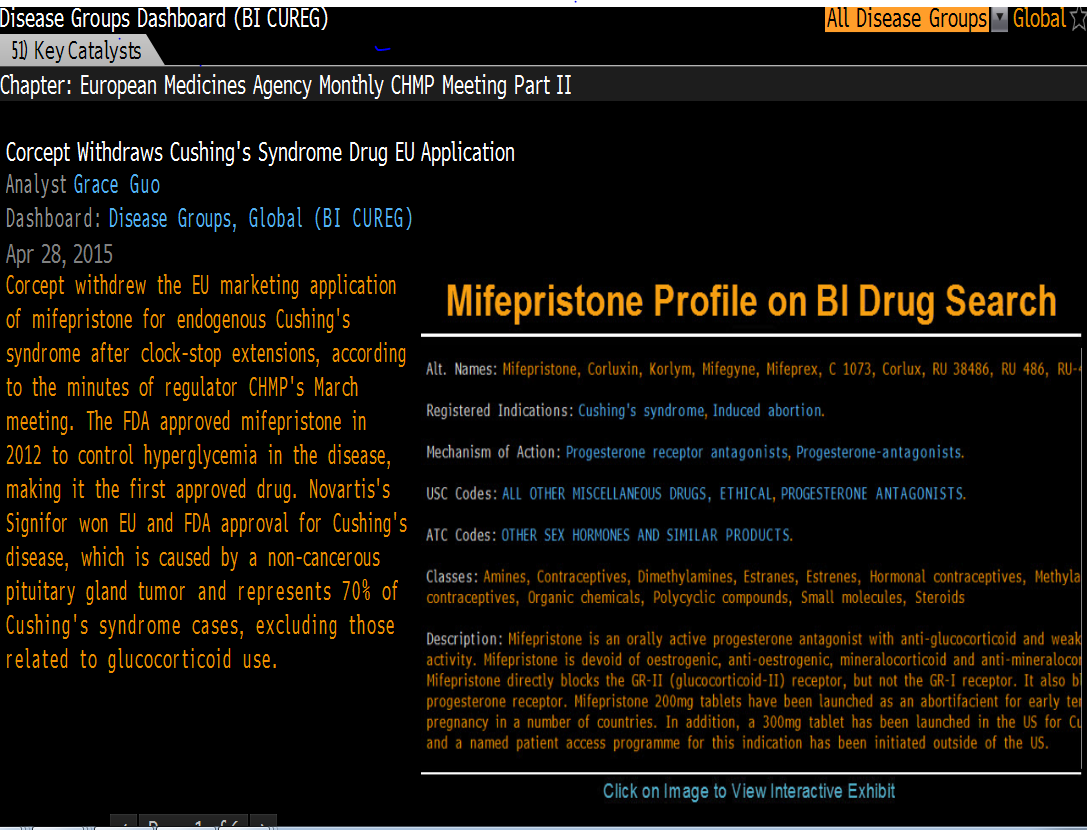

On April 28, 2015 Bloomberg reported Corcept withdrew Korlym's marketing application in the EU.

I asked Corcept about the withdrawal and Corcept's CFO, Charles Robb responded. He said, Corcept withdrew Korlym for strategic reasons.

If approved in the EU, Korlym would be tied to the price of Mifepristone when used as an abortifacient — at about 1/4 the price Corcept charges in the USA for Cushing's.

If Corcept's new compound, 125134 were then later approved for Cushing's, 125134's price would be tied to the lower EU price for Korlym.

By withdrawing Korlym, if and when 125134 is approved for Cushing's, there will be less for the EU to use to limit the sales price of 125134.

By withdrawing Korlym, Corcept can fully enroll the trials for 125134 in the EU, without cannibalizing paying patients.

I didn't ask whether or not the withdrawl would affect their revenue guidance for the year but during the conference call, Corcept reaffirmed their earlier guidance $47–53M.

3, but it's not even close which beer is better. (I like and drink both).

Look at their revenue and break even forecasts.

I expect CORT's shareprice to rise an average of .50 per quarter for the next 5-6 quarters. If they have good results in triple negative breast cancer in 1H15, they will go higher. If they don't have good results, I expect a hit but they will recover to the trend line of .50/quarter after the turmoil subsides.

FWIW

Best. Hope all is well.

Leslie

Robert, I don't have an account right now so I cannot reply privately.

My view, IIRC ex's thoughts on the trial, he's right on the problems the mixup introduced. No statistical help, not really. Help, in the broadest sense only—a signal.

One might take heart in the fact that ex posts here so often. I cannot believe it's only charity that returns him to the board so often. Then again, I don't know ex so I don't know why he posts. His clarity of thought and experience certainly benefits to the board—and is sorely needed since freethemice and mojo stopped posting.

FWIW.

Best always.

We each have to find our own way through the kale.

Wishing you the best.

I tend to discount posters that are predictably positive or negative. I reference ex because of his dispassionate assessment of the Peregrine story. Great respect here for that particular quality.

I have avoided retaking a position in large part because of the ongoing black hole of information as the downside risk is still considerable (even from here).

I'll be more inclined to revisit reinvestment in H215.

Rooting for the longs in any case.

The stock is in a classic small biotech information black hole, there's not going to be any real catalysts for a while. I think ex is right on the PIII trial timing.

I tend to think this bull market continues with increasing volatility for now. The volatility will not be PPHM's friend. Any big correction will hit high beta, info black hole stocks pretty hard.

Not triple negative.

Sport, please clarify. It's not a feature I've ever used. I cannot pm at this time.

Up to 25% in two arms.

We're range-bound until the next catalyst, which is likely the May 7th earnings call. Will uptake of Korlym for Cushing's decelerate? That's what Belanoff hinted at last call. I'll wait and see but, I wonder . . .

Then the interim data . . .

Cook said to make the stock more affordable to investors.

PG,

I do try to keep up. It's not easy.

I recently started taking work in my field again and the workload has been brutal since mid-december. With my girls getting older, I had more free time. This may have been the worst (and best) decision I've made in a while! Rewarding professionally. Even though I work out of the house, I haven't found a way to balance work and family life yet.

I'm not back in yet. My funds are profitably invested elsewhere. I may get back in in a year or two from now.

Depends on developments.

All the best.

Sorry, I just read the thread and didn't realize that the issue of what to make of the trial results had been discussed already.

If entire arms were switched, what is the problem? Unless the arms were mixed dosed, the protocol would seem to be followed. It would bring into question the results of the placebo and 1mg/kg arms though, wouldn't it? If the arms were simply switched, the placebo outperformed the 1kg/mg arm, no?

Is Belanoff saying that in 2014 they will net revenue of $56.2M?

The press release said:

“Korlym® revenue increased 56 percent in the fourth quarter compared to the prior quarter,” said

K. Belanoff, MD, Corcept’s Chief Executive Officer. “We expect our momentum to continue in 2014,

with Korlym revenue reaching the $24 million to $28 million range for the year.”

If "our momentum" (56%) is to continue, 24-28M has to represent Q414 net revenue.

56% growth starting at $4.1M Q413 net revenue would equate to quarterly revenue in 2014 of:

6,396,000.00 Q1

9,977,760.00 Q2

15,565,305.60 Q3

24,281,876.74 Q4

A 457% growth rate.

Yes? Or maybe he's not being specific about the rate of growth, just that positive momentum will continue through 2014.

Sept. 1, 2013

http://www.sciencedirect.com/science/article/pii/S0006322312010876

Mifepristone Alters Amyloid Precursor Protein Processing to Preclude Amyloid Beta and Also Reduces Tau Pathology

Results

Mifepristone treatment rescues the pathologically induced cognitive impairments and markedly reduces amyloid beta (Aß)-load and levels, as well as tau pathologies. Analysis of amyloid precursor protein (APP) processing revealed concomitant decreases in both APP C-terminal fragments C99 and C83 and the appearance of a larger 17-kDa C-terminal fragment. Hence, mifepristone induces a novel C-terminal cleavage of APP that prevents it being cleaved by a- or ß-secretase, thereby precluding Aß generation in the central nervous system; this cleavage and the production of the 17-kDa APP fragment was generated by a calcium-dependent cysteine protease. In addition, mifepristone treatment also reduced the phosphorylation and accumulation of tau, concomitant with reductions in p25. Notably, deficits in cyclic-AMP response element-binding protein signaling were restored with the treatment.

Patent Application/Publication, Jan 2, 2014

Use of Mifepristone for the Treatment of Amyotrophic Lateral Sclerosis

http://www.google.com/patents/US20140005158

CLAIMS(20)

What is claimed is:

1. A method for ameliorating the symptoms and/or slowing the rate of disease progression in a patient diagnosed with amyotrophic lateral sclerosis (ALS), the method comprising administering a therapeutically effective amount of a glucocorticoid receptor specific antagonist (GRA) to a subject in need thereof, with the proviso that the subject not be otherwise in need of treatment with a glucocorticoid receptor antagonist.

I understand that you believe that. I do not. Is it a placebo? I don't know. I suspect some efficacy, but the data has been so tarnished by irregularities I don't have any confidence in it at this point. The only way we are going to know is if they ever complete the PIII without additional irregularities cropping up. That's why I wrote: TBD.

Has anybody been consistently right or wrong about bavi or PPHM? TBD, isn't it?

Peregrine touted their 2nd Line PIIb as a gold-standard trial. It turned out to be a standard screwup for PPHM. Like the HFV government contract that they said they were confident would be renewed; like the PIIb 1st Line trial that read well in December but not in March when independent eyes evaluated the data . . .

I don't say that the current bavi PIII won't return stat. sig. but PPHM has given her critics ample, legitimate cause to be skeptical of the company and, as a result, all of its data. I can't see how anybody could be critical of the PPHM skeptics at this point given PPHM's track record and the sad state of their statistical data going into this PIII.

http://www.expertreviews.co.uk/pcs/1304572/apple-mac-pro-2013-sold-out-world-wide

Apple's high-priced Mac Pro has already sold out, with the company now unable to supply units until February 2014 for orders placed from today.

The problem with TNBC is, I believe, that the ORRs don't translate in OS very well (with chemos).

I'd rewrite your sentence as follows:

The complaint says ABV was willing to look at the data, but when the dose mixup was discovered, they backed out because what the company had been presenting was false and misleading.

To be clear, it doesn't say that additional problems with the data were discovered.

I take the document as being investor neutral. It accords with what is already known about the facts and Peregrine's potential liability.

IMO

Ted Talk — Jack Andraka, the kid who changed pancreatic cancer detection.

http://www.ted.com/talks/jack_andraka_a_promising_test_for_pancreatic_cancer_from_a_teenager.html

I think there's a good chance that bavi works based on the 3kg/mg arm. It just hasn't been proven to any reasonable certainty and we're years away from the getting proof one way or another.

Like you, I hope the data goes PPHM's way.

Okay, that's the last post on this . . . :o)

The 60% improvement is based on what? The FARGO f?!@# up trial data . . .

Although interesting anecdotally, not particularly useful in a regulatory environment or, even a scientific one. Very few conclusions can be drawn, none with any reasonable degree of certainty.

Some people at the FDA may feel sympathetic, but the agency isn't going to lower its approval standards because Peregrine got royally screwed.

The reason I posted initially was that the timelines for PPHM's happy surprise or tragic demise looked clearer to me—four and a half years at the earliest. I'll leave it at that 4 now, unless I come to believe that my conclusions are wrong.

GL2ALs, still rooting for you despite my pessimism.

Quick reply CP,

We disagree on how the FDA views the data. They aren't persuaded that there has been any compelling evidence of efficacy—no strong signals, not even close to stat. sig. since Fargo blew stat. sig out of the water.

What they have seen is that the safety data is good so far. Given that, they are allowing the PIII.

Does Bavi work? TBD. We'd all like to believe it does.

You should be careful about reading the tea leaves. You may have sufficient reason to believe your conclusions but do the conclusions follow necessarily. There's a big difference and the number of alternative possible reads of the same evidence are legion.

We should get together some time. I read your neck of the woods has one of the highest "happy population" quotients in the world. I'd love to come see why . . . !

If the interim look succeeds, the share price will soar and the ATM will become a more effective form of capital.

But how long will it take to get to the peek? I don't personally think the trial will enrol quickly. If it takes 1.5 years to enrol half the patients (best case scenario in my VHO), it will take another 3 years to get to the OS peek.

IMO, it's unlikely that BP will risk big bucks on a partnership considering the irregular state of the bavi data. Risk management necessitates a more definitive proof before inking a costly deal. At this point, the data is, functionally, a black hole—there are huge biostatistical uncertainties.

Peregrine will have to fund the trial and the rest of its business through the peek at minimum.

I don't agree with your loan analysis. We wouldn't have needed the ATM if Fargo hadn't happened, we would have partnered. So terribly sad.

All above IMO

New BSR Alert on Corcept, if you subscribe. Cannot share details due to licensing agreement.