News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Seeking Creative & Innovative Investment Ideas...

EDWARD STEVENSON

![]()

Seeking Creative & Innovative Investment Ideas...

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Seeking Creative & Innovative Investment Ideas...

What Will Change for Natural Gas ETFs?

by: Tom Lydon September 27, 2009 | about: UNG

Regulation as a result of speculation in energy exchange traded funds has forced fund providers to change the make up of the natural gas ETF portfolio. What has changed?

United States Commodity Funds (USCF) will be restructuring United States Natural Gas (NYSEArca: UNG) in anticipation of the government’s proposed position limit regulation in order to reduce speculation, report Dan Burns and Rebekah Kebede for Forbes.

The USCF will reduce the fund’s positions in listed natural gas futures and increase the fund’s holdings in over-the-counter natural gas swaps. Around 75% to 80% of UNG’s holdings are still listed as natural gas futures.

The change in the fund’s portfolio is an attempt to obviate potential CFTC regulations. UNG may still shift its portfolio even further, depending on the CFTC’s ultimate decision.

CFTC regulation came over concerns that ETFs were driving speculation and artificially boosting commodity prices. Analysts, however, point to the fact that data shows energy-based commodity ETFs were not sellers of contracts in the 6 to 12 months leading to the jump in energy prices. Furthermore, CFTC regulation could push ETFs to invest in over-the-counter vehicles, non-U.S. listed vehicles or downsize and return money to shareholders.

The USCF’s biggest concern is that regulation could result in higher costs for investors in energy ETFs without any real added benefits.

United States Natural Gas (NYSEArca: UNG): down 48.3% year-to-date.

ETF Ideas for China's Cleaner Energy Push.

by: Tom Lydon September 27, 2009 | about: KOL / LD / PKOL

The effects of pollution can no longer be ignored and China is taking up the fight. China focused its attention on coal mines and lead smelters in hopes of reducing pollution, and the result was a boon to both coal and lead-related ETFs.

China, one of the world’s biggest polluters, is becoming more environmentally conscientious. As a result, the government has started to crack down on illegal coal mines, lead smelters and other highly pollutant facilities, writes Tony Daltorio for Investment U. The government crackdown may not concern a foreign investor until one stops to think about the economic implications.

Simple economic supply and demand shows that China has reduced supply of both coal and lead by clamping down on pollution while demand remains unchanged, which could result in higher prices for both products. Now, China has to import coal and at a higher price for steel production and power plants.

China is also the world’s largest producer and consumer of lead. Global inventories of lead is already relatively low and China’s recent increased demand of lead resulted in lead prices that are higher than they’ve been for a year.

If China continues on its newfound environmentally-friendly path, the country will probably have to import more when seasonal consumption trends kick in, which would further drive up prices.

Market Vectors Coal (NYSEArca: KOL)

PowerShares Global Coal Portfolio (NASDAQ: PKOL)

iPath Dow Jones – UBS Lead ETN (NYSE: LD)

http://seekingalpha.com/article/163623-etf-ideas-for-china-s-cleaner-energy-push?

ETF Ideas for China's Cleaner Energy Push.

by: Tom Lydon September 27, 2009 | about: KOL / LD / PKOL

The effects of pollution can no longer be ignored and China is taking up the fight. China focused its attention on coal mines and lead smelters in hopes of reducing pollution, and the result was a boon to both coal and lead-related ETFs.

China, one of the world’s biggest polluters, is becoming more environmentally conscientious. As a result, the government has started to crack down on illegal coal mines, lead smelters and other highly pollutant facilities, writes Tony Daltorio for Investment U. The government crackdown may not concern a foreign investor until one stops to think about the economic implications.

Simple economic supply and demand shows that China has reduced supply of both coal and lead by clamping down on pollution while demand remains unchanged, which could result in higher prices for both products. Now, China has to import coal and at a higher price for steel production and power plants.

China is also the world’s largest producer and consumer of lead. Global inventories of lead is already relatively low and China’s recent increased demand of lead resulted in lead prices that are higher than they’ve been for a year.

If China continues on its newfound environmentally-friendly path, the country will probably have to import more when seasonal consumption trends kick in, which would further drive up prices.

Market Vectors Coal (NYSEArca: KOL)

PowerShares Global Coal Portfolio (NASDAQ: PKOL)

iPath Dow Jones – UBS Lead ETN (NYSE: LD)

http://seekingalpha.com/article/163623-etf-ideas-for-china-s-cleaner-energy-push?

Same 4-Bedroom House -- Wildly Different Prices.

by Les Christie

Thursday, September 24, 2009

The cost of a middle-management-type home varies significantly depending on where in the country you live. But there are some huge spreads within states, as well.

Imagine you're a mid-level executive living in Grayling, Mich., the "Canoe Capital of the World." You've received a job offer that pays twice as much in posh La Jolla, Calif., the seaside resort near San Diego.

It sounds like a no-brainer, right? Not only will you earn all that extra money, you'll be enjoying some of the best weather in the United States. You can boat year round.

What you may not have considered is how much it costs to buy the kind of home you've gotten used to in Michigan. As a matter of fact, you better plan on spending nearly 20 times as much, according to the 2009 Coldwell Banker Home Price Comparison Index.

The overall U.S. average for such a house is $363,401, but in Grayling, it sells for just $112,675, the most affordable market in the nation.

La Jolla, on the other hand, is the most expensive; a comparable house there goes for a cool $2.125 million. That's more than $2 million disparity is up from 2004, when the spread between the most expensive and most affordable towns was $1.5 million.

"La Jolla, loosely translated, means 'the jewel' in Spanish," said Rick Hoffman, a Coldwell Banker broker in San Diego. "It's always been a place everybody goes to. The weather is excellent. There's great shopping, restaurants and recreation. In non-rush-hour traffic you're only 15 minutes from downtown San Diego."

Grayling also has excellent recreational opportunities, many of which revolve around the Au Sable River, which runs through town. That makes the fishing and canoeing in this northern part of Michigan's Lower Peninsula splendid. Winter sports, like snow-shoeing, cross-country skiing and snowmobiling are also big.

But like most of Michigan, the economy here is slow. Much of the business is propped up by Camp Grayling, a nearby Army base. There's also the tourist trade -- lots of vacation homes in the area -- and timbering in the state forests, according to Laurie Jamison, a broker with Coldwell Banker Cornell Realty.

"If you had a $2 million home in Grayling, you'd be king of the mountain," she said. "I couldn't imagine seeing a house like that here." The most expensive home she sold recently was a big, lakefront property for about $600,000.

Big Affordability Improvement

La Jolla notwithstanding, housing affordability has improved dramatically, according to Jim Gillespie, Coldwell Banker's CEO.

"I am most intrigued with the affordability levels now seen across much of the nation," he said. "Thirty percent of the markets show this type of home to be below $200,000, illustrating the opportunity to take advantage of price declines, interest rate levels and increased selection of homes."

According to the report, in 84 of the U.S. markets Coldwell Banker covers, the sample home price averages under $200,000. At that price, the monthly mortgage costs should not exceed $1,200.

As for that house in Grayling -- factoring in 20% down and a 5.5%, 30-year fixed rate loan -- it would cost a mortgage borrower only about $512 a month.

This index, released Wednesday, is an "apples-to-apples" comparison of similar homes in so-called "move-up buyer" neighborhoods. It compares the prices charged for 2,200-square-foot, four-bedroom, two-and-one-half bath, single-family homes in more than 300 markets around the nation.

Under those same terms, the monthly mortgage bill would come to nearly $10,000 in La Jolla. Not that you could get the same deal. The loan would have to be a jumbo mortgage, since it exceeds cap limits for loans issued through Fannie Mae and Freddie Mac. That would add about a point to the interest rate and $1,000 to the monthly housing costs.

Some of the other very affordable towns include: Akron, Ohio, where this type of house costs $121,885; Fayetteville, N.C., $130,875; and Canton, Ohio, $131,867. The most affordable markets are sprinkled all over the Midwest, Southwest and South.

Most of the highest priced markets are in California. The Golden State accounts for eight of the top 10 towns. Beverly Hills is second at $1.982 million, followed by Greenwich, Conn., at $1.59 million. Boston is the other non-California town to crack the top 10; it was seventh at $1.34 million. That was one place behind San Francisco, the biggest city on the list.

Variations Within States

Not only are there huge affordability differences around the nation, there are big spreads within the same states. While California has many of the most expensive cities, for example, it also has some very affordable ones.

In Lancaster, Calif., which lies just north of Los Angeles and is one of the nation's fastest growing cities, the sample home goes for $165,205 -- nearly $2 million less than La Jolla.

West Hartford, Conn., has these exec homes for $242,789, more than $1 million less than Greenwich. In Massachusetts, a home in the old mill town of Worcester costs $242,769, a million dollars less than in Boston, just 47 miles away.

The smallest spreads occur in the wide-open-space states, such as Oklahoma, where homes in the most expensive market, Oklahoma City ($164,250), cost less than $10,000 more than the most affordable one, Tulsa ($154,800).

In Idaho, Boise homes cost $215,432 compared with $204,518 in Coeur d'Alene. And homes in Florence, Ky., cost $212,720, compared to $188,017 in Lexington.

http://finance.yahoo.com/real-estate/article/107816/same-4-bedroom-house-wildly-different-prices.html?mod=realestate-buy

Same 4-Bedroom House -- Wildly Different Prices.

by Les Christie

Thursday, September 24, 2009

The cost of a middle-management-type home varies significantly depending on where in the country you live. But there are some huge spreads within states, as well.

Imagine you're a mid-level executive living in Grayling, Mich., the "Canoe Capital of the World." You've received a job offer that pays twice as much in posh La Jolla, Calif., the seaside resort near San Diego.

It sounds like a no-brainer, right? Not only will you earn all that extra money, you'll be enjoying some of the best weather in the United States. You can boat year round.

What you may not have considered is how much it costs to buy the kind of home you've gotten used to in Michigan. As a matter of fact, you better plan on spending nearly 20 times as much, according to the 2009 Coldwell Banker Home Price Comparison Index.

The overall U.S. average for such a house is $363,401, but in Grayling, it sells for just $112,675, the most affordable market in the nation.

La Jolla, on the other hand, is the most expensive; a comparable house there goes for a cool $2.125 million. That's more than $2 million disparity is up from 2004, when the spread between the most expensive and most affordable towns was $1.5 million.

"La Jolla, loosely translated, means 'the jewel' in Spanish," said Rick Hoffman, a Coldwell Banker broker in San Diego. "It's always been a place everybody goes to. The weather is excellent. There's great shopping, restaurants and recreation. In non-rush-hour traffic you're only 15 minutes from downtown San Diego."

Grayling also has excellent recreational opportunities, many of which revolve around the Au Sable River, which runs through town. That makes the fishing and canoeing in this northern part of Michigan's Lower Peninsula splendid. Winter sports, like snow-shoeing, cross-country skiing and snowmobiling are also big.

But like most of Michigan, the economy here is slow. Much of the business is propped up by Camp Grayling, a nearby Army base. There's also the tourist trade -- lots of vacation homes in the area -- and timbering in the state forests, according to Laurie Jamison, a broker with Coldwell Banker Cornell Realty.

"If you had a $2 million home in Grayling, you'd be king of the mountain," she said. "I couldn't imagine seeing a house like that here." The most expensive home she sold recently was a big, lakefront property for about $600,000.

Big Affordability Improvement

La Jolla notwithstanding, housing affordability has improved dramatically, according to Jim Gillespie, Coldwell Banker's CEO.

"I am most intrigued with the affordability levels now seen across much of the nation," he said. "Thirty percent of the markets show this type of home to be below $200,000, illustrating the opportunity to take advantage of price declines, interest rate levels and increased selection of homes."

According to the report, in 84 of the U.S. markets Coldwell Banker covers, the sample home price averages under $200,000. At that price, the monthly mortgage costs should not exceed $1,200.

As for that house in Grayling -- factoring in 20% down and a 5.5%, 30-year fixed rate loan -- it would cost a mortgage borrower only about $512 a month.

This index, released Wednesday, is an "apples-to-apples" comparison of similar homes in so-called "move-up buyer" neighborhoods. It compares the prices charged for 2,200-square-foot, four-bedroom, two-and-one-half bath, single-family homes in more than 300 markets around the nation.

Under those same terms, the monthly mortgage bill would come to nearly $10,000 in La Jolla. Not that you could get the same deal. The loan would have to be a jumbo mortgage, since it exceeds cap limits for loans issued through Fannie Mae and Freddie Mac. That would add about a point to the interest rate and $1,000 to the monthly housing costs.

Some of the other very affordable towns include: Akron, Ohio, where this type of house costs $121,885; Fayetteville, N.C., $130,875; and Canton, Ohio, $131,867. The most affordable markets are sprinkled all over the Midwest, Southwest and South.

Most of the highest priced markets are in California. The Golden State accounts for eight of the top 10 towns. Beverly Hills is second at $1.982 million, followed by Greenwich, Conn., at $1.59 million. Boston is the other non-California town to crack the top 10; it was seventh at $1.34 million. That was one place behind San Francisco, the biggest city on the list.

Variations Within States

Not only are there huge affordability differences around the nation, there are big spreads within the same states. While California has many of the most expensive cities, for example, it also has some very affordable ones.

In Lancaster, Calif., which lies just north of Los Angeles and is one of the nation's fastest growing cities, the sample home goes for $165,205 -- nearly $2 million less than La Jolla.

West Hartford, Conn., has these exec homes for $242,789, more than $1 million less than Greenwich. In Massachusetts, a home in the old mill town of Worcester costs $242,769, a million dollars less than in Boston, just 47 miles away.

The smallest spreads occur in the wide-open-space states, such as Oklahoma, where homes in the most expensive market, Oklahoma City ($164,250), cost less than $10,000 more than the most affordable one, Tulsa ($154,800).

In Idaho, Boise homes cost $215,432 compared with $204,518 in Coeur d'Alene. And homes in Florence, Ky., cost $212,720, compared to $188,017 in Lexington.

http://finance.yahoo.com/real-estate/article/107816/same-4-bedroom-house-wildly-different-prices.html?mod=realestate-buy

What's Next for Gold and Silver ETFs?

by: Tom Lydon September 24, 2009 | about: DGL / GLD / IAU / SGOL

The price of gold has been staying steady above its four-figure mark, and investment in gold and its related ETFs has drawn many seeking to strike it rich. But will gold’s uptrend last?

Gold has held onto its $1,000/ounce price level but in real, or inflation-adjusted, terms, the precious metal is short of its all-time high, writes Paul Amery for IndexUniverse. After adjusting for the effects of U.S. consumer price inflation, it is calculated that gold’s 1980 peak price of $850 roughly equals $2,358 today.

Daniel Brebner and Deutsche Bank attribute inflation, inflation volatility and the performance of the U.S. dollar as the main drivers of gold prices. Brebner argues that gold does well in deflationary periods when gold is seen as a safe haven, and in inflationary environments when gold is hedged against money over supply. He sees periods of disinflation, or moderating inflation, as the bane of gold prices.

Currently, there are inflationary and deflationary voices in the market. But, Brebner sees that uncertainty over future price levels means inflation volatility, which he has said is bullish for gold.

Investor demand for gold is on the rise. China is seen as likely to purchase a hefty chunk of the world’s gold as it seeks to accumulate hard metal assets. And, of course, demand for gold ETFs is also increasing as gold investments become more popular.

Deutsche Bank says that if there is moderating risk premiums, low but contained inflation and recovery from financial crisis, gold could drop back to $650/ounce. If the markets are less benign, on the other hand, gold prices could reach up to $2,500.

Meanwhile, a pullback for silver is seen as in the cards after the recent run-up, reports Geoff Candy for Mineweb. RBC Capital Markets feels that despite the pullback they’re predicting, they’re still feeling positive about the metal because of a weakening U.S. dollar, which could continue to boost the price of precious metals. They also feel that growth in the industrial sector and investment demand will offset the drop in demand for silver in photography.

SPDR Gold Shares (NYSEArca: GLD): up 14.2% year-to-date

[chartetftrends.redinews.com/tools/C04?queryid=QJ33042&symbol=gld

iShares COMEX Gold Trust (NYSEArca: IAU): up 14.2% year-to-date

PowerShares DB Gold (NYSEArca: DGL): up 12.8% year-to-date

ETFS Gold Trust (NYSEArca: SGOL): launched earlier this month

RedChip Announces 34 Companies to Present At Its New York Equities Conference At the NASDAQ MarketSite.

CEOs of Participating Companies Will Deliver Financial Presentations From 8 a.m. to 5 p.m. EDT September 30th and October 1st, 2009.

Companies: American Lorain Corporation (ALN)

ORLANDO, Fla., Sept. 17, 2009 (GLOBE NEWSWIRE) -- RedChip Companies, Inc. today announced that the CEOs and executive teams of 34 emerging small-cap companies will deliver financial presentations during the 2009 RedChip New York Equities Conference on September 30th and October 1st, 2009 at the NASDAQ MarketSite (4 Times Square) in New York City. In addition, on September 30th, RedChip will ring the NASDAQ opening bell. The general track representing ten industries will be held on Wednesday, September 30th from 8 a.m. to 5 p.m. Eastern time. The China track presentations will be held on Thursday, October 1st from 8 a.m. to 5 p.m.

RedChip investor conferences are a nationally known forum for emerging small-cap companies to present their stories before hundreds of retail brokers, institutional brokers, fund managers, portfolio managers, accredited investors, and research analysts whose disciplined focus towards the small-cap markets represents their core investment strategies. Sponsors of the event include NASDAQ OMX, Expos2, Vintage Filings, Vcorp Services, and Maxim Group LLC.

Company presentations will be webcast live via http://www.RedChip.com and available for 90 days. Participating investors will have the opportunity to meet one-on-one with the CEOs of presenting companies, and thousands of investors from across the United States, Europe and Asia are expected to watch the conference online at RedChip.com. In addition, RedChip TV(TM) will be on-site conducting interviews with CEOs, which will be archived for later viewing at RedChip.com.

The conference will feature companies from the following industries: Biotechnology, Healthcare Technology, Education, Telecommunications, Oil & Gas, Basic Materials, Consumer Services, Industrial Goods, Energy, Alternative Energy, Medical Devices, Specialty Chemicals, Precious Metals Mining, and more.

To date, companies scheduled to present include the following:

Acorn International, Inc. (NYSE:ATV - News); American Lorain Corporation (NYSE Amex:ALN); The Quantum Group, Inc. (NYSE Amex:QGP); Longwei Petroleum Investment Holding Ltd. (OTCBB:LPIH - News); Globalstar, Inc. (Nasdaq:GSAT - News)...continued: http://finance.yahoo.com/news/RedChip-Announces-34-pz-423967558.html?x=0&.v=4

RedChip Announces 34 Companies to Present At Its New York Equities Conference At the NASDAQ MarketSite.

CEOs of Participating Companies Will Deliver Financial Presentations From 8 a.m. to 5 p.m. EDT September 30th and October 1st, 2009.

Companies: American Lorain Corporation (ALN)

ORLANDO, Fla., Sept. 17, 2009 (GLOBE NEWSWIRE) -- RedChip Companies, Inc. today announced that the CEOs and executive teams of 34 emerging small-cap companies will deliver financial presentations during the 2009 RedChip New York Equities Conference on September 30th and October 1st, 2009 at the NASDAQ MarketSite (4 Times Square) in New York City. In addition, on September 30th, RedChip will ring the NASDAQ opening bell. The general track representing ten industries will be held on Wednesday, September 30th from 8 a.m. to 5 p.m. Eastern time. The China track presentations will be held on Thursday, October 1st from 8 a.m. to 5 p.m.

RedChip investor conferences are a nationally known forum for emerging small-cap companies to present their stories before hundreds of retail brokers, institutional brokers, fund managers, portfolio managers, accredited investors, and research analysts whose disciplined focus towards the small-cap markets represents their core investment strategies. Sponsors of the event include NASDAQ OMX, Expos2, Vintage Filings, Vcorp Services, and Maxim Group LLC.

Company presentations will be webcast live via http://www.RedChip.com and available for 90 days. Participating investors will have the opportunity to meet one-on-one with the CEOs of presenting companies, and thousands of investors from across the United States, Europe and Asia are expected to watch the conference online at RedChip.com. In addition, RedChip TV(TM) will be on-site conducting interviews with CEOs, which will be archived for later viewing at RedChip.com.

The conference will feature companies from the following industries: Biotechnology, Healthcare Technology, Education, Telecommunications, Oil & Gas, Basic Materials, Consumer Services, Industrial Goods, Energy, Alternative Energy, Medical Devices, Specialty Chemicals, Precious Metals Mining, and more.

To date, companies scheduled to present include the following:

Acorn International, Inc. (NYSE:ATV - News); American Lorain Corporation (NYSE Amex:ALN); The Quantum Group, Inc. (NYSE Amex:QGP); Longwei Petroleum Investment Holding Ltd. (OTCBB:LPIH - News); Globalstar, Inc. (Nasdaq:GSAT - News)...continued: http://finance.yahoo.com/news/RedChip-Announces-34-pz-423967558.html?x=0&.v=4

Jazz and Transcept Pharmaceuticals on the Rise.

by: BioPharma Investor September 24, 2009 | about: JAZZ / TSPT

Two stocks of note in the past week are Jazz Pharmaceuticals (JAZZ) and Transcept Pharmaceuticals (TSPT). Last week, Transcept attended the BioCentury Thomson Reuters Newsmakers in the Biotechnology Industry Conference on Sept 16, 2009. Jazz was also in attendance. It seems this conference is playing out as stocks have risen in the last week.

Transcept's stock has risen from a low of 11.00 before the conference to its current trading at 13.75. This is a fast rising company in its first year on Nasdaq. Jazz has jumped from a low of 9.16 to its current trading value of 9.72. Jazz has been up from earlier news that the CEO purchased 150,000 shares on Sept. 1-2, 2009 at 7.21 a share (Jazz Pharmaceuticals Running On Buy From Smart Investor).

Although these stocks are running on Phase III highs I still like the buy option on both of these trades. NDA applications for Jazz have been received I see them reaching higher and higher levels into 2010. 3Q and 4Q should be good for both companies as sales should be ramping up. Transcept Pharma announced earlier from Glenn A. Oclassen, President and Chief Executive Officer commented, "Our overall staffing needs have been modified by the development of Intermezzo(R) to the point of NDA submission and our recently announced agreement with Purdue Pharmaceuticals to commercialize Intermezzo(R) in the United States.

Jazz Pharmaceuticals has completed a second Phase III pivotal clinical trial of JZP-6 on June 11, 2009. With positive results in the second study, the company anticipates submitting a New Drug Application for sodium oxybate for the treatment of fibromyalgia to the U.S. Food and Drug Administration by the end of 2009.

StreetInsiders market profile for Jazz Pharmaceuticals.

StreetInsiders market profile for Transcept Pharmaceuticals.

Jazz has four products in the pipeline for Fibromyalgia, Restless Leg Syndrome, Acute Repetitive Seizures, and Epilepsy/Bipolar Disorder. They are seeking partners for the lower clinical trials in phase I/II (Jazz Pipeline).

Transcept Pharmaceuticals, Inc. is a specialty pharmaceutical company focused on the development and commercialization of proprietary products that address important therapeutic needs in the field of neuroscience. Transcept has only one clinical products for insomnia patients who wake up in the middle of the night.

Intermezzo ® (zolpidem tartrate sublingual tablet) is a sublingual low dose formulation of zolpidem that has been developed for use as-needed for the treatment of insomnia when a middle of the night awakening is followed by difficulty returning to sleep. Phase 3 clinical trials have been completed for Intermezzo ® and, on September 30, 2008, Transcept submitted a New Drug Application to the U.S. Food and Drug Administration. Transcept anticipates action from the U.S. Food and Drug Administration (FDA) on its filed new drug application for Intermezzo ® on or before October 30, 2009.

Transept has a commercialization pact with Purdue Pharmaceuticals. Under the terms of the agreement, Purdue will pay Transcept near-term milestones that include an upfront cash payment of $25 million and an additional payment of up to $30 million based upon the timing of an FDA approval of Intermezzo®, which approval and payment are subject to review and acceptance by Purdue. Transcept is eligible to receive up to an additional $90 million upon reaching future milestones related to achievement of intellectual property and U.S. net sales targets.

Purdue will pay double-digit royalties to Transcept ranging up to the mid-twenty percent level on U.S. net sales of Intermezzo®. If Transcept elects to exercise its psychiatrist co-promotion option, Transcept will receive an additional double-digit royalty on the portion of U.S. net sales generated by psychiatrists. Under the agreement, Transcept can enter the market under the co-promotion option as early as the first anniversary of the commercial launch of Intermezzo® by Purdue.

Other Pharmaceuticals at the BioCentury Newsmakers Conference on September 16, 2009 where Enzon (ENZN), PDL BioPharma (PDLI), and Cougar Biotechnology (CGRB).

This conference went on in New York. San Fransciso also had a conference on their own with the BioPharma America 2009 presentation. Here is a list of presenters at the BioPharma America Conference: http://www.ebdgroup.com/bpa/prscomps.htm

http://seekingalpha.com/article/163183-jazz-and-transcept-pharmaceuticals-on-the-rise?

Six Double Digit Dividend Stocks Increasing Their Yields.

by: Dividends4Life September 25, 2009 | about: CIM / FLIC / HTS / LMT / MCD / TCAP

After Wednesday’s article High-Yield, High-Risk Dividend Stocks, I had hoped to feature a few high-yield stocks raising their dividends this week. Patiently I watched the news wire for some announcements that fit the bill, and it didn’t take long. As if they were waiting for the cue, three high-yield stocks recently announced increased cash dividends for their shareholders:

Chimera Investment (CIM) is a specialty finance company that invests in residential mortgage-backed securities (RMBS), residential mortgage loans, real estate-related securities and various other asset classes. Monday, CIM increased it quarterly dividend 50% to $0.12/share. The dividend is payable October 30, 2009 to common shareholders of record on October 1, 2009. The ex-dividend date is September 29, 2009. The current yield based on the new dividend is 11.82%.

Hatteras Financial (HTS) is an externally managed mortgage real estate investment trust (REIT) formed to invest in adjustable-rate and hybrid adjustable-rate single-family residential mortgage pass-through securities. Tuesday, the company raised its quarterly dividend 4.5% to $1.15/share. The dividend is payable on October 23, 2009, to stockholders of record on October 2, 2009, with an ex-dividend date of September 30, 2009. The current yield based on the new dividend is 13.94%.

Triangle Capital (TCAP) is a specialty finance company that provides customized financing solutions to lower middle market companies. Wednesday, the company bumped its quarterly dividend 2.5% to $0.41/share. The dividend is payable on October 22 to shareholders of record on October 8. The current yield based on the new dividend is 14.07%.

Though their yields are not double-digit, three additional companies provided double-digit dividend growth in their cash dividends:

The First of Long Island Corp. (FLIC) provides financial services through its wholly-owned subsidiary, The First National Bank of Long Island. Tuesday, the company increased its dividend 11% to $0.20/share. The dividend will be paid on October 9, 2009 to shareholders of record on October 2, 2009. To receive the dividend, you have to own the shares before September 30th. The current yield based on the new dividend is 2.98%.

Lockheed Martin (LMT) is the world’s largest military weapons manufacturer and is also a significant supplier to NASA and other government agencies. Thursday, the company raised its quarterly dividend 10.5% to $0.63/share. The dividend is payable Dec. 31, 2009 to holders of record as of the close of business on Dec. 1, 2009. The current yield based on the new dividend is 3.26%.

McDonald’s (MCD) is the leading global foodservice retailer with more than 32,000 local restaurants in more than 100 countries. Thursday, the company raised its quarterly dividend 10% to $0.55/share. The dividend is payable on December 15, 2009 to shareholders of record at the close of business on December 1, 2009.

MCD’s Chief Executive Officer Jim Skinner said,

So far in 2009 we’ve returned nearly $4.0 billion to shareholders through dividends and share repurchases, bringing total cash returned since the beginning of 2007 to about $15.5 billion. With today’s dividend increase, we expect to end the year near the high end of our three-year, $15 billion to $17 billion total cash return target.

The stock is a Dividend Aristocrat and has increased its dividend 33 consecutive years. The current yield based on the new dividend is 3.92%. [Analysis]

For long-term dividend investors, a high-yield is not the most important factor to look for, instead that honor belongs to consistently growing dividends. For stocks with a long string of consecutive dividend increases, see this list.

http://seekingalpha.com/article/163426-six-double-digit-dividend-stocks-increasing-their-yields?

Drug Makers in the Healthcare Reform Catbird Seat.

by: Rick Newman September 25, 2009 | about: BAX / BSX / MDT

As Congress gets closer to final healthcare-reform legislation, the central question remains murky: Who will foot the bill?

Figures contained in the $856 billion proposal by Democratic Sen. Max Baucus of Montana — which has emerged as the basis for a final compromise between the House and Senate — suggest that key parts of the healthcare industry are getting off easy. The Baucus bill would pay for itself in a number of ways, including taxes on some high-cost insurance plans, Medicare cost reductions, and cuts in federal benefits. It would also raise about $13 billion a year from fees paid by three industries: pharmaceuticals, health insurance, and medical devices.

Within each industry, the fees would be split among all companies according to their market share, so companies with the most business would pay the highest share of the industry fee, and vice versa. But the fees borne by each of the three industries follow a different logic. The pharmaceutical industry, for instance, would be required to pay a relatively low annual fee of $2.3 billion, even though it represents one of the biggest components—and the most profitable segment by far — within the overall healthcare industry. The medical device industry would pay a higher fee than Pharma, even though it's a smaller industry. And hospitals and other healthcare providers wouldn't pay any annual fee at all, even though that sector represents the biggest chunk of the overall healthcare industry, with more than twice the revenue of all pharmaceutical firms combined.

To see how the fees apportioned by the Baucus plan compare to the relative size and profitability of each industry, I analyzed data provided by research firm Capital IQ, a division of Standard & Poor's. Capital IQ determined the total revenue and net income for three groups of companies that approximate the three industries that would pay an annual fee, as the Baucus plan describes them. Then it aggregated the figures to determine each industry's size as a portion of all three combined. Here's how those breakdowns compare with the burden placed on each industry by the Baucus plan:

The data suggest that the pharmaceutical companies would be underpaying relative to their size, while device manufacturers would be overpaying. The $6.7 billion fee paid by health insurers would be comparable to the size of that industry, as measured by revenue. There are different ways to measure the size of each industry — since some companies are conglomerates that don't fall squarely into a single category — but Capital IQ's numbers are similar to other estimates.

The deal looks even better for pharmaceutical companies when the fees are measured as a portion of profits. Drugmakers had a combined net income of about $44 billion over the past 12 months, according to Capital IQ, so a $2.3 billion annual fee would represent about 5.2 percent of industry profits. The medical device industry earned about $5.1 billion over the past 12 months, which means a $4 billion annual fee would represent a whopping 78 percent of profits. Health insurers earned $11.3 billion, so $6.7 billion in fees would equate to 59 percent of profits.

There's more to the numbers. A Baucus spokesperson explains that other provisions of the bill would add to the amount various industries would contribute. Pharmaceutical companies, for example, have agreed to offer 50% discounts on name-brand drugs for Medicare recipients who have exhausted their drug coverage and must pay out of pocket. Combined with the annual fee, that adds up to an $8 billion contribution from drugmakers, or 18% of profits. Healthcare providers aren't assessed an annual fee in the bill, but other concessions add up to about $15.5 billion a year. With an annual net profit of $18.7 billion for hospitals and other healthcare providers, that would add up to 83% of net income. Concessions by the insurance industry would further reduce profits there, too, but the numbers are hard to quantify. There are no additional concessions by device manufacturers.

If the Baucus plan or something similar becomes law, more Americans will end up with health coverage, effectively enlarging the market and creating new business for most healthcare companies. So new fees that cut into profits could be offset by new revenue. Hospitals could reach their targets partly by cutting costs—a key goal of the bill — rather than paying fees. The numbers could also change as the bill gets modified and lobbyists work their black magic.

Still, the nature of the pain-sharing reflects the hardball tactics adopted by all sides in this bare-knuckles battle. When President Obama began pushing for healthcare reform after taking office in January, the pharmaceutical industry made early concessions and agreed to back the effort in exchange for a set annual contribution and a say in the crafting of the legislation. Other industries were less cooperative—and may now be paying the price.

Of course, the characters running all these industries are shrewd businesspeople, and their stance on reform is influenced by the degree to which they can pass on new costs to consumers or other customers throughout the supply chain. Prescription drugs are closely monitored by watchdog groups, the insurers that pay for them, and the consumers who use them and there's relentless pressure to lower prices. The pharmaceutical industry already has one of the highest profit margins in all of capitalism, so industry leaders may have decided they can afford a relatively minor across-the-board cut in profitability in exchange for reforms that ease the long-term pressure to slash prices—and add new customers.

Manufacturers of medical devices, on the other hand — which include companies like Baxter International (BAX), Medtronic (MDT), and Boston Scientific (BSX) — seem teed up to take a big hit. The industry's trade group, AdvaMed, has said it supports reform. But unlike the trade groups that represent health insurers and drug companies, AdvaMed has strongly protested the annual fee its industry would pay under the Baucus plan. Medical devices typically get sold deeper in the supply chain, further from the eyes of consumers and regulators. So instead of cooperating with reformers, industry leaders may be rolling the dice and hoping they'll be able to pass along new fees to their customers — or just gambling that healthcare reform will never happen at all. Intense opposition is certainly coming from somewhere.

http://seekingalpha.com/article/163475-drug-makers-in-the-healthcare-reform-catbird-seat?

BioMed News Bytes: NicOx, Allos, Pressure BioSciences, YM BioSciences. by: Mike Havrilla September 25, 2009 | about: ALTH / IGK / NICXF.PK / PBIO / YMI

On 5/19/09, NicOx (NICXF.PK) announced that quality of life and utility results from its first Phase 3 clinical trial for naproxcinod were presented at the International Society For Pharmacoeconomics and Outcomes Research Annual International Meeting in Orlando, FL. Naproxcinod is a novel type of anti-inflammatory agent, which completed a Phase 3 clinical program last year in patients with osteoarthritis.

The drug is designed to have an improved side effect profile (including a neutral effect on blood pressure) as compared to a standard dose of the widely used NSAID drug naproxen. Naproxcinod has completed three pivotal Phase 3 studies with positive results. On 9/25/09, NicOx submitted a NDA for naproxcinod to the FDA for an estimated decision date of 7/25/10 for a standard, 10-month review.

On 3/25/09, Allos Therapeutics (ALTH) filed a NDA with the FDA for Folotyn (pralatrexate injection) in the treatment of patients with relapsed or refractory peripheral T-cell lymphoma (PTCL). ALTH received a priority (six-month) review designation on 5/26/09 with a PDUFA decision date of 9/24/09 for a final decision by the FDA. PTCL comprises a biologically diverse group of hematologic malignancies that typically has a worse prognosis than other types of lymphoma and is less responsive to traditional chemotherapy regimens.

On 9/2/09, ALTH the Oncologic Drugs Advisory Committee (ODAC) of cancer experts voted 10-4 that the Company's drug would likely benefit patients with PTCL. On 9/25/09, ALTH announced that the FDA granted accelerated approval for Folotyn for use as a single agent for the treatment of patients with relapsed or refractory PTCL as the first and only drug approved by the FDA for this indication. In connection with the accelerated approval, ALTH has agreed to undertake additional clinical studies to further verify and describe the clinical benefit of FOLOTYN in patients with T-cell lymphoma.

On 9/25/09, YM BioSciences (YMI) announced operating results and issued an update on its clinical development programs. Nimotuzumab (nimo) is being advanced globally by a network of cooperative relationships with 32 Phase 2 and 3 clinical trials ongoing, 11 of which are being conducted by YM's majority owned subsidiary, CIMYM BioSciences or its licensees.

Daiichi Sankyo and Kuhnil Pharma are currently collaborating on a Phase 2 randomized, open-label trial they are conducting that is evaluating nimo plus irinotecan compared to irinotecan alone in patients with advanced or recurrent gastric cancer refractory to 5-FU-containing regimens which is designed to complete recruitment in calendar 2009. Daiichi has also launched a Phase 2 trial in first-line NSCLC bringing to three the number of NSCLC indications being investigated by YM’s direct consortium.

Randomized, Phase 2, double-blind trials in brain metastases from non-small cell lung cancer (NSCLC) and in NSCLC patients ineligible for radical chemotherapy were initiated in Canada; recruitment commenced in March 2009 for NSCLC and in September for the brain metastases trial. A Phase II, second-line, single-arm trial in children with progressive diffuse intrinsic pontine glioma (DIPG) is ongoing at multiple sites in the US, Canada, and Israel.

Oncoscience AG reports that it continues to recruit for a Phase 3 trial of nimo in adult glioma and a Phase II/III trial in pancreatic cancer.

Innogene Kalbiotech (IGK) reported marketing approval in the Philippines and Indonesia, bringing to 21 the number of countries that are now reported as having approved the drug for sale in specific indications. In January 2009, the National Cancer Centre of Singapore announced that it was launching a worldwide Phase 3, 710-patient trial of nimo in the adjuvant setting in head and neck cancer in cooperation with IGK. This trial is in addition to the on-going investigator-initiated Phase 2 trial in locally advanced head and neck cancer and the initiation of a Phase 2 trial in cervical cancer.

YM has received a license from the US Department of the Treasury's Office of Foreign Assets Control (OFAC) to further develop its lead product, nimo, for patients in the U.S. YM's first priority is discussion with the FDA on its two IND submissions to include US citizens in the randomized, double-blind Phase 2 trial of nimo in NSCLC patients ineligible for radical chemotherapy and the parallel Phase 2 trial in patients with brain metastases from NSCLC, both of which YM initiated in Canada during the 2009 fiscal year. Development plans may also include extending one of the Phase 3 trials being conducted worldwide into the US, such as the multinational 710-patient Phase 3 trial of nimo in the adjuvant setting in head and neck cancer.

YM also continues to prepare its second late-stage product, AeroLEF (aerosolized liposome-encapsulated fentanyl), for further development internationally. After consulting with regulatory bodies in Europe and Canada, the Company is now determining the optimal clinical path forward and conducting discussions with prospective partners around the Phase 3 strategy.

On 9/25/09, Pressure BioSciences (PBIO) announced the commercial release of ProteoSolve-CE NATIVE and ProteoSolve-CE STRINGENT, two novel, pressure cycling technology (PCT) dependent kits for the extraction of proteins from the nematode ("worm") Caenorhabditis elegans ("C. elegans"). The two kits contain proprietary reagents, consumable processing containers ("PULSE Tubes"), and instructions for use, and are intended to be used with the Company's patented PCT Sample Preparation System.

C. elegans is one of the most widely used model organisms in laboratory research today. It is an ideal study animal because it is small, not complex, easy to grow and maintain in the lab, and has a short and very predictable life cycle. Importantly, biological information learned from studying this worm has been shown to be directly applicable to more complex organisms, such as humans. Click here for my overview article from last week on PBIO, which also includes a CEO video interview.

Disclosure: No positions.

RMBS: Technical Analysis Video.

Testing critical support, could the market see another reversal in trend and rally? My thoughts and analysis in video format follow.

Link to Video: http://timelesswealth.net/ta/rmbs2.html

RMBS: Technical Analysis Video.

Testing critical support, could the market see another reversal in trend and rally? My thoughts and analysis in video format follow.

Link to Video: http://timelesswealth.net/ta/rmbs2.html

Rambus Technical Analysis Video.

Testing critical support, could the market see another reversal in trend and rally? My thoughts and analysis in video format follow.

Link to Video: http://timelesswealth.net/ta/rmbs2.html

To clarify something I released in the past: Europlasma is not an exclusive partner to Wireless Age Communications, Inc. in the United States, but specifically in Canada, hence the Port Hope, Ontario project.

ALN: American Lorain Corporation, profitable, undervalued, Small-Cap China stock.

Full Report: http://timelesswealth.net/alerts/alert_09242009.html

TimelessWealth.net issues undervalued investment idea with American Lorain Corporation: ALN ($2.57).

Dear Subscriber,

TimelessWealth.net has issued an undervalued investment idea with American Lorain Corporation (ALN), a Small Cap China stock. The Small Cap China Index (HAO) has appreciated 68% year-to-date, representing significant growth among companies of this class. After meeting listing requirements, American Lorain Corp. commenced trading on the American Stock Exchange (AMEX) on September 8th, 2009.

Among the thirty-four (34) emerging small cap inductees, American Lorain Corp. was invited to present at the 2009 RedChip New York Equities Conference on September 30th and October 1st, 2009. For over 17 years, RedChip has been dedicated to “Discovering Tomorrow's Blue Chips Today™.” RedChip's long history of success includes research coverage on Starbucks™, Nike™, MarketWatch.com™, Daktronics™, and many other companies before they were Blue Chips...continued.

You know what they say..."timing is everything"...and now may very well be WLSA's time, imho.

most penny stocks have NO fundamentals to speak of. That is a truly useless pursuit.

I agree with you in that sense, however, most investors here have found undervalued characteristic that they feel comfortable exposing their portfolios to. Since Fundamental Analysis would not work without something to analyze (like a balance sheet), the market has treated this one speculatively. However, that speculation is what separates true investors willing to dig deep into a company to find one that may potentially yield a high ROI, with those looking for a quick 'bang for their buck'. Speculation drives the market. Value investors will create serious movement once those fundamentals are reported through financial statements. I call it the risk vs. reward concept. Research is a must.

Simmonds has begun scheduling lunch with brokers, the first of which (if I recall correctly) is this afternoon. Another thing he mentioned were terms to the Connecticut deal favoring Wireless Age Communications, Inc. more so than before; he is leaving for Connecticut this Wednesday. I am sure we will hear more on these events soon...

PED: Natural Gas: America's Energy Salvation.

by: Joseph Shaefer September 06, 2009

Natural gas will be America’s energy salvation.

If you think solar, biomass, wind, lithium ion-powered, ocean thermal, currents and tides, and even tried-and-true geothermal and hydroelectric will somehow in the aggregate equal natural gas as a share of energy production, read here and here.

It’s time we stopped hiding our heads in the sand about today’s energy problems while spending / wasting tens of billions of dollars on taxpayer-funded grants, incentives and subsidies for tomorrow’s solutions. We need – and have readily available – an American source of relatively clean energy today for today’s needs, if only the politicians would stop spending on pork and get the hell out of the way of private industry that is trying to provide this source: clean-burning natural gas.

We pay much more for the electricity to power and light our homes and offices, the coal, heating oil or gas to heat our homes, and the gasoline to fill our automobiles, than we typically recognize.

We pay once to the utilities or at the pump, and once more when our taxes are withheld from our paychecks. Big government pork for ethanol subsidies, solar subsidies, biomass subsidies, and every other kind of can’t-stand-on-its-own-economics power are costing us, not just in monetary terms but in time value – we are looking so far down the road we don’t even see the 30-foot drop-off right in front of us. Think $4 a gallon for gasoline is high? Add in the subsidies your tax dollars are diverted to for a $0 return and you’re probably paying closer to $6 a gallon.

I say remove the subsidies, credits, and grants from all sources of energy. Big oil gets no special allowances for depletion. That’s the industry you chose, bubbas. You knew it was a wasting asset when you decided to enter the business. Same for natural gas and coal companies. And the same for nuclear, wind, solar, biomass, et al.

Clean renewable energy that is not a wasting asset remains the Holy Grail of energy production. If we shut off the spigot of vote-buying that comes from dispensing grants and subsidies, energy companies will still seek ways to harness the power of the sun and the wind. As long as the sun still shines, those who can turn this diffuse energy into a concentrated form will make money. But I’m tired of effectively paying $6 a gallon for gasoline when alternatives exist that are being ignored. Why are they being ignored? Mostly, so some people can feel morally superior while they freeze in the dark. Me. I’m not into moral superiority. I’d rather have a clean, well-lit place to work and live than to feel smug about my energy “consciousness.”

I’d like to see clean solar and wind as much as the next guy, but I won’t wear rose-colored glasses. I can’t ignore the fact that, after 30 years and $30 billion in subsidies, wind now meets 7/10 of 1% of US energy needs (about the same as when farmers used windmills 150 years ago) and solar is 12/100 of 1%. Let’s round those up to 1%. There are 1,440 minutes in a day. Are you willing to have your lights, air conditioner, computer, stove and every other appliance and convenience on just 14.4 minutes a day? Welcome to Baghdad.

Why Natural Gas

Natural gas is the second-most abundant fossil fuel in America. Coal is first. We are the Saudi Arabia of coal worldwide. China and India together don’t have as much coal as the US, which has 28% of the entire world’s reserves. But coal is dirty. Lots of for-profit firms are doing breakneck research to clean it up, but it’s – currently – dirty.

So is our choice dirty polluting coal or 14.4 minutes of power a day? Of course not. There’s imported oil. However, with the exception of tar-sands oil from Canada, when you add, to the $70 a barrel oil costs when ready for export, the transportation costs, the cost of keeping the Straits of Hormuz open, the costs of foreign wars to assure the continuing supply, the cost of the inevitable oil spills from time to time, and the foreign aid and sweetheart deals our nation makes to keep tyrants, misogynists, and perverts atop otherwise-shaky regimes, the true cost of oil is probably already $200-$300 a barrel.

That leaves natural gas as the only fuel we actually use in abundance and have in abundance right now, today, this minute.

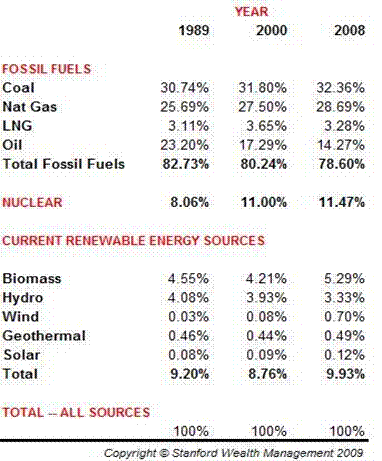

I created the chart below from the raw numbers of quadrillions of BTUs reported by the Department of Energy’s Energy Information Administration of the current mix of fuels used in the United States to produce energy.

Journalists, however, are more enamored of something new! and different! and therefore write reams on renewables and virtually nothing about something old and boring (but tried and true) like fossil fuels, so it’s easy to believe renewables constitute a larger proportion than they really do. Note, for instance, in the previous chart, the less-than-amazing ascent of heavily-subsidized solar from 8/100 of 1% 20 years ago to 12/100 of 1% today. That’s not to denigrate solar or to “wish” that it couldn’t have gone from 8/100 to 8% or 100%. But we must deal in facts if we are to ever wean ourselves from foreign oil and stop walking on eggshells around despots and ideological and religious fanatics.

HERE’s “Why Natural Gas”

1. According to Oil & Gas Weekly and the Energy Information Administration we have upwards of 100 years of natural gas remaining in the US at current rates of usage.

2. The estimate of proven reserves leapt *35%* in just the past year (creating downward pressure on prices in the short term.) No surprise to me. Every year of my 40 years in this business, I’ve been hearing about peak oil in some variation or another. “The world is running out of fossil fuels! We’re all going to freeze to death! We must subsidize unproven technologies to save us from Armageddon!”

What a bunch of hooey. Every year since the first Cassandra screamed this nonsense in my ear, we have increased our estimates of proven reserves. As technology allows us to find and produce gas from previously unknown or inaccessible formation, we’ll find even more.

3. Add Canada’s natural gas to the mix, since Canada is our biggest trading partner and the US is their closest (thus cheapest-to-transport-to) customer, and they have an abundance of nat-gas beyond the needs of their population. And since liquefying natural gas is expensive and potentially dangerous, it’s best to pipeline it from close-by fields rather than ship it liquefied across the world’s oceans.

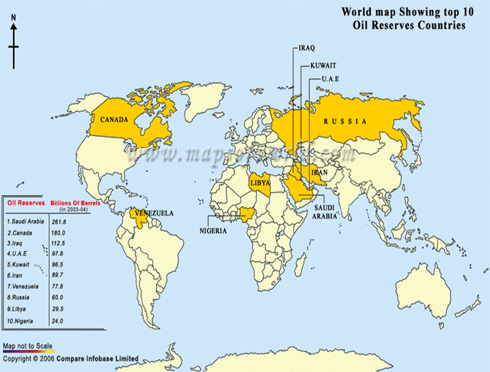

4. If we use more U.S. natural gas, we can tell the likes of Saudi Arabia, Iran, Iraq, Russia, Nigeria and Venezuela “no thanks” to their bribery, corruption and fleecing.

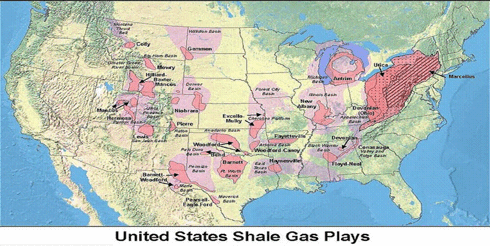

Take a look at the map below (click to enlarge). These are our now-known, proven shale gas reserves. Now note how close most are to population centers...

Okay, But Why NOW?

In previous articles, I began making the case for both nuclear and natural gas. I still believe both offer remarkably good investment opportunities in the months, years and decades ahead -- but I think natural gas will be the first to benefit. Why?

1. People are beginning to realize, in spite of Al Gore’s conflict-of-interest hawking of renewables he’s invested in, that nat-gas is the cleanest burning fossil fuel, is available in quantity right here at home, and is used to heat our homes, cook our food, power the electricity that turns on our lights and fuel the 7 million natural gas vehicles currently in use around the world.

2. The glut in supply of natural gas is both temporary and price-sensitive. The glut was created by new production coming online from shale gas plays. But at today’s prices, those wells are being shuttered. What company could stay in business if they were to sell gas at $2.56 per million BTUs (MMBtu) when it costs them $5.15 per MMBtu to get it out of the ground?

3. The natural gas glut is not only price-sensitive, it is seasonal, as well. As the winter season cranks up over the coming months, utilities will need to produce more natural gas-generated heat. As the days grow longer, we’ll turn our lights on earlier in the day and, if this year is like every other, we’ll settle in, turn up the electric blankets, play more electronic games, and cook more at home – primarily benefiting nat-gas and coal as the two primary generators of electricity in this country. (With nuclear close behind, the three of them accounting for 90% of our electrical generating fuel sources. Add hydroelectric and that leaves just 4% generated by oil, biomass, vegetable oil, solar, wind, etc.)

I believe natural gas is unlikely to remain depressed.

This is a seasonal play that hasn't changed in 50 years, yet the media always project declines or rises -- in any commodity, trend or stock -- as if they were linear. The market, however, is cyclical, not linear...

4. The Farmers' Almanac is predicting a cold winter. The squirrels, chipmunks and birds in my large yard seem to agree. All are scurrying about hiding food from each other earlier than I’ve ever seen. The Almanac predicts numbing cold from the Rocky Mountains to the Appalachians, with milder weather on the coasts. The National Weather Service is calling for a warmer-than-normal winter because of El Nino. In my experience, the animals get it right more often than the humans…

5. Natural gas-fired plants are currently operating at less than 50% capacity. If this administration and this country is really serious about cutting carbon emissions we will turn to natural gas now, not when two guys in their garage find the solar Holy Grail.

Next week, I will write an article on the three E&P (exploration and production) firms I believe will benefit most from an increase in America’s reliance upon “home-grown,” abundant, and cheap natural gas. I’ll also review what I think are the smartest natural gas pipelines for both income and growth.

If you can’t wait until then, here’s an ETF that I believe accurately covers the whole industry: the First Trust ISE-Revere Natural Gas Index Fund (FCG). I know and respect some of the principals at Revere (“Revere Data”) and am quite familiar with their methodology and hierarchy that creates a product- and service-based classification system to map where and how companies interact and compete.

FCG would be a good adjunct to the pipelines mentioned above in that it selects companies on the exploration and production side of the business. It selects only the top 30 stocks based upon an internal ranking system, then rebalances on a quarterly basis. Be aware that this methodology will add a level of “active” management versus the passive nature of many ETFs. That might be good, it might be bad, but I see FCG as a great way to give us broad exposure to the entire industry.

PED: Natural Gas: America's Energy Salvation.

by: Joseph Shaefer September 06, 2009

Natural gas will be America’s energy salvation.

If you think solar, biomass, wind, lithium ion-powered, ocean thermal, currents and tides, and even tried-and-true geothermal and hydroelectric will somehow in the aggregate equal natural gas as a share of energy production, read here and here.

It’s time we stopped hiding our heads in the sand about today’s energy problems while spending / wasting tens of billions of dollars on taxpayer-funded grants, incentives and subsidies for tomorrow’s solutions. We need – and have readily available – an American source of relatively clean energy today for today’s needs, if only the politicians would stop spending on pork and get the hell out of the way of private industry that is trying to provide this source: clean-burning natural gas.

We pay much more for the electricity to power and light our homes and offices, the coal, heating oil or gas to heat our homes, and the gasoline to fill our automobiles, than we typically recognize.

We pay once to the utilities or at the pump, and once more when our taxes are withheld from our paychecks. Big government pork for ethanol subsidies, solar subsidies, biomass subsidies, and every other kind of can’t-stand-on-its-own-economics power are costing us, not just in monetary terms but in time value – we are looking so far down the road we don’t even see the 30-foot drop-off right in front of us. Think $4 a gallon for gasoline is high? Add in the subsidies your tax dollars are diverted to for a $0 return and you’re probably paying closer to $6 a gallon.

I say remove the subsidies, credits, and grants from all sources of energy. Big oil gets no special allowances for depletion. That’s the industry you chose, bubbas. You knew it was a wasting asset when you decided to enter the business. Same for natural gas and coal companies. And the same for nuclear, wind, solar, biomass, et al.

Clean renewable energy that is not a wasting asset remains the Holy Grail of energy production. If we shut off the spigot of vote-buying that comes from dispensing grants and subsidies, energy companies will still seek ways to harness the power of the sun and the wind. As long as the sun still shines, those who can turn this diffuse energy into a concentrated form will make money. But I’m tired of effectively paying $6 a gallon for gasoline when alternatives exist that are being ignored. Why are they being ignored? Mostly, so some people can feel morally superior while they freeze in the dark. Me. I’m not into moral superiority. I’d rather have a clean, well-lit place to work and live than to feel smug about my energy “consciousness.”

I’d like to see clean solar and wind as much as the next guy, but I won’t wear rose-colored glasses. I can’t ignore the fact that, after 30 years and $30 billion in subsidies, wind now meets 7/10 of 1% of US energy needs (about the same as when farmers used windmills 150 years ago) and solar is 12/100 of 1%. Let’s round those up to 1%. There are 1,440 minutes in a day. Are you willing to have your lights, air conditioner, computer, stove and every other appliance and convenience on just 14.4 minutes a day? Welcome to Baghdad.

Why Natural Gas

Natural gas is the second-most abundant fossil fuel in America. Coal is first. We are the Saudi Arabia of coal worldwide. China and India together don’t have as much coal as the US, which has 28% of the entire world’s reserves. But coal is dirty. Lots of for-profit firms are doing breakneck research to clean it up, but it’s – currently – dirty.

So is our choice dirty polluting coal or 14.4 minutes of power a day? Of course not. There’s imported oil. However, with the exception of tar-sands oil from Canada, when you add, to the $70 a barrel oil costs when ready for export, the transportation costs, the cost of keeping the Straits of Hormuz open, the costs of foreign wars to assure the continuing supply, the cost of the inevitable oil spills from time to time, and the foreign aid and sweetheart deals our nation makes to keep tyrants, misogynists, and perverts atop otherwise-shaky regimes, the true cost of oil is probably already $200-$300 a barrel.

That leaves natural gas as the only fuel we actually use in abundance and have in abundance right now, today, this minute.

I created the chart below from the raw numbers of quadrillions of BTUs reported by the Department of Energy’s Energy Information Administration of the current mix of fuels used in the United States to produce energy.

Journalists, however, are more enamored of something new! and different! and therefore write reams on renewables and virtually nothing about something old and boring (but tried and true) like fossil fuels, so it’s easy to believe renewables constitute a larger proportion than they really do. Note, for instance, in the previous chart, the less-than-amazing ascent of heavily-subsidized solar from 8/100 of 1% 20 years ago to 12/100 of 1% today. That’s not to denigrate solar or to “wish” that it couldn’t have gone from 8/100 to 8% or 100%. But we must deal in facts if we are to ever wean ourselves from foreign oil and stop walking on eggshells around despots and ideological and religious fanatics.

HERE’s “Why Natural Gas”

1. According to Oil & Gas Weekly and the Energy Information Administration we have upwards of 100 years of natural gas remaining in the US at current rates of usage.

2. The estimate of proven reserves leapt *35%* in just the past year (creating downward pressure on prices in the short term.) No surprise to me. Every year of my 40 years in this business, I’ve been hearing about peak oil in some variation or another. “The world is running out of fossil fuels! We’re all going to freeze to death! We must subsidize unproven technologies to save us from Armageddon!”

What a bunch of hooey. Every year since the first Cassandra screamed this nonsense in my ear, we have increased our estimates of proven reserves. As technology allows us to find and produce gas from previously unknown or inaccessible formation, we’ll find even more.

3. Add Canada’s natural gas to the mix, since Canada is our biggest trading partner and the US is their closest (thus cheapest-to-transport-to) customer, and they have an abundance of nat-gas beyond the needs of their population. And since liquefying natural gas is expensive and potentially dangerous, it’s best to pipeline it from close-by fields rather than ship it liquefied across the world’s oceans.

4. If we use more U.S. natural gas, we can tell the likes of Saudi Arabia, Iran, Iraq, Russia, Nigeria and Venezuela “no thanks” to their bribery, corruption and fleecing.

Take a look at the map below (click to enlarge). These are our now-known, proven shale gas reserves. Now note how close most are to population centers...

Okay, But Why NOW?

In previous articles, I began making the case for both nuclear and natural gas. I still believe both offer remarkably good investment opportunities in the months, years and decades ahead -- but I think natural gas will be the first to benefit. Why?

1. People are beginning to realize, in spite of Al Gore’s conflict-of-interest hawking of renewables he’s invested in, that nat-gas is the cleanest burning fossil fuel, is available in quantity right here at home, and is used to heat our homes, cook our food, power the electricity that turns on our lights and fuel the 7 million natural gas vehicles currently in use around the world.

2. The glut in supply of natural gas is both temporary and price-sensitive. The glut was created by new production coming online from shale gas plays. But at today’s prices, those wells are being shuttered. What company could stay in business if they were to sell gas at $2.56 per million BTUs (MMBtu) when it costs them $5.15 per MMBtu to get it out of the ground?

3. The natural gas glut is not only price-sensitive, it is seasonal, as well. As the winter season cranks up over the coming months, utilities will need to produce more natural gas-generated heat. As the days grow longer, we’ll turn our lights on earlier in the day and, if this year is like every other, we’ll settle in, turn up the electric blankets, play more electronic games, and cook more at home – primarily benefiting nat-gas and coal as the two primary generators of electricity in this country. (With nuclear close behind, the three of them accounting for 90% of our electrical generating fuel sources. Add hydroelectric and that leaves just 4% generated by oil, biomass, vegetable oil, solar, wind, etc.)

I believe natural gas is unlikely to remain depressed.

This is a seasonal play that hasn't changed in 50 years, yet the media always project declines or rises -- in any commodity, trend or stock -- as if they were linear. The market, however, is cyclical, not linear...

4. The Farmers' Almanac is predicting a cold winter. The squirrels, chipmunks and birds in my large yard seem to agree. All are scurrying about hiding food from each other earlier than I’ve ever seen. The Almanac predicts numbing cold from the Rocky Mountains to the Appalachians, with milder weather on the coasts. The National Weather Service is calling for a warmer-than-normal winter because of El Nino. In my experience, the animals get it right more often than the humans…

5. Natural gas-fired plants are currently operating at less than 50% capacity. If this administration and this country is really serious about cutting carbon emissions we will turn to natural gas now, not when two guys in their garage find the solar Holy Grail.

Next week, I will write an article on the three E&P (exploration and production) firms I believe will benefit most from an increase in America’s reliance upon “home-grown,” abundant, and cheap natural gas. I’ll also review what I think are the smartest natural gas pipelines for both income and growth.

If you can’t wait until then, here’s an ETF that I believe accurately covers the whole industry: the First Trust ISE-Revere Natural Gas Index Fund (FCG). I know and respect some of the principals at Revere (“Revere Data”) and am quite familiar with their methodology and hierarchy that creates a product- and service-based classification system to map where and how companies interact and compete.

FCG would be a good adjunct to the pipelines mentioned above in that it selects companies on the exploration and production side of the business. It selects only the top 30 stocks based upon an internal ranking system, then rebalances on a quarterly basis. Be aware that this methodology will add a level of “active” management versus the passive nature of many ETFs. That might be good, it might be bad, but I see FCG as a great way to give us broad exposure to the entire industry.

PED: There are x number of reasons why to avoid a given stock, one key reason why the market will re-evaluate and potentially appreciate this oil & natural gas producer. Natural Gas has risen since early Septemeber, PED has lagged behind thus far. Based on this movement in the market, PED may experience a stronger than expected fourth quarter with Nat. Gas prices on the rise. Natural Gas is expected to rally into 2010 according to a large collection of analyst reports. My synopsis: while many have speculated that Natural Gas will bottom in October, somebody is already accumulating in the market for the inevitable, hence the price appreciation. In other words, we are staring at a potential bottom with this micro-cap, Natural Gas producer.

PED: There are x number of reasons why to avoid a given stock, one key reason why the market will re-evaluate and potentially appreciate this oil & natural gas producer. Natural Gas has risen since early Septemeber, PED has lagged behind thus far. Based on this movement in the market, PED may experience a stronger than expected fourth quarter with Nat. Gas prices on the rise. Natural Gas is expected to rally into 2010 according to a large collection of analyst reports. My synopsis: while many have speculated that Natural Gas will bottom in October, somebody is already accumulating in the market for the inevitable, hence the price appreciation. In other words, we are staring at a potential bottom with this micro-cap, Natural Gas producer.

Excellent, and yourself?

My thoughts were bearishness from a technical perspective, however, I hadn't examined the situation any further than that.

Want to read all about it online? It may cost you.

Newspapers expected to open Internet toll booths this fall as publishers test online fees

By Michael Liedtke, AP Business Writer

On Sunday September 20, 2009, 8:10 pm EDT

SAN FRANCISCO (AP) -- With their advertising revenue drying up, newspaper publishers spent much of the spring and summer debating whether to cut off free online access to some of the material they run in their shrinking print editions.

It looks like the talk will turn to action this fall, when some large newspapers are expected to put up Internet toll booths.

They'll be testing readers' willingness to pay for information and entertainment that mostly has been given away online for the past 15 years. That happened largely because most publishers could afford to subsidize their Web sites with profits from their print franchises. But now those profits have crumbled, just as the prices for online ads are tumbling, too.

A recent study by the American Press Institute found 58 percent of the responding newspapers are considering online fees. Of that group, 22 percent expect to introduce the fee before the end of the year. The findings drew upon 118 interviews of newspaper executives in the U.S. and Canada.

The free-to-fee transition likely will occur in tentative steps rather than bold leaps that would lock all online content behind a pay gate. Publishers are taking this cautious approach because they are still trying to devise online payment plans that will generate more revenue without alienating too many of their readers.

For instance, the Pittsburgh Post-Gazette, a newspaper with a weekday circulation of about 206,500, recently launched a Web site that includes coverage and commentary on sports, politics and entertainment that isn't in its printed product or free online edition. The service costs $36 annually or $3.99 per month.

Other newspapers that have talked up subscription plans remain reticent. Newsday of Long Island, N.Y., still hasn't rolled out fees for its Web site, even though the newspaper's owner, Cablevision Systems Corp., said it was going to do so this summer. Newsday spokesman Paul Fleishman declined to comment.

The conundrum facing publishers: It's hard to figure out how much, if anything, readers will be willing to pay. Internet search engines and digital communication tools such as Twitter and Facebook ensure people still will be able to find and share plenty of free content.

But running totally free sites hasn't been paying off for most newspapers. Even before the online market began to slump this year, Web ads were generating only a small fraction of the revenue that print ads do. The disparity has made publishers realize they need more ways to make money on the Internet, but few of them have been able to figure out how.

"This is like a four-dimensional chess game. It's really complex," said former newspaper editor Alan Mutter, who is now an industry consultant when he isn't writing "Reflections of a Newsosaur," a free blog.

The Associated Press also has been part of the online fee movement. The not-for-profit cooperative, which is owned by newspapers, is setting up a system that will track the usage of its stories. It's a crucial piece of a plan that could improve the AP's ability to run ads next to news stories and perhaps even lead the AP to charge readers to see major scoops or other "premium" content.

"The value of content has to rise," said Tom Curley, the AP's chief executive. "We are all looking how to make that happen."

Even as newspapers mull just how much to commit to charging readers, a competition is already brewing to provide the technology to enable it.

Four of the world's largest technology companies -- Google Inc., Microsoft Corp., IBM Corp. and Oracle Corp. -- have expressed an interest in developing an online payment system for publishers. Mutter also has been promoting his own approach to Internet fees, a concept he calls ViewPass.

Separately, more than 1,000 newspapers and magazines have signed nonbinding letters of intent to join an Internet fee system being assembled by Journalism Online LLC. It intends to begin collecting money on behalf of publishers before winter.

Backed by former leaders from Court TV and The Wall Street Journal, Journalism Online wants to run the cash register for a digital news smorgasbord. Readers will be able to buy stories from a wide range of participating publishers without having to repeatedly provide their credit card numbers and other personal information at each Web site. The content would be distributed on the Web and electronic reading devices, with each publisher dictating its own terms. As a commission, Journalism Online plans to keep 20 percent of the revenue collected through its system.

Although he isn't jumping on board with Journalism Online, News Corp. Chairman Rupert Murdoch is sold on online fees.

News Corp. already owns the newspaper industry's most successful Internet subscription model in The Wall Street Journal, with more than 1 million customers who pay for online access. The annual rates vary from $103 for an online-only subscription to $140 for a package that includes delivery of the print edition too. Now, Murdoch hopes to make online fees pay off for his other publications, which include the New York Post and The Times of London. Murdoch hasn't provided a timeline or specifics about his plans, however.

The New York Times is considering charging online readers a membership fee, with more details promised in the fall. It's a road the newspaper has been down before, only to reverse course after management concluded that the online subscription it required to read the Times' top columnists was crimping its Internet ad sales. The subscription service, which cost $50 per year, was scrapped in 2007 after a two-year run. It had 221,000 customers when the Times tore down the toll booth.