News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Seeking Creative & Innovative Investment Ideas...

EDWARD STEVENSON

![]()

Seeking Creative & Innovative Investment Ideas...

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Seeking Creative & Innovative Investment Ideas...

Housing Is Bottoming, But Wait for the Breakout in Homebuilders.

by: Cam Hui August 30, 2009

Bloomberg recent reported that Homebuilders are buying land after years of inventory cuts. Coupled with a buoyant new home sales report, some investors have concluded that housing has bottomed and is poised to rebound.

Wait for the relative breakout

The chart below shows the S&P 500 Homebuilders Index relative to the S&P 500. Relative to the S&P 500, the Homebuilding group is currently undergoing a basing process but calls for an upturn may be premature. Technically, the group needs to break out of its relative trading before we can definitely call for a recovery.

My gut feel tells me that sentiment isn’t quite washed out for an upturn. We need a magazine cover style capitulation, or for the popular media to really jump on the story. Here is an example from Britain’s housing bust from the 1980s:

http://www.youtube.com/v/azxNL-T3IFQ&hl=en&fs=1

Bottoms are a process

This form of relative analysis isn't new. I posted on the bottoming process undergone by the group last August and again in January. I suggest that investors shouldn’t get overly enthusiastic in anticipation of a rebound. We need to watch and wait for the relative breakout before sounding the all-clear.

Stock Market Overbought: What This Means for Silver and Gold.

by: Przemyslaw Radomski August 31, 2009 | about: DIA / GDX / GLD / HUI / SLV / SPY / UDN / UUP

This essay is based on the Premium Update posted August 29th, 2009

I have to confess to a love affair that goes back a long ways with that exciting, hyper-volatile metal-- silver.

This week The Wall Street Journal reported that silver has enjoyed greater price gains than gold so far in 2009. The Journal noted that silver often follows gold, although sometimes with greater moves since it is a less-active market and thus more prone to volatile price swings. Naturally, silver’s stillness is limited to many consolidation periods, and to the early parts of a particular upleg. When silver finally does move near the end of a rally, the move is likely to be substantial. So far in 2009, December silver futures have risen 26%, while December gold is up 6%, the Journal reported.

Knowing about the relationship between silver and gold can mean large profits at the right time, so I would like to revisit this topic.

Silver, sometimes referred to as "poor man's gold," is often bought alongside gold as a hedge against dollar weakness, inflation fears and geopolitical turbulence. But silver also has a more significant role as an industrial metal because of its application in batteries, cell phones, computers, TV’s, refrigerators, medical applications, satellites, weapons systems, electrical wiring applications, etc. In the majority of cases this silver is never recovered. Once it’s used up, it’s used up.

As mentioned earlier, the rule of thumb is that generally silver initially lags behind gold, but as gold gathers steam, speculators flock to silver and ignite the sharp moves higher for which this fidgety metal is so famous. We can also expect silver to drop faster than gold during a recession. We saw that in the recent stock panic when gold was fairly resilient while silver nose-dived. The yellow metal hit a 14-month low at its worst, while silver spiraled down to a 34-month low.

Today there is a confluence of factors on the demand side for silver: Investment demand, industrial demand and the fear factor due to the economic situation which has not yet resolved itself. We also need to keep in mind that we have another factor, one I touched on last week-- almost 2 billion new consumers in China and India who are moving into middle class status and are acquiring a taste for gadgets. Gadgets require silver. In other words, there is a growing demand for silver as an industrial metal and as an investment vehicle while the supply continues to dwindle.

Looking back at history we learn the lesson that we can expect silver to drop faster than gold during a recession, and silver to rise faster than gold during a bull market in the metals.

A simple application of this observation is to trade silver for gold in the middle of a recession, when a bull market in gold and silver is about to start, and to trade gold for silver at the top of a bull market in precious metals.

Today’s ratio of gold to silver is 64.6 ounces of silver equal the value of one ounce of gold. With gold today at $956, and a normal, historical 12 silver to gold ratio, (referring to its occurrence in nature, and ratio’s value through centuries) silver should be trading near $80.This is about 400% higher than it was trading for this week. So, if the price of silver gravitates to its historic ratio, we can bank on some nice profits. It’s impossible to tell the exact date when this would take place, but I expect the ratio to go much below its historical average of 12, most likely in a few years.

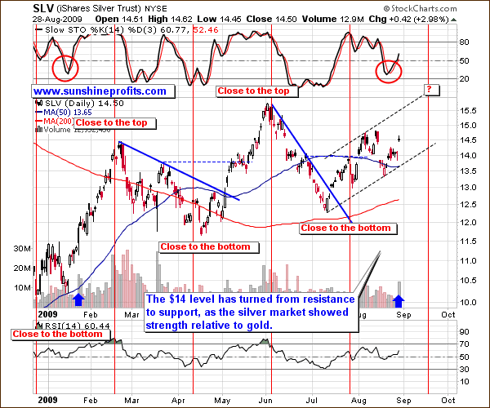

Since we’re already on the subject let’s begin with analysis of the silver chart.

As far as timing the silver market is concerned, the similarity is still intact between the two time frames that I mentioned in the previous Premium Update. The situation developed as I expected and we saw higher silver values this week. Not only did silver manage to stay above the long-term support lines, but it was also able to once again move above the short-term one. Moreover, this move (which took place on Friday, August 28th) materialized on high volume (as marked with the blue arrow on the chart above), which serves as a confirmation of the bullish signal.

The bottom in silver was accompanied by a buy signal from the Stochastic Indicator, which was also the case at the end of January 2009. Back then a relatively large rally followed, so this may also be the case here. Naturally, we may need to wait for additional few days of prices closing above the 14.5 level in order to confirm the move, but given the size of the volume on Friday, I think it is likely that we will move higher from here.

The analysis of the medium-term chart emphasizes the size of the volume of Friday’s session. Combining this bullish signal with the cycle analysis that I’ve featured suggests that higher prices are to be expected from here – with a local top several weeks away.

General Stock Market

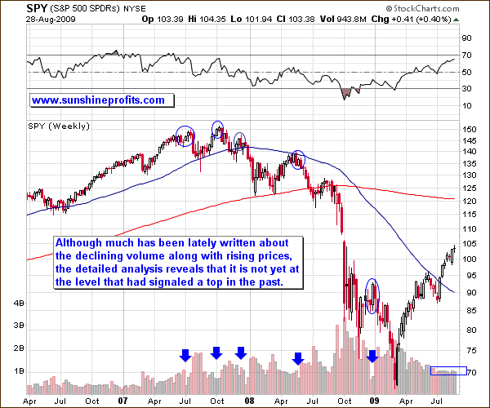

For a considerable amount of time the main stock indices have been rising on a declining volume. Such a divergence usually suggests that the rise is only temporary and that the true price direction is down. Whereas this could be the case here, I would like to point your attention to the fact that the level of volume we are seeing is not yet screaming “sell”.

Since it is the long-term tendency that is the subject of this analysis, I have used the weekly chart that filters out the daily noise. The weekly SPY ETF chart makes it easy to compare the volume that accompanied previous tops to the volume in the previous weeks.

Please note that past tops were mostly accompanied by volume that was visibly lower than what we have seen in the past several weeks, so we may indeed move even higher (The next Fibonacci resistance level is just below 110, which is also close to the upper border of the price gap - 108.02, which formed in early October 2008) before correcting.

Summary

This week the precious metals sector moved higher; silver rallied on strong volume, which may mark a beginning of a new substantial upleg. Gold is currently in a cloudy technical situation, and much depends on what happens in other markets.

The value of the main stock indices is naturally an important factor as well, especially for PM stocks and silver, due to its many industrial uses. For now the general stock market is overbought, and it moves higher on a declining volume, but the size of the volume is not yet very low, so it would not surprise me to see even more strength in DJIA and S&P 500 before they make a move lower. It’s too early to say whether such a move would drag PMs down along with them. Additional signals come from our indicators and from the analysis of other markets, but I will leave that part of the commentary to subscribers.

Stock Market Overbought: What This Means for Silver and Gold.

by: Przemyslaw Radomski August 31, 2009 | about: DIA / GDX / GLD / HUI / SLV / SPY / UDN / UUP

This essay is based on the Premium Update posted August 29th, 2009

I have to confess to a love affair that goes back a long ways with that exciting, hyper-volatile metal-- silver.

This week The Wall Street Journal reported that silver has enjoyed greater price gains than gold so far in 2009. The Journal noted that silver often follows gold, although sometimes with greater moves since it is a less-active market and thus more prone to volatile price swings. Naturally, silver’s stillness is limited to many consolidation periods, and to the early parts of a particular upleg. When silver finally does move near the end of a rally, the move is likely to be substantial. So far in 2009, December silver futures have risen 26%, while December gold is up 6%, the Journal reported.

Knowing about the relationship between silver and gold can mean large profits at the right time, so I would like to revisit this topic.

Silver, sometimes referred to as "poor man's gold," is often bought alongside gold as a hedge against dollar weakness, inflation fears and geopolitical turbulence. But silver also has a more significant role as an industrial metal because of its application in batteries, cell phones, computers, TV’s, refrigerators, medical applications, satellites, weapons systems, electrical wiring applications, etc. In the majority of cases this silver is never recovered. Once it’s used up, it’s used up.

As mentioned earlier, the rule of thumb is that generally silver initially lags behind gold, but as gold gathers steam, speculators flock to silver and ignite the sharp moves higher for which this fidgety metal is so famous. We can also expect silver to drop faster than gold during a recession. We saw that in the recent stock panic when gold was fairly resilient while silver nose-dived. The yellow metal hit a 14-month low at its worst, while silver spiraled down to a 34-month low.

Today there is a confluence of factors on the demand side for silver: Investment demand, industrial demand and the fear factor due to the economic situation which has not yet resolved itself. We also need to keep in mind that we have another factor, one I touched on last week-- almost 2 billion new consumers in China and India who are moving into middle class status and are acquiring a taste for gadgets. Gadgets require silver. In other words, there is a growing demand for silver as an industrial metal and as an investment vehicle while the supply continues to dwindle.

Looking back at history we learn the lesson that we can expect silver to drop faster than gold during a recession, and silver to rise faster than gold during a bull market in the metals.

A simple application of this observation is to trade silver for gold in the middle of a recession, when a bull market in gold and silver is about to start, and to trade gold for silver at the top of a bull market in precious metals.

Today’s ratio of gold to silver is 64.6 ounces of silver equal the value of one ounce of gold. With gold today at $956, and a normal, historical 12 silver to gold ratio, (referring to its occurrence in nature, and ratio’s value through centuries) silver should be trading near $80.This is about 400% higher than it was trading for this week. So, if the price of silver gravitates to its historic ratio, we can bank on some nice profits. It’s impossible to tell the exact date when this would take place, but I expect the ratio to go much below its historical average of 12, most likely in a few years.

Since we’re already on the subject let’s begin with analysis of the silver chart.

As far as timing the silver market is concerned, the similarity is still intact between the two time frames that I mentioned in the previous Premium Update. The situation developed as I expected and we saw higher silver values this week. Not only did silver manage to stay above the long-term support lines, but it was also able to once again move above the short-term one. Moreover, this move (which took place on Friday, August 28th) materialized on high volume (as marked with the blue arrow on the chart above), which serves as a confirmation of the bullish signal.

The bottom in silver was accompanied by a buy signal from the Stochastic Indicator, which was also the case at the end of January 2009. Back then a relatively large rally followed, so this may also be the case here. Naturally, we may need to wait for additional few days of prices closing above the 14.5 level in order to confirm the move, but given the size of the volume on Friday, I think it is likely that we will move higher from here.

The analysis of the medium-term chart emphasizes the size of the volume of Friday’s session. Combining this bullish signal with the cycle analysis that I’ve featured suggests that higher prices are to be expected from here – with a local top several weeks away.

General Stock Market

For a considerable amount of time the main stock indices have been rising on a declining volume. Such a divergence usually suggests that the rise is only temporary and that the true price direction is down. Whereas this could be the case here, I would like to point your attention to the fact that the level of volume we are seeing is not yet screaming “sell”.

Since it is the long-term tendency that is the subject of this analysis, I have used the weekly chart that filters out the daily noise. The weekly SPY ETF chart makes it easy to compare the volume that accompanied previous tops to the volume in the previous weeks.

Please note that past tops were mostly accompanied by volume that was visibly lower than what we have seen in the past several weeks, so we may indeed move even higher (The next Fibonacci resistance level is just below 110, which is also close to the upper border of the price gap - 108.02, which formed in early October 2008) before correcting.

Summary

This week the precious metals sector moved higher; silver rallied on strong volume, which may mark a beginning of a new substantial upleg. Gold is currently in a cloudy technical situation, and much depends on what happens in other markets.

The value of the main stock indices is naturally an important factor as well, especially for PM stocks and silver, due to its many industrial uses. For now the general stock market is overbought, and it moves higher on a declining volume, but the size of the volume is not yet very low, so it would not surprise me to see even more strength in DJIA and S&P 500 before they make a move lower. It’s too early to say whether such a move would drag PMs down along with them. Additional signals come from our indicators and from the analysis of other markets, but I will leave that part of the commentary to subscribers.

Port Hope will yield Wireless Age Communications, Inc. $2,000,000 in net income...if the Connecticut project involves half a dozen of these facilities dispersed across the state, assuming they derive similar margins and are no greater in size, the EPS exceeds $0.40 per share, once the share cancellation takes effect. These type of numbers would have a huge impact on meeting qualification for listing on a higher exchange and price per share altogether.

Remember multi-billion dollar enterprises and hopeful Resource Recovery Facilities (RRF) business partnering with Wireless Age Communications, Inc. wouldn't pursue projects without a large ROI.

Indeed, nice price action early into Monday's trading session.

Interesting, I will glance momentarily.

The pinksheet markets are volatile and stand to lose and gain price during the course of each and every trading session. "Timing is everything" is a good way to model a successful career in every market tier. Notice I commented on Quasar on the 17th of August when it was trading in the low $0.03s. On the 24th it peaked at $0.043; $0.044 on the 25th. As far as I am concerned, a 37.5% gain is very reasonable.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=40593183

Judging by your experience in the penny market, I'd suggest you attain a better understanding of distinguishing "investing" from "trading". Enough with the whiny posts.

You're welcome mgland, I'm glad to hear you found it useful.

Thank you. I'm looking for strong price action this week myself.

I would add WLSA to that list...

Authorized: 110,000,000.

Issued and Outstanding: 61,261,592.

Float (free trading): approx. 20,000,000.

SRSR ~ technical analysis in video format 08.28.09.

A reversal in trend similar to early August may be on the horizon following a downtrend reversal signal and confirmation coming off of Friday's trading session. My thoughts and analysis in video format follow.

Link to video chart: http://timelesswealth.net/srsr2.html

Technical analysis in video format 08.28.09.

A reversal in trend similar to early August may be on the horizon following a downtrend reversal signal and confirmation coming off of Friday's trading session. My thoughts and analysis in video format follow.

Link to video chart: http://timelesswealth.net/srsr2.html

SRSR ~ technical analysis in video format 08.28.09.

A reversal in trend similar to early August may be on the horizon following a downtrend reversal signal and confirmation coming off of Friday's trading session. My thoughts and analysis in video format follow.

Link to video chart: http://timelesswealth.net/srsr2.html

The Edward Stevenson Report: Watchlist 08.25.09

DNN

HIMX

JASO

TAMB

QUIX

WTU

HMPR

ADL

QASP

WLSA

The Edward Stevenson Report: Watchlist 08.25.09

DNN

HIMX

JASO

TAMB

QUIX

WTU

HMPR

ADL

QASP

WLSA

WLSA: Director, Approvals and Regulatory Affairs, Stein Lal, Sunbay Energy Corp.

http://www.sunbayenergy.com/about_us_management.php

Lal, former Deputy Minister of the Environment for Ontario, occupies a fundamental role ensuring grants and approvals are received in a timely manner. The development of renewable energy solutions is extensively encouraged by the recent Green Energy Act of Ontario as well as numerous as other initiatives across North America.

http://www.greenenergyact.ca/Page.asp?PageID=924&ContentID=1114

In 2001, Stein Lal retired as Deputy Minister of the Environment, after having served for over a decade. His professional background is in law.

Communications Forum

Perspectives on the Environment

March 28 2002

STEIN LAL, EX-DM MOE, ON GOVERNMENT

Stien Lal joined the public service of Ontario in 1988 as the Deputy Minister in the Ministry of the Solicitor General and since then has held that position in five other ministries retiring from the public service 2001 as the Deputy Minister of the Ministry of the Environment. During this period, Ontario under went unprecedented political change. As a result, Stien Lal has served in the capacity of Deputy Minister under all three governments. He now heads a consulting practice at the national and international level. Stien is a lawyer by profession, having been first called to the bar in England and subsequently in five other jurisdictions in Canada and abroad. He was appointed a Queen's Counsel in 1983.

Notes

Having worked in six ministries in Ontario, he has had the unique opportunity of seeing and appreciating some of the subtle and sometimes not so subtle differences between them. The OPS has its own culture and each Ministry has its own culture driven sometimes by the nature of their business, sometimes by their mandate or whether they are a regulatory or a non-regulatory Ministry...continued.

http://sustainabilitynetwork.ca/Events/Breakfasts/03282002A.htm

Lal involved himself in a environmental research group promoting education of the subject.

Pollution Probe is a Canadian charitable environmental organization that:

Defines environmental problems through research;

Promotes understanding through education; and,

Presses for practical solutions through advocacy.

Pollution Probe is dedicated to achieving positive and tangible environmental change.

The McLal Group Inc.

Stein Lal

Email: stindarlal@rogers.com

http://www.pollutionprobe.org/managing.shared.waters/organizationlist.pdf

National Environmental Law Section: A Return to Environmental Regulation? Another publication that lists Lal's involvement in Environmental movements.

National Environmental Law Section: A Return to Environmental Regulation?

During Deputy Minister Stein Lal’s visit to the

Ontario Section Executive meeting, we received

welcome assurances, particularly regarding the

improvement of lines of communication. One

of our Branch’s goals will be to pursue efforts to

improve communication. We are once again

hopeful that we can finally address this

longstanding concern on the part of the

environmental Bar in Ontario. http://dev.cba.org/cba/Sections/ELS/Eco_Bulletin/ecobul_99-12.pdf

Stein Lal is documented in numerous sources sharing a valued opinion on a study, conference, or involving himself in a beneficial organization.

The Associations of Municipalities of Ontario appointed Stein Lal to the Waste Diversion Organization. Lal promptly translates the experience to communications between Sunbay Energy Corp., and Turtle Island Recycling, a principle supplier of feedstock. His understanding of the waste management industry is key to partnerships continent-wide.

Associations of Municipalities of Ontario.

December 1, 1999 - FYI 99/015

AMO Confirms Appointees to the Waste Diversion Organization

Issue: The Board of Directors for the New Waste Diversion Organization (WDO) will undertake program design for waste diversion initiatives for the next year and prepare a longer term plan.

Facts:

AMO, along with the Ministry of the Environment, the Recycling Council of Ontario and various industry groups signed a Memorandum of Understanding (MOU) that establishes and sets out the structure and function of the new WDO.

AMO's representatives to the Board of Directors of the WDO are:

Terry Cassidy, Councillor, City of Quinte West, and Chair, Centre and South Hastings Waste Services Board

Joan King, Councillor, City of Toronto, AMO Vice-President, and Chair, AMO's Recycling Task Force

John Jardine, Commissioner of Environmental Services and City Engineer, City of London with corporate responsibility for waste diversion services and involvement in the London-Middlesex Waste Management Planning Study

Peter Partington, Councillor, Region of Niagara, AMO Board of Directors, and Chair, Niagara Region Corporate and Financial Service Committee.

Each municipal representative offers the necessary knowledge and skills to effectively represent the municipal sector, and they will be supported by a technical advisory group that will draw upon municipal staff experts from across the Province.

Other members of the WDO Board of Directors include:

John Hanson, Executive Director, Recycling Council of Ontario

Andy Brandt, Chair and CEO, Liquor Control Board of Ontario

Ron Hoare, VP Corporate Development, Para Paints

John Honderich, Publisher, Toronto Star Newspapers Ltd

Anthony Eames, President and CEO, Coca-Cola Ltd.

Bill McEwan, President and Chief Merchandising Officer, The Great Atlantic and Pacific Company of Canada

William Apted, President, Crown Cork and Seal Canada Inc.

Peter Elwood, President, Lipton

Stein Lal, Deputy Minister, Ministry of the Environment (non-voting status)

Corporations Supporting Recycling (CSR) is providing the administrative support for the WDO during the one-year term of the organization. CSR's address is 26 Wellington Street East, Suite 601, Toronto, M5E 1S2. http://www.amo.on.ca/AM/Template.cfm?Section=19995&TEMPLATE=/CM/ContentDisplay.cfm&CONTENTID=40663

The Ontario Public Service Employees Union facilitated a study in which Stein Lal took part in. The submission was titled, "Public Interests in Water Facilities Operations".

A Submission to the Walkerton Inquiry: Public Interests in Water Facilities Operations.

July 2001

25. Currently, the MOU names various senior public service employees as the Board Members though

there is no need, either in legislation or Management Board Directives, that the Board be drawn

exclusively from the public service. As of March 1, 2000, the Board consisted of:

John Fleming, Deputy Minister, Ministry of Correctional Services;

Stein Lal, Deputy Minister, Ministry of the Environment;

Donald Obonsawin, Deputy Minister, Ministry of Tourism;

Tony Salerno, Vice-Chair and CEO, Ontario Financing Authority;

Ron Vrancart, Deputy Minister, Ministry of Natural Resources. https://ozone.scholarsportal.info/bitstream/1873/8308/1/10295805.pdf

Sunbay Speakers Series is a program that Sunbay Energy Corp. put together in the discussion and introduction of their plasma gasification project in Port Hope, Ontario. Several newspapers documented Stein Lal as a guest speaker of this program.

Sunbay Energy presented guest speaker Stein Lal, former Deputy Minister of the Environment, in their first of a series at their Info centre on Walton St. Mr. Lal hosted a discussion of The Kyoto Protocol, Carbon Emissions and where Ontario fits in. Jordan Oxley, President of Sunbay Energy, completed the evening with a Q & A session and an update on project plans for the Port Hope Gasification Plant. A very informative evening! For more info drop into the Sunbay Info Ctr at 35 Walton St., Port Hope or call 905-885-0050.

http://www.snapnorthumberland.com/?option=com_sngevents&id%5b%5d=78666

Mr. Stein Lal, former Deputy Minister of the Environment reserves an important role in guiding Sunbay Energy Corp., along the path to success. His thoroughness in law and connections to decisive parties in government will be advantageous to the development of Sunbay's projects as renewable energy solutions.

WLSA: Director, Approvals and Regulatory Affairs, Stein Lal, Sunbay Energy Corp.

http://www.sunbayenergy.com/about_us_management.php

Lal, former Deputy Minister of the Environment for Ontario, occupies a fundamental role ensuring grants and approvals are received in a timely manner. The development of renewable energy solutions is extensively encouraged by the recent Green Energy Act of Ontario as well as numerous as other initiatives across North America.

http://www.greenenergyact.ca/Page.asp?PageID=924&ContentID=1114

In 2001, Stein Lal retired as Deputy Minister of the Environment, after having served for over a decade. His professional background is in law.

Communications Forum

Perspectives on the Environment

March 28 2002

STEIN LAL, EX-DM MOE, ON GOVERNMENT

Stien Lal joined the public service of Ontario in 1988 as the Deputy Minister in the Ministry of the Solicitor General and since then has held that position in five other ministries retiring from the public service 2001 as the Deputy Minister of the Ministry of the Environment. During this period, Ontario under went unprecedented political change. As a result, Stien Lal has served in the capacity of Deputy Minister under all three governments. He now heads a consulting practice at the national and international level. Stien is a lawyer by profession, having been first called to the bar in England and subsequently in five other jurisdictions in Canada and abroad. He was appointed a Queen's Counsel in 1983.

Notes

Having worked in six ministries in Ontario, he has had the unique opportunity of seeing and appreciating some of the subtle and sometimes not so subtle differences between them. The OPS has its own culture and each Ministry has its own culture driven sometimes by the nature of their business, sometimes by their mandate or whether they are a regulatory or a non-regulatory Ministry...continued.

http://sustainabilitynetwork.ca/Events/Breakfasts/03282002A.htm

Lal involved himself in a environmental research group promoting education of the subject.

Pollution Probe is a Canadian charitable environmental organization that:

Defines environmental problems through research;

Promotes understanding through education; and,

Presses for practical solutions through advocacy.

Pollution Probe is dedicated to achieving positive and tangible environmental change.

The McLal Group Inc.

Stein Lal

Email: stindarlal@rogers.com

http://www.pollutionprobe.org/managing.shared.waters/organizationlist.pdf

National Environmental Law Section: A Return to Environmental Regulation? Another publication that lists Lal's involvement in Environmental movements.

National Environmental Law Section: A Return to Environmental Regulation?

During Deputy Minister Stein Lal’s visit to the

Ontario Section Executive meeting, we received

welcome assurances, particularly regarding the

improvement of lines of communication. One

of our Branch’s goals will be to pursue efforts to

improve communication. We are once again

hopeful that we can finally address this

longstanding concern on the part of the

environmental Bar in Ontario. http://dev.cba.org/cba/Sections/ELS/Eco_Bulletin/ecobul_99-12.pdf

Stein Lal is documented in numerous sources sharing a valued opinion on a study, conference, or involving himself in a beneficial organization.

The Associations of Municipalities of Ontario appointed Stein Lal to the Waste Diversion Organization. Lal promptly translates the experience to communications between Sunbay Energy Corp., and Turtle Island Recycling, a principle supplier of feedstock. His understanding of the waste management industry is key to partnerships continent-wide.

Associations of Municipalities of Ontario.

December 1, 1999 - FYI 99/015

AMO Confirms Appointees to the Waste Diversion Organization

Issue: The Board of Directors for the New Waste Diversion Organization (WDO) will undertake program design for waste diversion initiatives for the next year and prepare a longer term plan.

Facts:

AMO, along with the Ministry of the Environment, the Recycling Council of Ontario and various industry groups signed a Memorandum of Understanding (MOU) that establishes and sets out the structure and function of the new WDO.

AMO's representatives to the Board of Directors of the WDO are:

Terry Cassidy, Councillor, City of Quinte West, and Chair, Centre and South Hastings Waste Services Board

Joan King, Councillor, City of Toronto, AMO Vice-President, and Chair, AMO's Recycling Task Force

John Jardine, Commissioner of Environmental Services and City Engineer, City of London with corporate responsibility for waste diversion services and involvement in the London-Middlesex Waste Management Planning Study

Peter Partington, Councillor, Region of Niagara, AMO Board of Directors, and Chair, Niagara Region Corporate and Financial Service Committee.

Each municipal representative offers the necessary knowledge and skills to effectively represent the municipal sector, and they will be supported by a technical advisory group that will draw upon municipal staff experts from across the Province.

Other members of the WDO Board of Directors include:

John Hanson, Executive Director, Recycling Council of Ontario

Andy Brandt, Chair and CEO, Liquor Control Board of Ontario

Ron Hoare, VP Corporate Development, Para Paints

John Honderich, Publisher, Toronto Star Newspapers Ltd

Anthony Eames, President and CEO, Coca-Cola Ltd.

Bill McEwan, President and Chief Merchandising Officer, The Great Atlantic and Pacific Company of Canada

William Apted, President, Crown Cork and Seal Canada Inc.

Peter Elwood, President, Lipton

Stein Lal, Deputy Minister, Ministry of the Environment (non-voting status)

Corporations Supporting Recycling (CSR) is providing the administrative support for the WDO during the one-year term of the organization. CSR's address is 26 Wellington Street East, Suite 601, Toronto, M5E 1S2. http://www.amo.on.ca/AM/Template.cfm?Section=19995&TEMPLATE=/CM/ContentDisplay.cfm&CONTENTID=40663

The Ontario Public Service Employees Union facilitated a study in which Stein Lal took part in. The submission was titled, "Public Interests in Water Facilities Operations".

A Submission to the Walkerton Inquiry: Public Interests in Water Facilities Operations.

July 2001

25. Currently, the MOU names various senior public service employees as the Board Members though

there is no need, either in legislation or Management Board Directives, that the Board be drawn

exclusively from the public service. As of March 1, 2000, the Board consisted of:

John Fleming, Deputy Minister, Ministry of Correctional Services;

Stein Lal, Deputy Minister, Ministry of the Environment;

Donald Obonsawin, Deputy Minister, Ministry of Tourism;

Tony Salerno, Vice-Chair and CEO, Ontario Financing Authority;

Ron Vrancart, Deputy Minister, Ministry of Natural Resources. https://ozone.scholarsportal.info/bitstream/1873/8308/1/10295805.pdf

Sunbay Speakers Series is a program that Sunbay Energy Corp. put together in the discussion and introduction of their plasma gasification project in Port Hope, Ontario. Several newspapers documented Stein Lal as a guest speaker of this program.

Sunbay Energy presented guest speaker Stein Lal, former Deputy Minister of the Environment, in their first of a series at their Info centre on Walton St. Mr. Lal hosted a discussion of The Kyoto Protocol, Carbon Emissions and where Ontario fits in. Jordan Oxley, President of Sunbay Energy, completed the evening with a Q & A session and an update on project plans for the Port Hope Gasification Plant. A very informative evening! For more info drop into the Sunbay Info Ctr at 35 Walton St., Port Hope or call 905-885-0050.

http://www.snapnorthumberland.com/?option=com_sngevents&id%5b%5d=78666

Mr. Stein Lal, former Deputy Minister of the Environment reserves an important role in guiding Sunbay Energy Corp., along the path to success. His thoroughness in law and connections to decisive parties in government will be advantageous to the development of Sunbay's projects as renewable energy solutions.

QASP: closing Monday's trading session with gains exceeding 31% ($0.042), Quasar Aerospace Industries, Inc. looks to continue its price rally on strong volume, potentially retesting earlier peaks.

Excellent trading session progressed on strong volume. Hopefully the price will look to encounter previous highs...

WLSA: Sunbay Energy Corp. President, Jordan Oxley.

http://www.sunbayenergy.com/about_us_management.php

Oxley is an intellectual, with a background in finance, economics, and philosophy. For a lengthy period of time, his occupation was in the banking sector as a venture capitalist, collaborating with seasoned executives. He began his career working closely with the Governor of the Bank of Canada.

Jordan began his career working closely with the Governor of the Bank of Canada helping to modernize the communications of that institution. He continued on to senior executive positions with technology, publishing, and consumer product companies, alongside intense pursuits as a venture capitalist and entrepreneur. A pioneer of high-tech socio-political messaging, Jordan has spoken at the annual conference of the Public Affairs Association of Canada and in many other forums.

Jordan has held the position of Fellow, International Institute for Public Ethics; Counselor, Canadian Institute of International Affairs; Treasurer, Dialogue Canada; Treasurer and Official Spokesperson, Unity Link / Unilien Society; Riding Treasurer, Liberal Party of Canada; Vice President, Association for Non-Resident Voting Rights; and has been an active member of Transparency International and the Mensa Society.

He holds degrees in Philosophy, Economics, and International Relations, studying at Queen's University, the University of Edinburgh, and the London School of Economics.

http://www.ekartingnews.com/news_info.php?n=3313

Oxley’s experience in the business and financial sector is well documented in numerous sources. Previously occupying a position at Bank of Canada, he helped modernize the communications of that institution.

http://www.bankofcanada.ca/en/res/wp/2000/participants2000.pdf

Oxley is also credited with numerous institutional publications on economics.

http://mil.sagepub.com/cgi/content/citation/27/1/158

http://www.thefreelibrary.com/Insuring+Canada's+exports:+the+case+for+reform+at+export+development...-a0172831282

Book Review: John Madeley, Trade and the Poor: The Impact of International Trade on Developing Countries (London: Intermediate Technology Publications, 1996, 210 pp., £ 11.95 pbk.)Millennium - Journal of International Studies 1997 26: 937-939.

http://mil.sagepub.com/content/vol26/issue3/

Oxley took part in the Transparency International Canada Inc. conference, as an active and regular member of the organization.

"TI-Canada held a seminar in Vancouver, February 4-5, entitled “Corruption and Bribery in Foreign Business Transactions: New Global and Canadian Standards,” in cooperation with the International Centre for

Criminal Law Reform and Criminal Justice Policy.

http://www.transparency.ca/Reports/Newsletters/TIN0301.PDF

BUSINESS ETHICS OFFICE ROOM 200F SCHULICH SCHOOL OF BUSINESS YORK UNIVERSITY 4700 KEELE ST. TORONTO, ONTARIO CANADA M3J 1P3 TEL: (416) 488-3939/736-5809 FAX: (416) 483-5128/736-5762 E-MAIL: TI-CAN@BUS.YORKU.CA

www.transparency.yorku.ca

In numerous sources, Oxley is associated with institutions/universities. They relate his past involvement and continued self-education. http://www.metroputnam.com/news/200807080517

Sun Energy Group, LLC: Oxley is credited with co-founding this renewable energy company with D’Juan Hernandez, a former executive of NRG Energy, Inc., the nation’s leading Independent Power Producer. Exelon Corp. on Tuesday delivered on its promise to scrap its hostile $9 billion stock offer to buy NRG Energy after shareholders at the smaller firm rejected its slate of directors.

http://www.marketwatch.com/story/exelon-scraps-bid-after-nrg-holders-vote?

The Lousiana Gasification facility listed under the presentation will be built under plasma gasification technology, that is, waste to energy. Oxley is no stranger having many years experience with this technology.

Location Metro New Orleans Region, Louisiana (Specific Sites Under Review) System Integrated Gasification Combined Cycle (IGCC) Net Capacity 138 Megawatts (MW) Annual Output 1.1 Million Megawatt Hours (MWh) Feedstock Input 2500 Tons per Day; 821,000 Tons per Year.

SUN ENERGY GROUP, LLC: LOUISIANA GASIFICATION FACILITY (LGF) presentation: http://www.labrownfields.org/downloads/presentations/LSWA-D'Juan%20Hernandez%20SG.pdf

Sun Energy Group: http://www.sunenergygrp.com/index.shtml

Oxley boasts as a former Investment Banker with Strategy Energy, Inc., a Canadian Investment Banking firm, specializing in energy debt and equity placements. Oxley's eMail address is listed as Jordan.Oxley@strategyenergy.com under his membership to the Canadian Wind Energy Association. http://www.canwea.ca/images/uploads/File/Members_only/Committees/Small_Wind/Small_Wind_Committee_Member_November.pdf

Video interview will Jordan Oxley. Note: Video is poor quality but the audio is well worth listening to.

Part 1:

WLSA: Sunbay Energy Corp. President, Jordan Oxley.

http://www.sunbayenergy.com/about_us_management.php

Oxley is an intellectual, with a background in finance, economics, and philosophy. For a lengthy period of time, his occupation was in the banking sector as a venture capitalist, collaborating with seasoned executives. He began his career working closely with the Governor of the Bank of Canada.

Jordan began his career working closely with the Governor of the Bank of Canada helping to modernize the communications of that institution. He continued on to senior executive positions with technology, publishing, and consumer product companies, alongside intense pursuits as a venture capitalist and entrepreneur. A pioneer of high-tech socio-political messaging, Jordan has spoken at the annual conference of the Public Affairs Association of Canada and in many other forums.

Jordan has held the position of Fellow, International Institute for Public Ethics; Counselor, Canadian Institute of International Affairs; Treasurer, Dialogue Canada; Treasurer and Official Spokesperson, Unity Link / Unilien Society; Riding Treasurer, Liberal Party of Canada; Vice President, Association for Non-Resident Voting Rights; and has been an active member of Transparency International and the Mensa Society.

He holds degrees in Philosophy, Economics, and International Relations, studying at Queen's University, the University of Edinburgh, and the London School of Economics.

http://www.ekartingnews.com/news_info.php?n=3313

Oxley’s experience in the business and financial sector is well documented in numerous sources. Previously occupying a position at Bank of Canada, he helped modernize the communications of that institution.

http://www.bankofcanada.ca/en/res/wp/2000/participants2000.pdf

Oxley is also credited with numerous institutional publications on economics.

http://mil.sagepub.com/cgi/content/citation/27/1/158

http://www.thefreelibrary.com/Insuring+Canada's+exports:+the+case+for+reform+at+export+development...-a0172831282

Book Review: John Madeley, Trade and the Poor: The Impact of International Trade on Developing Countries (London: Intermediate Technology Publications, 1996, 210 pp., £ 11.95 pbk.)Millennium - Journal of International Studies 1997 26: 937-939.

http://mil.sagepub.com/content/vol26/issue3/

Oxley took part in the Transparency International Canada Inc. conference, as an active and regular member of the organization.

"TI-Canada held a seminar in Vancouver, February 4-5, entitled “Corruption and Bribery in Foreign Business Transactions: New Global and Canadian Standards,” in cooperation with the International Centre for

Criminal Law Reform and Criminal Justice Policy.

http://www.transparency.ca/Reports/Newsletters/TIN0301.PDF

BUSINESS ETHICS OFFICE ROOM 200F SCHULICH SCHOOL OF BUSINESS YORK UNIVERSITY 4700 KEELE ST. TORONTO, ONTARIO CANADA M3J 1P3 TEL: (416) 488-3939/736-5809 FAX: (416) 483-5128/736-5762 E-MAIL: TI-CAN@BUS.YORKU.CA

www.transparency.yorku.ca

In numerous sources, Oxley is associated with institutions/universities. They relate his past involvement and continued self-education. http://www.metroputnam.com/news/200807080517

Sun Energy Group, LLC: Oxley is credited with co-founding this renewable energy company with D’Juan Hernandez, a former executive of NRG Energy, Inc., the nation’s leading Independent Power Producer. Exelon Corp. on Tuesday delivered on its promise to scrap its hostile $9 billion stock offer to buy NRG Energy after shareholders at the smaller firm rejected its slate of directors.

http://www.marketwatch.com/story/exelon-scraps-bid-after-nrg-holders-vote?

The Lousiana Gasification facility listed under the presentation will be built under plasma gasification technology, that is, waste to energy. Oxley is no stranger having many years experience with this technology.

Location Metro New Orleans Region, Louisiana (Specific Sites Under Review) System Integrated Gasification Combined Cycle (IGCC) Net Capacity 138 Megawatts (MW) Annual Output 1.1 Million Megawatt Hours (MWh) Feedstock Input 2500 Tons per Day; 821,000 Tons per Year.

SUN ENERGY GROUP, LLC: LOUISIANA GASIFICATION FACILITY (LGF) presentation: http://www.labrownfields.org/downloads/presentations/LSWA-D'Juan%20Hernandez%20SG.pdf

Sun Energy Group: http://www.sunenergygrp.com/index.shtml

Oxley boasts as a former Investment Banker with Strategy Energy, Inc., a Canadian Investment Banking firm, specializing in energy debt and equity placements. Oxley's eMail address is listed as Jordan.Oxley@strategyenergy.com under his membership to the Canadian Wind Energy Association. http://www.canwea.ca/images/uploads/File/Members_only/Committees/Small_Wind/Small_Wind_Committee_Member_November.pdf

Video interview will Jordan Oxley. Note: Video is poor quality but the audio is well worth listening to.

Part 1:

WLSA: Chairman and CEO, John G. Simmonds, Wireless Age Communications, Inc.

Simmonds carries decades of experience in turning development-stage projects into multi-million dollar ventures. Clublink Inc., as Canada's largest golf course operator with enterprise value of over $1,000,000,000 was founded by Simmonds in 1989.

In 1989, Mr. Simmonds purchased the first of many golf courses, Cherry Downs, a private 18-hole golf course located

just north of Toronto, Canada. Cherry Downs was later sold into a public company, which became Clublink Corporation (TO: LNK) and today is the largest golf course operation in Canada.

http://www.secinfo.com/d13Wqv.z2ap.htm

Simmonds' earlier practice led him into acquiring hopeless operations and restructuring them to sell for multi-millions. Dynacharge was sold to Duracell for $10,000,000 in 1985, after Simmonds had acquired it for $100,000.

In 1981, he began a long career of buying low cost acquisitions and building them up for later resale. He purchased Dynacharge out of bankruptcy for $100,000 and sold it four years later for $10 million.

http://www.321gold.com/editorials/moriarty/moriarty100103.html

In 1996, Simmonds sold Intek Diversified (IDCC) for $500,000,000 to Securicor of Engand. The symbol was later adopted by InterDigital Communications.

"LOS ANGELES, TORONTO, and SURREY, England--(BUSINESS WIRE)--June 18, 1996--INTEK/SIMMONDS(NASDAQ: IDCC ) SECURICOR(TSE: SMM LONDON STOCK EXCHANGE:SECURICOR) In a joint statement, Intek Diversified Corporation ("Intek") of Los Angeles, California, Simmonds Capital Limited ("SCL") of Toronto, Canada, and Securicor plc of Surrey, England, Tuesday announced that definitive agreements have been signed to combine Intek's Roamer One air time services business with the US Land mobile radio business of Midland International Corporation ("Midland"), a wholly owned subsidiary of SCL, and the narrowband wireless technology and manufacturing operations of Securicor Radiocoms Limited ("SRL"), a wholly owned subsidiary of Securicor Communications Limited.

http://www.secinfo.com/dsVS7.932j.c.htm

Simmonds manages numerous other entities and controls intellectual property for future venture consideration.

President and CEO of Newlook Industries Corp. (NLI.V), CEO of Gamecorp Ltd, formerly Eiger Technology, Inc. (GAIMF.OB), Chairman and CEO of Racino Royale, Inc., now InterAmerican Gaming, Inc., TrackPower, Inc., now Gate To Wire Solutions, Inc. (GWIR.OB), and Lumonall, Inc. (LUNL.OB).

http://pinksheets.com/edgar/GetFilingHtml?FilingID=3640627

In 1991, as a director of Glenayre Electronics, Simmonds aided in taking the company public on the Nasdaq for $80,000,000. The company peaked at $3,000,000,000 in the early nineties.

Simmonds recalls the day in late 1987 when he took control of Glenayre Electronics from Klaus Deering, the man who had spent 19 years building the company from an insignificant $300,000 outfit to a $34-million manufacturer of communications equipment. Speaking of those days now, he says: "I don't want to be dishonest, but I don't want to wash a lot of dirty linen in public--there wasn't a lot of it. Actually, Klaus and I got along pretty well," says Simmonds. http://findarticles.com/p/articles/mi_hb3379/is_198902/ai_n8117201/

Synopsis: Simmonds is a seasoned executive with decades of managerial experience in building successful enterprises. His judgment benefits the strong teams he assembles designated for specific ventures. His experience will be critical to launching waste-to-energy power plant projects in cooperation with Sunbay Energy Corp. President, Jordan Oxley, across North America.

WLSA: Understanding the Waste Management movement in Connecticut. Four key things that will net Wireless Age Communications, Inc. major contracts under plasma gasification technology.

Resource Recovery Facilities (RRFs) are incineration plants producing electricity by burning waste ("waste-to-energy").

RRFs treat 57% of municipal solid waste (MSW) generated in the state of Connecticut.

Contracts that supply MSW to Connecticut’s RRF facilities will expire over the next two to fourteen years.

2,168,850 tons of MSW will need alternative treatment.

If an alternative is not found, RRF enterprises in the state of Connecticut will be put out of business. In cooperation with Sunbay Energy Corp., and Wireless Age Communications, Inc., RRF facilities will be replaced with plasma gasification plants state-wide. Remember that plasma gasification is an inexpensive, efficient and renewable energy solution.

Key Factors Affecting Solid Waste Management in Connecticut.

http://tinyurl.com/mfrr7h

The context for solid waste management in Connecticut has changed substantially since the last statewide solid waste management plan was adopted in 1991. The following are among the key issues that will shape solid waste management in coming years:

If Connecticut doesn’t substantially increase the rate of MSW disposal diversion, it is projected to have an increasing shortfall of MSW in-state disposal capacity.

Currently there is increasing out-of-state capacity for solid waste disposal at competitive prices.

Solid waste is a commodity subject to interstate commerce laws.

Bonds that financed the construction of the MSW RRFs will be paid off, and municipal contracts to supply MSW to Connecticut’s RRF facilities will expire over the next two to fourteen years. Over this same time period, disposal capacity at four of the six MSW RRFs may shift from public to private ownership.

Recycling and solid waste management services are increasingly privately run and market-driven.

Connecticut’s waste diversion infrastructure is stagnant and State and municipal funding is inadequate to support and achieve increased source reduction, reuse, recycling, and composting.

Nationally, recycling of non-traditional material streams has grown significantly.

National and global recycling markets have grown substantially.

Other states and communities have demonstrated an ability to achieve higher waste diversion rates than Connecticut has achieved to date.

There is a growing interest in product stewardship and producer responsibility policies.

MSW

As shown in ES Figure 1, it was projected that in FY2005 approximately thirty percent of the municipal solid waste (MSW) generated was recycled; fifty-seven percent was burned at six regional MSW Resource Recovery Facilities (RRFs); nine percent was disposed out-of-state; and four percent was disposed at in-state landfills. Connecticut is more reliant on waste-to-energy facilities than any other state in the country. This reliance on RRFs results in a significant reduction in the volume of waste ultimately needing disposal at a landfill.

Over the past decade, Connecticut has become more reliant on out-of-state disposal options for MSW (mostly at out-of-state landfills). Since FY1994, out-of-state disposal of Connecticut-generated MSW has increased from approximately 27,000 tons/year to 327,000 tons/year in FY2004. This raises issues regarding inconsistency with the statutory hierarchy, and increased risk due to disposal cost fluctuations and

availability.

Breaking down the technology: "Discovery Channel features energy from waste plasma gasification".

Link to video: http://www.timelesswealth.net/video2.html

WLSA: Understanding the Waste Management movement in Connecticut. Four key things that will net Wireless Age Communications, Inc. major contracts under plasma gasification technology.

Resource Recovery Facilities (RRFs) are incineration plants producing electricity by burning waste ("waste-to-energy").

RRFs treat 57% of municipal solid waste (MSW) generated in the state of Connecticut.

Contracts that supply MSW to Connecticut’s RRF facilities will expire over the next two to fourteen years.

2,168,850 tons of MSW will need alternative treatment.

If an alternative is not found, RRF enterprises in the state of Connecticut will be put out of business. In cooperation with Sunbay Energy Corp., and Wireless Age Communications, Inc., RRF facilities will be replaced with plasma gasification plants state-wide. Remember that plasma gasification is an inexpensive, efficient and renewable energy solution.

Key Factors Affecting Solid Waste Management in Connecticut.

http://tinyurl.com/mfrr7h

The context for solid waste management in Connecticut has changed substantially since the last statewide solid waste management plan was adopted in 1991. The following are among the key issues that will shape solid waste management in coming years:

If Connecticut doesn’t substantially increase the rate of MSW disposal diversion, it is projected to have an increasing shortfall of MSW in-state disposal capacity.

Currently there is increasing out-of-state capacity for solid waste disposal at competitive prices.

Solid waste is a commodity subject to interstate commerce laws.

Bonds that financed the construction of the MSW RRFs will be paid off, and municipal contracts to supply MSW to Connecticut’s RRF facilities will expire over the next two to fourteen years. Over this same time period, disposal capacity at four of the six MSW RRFs may shift from public to private ownership.

Recycling and solid waste management services are increasingly privately run and market-driven.

Connecticut’s waste diversion infrastructure is stagnant and State and municipal funding is inadequate to support and achieve increased source reduction, reuse, recycling, and composting.

Nationally, recycling of non-traditional material streams has grown significantly.

National and global recycling markets have grown substantially.

Other states and communities have demonstrated an ability to achieve higher waste diversion rates than Connecticut has achieved to date.

There is a growing interest in product stewardship and producer responsibility policies.

MSW

As shown in ES Figure 1, it was projected that in FY2005 approximately thirty percent of the municipal solid waste (MSW) generated was recycled; fifty-seven percent was burned at six regional MSW Resource Recovery Facilities (RRFs); nine percent was disposed out-of-state; and four percent was disposed at in-state landfills. Connecticut is more reliant on waste-to-energy facilities than any other state in the country. This reliance on RRFs results in a significant reduction in the volume of waste ultimately needing disposal at a landfill.

Over the past decade, Connecticut has become more reliant on out-of-state disposal options for MSW (mostly at out-of-state landfills). Since FY1994, out-of-state disposal of Connecticut-generated MSW has increased from approximately 27,000 tons/year to 327,000 tons/year in FY2004. This raises issues regarding inconsistency with the statutory hierarchy, and increased risk due to disposal cost fluctuations and

availability.

Breaking down the technology: "Discovery Channel features energy from waste plasma gasification".

Link to video: http://www.timelesswealth.net/video2.html

WLSA ~ Chairman and CEO, John G. Simmonds, Wireless Age Communications, Inc.

Simmonds carries decades of experience in turning development-stage projects into multi-million dollar ventures. Clublink Inc., as Canada's largest golf course operator with enterprise value of over $1,000,000,000 was founded by Simmonds in 1989.

In 1989, Mr. Simmonds purchased the first of many golf courses, Cherry Downs, a private 18-hole golf course located

just north of Toronto, Canada. Cherry Downs was later sold into a public company, which became Clublink Corporation (TO: LNK) and today is the largest golf course operation in Canada.

http://www.secinfo.com/d13Wqv.z2ap.htm

Simmonds' earlier practice led him into acquiring hopeless operations and restructuring them to sell for multi-millions. Dynacharge was sold to Duracell for $10,000,000 in 1985, after Simmonds had acquired it for $100,000.

In 1981, he began a long career of buying low cost acquisitions and building them up for later resale. He purchased Dynacharge out of bankruptcy for $100,000 and sold it four years later for $10 million.

http://www.321gold.com/editorials/moriarty/moriarty100103.html

In 1996, Simmonds sold Intek Diversified (IDCC) for $500,000,000 to Securicor of Engand. The symbol was later adopted by InterDigital Communications.

"LOS ANGELES, TORONTO, and SURREY, England--(BUSINESS WIRE)--June 18, 1996--INTEK/SIMMONDS(NASDAQ: IDCC ) SECURICOR(TSE: SMM LONDON STOCK EXCHANGE:SECURICOR) In a joint statement, Intek Diversified Corporation ("Intek") of Los Angeles, California, Simmonds Capital Limited ("SCL") of Toronto, Canada, and Securicor plc of Surrey, England, Tuesday announced that definitive agreements have been signed to combine Intek's Roamer One air time services business with the US Land mobile radio business of Midland International Corporation ("Midland"), a wholly owned subsidiary of SCL, and the narrowband wireless technology and manufacturing operations of Securicor Radiocoms Limited ("SRL"), a wholly owned subsidiary of Securicor Communications Limited.

http://www.secinfo.com/dsVS7.932j.c.htm

Simmonds manages numerous other entities and controls intellectual property for future venture consideration.

President and CEO of Newlook Industries Corp. (NLI.V), CEO of Gamecorp Ltd, formerly Eiger Technology, Inc. (GAIMF.OB), Chairman and CEO of Racino Royale, Inc., now InterAmerican Gaming, Inc., TrackPower, Inc., now Gate To Wire Solutions, Inc. (GWIR.OB), and Lumonall, Inc. (LUNL.OB).

http://pinksheets.com/edgar/GetFilingHtml?FilingID=3640627

In 1991, as a director of Glenayre Electronics, Simmonds aided in taking the company public on the Nasdaq for $80,000,000. The company peaked at $3,000,000,000 in the early nineties.

Simmonds recalls the day in late 1987 when he took control of Glenayre Electronics from Klaus Deering, the man who had spent 19 years building the company from an insignificant $300,000 outfit to a $34-million manufacturer of communications equipment. Speaking of those days now, he says: "I don't want to be dishonest, but I don't want to wash a lot of dirty linen in public--there wasn't a lot of it. Actually, Klaus and I got along pretty well," says Simmonds. http://findarticles.com/p/articles/mi_hb3379/is_198902/ai_n8117201/

Synopsis: Simmonds is a seasoned executive with decades of managerial experience in building successful enterprises. His judgment benefits the strong teams he assembles designated for specific ventures. His experience will be critical to launching waste-to-energy power plant projects in cooperation with Sunbay Energy Corp. President, Jordan Oxley, across North America.

Indistinct statements in their release lead to my inquiry: http://finance.yahoo.com/news/Sinoenergy-Corporation-prnews-3736760286.html?x=0&.v=28

Based on their reply, Sinoenergy Corporation's future seems bright.

The same multi-billion dollar partners Simmonds was referring to? Pieces of the puzzle beginning to fall into place, with the Connecticut project to generate significant shareholder value imho...

WLSA: Understanding the Waste Management movement in Connecticut. Four key things that will net Wireless Age Communications, Inc. major contracts under plasma gasification technology.

Resource Recovery Facilities (RRFs) are incineration plants producing electricity by burning waste ("waste-to-energy").

RRFs treat 57% of municipal solid waste (MSW) generated in the state of Connecticut.

Contracts that supply MSW to Connecticut’s RRF facilities will expire over the next two to fourteen years.

2,168,850 tons of MSW will need alternative treatment.

If an alternative is not found, RRF enterprises in the state of Connecticut will be put out of business. In cooperation with Sunbay Energy Corp., and Wireless Age Communications, Inc., RRF facilities will be replaced with plasma gasification plants state-wide. Remember that plasma gasification is an inexpensive, efficient and renewable energy solution.

Key Factors Affecting Solid Waste Management in Connecticut.

http://tinyurl.com/mfrr7h

The context for solid waste management in Connecticut has changed substantially since the last statewide solid waste management plan was adopted in 1991. The following are among the key issues that will shape solid waste management in coming years:

If Connecticut doesn’t substantially increase the rate of MSW disposal diversion, it is projected to have an increasing shortfall of MSW in-state disposal capacity.

Currently there is increasing out-of-state capacity for solid waste disposal at competitive prices.

Solid waste is a commodity subject to interstate commerce laws.

Bonds that financed the construction of the MSW RRFs will be paid off, and municipal contracts to supply MSW to Connecticut’s RRF facilities will expire over the next two to fourteen years. Over this same time period, disposal capacity at four of the six MSW RRFs may shift from public to private ownership.

Recycling and solid waste management services are increasingly privately run and market-driven.

Connecticut’s waste diversion infrastructure is stagnant and State and municipal funding is inadequate to support and achieve increased source reduction, reuse, recycling, and composting.

Nationally, recycling of non-traditional material streams has grown significantly.

National and global recycling markets have grown substantially.

Other states and communities have demonstrated an ability to achieve higher waste diversion rates than Connecticut has achieved to date.

There is a growing interest in product stewardship and producer responsibility policies.

MSW

As shown in ES Figure 1, it was projected that in FY2005 approximately thirty percent of the municipal solid waste (MSW) generated was recycled; fifty-seven percent was burned at six regional MSW Resource Recovery Facilities (RRFs); nine percent was disposed out-of-state; and four percent was disposed at in-state landfills. Connecticut is more reliant on waste-to-energy facilities than any other state in the country. This reliance on RRFs results in a significant reduction in the volume of waste ultimately needing disposal at a landfill.

Over the past decade, Connecticut has become more reliant on out-of-state disposal options for MSW (mostly at out-of-state landfills). Since FY1994, out-of-state disposal of Connecticut-generated MSW has increased from approximately 27,000 tons/year to 327,000 tons/year in FY2004. This raises issues regarding inconsistency with the statutory hierarchy, and increased risk due to disposal cost fluctuations and

availability.

Four key things to help you understand the Waste Management movement in Connecticut.

Resource Recovery Facilities (RRFs) are incineration plants producing electricity by burning waste ("waste-to-energy").

RRFs treat 57% of municipal solid waste (MSW) generated in the state of Connecticut.

Contracts that supply MSW to Connecticut’s RRF facilities will expire over the next two to fourteen years.

2,168,850 tons of MSW will need alternative treatment.

If an alternative is not found, RRF enterprises in the state of Connecticut will be put out of business. In cooperation with Sunbay Energy Corp., and Wireless Age Communications, Inc., RRF facilities will be replaced with plasma gasification plants state-wide. Remember that plasma gasification is an inexpensive, efficient and renewable energy solution.

Key Factors Affecting Solid Waste Management in Connecticut.

The context for solid waste management in Connecticut has changed substantially since the last statewide solid waste management plan was adopted in 1991. The following are among the key issues that will shape solid waste management in coming years:

If Connecticut doesn’t substantially increase the rate of MSW disposal diversion, it is projected to have an increasing shortfall of MSW in-state disposal capacity.

Currently there is increasing out-of-state capacity for solid waste disposal at competitive prices.

Solid waste is a commodity subject to interstate commerce laws.

Bonds that financed the construction of the MSW RRFs will be paid off, and municipal contracts to supply MSW to Connecticut’s RRF facilities will expire over the next two to fourteen years. Over this same time period, disposal capacity at four of the six MSW RRFs may shift from public to private ownership.

Recycling and solid waste management services are increasingly privately run and market-driven.

Connecticut’s waste diversion infrastructure is stagnant and State and municipal funding is inadequate to support and achieve increased source reduction, reuse, recycling, and composting.

Nationally, recycling of non-traditional material streams has grown significantly.

National and global recycling markets have grown substantially.

Other states and communities have demonstrated an ability to achieve higher waste diversion rates than Connecticut has achieved to date.

There is a growing interest in product stewardship and producer responsibility policies.

MSW

As shown in ES Figure 1, it was projected that in FY2005 approximately thirty percent of the municipal solid waste (MSW) generated was recycled; fifty-seven percent was burned at six regional MSW Resource Recovery Facilities (RRFs); nine percent was disposed out-of-state; and four percent was disposed at in-state landfills. Connecticut is more reliant on waste-to-energy facilities than any other state in the country. This reliance on RRFs results in a significant reduction in the volume of waste ultimately needing disposal at a landfill.

Over the past decade, Connecticut has become more reliant on out-of-state disposal options for MSW (mostly at out-of-state landfills). Since FY1994, out-of-state disposal of Connecticut-generated MSW has increased from approximately 27,000

tons/year to 327,000 tons/year in FY2004. This raises issues regarding inconsistency with the statutory hierarchy, and increased risk due to disposal cost fluctuations and

availability.

SNEN: Sinoenergy Corporation will continue operations and benefit from the China stimulus plan granted towards alternative energy. Response via. eMail.

-----Original Message-----

From: tys [mailto:tys@sinoenergycorporation.com]

Sent: Monday, August 24, 2009 2:09 AM

To: XXXXX

Subject: re: Sinoenergy Corporation

Dear Mr. Stevenson:

Thank you for your letter. We appreciate your concern with SNEN.

We have indirectly benefited from the Chinese Government Stimulus Plan, however, the Stimulus Plan is for the "Green" Sector as a whole, rather than any individual company, therefore it takes time to see the effect.

Bankruptcy is not an option under consideration.

If you have any other questions, please feel free to contact us. Thank you.

Best Wishes

Selina TANG

Sinoenergy Corporation

Tel: +86 (010) 84927035 832

Email: tys@sinoenergycorporation.com

SNEN: Sinoenergy Corporation responds via. eMail. They will continue operations and benefit from the China stimulus plan granted towards alternative energy.

-----Original Message-----

From: tys [mailto:tys@sinoenergycorporation.com]

Sent: Monday, August 24, 2009 2:09 AM

To: XXXXX

Subject: re: Sinoenergy Corporation

Dear Mr. Stevenson:

Thank you for your letter. We appreciate your concern with SNEN.

We have indirectly benefited from the Chinese Government Stimulus Plan, however, the Stimulus Plan is for the "Green" Sector as a whole, rather than any individual company, therefore it takes time to see the effect.

Bankruptcy is not an option under consideration.

If you have any other questions, please feel free to contact us. Thank you.

Best Wishes

Selina TANG

Sinoenergy Corporation

Tel: +86 (010) 84927035 832

Email: tys@sinoenergycorporation.com

Meant to link to this message: http://investorshub.advfn.com/boards/read_msg.aspx?message_id=40683476

Out for a few here. All the best.

OPTT ($4.55) ~ reversal pattern. Book value $8.10/share, issued and outstanding shares: 10,210,354.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=40683476

SNEN ($1.36) ~ seeking a reversal in oversold conditions...issued and outstanding shares amount to 15,942,336; free trading, 7,580,000. Book value of $3.65/share.

SNEN ($1.36) ~ seeking a reversal in oversold conditions...issued and outstanding shares amount to 15,942,336; free trading, 7,580,000. Book value of $3.65/share.

A strong pincher hereabouts...link back.

OPTT ($4.65) ~ strong gap up heading into Friday's trading session.

Good Morning jimmybob.