Saturday, August 15, 2020 2:30:18 PM

Thoth, welcome back, great to have you here with us. I agree with all you mention in your post. I think shortly after Garnock is finished selling (I think we are almost there or already there) we are going to move up very fast as we did when Garnock came in (10 times or more in share price).

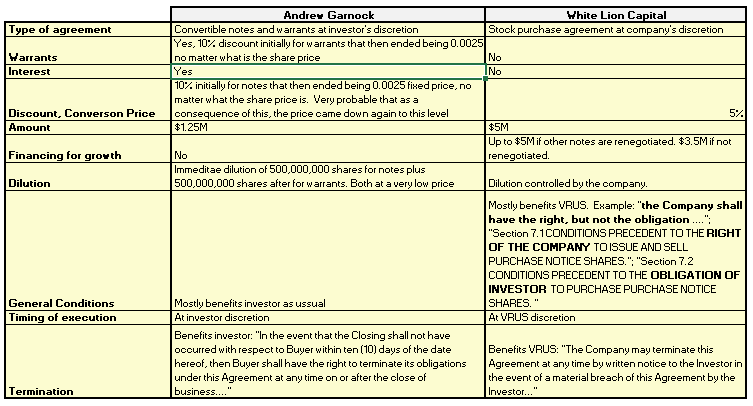

Following is my analysis of the agreement reached with White Lion as compared to Andrew Garnock's. I think most people don’t understand the great deal White Lion is for VRUS and why this is a much better agreement for the company and shareholders than Andrew Garnock’s.

The following table summarizes main the differences and all without exception are advantages of the new White Lion deal vs. Andrew Garnock’s.

One of the most important advantages for me vs. A. Garnock's deal is that discount with White Lion is only 5% vs. 10% and that the company is the one that decides when to convert or sell, not the investor. And very important to take into account that because of not financing for growth through Garnock's agreement, the company ended having to take the additional notes that then converted. I think Anshu learned from his mistake and now reached an agreement that left most of the financing for growth in case he doesn’t get commercial lending soon.

This new financing is a novel system that fully aligns investor to company interests. Because of the small discount of 5% investor has real benefits ONLY by the combined exponential effect of the two factors: high share price times big increase in share price. So for him as for the company is much better to buy the majority of shares at the higher price possible (higher base) and keep them as long as possible (higher increase in price).

Toxic finance discounts on the other hand are huge (around 50% to 60%), so there is where lenders make the money. That's why they start to dump shares as soon as they can and also because they know that as they dump, the share price starts to collapse and they lose their benefit or part of it if they wait.

For both, investor and company is not favorable to execute all the deal at this prices, but higher.I guess the company will execute at this level for any emergenciers and live the majority for much higher prices. Fortunatelly is at their discretion and not at the investor's discretion.

Additionally, as part of the agreement, there are limitations for the investor and for VRUS that represent benefits for shareholders. Examples of these are no dilution permitted for other deals and no short sales allowed. Also, as expressed all along the 8-K, White Lion has developed an extensive due diligence to VRUS and found it adequate to sign an agreement by which they have the obligation and the VRUS has the benefit of the $5M funds if they want to use it.

Link to 8-K:

https://www.otcmarkets.com/filing/html?id=14257168&guid=yK_6UnZYzV0m0yh

Following is my analysis of the agreement reached with White Lion as compared to Andrew Garnock's. I think most people don’t understand the great deal White Lion is for VRUS and why this is a much better agreement for the company and shareholders than Andrew Garnock’s.

The following table summarizes main the differences and all without exception are advantages of the new White Lion deal vs. Andrew Garnock’s.

One of the most important advantages for me vs. A. Garnock's deal is that discount with White Lion is only 5% vs. 10% and that the company is the one that decides when to convert or sell, not the investor. And very important to take into account that because of not financing for growth through Garnock's agreement, the company ended having to take the additional notes that then converted. I think Anshu learned from his mistake and now reached an agreement that left most of the financing for growth in case he doesn’t get commercial lending soon.

This new financing is a novel system that fully aligns investor to company interests. Because of the small discount of 5% investor has real benefits ONLY by the combined exponential effect of the two factors: high share price times big increase in share price. So for him as for the company is much better to buy the majority of shares at the higher price possible (higher base) and keep them as long as possible (higher increase in price).

Toxic finance discounts on the other hand are huge (around 50% to 60%), so there is where lenders make the money. That's why they start to dump shares as soon as they can and also because they know that as they dump, the share price starts to collapse and they lose their benefit or part of it if they wait.

For both, investor and company is not favorable to execute all the deal at this prices, but higher.I guess the company will execute at this level for any emergenciers and live the majority for much higher prices. Fortunatelly is at their discretion and not at the investor's discretion.

Additionally, as part of the agreement, there are limitations for the investor and for VRUS that represent benefits for shareholders. Examples of these are no dilution permitted for other deals and no short sales allowed. Also, as expressed all along the 8-K, White Lion has developed an extensive due diligence to VRUS and found it adequate to sign an agreement by which they have the obligation and the VRUS has the benefit of the $5M funds if they want to use it.

Link to 8-K:

https://www.otcmarkets.com/filing/html?id=14257168&guid=yK_6UnZYzV0m0yh