News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Hi Everyone,

Just wanted to introduce myself! My name is Rob and I am so glad I finally joined this site! I have been reading posts here for a while and everyone seems like a real knowledgeable bunch ! A little bit about me: I run a Website for Rent to Own Homes (Lease2Buy.com), and I've been in the field for over 10 years. It amazes me how much this field keeps evolving, and I am so grateful to see the larger market turning around!!

HLXH is on the move - 2.8 float housing stock, with solid 2011 financials expected next week.

Less Than 24 Hours After My Warning Of Extensive Legal Risk In The Banking Industry, The Massachusetts Supreme Court Drops THE BOMB!

Reggie Middleton

Jan 11, 2011

The day after I posted "As JP Morgan & Other Banks Legal Costs Spike, Many Should Ask If It Was Not Obvious Years Ago That This Industry May Become The "New" Tobacco Companies" http://boombustblog.com/reggie-middleton/2011/01/06/as-jp-morgan-other-banks-legal-costs-spike-many-should-ask-if-it-was-not-obivous-years-ago-that-this-industry-may-become-the-new-tobacco-companies/ wherein I made clear my opinion that the legal and litigation risks that the banking industry faces is woefully underestimated, the Massachusetts Land Court Decision that invalidates foreclosures based on post sale assignments was up held by the Massachusetts Supreme Court. This is permanent, and precedent setting, absolutely justifies and vindicates my post from the day before, which also contained links to other posts which any declared sensational just a few days before, ex., The Robo-Signing Mess Is Just the Tip of the Iceberg, Mortgage Putbacks Will Be the Harbinger of the Collapse of Big Banks that Will Dwarf 2008! http://boombustblog.com/reggie-middleton/2010/10/12/the-robo-signing-mess-is-just-the-tip-of-the-iceberg-mortgage-putbacks-will-be-the-harbinger-of-the-collapse-of-big-banks-that-will-dwarf-2008/ and As Earnings Season is Here, I Reiterate My Warning That Big Banks Will Pay for Optimism Driven Reduction of Reserves. This is a very big deal since it actually unravels many thousands of foreclosures and sets precedent to be examined across the country (all 50 state's attorney generals are looking into fraudclosure issues) that will really cause material damage to the banks that are pursuing (have pursued) said foreclosures. As reported in the Massachusetts Law Blog:

Breaking News (1.7.11): Mass. Supreme Court Upholds Ibanez Ruling, Thousands of Foreclosures Affected

http://www.massrealestatelawblog.com/2011/01/07/ibanez-foreclosure-ruling-upheld-an-indictment-of-the-securitized-mortgage-system/#utm_source=feed&utm_medium=feed&utm_campaign=feed

Update (2/25/10) - Mass. High Court May Take Ibanez Case

Breaking News (10/14/09) - Land Court Reaffirms Ruling Invalidating Thousands of Foreclosures. Click here for the updated post.

None of this is the fault of the [debtor], yet the [debtor] suffers due to fewer (or no) bids in competition with the foreclosing institution. Only the foreclosing party is advantaged by the clouded title at the time of auction. It can bid a lower price, hold the property in inventory, and put together the proper documents any time it chooses. And who can say that problems won't be encountered during this process?... Massachusetts Land Court Judge Keith C. Long

"[W]hat is surprising about these cases is ... the utter carelessness with which the plaintiff banks documented the titles to their assets." -Justice Robert Cordy, Massachusetts Supreme Judicial Court

Today, the Massachusetts Supreme Judicial Court (SJC) ruled against foreclosing lenders and those who purchased foreclosed properties in Massachusetts in the controversial U.S. Bank v. Ibanez case...

... For those new to the case, the problem the Court dealt with in this case is the validity of foreclosures when the mortgages are part of securitized mortgage lending pools. When mortgages were bundled and packaged to Wall Street investors, the ownership of mortgage loans were divided and freely transferred numerous times on the lenders' books. But the mortgage loan documentation actually on file at the Registry of Deeds often lagged far behind.

In the Ibanez case, the mortgage assignment, which was executed in blank, was not recorded until over a year after the foreclosure process had started. This was a fairly common practice in Massachusetts, and I suspect across the U.S. Mr. Ibanez, the distressed homeowner, challenged the validity of the foreclosure, arguing that U.S. Bank had no standing to foreclose because it lacked any evidence of ownership of the mortgage and the loan at the time it started the foreclosure.

Mr. Ibanez won his case in the lower court in 2009, and due to the importance of the issue, the Massachusetts Supreme Judicial Court took the case on direct appeal.

The SJC Ruling: Lenders Must Prove Ownership When They Foreclose

The SJC's ruling can be summed up by Justice Cordy's concurring opinion:

"The type of sophisticated transactions leading up to the accumulation of the notes and mortgages in question in these cases and their securitization, and, ultimately the sale of mortgaged-backed securities, are not barred nor even burdened by the requirements of Massachusetts law. The plaintiff banks, who brought these cases to clear the titles that they acquired at their own foreclosure sales, have simply failed to prove that the underlying assignments of the mortgages that they allege (and would have) entitled them to foreclose ever existed in any legally cognizable form before they exercised the power of sale that accompanies those assignments. The court's opinion clearly states that such assignments do not need to be in recordable form or recorded before the foreclosure, but they do have to have been effectuated."

The Court's ruling appears rather elementary: you need to own the mortgage before you can foreclose. But it's become much more complicated with the proliferation of mortgage backed securities (MBS's) -which constitute 60% or more of the entire U.S. mortgage market. The Court has held unequivocally that the common industry practice of assigning a mortgage "in blank" -- meaning without specifying to whom the mortgage would be assigned until after the fact -- does not constitute a proper assignment, at least in Massachusetts.

This is a very interesting development, and I would like to make note that the buck stops here since this is Supreme Court. I normally do not excerpt or quote this much of another blog or news source, but since the content is legal in matter and this particular blog (Massachusetts attorney) appears to have put a strong legal analysis on the topic, I will continue. I urge others to visit the Massachusetts Law Blog for more info. Back to his write-up...

*

Despite pleas from innocent buyers of foreclosed properties and my own predictions, the decision was applied retroactively, so this will hurt Massachusetts homeowners who bought defective foreclosure properties.

*

If you own a foreclosed home with an "Ibanez" title issue, I'm afraid to say that you do not own your home anymore. The previous owner who was foreclosed upon owns it again. This is a mess.

*

The opinion is a scathing indictment of the securitized mortgage lending system and its non-compliance with Massachusetts foreclosure law. Justice Cordy, a former big firm corporate lawyer, chastised lenders and their Wall Street lawyers for "the utter carelessness with which the plaintiff banks documented the titles to their assets."

*

If you purchased a foreclosure property with an "Ibanez" title defect, and you do not have title insurance, you are in trouble. You may not be able to sell or refinance your home for quite a long time, if ever. Recourse would be against the foreclosing banks, the foreclosing attorneys. Or you could attempt to get a deed from the previous owner. Re-doing the original foreclosure is also an option but with complications.

*

If you purchased a foreclosure property and you have an owner's title insurance policy, you have a potential claim against the title policy. Contact our office for legal assistance.

Here he puts in some self promotion, but hey... I'm one to talk. I actually appreciate the legal analysis and am glad to have him offer services in the arena.

*

The decision carved out some room so that mortgages with compliant securitization documents may be able to survive the ruling. This will shake out in the months to come. A major problem with this case was that the lenders weren't able to produce the schedules of the securitization documents showing that the two mortgages in question were part of the securitization pool. Why, I have no idea.

*

The decision, however, may not prove to be anywhere near the Apocalypse it's been hyped to be. The Court said that "[w]here a pool of mortgages is assigned to a securitized trust, the executed agreement that assigns the pool of mortgages, with a schedule of the pooled mortgage loans that clearly and specifically identifies the mortgage at issue as among those assigned, may suffice to establish the trustee as the mortgage holder. However, there must be proof that the assignment was made by a party that itself held the mortgage." This opens the door for foreclosing lenders to prove ownership with proper documents. Furthermore, since the Land Court's decision in 2009, many lenders have already re-done foreclosures and title insurance companies have taken other steps to cure the title defects.

I am not a lawyer and this is not my purview, but things may not be quite that simple. The securitized trust documents themselves have timing issues that may come into play. See the email chain conversation below for more on this topic.

*

The ruling may be limited only to Massachusetts and states operating under a non-judicial foreclosure and "title theory" laws. The Court was careful to point out that Massachusetts requires very strict compliance with its foreclosure laws. The reason for that is Massachusetts is a non-judicial foreclosure state-meaning lenders don't need a court order to foreclose-and that the state operates under the "title theory" which is a fancy way of saying that the bank is really the legal owner of your house.

*

Watch for class actions against foreclosing lenders, the attorneys who drafted the securitization loan documents and foreclosing attorneys. Investors of mortgage backed securities (MBS) will also be exploring their legal options against the trusts and servicers of the mortgage pools.

It appears as if he contradicted his statement above. I can practically guaranteed that this significantly increases the risk. volume and velocity of litigation. Think about it. If you were a REMIC investors, would you be sitting pat, or calling your attorney.

* The banking sector has already dropped some 5% today (1.7.11), showing that this ruling has sufficiently spooked investors. (But Merrill Lynch just went on a buying spree on the banking sector-showing that the real experts are betting that this decision and others which will follow will not substantially affect banks' profitability).

I have absolutely no idea what he means by Merrill Lynch going on a buying spree - actually using their (BofA's) balance sheet? I seriously doubt so. I also take umbrage to the assertion that Merrill Lynch constitutes a "real expert"(s) in terms of mortgage and real estate valuation and risk assessment, since they "experted" themselves into a near collapse over these very same assets.

Interested parties may download the actual ruling here: Ibanez-Case-JAN-2011. I actually engaged in an interesting email exhange with a BoomBustBlogger over this fraudclosure issue, and would like to share the email chain with the blog.

10/21/10

Reggie,

You see that the various large shoes we were discussing have begun dropping. Multi-billion dollar demands by non-agency bondholders for putbacks, and now the government is being forced to take action. I read elsewhere that a group of hedge funds is organizing for a similar demand. I view with interest the tiny levels at which the banks are reserving against these events in comparison with the present (and probable future) size of the put-back demands. Again, this is only ONE tentacle of the monster.

So far, the putback demands appear to be merely rep and warranty driven, i.e, the failing loans do not meet the underwriting requirements as represented in the prospectus. This does not implicate the REMICs' tax-exempt status. However, as claims for wrongful foreclosure based on the failure of loans to be properly deposited into trust are proved true -- or as the same facts are brought to light by 50 state attorneys general -- it will be implicated. This may produce a larger wave of claims by bondholders, both because of the loss of tax structure as represented and warranted, and because the knowing failure to properly deposit the loans (which will be inferred from the systematic extent of the failure) may support securities fraud claims. I will be very interested to see how you quantify the size of the problem for the banks.

1/1/10

Reggie:

... I assume you saw stories on the Mass. Court ruling in Ibanez. The obvious question was, "Why didn't they just back up and start over after getting the assignments done correctly?" The answer: They had no choice but to either litigate the homeowners into submission or pay the homeowners to go away. They chose the former strategy and it failed. Why did they have those choices? As you and I discussed awhile back: the REMIC. If the loans were not originally assigned to the trust by the deadline, the REMIC lost its special tax status, and the banks were forced into the argument that an after-the-fact assignment had the effect of an original timely assignment (so that, getting a state court to bite on this, they could then go argue the same point to the IRS, i.e., "no harm no foul"). The Mass. Court, to its credit, saw through the bullshit and upheld the rule of law.

The implications of this for the REMICs (actually, the banks that created and sold them) and homeowners going forward are huge. Homeowners can now see the light, and if there's any question about the ownership of the loan, stick a hot poker in that issue (demand proof of ownership, either directly before litigation or in discovery when litigation has started) until the banks cry uncle, meaning pay through the nose to buy off the homeowners and save the REMIC's tax status. The banks face the prospect of enormously increased costs, for any of: (a) litigation expenses as this issue becomes harder fought by the homeowners; (b) increased settlement costs as homeowners realize their advantage and demand more pounds of bank flesh to go away; or (c) payments to REMIC investors for losses caused by the banks' failure to properly assign the loans in the first place. Who's going to suffer the worst?

Again, JPM et. al. have been much too optimistic in reserving for these occurrences, as clearly detailed in my post As Earnings Season is Here, I Reiterate My Warning That Big Banks Will Pay for Optimism Driven Reduction of Reserves. The legal costs looked bad before this decision, as stated in As JP Morgan & Other Banks Legal Costs Spike, Many Should Ask If It Was Not Obvious Years Ago That This Industry May Become The "New" Tobacco Companies and it simply looks much worse now. To think, so called experts wonder why I am bearish on JP Morgan and the big banks...

... There is no chance for appeal in the Mass case; the decision came from the state's highest court. This quote from the court illustrates that this was not rocket science; the banks' lawyers never should have taken the risk of the appeal rather than settling and leaving the record with an unreported trial court decision of much less import:

"The legal principles and requirements we set forth are well established in our case law and our statutes. All that has changed in the plaintiffs' apparent failure to abide by those principles and requirements in the rush to sell mortgage-backed securities."

... I agree with everything in your post ["As JP Morgan & Other Banks Legal Costs Spike, Many Should Ask If It Was Not Obvious Years Ago That This Industry May Become The "New" Tobacco Companies"]. I noted someone's comment about BAC's settlement with Fannie and Freddie (paying about 2 cents on the dollar to eliminate hundreds of billions of putback claims, a bailout in disguise for which somebody should go to jail). Otherwise, I think the banks differ from the tobacco companies in a couple major respects: (a) they don't sell an addictive product which may be somewhat economically insensitive; and (b) they don't have access to overseas growth like the tobaccos do. By failing to adequately reserve and kicking the can, they're making the end only that much bloodier (or betting on TARP II, III and IV, which may not be a bad bet).

Actually, the banks did have an overseas growth model, the sales of securitized products. One would have thought that that model had come to an end due to the crash and burn effect, alas it has not and the reason is because the banks due sell what appears to be an addictive product.

1.

The reach for unrealistically high yields in the case of yield hungry institutional investors such as pension funds. As stated Reggie Middleton vs Goldman Sachs, part 1, For Those Who Chose Not To Heed My Warning About Buying Products From Name Brand Wall Street Banks, and "Blog vs. Broker, whom do you trust!," Goldman's peddling of products often spells doom for the consumer (client) and bonus for the producer (Goldman). Goldman is now underwriting CMBS under a broad fund our $19 billion bonus pool "buy" recommendation in the CRE REIT space reference Reggie Middleton Personally Contragulates Goldman, but Questions How Much More Can Be Pulled Off. Now, after all of the evidence that I have presented against the CRE space, who do you think would be better for clients net worth, Reggie's BoomBustBlog or Goldman? There is also the most recent evidence from just last week: Morgan Stanley Jingle Mail: Loses Properties To John Paulson Investment Consortium & Itself.

2.

The satisfaction of the get rich quick(er) urges to be had in their retail, HNW and UHNW clients. A perfect example is the Facebook offering, of which I am preparing an extra special analysis for my blog's subscribers to be released in a day or two wherein I will show how those Goldman clients are throwing their money into the Goldman bonus pool/Facebook working capital fund abyss - that is if I haven't demonstrated such already:

* Facebook Becomes One Of The Most Highly Valued Media Companies In The World Thanks To Goldman, & Its Still Private!

* Here's A Look At What The Goldman FaceBook Fund Will Look Like As It Ignores The SEC & Peddles Private Shares To The Public Without Full Disclosure

* The Anatomy Of The Record Bonus Pool As The Foregone Conclusion: We Plug The Numbers From Goldman's Facebook Fund Marketing Brochure Into Our Models

Now, back to the email exchange...

The limiting factors on the homeowner side are: (a) an imbalance of knowledge of their options as compared to the banks; and (b) an imbalance of resources ($) to pay lawyers to fight the banks. Although I think the internet and its democratic access to information changes the equation for the first issue, it's still like retailers selling gift cards - they make money because they know a large percentage of people will stick the card in the drawer and forget about it, and in doing so will have given the retailers free money. Many homeowners who are in position to challenge a foreclosure, and thereby squeeze a bunch of money out of the banks, never will. The $64 question is, how many will?

I have a very strong feeling that many distressed homeowners that read BoomBustBlog can be considered to be amongst that educated elite.

Now there's a state appellate court decision for every other state appellate court to look to for guidance. Stupid. This is like a case I had in federal court several years ago against the U.S. gov't. We obtained a ruling imposing estoppel against the gov't - which is nearly impossible to get. The gov't did NOT appeal that decision, only the decision granting us fees (which it lost). It avoided an appeal for the same reason - it did not want a Xth circuit decision upholding estoppel against it sitting out there for the rest of the world to model from.

The only logic that I see in the bank's decision to litigate was that if you pay off one homeowner, you create a pattern where you will end up having to pay off others until it get's to the point where you will have to litigate the issue to its ultimate conclusion anyway. Hard to say which route would have been more efficient and cheaper, but I do know that this is far from a desirable outcome for the banking industry.

http://www.safehaven.com/article/19615/less-than-24-hours-after-my-warning-of-extensive-legal-risk-in-the-banking-industry-the-massachusetts-supreme-court-drops-the-bomb

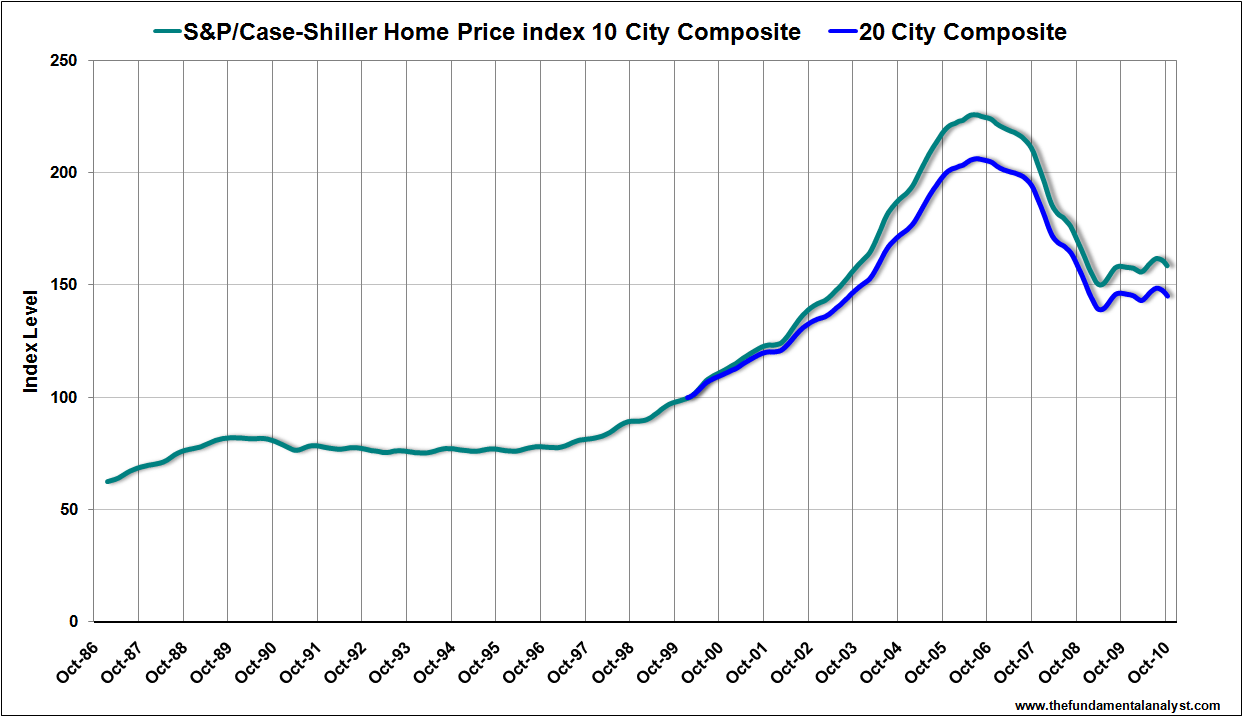

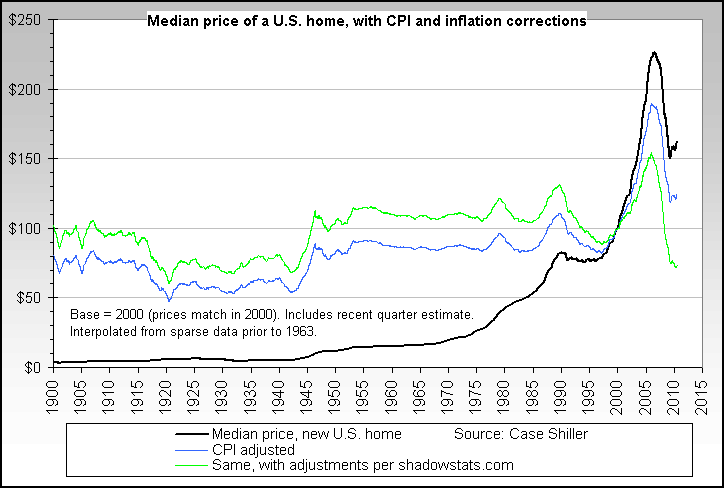

Case-Shiller Housing Chart

S&P Case-Shiller housing data was released Tuesday (report).

(check out this link for a full examination of the Case-Shiller)

http://www.standardandpoors.com/servlet/BlobServer?blobheadername3=MDT-Type&blobcol=urldocumentfile&blobtable=SPComSecureDocument&blobheadervalue2=inline%3B+filename%3Ddownload.pdf&blobheadername2=Content-Disposition&blobheadervalue1=application%2Fpdf&blobkey=id&blobheadername1=content-type&blobwhere=1245231571069&blobheadervalue3=abinary%3B+charset%3DUTF-8&blobnocache=true

Bottom line up front: The report noted a deceleration in home price growth rates in most of the areas surveyed. Take a look at the circled area in the chart below - notice anything? Hmm, could this be the beginning of another leg down for the housing market?

http://economicrot.blogspot.com/2010/10/case-shiller-housing-chart.html

Delinquencies May Be Down, But 4.3 Million Homes Are 90 Days Delinquent Or In Foreclosure

Calculated Risk.com

Dec. 31, 2010

LPS Applied Analytics released their November Mortgage Performance data. According to LPS:

* The average number of days delinquent for loans in foreclosure is a record 499 days

* Over 4.3 million loans are 90 days or more delinquent or in foreclosure

* Delinquency rates are down across all products as more loans entered foreclosure and new delinquencies declined.

* Foreclosure inventory increases are being driven both by elevated levels of foreclosure starts as well as a very limited amount of foreclosure sale activity.

LPS Data November

Image: Calculated Risk

This graph provided by LPS Applied Analytics shows the percent delinquent, percent in foreclosure, and total non-current mortgages.

The percent in the foreclosure process is trending up because of the foreclosure moratoriums.

According to LPS, 9.02% of mortgages are delinquent (down from 9.29% in October), and another 4.08% are in the foreclosure process (up from 3.92% in October) for a total of 13.10%. It breaks down as:

* 2.61 million loans less than 90 days delinquent.

* 2.16 million loans 90+ days delinquent.

* 2.16 million loans in foreclosure process.

For a total of 6.92 million loans delinquent or in foreclosure.

Note: I've seen some people include these 7 million delinquent loans as "shadow inventory". This is not correct because 1) some of these loans will cure, and 2) some of these homes are already listed for sale (so they are included in the visible inventory).

Two key numbers to watch in 2011 are:

* New delinquencies. With falling house prices, delinquencies could start to increase again.

* Foreclosures. With the end of the foreclosure moratoriums, foreclosure sales should increase - and the number of homes in the foreclosure process should decline. However REOs (Real Estate Owned) will increase unless the homes are sold.

http://www.businessinsider.com/delinquencies-may-be-down-2010-12#ixzz1A5mQMzrP

Housing Pain Pits Neighbor Against Neighbor in Florida

Dan Fitzpatrick

WallStreetJournal.com

Dec 31, 2010

Lauderhill, Fla.

Few things agitate Sid Schulman, who often shoots the breeze with other retirees and flirts with women friends at their condominium complex here.

But it galls him when neighbors stop paying their mortgages and maintenance fees, and leave the cost of community upkeep to others. "I am paying for these guys," said the 75-year-old sitting poolside, a diamond stud in his left ear.

Last year, he took matters into his own hands. Near the mailbox of each condo building he posted a list of residents delinquent on their maintenance fees, with the message "Pay up or move out" and the same in Spanish, Pague O Mudese. He also tried, unsuccessfully, to get the cable company to cut off service to nonpayers.

The public shaming angered some of those named. "You know where I live—come and tell me that to me face," said Lorena Garcia, 36, who lost her job and ability to pay.

The storm that struck the housing market has strewn many casualties—lenders, builders, real-estate agents, mortgage-bond investors.

Add to the list the comity of certain communities where residents live close together, some of them paying their mortgages and homeowner-association fees, and some not.

As banks slow foreclosures amid concerns about sloppy record keeping, some delinquent homeowners get to stay put even longer without paying. The delays are further inflaming some neighbors who consider that unfair.

The condo complex Mr. Schulman and Ms. Garcia share, called International Village, has installed a fingerprint-scanning device at its central clubhouse, to keep residents who are more than 90 days behind on their maintenance fees from swimming in the pools, playing on the racquetball courts and using the game room, where canasta and mah-jongg competitions are held.

In a particularly stark example of housing tensions found in many places to varying degrees, the International Village homeowners association responded to the banks' slowdown in foreclosures with an aggressive step: It began its own foreclosure process. Florida law permits that under certain circumstances. A nonprofit homeowners association can take temporary title of residential units from people who aren't paying monthly fees they agreed to pay.

The scene of these frictions is a 28-acre community in southeastern Florida's Broward County that spreads out on a peninsula, surrounded by a canal, a lake and an eight-foot stone wall. Oak trees shade the gated entrance to International Village, at the center of which is the Bavarian clubhouse, built with a 24-foot ceiling and stone fireplace. Three-story residential buildings, each with about 76 condos, are grouped according to their architectural roots, bearing names like Yorkshire and Bordeaux. In the morning, residents gather at the pool for "aquacise."

Early marketing brochures for the complex, built in the 1970s, lured well-off retirees and snowbirds by promising "seventh heaven for people who insist on living first class."

Later, easy lending during the housing boom put the condos within reach of lower-income buyers. According to Michael Schenkel, a real-estate professional who owns three units in the complex and manages others, average prices for its one-bedroom condos peaked at about $120,000 in 2006.

Then Florida's sagging economy started costing residents their livelihoods and ability to pay. Ms. Garcia bought a two-bedroom in International Village in 2005 for $190,000, but she lost her job. With her cash dwindling as she went through a divorce, she says, she stopped making her $1,500 monthly mortgage payments in 2008.

Special assessments pushed up the monthly maintenance fee she owed to the homeowners association. Ms. Garcia didn't pay that, either.

Now, owners of about 128 of the 832 units at International Village, just over 15%, are 90 days or more behind on their fees. Banks won't lend on residences in the complex until the percentage of fee delinquents drops below 15, according to Mr. Schenkel.

The problems feed on themselves: "Banks will not write mortgages in communities with high delinquencies," he said, "and property values will not increase until we get financing from major banks." He says the value of one-bedroom units has tumbled as much as 75%.

With the homeowners association unable to collect maintenance from so many units, the complex is showing the wear: torn screen doors, roofs in need of repair, carpets getting shabby. Earlier this year, the total of delinquent fees passed $1 million, equal to a third of the association's annual budget.

"The foreclosure process takes over two years," Mr. Schenkel said. "You can get away with living for free for two years, not paying mortgage and maintenance."

Larry Kornblith takes a dim view of that. "The ones who are delinquent are parasites," the 82-year-old bluntly declared, relaxing near the pool in a Fila shirt and white Nike tennis shoes. "If you can't afford it, get out."

There are divisions, too, among the people current on their payments, because they don't all agree on how the homeowners association should deal with those who aren't.

Doug Meyers, a resident who owns more than a dozen units and is up to date on his payments, voted on the association's board against installing the fingerprint scanner. He was skeptical it would work. He says some neighbors accused him of protecting residents who were delinquent.

"They make it personal. It bothers me, personally. It hurts me," said Mr. Meyers, 54, adding that he now tries to avoid some fellow residents.

Others wanted the association to get tougher. Among these was Michele Tersigni, a 53-year-old resident who works as an administrator at a doctor's office. She won a seat on the homeowners-association board early this year and in May became its president.

She quickly made changes, such as hiring security guards directly instead of through a service, to save money. And, responding to residents' complaints about people staying on in homes they were no longer paying on, she hired new lawyers who would be more aggressive.

After foreclosure problems such as "robo-signing" of documents erupted this fall, new applications for court approval of foreclosures in Broward County—which totaled 1,693 in September—tumbled to 224 in November and 137 in December through the 23rd of the month, according to Legalprise Inc., a data firm. Countywide, foreclosure applications on more than 38,000 residential units are awaiting a court's approval to proceed.

The homeowners association countered the delays. Acting under the Florida law, it took temporary title to two condos in October and another in November. It plans four to five more in January. The move enables the association to rent out the units and get them back to producing income.

If lenders eventually foreclose on the condos, the association can start proceedings against the lenders to obtain some past-due maintenance fees. Lenders that take over units are liable for maintenance fees as long as they own them.

Ms. Tersigni says something had to be done because maintenance was slipping. "I just want to give people who are paying the rights they deserve," she said.

The village is abuzz, she added, with stories of owners not paying even though they could afford to. Ms. Tersigni's predecessor as board president, Scott Samuels—who admits to not being aggressive enough in dealing with the delinquency problem—said some owners were letting their units go into foreclosure while renting them out to tenants not registered with the association.

"Owners are collecting money, and we are not getting our money," he said.

Ms. Tersigni said some owners "make the money—they just refuse to pay because they can get away with it. They will put money aside and buy something else."

Ms. Garcia says that was never true in her case. "Every house has its own problems. You can't judge people," Ms. Garcia said. The homeowners association, to her mind, is "taking advantage of people who really have problems."

In August, about two years after she stopped paying her mortgage, Ms. Garcia lost her apartment to a foreclosure by the lender, although she continued to live in International Village in someone else's unit.

On the day she and her husband were vacating their own apartment, two female neighbors openly celebrated while making their way to the pool. "Thank God they are moving out," said one, a blue ball cap pulled over her eyes.

The other, wearing an olive-green dress and sunglasses, said she couldn't understand why Ms. Garcia had been allowed to stay so long. "It takes so long to get them out," she said, and then listed others she said were behind on payments.

Some residents are troubled by the tensions, which are reflected in a sign put up near the clubhouse: "The prior leadership did not take a pro-active position with delinquents who failed to pay. We must not let this happen again."

"I feel like we are being singled out, like we're not part of the community," said one young resident, who added that he wasn't going to provide a fingerprint for access to the clubhouse because he knew he would be denied. "What do they want next, my DNA?"

Franck Noel, 32, said the homeowners association moved to foreclose on his unit even after he paid $1,753.79 in late fees. When he brought his situation up at a board meeting it got unruly. Someone called the police, who Mr. Noel says stayed out by the gate and didn't enter the clubhouse.

The police department says it was informed there was hostility inside the clubhouse relating to a foreclosure and there was a request that the subject be removed. But no police report was filed on the incident.

Mr. Noel said a resident dragged him out by his collar. Ms. Tersigni said he left without being forcibly removed.

She acknowledged that the move against his residential unit was an error and said the association eventually recognized this and dealt with it.

Mr. Noel, noting that some board members own multiple units, alleged that the association was eager to foreclose because some on the board "want to buy these units cheap and own them for themselves." Mr. Meyers, a board member who owns a number of units, dismissed any talk of his manipulating the system as "lies" and "slander."

Said Mr. Noel: "I don't trust anybody here."

http://online.wsj.com/article/SB10001424052748703326204575616340542578852.html?mod=WSJ_hp_mostpop_read

Deficit Commission: How Mortgage Deductibility Affects Housing Prices

The Market Flash

December 13, 2010

The Deficit Commission, chaired by Erskine Bowles and Alan Simpson, had many interesting proposals concerning deficit reduction. One can debate the relative merits and demerits of each proposal and the economic benefit to the country. However, our job as investors is to evaluate the impacts of what they propose and take advantage of any changes in valuation before the wider market discounts the changes. The proposal on the table is to limit mortgage deductibility only for mortgages of 500k or less.

The purpose of this article is to examine the effect of that proposal on houses that would have a mortgage of greater than 500k. Obviously it is not known whether the Deficit Commission's suggestion on mortgage deductibility will be implemented, but just the discussion of it can affect current prices.

First things first: The U.S. tax policy of mortgage deductibility is baked into the price of every house in the United States, whether that house has a mortgage or not. The U.S. has had mortgage interest deductibility since the 1950s or earlier. Each home in the U.S. is valued at what it can currently sell for to new buyers who generally have to get a mortgage to make the purchase. Any buyer who is purchasing with a mortgage, takes out a bigger mortgage than they would otherwise because mortgage interest is fully deductible on their tax return.

So all housing prices in the U.S. now, both at the high end and the low end, reflect the fact that interest on mortgages is tax deductible. There is some part of the value of every house that would fall if mortgage deductibility were taken away. There are many countries in the world that don’t allow mortgage interest deductibility so it’s not a constitutional right.

So let’s establish the price of houses that will not be affected by the Deficit Commission’s proposal. This is pretty easy. Mortgages up to 500k will still be deductible and just for the sake of simplicity let’s assume a bank would want 100k down on a 500k mortgage. So for houses of 600k or less, it’s business as usual in terms of valuation. If the 500k is not adjusted for inflation going forward that could raise or lower the price of houses near the top end of the range, depending on what the decision was.

The purpose of this article is to use some financial/mathematical techniques to guesstimate the affect of the Deficit Commission’s proposal on houses that have a greater value than 600k, just factoring in the deductibility of mortgage interest. Many things affect high end housing prices; elasticity of demand, how much down payment is made for a house in a certain price range, and the local employment market.

This article is going to focus only on the mortgage deductibility effect on housing prices of greater than 600k. The approach is to discount the present value of 30 years' worth of interest payments in a world where there is mortgage interest deductibility and a world where there is not. The difference between those two numbers should be a rough estimate on housing prices over 600k of having their mortgage deductibility taken away by the Erskine/Bowles commission. Present value is a financial concept that allows a single number in the present to represent the value of a series of future payments. Here our future payments are interest paid on a mortgage and the Present Value is the amount that can be borrowed to buy the house.

So let’s look at the effect of taking away mortage deductibility on mortgages over 500k. I am going to include the Excel® formulas used in the calculations so you can make your own calculations if you are interested in a different price range or want to use different assumptions. I am going to target a mllion dollar house. 600k of the value of the house is unaffected by the Deficit Commission's proposed change.

The amount over 600k I am going to break down into roughly 300k of borrowing and 100k more of down payment and the principal portion of the mortgage payment. So our borrower in the current world of unlimited mortgage interest deductions is willing to pay $1800 of interest required to buy the last 400k of the million dollar house. Keep in mind this $1800 is just the interest portion of the mortgage, not the entire payment. Assuming a 6% discount rate and 30 years of discounting, this provides 300k of present value to buy the million dollar house:

$300,225 = PV(.005,360,1800)

Excel uses non percentage interest rate numbers for the periodic interest rate so 6% would be .06/12 = .005. I chose a 6% discount rate because I thought it was a more representative rate over the next 30 years, and it converted to monthly compounding cleanly. Use a different discount rate if you think that’s more correct. Assume 30 years' worth of discounting 30*12=360. $1800 is the monthly interest in a mortgage deductible world. The = sign and to the right is what you put into any Excel cell.

Now what happens when Erskine/Bowles wipes out mortgage deductibility over 500k? We need a formula that shows what monthly interest a person would be willing to pay if the interest is not deductible. That formua is:

(1 – MarginalTaxRate) * PaymentWithDeductibility = InterestPaymentWithoutDeductibility

The highest marginal tax bracket proposed by Erskine/Bowles is 23%. So our borrower is indifferent between making an interest payment of $1386 in a world where there is no mortgage deductibility for mortgages > 500k OR paying $1800 a month, deducting an extra $21,600 ($1800 * 12 months) from his joint income of 350k, and paying $7128 (33% joint bracket) less in taxes because his mortgage was deductible. So now we plug this new lower interest payment into Excel and discount to the present:

$231,175 = PV(.005,360,1386)

So we see roughly 70k less present value ability on the part of borrowers, given that mortgages > 500k are not deductible. Proportionally, and to get to a round number, we will take another 30k of down payment and principal payments because we can borrow less, so 100k less to buy the house with. The rather stark conclusion of this exercise is that the price of every house in the U.S., ceteris paribus, will drop by one quarter of its value over 600k if the Deficit Commission’s recommendation on mortgage deductibility becomes law.

I am pretty sure most members of the Deficit Commission own homes worth more than 600k so you can’t say they were acting in their own self interest with this suggestion. I would argue that grandfathering the clause in (allowing existing mortgages > 500k to keep their deductibility) mostly doesn’t matter. Prices in the real estate market are set by the marginal (new) buyer, not by the people who already own homes, and as time goes on, existing mortgages will bleed off.

One could even argue my estimate is low. If the law changes, it changes for the foreseeable future. My assumption of 30 years is probably too short, given that mortgage deductibility is removed theoretically forever. Your buyer and your buyer’s buyer won’t be able to deduct the mortgage interest. But if you increase the discount periods to 720 (60 years) you will see it only makes about a 10k difference. Using a higher discount rate (12% for example) would make the price change greater than a quarter. Using a lower discount rate (1.2% for example) would make the price change less than a quarter.

This discussion reveals one of the problems with law and economics. Something may be a good idea but if you have huge existing pricing in the market built up around it, it becomes difficult to change. I personally don’t think the U.S. should have ever have had mortgage deductibility at any level. I would go so far as to say that the Financial Panic of 2008 would have been less severe, or perhaps not have happened at all, if there was no mortgage deductibility.

However, once bad policy is implemented, prices adjust and change becomes problematical. In this case, people who bought expensive homes more recently could get punished for making a decision based on the current state of the tax law.

The investing takeaways focus on home builders, mortgage REITs, and realtors. Of the homebuilders, NVR Inc. (NVR), D.R. Horton (DHI), and Toll Brothers (TOL), Toll Brothers seems to focus more on the high end market. Prices of new homes have to be greater than 600k to depress the stock. Mortgage REITs Annaly (NLY) and Anworth (ANW) could be affected if the size of mortgages fall, or mortgage volume falls. High end realtors would clearly be impacted. Sotheby’s (BID) had a large high end real estate broker network but I’m not sure what percentage of their net income is from the real estate group.

Taking long/short action now given the uncertainty of whether the Deficit Commission mortgage proposal could be implemented, is not warranted. If the mortgage deduction looked likely to become law or became law, the impact in the housing market is going to be large. As I mentioned above, even serious discussion of this proposal could cause high end housing prices to fall. I abhor chartism (looking at past prices to discern future prices) but I do look at past prices when I think I have an idea the market hasn’t discounted yet. In this case you would check the price of the stocks above or others you can think of over the last six months. If they are flat or opposite your guess you still have time to implement your bet that the market hasn’t discounted the ramifications of the ideas presented in this article.

http://seekingalpha.com/article/241447-deficit-commission-how-mortgage-deductibility-affects-housing-prices

Mortgage Rates for 30-Year U.S. Loans Advance to Seven-Month High of 4.86%

Prashant Gopal

Dec 30, 2010

Mortgage rates for U.S. loans climbed to a seven-month high, increasing borrowing costs for homebuyers in a sluggish real estate market.

The average rate for a 30-year fixed loan rose to 4.86 percent in the week ended today from 4.81 percent, Freddie Mac said in a statement. The average 15-year rate advanced to 4.2 percent from 4.17 percent, the mortgage-finance company said.

Rising home loan rates may limit homebuyer demand as housing remains a weak link for the economy. Home prices in October fell 0.8 percent from a year earlier, the largest year- over-year decline since December 2009, the S&P/Case-Shiller index of property values showed this week.

“Optimism is fading from the housing market,” Robert Shiller, an economics professor at Yale University and co- creator of the index, said on Bloomberg Television on Dec. 28.

Sales of new and existing homes rose less than economists estimated in November even as mortgage rates sank to the lowest levels on record, reports from the Commerce Department and the National Association of Realtors showed last week.

Pending home sales climbed more than forecast in November, a sign demand is recovering following a post-tax credit plunge, according to a report from the Realtors group today. The data are based on contract signings, while existing-home sales represent closings.

The rate for a 30-year loan has climbed for six of the past seven weeks amid speculation that President Barack Obama’s agreement to a two-year tax cut extension will boost economic growth and inflation. The rise pushed the monthly cost of a $300,000 loan to $1,585 from $1,462.

Borrowing costs are still near historic lows. The 30-year fixed rate averaged about 4.7 percent in 2010, the lowest on an annual basis since 1955, Frank Nothaft, Freddie Mac’s chief economist, said in a statement today.

http://www.bloomberg.com/news/2010-12-30/mortgage-rates-for-30-year-u-s-loans-advance-to-seven-month-high-of-4-86-.html

Pending Sales of U.S. Previously Owned Homes Rise

Bob Willis

Dec 30, 2010

The number of contracts to buy previously owned homes rose more than forecast in November, a sign sales are recovering following a post-tax credit plunge.

The index of pending resales increased 3.5 percent after jumping a record 10 percent in October, the National Association of Realtors said today in Washington. The median forecast in a Bloomberg News survey called for a 0.8 percent rise in November, and the gain was the fourth in five months. The group’s data go back to 2001.

Home demand is stabilizing after sales collapsed to a record low in July, as the effects of a tax incentive worth as much as $8,000 waned. A jobless rate hovering near 10 percent means foreclosures will remain elevated and any recovery in housing, the industry that precipitated the worst recession since the 1930s, will take time to develop.

The figures are “in line with an ongoing gradual pickup in existing-home sales in December,” Yelena Shulyatyeva, an economist at BNP Paribas in New York, said in an e-mail to clients. “Housing demand should continue its uneven recovery entering 2011 as housing oversupply should keep pushing housing prices down.”

A report today from the Labor Department showed claims for jobless benefits fell last week to the lowest level since July 2008, showing the labor market is improving heading into 2011. Filings decreased by 34,000 to 388,000 in the week ended Dec. 25, fewer than the lowest estimate of economists surveyed.

Business Barometer

Other figures showed the economy accelerated at the end of the year. The Institute for Supply Management-Chicago Inc.’s business barometer jumped to 68.6 in December from 62.5 in the prior month. Readings greater than 50 signal expansion and the level was the highest since July 1988.

Stocks fluctuated between gains and losses after the reports. The Standard & Poor’s 500 Index fell 0.1 percent to 1,258.23 at 11:17 a.m. in New York. The benchmark 10-year Treasury note declined, pushing up the yield to 3.39 percent from 3.35 percent late yesterday.

The projected increase in pending home sales was based on the median of 24 forecasts in the Bloomberg survey. Estimates ranged from a drop of 5 percent to a gain of 5 percent.

Two of four regions saw an increase, today’s report showed, led by an 18 percent jump in the West. Pending sales rose 1.8 percent in the Northeast. They fell 4.2 percent in the Midwest and 1.8 percent in the South.

November 2009

Compared with November 2009, pending sales in the U.S. were down 2.4 percent.

Even as the labor market is improving and manufacturing is growing, housing remains a weak link. NAR chief economist Lawrence Yun last week estimated there were about 4.5 million distressed properties that could potentially reach the market in coming months.

Average home prices as measured by the S&P/Case-Shiller indexes have begun dropping again after rising when the tax incentive was in effect. The group’s 20-city index fell 0.8 percent in October from a year earlier, the biggest year-on-year decline since December. It fell 1 percent from the prior month, and is down 30 percent from its July 2006 peak.

Reports earlier this month showed the housing market is stuck near recession levels. Housing permits fell in November to the third-lowest level on record, while starts rose for the first time in three months, the Commerce Department reported Dec. 16.

Home Sales

Sales of new and existing homes last month rose less than projected by the median forecast of economists surveyed by Bloomberg, reports from the Commerce Department and the National Association of Realtors showed last week. Existing home sales represent closings on the contracts captured by the pending sales gauge.

Hovnanian Enterprises Inc., the largest homebuilder in New Jersey, on Dec. 22 reported a fourth-quarter loss bigger than analysts expected as revenue fell 19 percent.

“The year can generally be described as one where we and the industry were bouncing along the bottom,” Chief Executive Officer Ara Hovnanian said on a conference call.

Even so, economists in the past two weeks have boosted projections for fourth-quarter growth, reflecting a pickup in consumer spending and passage of an $858 billion bill extending all Bush-era tax cuts for two years.

http://www.bloomberg.com/news/2010-12-30/pending-sales-of-existing-homes-rose-3-5-in-november-exceeding-forecasts.html

"Put It All Back" Gains Mainstream Credence

From Randall Wray @ Bengiza

(also writing at Huffington Post)

Dec. 31, 2010

It is time to push the reset button. All foreclosures should be stopped immediately. The REMIC trustees should be audited to see if they have properly followed the requirements of the PSAs and laws applying to REMICs. If they do not have the notes, the securities should be put back to the banks. If the banks cannot absorb the losses, they must be closed and resolved. The FDIC in turn will end up with the mortgage backed securities and underlying mortgages. Working with Freddie and Fannie, all of these should be modified, into new fixed rate mortgages—with a “clawback” to reset principle to current market value of the homes, and with new notes. Investors are going to take losses so there will be fall-out that government will have to address. There will be hundreds of billions of dollars of losses. Congress must find a way to mitigate effects on the economy as well as on investors in MBSs and other assets related to real estate. This is a big problem, but it is not insurmountable.

Yep.

From 2010-10-11:

It is time to take this edifice and throw it in the trashcan, after forcing its members to fix all the titles they have damaged - at their expense - and record true and correct assignment information.

Oh wait - that's a problem isn't it..... what if the assignments never actually happened, and the REMICs hold an empty box? Why that could get messy..... Hmmmm....

And before, in May of this year, I said:

I recently spoke with an attorney who is aggressively pursing these issues when his clients are faced with foreclosure, with some (and likely growing) success. He related to me that he spoke with the FCIC and was asked "Well, what is your solution? Are you asking that we nationalize all the (large) banks?"

If that's not an admission that FCIC knows the large banks were and are complicit in this and if forced to admit the truth in their financial statements would be rendered insolvent I don't know what is.

Note that the FCIC studiously avoided talking about this "wee problem" in their reports thus far, and now they're "done." Uh huh. That's yet more willful blindness folks.

What did I say at the time?

Now we're faced with having structuralized a $1.5 trillion annual budget deficit into the indefinite future while those who were "helped" by HAMP and similar programs are facing re-default a few months to a couple of years down the road. DTIs over 60% virtually guarantee that outcome. At the same time the holders of these notes were sold a bill of goods and eventually some of them will wise up to the fact that the so-called "bankruptcy remote trusts" that allegedly hold the paper (and thus immunize the banks that created them) are legally defective. Those holders, when (not if) they suffer actual principal and coupon loss, can be reasonably expected to pursue their remedies at law with the aim of voiding the trust and opening the assets of the creating financial institution to attack.

If this line of inquiry is pursued it is entirely possible that these trusts would in fact be voided, and the resulting exposure landing on the major financial institution balance sheets would render them insolvent.

You heard it here first.

http://market-ticker.org/akcs-www?post=175887

The Dead Sign Affidavits - Nationwide

Karl Denninger

Market-Ticker.com

Dec. 31, 2010

When are we going to see law enforcement actually enforce laws?

She died in 1995. Yet her signature later appeared on thousands of affidavits submitted by one of the nation's largest debt collectors, Portfolio Recovery Associates Inc., in lawsuits filed against borrowers.

Some regulators complain that the use of Ms. Kunkle's name reflects an epidemic of mass-produced, sloppy and inaccurate documentation in the debt-collection industry.

Complain? Sloppy? Inaccurate?

Perjury is a felony!

And using the signature of a dead person sure looks like perjury to me (can't swear to what you can't see because you're dead!) along with "uttering" - that is, forgery.

It has to be forgery since the person is dead, right?

"When you see corner-cutting like this, it's alarming," Minnesota Attorney General Lori Swanson said about the Kunkle case.

Corner-cutting?

The State Attorney General for Minnesota calls this corner-cutting?

I guess robbing a bank in your jurisdiction would be "corner cutting" when it comes to acquisition of money, right? It's just an easier way to get money than actually earning it honestly.

Law enforcement, including attorneys' general, sucking off banksters and their cohorts in the "debt collection" industry is an outrage. These are not "cut corners" they're apparent felonies and must be investigated and prosecuted as exactly that.

What The Attorneys General of this nation at both Federal and State level have proved, beyond any reasonable doubt, over the last three years is this:

There is no longer a rule of law in this nation and there are no longer law-enforcement agencies that will enforce the law when the party harmed is an ordinary citizen. None. Neither political party will bring a single felony-level charge against these jackals.

I leave to the reader's own determination what sort of response is appropriate in light of the continuing documentation that willful and intentional refusal to investigate and prosecute apparent felonious acts is not an isolated incident but rather has become the standard and expected procedure and response by alleged "law enforcement" at the highest levels of our government when it comes to those firms, including but not limited to banks and collection agencies.

http://market-ticker.org/akcs-www?post=176183

Real Estate Spin Continues by Mainstream Media

Greg Hunter

USA WatchDog.com

27 December 2010

The mainstream media was at it again last week–putting a positive spin on the awful real estate market. The USA Today headline on top of the “Money” section last Thursday read “Optimism for home sales adds up.” The story said, “The trend is starting to move in the right direction,” says Diane Swonk, chief economist at financial services firm Mesirow Financial. A string of new housing data is building optimism. Existing home sales in November rose 5.6% from October to a seasonally adjusted annual rate of 4.68 million, the National Association of Realtors reported Wednesday. Demand has steadily improved since bottoming in July following the end of the buyers’ tax credit.” (Click here for the complete USA Today story.)

The headline and the beginning of the story would lead you to believe everything is turning around and the worst of the housing meltdown is behind us. The article failed to include the true context of that whopping 5.6% rise in sales. Here’s how Marketwatch.com reported the exact same story, “Sales of existing homes rose 5.6% to a seasonally-adjusted annualized rate of 4.68 million, the National Association of Realtors said Wednesday . . . Even so, sales were still 27.9% below prior-year levels and below the 5.26 million in June when a homebuyer tax credit existed.” (Click here to read the complete Marketwatch.com story.) Yes, the spin from USA Today left out the fact home sales were still nearly 28% below last year’s levels.

This is despite the homebuyer tax credit program that doled out up to $8,000 for buying a home. USA Today buried the real headline and that was this little morsel, “Home prices, down almost 30% from their 2006 peak, will fall 5% to 7% more before potentially rebounding later in the year, says Patrick Newport, IHS Global Insight economist. Banks will repossess 1 million U.S. homes next year, on top of 1 million this year, says market researcher RealtyTrac.” How are back to back years with millions of “home repossessions” and declining prices of another “5% to 7%” not the lead in a story? What does “Optimism for home sales adds up,” mean? Optimism adds up to another million foreclosures and another price decline? This is just another attempt to put lipstick on a pig of a housing market.

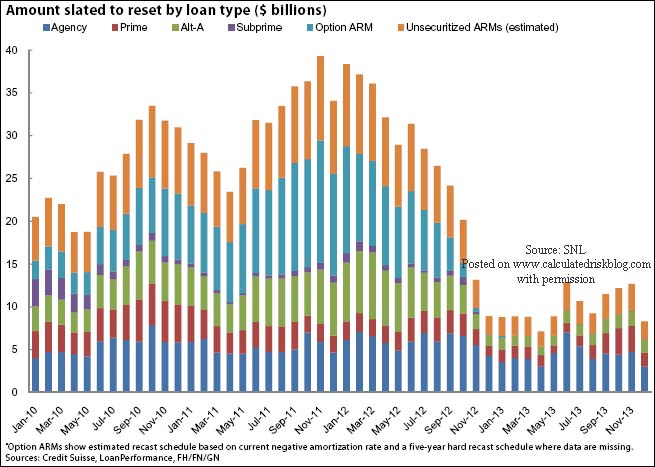

The best road map of where housing is going in the next couple of years can be foretold by looking at this mortgage reset chart from Credit Suisse. (see below) Look at the tsunami of mortgage resets for all sorts of Adjustable Rate Mortgages that don’t fall off until the end of 2012. I know I have used this chart in the past, but when it comes to predicting the real estate market, this is the proverbial picture that is worth a thousand words!

In the latest report from Shadowstats.com, economist John Williams says the “housing crisis appears to be intensifying.” Here’s what Williams says the so-called “recovery” looks like on a graph when it comes to housing start data. Do you see any recovery there? Is that what a “move in the right direction” looks like?

The NAR and USA Today omitted an important fact about those 4.68 million sales of existing homes. Williams says, “Foreclosure activity remained a major distorting factor for home sales, with “distressed” activity accounting for an estimated 33% of existing sales in the NAR’s November reporting. . .”

That means 1/3 (1.56 million homes) of that 4.68 million total were foreclosure sales. There’s not much “optimism” for the million and a half families who lost their homes this year. There is just no good way to spin that American tragedy.

http://usawatchdog.com/real-estate-spin-continues-by-mainstream-media/

Banks Behaving Badly: Mistaken Foreclosures Roll On

Scott Van Voorhis

December 27, 2010

Imagine returning from a visit to grandma over the holiday weekend to find your house padlocked and your furniture and possessions cleaned out.

Then imagine your shock at finding out, after you called 911, the perpetrator was not some low-life burglar but your mortgage lender.

How could this be, you might ask, having never skipped a mortgage payment?

Well it's a question homeowners across the country continue to ask as the problem of "mistaken foreclosures" continues, despite months of negative publicity for some of the nation's top banks.

In one of the more recent cases, a Florida couple worked out a loan modification agreement and was making all their payments when they received a devastating letter from J.P. Morgan Chase. Their condo, Magaly Cervantes and Julio Bermudez, was told, had been foreclosed on and sold online.

A trip to the local courthouse led nowhere - the bank only began reviewing the case after some embarrassing attention from The Wall Street Journal.

Other cases are even more heart rending. A Pittsburgh woman who was not in default on her mortgage returned home from work one day last year to find her house padlocked, the utilities cut off and her parrot, Luke, gone.

Angela Iannelli finally got her parrot back, though the bank made her drive out of her way to pick Luke up. She is now negotiating a settlement with the bank.

Mimi Ash recently filed suit against the Bank of America after her ski chalet was cleared out and padlocked and her possessions - including her late husband's ashes - hauled away. She was behind on her payments, but had been trying to catch up

Others, while their homes have yet to be seized, have had to spend thousands on legal fees to fight off erroneous foreclosure filings by their lenders.

Warren Nyerges was particularly shocked to be hit with a foreclosure notice. After all, he bought his $165,000 Naples, Fla., home back in 2009 with cash.

But despite waiving a copy of the cashier's check in front of multiple bank employees, Nyerges was forced to hire a lawyer and go to court before the bank would back down, The Huffington Post reports in an excellent story detailing the growing number of foreclosure snafus.

There's a common theme here. Once you have been thrown onto the foreclosure assembly line, even if you are a victim of mistaken identity, it can be hard if not near impossible to get off.

Reading these stories is enough to make anyone fume. But the defense offered by the banks is even worse.

The line goes something like this: Sorry, we are struggling to process an unprecedented number of foreclosures and it's inevitable that mistakes will happen along the way. Anyway, such cases are rare and we are constantly upgrading our procedures.

How in the world is this defense acceptable?

It's akin to the airline industry saying, after a flurry of tragic crashes, that we all just have to accept that mistakes will happen and people will die occasionally. After all, ten million people made it to their destinations safely during the same time period.

You can just imagine what Congress, prodded by an angry electorate, might do when confronted with such an obtuse and insensitive defense.

Well this kind of lame-brain defense shouldn't fly either for the banking industry.

OK, we are not talking about the loss of life here. But certainly property rights - and the freedom from fear that your livelihood or home or possessions can be randomly seized by either a government agency or a corporate bureaucracy - is key part of what holds our free market, democratic society together.

No city or state government would last long in office if it began seizing the homes of upstanding citizens for nonpayment of taxes and then responded, when confronted by its errors, by dragging its feet.

So how does a key part of the private sector get away with behavior that would have made the Soviet bureaucrats of old crack a smile?

http://www.boston.com/realestate/news/blogs/renow/2010/12/banks_behaving.html

Faces of the Home-Foreclosure Crisis

The Tidal Wave of Defaults and Delinquencies That Began Four Years Ago Has Hit Individuals at All Levels of Society

WSJ.com

Dec. 30, 2010

The foreclosure crisis that erupted four years ago has claimed more than five million American homes—about 10% of all homes with a mortgage. It began in lower-income neighborhoods and has spread to some of the most exclusive addresses in the U.S.

The seeds of the crisis were planted a decade ago when banks, discovering the high returns from selling bundles of securitized mortgages, relaxed lending standards and originated millions of adjustable-rate subprime mortgages. Such loans were designed to allow just about anyone to get a home loan.

When interest rates on the adjustable-rate mortgages finally climbed, many borrowers began falling behind on their payments, leading to the first wave of delinquencies and defaults.

At the start of 2008, with the U.S. economy weakening and job losses multiplying, the defaults began to spread as millions of Americans with plain-vanilla prime mortgages also ran into trouble making their payments. In some cases, borrowers found they had paid inflated prices for homes they could no longer afford. Others got into trouble by or borrowing against the equity in their homes. According to the Federal Reserve, Americans withdrew more than $1.1 trillion of equity from homes in 2006 and 2007.

By the end of 2008, with home values plunging, one in six homeowners found themselves underwater—owing more on their homes than they were worth. Borrowers, even those with stable jobs, began to see such negative equity as a reason to stop making their payments. That triggered the third wave of the foreclosure crisis: the strategic default.

The Obama administration is working with banks to head off future defaults and stanch the foreclosure wave by modifying mortgages. The federal programs have so far disappointed. The Home Affordable Modification Program, for example, was launched in the summer of 2009 with the intention of modifying three million to four million loans. So far, it has provided permanent help to fewer than 450,000 struggling borrowers.

Here are six stories of people caught in the foreclosure crisis, by circumstance or choice—from those who fell victim to hard times to others who squandered equity on cash purchases.

The crisis looks set to continue. Another four million people are in danger of losing their homes, according to the Mortgage Bankers Association. And until foreclosures are cleared, the housing market is unlikely to recover.

The foreclosures have had a silver lining for one group of Americans: Many families locked out of the housing market during the boom can now afford to buy.

—Robbie Whelan

Loan Choice Proved Costly

When Ghislaine Apollon emigrated from Haiti to the U.S. in 1974, she dreamed of owning a home. In 1997, after years of scraping by, she bought a fixer-upper in the Queens section of New York City.

Her original $147,000 mortgage was affordable on her income of about $1,600 a month from working in a hospital linen department, she said. Ms. Apollon then made some costly choices. First, she refinanced several times and took out large amounts of cash, pushing her loan balance to nearly $400,000. And the last time she refinanced she ended up with an option adjustable-rate mortgage, which lets borrowers select from different payment choices. Ms. Apollon, like many borrowers, opted to pay the minimum, which adds to the balance.

Option ARMs have become the focus of state investigations and lawsuits by borrowers who believe they were misinformed about the loan's complicated structure.

Consumer advocates say such option ARMs have proven a problem nationwide. "Every option ARM that we've seen has been delinquent," said Farida Rampersaud, director of the Foreclosure Prevention Services Program at the Ridgewood Bushwick Senior Citizens Council Inc. in Brooklyn, N.Y. "In most instances, the homeowner doesn't understand the nature of the product."

Trouble for Ms. Apollon started almost as soon as she moved into the single-story home. The ceiling leaked; the basement flooded several times. She refinanced several times to fund repairs, ratcheting up her monthly payments each time.

Ms. Apollon refinanced a final time in 2007 with Countrywide Financial Corp., which was acquired by Bank of America in 2008. This time, she wasn't looking to pull out money, but to get into a mortgage with more affordable payments. Ms. Apollon said she was stunned when she realized the consequences of her decision to make minimum payments: After a few years, "my mortgage went up and up and up" to $1,700 a month.

Realizing she would have to pay much more than that a month to start reducing her loan balance, Ms. Apollon sought a loan modification. She is being helped by Neighborhood Housing Services of Jamaica, a nonprofit.She wants a plain fixed-rate mortgage that doesn't grow.

Lenders aren't granting nearly as many loan modifications as consumer advocates would like, but Ms. Apollon has a few things in her favor. Under a 2008 settlement with several state attorneys-general over charges of predatory lending by Countrywide, Bank of America agreed to modify the terms of certain subprime and option ARM mortgages.The bank said it reviewed Ms. Apollon for that program in August 2009, but "her financial situation did not support a modification."

She was denied a modification under a government program earlier this year and stopped making payments in October. Bank of America said it was reviewing her request for a modification.

Ms. Apollon -- who receives extra income by renting part of the home to a relative -- has been depositing $1,600 a month into an account to get her mortgage back on track if she's granted a modification and to show that "I'm willing to pay," she said.

—Dawn Wotapka

Lost: A Business, Then a House

Like other people whose fortunes were tied to real estate, Sidney Banner has suffered a one-two punch from the downturn.

In 2008, he lost his small, family-run commercial-mortgage brokerage business, when tighter lending requirements made it difficult to finance sales of commercial properties.

This month, the 84-year-old Mr. Banner and his wife lost their 3,200-square-foot home in an affluent section of Boca Raton, Fla. They've moved into an 880-square-foot rental apartment in a modest neighborhood of Palm Beach County, cutting their monthly housing expenses from $2,600 to $400.

Mr. Banner bought his house 22 years ago for $296,000. By 2007, the house was valued at $429,000. Like many other homeowners at the time, Mr. Banner tapped the equity in his home by taking out a $250,000 loan. He used the money to try to keep his business afloat as the real-estate market unraveled.

A year later, Mr. Banner defaulted on his first and second mortgages; the value of his home fell to $350,000. It is now scheduled for auction in January at a foreclosure sale.

"When things were good, making payments was easy," Mr. Banner said. "But now I've cut down to the bone, to the point that we can live on Social Security payments."

Many former mortgage brokers have been able to find new jobs working for banks and other companies. But Mr. Banner typifies one problem facing older Americans: the difficulty of finding employment. Only about 6.1 million of the 38 million Americans aged 65 or older were employed in 2009, according to the Bureau of Labor Statistics.

For two years, Mr. Banner and his wife received $1,200 a month in unemployment payments, in addition to their $3,200 social-security checks. The unemployment payments have now run out, so Mr. Banner said he was going back to work. He hopes to start a company brokering small commercial-real-estate loans to borrowers he finds through online advertising and Craigslist.

Mr. Banner said the foreclosure may have been a blessing in disguise: "My wife and I are both very much more relaxed now that we walked away from this enormous responsibility, and all these people calling us every day, looking for something they're not going to get."

—Robbie Whelan

After the Good Life Goes Sour

Like many Americans who saw their home values shoot up during the housing boom, Christine Carr found lots of ways to spend her equity windfall.

A decade ago, she and her husband paid nearly $180,000 for a three-bedroom home in Dallas, N.C., outside Charlotte. Their income easily covered the $1,100 monthly mortgage payment.

In 2006, after discovering the house's value had skyrocketed by $100,000, the couple took out a second mortgage and got cash. They bought a $70,000 camper, took a cruise to Alaska and vacationed in Belize. The new loan added $698 to the couple's monthly payment.

"We had a ball," she said.

Three years later, her husband moved out and stopped contributing to the mortgage payments, she said. Then she lost her job as a consulting firm's marketing manager. In April 2009, Ms. Carr put the house on the market for about $235,000. With no income, Ms. Carr, now divorced, didn't qualify for a loan modification, which would have lowered her mortgage payment.

In July 2009, she asked the lender, Bank of America, to let her hand over the home to avoid the foreclosure process. But the two sides couldn't come to terms.

With no interest from buyers, Ms. Carr stopped making payments that August. "It was a gut-wrenching decision," the 46-year-old woman said. "I was raised to live up to my commitments."

These days, she receives a monthly statement that details the swelling late fees and penalties for both of her loans. Although she found work in March this year, Ms. Carr said she had no intention of paying: She has moved to a rental and her Dallas home sits abandoned. The luxury camper was sold for "a lot less" than the purchase price, she said.

Ms. Carr said she felt guilty but was ready to move on. "It makes me sick to my stomach sometimes, just thinking about it," she said. "But once you make the decision, you stick with it."

—Dawn Wotapka

Housing Nightmare Is a Dream for Some

Last year, Bret Sands and his fiancee, Fysah Thomas, shared a cramped $600-a-month studio apartment. Today, they're living in a Seattle lakefront property with three bedrooms, hardwood floors and a spiral staircase.

"This is a freaking dream house," said Mr. Sands. still giddy months after purchasing the home in March.

If there's an upside to the foreclosure crisis, it is largely enjoyed by people like Mr. Sands and Ms. Thomas: They can now afford to buy. He's a surveyor of marine vessels and she's the lead vocalist in a band. Both watched the mid-decade housing boom pass them by, thinking they'd never be able to join.

Then the bubble burst. According to the Case-Shiller Home Price Indices, prices in Seattle through October were about 25% off their July 2007 peak—with single-family homes now selling at a median price of $481,000, according to the local multiple listing service.

In 2008, Mr. Sands, age 34, started to see the stock market falter and grew worried about his retirement savings account. He took $60,000 out of the account, and with an eye on plummeting home prices, he and Ms. Thomas decided to buy a house.

They never intended to buy a foreclosure but nothing else fit their budget.

After two months and about 30 tours with SeattleHome.com real estate broker Sam DeBord they found their house. It went into foreclosure when its owner's restaurant went belly up. Ms. Thomas saw it during a random web search. The couple paid $232,000 for a house that in 2007 had been appraised at $300,000. One of its main attractions: It sits among much larger, half-million-dollar homes along Angle Lake.

"We wouldn't have been able to afford a house if the market hadn't dropped," Mr. Sands said.

With help from friends and Ms. Thomas's carpenter father, they have embarked on renovations: paint, French doors, new bathroom, new kitchen.

Because the house needed so much work, Mr. Sands kept a lot of his cash to pay for renovations. He put about $9,000 down under a loan insured by the Federal Housing Administration.

"It should be an inspiration to any other people like us," Ms. Thomas said. "Being able to buy a home is one of the most important decisions you can make."

—Mitra Kalita

Falling Value Ruled Out Refinancing

Kelli Kobor and her husband thought they were making a safe investment in 2004 when they made a $350,000 down payment on the $1.3 million purchase of their five-bedroom Dutch colonial in Kenilworth, Ill., a wealthy suburb on Chicago's North Shore.

Ms. Kobor and her husband have no other debt. They never refinanced or took out a second mortgage. But like many other Americans, they ran into trouble making their mortgage payments last year after Ms. Kobor's husband lost his job and later found a new one that paid much less.

Their home had fallen in value, wiping out any equity and making it impossible to refinance. Ms. Kobor wasn't eligible for the government's loan-modification programs because her loan was too large; her mortgage servicer offered a six-month interest-rate reduction that tacked the payment shortfall onto their loan.

Tired of feeling "strung along," they ultimately surrendered the home to the bank in what's known as a deed-in-lieu of foreclosure, and moved out in August. They now rent a three-bedroom ranch-style home in Deerfield, about 10 miles away.