News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Arctec

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

What part of Pinksheets.

Do you not understand?

What has been promised??

There have been no press releases.

As you have said the filings are incomplete.

So nothing has been promised.. Nothing

This is a pink sheet stock, that hasn't filed for 10 years..

OTC Reporting Standards.

Regulation A Reporting Standard: Companies subject to the reporting obligations under Tier 2 of Regulation A under the Securities Act must continue to file, on an ongoing basis, all annual, semi-annual and other interim reports required to be filed on EDGAR. Audited annual financial statements must be prepared in accordance with Regulation A. Additional disclosure obligations, like quarterly filings and annual certifications must be posted, in order to comply with the eligibility requirements of the OTCQX and OTCQB Markets

https://www.otcmarkets.com/learn/reporting-standards

Hi.

Hope you are doing well....

Check your e - mail as I'm going to send you one

By Thanksgiving, I will have all monies out of USD accounts. I will only have minimum monies in CAD accounts. All of my assetts will be held strictly by me with no 3rd party in between. Also note that I won't have any paper assetts!!! Have lots of food stocked up...

Hey Tack, John, Ed, Rocket. Hope you guys are doing great and make it through this mess OK.

Ya. He couldn't do it with Gold, copper or U. might as well get dirty with coal.

Well NAG will prolly run over a buck now that I won't ever buy anymore.

Well have a good summer. You won't be seeing me around here for a while.

Coal is King!!!!

I don't have anything good to say about these guys.. So I won't sayanything..

What a beautifull sight.

Cline Mining.

Fording Canadian Coal Trust (FDG.UN : TSX : $70.20), Net Change: 2.69, % Change: 3.98%, Volume: 594,287

Grande Cache Coal* (GCE : TSX : $6.98), Net Change: 0.51, % Change: 7.88%, Volume: 2,573,194

Western Canadian Coal* (WTN : TSX : $5.85), Net Change: 0.70, % Change: 13.59%, Volume: 5,364,523

4-3-2-1...Earth below us, drifting falling, floating weightless, calling calling home...Canadian coal stocks continue to run as

analysts expect coking coal prices to stay high for longer. Media reports are saying that some producers are demanding up to

$350/tonne this year, which is higher than the benchmark set by BHP Billiton (BHP). While some expect the Queensland

supply situation to return to normal through 2008. Others say infrastructure constraints both in Queensland and elsewhere

around the world should limit potential supply growth for at least the next two or three years. Canaccord Adams' benchmark

2008 coal-year contract price forecast is US$300/tonne for hard coking coal and US$245/tonne for ULV PCI coal. Under

"High" case commodity price assumptions there still remains significant upside to Canadian coal stocks from current levels.

The trend seems to me that it is up. Untill the election anyway. But could change on a moments notice. I still wouldn't buy a bank stock with someone elses money.

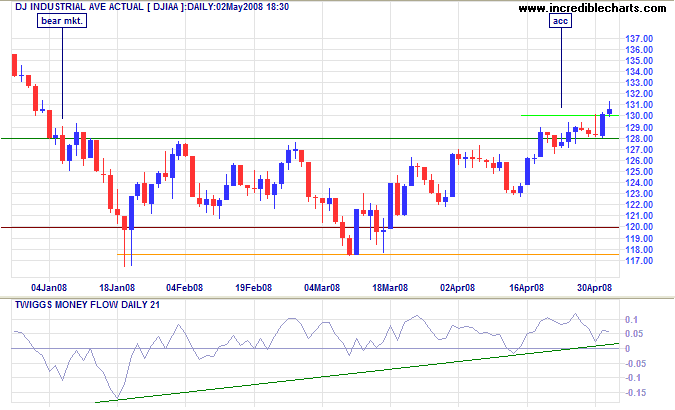

The Dow closed above 13000, confirming the breakout, after a short retracement respected the new support level at 12800 — signaling buying pressure. Twiggs Money Flow holding above zero confirms the buying pressure signal. Reversal below 12800 is now unlikely and would warn of another test of 12000/11750.

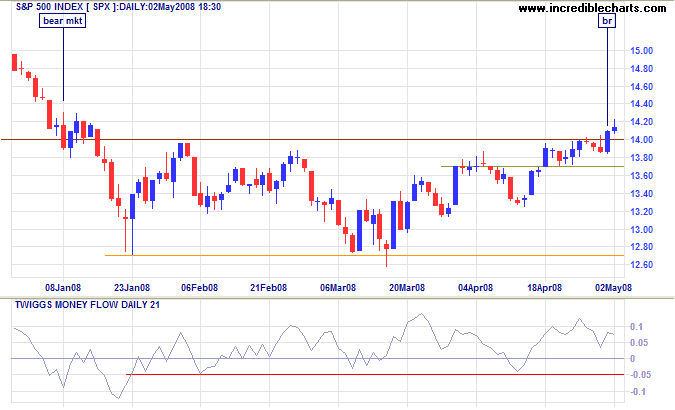

Long Term: Dow purists may disagree (the January reaction only lasted 8 days but retraced roughly half of the previous decline) but the breakout should be treated as a reversal of the primary trend. The signal has now been confirmed by the S&P 500.

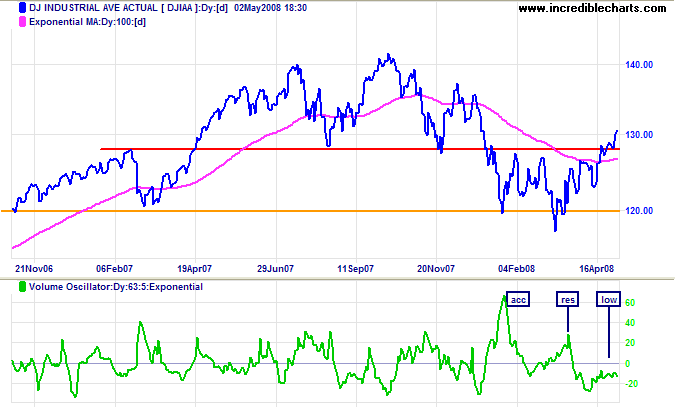

The Volume Oscillator (63,5) highlights unusual activity levels. A large spike in January shows strong support at 12000. The March spike, on the other hand, shows resistance. However, the index continued to rise, indicating that sellers were overwhelmed by buyers. We would normally see a similar pattern at the April breakout, but low levels indicate an absence of sellers, who would normally be expected to recoup some of their earlier losses as prices recovered. These potential sellers remain in the wings and could strengthen resistance at the previous high of 14000.

Buffett says he bought $4-billion of auction-rate debt

Joan Gralla and Jonathan Stempel

Saturday, May 03, 2008

OMAHA, Neb. — Warren Buffett Saturday said his Berkshire Hathaway holding company bought $4-billion (U.S.) of auction-rate securities during the market's recent distress.

Speaking at Berkshire's annual shareholder meeting, Mr. Buffett also said his new municipal bond insurer, Berkshire Hathaway Assurance Corp., is becoming a major force, capturing higher premiums than rivals that have been strained by exposure to subprime mortgages.

The $330-billion market for auction-rate securities, which are long-term bonds whose rates are reset periodically, froze this winter.

Investors flooded dealers with paper backed by bond insurers whom they feared would lose their “triple-A” credit ratings. As a result, many municipal bond issuers were for several weeks forced to pay uncommonly high interest rates.

Mr. Buffett spoke of how debt issued by the Los Angeles County Museum of Art fetched a 3.15 per cent interest rate on Jan. 24, and 8 per cent just three weeks later.

He also said Berkshire has bought auction-rate debt with an 11.3 per cent rate from one broker, at the exact time another broker was offering a 6 per cent rate.

“Those are huge dislocations in the market. That's crazy,” Mr. Buffett said. “Those are great times to make unusual amounts of money.” He said, nonetheless, that Berkshire, whose market value is more than $200-billion, is so large that such investments won't have a big impact on results.

Mr. Buffett also confirmed that the bond insurer he created in December was rapidly increasing market share, having won some $400-million of business in the first quarter.

Berkshire Hathaway Assurance has won “triple-A” ratings from Standard & Poor's and Moody's Investors Service.

While some rivals such as MBIA Inc. and Ambac Financial Group Inc. have also carried those ratings, Mr. Buffett said some market participants are willing to pay premiums above 2 per cent. That's well above the 1 per cent to 1.5 per cent that those other insurers typically charge.

He also said almost all of the secondary business came from issuers that already had insurance from rivals.

“It tells you something about the meaning of ‘triple-A' in the bond insurance field in the first quarter,” Mr. Buffett said.

Mr. Buffett also confirmed that in the primary market, Berkshire has insured nearly $400-million of Detroit sewer and water disposal system bonds.

In addition, he praised Ajit Jain, the Berkshire insurance executive who has overseen the development of the bond insurer. Many analysts and investors have said Mr. Jain is a top candidate to eventually succeed Mr. Buffett as Berkshire's chief executive.

“Ajit has done a remarkable job in this area,” Mr. Buffett said. “It's pretty remarkable, and I congratulate him for it.”

The Dow Industrial Average reversal to a primary up-trend has now been confirmed by the S&P 500. Expect a test of the 2007 highs at 14000. While the market is recovering, this is more a function of cheap money than a booming economy — the old maxim still applies: Don't fight the Fed. Milder than expected employment losses may hint at a soft landing, but the housing market collapse and resultant credit squeeze are likely to plague the economy for some time. Banking, housing and other cyclical sectors should be treated with caution.

The FTSE 100 and Nikkei 225 have also confirmed the Dow signal, while Asia-Pacific markets all look promising

There won't be a mine John. 'specially from these guys.

COW

Between you T, and John. That shouldn't be a prob.

Pullback from a 450% Run 10 days Ago, the GAP story is Fascinating

Major Implications For Cancer ?

Microcaps (and penny stocks in general) can be both exciting and very frustrating. While volatility seems to be the norm, every decade we also see something astonishing come out of a few of these small companies. Astonishing may mean a stock like Bre-X that starts out near 0.40 and ends up near $300 before someone is thrown out of a helicopter. Or it may mean honest discoveries like Diamet that went from penny status to a diamond mine worth Billions, Diamond Fields massive nickel discovery at Voisey Bay, Arequipa's gold discovery and buyout by Barrick in Peru. There are several more like this and likewise for the oil & gas industry.

The interesting part of all this, is that these are resource stocks. Success stories in the tech space we watched in 1999 and 2000 thanks to irrational exhuberance and an overheated market - although some amazing stories came out of that era like Research in Motion and their Blackberry which drove the price from under $3 to well over $100 now.

While all this is the stuff dreams are made of from a financial point of view, they did nothing to contribute to the betterment of mankind. Unless of course you count the Blackberry which for some is as critical as an oxygen tank attached to an emphysema patient ! And by betterment I mean contributing to our quality of life, not buying a new Lexus because your stock just went from a dollar to twenty.

So that brings us to the Biotech sector. From a microcap perspective, its often very difficult for these little companies to raise capital and as such, you rarely hear about major discoveries coming out of this field of science. Thanks to heavy regulation, they can take years to mature and if something significant does comes along, the majors typically buy them out before a massive double digit run in share price can occur. I've been buying penny stocks for over twenty years now and while I'm sure I've forgotten something by now, I cannot remember a huge biotech story coming out of Canada (from a small or microcap perspective).

That brings us to PharmaGap (GAP.V $0.35)

www.pharmagap.com

First and foremost. My introduction above is not meant to indicate this is the next retirement income plan. It simply demonstrates the potential of microcap stocks and proves that while its very difficult hitting a home run on these stocks, its also possible.

I typically don't bother with biotechs because very few ever amount to anything before they run out of cash, and I don't have the patience to sit on a penny stock for three years waiting for a miracle to occur. In addition to this, you need a very strong stomach for volatility. Pharmagap is a perfect example as it gained 450% in 1 day after running from $0.20 to $1.10 on April 17th as millions of dollars worth of buying piled into this stock. Yet you see the price now.

The morning of the 17th we sent GAP to our paid subscribers once a very important news release was issued. While everyone watched this incredible rise in price, we've now watched that same stock get destroyed from its high. The problem can be summed up in one word... traders. A tremendous amount of buying came into this company on news I will highlight below but with little happening in this market for the technical traders, it didn't take long for the gains and volume to pop onto the TSX.V radar. If momentum is positive, the trend remains intact. If the tide turns, so does the share price. As the price fell, the traders moved out and those who bought for a longer term hold likely second guessed their decision and cut a quick loss. People typically read into a trading pattern following news and use this to try and determine whether their assesment was right or wrong.

What all this "may" have done, is create a new opportunity for others. Had this stock not fallen back so hard I would have waited a long time before introducing it to free subscribers or on Stockhouse - the risks were just way too high. Even right now, the risks may be very high. This stock rarely ever traded prior to this news and the last few financings were done at $0.06 by the CEO. Unfortunately this company was so low on anyone's radar that the price and volume were ridiculously low.

World Class Management & Researchers

It was also this very same reason I (at first) totally ignored the news release I saw on April 17th. I honestly thought that in typical penny stock fashion it was nothing more than hype to help some slimey promoter get his stock off. It wasn't until I quickly did more research and found out this company was a spinoff from the National Research Council of Canada (Canada's premier biological research organization) and the scientists behind this company were (surprisingly) amongst the best in their field. In addition to the scientific side, they have tremendous talent on the other side of the equation. As an example, their Chief Operating Officer was Vice President, Investment Banking with Credit Suisse First Boston in New York and TD Securities in New York and Toronto. This quickly ruled out the slimey promoter theory and immediately provided credibility.

Why the Excitement ?

In early trials on mice (announced April 17th), they treated a control group that resulted in tumours disappearing in 4 of the 5 with the 5th having enough damage to the tumour it could be easily broken down. In all other control groups (including chemo), there was no impact and the tumours would have resulted in death. What was amazing, this result was on a cancer type that accounts for 30% of all breast cancer with NO known treatment. Basically it moves so fact (typically to the lungs) that the patience dies in a short period of time.

In addition to this, they had excellent results on colon cancer treatment as well. Its this impact on the breast cancer tumours that is amazing however. If this continues and can be proven safe for humans, it "may" become a major breakthrough in cancer treatment.

The Memorial Sloan-Kettering Cancer Institute New York

www.mskcc.org

In an independent validation of GAP's potential, the company announced on April 24th they were partnering with The Memorial Sloan-Kettering Cancer Institute of New York - one of the world's premier cancer centers. This is over and above the research being done on breast cancer mentioned above. The Institute will be working with the company to develop a selective inhibitor of PKC theta for use in treatment of sarcomas, cancers of supportive and connective tissue (that is bone, cartilage, fat, muscle and blood vessels).

Said Sloan-Kettering's Dr. Schwartz: "I look forward to continuing my collaboration with PharmaGap for this exciting new compound, as it holds the promise of new treatment alternatives in the future for sarcoma patients. Selectively targeting PKC theta may provide therapeutic benefits not provided by current treatments."

Protein Kinase C (PKC)

Over the ages, experimental biology has used two research approaches, in vitro (within the glass) and in vivo (within the living). Typically drug candidate selection and experimentation occur at the simpler "test tube" level. The final proving ground is at the living level of Mice and Men and clinical trials.

Enter the Brave New World of computer biologists and their approach - in silico (within the silicon chip) where computer simulations model natural and laboratory processes.

PharmaGap is on the leading edge of in silico drug development. Their primary candidate, PhG-alpha-1, is one of a new breed of targeted cancer drugs that largely confine their activities to the tumor cells. Consider the huge benefit of hitting the target with a bullet compared to standard "shotgun" chemotherapies, where the hope is that they kill the cancer before they kill the patient.

PharmaGap's current research centers on a family of naturally occurring enzymes known as Protein Kinase C (PKC). These enzymes have diverse and important effects on our cells. They must be highly regulated or controlled to maintain certain aspects of that delicate balance known as health. Numerous cancers involve over expression of PKC - too much of a good thing.

One member of the PKC family is especially noteworthy in the cancer realm - PKC alpha, which is the selected target for the PhG-alpha-1 drug.

Besides targeting, another very positive angle for PhG-alpha-1 relates to an unfortunate characteristic of many cases of cancer - Multi Drug Resistance or MDR. Special proteins embedded in the cell membrane, called MDR pumps, actually "spit out" any chemotherapy drug that enters the cancer cell - great for survival of the cancer cell, but certainly not the patient. There is a strong correlation between high levels of PKC and MDR activity. Perhaps PhG-alpha-1 could be a stone that kills two birds at once. The strategy of combining PhG-alpha-1 with other chemotherapeutic agents may open up a wider range of possibilities.

The area of PKC research is receiving much attention these days, and for good reason. Other members of the PKC family are implicated in such disorders as diabetes, cardiac disease, and Alzheimer's. PhamaGap recently announced they are pursuing drugs to combat PKC theta (cancer again) and PKC epsilon (Alzheimer's).

In the world of biotech drug development, success has been, and continues to be, a very elusive dream - not unlike the discovery of a multimillion ounce gold resource. And PharmaGap is not the only company in the PKC arena. But with some of Canada's best and brightest working on the leading edge, PharmaGap merits serious attention.

From its inception in 1999, PharmaGap has undertaken the scientific research and development work required to understand the many ways in which the 11 unique isoforms making up the family of proteins named Protein Kinase C (PKC) act within the human body in relation to human diseases. PharmaGap has developed proprietary computer-based methodologies that provide the ability to design selective inhibitors for PKC isoforms.

The importance of the PKC family is well known in the medical and pharmaceutical industry and has been and continues to be the subject of significant preclinical and clinical research.

PKCs are associated with a range of human disease conditions, including not only cancer, but also metabolic diseases such as diabetes (PKC beta, epsilon), cardiac disease (PKC delta), Alzheimer's (PKC epsilon) and neurological disease (PKC gamma). In addition to its compounds targeting PKC alpha and theta, PharmaGap has designed, and is currently optimizing prior to synthesis and testing, an inhibitor for PKC epsilon.

April 17th News Excerpt

You can grab the full news release at www.stockhouse.com or any service you typically use, but here is the most important excerpt: The other control groups they used were: saline only, PhG (their drug) along with Chemo, and Chemo Only. The control group with their drug only PhG is referenced below - this is what killed the tumours

Breast cancer metastatic model

In this model, human breast cancer of the type Estrogen Receptor negative, which as a group represents the 30 per cent of breast cancers which are not currently treatable by available drug therapies, were implanted into the bloodstream and provided with a seven-day period to allow tumours to form. The type of cancer cells implanted is known to be highly invasive to the lungs, within a three- to five-day period following implantation. Following this establishment period of seven days, the treatment regime began in the eight groups of five mice.

In the group of five mice receiving PhG-alpha-1 at the dose of one milligram per kilogram of body weight, four of five (80 per cent) when euthanized at the end of the trial period were observed to be tumour-free on postmortem examination, with no effect on other organs. The remaining mouse had developed a single small, friable (easily broken down) tumour. In the two control groups (saline and chemotherapy alone), nine of 10 (90 per cent) developed tumours, with only one surviving to the end of the trial and with ancillary organ damage to some degree. For all other treatment groups, 22 of 25 (88 per cent) developed tumours, and none survived to the end of the trial, again exhibiting ancillary organ damage.

Taser Intl. (TASR : NASDAQ : US$7.53), Net Change: -1.89, % Change: -20.06%, Volume: 15,997,852

Putting the barb back in “barbarism”. It's been a really long time since we've composed a cathartic diatribe against this guiltybefore-

charged product maker. So, here goes nothin'...Speaking of nothin', the company earned $1.2 million ($0.20 per share) in

Q1 vs. the $0.5 million earned in the year-ago period. Look on the bright side, EPS did double. And you still haven't been

zapped yet for not paying your SkyTrain fare. Revenues were up 47% to $22.5 million. That's a net profit margin of about

4.44%. Look on the bright side, that's more than what Wal-Mart (WMT) earns (on the other hand, Wal-Mart is a viable

company). And don't forget that the company is working on some neat (if not tidy) next-generation products such as the Taser

XREP and Taser Shockwave area denial system. The XREP is a "wireless" barb that is shot out of a shotgun and can fly up to

65 feet. As for the Taser Shockwave, check out the video on gizmodo.com. Go trick-or-treating to the wrong house and your

kids might pay for it.

I can see it now.

Come on down and apply for our new Ultra Low Subprime Mortgage!

Sorry, I'm not politicaly correct. They are getting Taserd to death!! LOL

These guys are getting beat up.

They don't need any money. Got 60 mill in the bank. Sales are growing by 47% a year. Lots of interest from the international community.

They are getting sued by an otc company for false advertising relating to a product comparison. Stinger Systems are the ones that are suing them. STIY. Note that Stinger also has 11 charges against it by the sec.

Can you do order entry on it?

I don't know how to swim!!

A few years later and Rudolf Diesel’s body is found drifting face down in the English Channel.

SKF AMEX ProShares UltraShort Financials ProShares Top Triangle $98.50 Target Price $48.00 - $57.00 Intermediate-Term Bearish

That is what I want one for. to take to work.

Unlimited means unlimited hours through the day, not unlimited band width. That is what is in my land line contract.

Holy Moly. Telus here says that they have an unlimited plan for a 100 bucks a month. I'll check it all out real close before I do anything. Prolly a waste of mone as cell phone service in the mountians isn't very good anyway. and a guy should always be able to find a place in a town to get a signal.

OK. I guess I'll have to try it out. i don't know anybody that does either.

Do you know anybody that uses a cell?

Back to 1.36.9 this morning.

What do you use for a modem to run your laptop? do you plug your cell phone into it or just use it at the hotel where there is service?

Yes. last week.

Yep. That is why we have to invest/ trade wisely.

Yep. It is cheaper once a guy is out of the GVRD.

Was 1.29.9 last week 1.36.9 yesterday and 1.39.9 this morning.

To buy vegetable oil is no cheaper than diesel. Unless you get used stuff from a resturant for free.

If i were you I'd get rid of the Ford and buy a Dodge. Can't beat those cummins.

The lost boys of oil and gas are back

NORVAL SCOTT

Friday, April 18, 2008

CALGARY — — David Johnson remembers the dark days of last winter, when interest in small oil and natural gas companies like his was so low that investors in Toronto wouldn't even bother meeting with juniors seeking to raise money.

His company, ProEx Energy Ltd., has been chasing gas in unconventional plays in northeastern British Columbia since 2002, and has built up an attractive collection of prospects and healthy and growing production. He had enough money to operate, but investors had lost interest and the stock had fallen to a three-year low.

What a difference a winter — and a big leap in natural gas prices — makes. Since December, ProEx's stock is up 50 per cent, money managers are clamouring to get into its Montney play and Mr. Johnson can finally afford to sneak away to his boat off the Gulf Coast of Florida for a respite from the renewed energy rush.

"From an investor perspective, what's changed is the fundamental rejuvenation of the industry," he said this week from the deck of his boat.

"When you have one breakthrough it really sparks a whole series of incremental advances that are revitalizing the Western Canadian basin. It's got everyone pumped up, myself included."

Oil hit new records this week — including a record trade of $117 (U.S.) a barrel yesterday afternoon. That's created anxiety among motorists and economists but put the bloom back on the rose of Alberta's junior oil and natural gas industry and its increasingly unconventional resource plays.

The share prices of companies with exposure to those potentially lucrative areas are through the roof and interest in providing financing to them is returning in tandem, with a spate of major deals seen this month alone. (Measuring a cross-section of more than 100 companies, ARC Financial's Junior Producers Equity Index has risen by about 20 per cent in 2008. The TSX composite is up 2.9 per cent.)

While high oil and gas prices play a huge part in the turnaround, they're not the only factor. Investors, fleeing the carnage of the financial sector, are seeking a safe haven for their cash — and they appear to be attracted to the promise of new technology that is taking companies like ProEx and Birchcliff Energy Ltd. to new frontiers. Another unconventional gas player, Birchcliff's stock has more than doubled since December, prompting the company to launch a new equity issue in February that was oversubscribed by at least twofold.

It's a dramatic shift in sentiment. The junior sector had been wallowing in misery for nearly two years, a slump that started with the implosion of the country's energy trusts in 2006, when Ottawa took away the popular option that had created a wealth of buyers for the growing assets of junior companies.

A cocktail of other factors — disappointing gas prices, higher costs, and changes to Alberta's royalty regime — had driven investors further away from the sector. Share prices bottomed out in December and January. Lines of credit ran dry. The outlook was bleak.

What changed wasn't just perceptions of where commodity prices were headed, although that didn't hurt. Instead, there was a realization that junior companies are mastering the exploitation of unconventional resources at a time when demand for oil and gas looks to be stronger than ever — a heady combination of factors that, to many investors, smells of substantial long-term gains.

"The basin is changing, and the business model is changing too. Conventional firms can still be successful, but the economics are getting more difficult, in Alberta especially," said John Chambers, president of Calgary-based First Energy Capital Corp. "Resource plays — with their longer reserve lives — are the focus."

NEW FRONTIE RS

For Canada, the sea change is not the return of juniors but the fact that their hottest fields aren't necessarily in Alberta, the country's traditional oil and gas home. Companies are looking to the booming Bakken and Shaunavon oil fields in Saskatchewan, and even to the possibility of producing gas from shale rock in Quebec.

The greatest excitement, however, is in the Montney play, located mostly in northeastern British Columbia, although it extends into Alberta. (It gets its name from a B.C. town close to the Alberta border, northwest of Fort St. John.)

Montney is estimated to hold as much as 50 trillion cubic feet of gas (tcf), more than the proven reserves for all of Alberta (41 tcf). The challenge: How to profitably extract the resource at current prices.

The development of new fracturing techniques — in effect, setting off underground explosions to free the gas — has made that possible, so much so that Montney is now seen as viable. Companies don't have to do much more there than dig another well next to the one that's already working, rinse and repeat, and watch the money roll in.

Doing just that, Duvernay Oil Corp. is also feeling the Montney love. The large Calgary-based junior produces more than 20,000 barrels of oil equivalent a day. Its stock has almost doubled in value since December to all-time highs, as dramatic successes at Montney helped boost both production and estimates of its oil and gas reserves.

Earlier this week, Duvernay launched a $77.4-million (Canadian) bought-deal financing — a deal in which a broker buys new shares in a company in exchange for guaranteed cash, before selling on the equity to buyers — in order to fund an expanded drilling program. The move, coming at a time of relative drought for such arrangements, raised an eyebrow.

"We wouldn't have done the deal four months ago. We certainly wouldn't have got this price," Mike Rose, Duvernay's chief executive officer, said in an interview. "But our share price had had a nice appreciation from its lows and commodity prices are strong … and we had a fair idea it would be favourably received."

It was. Not only did brokerage Peters & Co. sell the new Duvernay stock almost instantly, but it felt it could have sold three times as much as was on the table.

"Montney is such a hot play right now, there's substantial activity there and the companies are having no problems making money," said David Doig, a Calgary-based analyst at Union Securities Ltd. "It's going to be a very successful play, so people are throwing cash at it."

Among juniors with Canadian oil and gas production, the only bigger financing this year than Duvernay's was one by Birchcliff Energy, which secured $130-million from investors in February. The carrot, again, is Birchcliff's vast exposure to unconventional gas; the company has as much as $1.5-billion worth of drilling opportunities in Alberta, much of it in the Montney play.

"The institutions are very focused on these large resource plays where you can do significant development work, and they'll finance repeatable, sustainable drilling," said Birchcliff chief executive officer Jeffrey Tonken, speaking from Toronto's airport after a hectic three-day tour meeting U.S. and Canadian investors.

According to Mr. Tonken, the company could have sold two or three times as much equity to institutions, but decided to raise only as much as it needed to pay off a bridging loan and finance some drilling.

"We had significant support because of our results and commodity prices, so we went to the market," he said. "Rule number one in this business is take the money when you can get it."

Almost 18 per cent of Birchcliff's stock — worth $230 million — is held by one investor: Seymour Schulich, the billionaire philanthropist with a reputation for investing in only a few companies, but regularly backing the right horse.

Mr. Schulich bought another 1.2 million shares in Birchcliff in the February financing deal; he believes that the stock could climb to $50 a share in the next three years from more than $11 a share today, as long as natural gas prices hold up.

"I really like them, and the play has a lot of potential," he said in an interview. "But the management has had some great success in the past and they run the company as it should be run, which is very attractive. You can't pay too much for good management or too little for bad management." HOW TO BE JUNIOR

While the management teams that run Canada's juniors vary wildly, from slick money makers to cowboy wildcatters, their business plans have never wavered far from a simple template.

They aim to find an asset, prove it has some decent reserves, get production to about 1,000 barrels of oil equivalent a day, and sell out to an energy trust with deep pockets that's aiming to boost its resources. If successful, the company management does the same thing all over again, but with greater backing from investors who now trust that the team knows how to create big returns.

It's a strategy that has served the country well, creating a thriving market for junior oil and gas companies, the likes of which doesn't exist anywhere else in the world. However, the rug was pulled out from the sector's feet in October, 2006, when Finance Minister Jim Flaherty pulled out his Halloween surprise — that income trusts would have to pay tax like normal corporations in the future.

As well as crippling the trusts, the decision effectively removed juniors' planned exit routes in one fell swoop, leaving their business plans in tatters. Several body blows followed; natural gas prices — so strong in 2005 because of hurricanes Katrina and Rita — stagnated, as mild North American summers and winters left demand flat.

Costs of manpower and materials continued to rise because of the oil sands boom, while the knockout punch was delivered last October, when the Alberta government introduced a new royalty structure on gas and oil production. Producers will have to pay the government more when prices are high.

Last winter, matters came to a head; all companies, not just juniors, slashed their drilling plans in Alberta, either turning turtle altogether or redeploying capital to B.C. or Saskatchewan. Drilling in Alberta fell to five-year lows.

Since then, drilling firms have cut prices for rigs, some by as much as 25 per cent from last year.

For Jennifer Stevenson, managing director at Qwest Energy Investment Management Corp., that means busy times. Her equity fund subscribed to all three April bought-deal financings — Crew Energy Inc., Celtic Exploration and Duvernay — and expects to be involved when new offerings take place.

Her rationale for the purchases is that she believes the junior market has bottomed out and is on the way up. Cost structures are much improved, and companies are making money again.

"In the last eighteen months, these companies have largely not been able to access the equity market for hard dollars, but now the positive tone is back," she said. "The strong companies have survived the downturn and now they're beginning to prosper."

For Ms. Stevenson, one big change is in natural gas. Usually, North American prices for the commodity dip in April — the so-called "shoulder season" — as demand for heating gas falls. Equally, summer demand (for electricity generation, to power air conditioners) hasn't yet kicked in.

This April, gas prices are above $10 a million British thermal units — a figure that's historically high by any measure, let alone for the time of year. They're a strong indication that North America has worked through the overhang in inventories seen in 2006 and 2007.

"The markets are starting to appreciate that the price is here to stay," she said. And for Ms. Stevenson, comparing the futures market for gas to the valuations of natural gas juniors, there's only one conclusion: Companies are substantially undervalued. She wants to get hold of as much equity as possible in gas-weighted names, particularly those with exposure to big unconventional plays.

THE NEW HIGH TECH

The shift to unconventional supplies is a direct result of the maturing Western Canada Sedimentary Basin, where much of the easily accessible oil and gas reserves have been used up. That's pushing firms into developing so-called unconventional supplies — natural gas found in tight shale formations or in coal beds. Or, of course, the mix of grit and crude that comprises Alberta's oil sands.

The problem with unconventional resources is that the oil or gas is difficult to get out, so companies have to throw science and money at it.

Even with better cost structures and prices, attacking unconventional resources might still seem a bit of a stretch for junior firms that don't have the capital base — and room to play — as, say, an EnCana Corp., the leader in developing unconventional gas resources.

Quietly, that picture changed last year. People started to notice that Petrobank Oil and Gas Resources Ltd., a junior oil and gas company with a reputation for trying out new technology, was getting remarkable results from the Bakken oil field.

Most firms saw Bakken, where light oil is trapped in very tight formations of shale, as being too tricky and expensive to develop. While there was clearly oil there, it was trapped in non-porous rock formations that kept it from flowing out into wells in any great volume. Essentially, the play was seen as being uneconomic.

Petrobank turned the conventional wisdom on its head by using a system that was developed by Packers Plus Energy Services, a closely held company whose technology had attracted attention for opening up tight gas plays in the United States, but hadn't yet gained traction north of the border.

"We knew we had to do something different to get the oil out of there, and our technical guys basically tore the whole [play] apart trying to work out what the best solution was," said Petrobank vice-president Chris Bloomer. "It turned out the fracturing technology was the key."

The system works by creating a series of explosions along the length of a horizontal well, literally breaking apart the rock formations and opening up fissures in the shale. Vast amounts of sand — as much as 75 tons — are pumped down the well, keeping the cracks open and allowing oil or gas to flow out at volumes far more comparable to a conventional well.

Effectively, multifracturing allows a company to replace as many as 10 vertical wells with one single horizontal well, greatly reducing the costs of developing unconventional plays like Bakken or Montney, while producing five times as much oil or gas. Not bad for a system that Dan Themig, Packers Plus's chief executive, first came up with when doodling on an airline napkin.

After Petrobank reported its Bakken production figures last year, Mr. Themig's phone started ringing "off the hook" as companies called up to use Packers Plus's technology, he said in an interview at the firm's head office in Calgary.

"We couldn't get any momentum until Bakken hit, but then company after company started to call and say that they wanted to use this system," he said. "It was the quickest adaptation of technology I've ever seen."

As a result of its success in the U.S. and now Canada, Packers Plus's rise has been meteoric. Mr. Themig says the firm has doubled in size every year since 2005, and is on course to do again in 2008, while the number of employees has soared from 30 to 240. The company expects to fracture as many as 1,000 wells this year worldwide. OLD FEARS

For Art Korpach, head of global oil and gas at CIBC World Markets, the mood is one of excitement that juniors are once again a viable business in which to invest. But there is also caution, and investors are focusing solely on firms' long-term strategies.

"The primary reason for the renewed interest is that companies have found some exciting things to pursue," he said. "But the market is distinguishing far more today between firms than it did in the past. Interest depends on the company's strategy, how it's going to use its money, and the reputation of its management. For firms trying to get capital for a marginal story, it's more difficult."

As a result, the juniors sector is set to be bifurcated between the haves, who got into resource plays early and are poised to make big profits, and the have-nots. The consequences will be that the strong companies will buy out the weak ones, Mr. Korpach said, leading to a situation where juniors get substantially bigger, effectively becoming intermediate players with a greater ability to more capably take on expensive, yet profitable, plays like Montney and Bakken.

"The junior space will consolidate to create a set of larger entities that have the ability to play in some of these trends," he said. "People are very much focused on getting into a longer-term game."

ProEx's Mr. Johnson has come to a similar conclusion. He expects juniors to attempt to copy the success of firms like his own by chasing unconventional plays elsewhere, in order to achieve success.

"Everyone in this business is smart, and people are going to look at what assets are doing well and say that they should get hold of some of those," he said. "They're going to have to go out and find something that's more appealing to investors or die on the vine."