Wednesday, July 15, 2020 10:22:47 AM

On the other hand, as shown below, last year the price started to increase and multiplied by around 20 times in 6 months when the new notes and warrants to replace the previous notes were announced:

I think the story is going to repeat and now with a much higher price increase than 20 times, because the company has a much bigger business (when previous agreement was done, the company only had the GCC business) and much higher Revenue (last Q Revenue $4.647 million during Covid and $6.173 million pre Covid and last Q Revenue reported when previous agreement announced was only $1.371 million). Additionally, now the funding is not only for paying notes but mainly for growth.

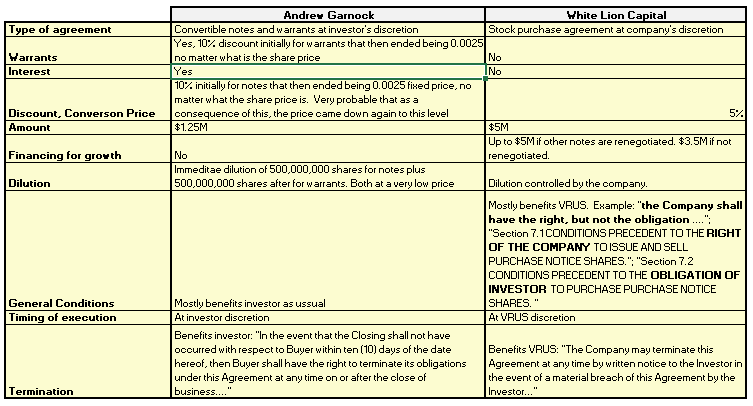

Because of not financing for growth through Garnock and Berdon agreements, the company ended having to take the notes that converted. I think Anshu learned from his mistake and now reached an agreement that left money for growth in case he doesn’t get commercial lending soon.

This new financing is a novel system that fully aligns investor and company . Contrary to toxic financing, both parties maximize benefits ONLY if price goes up as I’m going to explain. There is a limitation in the amount of financing of $5M and in the number of shares that the investor can have at any time of 4.9% of outstanding shares.

From company’s point of view, if share price goes up, less shares have to be issued to get the $5M in finance.

From the investor’s point of view, they have a limited number of shares that they can buy at each point in time, that is the smaller between:

- The number of such shares that, when aggregated with all other shares of Common Stock then owned by the Investor, would result in the Investor owning the Beneficial Ownership Limitation of 4.9% of the then outstanding shares

- 250% of the average daily trading volume in the 5 business days previous to the purchase notice.

So, the way to maximize the benefit for the investor is if they buy not at this share prices but much higher and with higher percentage increase in price.

Examples using just a 50% increase in price;

100,000,000 shares X 0.003 x 50% increase= $150,000

100,000,000 shares X 0.03 x 50% increase = $1,500,000

And if the percentage is more than 50%, benefit for investor will be much higher:

100,000,000 shares X 0.03 x 500% increase = $15,000,000

So, since the discount on the shares is only 5% of the share price, the ONLY way to maximize investor's benefit is by the exponential effect of the combination of two factors: share price times increase in share price. And that makes benefit explode.

Toxic finance discounts on the other hand are huge (around 50% to 60%), so there is where lenders make the money. That's why they start to dump shares as soon as they can and also because they know that as they dump, the share price starts to collapse and they lose their benefit or part of it if they wait.

For both, investor and company is not favorable to execute all the deal at this prices, but higher.

Additionally, as part of the agreement, there are limitations for the investor and for VRUS that represent benefits for shareholders. Examples of these are no dilution permitted for other deals and no short sales allowed, so guess what will happen with OS and share price. Also, as expressed all along the 8-K, White Lion has developed an extensive due diligence to VRUS and found it adequate to sign an agreement by which they have the obligation and the VRUS has the benefit if they want to use it of the $5M funds.

If Anshu can negotiate the extension of the existing notes supported on this agreement, it would be much better, because he will be able to use all of the $5M for growth and also he will be able to use it at much higher share prices.

You don’t have to believe me blindly. I'm a more than 3 years loyal shareholder, so I know what I own. Your own Due Diligence is your best weapon. It's all in the 8-K filing.

VHAI - Vocodia Partners with Leading Political Super PACs to Revolutionize Fundraising Efforts • VHAI • Sep 19, 2024 11:48 AM

Dear Cashmere Group Holding Co. AKA Swifty Global Signs Binding Letter of Intent to be Acquired by Signing Day Sports • DRCR • Sep 19, 2024 10:26 AM

HealthLynked Launches Virtual Urgent Care Through Partnership with Lyric Health. • HLYK • Sep 19, 2024 8:00 AM

Element79 Gold Corp. Appoints Kevin Arias as Advisor to the Board of Directors, Strengthening Strategic Leadership • ELMGF • Sep 18, 2024 10:29 AM

Mawson Finland Limited Further Expands the Known Mineralized Zones at Rajapalot: Palokas step-out drills 7 metres @ 9.1 g/t gold & 706 ppm cobalt • MFL • Sep 17, 2024 9:02 AM

PickleJar Announces Integration With OptCulture to Deliver Holistic Fan Experiences at Venue Point of Sale • PKLE • Sep 17, 2024 8:00 AM