News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Cassandra

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Dilution always trumps "technicals." DTC-chilled IJJP is and always has been a pump and dump dilution machine to enrich Pope and the multiple notorious toxic financiers with which he does deals.

The current dilution scheme orchestrated by convicted felon Ronald S. Goulding and other flagrant securities law violators using the Section 3(a)(10) exemption from registration is more creative than the former Reg D Rule 504 done with the likes of Big Apple Consulting, Fairhills Capital, Magna Group/Hanover Holdings and Blulife, Inc. is more creative and estoeric than 504 schemes but likely just fraudulent.

I've posted due diligence information about IJJC and Pope for over four years and am extremely familiar with the company's sordid history of pumping widely varying business plans that never achieved anything, toxic dilution, dormant periods a the previous reverse split after diluting the stock into the ground with Big Apple Consulting.

Pope was not deterred when BAC and 4 of its principals were charged by the SEC with multiple counts of fraud and securities law violations. He actually engaged Boost Marketing, a new iteration of BAC run by the same cast of fraudsters, to be the replacement IR firm.

It's unfortunate that the false and misleading press releases about the purchase of rights to a potential income stream in the millions of dollars from two medical marijuana farms that have not yet been built has been taken as some sort of gospel truth.

Even at first glance, the story seems too good to be true. However, if one takes the time to perform actual due diligence review of the Section 3(a)(10) exemption as it is being used in this case, the details of all of the share issuances from IJJP, TWDL, ENTI, GEAR, HALB and CWIR as well as the entire cast of characters, it's easy to see that the farms being built through these deals and generating the kind of potential income projected is extremely unlikely.

IJJP's cannabisheadliners.com website that included some of the documents for the deals was online for less than 72 hours between Jan. 14-16. Some of the document links still work (for now). I downloaded all I could and will upload to a file-sharing site in case they disable the links. I'll also post more screen shots to expose the facts, lies and misinformation and will include links to the source documents so people can review in context.

Yesterday's PR and SCV paid promo audio interview contained blatant falsehoods

SEC enforcement action is a real possibility with the convoluted and wide-reaching pump and dump scheme that attempts to circumvent registration requirements with improper application of the Section 3(a)(10) exemption.

This "consortium" was put together by attorney convicted felon Randall S. Goulding who represents all 6 of the public companies involved despite existing charges by the SEC of fraud and custodial violations through The Nutmeg Group, LLC. an investment advisory firm he owns with his brother David Goulding.

http://www.sec.gov/litigation/litreleases/2009/lr20972.htm

https://www.sec.gov/litigation/complaints/2009/comp20972.pdf

A fairness hearing regarding a stipulated debt settlement by share issuance was held on 11/27/3014 in the matter of a lawsuit Goulding's law firm, Securities Counselors, Inc., filed against TWDL for unpaid legal fees. Goulding used to occasion to tack on share issuances by the 6 public companies in exchange for property interests owned by several parties who are supposedly going to build medical marijuana farms through World of Marihuana (WOM) and Michigan Plant Technologies (MPT) neither of whom currently are currently licensed or sell any product.

The massively misleading WOM website falsely tries to make it look like it currently sells medical marijuana, vaporizers, storage containers, etc., but it doesn't. The website exists to sell free-trading stock issued in the 6 companies: IJJP, TWDL, ENTI, CWIR, GEAR and HALB.

The whole venture is an abuse of the Section 3(a)(10) exemption from registration and likely massive fraud with false and misleading press releases to pump the stock so that the newly-issued free-trading shares can be dumped.

I would not be surprised to see SEC action against multiple parties and companies in this matter. It is not unlike a previous abuse of the same exemption in which the SEC filed injunctive action:

http://www.lawupdates.com/summary/civil_injunctive_action_filed_against_penny_stock_financiers_and_two_public/

From the SCV audio interview with Cliff Pope released this evening, it's clear that using Section 3(a)(10) is the business plan for IJJP, which is extremely risky and foolish.

FWIW, I did warn people about Peter Villiotis, the massive toxic dilution and his numerous false and misleading press releases including multiple bogus offers of a spin-off dividend and a $4 million cash "gift distribution" through convertible Series C preferred shares which I warned would end up worthless.

Former PVEC employees Kerry Thacker and Jason Baker (who now have a $365,000 IR contract to provide services to XNRG through their company CM Research, LLC) were members of the PVEC/VDSC management team who participated in the decision to announce the ridiculous $4 million cash gift and continued to provide credence to the concept that the non-existent money would actually be distributed to holders of Series C certificates until they left.

The stock has had no bid since July 2014 and the ask dropped to $.00001, trades as which don't even register on the chart:

Some of the legal documents submitted to the submitted to the Circuit Court in Waukegan, IL filed by Randall S. Goulding of Securities Counselors, Inc. (SCI) regarding the settlement of his debt claim against TWDL for unpaid legal fees using the Section 3(a)(10) exemption from registration can be found in these links:

https://app.box.com/s/3zjz7smtranwias5lhrlvurhnpf3d6nf

https://app.box.com/s/833u9k6u6n81p8ejzc83t11vcp02kx3x

This bogus Section 3(a)(10) debt settlement action involves 7 PK companies and several individuals and private companies. The companies are IJJP, TWDL, HALB, CWIR, ENTI, HALB and IDGC.

Some of the individuals and private companies who are being issued shares from one or more of these companies can be found in this post:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=110291300

High volume dumping on this illiquid stock. Well, the volume is high given BRNE's trading history.

TWDL CEO Margo Cadena had 50 million shares of TWDL stock issued to her in the SCI TWDL debt settlement action using (abusing) the Section 3(a)(10) exemption to registration so that the shares would be free-trading rather than properly restricted.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=110307113

Issuing shares directly to a control person may be a direct violation of the exemption.

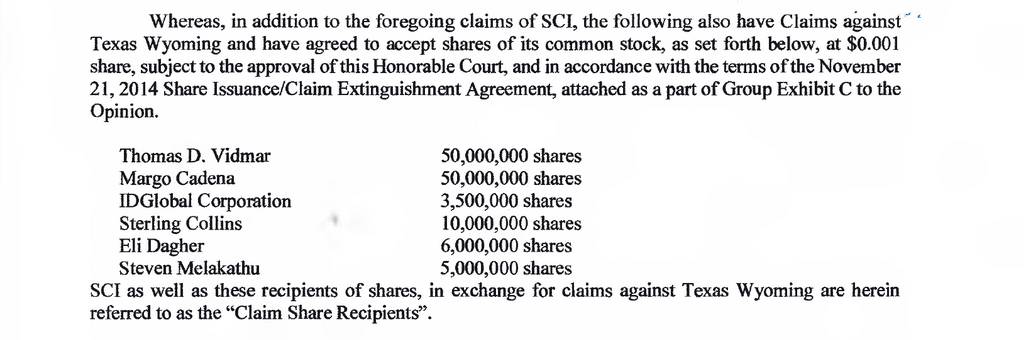

124,500,000 shares of TWDL free-trading stock were issued to the following non-party participants in the SCI TWDL debt settlement:

Thomas D. Vidmar: 50,000,000 shares (tigervidmar@yahoo.com)

Margo Cadena (TWDL CEO): 50,000,000 shares (cadenamargo@yahoo.com)

IDGlobal Corporation (IDGC): 3,500,000 shares (sdufort68@gmail.com)

Sterling Collins: 10,000,000 shares (stervc@gmail.com)

Eli Dagher: 6,000,000 shares (elid58@yahoo.com)

Steven Melakathu: 5,000,000 shares (Steved@countermail.com)

https://app.box.com/files/0/f/2988035313/1/f_25294735307

TWDL chart shows that the paid promotions only worked for one day.

Parties involved in the SCI TWDL debt settlement using (abusing IMO) the Section 3(a)(10) exmption of the Securities Act in order to issue free-trading rather than restricted shares of the 6 issuing companies are listed below:

NOTICE OF MOTION / CERTIFICATE OF SERVICE

to Approve Settlement and for an Agreed Order to Dismiss the Case

to:

Gear lntemational, lnc. ("Gear") at carltonwingett@gmail.com

Tykhe Corporation (formerly, Halberd Corporation ("Tykhe") at john@maddoxcpas.com

Texas Wyoming Drilling, Inc. ("Texas Wyoming") at cadenamargo@yahoo.com

National Properties Trust (formerly, Encounter Technologies lnc., "National Properties") at randolphshudson@gmail.com

IJJ Corporation ("IJJP") at cpope@ijjc.com

Fuzznbuzz Brands, Inc. ("Fuzznbuzz") flnymike@gmail.com

And their attomeys, Laura A. Balson, Golan & Christie LLP at labalson@golanchristie.com

Expanse Enterprises, LLC ("Expanse") at ryan@gouldingcpa.com

Capitol Capital Corporation at Howardsalamon@gmail.com

Corr Brands, lnc. at rjCorr@gmail.com

Richard Goulding M.D., Freelance, LLC at gouldnland@aol.com

Securities Counselors, lnc., and its assignee Robyn Goulding at skiframa@yahoo.com

Pope Enterprises, LLC at cpope@ijjc.com

North Shore Equity Trading lnc. at itrade60@aol.com

Take Flight Equities, Inc. at bwright@cgrowthcapital.com

Nobilis Consulting LLC at NSET60@ymail.com

Belmont Management Services LLC at guyvincil@gmail.com

And their attorneys, Securities Counselors, lnc. (SCI) at RSG@Gou|ding|aw.com

Thomas D. Vidmar at tigervidmar@yahoo.com

Margo Cadena at cadenamargo@yahoo.com

IDGlobal Corporation at sdufort68@gmail.com

Sterling Collins at stervc@gmail.com

Eli Dagher at elid58@yahoo.com

Steven Melakathu at Steved@countermail.com

And their attorneys, Securities Counselors, lnc. (SCI) at RSG@Gouldinglaw.com

Several of the people involved in this bogus SCI TWDL debt settlement deal have had past and/or current actions against them by the SEC. Some of those involved, such as Goulding's SEC-barred law partner in SCI, Carl N. Duncan, are buried in the lawsuit documents. Others that are not specifically mentioned can be found by researching the history of relationships.

This is an extremely convoluted share-selling scheme that I firmly believe violates multiple securities laws and needs to be reported to the SEC. The IJJP press releases have been very misleading.

IJJP CEO and MANAGEMENT are not here for chump change.

Parties involved in the SCI TWDL debt settlement using (abusing IMO) the Section 3(a)(10) exmption of the Securities Act in order to issue free-trading rather than restricted shares of the 6 issuing companies are listed below:

NOTICE OF MOTION / CERTIFICATE OF SERVICE

to Approve Settlement and for an Agreed Order to Dismiss the Case

to:

Gear lntemational, lnc. ("Gear") at carltonwingett@gmail.com

Tykhe Corporation (formerly, Halberd Corporation ("Tykhe") at john@maddoxcpas.com

Texas Wyoming Drilling, Inc. ("Texas Wyoming") at cadenamargo@yahoo.com

National Properties Trust (formerly, Encounter Technologies lnc., "National Properties") at randolphshudson@gmail.com

IJJ Corporation ("IJJP") at cpope@ijjc.com

Fuzznbuzz Brands, Inc. ("Fuzznbuzz") flnymike@gmail.com

And their attomeys, Laura A. Balson, Golan & Christie LLP at labalson@golanchristie.com

Expanse Enterprises, LLC ("Expanse") at ryan@gouldingcpa.com

Capitol Capital Corporation at Howardsalamon@gmail.com

Corr Brands, lnc. at rjCorr@gmail.com

Richard Goulding M.D., Freelance, LLC at gouldnland@aol.com

Securities Counselors, lnc., and its assignee Robyn Goulding at skiframa@yahoo.com

Pope Enterprises, LLC at cpope@ijjc.com

North Shore Equity Trading lnc. at itrade60@aol.com

Take Flight Equities, Inc. at bwright@cgrowthcapital.com

Nobilis Consulting LLC at NSET60@ymail.com

Belmont Management Services LLC at guyvincil@gmail.com

And their attorneys, Securities Counselors, lnc. (SCI) at RSG@Gou|ding|aw.com

Thomas D. Vidmar at tigervidmar@yahoo.com

Margo Cadena at cadenamargo@yahoo.com

IDGlobal Corporation at sdufort68@gmail.com

Sterling Collins at stervc@gmail.com

Eli Dagher at elid58@yahoo.com

Steven Melakathu at Steved@countermail.com

And their attorneys, Securities Counselors, lnc. (SCI) at RSG@Gouldinglaw.com

The first tranche of free-trading shares to be issued to the PIE share recipients by IJJP and the other five companies has already been issued according to a PR issued by IDCG today announcing that it has been retained by Corr Brands, Inc. (CBI), which is one of the 12 PIE share recipients.

As shown in the PR, CBI has received 1/3 of the shares shown to be issued by the 6 companies in legal documents submitted to the court regarding the settlement of TWDL debt to Securities Counselors, Inc. From the IDGC PR:

The 2 billion share issuance is really not going to be 2 billion. It already has been cut in half.

It's there in the filings too. Each tranche will be based on the share price at such time. As of now, the first tranche hasn’t been issued from what I have learned.

The company believes that with the deals they have lined up, the price will be high enough to where it should only actually be a few hundred million shares (if that) and not 2 billion, ...

... but the worst case scenario had to be presented to the court at such time months ago based on where IJJP was trading at back then.

We are beyond the worst case scenario as the price is actually much higher than the original price used to consummate the deal.

Bottom line, what it comes down to is that a few hundred million shares in exchange for $2.1 million in Net Income is a great deal for any stock... especially a penny stock.

WOM Cananda has been operating for five years...

Domain Name: WORLDOFMARIHUANA.COM

Registry Domain ID:

Registrar WHOIS Server: whois.networksolutions.com

Registrar URL: networksolutions.com

Updated Date: 2014-11-06T18:11:07Z

Creation Date: 2013-11-09T05:22:32Z

Registrar Registration Expiration Date: 2016-11-09T05:00:00Z

Registrar: NETWORK SOLUTIONS, LLC.

Registrar IANA ID: 2

Registrar Abuse Contact Email: abuse@web.com

Registrar Abuse Contact Phone: +1.8003337680

Reseller:

Domain Status:

Registry Registrant ID:

Registrant Name: PERFECT PRIVACY, LLC

Registrant Organization:

Registrant Street: 12808 Gran Bay Parkway West

Registrant City: Jacksonville

Registrant State/Province: FL

Registrant Postal Code: 32258

Registrant Country: US

Registrant Phone: +1.5707088780

Registrant Phone Ext:

Registrant Fax:

Registrant Fax Ext:

Registrant Email: e57ry7wf7fs@networksolutionsprivateregistration.com

Registry Admin ID:

Admin Name: PERFECT PRIVACY, LLC

Admin Organization:

Admin Street: 12808 Gran Bay Parkway West

Admin City: Jacksonville

Admin State/Province: FL

Admin Postal Code: 32258

Admin Country: US

Admin Phone: +1.5707088780

Admin Phone Ext:

Admin Fax:

Admin Fax Ext:

Admin Email: e57ry7wf7fs@networksolutionsprivateregistration.com

Registry Tech ID:

Tech Name: PERFECT PRIVACY, LLC

Tech Organization:

Tech Street: 12808 Gran Bay Parkway West

Tech City: Jacksonville

Tech State/Province: FL

Tech Postal Code: 32258

Tech Country: US

Tech Phone: +1.5707088780

Tech Phone Ext:

Tech Fax:

Tech Fax Ext:

Tech Email: e57ry7wf7fs@networksolutionsprivateregistration.com

Name Server: NS1.WIX.COM

Name Server: NS2.WIX.COM

DNSSEC: Unsigned

URL of the ICANN WHOIS Data Problem Reporting System: http://wdprs.internic.net/

>>> Last update of whois database: Mon, 26 Jan 2015 08:28:34 GMT <<<

The SEC has charged PKGM's auditor M&K CPAS PLLC with violating the antifraud provisions of the Securities Act of 1933 and Rule 2-02(b)(1) of Regulation S-X as well as engaging in improper professional conduct under Rule 102(e) of the Commission’s Rules of Practice in microcap scheme involving 20 bogus mining companies: http://www.sec.gov/news/pressrelease/2015-9.html#.VMJ65_54pcR

PKGM's sole officer and director, recidivist microcap dilution scammer David Lovatt, fired original auditor Salberg & Company, which provided the audit for the S-1 registration statement, and engaged M&K CPAS in its place on 9/5/14. This action was taken 10 days before the first 10-Q due following effectiveness of the registration and likely indicates that Salberg & Co. was not supportive of the unaudited financials Lovatt was submitting.

The 8-K announcing the change in auditor was required to be filed by 9/11/14, 4 business days after the change, but Lovatt did not file it until 9/22/14: http://ih.advfn.com/p.php?pid=nmona&article=63765162

On 9/15/14, Lovatt filed a for NT 10-Q indicating that the 10-Q would be late. The 10-Q and was filed on 9/22/14, the same day as the very late 8-K:

http://www.otcmarkets.com/stock/PKGM/filings

http://www.otcmarkets.com/edgar/GetFilingHtml?FilingID=10204455

http://www.otcmarkets.com/edgar/GetFilingHtml?FilingID=10213844

From the SEC announcement:

SEC Announces Charges Against Attorneys and Auditors in Microcap Scheme Involving Purported Mining Companies

Texas-based audit firm M&K CPAS PLLC and partners Matt Manis, Jon Ridenour, and Ben Ortego were similarly engaged by Briner for the purpose of auditing the financial statements of some of the mining companies. The audits they conducted also were allegedly so deficient that they amounted to no audits at all, and they ignored red flags that Briner was engaging in fraud.

“Attorneys and auditors have a serious obligation as gatekeepers to protect the integrity of our markets, and the individuals we’ve charged in this case failed the investing public in their roles,” said Sanjay Wadhwa, Senior Associate Director for Enforcement in the SEC’s New York Regional Office.

The matter will be scheduled for a public hearing before an administrative law judge for proceedings to adjudicate the Enforcement Division’s allegations and determine what, if any, remedial actions are appropriate. The Enforcement Division alleges that Briner, Dalmy, and the auditors violated the antifraud provisions of the Securities Act of 1933 and that the auditors violated Rule 2-02(b)(1) of Regulation S-X and engaged in improper professional conduct under Rule 102(e) of the Commission’s Rules of Practice.

GRBG is long dead and abandoned by the revolving string of fraudsters, notorious toxic financiers and nefarious related attorneys who ran it only as a share-selling pump and dump scam with no actual business ever occurring. The DTC deposit (DWAC) chill placed on 7/21/11 and well-established dilution disaster reputation made it harder to continue the dilution schemes so the rats finally all fled the ship.

The corporate shell is revoked with no officers remaining. No business can legally be conducted. OTC Markets has a Cavaeat Emptor warning and also warns that the company can't be contacted.

The website domain was abandoned well over two years ago and someone else registered it. Although it seems obvious from the content of http://www.greenbridgeindustries.com that there is no relationship to the former public company, you can contact the new registrant to inquire: Christopher P. Gregg, 636-459-5068, news@greenbridgeindustries.com

Domain Name: GREENBRIDGEINDUSTRIES.COM

Registry Domain ID: 1759336364_DOMAIN_COM-VRSN

Registrar WHOIS Server: whois.godaddy.com

Registrar URL: www.godaddy.com

Update Date: 2014-10-24T10:59:43Z

Creation Date: 2012-11-14T17:28:57Z

Registry Registrant ID:

Registrant Name: Christopher P. Gregg

Registrant Organization:

Registrant Street: 4744 Rodney Street O

Registrant City: Fallon

Registrant State/Province: Montana

Registrant Postal Code: 63366

Registrant Country: United States

Registrant Phone: +0.6364595068

Registrant Phone Ext:

Registrant Fax:

Registrant Fax Ext:

Registrant Email: news@greenbridgeindustries.com

Name Server: NS1499.WEBSITEWELCOME.COM

Name Server: NS1500.WEBSITEWELCOME.COM

DNSSEC: unsigned

URL of the ICANN WHOIS Data Problem Reporting System: http://wdprs.internic.net/

Last update of WHOIS database: 2015-01-23T07:00:00Z

For more information on Whois status codes, please visit

https://www.icann.org/resources/pages/epp-status-codes-2014-06-16-en

Unfortunately the SEC often considers "creative accounting" that blatantly violates GAAP to be fraud.

There is no doubt in my mind that accounting fraud has been committed in multiple XNRG quarterly and annual financial reports even though the latter were audited. In fact, basic accrual accounting principles were not followed regarding multiple transactions -- especially in the category of prepaid expenses.

Upon further thought, I realize the "E" wouldn't be added to the XNRG symbol because the stock has already been removed from the OTCQB trading tier and trades via OTC Link (fka Pink Sheets). Other than being downgraded from Current Information status, there is no real penalty for XUN's 10-Q filing delinquency (unless the company remains delinquent for many months and therefore risks revocation of its registration).

There is no legitimate reason that Jerry couldn't and still can't file the 10-Q with its disclosure information and financial statements. It's revealing that he gave no explanation in his comment that was posted here. IMO, he is not filing because of the impropriety of showing extinguishment of the EVCI-purchased debts prior to all of the shares being issued and included in the OS and float. Even though the financials are unaudited, the auditor usually reviews them. The new auditors may be less willing to expose themselves to accounting fraud allegations from the PCAOB and SEC than were Weinberg & Baer.

It's also likely that other disclosures are worse than investors expect and Jerry does not want sentiment to become even worse.

When the company is downgraded from Current Information status at OTC Markets, stock promotion becomes riskier and can result in a Caveat Emptor warning or even an SEC suspension. Although CMR doesn't consider its services to be stock promotion, the SEC or OTC Markets may disagree. The contractual agreement to have subcontractors post repetitively about the stock on social media and other Internet sites likely constitutes promotion.

The Company plans to file its Form 10-Q no later than 30 calendar days following the prescribed due date.

IJJP has a DTC Deposit (DWAC) Chill (is not DTC eligible) due to multiple toxic funders dumping unregistered, non-exempt shares onto the public market.

Given the specific parties involved as well as the previous and current SEC actions against some of them, it's doubtful that the DTC would ever remove the chill which was placed after the SEC filed action against Fairhills Capital for fraudulently dumping unregistered shares of approximately 100 PK companies on the open market.

DTC chill list: http://www.clearstream.com/blob/65974/04319797d7d56c1f27ce928f118ce280/dtcc-deposit-chills-pdf-data.pdf

CEO Clifford Pope has an extensive history of dealing with some of the most notorious toxic diluters and their fraud-enabling attorneys, including the current one, Randall S. Goulding. Goulding is a convicted felon who is currently being sued by the SEC which he was required to disclose in his recent IJJP attorney opinion letter submitted to OTC Markets but did not.

Read the iBoxes of the following forums for DD on some of IJJP's funders who have also been responsible for the destruction of many dozens of formerly popular OTC stocks:

Big Apple Consulting/Boost Marketing

Fairhills Capital/Edward Bronson

Magna Group/Hanover Holdings

Blulife Inc. (Vivian Blumenthal and Joseph M. Blumenthal) is another toxic financier and got caught holding a bag the last time IJJP was diluted into the ground.

BAC, like Fairhills, has been sued by the SEC for fraudulent selling of unregistered, non-exempt stock on the open market as has Joseph Blumenthal of Blulife (which is why he can't list himself as an owner of Blulife).

Dilution will resume as is always the case with Pope and IJJP. In fact, the supposed $2.1 million in future potential net annual income comes at a cost of over 2 billion new shares of IJJP stock to be distributed to various people and entities who put the debt conversion deal together. There is no guarantee that the cannibis farm will ever be built or any revenue will ever be seen.

... we also have 82% of the ss owned by insiders...

IJJP: Dilution of 2 billion plus new shares is required for the MMJ deal as was shown on the canabisheadliners.com website when it was up briefly on Friday:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=110078910

If one really thinks about it, companies don't just get $2.1 MM/year in revenue for nothing. That said, the revenue is projected for an MJ farm that has not been built and likely never will. If something sounds too good to be true, it almost always is.

The goal with all of the stocks involved is for those who put the deal together to pump and dump for personal gain. Some traders will profit from the promo momo while others will be left holding a bag of worthless shares when the momentum dies, the truth comes out or the dilution hits.

SEC action such as a suspension is also a very real possibility given the multiple nefarious characters involved in the deal (some of whom already have current or past action against them) and/or the probable abuse of the Section 3(a)(10) exemption from registration for the new shares to be issued.

IJJP is nothing but a renewed pump and dump scam with temporary momentum due to announcement and promotion of false and misleading information.

IJJP is required to issue over 2 BILLION new shares to get this "projected" (non-existent) income from a Canadian pot farm that has not been built or even financed and likely never will.

The devil is in the details of some of the documents shown on the canabisheadliners.com website that was taken down for maintenance after being active briefly on Friday. The site was taken down to hide the facts of what this deal really is and who is involved.

This is a debt conversion deal using the Section 3(a)(10) exemption from Securities Act registration. It was set up by Randall Goulding and co-conspirators and is very likely a misuse/abuse of the exemption.

http://www.sec.gov/interps/legal/cfslb3r.htm

Traders can profit from the promo momo while it lasts, but IJJP will be revealed again as just a pump and dump scheme.

A continuation of the patent troll business plan of filing frivolous lawsuits against companies that actually make and sell products with the goal of settlements that are far less than nuisance value.

Lawsuit settlements have never provided value to e.Digital's common shareholders, but speculation of them can drive the share price.

COB Allen Cocumelli receives a monthly retainer to manage the outside attorneys who file these lawsuits so why does EDIG need a CEO making over $200K/year in salary and perks? It really makes no sense.

What does Fred Falk actually do? What has he ever really done as CEO?

You can't believe anything TNKE publishes, including its financial statements and press releases.

Tanke is a China-based pump and dump scam that didn't even trade until several months after Evotech Capital SA took majority ownership and spent over $100K promoting the stock through numerous newsletters in late April and early May (see chart at bottom). The number of unrestricted shares increased exponentially just before the promotions and were dumped on the open market.

I suggest doing some due diligence research on Evotech, Basilio Chen, Martin Nielson, Nick Balomenos, Abraham Cinta, etc. as well as their other scam companies and fake acquisition deals with companies with which Evotech was involved. http://www.evotechcapital.com/en/

INSIDERS OWN 82% of it I heard...

IJJP: Cede & Co. and toxic funder Blulife are not "insiders." Insiders do not own 80% of the OS. The only insider is Clifford Pope, who controls IJJC (IJJP) with super-voting preferred shares and reported that he owned 25.5% of the common stock as of the last report (see screen shot below).

Cede & Co. is the nominee name of the DTC, which is the "registered holder" of securities held in street name (broker's name) by the actual beneficial owners. Although Cede $ Co. has custody, it does not own the stock and it is improper to list it as a block owner as did Cliff Pope. The vast majority of retail owners hold their stock in street name under nominee name Cede & Co.

Blulife Inc. is one of the toxic funders Pope has used over the years to enrich himself. Previous ones include notorious diluters Big Apple Consulting (BAC), Fairhills Capital and Magna Group (see links for more DD). BAC and Fairhills have been sued by the SEC for fraudulent selling of unregistered, non-exempt stock on the open market as has Joseph Blumenthal of Blulife (which is why he can't list himself as an owner of Blulife).

Blulife (sometimes misspelled as Bluelife) has also provided toxic funding to TDEY, MPIX and ILIV among others. People involved with Blulife include Vivian Blumenthal and Joseph M. Blumenthal as well as the mysterious Joseph Allen. Joseph Blumenthal has a permanent ban on involvement with penny stocks due to a previous pump and dump scheme.

More DD on Blulife and these individuals.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=108223018

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=108223352

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=108192845

The address for Blulife registered with the FL Dept. of Corporations is 6280 NW 42nd Way, Boca Raton, FL 33496: http://visulate.com/rental/visulate_search.php?CORP_ID=P10000031429

Clifford Pope has always relied upon toxic dilution to provide his income as none of his various business plans over the years has ever generated income. Dilution will certainly return to IJJP.

After the SEC took action against Fairhills Capital (Edward Bronson) for its fraudulent Rule 504 financings, most of the companies involved participating in the scheme received DTC Deposit (DWAC) Chills including IJJP:

DTC Chill List: http://www.clearstream.com/blob/65974/04319797d7d56c1f27ce928f118ce280/dtcc-deposit-chills-pdf-data.pdf

IJJP's current attorney, Randall Goulding, was sentenced to 6 months in prision for fraud in 1994: https://www.courtlistener.com/opinion/672079/united-states-v-randall-s-goulding-and-michael-m-u/

Goulding, his brother David and their Nutmeg Group is currently being sued by the SEC, which Goulding does not disclose in his IJJP attorney letter as required: www.sec.gov/litigation/litreleases/2009/lr20972.htm

Ownership as disclosed by IJJP in the most recent report. Neither Cede & Co. nor Blulife are insiders.

Source: http://www.otcmarkets.com/financialReportViewer?symbol=IJJP&id=127814

Insiders Own 80% of the OS - Wow this is a rocket ship scenario getting ready to launch!

Common shares:

Name of Owners, # of shares % of ownership Corporate st.

Clifford Pope 290,423,370 25.50% CEO President

1325 Cavendish Drive

Silver Spring, MD 20905

Cede & Co (DTCC)

Cede & Co

55 Water St - 3rd Floor 545,805,122 47.92% Non-Corporate Officer, DTCC

shareholder,

Blulife Inc.

Joseph Allen

55 Southeast 2nd Ave, 105,000,000 9.22% Non Corporate

Beach, FL 33444

Total # shares insiders own = 941,228,492

Total # shares OS = 1,166,385.000

941,228,492\1,166,385.000 = .806(100) =80.6 % of total OS is own by insiders...

Preferred shares:

Clifford Pope C 1,000,000 100% CEO President

1325 Cavendish Drive

Silver Spring, MD 20905

The new AERS address is a Davinci Virtual Office which costs $79.00/mo. These virtual offices, much like UPS Store addresses, are a favorite of scam penny stock companies.

90 State Street, Suite 700, Albany, New York 12207:

http://www.davincivirtual.com/loc/us/new-york/albany-virtual-offices/facility-1190

Suite #700 is shown for Davinci's day offices and meeting rooms available for hourly rental:

http://www.davincimeetingrooms.com/new-york/albany-meeting-rooms/day-offices

http://www.davincimeetingrooms.com/new-york/albany-meeting-rooms

The former AERS address of 69 Trinity Place, Albany, NY 12202 is a residential apartment building named The Schuyler Apartments:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=105160145

PVEC does not appear to have a DTC deposit chill although it likely should have one.

Deposit (DWAC) chill list:

http://www.clearstream.com/blob/65974/04319797d7d56c1f27ce928f118ce280/dtcc-deposit-chills-pdf-data.pdf

IJJP had only one trade on 12/17/14. Oddly, it was between the bid and ask:

IJJC (IJJP) is the same "no actual business" scam it's always been under Cliff Pope. I've been warning about the CEO/company/stock for years and haven't been wrong yet. Dilution will always come back into the picture and the proceeds will all be used to pay Pope as has always been the case.

There have been a variety of pretend business plans over the years all supported by the company's website. The goal is always to support dilution. Pope typically lets the company go dormant for an extended time after diluting it into the ground. Look for another reverse split before he reignites the toxic dilution and issues "pump to dump" PRs.

Additionally, medical marijuana has nothing to do with Pope's new pretend business plan which is a membership website to offer services to other companies. The last business plan was to sell disaster preparedness supplies.

The history of the company and the CEO is a red flag that would likely cause many to avoid playing the stock.

Attorney Opinion Letters: The SEC needs to charge more of the attorneys who facilitate the numerous fraudulent schemes by providing bogus opinion letters to transfer agents that result in the issuance of unregistered, non-exempt stock to the public as done with TECO.

The penalties need to harsher as well. Without the bogus opinion letters, this particular kind of fraud would largely be prevented.

IMO, TAs need to be more vigilant as well and should not look away when its obvious that no exemption from registration actually exists despite getting a letter from a shady attorney. TAs should provide an additional level of gatekeeping and should not allow themselves to be gagged to hide actual share structures.

Samuel E. Whitley's Whitley & Associates has other clients that have run into trouble. Known OTC client list:

http://www.otcmarkets.com/research/service-provider/Whitley-&-Associates-LLP?id=1633&b=n&filterOn=3

Firm website: http://www.whitleylawgroup.com/Attorneys/Samuel-E-Whitley.shtml

It depends on the loan agreement or the conversion agreement if the debt is sold to an entity other than the lender. In some cases the lender or the buyer of the debt will accept a certain number of shares in exchange for the entire debt all at once, usually priced at about 50% of the market price.

In other cases a debt is sold in tranches, allowing the entity receiving conversion shares shares to sell the first tranche before accepting or pricing the next and so on until the debt is paid. Again, conversion shares are usually issued at about 50% of market.

Both methods are toxic, but the second method is a spiraling toxic conversion as the sale of a tranche often depresses the market price so each subsequent tranche is priced even lower than the former.

Clarification ... Although FINRA shows "penny for the lot" transactions as occurring at $.0001/share for trading records, the broker reports only the $.01 for the lot as sale proceeds to the client and the IRS.

Caution! Obtain tax advice only from an accountant or an attorney.

One's "intent" regarding a stock has no bearing in the IRS rules. Although one may be able to file returns writing off any number of things that don't actually qualify and not get caught, if one is audited there could be serious consequences.

The only safe way to claim a loss on a worthless penny stock that is to have it removed from your portfolio. This can be done in a worthless securities transaction in which the broker buys all your shares for $.01 (aka "penny for the lot" transaction). Brokers have different requirements for doing this but after 2008, it became easier through "abandonment" of the stock.

If you have offered your stock for sale at market for several weeks or months and haven't been able to sell, you may want to ask your broker to do this kind of transaction for you. In this case, it is documented as a sale and reported to the IRS.

These transactions are required to be reported to FINRA and show as occurring at the lowest price of $.0001/share. With many completely dead stocks, most or all of the volume shown is actually such trades.

PVEC still trades and, through accounting fraud, shows positive net worth (shareholder equity). Trying to do a write-off without ridding one's portfolio of the stock is very risky. It's doubtful that one could provide the required documentation to prove it being worthless if it is still held.

Also, most OTC penny stocks including PVEC don't have registered stock so there is no registration for the SEC to revoke (which would eliminate the ticker). Their tickers can remain in your portfolio in perpetuity -- long after all evidence of life is gone.

When they (your broker) gets them off the books...their own matter not yours.

The stock went right back to $.0001 today on a trade of 50,000 shares ($5).

It seems that Ken Ash may be privately trying to stimulate buying of the stock of this dead shell with promises of news. People need to remember that PIPI is a grey market, caveat emptor stock with a DTC Deposit Chill. Ash is/was also not an officer of PIPI.

The former website had stated that his nephew Georgos Androutsopolous resigned as CEO and the sole officer although his name was never withdrawn from the NV SOS filing. The corporation is revoked by the NV SOS.

What is Ash doing for IDCN for which he is the court-appointed custodian and made himself CEO after changing the name to Sidewinder Resources?

It's hard to believe that anyone would still follow Ken Ash after two stocks in which he was heavily involved and touted ended up suspended by the SEC. Those he refers to as members of his "Stock Charter Group" likely ended up with the biggest losses.

Why does CMR "need" upfront payment of the entire $365,000 contract fee before beginning its 13 months of consulting/IR/stock promotion services?

This is extremely unusual in any business. Why would Jerry agree to this when the company is so deeply in debt and can't pay any of its bills let alone engage in operations?

What do Kerry Thacker and Jason Baker, the owners of CMR, bring to the table that is worth over $400K when the 10% EVCI fee is added? Their fee equates to over 4 billion shares that need to be sold to pay for them to engage "subcontractors" tout XNRG stock on message boards and social media. That kind of massive dilution certainly counteracts any kind of buying demand they can drum up by touting.

Prior to being individually hired by Peter Villiotis to tout PVEC (fka VDSC) in October and November 2013, they were rather new to penny stock trading. Both were given executive titles and official officer positions yet during their tenure PVEC massively diluted and has been at no-bid for the last 5.5 months. When working for PVEC they revealed their iHub IDs:

Kerry: http://investorshub.advfn.com/boards/profilea.aspx?user=391255

Jason: http://investorshub.advfn.com/boards/profilea.aspx?user=386974

CMR's contract with XUN calls for Kerry and Jason to utilize subcontractors to do all of the work. Other than the specified posting on social media and stock message boards, why does CMR need subcontractors? CMR and its subcontractors who tout the stock are almost certainly subject to disclosure under Section 17(b) of the Securities Act.

Can anyone explain why a newly-created company like CMR with two principals whose only prior experience in IR for a penny stock was with PVEC which ended up at no-bid, would be worth paying $356,000 at all let alone to pay the entire 13-month sum up-front?

As recent public filings indicate (and as has already been made public by me), CM Research (also known as CMR) has been contracted by Xun to provide consulting services, covering a myriad of tasks. However, these services are yet to be provided and will commence at a future date. The extent of these services is as listed below. It is anticipated that these services will begin in the forthcoming weeks. Anything stated to the contrary is misinformation.

Client herewith engages Consultant and Consultant agree to render to Client: public relations, communications, advisory and consulting services as follows:

A The consulting services to be provided by Consultant shall include, but are not limited to, the development , implementation and maintenance of an ongoing program to increase the investment community's awareness of Clients activities and to stimulate the investment community's interest in Client . Client acknowledges that Consultant's ability to relate information regarding Clients activities is directly related to the information provided by the Client to the Consultant.

B. Client acknowledges that Consultant will devote such time as is reasonably necessary to perform the services for Client, having due regard for Consultant's commitments and obligations to other business for which it performs consulting services.

C. Consultant will utilize its subcontractors to provide the following:

• Re-face investor page of site and manage information data on site for investors if it needs to be changed;

• Advise on the positioning of press releases prior to distribution;

• Manage Public/Media Relations to the general market place with a look to create conversations between investors;

• All marketing and public relations as defined by the Client or the Consultant ;

• Social Media Matrix (SMM) program - Designed to bring awareness to company name, ticker and product throughout the social media. Consultant will utilize Linkedln, Digg, Stumble, Face Book, Twitter, Penny stock tweets, various boards and blogs to bring the Client's profile and/or news in front of traders daily. The subcontractors will message in an effort to be repetitive and subliminal. Strongest rewards are appreciated in four to six weeks;

• Search Engine Optimization (SEO) program - Objective drive potential investors directly to Client's website based on key phrase "Energy, Oil, Oil and Gas, and Alternative Fuels";

• Temporary website construction including subsidiary websites construction;

• Permanent website construction including subsidiary websites construction;

• Create and distribute radio interviews;

• Create and distribute video clips;

• Create and manage corporate blog; and

• Other as directed or requested by the Client.

Thank you,

Kerry

Founder & Managing Member, CM Research, LLC.

The share price has shown as $.004 since 11/26/14 when someone bought 250,000 shares at that price giving PIPI a market cap of $1.1 million. Ken Ash or someone else may be trying to make it look like the stock/shell is not dead.

Historical trades: http://ih.advfn.com/exchanges/USOTC/PIPI/historical

I place the blame solely on former CFO, for no bid ...

TNKE trading at all-time low of $.0012 with little volume. The chart tells the tale of a pump and dump scam to enrich Evotech.