News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

TMLonggun

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Yes, and I didn't like it but I don't assign an absolutest evil intent to every event. The world isn't this black and white.

It was either deliberately fraudulent or enormously irresponsible to do what they did.

Say there are five or six relevant points to a discussion. A fair presentation would be to touch on all of them. On this board there are two polarized sides that ignore important evidence. They just pick the elements that support their position and ignore the rest.

Despite criticizing longs for having x-ray vision, we have several self proclaimed mind readers with "genuine" psychic powers. They have this power because they can tell us the "truth" vs the actual comments and quotes on record.

Q: Did AR leave because of Mexus or other internal/market reasons? (beat to death topic x 1000 returns for extra controversy!)

A. While the drill results hardly helped, the prevailing evidence gives me the firm conclusion they left primarily for market and internal reasons.

1. The initial drill results were objectively poor. This is a legit reason to pull out eventually but not during phase 1 drilling. Only 1 in 10,000 geological anomalies becomes an operating mine so professional companies like AR don't just go "we drilled .2% of our targets so we declare this property uneconomic and we are leaving." That is not how exploration works in this industry. On my own claims it has taken multiple rounds of exploration to find economic gold. The AR drill results weren't good but they are far from a complete condemnation of the property as presented by other posters.

2. AR self proclaims a cost cutting and tightening period, based on need for capital and fear of a protracted period of low gold prices. (Ample direct quotes from numerous executives in the filings and the AR PRs around this period demonstrate this conclusively. Many are included in my previous posts.) Only on this board could someone post "I love strawberries" and the response would be "PROOF this poster HATES strawberries. QED" - It is literally the exact opposite of what is said. Personally I take the words of these well known executives at face value... but I am admittedly not psychic.

3. AR sells the ultra high grade La Fortuna project within a couple months of terminating the Mexus JV. So they got rid of Mexus because they have no potential but then their next act is to knee jerk sell of one of their best properties with lots of drilling and outlined HG resources because... I guess all that great gold they discovered has no potential too. It needs to be sold at pennies on the dollar ASAP because it is just too similar to Mexus. The true reasoning clearly can't have anything to do with what the management is saying: they are trying to cut costs and raise cash for a potential lean period and to fund Magino.

4. Gold sentiment craters during this period. Mid and large tier miners naturally cut expenses and lower costs. First up the chopping block is expendable JVs and exploration - this is an industry/company decision and has nothing to do with the quality of the areas getting axed. If Mexus gets the JV cancelled it is apparently because they are awful but if dozens of other juniors get a similar outcome for their agreements during the same market period this would be evidence away from the "awful, no potential" thesis. This is rational market activity (at least from a self preservation POV) and not a sinister indictment of any of the properties involved.

5. AR had a desperate need to raise ~200 M for their new mine while financing for these types of ventures is drying up (well documented by other analysts during this period).

6. AR undergoes a major management restructuring, publicly changing the focus from growth to capital conservation. This changes the direction of the company and the types of short term actions they take. This happens nearly every time in the cyclical mining industry (bull, bear action). In prevailing periods of high prices they produce at all cost and then during leaner periods they cut and optimize, cutting exploration and development in a penny wise- pound foolish (myopic) manner, which creates a future shortage of metals due to the huge development lead times. This act is what creates the cyclicality of the mining industry and future bull and bear markets.

So what is more likely to be true: AR used a small portion of their phase one drilling to fully evaluate Mexus' huge property and then left because they saw no potential or... all the other evidence is considered and they left merely to do what they thought was best for their company at the time?

Longs have x-ray goggles that can see to the center of the Earth while the other guys are actually psychic, capable of reading the minds of management and getting the really real truth--despite ample evidence to the contrary.

Argonaut management and now PT too?

Quick, do me next. What do I want to have for breakfast?

I am pretty sure there are several million dollar prizes available for anyone that can "prove" their gift, go claim it and then come back and buy a few shares.

Painting everything as a wonderful investment opportunity...there is no mention of the other red flags here

No, but I assume we will be credited/compensated.

Do you mean shareholders? How would that even work? The money is gone/spent.

Maybe more stuff about climbing up into a valley and seeing that every boulder sparkles and is made of gold or somesuch....story time is fun.

No, but I assume we will be credited/compensated.

We have been told there are about 4000 oz contained on the pad and in a year of stop-start leaching (but still most of a year under solution) they recovered 8 oz (.2% of contained metalics). That is just bad and I don't have a logical chemistry explanation for why this final stage of recovery is so elusive, although there probably is one. Salt or no salt it should be higher than that especially since this is with enriched grades, ie the solution they are recovering should be the richest at the front end of the cycle. Obviously if they leach for a year and then recover after I don't expect them to run a year's worth of solution through their plant in a day but that initial production should be way beyond 8 with these grades - it should be banging out at capacity cleanups. If the plant was at or near capacity I would be confident they could recover ~70%, the issues are mostly solved, and that we'd be golden. Yet it is far from it and this has me concerned that they are not recovering much of anything. Clearly the ore is leaching into solution, but why can the filters not recover it? Usually what I see happen is a mine would stack ~4000 oz, expect 75% and then get 40-60% recovered or 1600-2400 oz - enough that they produce a pretty decent amount but not enough to make a profit without making potential tweaks like smaller crush size. Announcing 8 oz after all the overly optimistic company predictions produced the exact market reaction it deserved. It would have been better to just call it "a small amount of dore" or something. What I would have preferred would have been an upfront announcement whenever the contamination occurred, explaining what happened and that all recovery had for practical purposes ceased because of the issue along with an explanation of how they are going to rectify it and improve things in the future.

I just give my honest opinion while trying to be as objective as I can. I try and be realistic but I lean towards optimism, otherwise I think life would be pretty gloomy in general. Getting to the truth is important to me though, so I kind of find the blind pessimist/optimists to be a tad silly because they will both invariably miss the mark. I like to be the contrarian and bet against the group as a whole. I am inclined to take an extra bullish slant at the moment because current sentiment is very negative and I feel that we have enough skeptics that anything negative will probably be discussed in an obsessive level of depth, so I'll focus more on the other side but I still acknowledge the other side exists.

Mexus is a really interesting company. That's why we are all here. Hundreds of juniors barely get a message a month, yet look at the hours people have expended reading this board. Mexus has obvious potential and obvious flaws that are visible to laymen, along with the whole gambit of junior mining risks. Focusing on just positives or negatives or locking your opinion in stone is not conducive to making rational decisions in the moment. What matters is the balance, the mental arithmetic. Making money in this sector requires an actor to be flexible and pragmatic - no one wants to ride a failing junior to zero and no one wants to sell precisely at the moment they should add to their positions or hold. As it is often said in this sector, the best time to buy is usually when you feel terrible doing it. I like the idea of using my own and other people's emotions as a barometer, it is actually very useful. These are the classic market emotions of fear and greed and they drive people in ways that generally make them lose money. As much as it pains me to say, even if the mine is successful there will still be lots of upset people that somehow lose money despite multiple opportunities to make out like a bandito.

Take the hypothetical purchase of $5,000 of stock at .24. Dollar cost averaging is almost always more effective than letting your emotions get ahead of you and buying a big lump sum and chasing a stock to a high point. Consider how much better shape the purchaser would be in if they DCA $500/month every other month for 20 months. This also demonstrates the importance of timing and the psychological impact of recent events. Message boards are haunted by these "I only bought once at the all time high and am here to complain," style posts. They are bears for life. Yet if that hypothetical person would have bought 9 months earlier their $5,000 would be worth over $1,000,000 at the same point. Anyone that makes a million in less than a year will be a diehard long and will probably be unshakable in their convictions. This is why most of us are here- those sorts of returns are nearly unheard of even in many risky sectors. That legendary gain involved not an ounce of gold, only rational appraisal. People seem to tell only one half of the story and I don't think that is a fair way to represent things, the omissions are glaring. I am amazed people can complain about terrible performance on a stock while ignoring the fact that this particular one has had several multi-thousand percent moves, and many multi-hundred percent short term waves to trade or sell. This includes some of the highest gains over the shortest periods in junior mining history. The truth is, if you are nimble and use your brain instead of your emotions there are obvious times to buy and sell portions of your positions while holding a core for the (hopefully) big win at the end.

I probably haven't mentioned this before because it isn't my style but maybe the illustration will beneficial. I bought Mexus below .01 and I sold above .21, one of the only sales I have made in this stock. Was that pure luck? Not at all. I have repeated similar scenarios too many times for it to be chance. A 600k market cap for Mexus was absurdly low and undervalued, worth a buy, and 200 million with no production was overvalued compared to its peers and worth a sell. I wait for the moves because I am very patient and I don't generally let my emotions rule my behaviour. All luck, people could say...except I keep doing it consistently over the years, on multiple occasions and stocks. This is the same sort of mindset that is important in mining. You have to consistently move ahead knowing there will be ample impediments, grind out all the tedious requirements that mines need, and then move ahead with a degree of perspective while being mindful of the pitfalls along the way. Since mining is so cyclical, I believe that mines should aggressively expand in bear markets and sell during bulls. What this can often mean in practical terms is that mines and juniors can often price stagnate for years through no direct fault of their own... and still end up being an absurd bargain despite or perhaps because of the prevailing sentiment. These stagnation/erosion trends allow a rational investor to buy quality assets at bear market values. Why do great stocks sometimes remain cheap for years, especially in the mining industry? I think this is relevant because the charts will often look like MXSG's and then when a new bull market inevitably arises, like the dawn inexorably breaking from the night, a rising tide will lift all boats regardless of quality (having less holes is preferable). Many will make fortunes off crappy stocks that will never mine an ounce. Being invested in already profitable miners is the layup, low risk, quite high reward strategy, while trying to narrow down high risk, high reward juniors with high exploration and near term production potential for your speculative slots/lottery ticket.

I think shareholder reactions to the latest PR, while emotional and angry, were mostly justified. Mexus has always been weak in this regard. There was nothing in PRs lately to signal or give us a heads up for the disappointing numbers announced. I don't care about 8oz of gold, I do care about if they can increase and improve on it. Keep doubling it and people will see progress and the trickle can easily become a flood.

An example that may help people here might be the Seabee turnaround story, about a famous mine in Saskatchewan. The mine has had many good times and bad, usually coinciding with a bull and bear market along with some company specifics. What is important is that when I looked at them the second time I found they were then losing money. They had some management and direction changes and gradually this going concern shifted - following a clearly observable path of improvement. First they lost a lot, then less money per oz, and then they quickly shifted to earning a small profit. Then each quarter improved upon the last, inspiring ever higher valuations. It was clear their strategy was working, so they kept going, choosing to mine only higher grades instead of stuff they would lose money on (what a strategy!). Their profits kept increasing and this was the perfect time to gradually accumulate a large position and hold until their profits expanded to a level that made them highly undervalued from the perspective of a value investor. Huge gains, lovely buy-out, low risk, high reward. There were those who said Seabee could never be turned around at the prevailing gold prices or that "high grading" their mine would lead to sterilization of reserves and rapid depletion. Failure begets failure, no one learns anything, new management can't fix the mistakes of the past or change the economics of the deposit in the ground etc. They were resoundingly wrong and eventually the profits grew so large that there was not a single critic or bearish analyst remaining by the time they were acquired for a hefty premium after a blistering rally. Mexus can follow the same route.

The only thing about that last Mexus PR that disturbed me was implied 0.2% recovery rate. That is basically zero. I never would have considered 0.2%, that's the lowest I have ever heard of in this style of operation under any conditions. Their own previous tests were 76% and that is inline with all the neighbours. They need to do whatever is necessary to get themselves in shape as a normal heap leap operation. There is nothing preventing them from improving and learning from their mistakes. Even poor results have a small bright side. For like the great investor Klarman points out in Margin of Safety, a stock becomes MORE attractive, not less, as its price declines (as long as its intrinsic value is stable or increasing). That is somewhat subjective, so make up your own minds. It is also easy to improve on such a low number and rebuild confidence going forward like Seabee did.

Losing some money on a high risk - high reward stock sucks but it certainly doesn't mean that those types of risks are not worth taking if it meets your circumstances. No one wants to lose their principle but I would venture the same people would also feel cheated if they gave in to their emotions and talked themselves out of a good bet to turn the price of a modest used vehicle into a fortune that could change their life forever.

For over a decade I have been working on a very large writing project. I could have done something simple and easy but chose to instead to pursue something most would consider impossible or absurdly difficult because I believe that the long term payoff in terms of the narrative and monetary value will be immense. I will merely say this: ambitious, worthwhile projects take time and effort. It requires reworking things and having your mistakes challenged, rectified and then polished. Ambitious projects are the most satisfying and rewarding activities in the world because, even though in truth most such ideas perish, those that succeed literally change the world, and nearly always for the better. I try not to occupy my time or money with anything less meaningful. Mining is synonymous with risk and wealth creation. A bonanza can form an industrial dynasty, its wealth rippling through time and across huge areas.

It all comes down to common sense. If another year goes by and they still are floundering and at billions of shares outstanding then that isn't going to work out well. Yet they have good grades at the surface and logistical advantages compared to other nearby mines. If they can figure out how to leach, Mexus can too. The 8bros vat leach has some advantages too, mainly in how easy it should be for them to test and improve recoveries while maintaining stricter controls. Quicker cycle time also means more batches to test and refine. The high grades imply low initial costs per oz. I don't know if this will work out smoothly from the get-go (probably not) but it is the kind of thing I like about Mexus and would speculate on. Low cost of vats and initial startup equipment with potentially quick production and high margins. Even at a 50-50 chance that is still a compelling risk and reward, something that could generate millions for thousands. Great, if it works. If not, bad. I think odds are it will work out and that it should be easier to recover from the vat than whatever salty business is now going on at Elena.

I am still confident Mexus will crack their metallurgy and the trickle will one day become a steady flow, they just have to do it in a timely manner or the profit potential of current holders will diminish.

I hope everyone has a great day. Stocks go up and down, but you don't have to let them drag your mood along too.

Git,

You can't have it both ways. You argue we need detailed test and feasibility work to make a project run properly yet object when we spent a year testing and proving it up with actual test production, ie doing exactly what you wanted. The glass isn't half full. This is a 10 year mining project that seems like it will be completed in less than 10 years. If a 10 year project gets completed in 8, that is good and ahead of schedule even with a year of "ineptitude." If we flip the scenario, and imagine a typical junior say 5 years into its dev cycle and they spend a couple years working out metallurgical kinks and doing lots of bulk samples, column and roll tests etc - I almost can guarantee you would describe that as "typical" vs "ineptitude." The work/time/money etc seems to get spent no matter who is in control or what route they take. Yet Mexus' shoestring approach is still doing this for much less time and money than a typical open pit heap leach mine.

The previous discussion was in regards to how long it takes to leach gold with cyanide under typical conditions - anywhere from a few weeks to a month or two for decent recovery, then residual recovery for several years. That is accurate. What we did not discuss was how long it would take to iron out any metallurgical issues. Gold grades rose during leaching but so too did contaminants like clay and lead along with other factors that changed the PH balance and made recovery difficult, even if the grades were initially rising as intended.

I can't reply to pm so I will respond here.

In regards to waiting for news on a specific date in the next week: I don't believe this is an all or nothing scenario and our valuation is definitely not based on some arbitrary timetable like, "if there is no good news by Feb 6th the stock will be doomed forever." It doesn't work like that - it is a range. It is not good to go back and look at PRs of "imminent" gold production last summer, that's not great for confidence and I wish it were otherwise - but one thing still is: they never stop trying and the problems they face are far from insurmountable. They can't magically make higher grades, but they can solve metallurgical issues. They will be able to crack it with enough time and money, even if issues are not completely solved at the moment. I am eagerly waiting for the next status update as well. It is a simple matter of sooner is better and then, at some point, the stock may shift from attractive to unattractive or vice versa.

On more mining properties: I would also agree that the way their focus seems to have shifted seems a bit unusual on the surface. But this makes more sense when you consider that MarMar is now in complete control at Elena (Lemas observing) and Mexus doesn't really have much, if anything left to do on the project directly until there is money, freeing manpower to focus and work on other prospects. Mexus has a number of attractive exploration targets and potentially near term production sources. If they ever get some decent income, I think they can push these other projects ahead rapidly and with minimal cost (with the same caveats of current operations). In the end, having five high grade prospects is better than having less, even if some of the projects have dubious value until more exploration and development work is done. To be honest, I think people would complain either way, regardless of whether Mexus pushes ahead or turtles in to conserve its strength until Elena produces. They should be focused on generating shareholder value, which I think they are doing, even if it isn't a direct/immediate correlation with the stock price. We should get some information on which way this is trending shortly.

As for timetables, I will reiterate what I said previously. I expect an update in the first part of this month and at least a trickle of production from Elena in the next two months. At that point either it will increase and recoveries will improve and they press ahead on the right track or they need to get some additional expertise or improvements. Now it is mining so maybe this ends up taking another year - not expected or ideal but totally within the realm of possibility. If it does take a significant amount of time (say more than 6-12 months) shareholders can probably still make money, but maybe they are looking at a double or triple instead of a 10bagger+ if successful and taking an elevated amount of risk. A junior's risk/reward changes a lot throughout its life-cycle and shareprice movements. If I think a stock is attractive I will buy or hold, if not I will sell. I think an entry is quite appealing right now - and that will change as results warrant (pos or neg). Mexus could be a sell in 3 months and a strong buy in 6, we have no way of knowing until we get closer to those moments and can draw more accurate conclusions and update our perceptions to reflect the facts of the moment.

I am quite bullish right now because I see incremental progress accumulating into success combined at a time when shareholder morale is very low - this is the perfect environment to release good numbers and get a disproportionate impact as bears become bulls and reevaluate their position and fight against their emotions of fear and greed. Now is this going to happen? I think so but we will just have to wait and see.

All in my opinion of course.

-TML

It is just an opinion based on what I consider ample evidence and a little common sense regarding the general scale of the project. There have been 1000s of grab samples, RC drilling and limited core drilling done. There is a large section of the area I consider obviously economic and interesting even without a DFS and many places that I think even a really pessimistic geologist would be excited about drilling and exploring further.

The Elena deposit:

1. Is near surface.

2. Is high grade, 1st quartile for the area.

3. Is in a low cost district.

4. Is in an area with historical records showing bonanza grades and known for its large gold nugget finds and numerous gold rush workings and discoveries.

5. Is next to nearby deposits with much lower grades that are earning ample profits for neighbours.

6. Has absurdly long strike length for vein material (800M). It obviously extends for at least 100M (based on samples and work in the UG). These types of major vein structures can easily extend to the 500M level. This is frankly enormous from a tonnage standpoint even without considering the high grade halo surrounding the veins themselves.

7. Is next to an area of significant placer production.

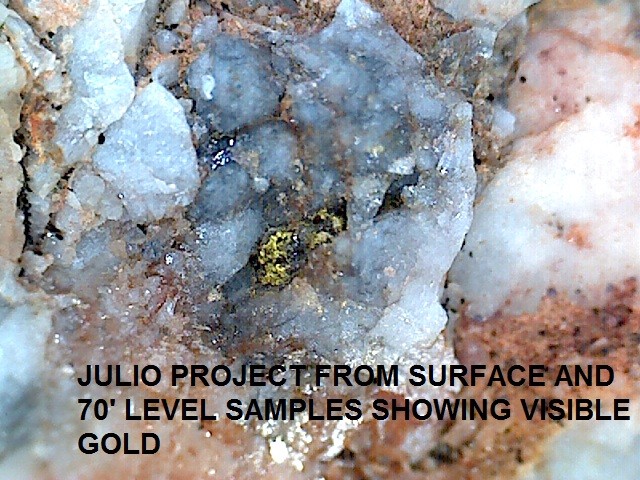

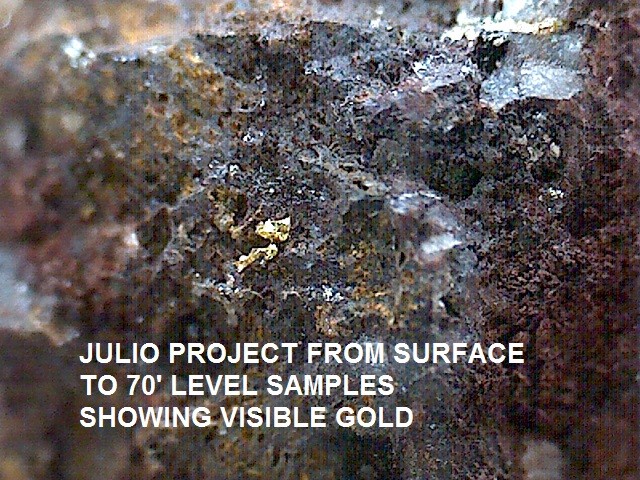

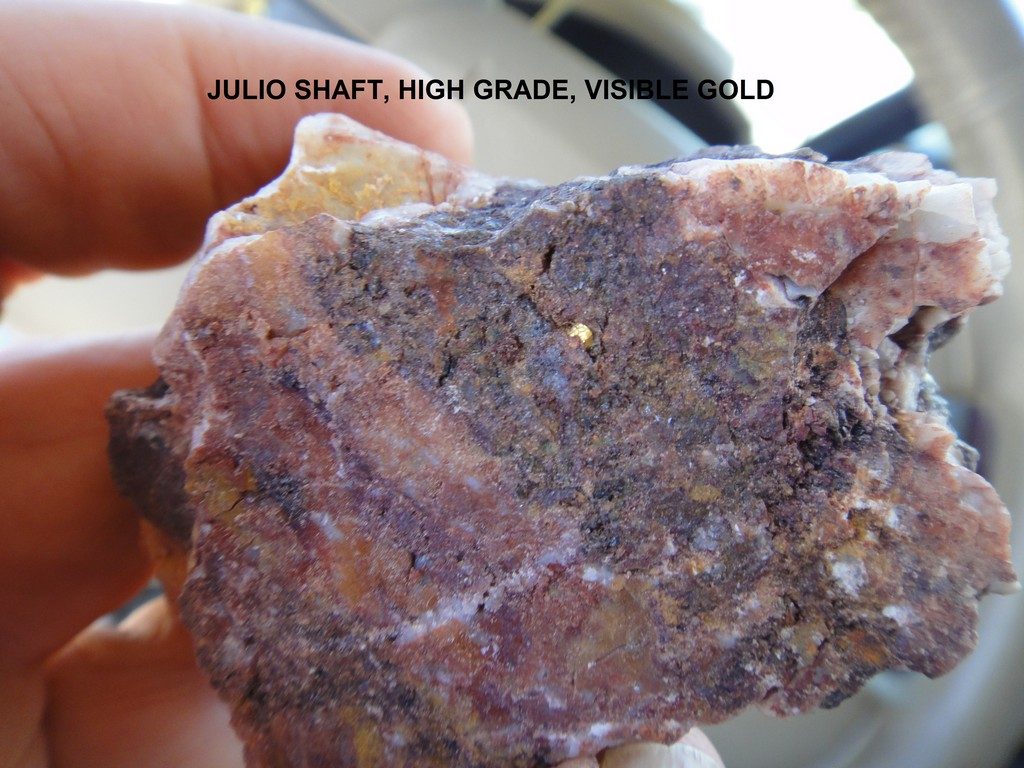

8. Is full of rare visible gold found in drill core and numerous samples from UG levels, hanging wall and face.

9. Connected to significant recent multi-million dollar UG production.

10. The project is fully permitted and has full social license to operate and expand.

11. The project is in an area of low environmental impact and low population density, an area highly desirable for mining development.

12. Possesses a lot of near surface oxidized material that is usually inexpensive to process.

13. Is next to a quality highway, great mining infrastructure, power, and mining labour and supplies in Hermosillo. Shoestring Miner PT and Walnut Grove is just a bonus.

14. Is within the Sonora-Mojave Mega-shear formation, an immense scale mining trend that generates and focuses interest, just like other districts including the Carlin Trend.

15. Has about 500k tonnes of production estimated in what would probably be considered around the inferred resources level- not enough to bet my life on it but enough to demonstrate there is definitely something there, enough to theoretically generate cash-flow and bootstrap the development of the rest. I believe these ounces exist in the ground regardless of whether Mexus can file a piece of paper that proves them as SEC compliant reserves. Let's see what they actually produce. I will bet they will be in the ballpark of the estimates.

This was just off the top of my head. Surely a somewhat reasonable person would admit Mexus, at the very least, has a compelling exploration project even if they are not sold on its economic viability -- which might be proven here shortly. I think the project has a lot of advantages which is why I was always so confident they would be able to get some kind of JV deal and put the property into production and, once in production, eventually earn some profits.

Goldbugy,

I can only speak for myself and offer a few thoughts. I try not to do short term predictions because they are very hard to make. The Elena project is now completely under MarMar's control and I am taking that as a positive that implies that all the bugs in the plant are (mostly) worked out and that production is finally ready to move ahead in earnest. Once the metallurgical issues are resolved, MarMar can put their core competences to use and things will move ahead quickly. I believe they are at or very near this point and will post some results within the next couple months.

As for a timetable, shareholders are right to be concerned with delays. In a company like Mexus dilution is the #1 risk factor - and it is a long list in this industry. Every delay and error decreases the profit potential of long term shareholders as the OS rises. I pointed this out last year, that Mexus at 200M shares outstanding is a very different beast from one with 1 billion shares, even if the shares are tightly held. Market cap is king.

A better question I think is, "How much time is reasonable to give Mexus to produce a profit?"

Many of the readers of this board are familiar with a certain miner in Nevada that has world famous gold and silver claims. This miner explored, raised capital, did a bunch of tests and studies, raised more money, consolidated the district, drilled out a huge deposit, got permits and then built out a very nice little mining operation. This took many years and over $100 million dollars. Only problem was they lost money on every ounce produced and cratered the entire value of their company via dilution and their failure to execute. They had a plan to increase production and they did after raising more money to cover their loses. The result was more ounces produced at a loss. Even though they were on paper successful (permits, good geological reports, discovery and construction complete) and market cap had risen significantly, many long shareholders still lost money even as the company became more valuable. The discussions are kind of interesting and still going on today as far as I know. As a shareholder it is obvious - what is the value of 3 million ounces of gold that are produced at a loss? Zero- even though they spent millions to outline them. It might have a huge value at higher gold prices, but none as is. I gave this company ample time to correct, to mine higher grade sections and optimize their process. The longer this process took (beyond a reasonable tune up period), the more stock I gradually sold as the risk reward equation shifted and the likelihood of them being able to earn a single dollar disappeared. Soon they had diluted my original investment by about 20x, essentially stealing all hope of a profit. After bungling for 1-2-3 years (and this after doing all the expensive stuff necessary to ensure they operate at a profit from the get go) I was long gone and the stock had begun its inexorable decline. It is also interesting because that stock had a very similar "die hard" shareholder group that would ride it to zero, believing riches were coming the next day. Yet profits still matter. A lot.

So let's not do that with Mexus. Mexus has a superior deposit with relative efficiencies and is also different in the respect that because they didn't spend $200m on studies and tailor made equipment in advance and I am naturally giving them more time to optimize than I would otherwise. I am going to give them about 12-18 months more before I would consider exiting. I doubt I will have to wait that long though. I think two months is reasonable for them to show us something worthwhile. If we are still asking "How much longer for an Elena gold pour?" in 6 months then the stock will begin to decline and dilution rates will gradually increase. Either they will sort things out and turn a profit, or a downtrend will develop and continue. Once profits are achieved, the stock will probably rally in a very volatile, haphazard manner for 18-24 months and that is where you can usually take a good slice of optimal profit. As far as entries into a junior miner go - right now is about as good as it gets - if you believe they will be able to make money any time soon. I do. We will just have to wait and see and adjust our perceptions as things move on.

The geology is simple while the metallurgy is not - it took SCY years and millions to understand and crack the HPAL process and get good recoveries. Then you can't just mine ore if you do not have a plant to process it, (what would you do with it???) even if you know how to extract the minerals. Before they can build a plant they must raise money, done via "talking about it" to financiers and banks, usually for about a year or so, sometimes much longer. This is a specialty project after all.

Also there is no way they will get $125k a lb that would provide no value to most industries that desire it. Mass production will drop the price for commoditized 97-99% powder oxide powder hopefully to less than $1500/kilo - providing win win cost benefits to countless industries.

I agree. It should also be noted Niocorp is mainly about niobium while SCY is a pure scandium play, with all the pros and cons that entails. SCY has basically unlimited production potential while Nio's scandium ore is not even correlated directly with niobium, which means they are kind of going in two directions. SCY is easy geology at surface (like Mexus), NIO is deeper and complex. Nio needs a billion dollars (ouch) SCY needs 1/10 that for a much higher margin project. SCY needs 125% market cap for their project, Nio needs 560%+ - very hard to raise 5.6 x your market cap for a project. Very easy in comparison to raise 100m (near market cap) with a DFS that has such a high IRR.

The market desires reliable supply and any one project is insufficient to provide that. If the sector leaders succeed, then the new class of scandium juniors and wannabes will develop their deposits - scandium is found all over the world, US, Canada, northern Europe, Australia etc but nothing quite matches the Australian laterites which are the undisputed mother lode of scandium - bar none - no known comparable deposits exist outside of Australia. Look at the grades and depths side by side - they are striking. Niocorp can easily succeed and make a lot of money for its holders but comparing their scandium discovery to SCY or any of the other Australians like Clean Teq or Metallica is a joke. One is a lean, mean Olympic athlete, the other is a tad overweight.

Side note: Clean Teq now has a Canadian listing (finally!) and is an excellent company with fascinating water purification technology and some of the best scandium on Earth. Kind of an interesting combo, even if they have slowed development of their mining projects as I understand it. On my list to do some research, I really like Friedland.

Probably worth it to own a basket of scandium companies weighted in SCY's favour imo.

I bet SCY starts to raise money here shortly and that should begin the next (less boring) stage of the mine cycle. In the mean time, we wait patiently (or not).

It is indeed missing the words "of the mineralized intercept" but that is what is generally looked at in all assays, and assumed by anyone familiar with this stuff. If I said "company x has great assays! They hit a big strike of over an ounce per tonne average!" clarifying that the grades are of a mineralized intercept is redundant. I highly doubt very many people (if any) looked at this information when it was fresh and just released and thought the entirety of all the cores from top to bottom averaged .4 g/t. (These are probably the same people who bought 100% of their stock at the high in 2012 and never lowered their cost basis since). Even if someone was under such an erroneous assumption, they would only have had to adjust their eyes a few centimeters down to the table that clearly showed the intercept lengths and assays - along with the dead sections that would make a .4g/t total average impossible at a glance even to someone with abysmal math skills. It is not deliberately misleading as you say because the original PR had a link to the assay results literally one or two sentences down from the sentence you disapprove of. I would personally argue that beating a dead horse years after the horse and the sources have expired is misleading, perhaps deliberately so.

To put this to bed, here is a fresh link to the assay chart that expired over a year ago:

https://www.dropbox.com/s/8bxmffebl7i68v5/Partial_Assays_from_Argonaut.pdf?dl=0

Hello,

[Removed potentially offensive text, all names, some educational value, and all examples and direct references. Discussion of the sentiment of bulls and bears is on topic and relevant and does not mention specific posters.]

I hope everyone is well. I have been occupied lately.

Mexus is in a stage of optimization and they will either succeed and earn a profit or they will not and dilute excessively and sap all potential profit. The outcome is binary and no words on a message board will change that. The doubters will always take a (warranted) pessimistic point of view and largely ignore data points that don't fit their perspectives while the believers will do the same with the inverse.

I think both sides raise excellent points...and also frequently [argue illogically]. The outcome is binary, yes or no, but the percentage likelihood is distorted by both longs and skeptics and I think both get it incorrect because of their implicit biases. I am guilty of this too but when interactions become very polarized it is often smart to take a step back and observe.

A skeptic can easily throw out the boilerplate warning that exists in every stock and mining stock in the world and be confident that they will be statistically correct over a large sample size-- but you can't do this accurately on an individual basis without considering the specifics of the equity/mine in question. If you just look only at the risk column it is significant and will negatively skew your perceptions. By this stuff I mean the generic posts about mining being risky, information I would hazard 100% of the board is aware of, yet is repeated every day.

So for good measure:

Mining is a very risky industry and most of the explorers fail to find an economic discovery and end up wasting their shareholder's money. There are thousands of mining stocks yet only the top 5-10% significantly outperform their peers and generate most of the sector performance --stock picking is crucial. There are hundreds of scam mining companies who only mine gullible investors instead of metals. It costs tens of millions if not hundreds of millions of dollars to open an average small scale hard rock mine and even doing the most stringent and costly studies and exploration will not guarantee the commercial success of a project. Several reputable geologists in this industry (Cook et al) estimate that only one in ten thousand geological anomalies (prospects) become a profitable mine and that developing them from discovery to production now takes well over 10 years on average in North America (slightly less in Mexico, slightly more in Canada). Mining is risky, prone to extreme delays, expensive, dangerous, immensely time consuming....and a potential lucrative business if successful. So knowing all that, if you just pull up a random ticker of a penny miner and had to speculate in one second on the chance that it would become a successful miner and earn a profit for its shareholders... I would estimate it is 1% at best, probably a small fraction of that. So if you were a junior mining bear you could be right most of the time without ever even opening your eyes.

A rational person therefore would never invest/speculate in this sector unless they were confident they could increase their success rate. The rewards for a successful project are great, but they aren't so great that anyone with sense would tolerate less than a 10-15% shot at making 10x your money. I think some will argue you can't increase your success rate and that investing in a junior without billions in studies and earnings is always a gamble- it is too complex to figure out, has too many variables etc. I don't agree with this line of thought at all and as proof I would point to a couple dozen good stock pickers that have such high accuracy that they sit so many standard deviations away from the dart board that it is 100% obvious they are on to something more than mere chance. Winning the lottery once is luck, winning it 4x in a row or 5/10 tickets is worth investigating how they are doing it.

Which leads us to "how?" How do guys like [censored names of stock pickers] pick many more successful juniors than should be possible?

Well, they openly tell us. Is it pure random chance? No. Prayer? No. Lucky rabbit's foot? Nope. It is methodology and research tempered with common sense and experience. They discovered after doing this 100s of times that certain attributes in a company make them much more likely to succeed in the long term. Identifying them means a greater chance of success. There is obvious stuff, you want dedicated management with skin in the game and interests aligned with holders, you want them to have cash, you also want a high quality project/property in a low cost district where it is easy to get permits etc.

[note this is on topic, a discussion of a common argument and not the posters who make them]

Which leads to some of the most bizarre conversations on this board essentially trying to answer the question, "Are the Mexus claims likely to contain economic gold worth mining?" Some skeptics may opine that they don't believe that to be the case, or that they cannot possibly know until everything is Swiss cheese or dore. I find this very conservative position to be strange and illogical. It is as if no mining in human history has ever been accomplished without the SEC. I have invested in early stage discoveries many times - and I did this not because "I couldn't possibly know" and "just felt lucky" but because the potential discovery was of obvious impact and of significance even to a layman. It just matters if it is comparatively impressive - average and below is risky, but if you have high grades competitors and potential partners are drawn to the margin. This is important because obviously impressive stuff is easy to market and communicate/contrast with other projects. Potential discoveries can be identified early without huge data sets and without a university degree/expertise. In my experience, results can be objective and built a within a more subjective overall opinion that can form a speculative thesis if there is enough evidence. Skeptics will pretend we cannot possibly have ANY idea of whether Mexus' initial deposits are economic and this is absurd. We don't need to be accurate to a percentage point, we just need to get a general sense of the potential and likelihood of discovery.

All we are trying to do is decide if we have enough reasons/evidence to make an informed speculative bet on Mexus.

[This example is on topic because it is a very common argument repeated on this board. If you insert Mexus specifics the case is not as quite as compelling as my example but it still demonstrates the absurdity of the argument that success is impossible without exhaustive exploration and studies.]

Let's do a little mental experiment:

Some prospectors in Alaska arrive following rumors and discover abundant minerals nearly everywhere they look, but none of the gold they were seeking. They keep looking and find strange green rocks. Eventually they discover shining pebbles made of what seems to be copper and so they follow them to a valley where the pebbles seem to be heavily concentrated, getting larger as they go. Soon they can't take a step without tripping on the big rocks. The team spreads out and discovers that in fact most of the giant boulders in the valley seem to be made of nearly solid copper of absurdly high grades. The team surveys the area and finds a similar level of copper boulders strewn throughout the valley and copper fused rocks leading up into the mountains, stretching for as far they could see. They make camp and one man finds a several large gold nuggets in a nearby stream. One of the team is shocked when his cook fire smelts the nearby ground into a molten puddle, while another explorer breaks his leg on one of the elephant sized copper boulders while posing for a picture.

Now what should they do? What makes the most sense?

1. They begin mining immediately on a small scale, starting with the most obvious high grades. They then reinvest profits in equipment and exploration and expand over time.

2. They cannot possibly know anything about anything and no judgements or opinions could possibly be made about the viability or potential of the deposit. There is no conceivable way to know if a field of giant boulders made of copper is valuable or even feasible to process without spending many years and millions in studies while hiring the best experts in the world. Without the SEC the Pyramids would not have been built.

Common sense matters, even if it should be renamed, "rare/uncommon sense".

Which brings us full circle to Mexus and the long side.

There exist many pieces of evidence that points to a high likelihood of Mexus possessing several hundred thousand ounces of high grade gold within a system that could potentially hold millions more(imo). This area is highly likely to contain an economic gold deposit beyond what has been outlined by Lemas and 100s of grab samples and limited RC drilling and coring. Even though these would not even technically qualify as "inferred" or "indicated" resources on a 43-101 I am more than confident they exist.

Why is it so hard for some to conceive that a gold deposit could exist on land that had:

-Recent multi-million dollar production from a tiny section of the Julio shaft between the 50 and 100 foot levels, allegedly taken by one man with hand tools.

-Multi-million dollar historic production from Spaniards and family artisans over 100s of years.

-Multi-thousand ounce historical production from placer production.

-very large high purity nuggets discovered near surface, indicating a nearby lode source.

-Cortez Boot - nearly 400oz nugget, largest in the Western Hemisphere discovered a short distance away to the north.

-The Trend. The Sonora-Mojave Megashear trend is home to some of the largest mines on Earth. Other mines on this low cost trend often stack and produce profits from deep pits with grades less than .5g/t, equating to a very high competitive advantage for Mexus' grades, at least during the first couple years of production. Examples include [censored].

-3rd party shareholder confirmation of near surface samples, shaft area.

-3-5oz/t Julio hanging wall assay.

-1km long vein system with historical assays over 100 oz/t, mined in pockets from surface.

-Abundant visible gold in drill core from Julio area and in shaft wall samples. No stock photos here, just gold.

Finding gold is always a long shot but searching on claims like these dramatically increase the odds.

Now none of this "proves" the deposit is economic, it only serves as evidence that the property is not exhausted and would be much more likely than average to contain economic gold--at the very least far more so than random chance or someone digging in their backyard by orders of magnitude. When I factor in the potential of the property down to say 500 feet the numbers get enormous. Even using only the tip of the iceberg, there is a 100% chance in my mind of at least one un-mined bonanza pocket near the existing shaft and ~200,000 oz contained just in the easily accessible material available at surface.

Considering the development time, progress rate, and ongoing education and dedication of management, I think this is an excellent speculation with a high chance of success and a compelling risk/reward equation at this moment in time.

Consider this:

Mexus has initially stacked high grades. If Mexus had stacked low grades in line with many nearby peers that would be difficult to change and make money off of without a large scale operation. This high grade represents their potential margins and anything above 1g/t is quite high for this area. Stacking up to ~3g/t+ with pockets of higher grades is exceptional and represents such a thick margin that I think it would tolerate almost monumental mismanagement and low efficiency and still make a small amount of money. If the gold isn't in the ground or stacked on the pad it cannot be extracted --Mexus has proven beyond the shadow of a doubt they have some very high grades and this is the most important part.

It should be noted there are gold mines out there that have failed even with high grades stacked upon their pads/ran through their mills. It isn't enough to just mine good grades - they need to be leached and processed effectively. Getting this right is one of the reasons for some of the development studies we glossed over, saving time and money, but also by its very nature necessitating a potentially long optimization phase and the expectation thereof.

There are many ore types that are very complex and require a lot of metallurgical testing and tinkering to find an optimal cost/benefit to extract. Sometimes a mine will stack sulphide rich ore and even with high grades, gets low % recoveries into the pond. Sometimes the ore needs more crushing, roasting, agglomeration etc meaning this could cost a lot of time and money to crack and not doing it may lead to a failure. Many of these complex ores will require capex and equipment worth over one billion dollars for a commercial operation. Yet Mexus, despite perhaps suboptimal crushing, is clearly leaching the ore at an impressive rate. The pond is pregnant- getting to this point is by far the most difficult challenge in this type mine and they are done. Imagine they instead stacked high grades and there is nothing in the pond - that is a lot of potential work to figure out, with many expensive pitfalls.

The last step is recovery and here I would posit that given the grades of the pond and the operation of a fully functioning MC, the recovery of gold is a certainty. I don't see how it could not be recovered without some kind of serious flaw in the construction or engineering of both of the plants. No amount of money can improve what's in the ground and increasing recoveries can often be enormously expensive but this is different. This is close to the last step, essentially the X in the alphabet of mining, and can be fixed with money and time. The delays aren't ideal but expected when mining with a shoestring budget. Next up: golden laces.

Have a great day everyone!

One more rubber stamp mining license to go, financing should be right behind. Going to be an interesting couple of months I think! Nearly two million dollars/4 mil shares traded today. The rally continues and SCY is held tightly. I think it could easily go to .75 or so in the short term.

Financing on very good to excellent terms is now imminent in my opinion. SCYWARD!

I had a few good links but they no longer appear to work. What you can do is go to a stock screener website (Bloomberg, Fool, Google Finance etc) then sort by industry (metals and mining) and see what you find. Kitco also frequently posts analyst opinions in charts so you can see a large block of the sector in pms as opposed to base metal companies. Another thing you can do to learn more about miners and their ratios is to pull up miners within Mexus' potential peer group. You will probably be surprised at what you find but be wary, for it is nearly impossible to make an apples to apples comparison in this industry without knowing a lot about the specific stocks and projects.

I have mentioned this a few times before but juniors tend to spend money, not make it - this makes any earnings, regardless of ratio, comparatively more valuable than a company with negative earnings and dilution to pay for it. So in plain English: If you pull up 200 juniors I would bet at least 180 of them have negative earnings. So if you have a company in the top 10% that has a P/E of 1000 - that is an absurdly high ratio but it is still comparatively resilient when placed beside its non profitable peers. Once a mine is proven and established they tend to get low P/Es similar to utilities, reflecting steady income from known customers and contracts and plants/reserves, and the high likely cost of capex for increasing eps. Of course a miner's value is not derived 100% by earnings.

Fresnillo the behemoth is a 12 billion 30x stock, GORO is a P/E of 55, AR nearly -$2 eps on a $2 stock - yowzers. Bunch of juniors, all negative, Torex - p/e of 618! Marlin -20 cents, Timmins P/E of 8 - undervalued, GoldCorp - 80, Yamana and Primero, hugely negative etc. I just looked through about 50 of these, only Timmins was under-priced by P/E ratio but it is hard to tell without knowing a lot about the specific companies. Maybe low ratio company X is running out of high grade ore in a risky country while high ratio company B has been using its income on acquisitions and expansion and will have a huge mine coming online soon. All you can do to make better mining speculations is to learn more about other projects so that you can make better comparisons, mentally rank them, and potentially find cheap gems.

I would argue that Mexus is highly likely to receive more than a 10x ratio in this current environment, especially since if they prove one low cost mine it makes it more likely the market will believe they can do the same at the SF or potentially elsewhere. I don't think Mexus will ever have a 100-600 ratio beyond start-up but anything is possible. I found so many absurdly high P/E examples I will stop there because I don't want to imply that I think Mexus will be justifiably priced at such a high multiple if they go on to earn significant income. They could be, but if that ever happens it would probably be a good place to take ample profits.

March 2, 2017 (Source) — Scandium International Mining Corp. (TSX: SCY) (“Scandium International” or the “Company”) is pleased to announce it has signed a Memorandum of Understanding (“MOU”) with Weston Aluminium Pty Ltd (“Weston”) of Chatswood, NSW, Australia. The MOU defines a cooperative commercial alliance (“Alliance”) to jointly develop the capability to manufacture aluminum-scandium master alloy (“Master Alloy”). The intended outcome of this Alliance will be to develop the capability to offer Nyngan Project aluminum alloy customers scandium in form of Al-Sc Master Alloy, should customers prefer that product form.

HIGHLIGHTS:

MOU outlines terms of a commercial alliance with Weston Aluminum,

Represents key steps towards Master Alloy manufacturing agreement,

Allows SCY to quickly apply know-how alongside operating aluminum processor,

Supports a product offer more suitable to many downstream customers, thereby expanding the potential customer base, and

Allows SCY to bring added value to significant potential scandium markets.

The MOU outlines steps to jointly establish the manufacturing parameters, metallurgical processes, and capital requirements to convert Nyngan Project scandium product into Master Alloy, on Weston’s existing production site in NSW. The MOU does not include a binding contract with commercial terms at this stage, although the intent is to pursue the necessary technical elements to arrive at a commercial contract for conversion of scandium oxide to Master Alloy, and to do so prior to first mine production from the Nyngan Project.

Discussion:

SCY has been developing an internal understanding and capability to convert scandium oxide to Master Alloy for some time. In 2014, the Company announced it applied for a US Patent on Master Alloy production, which is still in the application phase. That Patent Application addressed scandium Master Alloys with both aluminum-base and magnesium-base metals. The Company has investigated scandium Master Alloy manufacturing processes previously with the CSIRO, in Australia, and Kingston Process Metallurgy (KPM) in Ontario, Canada. Further, the technical team in SCY has previous relevant experience in this metallurgical area.

Weston Aluminium is a privately-owned, established secondary aluminum and industrial services company with its production facilities located near Kurri Kurri in, NSW, approximately 50km from Newcastle and 400km from the Nyngan Project. Using an environmentally attractive ‘non-salt’ processing technology from Asahi Seiren in Japan as its core technology, Weston has further developed its application to process all forms of aluminum bearing dross and by-products from the aluminum industry, and manufacturing Aluminum Deoxidant for steel making for BlueScope Steel at Port Kembla NSW and Arrium at Whyalla SA. Weston recycles industrial aluminum scrap, and dross, principally from the Tomago Aluminum Smelter located north of Newcastle, which is an independent joint venture between Rio Tinto Alcan, CSR and Hydro Aluminum. Weston today recycles 20,000 tonnes of aluminum materials annually, and has established capability in recovering valuable metals from metallurgical process dross materials, resulting in zero land fill.

Recorded on Feb 26th released Feb 27th evening, ihub release March 1st evening.

Tyler Martin Mexus Interview

http://vocaroo.com/i/s0hWFrAJQKmT

Hey this is Omer Aubin and I am here with the speculator Tyler Martin and today we will be discussing Mexus Gold US and junior mining in general.

So, for starters, who are you?

My name is Tyler Martin and I have been investing since I was eight years old. I have also become a pretty proficient junior mining speculator over that time, although investing and speculating are two very different disciplines.

What are the differences between speculation and investment?

A speculation is an educated bet on something that a company or person has no or limited control over. Examples of speculative questions would be: how can I profit from a political event? is a mining company capable of discovering something? Are they likely to? If they do can they expand the deposit, can they mine it at a profit, will they be able to receive permits or social license, raise money etc? On the other hand, investing is usually just basic math: you buy undervalued companies that exhibit strong profits, dividends, low ratios etc that are trading at cheap prices and then you hold these stocks until the market recognizes these facts. The beauty about junior mining, aside from its great wealth creation, is the fact that if you correctly pick your stocks you can often make a lot of money on the speculative side AND THEN make even more money on the investment side if a miner goes on to produce at a profit.

What are some of the things you are known for?

I have done a few interesting things including calling the 08/09 bottom for commodity stocks and then going on to rank in the top ~10-20 for publicly performing portfolios on Motley Fool for a couple years or so. At about this time too is where I really got a strong appreciation for junior miners and commodity stocks along with the wealth creation they can produce. There was this perfect moment back in 08/09 when mining companies were still making money and yet were priced as if the world would immediately stop consuming commodities and was going into an apocalypse that they would never recover from. Many of those stocks ran up over a thousand percent, including TCK and ANV. Commodity stocks are the only type of stock aside from technology where they can start with almost nothing but a dream, and then through discovery, create enormous value. In the past ten years I have publicly called at least 50 500% + multibaggers, even managing to buy the bottom and sell close to the exact top more than a few times, not always, but quite often. There is clearly a time to get in and out with these stocks. In recent history I had a position in one of Canada's 2016 top gold performer, Claude Resources, a company I bought the low and sold the high within a few percentage points for about 1000% in two separate instances over several years. Claude was bought out in 2016 for a large premium after a great run-up after the company made some changes and became profitable. Claude is a good example of a speculative miner that becomes an undervalued investment, shifting from an educated bet to a no-brainer Ben Graham style value investment. Other than that, my family owns lots of SCY, (Scandium International) a very unique mineral company that has an absurd amount of potential and that could radically change many industries and products for the better including fuel cells, bloom conversion technology, and aluminum alloys for aircraft and light vehicles among other things. SCY has gone up about 1500% or more since I entered and I would say SCY is the limit there. Last but not least, I own a decent chunk of Mexus Gold, and as far as I know, it is the top gold performer of 2016 in the gold sector for about a 16,000% increase from its lows to highs. I don’t have 100% accuracy - but I am well above average including many highly paid analysts. I have only had one notable mistake in recent memory, which was Rubicon Minerals, a company I previously made a pretty decent % off of on the exploration but lost on the production speculation.

As of this moment, Mexus Gold US is currently the only junior mining company I own in my personal accounts and for very good reason.

What is Mexus Gold?

Mexus Gold is a US based junior mining company that has its main mining operations in northern Mexico, in Sonora state along the Sonora-Mojave megashear geological formation that is home to some of the largest and most successful gold mines ever. The flagship property, the 7300 acre Santa Elena, is located northwest of Hermosillo and is a high grade, near surface deposit that is geologically simple to interpret and chemically advantageous to process. The mine is anticipated to pour its first gold dore in March or April of this year. Mexus also controls another nearby mine, the San Felix, which has substantial infrastructure in place along with a very large land package of 26,000 acres with several unmined pits cleared of overburden which should reduce initial mining and startup costs. As the mine is already built, the San Felix is could be placed into production very swifty at relatively low cost. Both the Elena and Felix are operated by Mexus’ JV partner, MarMar, under an agreement by which they construct and operate the mines in exchange for half of the revenue after operating expenses (once startup costs have been repaid). Mexus also controls several other exciting nearby exploration projects including the high grade and near surface mineral prospects of the silver discovery at Ocho Hermanos and the very impressive copper and gold target at Scorpio, with both target’s initial surface results currently many times the industry’s mined average. In my opinion, the company’s high grade projects, large production potential, low debt, and low cost philosophy make it a compelling value generator compared to the vast majority of other juniors.

What is the company's current focus?

Mexus and MarMar are focused on getting their primary project, the Santa Elena mine, into production. The objective would be to pour gold at a profit, optimize and expand the operations, and then begin to shift focus to development at San Felix’s parallel crew. Once the company has both operations producing they will then start to explore their other properties along with the current mines in an attempt to discover more minerals for future production.

Could you tell us a little bit more about the Elena project and why you think it will be a successful mining operation?

Sure. The Elena claims were family controlled for generations and this kept it off the direct market and out of Fresnillo’s paws. Mexus made an agreement with the family in 2011 to develop the property. They did a bunch of initial discovery work that found excellent results following a system of gold bearing quartz veins and the surrounding shear zone that the veins have eroded into over time. High grade mineralized material was found throughout the area and the decision was made to place the project into production to mine the obvious high grade sections visible from the surface. As of this moment construction appears to be complete on the Merrill Crowe recovery plant and the associated pads and ponds along with over 3 meters of material stacked on their pad, just waiting for the spray lines and cyanide. The long, costly road of mine development is nearing its end and Elena has got there early and well under budget.

The main reason I have always believed that the project would be JVed and ultimately mined successfully is because the Elena project is impressive on a relative basis. If you look at the trend itself and these gigantic gold mining operations, from La Herradura to La Colorada, Noche Buene etc, you will see that these world famous mines all around the area are producing profits at tiny fractions of a gram (0.56,0.64, 0.79 etc and even well under half a gram in Durango), even during the currently depressed gold price environment. So if some of these guys are mining low grade sulphide ore deeper in their pits and trucking it for miles...and still doing it with a smile on their faces and earning lots of money… then comparing this to the Santa Elena where there is no overburden, the gold bearing material starts at surface, the grades are anywhere from say two or three to several hundred times what everyone else is mining, and then they only have to move it a pitiful distance while still operating within that same low cost district.... That seems like a scenario that has a very compelling risk and reward equation to me. This relative margin that these deposits represent is a competitive advantage and the reason other miners have been interested in the property for decades.

But how do you know that the gold is there? Isn’t entering production without traditional exploration and feasibility work risky?

Sure, of course it is risky - everything is risky, but to be fair Mexus has done a lot of exploration work - just not at the level of a bankable feasibility study. Mining is a risky business in general, notorious for delays and high profile failures… but there are also common sense elements that can be applied to this. First of all, even doing all that very expensive, time consuming work is still not a guarantee of success or future results. Examples like Rubicon spring to mind - it looked great on paper and pleased all the government officials and geologists but ended up being a complete disaster for shareholders. Despite a near billion raised and countless encouraging studies spanning 1000s of pages it didn’t - or hasn’t yet led to any profits and the old holders were wiped out. That is an example of something that looked impressive at first, second, and third glance, it pleased all the experts, but was actually highly flawed. Mexus sort of gives the opposite impression, if you only do ten minutes of research you will be disappointed by their lack of cash and rough appearance and then potentially dismiss what is probably one of the most compelling opportunities I have ever seen in this sector. There are some that will point to the lack of feasibility work as if it means the project is highly unlikely to succeed without it but I would point to the tens of thousands of years of human history that existed before 43-101s and IG7 compliant reserves - there has always been a way humans have mined, even with no technical skills or geological knowledge whatsoever. It is called common sense and mining what you see and then stopping when you run out. This is the old timer method and it works marvellously for near surface deposits with visible gold and easy to understand geological cues. As evidence of this I would point to the thousands of examples of this being successfully done during the last few gold rushes.

So do I think there is gold on the property? Absolutely! For starters this area is famous for its gold discoveries and its well known mining heritage and the trend itself is now home to gigantic, world class mines. The Elena mine site once had outcroppings in the multiple kilos of gold per tonne range (this is in the ballpark of 100 oz/t gold you stub your toe on). These outcropping were high-graded long ago as part of the artisanal and historic mining work on the property. Many other comparable areas with such finds would have been mined extensively and drilled to oblivion but this property has not been, owing to its strong family ownership over the years. To me, that alone, demonstrates this is a property with very high exploration potential and more than a decent chance of striking a bonanza. Even if the old timers would have mined huge sections, which they did not, choosing instead to cherry pick the best surface material they could find, there would almost certainly be a lot of lower grade ore that was unappealing to them but would make an excellent heap leach project in 2017. Mexus has also found large amounts of visible gold in the drill cores from the veins and shaft area. Most mined gold nowadays is microscopic so if you can see it with the naked eye that is very encouraging, and rule of thumb is it is economic as long as it isn’t in Antarctica, deep, hard to recover, or under a lake. The shallow shaft on the property has ample historical production and current assays in the hanging wall of gold measured in ounces per tonne - this proves that the surface grades continue at depth and become substantially higher grade, at least in some areas, down to 50-100 feet at the very least. There are assays up to about 6.5 oz/t from the underground and I am aware of limited historical production done relatively recently that was in the neighbourhood of sat .25 to .5-20 oz/t from that same underground mine, making at least a section of it one of the highest grade gold deposits on earth. This is all located a small distance away from where they are now mining and seems to be one connected system. There are mining companies that haven’t heard the expression “ounces per tonne” in decades! If you extrapolate out the results from the shaft and match it with the 800 meter long vein system it is a slam dunk for a million ounces minimum in my opinion and I don’t think it is that hard of a prediction to make. Estimating the size of mineral deposits in early days is something I have had a lot of success with, and, in my opinion, Mexus’ is the easiest million oz I have ever looked at. There are examples like Golden Eagle that show a company can be bought out for a huge sum with limited drilling as long as long as they demonstrate a large, simple, high grade, and above all consistent project that has obvious merit to a buyer. I don’t know for certain how much gold is there but an initial potential deposit of 1-3 million ounces seems like the tip of the iceberg. Third party assays of average looking rocks laying around the area often assay at 10-20 grams per tonne or more. Mexus and MarMar geologists have done lots of sampling and assays demonstrating there is lots of mineralized material in the 1 to 2 gram average range, enough for a year or two of production without much additional exploratory work. The company recently released a column test with a recovery of .7 grams, which is well above the head/assay grade of many of their renowned neighbours and is right on target for a conservative 1 gram average stacked on their pads. The general area of the mine is also famous for its large, very high purity nuggets and historical placer and artisan production. Some of the nuggets found by Mexus shareholders on brief site visits to the property were just absolutely immaculate - way bigger than anything I have ever found prospecting or even bought online. These are some of the most beautiful, pure, and massive nuggets I have ever seen, they are clearly close to a lode source and the veins they eroded from. The claims are also in the general area of the famous Cortez Boot discovery, the largest nugget found in the western hemisphere, at nearly 400 troy ounces. The number of stories and anecdotes goes on and on forever… from panning gold on the haul roads to old nugget discoveries from hundreds years ago. Some of the information is perhaps unreliable, not well recorded, or lost to time but, there is still enough evidence there to make it obvious to me that they have a desirable project. So in the end is there a piece of paper that says they have proven a million ounces of high grade gold beyond the shadow of a doubt? No, but there exists so many signs that I think it is likely the Elena claims have a lot of economic gold, probably at least a million ounces representing lowest quartile costs to produce because of the project merits and high grade relative to their low cost peers.

What can you tell us about Mexus’ management team?

Mexus’ management team is Paul Thompson. He is an experienced serial entrepreneur that has owned and operated gold mines in Mexico and California. He also is a skilled fabricator and low cost operator with expertise in construction and project management. If you want something built at low cost and with a little unconventional ingenuity I would say he is your man. Paul has proven himself as a trustworthy CEO and dealmaker.

Mexus also has a small team of advisors that assist Mr. Thompson.

The current company structure is, at the moment, more dependent on Mexus’ JV partner, MarMar than on Mexus itself.

What can you tell us about MarMar?

MarMar is a Mexican holding company run by Marco Martinez, a wealthy businessman and entrepreneur from the area. MarMar has done contract work at several of the nearby mines including La Herradura and they have directly applicable production experience at similar mines. They also control a very large fleet of heavy equipment and have the manpower to operate them. If they use even 20% of their capacity Mexus will be a large regional producer and most likely enter six figure gold production. The deal with MarMar is one of Mexus’ strongest advantages over similar companies. They gain not only cash to construct their mine and an experienced regional operator but also access to equipment and labour including specialists like geologists along with political and legal capital they would not otherwise have access to as a foreign operator in Mexico.

What do you think is a reasonable market cap for Mexus if it had both mines producing at a profit? What do you think of the company’s long term potential?

Hard to say without knowing exactly what grades they consistently stack and how much they produce over time. Mexus can conservatively be worth 10-20x their net income, so if the grades are average at 1 gram and they achieve 10k t/day as their first target at Elena that is probably around 25,000 oz, or somewhere around 20 million dollars after tax. A low ratio of ten to fifteen puts them at about 200-300 million market cap, around 50 cents a share.

If they did about the same at San Felix that is around a dollar for fair value using earnings alone. If you start adding in values for other properties, equipment, plants, exploration work etc there is a lot of additional market cap there without even applying a premium that Mexus should likely receive as the preeminent project in the area with what I believe will be much larger profit margins than their peers.

Now here is where things get interesting - that is about a ten bagger for what I view as a fairly conservative case - but what if we go beyond? What happens when they ramp up from 10 to 20k a day to 25k a day at both projects? What if grades come in higher than that base case as I expect? What if gold prices rise? What about the other high grade properties?

Well I will let people crunch their own numbers but, needless to say, the potential values start to get enormous. Then, long term, if you imagine three to five years out, dividends paid and gold flowing while exploration programs churn out impressive results from already known high grade zones… Mexus is limited purely by what it can profitably produce and find along with the prevailing gold sector sentiment. If the properties are the limit then we are in great shape because I believe the Santa Elena will rival other mines of the area and that the value goes DEEP here. The surface seems like more than enough to make current holders rich - what lies beneath is nothing less than the potential for one of the largest gold mines on earth.

Where do you think gold prices are headed?

I honestly don’t know and I am sort of agnostic to this. I am biased towards it going higher, especially over a long term period but over say the next year or two? No idea. This is one of the reasons I like Mexus and high grade projects in general. Gold prices stay the same? We make bank. They drop significantly? They could survive and live to fight another day. They rise? Bust out the champagne - we got that upside for free! At $800/oz Mexus is worth very little; at $2-$5000/oz it is a multi billion dollar venture.

Did you have some other points that you wanted to add?

I wanted to just quickly elaborate on something I mentioned before. One of Mexus’ core strengths is that they have achieved remarkable progress without taking on significant debt - this is largely unheard of in the mining industry. Miners are some of the most indebted companies on Earth and often take over a decade and tens to hundreds of millions to develop and then, when they finally start production, they have a noose around their necks. Mexus has done it all in a few years with no real debt to speak of. Mexus is also owned and funded by shareholders, not by banks or vulture financiers, which is highly unusual.

This tightly knit shareholder group means that the float is controlled by smart money and any buying or selling pressure will have exaggerated moves on the stock price. I feel these shareholders are also likely to hold the majority of their stock because they appreciate and understand the company’s potential and are convinced by the evidence there is enough gold to get started and lots more to be discovered in the local proximity.