News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

GermanCol

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Flipper44, let me offer you my opinion as an answer to your question. I disagree with the following statement from CherryTree1:

The price dropped to something like 0.5 cents. Undoubtedly all stop loss orders were triggered at that price so nothing left to cancel.

Charlye, regarding your inquire:

My inquire is...Dont you think that it was better for the company to wait for a better pps to obtain a better deal due to the fact that the company decides when? or they decided to pay as soon as possible to avoid bigger problems?

Anyway, if Verus are now out of the woods, finacially wise, we all here will expect an easy 0.035 come back soon, as they will report a good Q3,lets say USD6M but a really record revenues on Q4 and next Q1, really game changers to see even profit, now that they have corrected Anshus compensation

I want to share my theory of why I think we are going to be free from notes and convertible notes very soon and company is going to announce it. I also think this note payment is going to bring a huge share price increase. In the table below is the information for all notes and convertible notes ordered by maturity date that I have put together looking at our filings and crossing information.

What is highlighted in pink is what is my estimation according to last filings and OS changes. The numbers not highlighted in pink are exact numbers coming from previous filings. In the last line you will see the average share prices for VRUS for the different Qs, that are always higher than the estimated conversion prices, so the numbers make sense.

As some of you should remember, around Jan 31st 2020 the company got delinquent in reporting and the notes at that time defaulted, so they had to start to renegotiate the corresponding terms and payments with noteholders. In the table is the information of how they have been paying them.

Then, on August 19th Anshu’s tweet he said that the recent volume was not from White Lion. The only way he could now that was if no shares had been sold to White Lion until that date. Also, to reinforce this theory, the last change in OS from August 10 to August 24 was 607,268,379 (3,782,151,277 – 3,174,882,898) that is just a little bit more than the number of shares registered for White Lion sale on last S-1 (598,515,704). Also I think the company was waiting to make sure previous noteholders had converted and sold or almost sold all shares before selling to White Lion, so the share price would not have a double effect of selling, so that conversion price would be higher with benefits for the company.

So according to my theory, what occurred is that they paid all the notes according to the table presented above (they probably used all or part of last 3 notes to pay in cash part of previous notes still outstanding) and then on Monday 24th of August or around that date they sold to White Lion and final sale price will be around $0.00114 (0.0012 * 95%. 0.0012 was the lowest price on August 24th and for the whole week). With that money from WL they will pay all or part of the last notes for $165K, $153K and 63K plus Monaker note (according to dates agreed by VRUS and Monaker).

Reinforcing this theory is the timing and proximity of last two PRs. Timing was excellent because if WL dumped part of the shares sold to them in order to pay less for the shares, thanks to the news on Monday the price didn’t go down by much and then started to climb. And then when price was coming back the following day, the second press release made it jump again as it did Yesterday. So if this is the case, payment by White Lion will be not less than 0.00114 per share. Also take into account that the deals with NHL Meijer, TJ Maxx, Marshalls and Big 5 were from before, sure not at the same time, but news were strategically timed.

Also reforcing this theory is that the last 3 notes can start converting by the noteholder by 26 Oct 2020, 8 Nov 2020 and 10 Jan 2021 respectively, so before those days is important to pay them because they have a huger discount than WL.

Very important to note in the table above in the line Total that in the Q3/Q4 2020 for the first time the notes amount is decreasing and by a huge amount (1,626,000). Before that, it was always increasing or stable (600,000, 605,000, 405,000o, 0 and 709,500 from Q2 2019 to Q2 2020).

Much people forget what happened to businesses around the world with Covid and I see VRUS not only surviving, but doing great improvements.

And finally something to think, dilution for the last year of around 65% is nothing compared to price reduction by more than 10 times from highs that has come just as a temporary situation due to supply vs. demand of shares (due to Garnock sale and note conversions mainly) that will change dramatically very soon. So just with the same business, price should be around 6 times the price now if it were just for dilution (10 / 1.6 = 6.26), but also we now have a much bigger business. We are tremendously undervalued.

Excellent post and observations cowsgomoo. Agree 100%. Now following you.

Great!! I come from/live in South America. Tough times covid-wise here also. I hope we all get out of this situation soon.

Thanks a lot 2times2. Actually my first language is Spanish, but was able to translate your kind words. Happy to have you here in VRUS!!

The same to you!! Thanks a lot and enjoy the rest of your weekend too. Agree, I think a big run is coming soon.

Regards,

GC

Thanks SPORTYNORTY, appreciate your comments. Specially coming from somebody with such an impressive ratio of followers (6094) vs. posts (17,919) plus the big number of followers itself. I Haven't seen that before. That speaks very good about yourself. I was impressed when I saw you joining VRUS, so you got a new follower here. That also made me more confident about very good times coming for VRUS. I agree much higher price is coming soon, note conversion and Garnock's dump is almost over if not over already.

P.D.: In case you find mistakes in my writing, please take into account English is not my native language.

Agreed 100%. Welcome to VRUS from a longtime shareholder.

I continue to think that part of White Lion funds are going to be used to pay notes and the majority is going to be used for growth, as I mentioned in my post. I don't see how the 8K changes any of that at all. The total amount of $5M is much more than what is going to be paid to Monaco and we still don't know if all or part of Monaco's note payment will come from White Lion, if any. I guess at least part of it will come from WL. I think we will know or have a better idea how those funds are going to be used soon. Around Sept 15th when Q3 is reported the picture will be clearer.

kingpindg, please let me give you my point of view. I agree with Thoth, from my point of view White Lion's deal is much better than Garnock's. I don't see White Lion controlling the price because the company decides when to sell (and has the right to do it vs. White Lion, that has the obligation to buy if the company wants to sell), not White Lion and also since White Lion can only have less than 5% of the OS at any time, they can not dump in the way Garnock did. Also, with the small discount vs.share price of 5% it's not worth for them to sell fast. The benefit for them comes mainly by letting the price go up and selling responsibly if they decide to do it. Finally, what I see in Garnock's case is one person deciding and being more driven by emotions, vs. a company with more people involved in decisions.

You're very welcome shots60 and thanks a lot for your words. Our time will come soon.

Can you share the parts that I supposedly intentionally left out? I'm ready for the discussion but if it is serious and with facts and evidence.

What I posted is correct. And what is mentioned in the post I'm replying to is standard wording for S-1's. The same was included in S-1 / S-1A for the case of Andrew Garnock of situations that "may" happen, not that "will" happen. See page 20 of 104 in the PDF below corresponding to Garnock's S-1A that mentions the same:

https://www.otcmarkets.com/filing/conv_pdf?id=13567553&guid=F6P6UF3pD-hSl3h

The difference is that in the case of White Lion there is explict prohibition for them or any of its affiliates to short, as shown in the corresponding 8-K, Section 5.1:

Section 5.1 SHORT SALES AND CONFIDENTIALITY. Neither the Investor, nor any affiliate of the Investor acting on its behalf or pursuant to any understanding with it, will execute any Short Sales during the period from the date hereof to the end of the Commitment Period.

Essentially the noteholder is getting the inventory for free and paying for it when sold but that money goes directly back to the noteholder.

First, Accredited Investor shall make the following payments to the following BLF vendors (the “Vendor Payment” amount):

$ 34,989.40 (production)

$ 14,166.10

$ 2,455.00

$ 8,250.00 (bagging)

TOTAL$ 59,860.50

Thoth, welcome back, great to have you here with us. I agree with all you mention in your post. I think shortly after Garnock is finished selling (I think we are almost there or already there) we are going to move up very fast as we did when Garnock came in (10 times or more in share price).

Following is my analysis of the agreement reached with White Lion as compared to Andrew Garnock's. I think most people don’t understand the great deal White Lion is for VRUS and why this is a much better agreement for the company and shareholders than Andrew Garnock’s.

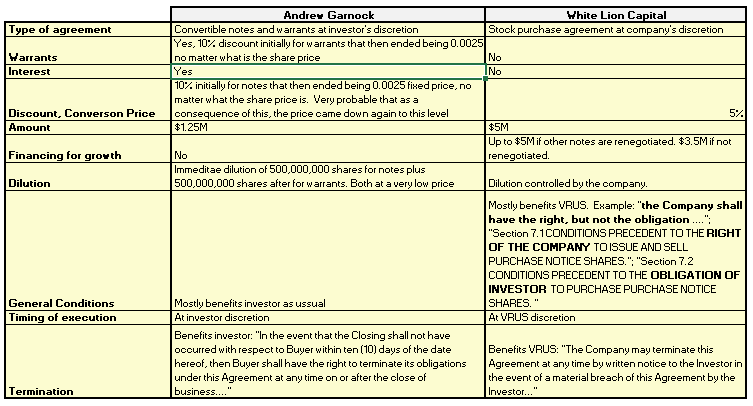

The following table summarizes main the differences and all without exception are advantages of the new White Lion deal vs. Andrew Garnock’s.

One of the most important advantages for me vs. A. Garnock's deal is that discount with White Lion is only 5% vs. 10% and that the company is the one that decides when to convert or sell, not the investor. And very important to take into account that because of not financing for growth through Garnock's agreement, the company ended having to take the additional notes that then converted. I think Anshu learned from his mistake and now reached an agreement that left most of the financing for growth in case he doesn’t get commercial lending soon.

This new financing is a novel system that fully aligns investor to company interests. Because of the small discount of 5% investor has real benefits ONLY by the combined exponential effect of the two factors: high share price times big increase in share price. So for him as for the company is much better to buy the majority of shares at the higher price possible (higher base) and keep them as long as possible (higher increase in price).

Toxic finance discounts on the other hand are huge (around 50% to 60%), so there is where lenders make the money. That's why they start to dump shares as soon as they can and also because they know that as they dump, the share price starts to collapse and they lose their benefit or part of it if they wait.

For both, investor and company is not favorable to execute all the deal at this prices, but higher.I guess the company will execute at this level for any emergenciers and live the majority for much higher prices. Fortunatelly is at their discretion and not at the investor's discretion.

Additionally, as part of the agreement, there are limitations for the investor and for VRUS that represent benefits for shareholders. Examples of these are no dilution permitted for other deals and no short sales allowed. Also, as expressed all along the 8-K, White Lion has developed an extensive due diligence to VRUS and found it adequate to sign an agreement by which they have the obligation and the VRUS has the benefit of the $5M funds if they want to use it.

Link to 8-K:

https://www.otcmarkets.com/filing/html?id=14257168&guid=yK_6UnZYzV0m0yh

Excellent post Charlye, agree 100%. I think AG is out or almost out and good times are coming. We need to hold tight and don't let emotions get in the way.

Thanks a lot Doc logic for your answer!! Appreciate it.

Could the IDH mutation be used also to help in the differentiation between pseudoprogression and real progression and give some kind of confirmation? Any thoughts?

Happy to see you Pro-Life!!!

Exactly Bud and all this intensified action of "saviors" looking for cheap shares make me think great times are coming soon. Good to be here with you.

Please share with us the facts and evidence of what you are saying so we can have a structured conversation. Enlighten us please.

Right my friend, it is another lie coming from somebody that hasn't proved anything he writes and has no idea about finance: "negative net revenue", lol. What in the world was he trying to say, maybe negative net income? Lol lol lol. Net revenue means revenue minus discounts and related items. No cooked books, no fraud. Why all this accusations without any proof? Why they waste all this time here posting?

Prove it. Still waiting and zero evidence.

People, please beware of false information. Following is the evidence that what is being said in the post I'm replying to is absolutely false, because the $5 million payment is contingent based on sales and if VRUS has to pay the 5 million is because it has made much more revenue and profit from this license:

As described in Note 6, during April 2019 the Company acquired the License to sell MLB-branded frozen dessert products and confections as part of its acquisition of BLF. The consideration payable to the seller of BLF includes $5,050,000 of contingent consideration, of which $50,000 is due upon the initial sale of an MLB-branded product and of which $5,000,000 is to be paid over time, through December 31, 2022, based on future sales of MLB-branded products (the “Earnout”). The Earnout is payable on a quarterly basis at $1.00 per case sold for sales that have a minimum gross margin of 20% per case. The Earnout payable each quarter is limited in aggregate to the operating income of BLF; however, any amounts constrained due to this limit may be rolled forward to future periods and paid when there is sufficient excess operating income. The Company accrues for this contingent consideration when payment becomes both probable and estimable.

No, is not toxic.

What is a Toxic Funding

A toxic financing is convertible debt or preferred stock that allows the financier, the holder of the debt or preferred shares, to essentially receive an unlimited number of free trading common shares when they convert their debt or preferred shares to common stock.

What Is Toxic Debt?

Toxic debt refers to loans and other types of debt that have a low chance of being repaid with interest. Toxic debt is toxic to the person or institution that lent the money and should be receiving the payments with interest. Toxic debt generally exhibits one of the following criteria:

Default rates for the particular type of debt are in the double digits

More debt is accumulated than what can comfortably be paid back by the debtor

The interest rates of the obligation are subject to discretionary changes

Any debt could potentially be considered toxic if it imposes harm onto the financial position of the holder.

Section 2.1 PURCHASE NOTICES. Upon the terms and conditions set forth herein (including, without limitation, the provisions of Article VII), the Company shall have the right, but not the obligation, to direct the Investor, by its delivery to the Investor of a Purchase Notice from time to time, to purchase Purchase Notice Shares provided that the amount of Purchase Notice Shares shall not exceed 250% of the Average Daily Trading Volume or the Beneficial Ownership Limitation set forth in Section 7.2(g)

Section 7.1 CONDITIONS PRECEDENT TO THE RIGHT OF THE COMPANY TO ISSUE AND SELL PURCHASE NOTICE SHARES.

Section 7.2 CONDITIONS PRECEDENT TO THE OBLIGATION OF INVESTOR TO PURCHASE PURCHASE NOTICE SHARES.

I think it's time. GLTU too.

Prove it.

GLTU in your quest to defend crappy OTC managements & company fundamentals .

You quoted me and then implied that I said that every company needs dilution and said that what I was saying is false. I'm waiting for you to prove that what I really said is false. By the way, following is my whole quote, not the piece out of context you shared and it shows with numbers that what you said about constant dilution is absolutely false:

Companies need dilution to grow, the important thing is to have it controlled. Good news is that for the case of VRUS, it has been around 10% in one year and in the last 8-K filed announcing White Lion deal it didn't change in 15 days vs. previous one reported in the last 10Q, so it looks like the dilution generated by the conversion of notes is already finished as it also looks like in L2 with the MMs present and the type trading in the last days:

(2,593,435,051 - 2,290,449,898) / 2,290,449,898 = 13.2%

Prove that what I said is completely false or untrue. I mean what I said, not the fabricated version of what I said. I didn't say every sh**ty (word used by poster I'm replying to, that can be seen in his post) company or every company needs dilutipn. Don't change what I said and don't use sentences out of context.

Excellent post as usual!!! Thanks my friend!!!

Thanks Capitalvaluetrade for your comments, In the following link you can find the new version of my analysis in case you haven't seen it:

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=156918633

Fortunately that doesn't change at all my opinion of this deal being excellent and much better than Andrew Garnock's. Almost everything is unchanged from previous analysis. Is not that I admitted that I misunderstood the filing as Okavango is trying to make it look like, I just misunderstood one specific point of the filing at the beginning and corrected it.

Prove it

Prove it is not real. More misinformation?

Where are the facts? And the answer to my questions?

Where is it?

LOL, really? VRUS is a scam and all are aware.

it's even right there in some of the links you provide..

You think the math is incorrect? Please enlighten us, where is it wrong? Obviously VRUS dilution is based on VRUS OS. Aren't we talking about VRUS? Isn't this VRUS board where you spend hours and hours I don't know why. With you logic Apple is a terible company becuase they have 4.33B OS almost double VRUS has. Enlighten us with the definition of normal amount of shares.

Dilution is not good. Period.

The terms are still toxic and not good. Period.

Using fuzzy math on the numbers without using logic does not make it a fact.

I and others have provided the WELL KNOWN AND OBTAINABLE FACTS many times over, so I do not need to spoon feed anymore.

Please tell me why I am incorrect and either don't want others to see truth or don't understand what you mean. I just want facts like I'm giving them.