News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

We're All Going to Pay For the Housing Mess

Adam Brochert

Goldversuspaper.blogspot.com

September 21, 2009

The citizens of the United States will be paying to clean up the collapse of the real estate bubble. It doesn't matter if one participated in the housing boom or not - we are all going to pay and pay dearly for this mess. Renters, owners and speculators are all equally on the hook if they are taxpayers (did you know that 40% of people living in the U.S. pay or owe no federal income tax?). http://www.taxfoundation.org/news/show/1410.html

Now it is true that those who go through a foreclosure or bankruptcy will have much stress and will take a big hit on their credit score. Those who avoided the bubble, have paid off their house in full and/or don't look at their home as an investment but rather a place to live won't have to deal with these stressors, assuming they don't become a victim of unemployment in the months ahead.

But make no mistake about it, a big chunk of the losses from the housing bubble are going to be put on the taxpayer's tab. The first round of the "bailout ball" was forced upon the unsuspecting American citizenry by Hanky Panky Paulson and his crew to "save the world" from a certain and horrible economic death. The second and third rounds will involve similar sums of money but will come from different angles.

First and most obvious is the number of bank bailouts that the FDIC, and thus the American people, will need to fund. The FDIC will absolutely tap its new $500 billion line of credit from the U.S. Treasury http://online.wsj.com/article/SB125328162000123101.html . To pretend otherwise is silly and/or dishonest, as hundreds of additional banks are going to fail before this fiasco is over. In the linked article above, Sheila Bair is quoted as saying:

"Marking banking assets to market prices doesn't make sense."

No, of course it doesn't make sense. Telling the truth and doing the rational and responsible thing would immediately bankrupt our entire banking system overnight. It is much better to pretend that you haven't lost any money on any of the assets you have and instead tell people that they are still worth what you paid for them, even if their value has been reduced to zero. This is our government-banker keiretsu hard at work discouraging reality, honesty and integrity. If the head of the FDIC feels this way, there is no hope for improved transparency of bank balance sheets and no realistic way to fairly value these banking firms (Stay away! Sell!).

In the mean time, these bank "assets" are trending towards zero or less than zero (in the case of some derivative instruments and homes that have gone through severe "trash outs"), which means that when the FDIC finally does step in, it will cost U.S. taxpayers much more than biting the bullet and bailing out these banks now. All the profits for bankers are and will remain privatized but any and all of the big losses will be put on the taxpayer's tab as much as possible. The larger banks are not stupid and have found a way to try to salvage some extra profits out of this mess (in addition to being able to stay in business) by asking their pre-bought bureaucrats to jump into the shark pool.

This is where the second of the two remaining big components of the government housing bailout comes into play. This is even more nefarious than the direct bank bailouts. It has to do with Freddie Mac, Fannie Mae, the FHA and Ginnie Mae. These institutions are now guaranteeing 90% of new home loans generated in this country, including the refinancing and modification of loans gone bad. Why make lots of loans in the middle of a real estate collapse? Oh yeah, I forgot - it's because all the inevitable losses will just be put on the taxpayer's tab, so who cares?

This is, in essence, a transfer of toxic loans from private balance sheets to the government balance sheet. Underwriting standards have been subprime and lax for these new government-sponsored loans. Private mortgage originators are going hog wild signing up anyone with a pulse who still wants to buy a house (Don't buy - rent!) if they can meet the government standards because these originators know they can turn around and pass the hot potato onto the government, making a profit/commission in the process.

In the mean time, these loans are already going bad at a alarming rate akin to subprime loans. Capital reserves are dangerously low at the government sponsored entities and rapidly declining, which means more taxpayer money will be needed down the road to bail these quasi-companies out (don't believe articles like this where officials say they won't need extra funding - they will). The low down payments and lax lending standards required for many home loans are what helped get us into trouble in the first place and I would hazard a guess that many of the home owners partaking of these new toxic government loans are going to be close to underwater by the time the ink dries on the final loan documents.

This scheme is also why private banks are ignoring overdue debtors for up to 2 years without finishing the foreclosure process. Not only have Sheila Bair and other apparatchik ilk encouraged private banks to avoid taking losses by allowing banks to keep home loans on the books as assets with an inflated and unrealistic value to bolster their balance sheet and make them look vaguely solvent, but the other part of the plan for banks is to stall while trying to find a way to get their toxic loans onto the books of Uncle Sam and the American taxpayer. They will find a way, believe me.

The private, non-federal, for-profit federal reserve corporation is warming up to the scam and moving things along nicely by purchasing large amounts of commercial and residential mortgage debt. This, of course, will all be foisted onto the taxpayer tab at the opportune time. When this occurs, it will sold as "an investment," but this will be yet another cruel joke on the American people.

So, in the end, it's all coming together for many bankers. The housing and commercial real estate collapse continues unabated and the bill is increasingly going to be put on the U.S. taxpayer's tab, allowing many bankers to get off scot-free and pocket some dough in the process. This moral hazard Uncle Sam is creating ensures more risk-taking and speculation in a real estate market the government has no business encouraging people to speculate in right now. It also absolutely guarantees an even bigger disaster down the road for Uncle Sam's balance sheet. Privatizing gains and socializing losses - damn it feels good to be a banksta!

Such moral hazard also encourages debtors to just walk away from any bad housing debts. When people aren't paying their mortgage, they rarely will make property tax payments, so this federal government interference/moral hazard and willful banker neglect of past due loans will also impact local governments tremendously. It is likely that these local governments will try to squeeze some blood out of a stone by asking those left standing who either own their homes or still pay their mortgage to pay higher property taxes. Being financially responsible increasingly means being asked to bend over and accept higher taxes and/or currency debasement while feeling "left out" of the debtor party.

Many citizens support the government "stabilizing" housing prices based on self interest. Yet such folks don't realize that government can only waste money while making things worse for the whole country and not doing anything but prolonging the pain that has to happen to allow the market to heal. Bad debts must be liquidated, not hidden or subsidized. Government cannot "stabilize" housing, but they can put lots of toxic liabilities on the taxpayer tab while the real estate market proceeds lower to the same levels it was going to go anyway.

Unfortunately, all of this government interference does mean that housing will take longer to find its true bottom - I think we're looking at 2014 or later. It also means that the government debt load is going to increase astronomically over the next few years (what's a few extra trillion, eh?), almost ensuring a serious currency dislocation at some point down the road. Be sure to watch with feigned amusement when the apparatchiks tell you in a year or two that no one saw it coming as the next bailout is announced or a currency crisis/capital flight rears its ugly head. Home sweet home, yeah right. We're all going to pay for the housing mess - one way or the other.

http://www.financialsense.com/fsu/editorials/brochert/2009/0921.html

The Bounce in the Housing Market, Interest rates and the Economy

Sol Palha

Tactical Investor

September 18, 2009

Science is a first-rate piece of furniture for a man's upper chamber, if it has common sense on the ground floor.

~ Oliver Wendell Holmes 1809-1894, American Author, Wit, Poet

Stories such as the one listed below are going to increase in the months to come; indeed since that story came out in June, we have seen articles of a similar nature advocating that real estate has put in a bottom and that its time to buy. At some point even the most sceptical will feel inclined to believe that the housing sector has put in a bottom.

For June, the Realtors group said its pending home sales index rose 3.6 percent to 94.6, from an upwardly revised reading of 91.3 in May. The last time there were five consecutive monthly gains was July 2003. The results were far better than analysts expected. Economists surveyed by Thomson Reuters expected the index to come in at 91.2. The report tracks signed contracts to purchase previously owned homes and is considered a barometer for future home sales. Typically there is a one- to two- month lag between a sales contract and a completed deal. The jump in pending home sales coincides with other positive trends in the residential real estate market.

For the first time in five years, home resales have risen for three months in a row, increasing almost 4 percent in June. Low prices, attractive mortgage rates and a first-time homebuyer’s tax credit of up to $8,000 have kick-started sales. "Because housing is so affordable in today's market, job security and the first-time buyer tax credit are bigger factors in influencing home sales," said Lawrence Yun, the Realtors group's chief economist, in a statement. Also Tuesday, homebuilder D.R. Horton Inc. said its fiscal third-quarter losses shrank from the year-ago period, as it took smaller charges against the falling values of its land and unsold homes. Yun said he expects existing home sales to gradually rise over the balance of the year, with conditions varying around the country. Full Story

Under normal conditions, we would also be inclined to believe that the housing sector has put in a bottom. However, conditions are far from normal, and we would like nothing more than to see the housing sector put in a long term bottom as soon as possible. In life what one wants and what one gets are always different, and as such there are too many factors that suggest a sustainable bottom cannot take hold now.

Some reasons behind the increase demand for homes

1) First time home buyers are being offered a credit of 8,000 which is fully tax deductible on the purchase of their first home.

2) Many individuals felt priced out of the market for the last few years and now that prices have fallen considerably they feel that they are getting a bargain.

3) To add to the allure of buying a house, low interest rates are being promoted and when combined with the above factors it can make for a very convincing story.

Regardless of the rosy picture so many experts are now painting, the factors that provide the foundation for a strong economy and in turn a strong housing sector are not there:

Unemployment numbers continue to rise. In addition the number of individuals who have been looking for a job in excess of 6 months continues to rise.

Salaries are not increasing or keeping up with inflation (do not believe the fake numbers that are put out, all one has to do is look at the cost of many necessities to see that inflationary forces are alive).

Even the post office is now ready to take drastic measures to cut down expenses (possibly closing up to 1000 branches). Almost every state in the US is facing rather large budget deficits, IRS tax receipts are down and while many companies are not firing as many employees as they were a few months ago, they are not aggressively hiring either.

Thus it is hard to imagine how this sector can make a strong come back if the Job market is sour. People spend money when they make money, but if they are not making as much or not making any, then going out and making a large purchase such as home is not an option. Let's not forget that most banks have now placed restrictions on how new loans are approved; gone are the days when you could just walk in and all you had to say was “ I want to buy a home” and then scratch your name on the contract and walk out with an approval. The trading desks of many large banks are now accounting for over 50% of their revenue; this illustrates that banks do not think the real estate sector is going to make a come back soon for they would rather risk playing the market than lend money to the consumer.

The one year housing index chart looks very bullish and if one looks just at this chart one would think that the good times are here to stay. From its low in March the index is up almost 100%, by any measure that is a stunning rally. It is now running into resistance and based on the current pattern it will most likely overcome this resistance after a few attempts.

The 3 year chart, however is very revealing and the rally does not look quite as impressive as it does in the 1 year chart. It is still trading a long way of its highs in the 250 plus ranges. We are not trying to throw cold water onto the scene and spoil the party. We would like nothing better than to join the party but cannot find any long term reasons to do so. The housing index could rally significantly higher from its current levels and the long term outlook would still remain bearish. If it manages to trade past 120 for 5 days In a row, the next target becomes 150; a weekly break past 150 and it could trade as high as 180 before resuming its long term downward trend.

The deficits are simply too high and the U.S. instead of putting the money, they print to good use (if there is such a thing as they don't really own the money in the 1st place), the government is instead spending money at an unsustainable rate. One does not rehabilitate a drunk by substituting cheap beer for expensive cognac; the only way to rehabilitate this chap is to cut his supply of booze and offer him treatment. The U.S. seems to think that the answer to our debt problems is taking on more debt.

Let's assume for some strange reason (one that we have missed or cannot locate) the real estate market actually recovers and starts a new long term up trend. The massive amount of money the Fed is creating is going to result in foreigners demanding significantly higher rates for the risks they are taking in purchasing US debt. The national deficit is at a stunning 11.68 trillion and rising. The year is not even over, and we have already added 1.4 trillion dollars to it, next year, we are going to add a minimum of another 1.2 trillion dollars and that's assuming things don't get worse. These figures do not include unfunded liabilities such as Social security, which is set to run out of money by 2029. The debt has continued to increase at an average rate of 3.96 billion dollars every single day since Sept 2007; the keyword is average for clearly we are running well above average this year.

Initial projections now are for the deficit to increase by an additional 9.3 trillion in 10 years; at the rate we are going, it's going to occur at a much faster pace. Soon annual deficits will account for 4% of the overall economy; a figure that history has proven to be unsustainable. In less than 10 years the total deficit will most likely exceed 82% of the overall economy and from there it there would be very little time left before the US crumbles. The big question going forward is how are we going to be able to pay the interest on this deficit, plus all the other unfunded programs that need capital, the biggest of which is Social security without going bankrupt?

Since 1969 Congress has spent more money than its income and people wonder why the average Americans spends more than he makes; the leaders are saying its okay to do so. Now for the kicker, the interest paid on the national debt is the third largest expense in the Federal budget. Defence is still the number one but one wonders how long it will hold this position. In 2006 interest payments totalled 405 billion, for 2007, they came in at 429 billion, for 2008 the figure was 451 billion and as of June 2009, total interest payment are 320 billion dollars. In comparison the budget at NASA is 14 billion, the education budget is 61 billion and Dept of transportation has a budget of 56 billion only. It makes one wonder what the government is thinking. One would think that congress would start spending less but as each year passes, they spend more. We are soon going to arrive at a point where the interest payment alone will exceed 1 trillion dollars; many nations’ economies do not even account for half of this amount, and yet they remain solvent. The US with the world’s largest economy cannot live within its means. Given the current rate at which the US is printing money, the unthinkable might just become a reality. The U.S might be pushed into bankruptcy. History is a wonderful subject, it provides a clear guideline of not only what was done but will occur again. History always repeats itself.

The U.S. has two options, declare bankruptcy, or start to implement massive budget cuts and raises taxes; there are no other options. The cuts will have to be huge for they will wait until the end to implement them; every administration wants to look good and simply passes the buck to the next administration.

We do not know how the things will unfold exactly, but any person with simple common sense understands that something will have to give otherwise the whole system will fall apart. The debt is now 11.68 trillion, in a few years it will hit 15 trillion, and in less than 10 years it could be well over 19 trillion. Overseas investors are already questioning the logic of investing in a nation that has no regard for its currency whatsoever; how long will they continue to buy this debt when interest rates are so low? They are going to start screaming for higher rates and as the US creates more money, they will demand even higher rates and so a vicious cycle will unfold. Rates could eventually hit the 20-25 percent mark.

This is why we find it very hard to believe that the real estate sector has put in a long term bottom, for the top players are doing everything in their power to debase the US currency. Real Estate does not perform well in a high interest rate environment.

Conclusion

The housing sector and the financial sectors are the back bones of this country's economy and if both are still in trouble, it becomes very hard to make a good argument for a long term bounce in the real estate sector. This does not mean that the real estate sector cannot experience a pretty strong bounce in the short term time frames, but it does mean that this bounce is not sustainable.

The interest payments on our national debt are staggering and anyone with a bit of common sense can see that this trend is not sustainable. The government bickers when it has provide extra funding to local programs but they have no problems almost spending close to half a trillion dollars annually on the interest that is due on our national debt.

The world at large has entered into the phase of extremes; the situation is either very good or very bad. Look when the markets were crashing early this year they crashed hard, when they started to rally, they mounted an incredibly strong rally. There is no in between stage; the same trend is pushed to the limit until it is completely unsustainable and the correction or the move upwards is usually extremely explosive. These movements are reflective of the world we will live in today.

Fed funds rate is trading at multi decade lows; this market has been in a bear market for almost 27 years. This is a very very long time and thus once a new trend starts, one can expect it to last for a very long time; it’s just a matter of time before this market experiences a trend change as it is now trading at a very extreme point. Extreme conditions never last forever. From a long term perspective, one has to start preparing for a high interest rate environment.

The bond market has rallied towards super bubble proportions, and it is therefore, destined to mount an equally strong correction. A foretaste of what lies in store was seen this Jan when the bond market mounted a very strong correction. From its high to its recent low in the middle of June the bond market experienced a 20% correction. This is a very large move considering that it took place in just a span of 6 months.

Interest rates will probably test their lows once more and bonds, on the other hand will test their highs one more time before putting in a multi year top formation. Interest rates are at historic lows, and as such they cannot stay at these levels forever, especially when the Fed is printing new money at a mind boggling rate.

Additional Negative Development

Consumers cut down debt levels by a whopping 21.6 billion in July; this amounts to annual decline of 10%. Economists were expecting credit to drop by 4 billion. For an economy that only expands when more debt is taken on (76% of our GDP is based on consumer spending) the long term growth prospects appear to be rather dim.

The story below also highlights how this economic down turn is affecting the entire world. Under normal conditions such a massive drop in real estate prices coupled with a weak dollar would attract droves of overseas investors but instead the opposite has occurred.

Interest in U.S. real estate by international buyers declined due to the worldwide recession and severe credit crunch, according to the 2009 National Association of Realtors® Profile of International Home Buying Activity.

The share of Realtor® clientele who are foreign buyers is smaller than in previous years, but among those purchasing nearly half paid all cash – bypassing the mortgage process. Twenty-three percent of survey respondents served at least one international client in the 12-month period between the end of May 2008 and the end of May 2009, down from 26 percent in the 2008 study. During this period an estimated 154,000 homes were sold to foreign nationals, which is down from approximately 170,000 international transactions during the previous 12 months. Full Story http://www.realtor.org/press_room/news_releases/2009/09/crunch_international

Finally, a very funny thing occurred in Zimbabwe before hyperinflation struck that nation. Individuals started to purchase treasuries driving yields (interest rates) lower and then out of no where they were hit with inflationary forces which later morphed into hyperinflation. Is not the exact same thing taking place in the United States? From Nov to Dec 08, individuals poured money into the bond market even though their rate of return when adjusted when adjusted for inflation was zero at best and negative at worst. History sadly always repeats itself. In 1980 one Zimbabwe dollar was roughly equivalent to one US dollar; today it takes almost 6 trillion Zimbabwe dollars to buy 1 USD.

No market can remain in a bullish or a bearish phase forever; at some point, the trend will change. Investors who are still holding onto adjustable rate mortgages or who have fixed rate mortgages that were obtained at much higher rates should re finance and lock in these low rates now. If you can sell for a profit or break even, then your best bet would be to get out now as prices are destined to fall much more in the years to come.

Use Strong pull backs in the Gold, Silver and Palladium markets to add to your bullion positions. Individuals willing to take on a bit more risk can purchase a basket of stocks connected to the commodity's sector; use strong pull backs to open up new positions or add to your current ones.

http://news.goldseek.com/TacticalInvestor/1253293200.php

Housing Suffering Relapse Confronts Bernanke Credit Conundrum

Kathleen M. Howley and Rich Miller

Sept. 21, 2009

Bloomberg

The recovering housing market may be heading for a relapse as President Barack Obama and Federal Reserve Chairman Ben S. Bernanke consider ending support for the source of the global financial crisis.

The Obama administration is studying whether to let a first-time home buyers’ tax credit expire as scheduled at the end of November. Bernanke and his Fed colleagues may continue talking this week about how to wind down purchases of mortgage- backed securities, according to Peter Hooper, chief economist at Deutsche Bank Securities Inc. in New York. The two programs have helped stabilize real-estate demand, with new-house sales rising 9.6 percent in July from the prior month, the most since 2005.

Ending these efforts may stifle the housing rebound by depressing sales and pushing up both mortgage-backed bond yields and interest rates on home loans, even in the face of the record-low zero to 0.25 percent short-term rates the Fed has engineered, said economist Thomas Lawler. A weaker housing market would likely dampen the economic recovery and undercut shares of builders including Fort Worth, Texas-based D.R. Horton Inc. and Miami-based Lennar Corp., that have risen 40 percent this year, based on the Standard and Poor’s Supercomposite Homebuilding Index of 12 companies.

“Things could get ugly,” said Lawler, an independent consultant in Leesburg, Virginia, who spent 22 years at Fannie Mae, a Washington, D.C.-based government-controlled mortgage- finance company. “We could be facing a triple whammy at the end of the year: the expiration of the tax credit, the end of the Fed mortgage-buying program and rising foreclosures.”

Major Test

This is the first major test of policy makers’ ability to coordinate exit strategies as they seek to wean the economy off government support, said Brian Bethune, chief financial economist of IHS Global Insight, a forecasting company in Lexington, Massachusetts.

They have already acted separately, with the administration ending its $3 billion “cash-for-clunkers” automobile trade-in program on Aug. 24 and the Fed starting to wind down its purchases of Treasury debt, which totaled $285.2 billion between March 25, when the initiative began, and Sept. 16.

The 55-year-old Bernanke and his colleagues, who meet tomorrow and Wednesday to map monetary strategy, discussed “tapering” off the Fed’s purchases of mortgage-backed securities and housing-agency debt at their last gathering in August, according to the minutes of that meeting. No decision was made by the central bank’s policy-making Federal Open Market Committee.

Mortgage-Backed Securities

Under the current program, the Fed is scheduled to buy up to $1.25 trillion of mortgage-backed securities and $200 billion of agency debt by the end of the year. So far, it has purchased $862 billion of the former and $125 billion of the latter.

A trio of Fed presidents -- Jeffrey Lacker of Richmond, James Bullard of St. Louis and Dennis Lockhart of Atlanta -- has publicly raised the possibility the central bank might not spend all the money authorized for the mortgage-backed securities. Lacker questioned whether the economy needs the additional stimulus in an Aug. 27 speech.

New York Fed President William Dudley, who is vice chairman of the FOMC, has sounded more cautious.

“The market expects us to complete these programs,” he said Aug 31. “To contradict that market expectation is a pretty high hurdle.”

Abrupt Stop

An abrupt stop might push up mortgage rates by a half to one percentage point, said Hooper, a former Fed official. Tapering off -- by reducing weekly purchases and stretching them beyond the end of the year -- would have a more muted effect, pushing rates up by at least a quarter percentage point, he said, adding that the Fed may announce just such a strategy after its meeting this week.

Mortgage rates for 30-year fixed home loans averaged 5.04 percent in the week ended Sept. 17, down from 5.07 percent the previous week, according to McLean, Virginia-based Freddie Mac, a government-controlled mortgage-finance company.

Borrowing costs for home buyers are relatively high based on the historical relationship with the Fed’s target rate for overnight loans between banks, currently at zero to 0.25 percent.

The yield on the benchmark 10-year Treasury note is 3.22 percentage points more than the federal-funds rate, compared with an average of 1.45 percentage points during the past 20 years, according to data compiled by Bloomberg. Thirty-year mortgage rates average 1.69 percentage points more. While that is down from 3.19 percentage points in December, it is still above the average of 1.4 percentage points for this decade before the credit markets seized up in the second half of 2007.

Fed Purchases

The Fed’s purchases of mortgage-backed debt so far this year have dwarfed net issues of such securities by Fannie Mae, Freddie Mac and government-run mortgage-bond insurer Ginnie Mae, which totaled about $440 billion through the end of August, said Walt Schmidt, a mortgage-bond strategist in Chicago at FTN Financial.

Once the Fed exits the market, the spread between yields on mortgage-backed debt and Treasury securities will have to rise, perhaps by a half percentage point, in order to attract other buyers, he said. The spread now is about 140 to 145 basis points, down from around 215 at the start of the year.

“One of the key linchpins to the restabilization of our economy is getting housing back,” said Laurence Fink, chairman and chief executive officer of New York-based BlackRock Inc., the largest publicly traded U.S. money manager. “There is a great need” for the Fed to “continue to invest in the mortgage market right now,” added Fink, 56.

Crucial Extension

A number of Washington-based organizations -- the National Association of Home Builders, the National Association of Realtors and the Mortgage Bankers Association -- say an extension of the buyer’s tax credit is also crucial.

Lawrence Yun, chief economist of the realtors’ group, estimates that about 350,000 home sales through August were directly attributable to the tax credit of up to $8,000 for first-time buyers.

Treasury Secretary Timothy Geithner, 48, called signs of stabilization in the U.S. housing market “very encouraging” and told reporters on Sept. 17 that the Obama administration will take a “careful look” at extending the credit.

Congress may not pass an extension; the chances “seem slim,” said Mark Calabria, director of financial-regulation studies at the Cato Institute in Washington and a former staffer on the Senate Banking Committee. Public opposition to increasing the federal budget deficit is high, and there’s little appetite on Capitol Hill for finding spending cuts to offset the cost of the tax credit, he said.

Fastest Pace

The deficit will total $1.6 trillion this year as revenue falls and the government spends at the fastest pace in 57 years, according to the nonpartisan Congressional Budget Office.

In a sign of the public’s concern about the deficit, 62 percent of people surveyed in a Sept. 10-14 Bloomberg News poll said they would be willing to risk a longer-lasting recession to avoid more government spending.

The impact of terminating the tax credit will show up first in the new-home market, said David Crowe, chief economist of the home-builders’ association.

“It takes at least four months to build a house, and you need to buy it before Dec. 1 to qualify,” he said. “If you haven’t started building it by now, it’s too late.”

Housing Starts

Single-family housing starts fell 3 percent in August to a 479,000 annual rate -- the first decline since January -- according to seasonally adjusted figures in a Sept. 17 report from the Commerce Department.

Residential construction and home sales led the way out of the previous seven recessions going back to 1960, according to David Berson, chief economist of PMI Group, a mortgage insurer in Walnut Creek, California. Real-estate sales fuel consumer spending, which historically accounts for about 70 percent of gross domestic product, he said.

“Housing has been the sector of the economy with the largest multiplier effect,” said Berson, former chief economist at Fannie Mae. “Whether buying new homes or existing homes, people tend to fill them up with things: new furniture, new appliances, new window coverings.”

To be sure, some economists are betting the housing recovery is here to stay. The market has “clearly bottomed,” said Dean Maki, chief U.S. economist for Barclays Capital in New York.

Even some of the optimists are hedging their bets given how dependent the market has been on government and central bank support.

“I’m right in there with the rest of the cheerleaders, but there are no historical anecdotes, no historical data points to use for this,” said Lewis Ranieri, the 62-year-old mortgage- bond pioneer who is chairman of New York-based Hyperion Partners LP. The U.S. housing market is “still very fragile.”

To contact the reporters on this story: Kathleen M. Howley in Boston at kmhowley@bloomberg.netRich Miller in Washington rmiller28@bloomberg.net

http://search.bloomberg.com/search?q=Peter+Hooper&site=wnews&client=wnews&proxystylesheet=wnews&output=xml_no_dtd&ie=UTF-8&oe=UTF-8&filter=p&getfields=wnnis&sort=date:D:S:d1

fw: FORECLOSURES: They're Not Just For Breakfast

From: Jack Harper (jack.harperxxxx)

Sent: Thu 9/10/09 7:41 PM

To: xxxxxx

Hey! I'm working on the solution to this MEGA-PROBLEM.

Jack

World Freeman Society Public Forums....

Re: How to drive the banker crazy....

by charlesGGG » September 10th, 2009, 3:25 am

Hello All,

I would like to give many thanks to JackieG for the help and assistance accorded me and my sister a few months ago....and I now come back with the latest update.

My case is still yet to get to court (october period) but my sister's case has happened and is what i will comment on....Shady dealings.

As instructed, we sent off the prerequisite letters (based in UK) and visited 3 solicitors and 2 barristers all refused to take on the case some even said the legal arguement was sound but we should still "just comply" and pay the arrears on the mortgage and get-off with only a suspended court order and not full possession/forclosure.

So we decided, to hell with those cowards and went into court as litigates in person...THEN....THEN....THEN the most craziest hearing took place.

the original solicitor for the mortgage company withdrew and he was replaced with a new person (I think barister) who then admits that they've sold the mortgage - which is what we've been saying all along and therefore, they have no standing in court. And also they haven't produced the info we requested in the letters we sent previously and as such are in dishonor.

The criminal judge first of all refused to let me speak on the threat of being in contempt of court (property in my sisters name) and agreed to change the claimant/plaintiff right there and then from the old mortgage company to the new one, and by default rendering all the letters and all the evidence we submitted null and void. At this point I protested to not excepting their proof of new ownership without verification from the land registry etc and that the case should be adjourned for new evidence being introduced to court, but no joy. Thrown out of court and told to carry on paying the illegal mortgage to the so-callled new owner

"suspended possession order" ---Bastards.

Was advisd to have an informal discussion with another barrister (we wanted to appeal) but after he said alot of bollucks mainly about the costs, it kind of drained my energy especially knowing that I had to refresh for the next round in october.

So back at it sending off the letters---they are again not responding, telling them they are in dishonor etc etc and if they don't comply then i will consider the matter settled but all they will do is wait till they get to court and pull something sneaky again.....SO currently looking for methods to f@...ck them up legally if they try it. More coward solicitors still not wanting to take the case, those that do find it interesting also want large amount of MONEY upfront....don't trust them.

So far the score is 2-1 to them.

We will not go silently into the night.....!!!!!

For Commercial Real Estate, Hard Times Have Just Begun

TERRY PRISTIN

September 1, 2009

As the commercial real estate market heated up earlier in the decade and lenders competed feverishly to issue ever-riskier mortgages, hundreds of bankers, investors, lawyers, brokers, appraisers, accountants and analysts flocked to an investors’ conference in Florida each January to celebrate their good fortune with lavish beach parties featuring bikini-clad models and popular entertainers.

But in what a Prudential Real Estate Investors report described as “a move of near-perfect symbolism,” the conference sponsor, the Commercial Mortgage Securities Association, recently announced that next year’s event would be relocated from South Beach to Washington, where the industry has been lobbying strenuously for federal assistance.

These days, the people who buy and sell office buildings, shopping centers, warehouses, apartment buildings and hotels are hardly in a festive mood, despite some recent encouraging signs relating to the job and housing markets and a recent increase in sales of small office buildings.

Even though industry lobbyists were able to persuade Congress to extend a loan program aimed at prodding the stalled securitization market back to life, several analysts said it was unlikely to head off a spate of defaults, foreclosures and bankruptcies that could surpass the devastating real estate crash of the early 1990s. “It will prop up a few deals, but you can’t stop the wave that’s coming,” said Peter Hauspurg, the chief executive of Eastern Consolidated, a New York brokerage firm.

The distress is still in its early stages, analysts said. “We are between the first and second inning,” said Richard Parkus, who directs research on commercial mortgage-backed securities for Deutsche Bank. “We’re going to have to get through a very difficult period.”

Mr. Parkus said that vacancy increases and rent declines already mirrored what happened in the 1990s, and until new jobs were created, generating an increase in demand for commercial space and more retail spending, this was not likely to be reversed.

Building values have declined by as much as 50 percent around the country, and even more in Manhattan, where prices soared the highest. As many as 65 percent of commercial mortgages maturing over the next few years are unlikely to qualify for refinancing because of the drop in values and new stricter underwriting standards, he said.

Fitch Ratings recently reported that $36.1 billion in securitized loans — mortgages pooled, sliced into different categories of risk and sold to investors — have been transferred so far this year to a “special servicer,” an agency that handles troubled loans. Such a transfer is prompted by a bankruptcy, a 60-day delinquency or the prospect of an imminent default. In all, some 3,100 loans representing $49.1 billion, or 6.1 percent of the total, are currently in special servicing, an amount that could grow to nearly $100 billion by the end of the year, Fitch said.

But the damage is expected to be even greater for banks, which are holding $1.3 trillion in commercial mortgages (including apartment buildings) and $535.8 billion in construction and development loans, said Sam Chandan, the president of Real Estate Economics, a New York research company. About $393 billion worth of mortgages are scheduled to mature by the end of next year alone, and an estimated $39 billion more were due to expire this year but have been extended, he said.

By midyear, Real Capital Analytics, a New York research company, had identified $124 billion worth of distressed property. Less than 10 percent of the distress had been resolved through loan modifications or sales.

The downturn in commercial real estate is already having repercussions for local governments. New York City’s general fund, to cite an example, collected $2.1 billion from transfer and mortgage recording taxes at the peak of the market in the 2007 fiscal year, according to Frank Braconi, chief economist for the comptroller’s office. This fiscal year, it is expected to receive only $767 million, he said.

In New York, with its concentration of tall office towers, commercial mortgage-backed securities play a bigger role than they do elsewhere. The brokerage firm CB Richard Ellis estimates that about half the transactions in recent years involved securitized financing.

The mechanism set up to manage problems with the underlying mortgages is being put to the test for the first time. Some longtime real estate investors who profited from the ready access to mortgages made possible by securitization now complain that the system is impersonal and rigid. Instead of negotiating directly with a lender sitting across a table, Norman Sturner, a partner at Murray Hill Properties, a New York real estate company, said he had been forced to deal by telephone with “a third party sitting out in the Midwest” who seemed indifferent to his problems.

Since the master servicer, which handles the routine servicing of the loan, has no authority to restructure it, the landlord has no way to tackle anticipated problems before it comes into the hands of a special servicer and is already in trouble. “What’s going to happen when billions of dollars can’t be repaid?” said Mr. Sturner, who owns and operates five million square feet of office and apartment buildings.

Mr. Sturner, a 39-year industry veteran who bought aggressively during the real estate boom, would not comment on any specific loans. But a Manhattan real estate executive, who declined to be identified commenting on another’s business dealings, said that Mr. Sturner recently stopped paying his mortgage on One Park Avenue, a 20-story Art Deco building between 32nd and 33rd Streets, which he bought for $550 million in 2007, so that he could have the loan transferred to a special servicer.

Last year, one tenant, the Segal Company, a company specializing in employee benefits, said it would move at the end of this year to West 34th Street, leaving three floors at One Park Avenue vacant when new tenants are hard to come by and rents have fallen significantly. Fitch downgraded the securities backed by this loan in August.

The rising incidence of delinquencies and defaults has cast a spotlight on the special servicers, who are chosen by the investors who hold the riskiest bonds, and, in most cases, are part of the same firm. Six companies control 85 percent of the business, according to Fitch.

One source of conflict is that pension funds, endowments and other institutional investors with the most protected securities are often eager to liquidate their positions as quickly as possible, and those with the riskier portions resist taking an immediate loss.

Patrick C. Sargent, the president of the Commercial Mortgage Securities Association, said that despite an apparent conflict of interest, the servicers are accountable to all classes of bondholders and are required to maximize the proceeds for the investment as a whole. Falling short can lead to a lawsuit or a ratings downgrade. “They are in a fishbowl,” he said. “They are going to be watched.”

Critics say the special servicers are overwhelmed by the current workload. “The people we are dealing with are swamped beyond any measure,” said Paul M. Fried, a managing director of Traxi, a New York consulting company, who is advising borrowers with securitized loans.

But one executive at a special servicer whose employer would not allow his or his company’s name to be used said that his firm had tripled its staff in the last two years, and that other companies were also hiring asset managers.

Despite the criticism, Stephanie Petosa, a managing director at Fitch, which rates special servicers, said they were equipped to handle the workload. “I think they are moving at a reasonable pace, given the current environment,” she said.

http://www.nytimes.com/2009/09/02/business/economy/02office.html?_r=1&partner=rss&emc=rss

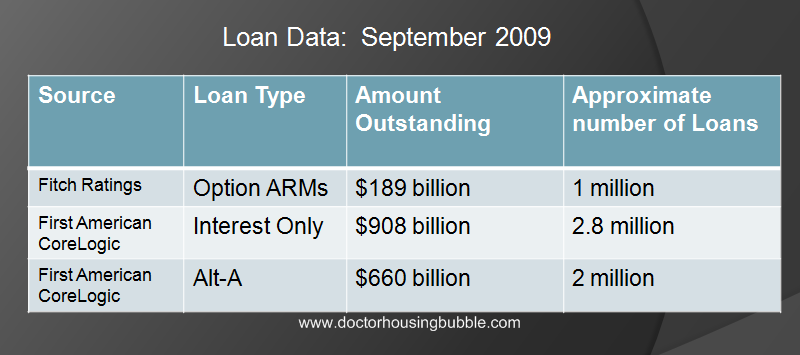

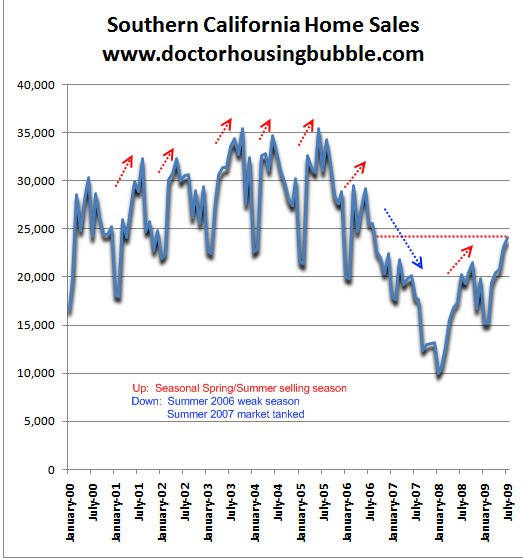

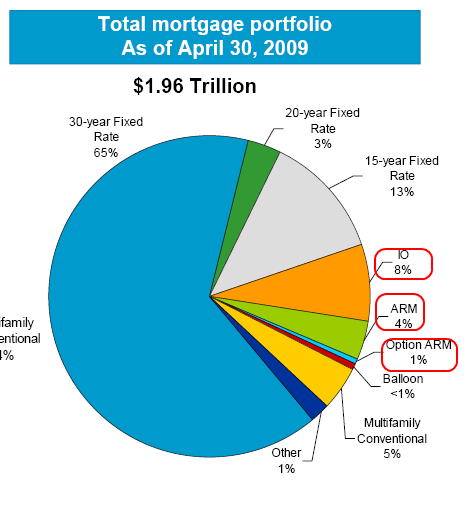

$1.1 Trillion in Toxic Loans: $908 Billion in Interest Only and $198 Billion in Option ARMs. The Zombie Loans that Simply Don’t Die.

Dr.HousingBubble.com

Sept 10, 2009

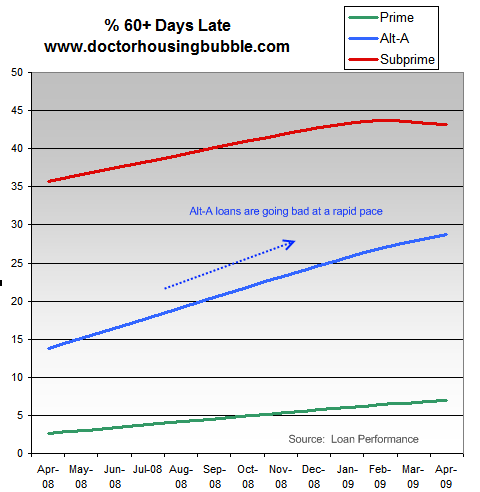

Two years of a deep and prolonged recession and we still can’t seem to get a hold of the toxic assets plaguing the books of banks. Much of this comes from the scamming and blood sucking from banks on the taxpayer. How can $13 trillion in backstops and commitments not resolve the problem? First, the banking system operates as a crony operation looking to serve its own interest even if it comes at the detriment of the entire economy. News coming out this week simply reaffirms what we have been saying for the entire year. The Alt-A and option ARM wave is imploding right on schedule.

When I wrote about the Alt-A loans back in May of this year, we put a ballpark figure of $1 trillion for toxic mortgages. So after all the gimmicks and money being thrown at the system it turns out that we still have over $1 trillion in junk mortgages. A recent analysis by First American CoreLogic put the amount of Interest Only mortgages at $908 billion with 2.8 million loans active. Fitch Ratings came out this week showing that there are still $189 billion in option ARMs in the system. For all you folks who thought that all the option ARMs were modified, the data shows only 3.5 percent of the nearly 1 million loans have been modified. And those that have been modified still re-default at incredibly high rates.

So let us put this into perspective with current data:

Now a couple of things to mention. There is overlap between a few categories. For example, a large number of the option ARMs fall under the Alt-A category. Many Interest Only loans are also Alt-A loans. A better estimate is the specific category of Option ARMs and Interest Only and that is a combined total of $1.097 trillion. This is the number of loans out in the system currently. Plus, there are still many active subprime loans. These loans are part of the zombie bank balance sheet.

Yet the reason these loans will be so problematic is how borrowers are viewing the future:

“(NY Time) With many of these homes under water — worth less than the loans against them — many interest-only mortgages will soon become unaffordable, as the homeowners have to actually start paying principal. Monthly payments can jump by as much as 75 percent.

The Mollers owe so much more than their house is worth, and have so few options, that they are already anticipating doom.

“I’m praying for another boom,” said Mr. Moller, 34. “Otherwise, we’ll have to walk.”

Keith Gumbinger, an analyst with HSH Associates, said: “This is going to be the source of tomorrow’s troubles. The borrowers might have thought these were safe loans, but it turns out they bet the house.”

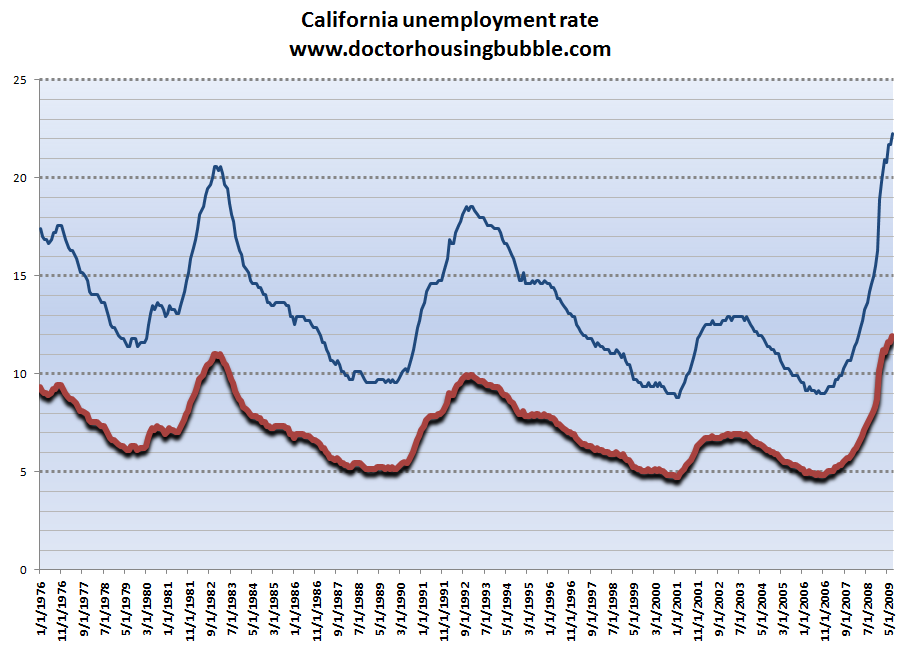

Praying for another epic housing bubble is highly unlikely. The Mollers by the way bought in over priced and over hyped San Diego. San Diego, just like Los Angeles and Orange counties has a legion of people that are praying for another boom to come along. Forget about jobs or income, they conveniently ignore the 11.9 percent unemployment rate and the reality that the state has had to budget some $60 billion in budget cuts. If we use a better measure of unemployment and underemployment, the state has a rate above 22 percent:

What does this data tells us? First, these loans are doomed to fail. It isn’t a question of whether they will fail but how bad will they fail. The issue of shadow inventory is important because many of these banks are simply not moving on homes and ignoring the foreclosure process completely. Not true? Well look at some examples across the country:

“(Cleveland) Renetta Atterberry thought she had lost her East 102nd Street house. So she was shocked to learn in January — five years after her mortgage company filed for foreclosure — that it was still in her name.

Worse, the long-vacant rental home had been vandalized and she faced a raft of housing code violations. Since then, she has been saddled with debts of about $12,000 to pay for demolition and back taxes.

“I thought I had nothing else to do with that home,” said Atterberry. “I was so embarrassed and humiliated by this.”

Her mortgage company didn’t buy the house and never took it to sheriff’s sale to see if somebody else would, leaving Atterberry the legal owner, responsible for upkeep and taxes.

These so-called “bank walkaways” are another troubling development in the foreclosure crisis, particularly in cities like Cleveland with weaker housing markets, say housing advocates and government officials.”

In many other areas, banks are simply walking away from homes. In fact, it is a cold and calculating move. If they take possession of a property, they are responsible for taxes and maintaining the property according to city ordinances. Instead, they do nothing. In their calculus, they figure legal fees and handling the foreclosure process correctly outweigh doing absolutely nothing. You would think with trillions in bailouts banks would have a structured system in place after two long years into the crisis but they are as incompetent as they ever were. That is why it is maddening to entrust the people that created this mess to get us out of it. We need a new group and a new way of thinking. A first easy step is to eliminate the CEOs of every single top bank in the country. Also, we should claw-back any bonuses and compensation from these scammers.

If you think it couldn’t get any more ridiculous, the U.S. Treasury on their FAQ actually tells you how you can contribute to help pay down the national debt! Bwahahahaha! You must have cajones the size of watermelons to ask for something like that.

But back to the toxic loans, the clock has now stopped ticking:

“The interest-only periods, which put off the principal payments for five, seven or 10 years, are now beginning to expire. In the next 12 months, $71 billion of interest-only loans will reset. The year after, another $100 billion will reset. After mid-2011, another $400 billion will reset.”

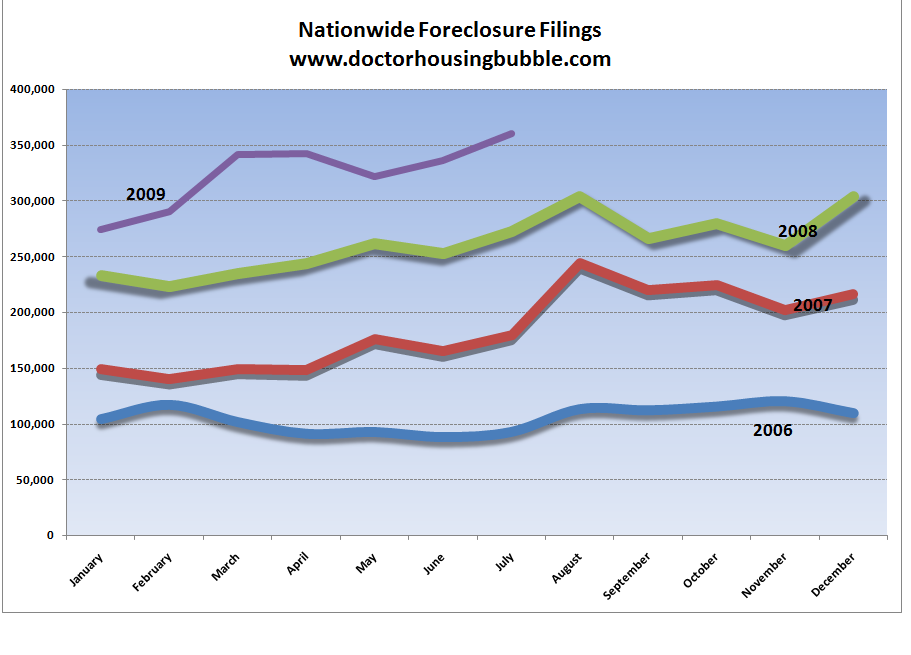

So much for these loans being resolved. You might be asking, what have banks been doing with all this money? Well first, they haven’t done much to stop nationwide foreclosures:

So not much is being done there. Maybe they’re lending more money. Nope:

“(MarketWatch)- U.S. consumers reduced their credit burden by a record amount in July, the Federal Reserve reported Tuesday. Total seasonally adjusted consumer debt fell $21.55 billion, or at a 10.4% annual rate, in July to $2.47 trillion. This is the sixth straight monthly drop in consumer credit. Consumers have retrenched since the financial crisis hit the economy in full force last September. Credit has fallen in every month since then except January.”

This really leaves you scratching your head. If they aren’t helping on the foreclosure front and aren’t lending, then what are they doing? How about paying out massive profits to their cronies:

“(Bloomberg) — Goldman Sachs Group Inc. posted record earnings as revenue from trading and stock underwriting reached all-time highs less than a year after the firm took $10 billion in U.S. rescue funds.

Second-quarter net income was $3.44 billion, or $4.93 a share, the New York-based bank said today in a statement. That surpassed the $3.65 per-share average estimate of 22 analysts surveyed by Bloomberg and was 65 percent higher than last year’s second quarter.”

So that’s where the money is going. The pretense that the money was to help the average American consumer was a gigantic stinking load so they could continue paying one another massive amounts of money. Incredibly for bringing the country near the brink of another Great Depression they are rewarded. We still haven’t seen a comparable Pecora Investigation. We have a committee looking into the causes as if we need to understand anymore! The banking system is corrupt to the core! It produced a minion of greedy short sighted thinkers that paper pushed this country into believing flipping homes to one another and sticking on granite countertops to every home was the ultimate sign of success. A massive and epic fraud. This is something we already know. Yet here we are allowing these same players to continue to game the system while 26.3 million Americans are unemployed or underemployed seeing the middle class evaporate like a drop of water in the Mojave Desert.

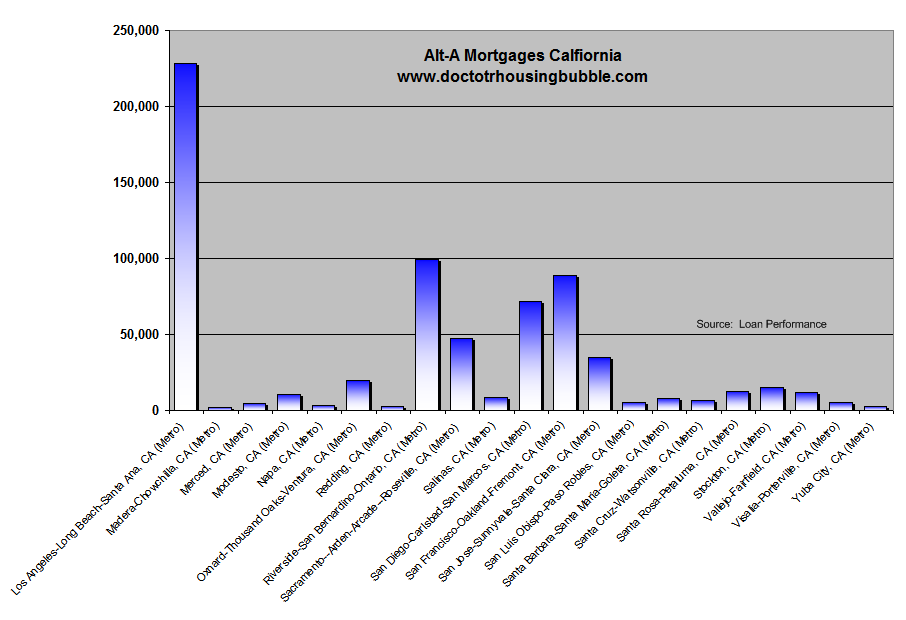

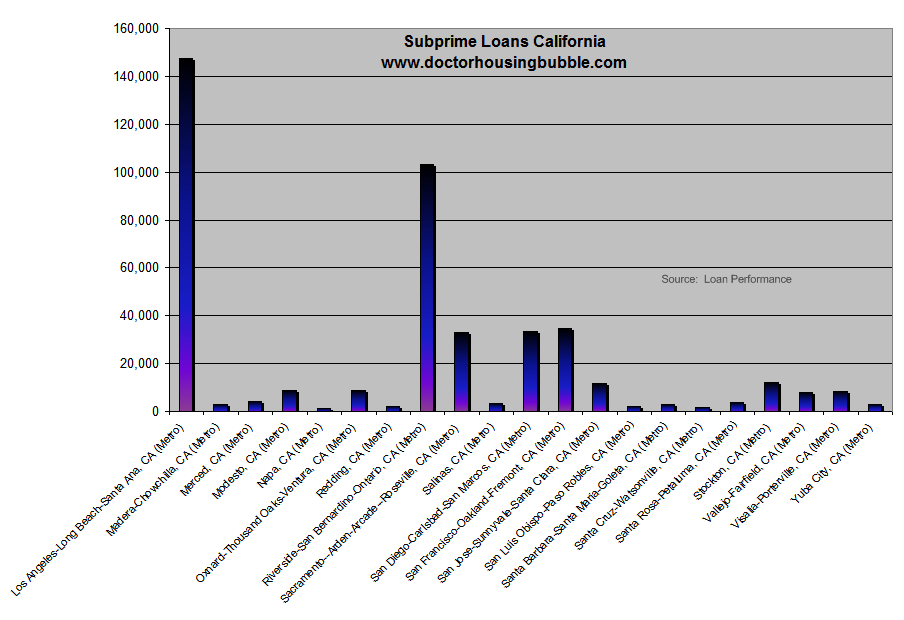

Leave it to California to have these same players proclaim that the bottom is here. Where do you think most of the $1.1 trillion in loans sit? California, Florida, Nevada, and Arizona own 75 percent of the option ARMs. Alt-As? California holds 42 percent of all loans categorized as Alt-As. Yet here people are thinking it won’t impact them in Pasadena, Culver City, or other semi-prime areas.

And guess what? There is this naïve notion that somehow these areas are populated by rich households able to withstand any economic hardship. Right on time to eliminate that wrong perspective:

“(Bloomberg) Wealthy Families Face Bankruptcy on Real Estate Crash

Wealthy individuals’ Chapter 11 bankruptcy filings jumped 73 percent in the second quarter from a year earlier, according to the National Bankruptcy Research Center, a research firm in Burlingame, California.

More individuals or families with at least $1,010,650 in secured debt and $336,900 unsecured are using Chapter 11 of the U.S. bankruptcy code typically associated with business reorganizations. Falling U.S. home prices leave them unable to refinance or sell properties when they drop below the value of the mortgage, said Joseph Baldi, a Chicago bankruptcy attorney.

Chapter 11 is more expensive and time-consuming for debtors and creditors than a Chapter 7 liquidation of assets. Wealthier people filing for bankruptcy typically have large homes, two car payments and children in private schools, said Leslie Linfield, executive director of the Institute for Financial Literacy in Portland, Maine, a credit-counseling and research group.

“You’re living on the edge, you’re juggling those financial balls,” Linfield said. “When one ball goes, they all fall down.”

People forget that a vast majority of people live on the financial edge. If you live in keeping up with the Joneses areas like Orange County, if you make $150,000 many times you are spending $175,000. Make $300,000? Some spend up to $400,000. That is the issue. Americans from poor to rich spend more than they make. This is now fundamentally changing by force. People forget that a million dollar mortgage carries enormous costs. In some areas like Irvine you saw million dollar homes going to people that made $200,000! Maybe this is out of the realm of most people. Take a look at this sample option ARM case:

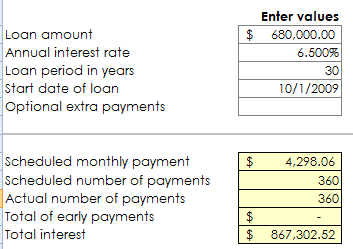

“(NY Times) Mr. Clavon, 63, was planning to sell the home in a few years and retire to Palm Springs. So he got a loan called an option adjustable rate mortgage, or option ARM, which allowed him to pay less than the interest for the first five years.

On his annual salary of $100,000 as a television camera operator, he could afford the $2,200 initial mortgage payments. And he planned to sell the home before the mortgage reset.

Because Mr. Clavon made only minimum payments on his mortgage, his balance has risen to $680,000 from $618,000, on a house worth closer to $400,000.”

Mr. Clavon is in good company. As it turns out 94 percent of option ARM borrowers made the minimum payment.

His payment is scheduled to go over $4,000 in two years. In fact, it might go much higher since he has paid zero to his principal. Let assume he refinances his mortgage to a 30 year fixed jumbo:

Given Mr. Clavon is 63, what bank is going to offer him a 30 year loan on a home that is underwater by $280,000? According to our numbers, he will pay off the home at 93 if he goes with a 30 year fixed mortgage. Why not go for the 40 year loan mods and be done at 103? The home is located in California (of course). Look at the above though, even with a refinance his principal and interest payment alone is $4,298. Add in insurance and taxes and his payment goes up to $5,000! That will virtually eat 100 percent of his net pay.

You might ask why banks have not dealt with these loans. Easy, that loan of Mr. Clavon is still on the bank balance sheet at face value. Do you think they want to lower it to $400,000 and eat the loss? They will go under. Shadow inventory is here and only those who are blind choose to ignore it.

This case isn’t unique. You can rummage through the multiple Real Homes of Genius examples and you will realize California is littered with these mortgages. People and banks praying for another boom so they can off load these homes to other suckers. Sounds like a fantastic strategy to me.

http://www.doctorhousingbubble.com/1-1-trillion-in-toxic-loans-908-billion-in-interest-only-and-198-billion-in-option-arms-the-zombie-loans-that-simply-dont-die/

Banks Load Up on Mortgages, in New Way

David Enrich

Sept 11, 2009

Banks have been silent partners in the meteoric rise of the Federal Housing Administration.

In the past year, the nation's financial institutions have snapped up securities backed by Ginnie Mae, a government-owned agency that guarantees payments on mortgages backed by the FHA. That helped drive demand for Ginnie securities and created an outlet for billions of dollars of FHA-backed loans made to borrowers who in many cases couldn't afford big down payments.

As of June 30, the roughly 8,500 federally insured banks and thrifts were holding $113.5 billion of Ginnie securities, compared with just $41 billion a year earlier, according to a Wall Street Journal analysis of bank financial disclosures. It is the largest amount that banks have reported holding since at least 1994.

Banks, sometimes with the blessing of federal regulators, have been loading up on Ginnie securities for one main reason: They make their balance sheets look healthier. Since the securities are guaranteed by the government, federal banking regulators have deemed them risk-free, meaning that adding them to a bank's investment portfolio, or replacing assets deemed riskier, lowers the overall risk of the portfolio in the eyes of regulators.

Some banks have used government cash infusions under the Troubled Asset Relief Program to buy Ginnie Mae bonds.

Having an eager buyer for its securities has made it easier for Ginnie Mae to increase the amount of debt it issues, though there appears to be no connection between the banks' increased appetite and the increasing supply of Ginnie Mae securities.

Because Ginnie Mae can issue significant amounts of securities, the FHA can back more loans and the high demand helps keep interest rates low. The irony is that banks that are reluctant to lend and are trying to unload their own mortgage holdings are at the same time helping to prop up the housing market by buying up securities backed by mortgages.

Through August, Ginnie had backed $298 billion of mortgage-backed securities in 2009, the most in its 41-year history and nearly double the amount in the same period last year. That represents about 20% of total new mortgages in the U.S. In addition to FHA-backed loans, Ginnie also guarantees securities comprising mortgages backed by the Department of Veterans Affairs and other federal agencies.

Ginnie and the FHA, units of the U.S. Department of Housing and Urban Development, have become two of the most powerful mortgage financiers in the U.S. When banks make home loans, the FHA insures them against default. Then the mortgages are pooled together and packaged into mortgage-backed securities. Ginnie guarantees that buyers of those securities -- including banks and other investors -- will continue to receive interest and principal payments on the debt, even if borrowers start to default.

FHA Paying the Price ?

Over the past year, FHA has played a key role in supporting the struggling housing market by buying up mortgages made to home buyers who can't afford big down payments or homeowners who want to refinance but have little equity in their homes. The FHA may be paying a price for all its lending. Rising losses on the mortgages have drained the agency's reserves.

Holding Ginnie bonds help banks look better because federal bank-capital guidelines give the Ginnie securities a "risk weighting" of 0%. That means banks don't have to hold any cash in reserve to protect against losses. By contrast, securities backed by Fannie Mae and Freddie Mac, the two mortgage giants seized by the government, carry a 20% risk weighting, meaning some cash needs to be set aside to hold them, even though most banks and investors think there is scant risk of Fannie or Freddie securities defaulting. Privately issued mortgage-backed securities can receive risk weightings of 50%, while many other types of debt carry 100%.

Because of the different risk weightings, bankers say they are selling relatively safe assets like Fannie securities and replacing them with Ginnie securities. The move doesn't shrink banks' balance sheets or remove their troubled assets. But it reduces their total assets on a risk-weighted basis. That is important because risk-weighted assets are the denominator in some key ratios of bank capital.

"With the pressure for capital, that's really made the Ginnie Maes more attractive," said John C. Clark, chief executive of First State Bank in Union City, Tenn. The bank's holdings of Ginnie securities jumped to $66 million at June 30 from less than $4 million a year earlier.

Like some peers, First State bankrolled those purchases partly with taxpayer dollars that were intended to stabilize the banking industry and jump-start lending. The 32-branch bank used a "significant portion" of the $20 million it received through TARP to buy Ginnie securities, Mr. Clark said.

Mr. Clark credits the strategy with helping First State preserve its capital ratios even as loan defaults swelled to $9.5 million on June 30 from $1.6 million a year earlier. During the same period, its total risk-based capital ratio climbed to 11.3% from 10.7%. That gave First State some breathing room above the 10% ratio regulators require for banks to be deemed "well capitalized."

This spring, executives from Warren Bancorp Inc., a small Michigan lender struggling with rising losses, sat down with examiners from the Federal Reserve to discuss the bank's dwindling capital. Bank officials pitched the idea of buying millions of dollars of Ginnie securities

"The examiners thought it was a good strategy for us to use," said Kim Keeling, the six-branch bank's chief financial officer. She called it "the quickest and the least costly option" for addressing the bank's depleted capital ratios.

Ms. Keeling acknowledged that the strategy doesn't ease the bank's underlying problems. "The whole capital ratio can be manipulated ... in many ways to make it appear better or worse," she said.

A Fed spokeswoman declined to comment.

Some bankers and other experts criticize the strategy's benefits as largely cosmetic, saying it is an example of how the federal rules governing bank capital are prone to manipulation. Buying Ginnie securities "helps alleviate some of the pressure but doesn't address the problem at large," said Ken Segal, senior vice president with Howe Barnes Hoefer & Arnett, a brokerage firm that advises small and midsize banks. "There's still the endemic problem" of bad loans.

Others say bank purchases of Ginnie securities are a prudent risk-reduction strategy. Bankers rightly perceive Ginnie securities as safer than almost any other investment, said Roger Lister, chief credit officer for financial institutions at bond-rating firm DBRS. "It may not just be for regulatory-capital arbitrage," he said.

Prosperity's Buying

In St. Augustine, Fla., Prosperity Bank increased its holdings of Ginnie securities tenfold over the past year. The lender, with 20 branches and $1.2 billion in assets, simultaneously dumped most of its Fannie and Freddie securities, even though they seemed safe.

"There's no more risk in Fannie and Freddie securities than in a Ginnie security," despite the different capital treatments, said CEO Eddie Creamer.

Mr. Creamer worries the capital rules could inadvertently make mortgages harder to come by. As banks dump Fannie and Freddie securities, their prices are likely to come under pressure. That inflates their yields, which translates into higher interest rates on the mortgages that they finance.

"It has a broader implication on the availability of those mortgages and the costs of those mortgages," Mr. Creamer said.

—Maurice Tamman contributed to this article.

Write to David Enrich at david.enrich@wsj.com

http://online.wsj.com/article/SB125253192129897239.html

Failing loans for commercial real estate threaten small banks

By Pallavi Gogoi, USA TODAY

Updated 12h 48m ago

Bank stocks have roared back from a near-death experience, which might be diverting attention from a new threat looming for the industry: commercial real estate.

The speed at which loans on commercial properties such as office buildings and malls are souring is "unprecedented," a recent report from Deutsche Bank said. The delinquency rates on these loans reached 4.1% in June, more than double the March rate. Banks are most vulnerable because they hold about $1 trillion of commercial real estate loans and an additional $530 billion in construction loans.

Job losses have led to rising office vacancies. Tight-fisted consumers have helped close retailers such as Circuit City, forcing mall landlords to default on loans. That is having a tiered effect on the banking industry:

•It is especially noxious for the smallest banks, which have very large portions of their loan portfolios exposed. That's the chief reason bank failures have hit 89 this year, vs. 25 for all of last year. For instance, one of the latest banks to fail, Affinity Bank, had 46% of its $805 million in loans to commercial properties. That compares with 33% for all banks, says Keefe Bruyette & Woods.

•Regional banks are also highly exposed and are a bigger worry for the economy because many are large. United Commercial of San Francisco is first on the "top potential concerns" list of Barclays Capital research. The bank, with assets of $12.7 billion, missed a regulatory deadline for filing its second-quarter report and is restating its 2008 financial statements. Tuesday, it named a new CEO. United Commercial wouldn't comment.

•The very largest banks, those with at least $1 trillion in assets, are less exposed. JPMorgan Chase has about 5.4% of such loans, and Citigroup has 3.4%, according to government filings. Among them, Wells Fargo has the largest exposure, with about 16.5%of its $821 billion loan portfolio made up of commercial mortgages or construction loans.

Meanwhile, bank stocks, as measured by the Financial Select Sector SPDR exchange traded fund, which suffered big losses previously, are up about 150% since the March low, more than double the broad market's gains. Yet the potential danger to the banking industry could grow, because the losses will likely get worse.

The National Association of Realtors projects that retail vacancy rates will increase from 11.7% in the second quarter of 2009 to 12.9% in the same period of 2010, the highest vacancy rates since 1991. And office building vacancy rates are expected to rise from 15.5% to 18.8%. "Who knows how long it will take to fill the building with employees again?" says Fred Cannon, chief equity strategist at Keefe Bruyette & Woods.

http://www.usatoday.com/money/industries/banking/2009-09-09-commercial-real-estate-loans_N.htm

Shadow Inventory Proof and Banks Delaying Losses for another Day. Banks Employing the Stick Your Head in the Sand Solution for the Financial Crisis

Dr.HousingBubble.com

Sept. 10, 2009

Apparently acknowledging shadow inventory is like holding onto childhood superstitions like believing in Santa Clause or the financial Easter Bunny. Over the last week, many of you have sent me articles where many authors both amateur and professional have started attacking shadow inventory and started proclaiming that it was a myth. Shadow inventory does not exist according to these new articles. Some of these authors went ahead and made up their own definitions of shadow inventory which in itself is curious since this inventory supposedly does not exist. The problem of course is that there are many definitions of what shadow inventory is so I will try to reiterate what I have been talking about for months.

Here is how I define this category of inventory:

“(Doctor Housing Bubble) What is shadow inventory? First, shadow inventory is housing units that are not making it onto the public market for one reason or another. There is speculation surrounding why this is happening. Lenders are overwhelmed and simply do not have the human capital to handle the glut so goes one theory. Others speculate that lenders are simply too incompetent to have a system in place to handle the mess they created.”

This is rather clear and many people when referring to shadow inventory are discussing it by this definition. Essentially shadow inventory encompasses housing inventory that isn’t viewable by the public or measured in more historical standards. Calculated Risk does an excellent job breaking down some of the categories:

“(Calculated Risk) There are several categories of shadow inventory:

REOs. There are bank owned properties that have not been put on the market yet. Several sources have told me the number is growing – no one knows why except possibly for accounting reasons (the banks might have to take an addition write down when they sell the property).

Foreclosures in process. The delinquency rate has continued to rise, and this will probably lead to many more foreclosures later this year. The number of foreclosures depends somewhat on the success of the modification programs. Last year many delinquent homeowners listed their homes as “short sales” – so those homes were not shadow inventory, however fewer delinquent homeowners are listing their homes now as they try to work with their lenders on a modification. Some percentage of these homes are shadow inventory.

New high rise condos. These properties are not included in the new home inventory report from the Census Bureau, and do not show up anywhere unless they are listed.

Homeowners waiting for a better market. This was the group mentioned in the Reuters story (the article also mentioned foreclosures). These are homeowners waiting for better market conditions to sell.

Inventory is usually the best metric to follow for the housing market – and according to recent releases inventory is declining for both new and existing homes – however shadow inventory clouds this picture.”

I would also add homeowners that have stopped paying but banks are simply not contacting them. In fact, according to Amherst Securities Group LP the foreclosure process now takes 18 months to 2 years, up from 15 months only a year ago. 2 years! I have had many e-mails from people telling me they have been in their homes without making a payment for 12 months. Amazing. Others have stopped making payments and the banks have yet to contact them. The bottom line, there is shadow inventory. These are homes that in every other time in history would have been on the market as additional inventory. I am open to debating the amount of shadow inventory but to say it is a myth is non-sense. In fact, to think there is no shadow inventory is to believe in banking data and give the crony capitalist the benefit of the doubt that they are handling things correctly.

In addition, the crux of the argument for those stating the non-existence of shadow inventory is narrow in focus. What they are arguing is basically one angle of the story. Their point is that banks are not hoarding REOs and there will be no flood of inventory in the next few months. On this point, they are correct. That however does not mean there is no shadow inventory or that somehow it is a myth.

to continue reading extensive article go here:

http://www.doctorhousingbubble.com/shadow-inventory-proof-and-banks-delaying-losses-for-another-day-banks-employing-the-stick-your-head-in-the-sand-solution-for-the-financial-crisis/

Housing sales come back, led by first-timers

Posted Aug 23rd 2009 11:10AM by Tom Johansmeyer

Filed under: Housing, Recession

It looks like the housing market is coming back, but there's still reason to be careful. In July, home resales had their highest monthly increase in at least a decade. The rush is driven in part by a tax credit that expires on November 30, 2009. The rate of sale grew 7.2%, ahead of expectations.

Last month, sales hit a seasonally adjusted annual rate of 5.24 million in July -- up from a 4.89 million in June. This is the fourth month in a row in which seasonally adjusted sales increased, and it was the strongest growth rate since August 2007. A Thomson Reuters survey had forecast 5 million, but the reality exceeded that.

Of course, the good news is clouded by fears that further job cuts, an increase in mortgage rates, and the expiration of the tax credit could lead to another drop in sales and home values, especially for all the recent first-time homebuyers who would see their initial forays into home ownership sink underwater. First-timers are picking up one of every three homes sold.

So, there's a sign that the economy is recovering, but there are still pressures from several fronts that could turn the trend. Again, the sentiment is: "proceed with caution."

Tags: home prices, home sale trends, home sales, home values, housing bubble, housing market, housing prices, housing sales, housing sector, inthenews, mortgage rates, mortgages

Bernanke: Economy On Verge Of Recovery

http://www.wwj.com/Bernanke--Economy-On-Verge-Of-Recovery/5056804

Federal Reserve Chairman Ben Bernanke declared Friday that the U.S. economy is on the verge of a long-awaited recovery after enduring a brutal recession and the worst financial crisis since the Great Depression.

Economic activity in both the U.S. and around the world appears to be "leveling out," and "the prospects for a return to growth in the near term appear good," Bernanke said in a speech at an annual Fed conference in Jackson Hole, Wyo.

Major stock indicators, which were up moderately before his comments, surged more than 1 percent. Bernanke's remarks energized investors after a choppy week of trading amid mixed signals on the economy.

The upbeat assessment was consistent with the Fed's observations earlier this month. The central bank has taken small steps toward pulling back some emergency programs to revive the economy.

Still, Bernanke stressed Friday that despite much progress in stabilizing financial markets and trying to bust through credit clogs, consumers and businesses are still having trouble getting loans. The situation is not back to normal, he said.

Restoring the free flow of credit is a critical component to a lasting recovery.

"Although we have avoided the worst, difficult challenges still lie ahead," Bernanke told the gathering. "We must work together to build on the gains already made to secure a sustained economic recovery."

Strains in financial markets worldwide persist. Financial institutions face "significant additional losses" on soured investments and many businesses and households are experiencing "considerable difficulty" in getting loans, he said.

Elsewhere at the conference, European Central Bank President Jean-Claude Trichet responded to a research paper on the origins and the nature of the financial crisis by saying he was a "little bit uneasy" about talk of a return to normalcy.

"We know that we have an enormous amount of work to do and we should be as active as possible," Trichet said.

The remarks by Bernanke, Trichet and others come two years after the financial crisis broke out and nearly one year after it had deepened to the point of sending the nation into a near meltdown.

The bulk of Bernanke's speech was a chronicle of the extraordinary events of the past year. Financial markets took a turn for the worst starting last September and into October, nearly shutting down the flow of credit. The crisis felled storied Wall Street firms and forced the government to take over mortgage giants Fannie Mae and Freddie Mac, as well as insurance titan American International Group Inc.

Despite efforts to save it, Lehman Brothers failed. It filed for bankruptcy on Sept. 15, the largest in corporate history, which roiled markets worldwide.

To prop up shaky banks, the government created a $700 billion bailout fund, a program that proved wildly unpopular with an American public suffering fallout from the recession.

The Fed swooped in with unprecedented emergency lending programs to fight the crisis. It eventually slashed a key bank lending rate to a record low near zero. And Congress enacted programs to stimulate the economy, the most recent coming in February with President Barack Obama's $787 billion package of tax cuts and increased government spending.