News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The grains look really good from here including rice and bean oil.

Elevated sugar prices mean that inflation and gold have not peaked yet - MarketGuage's Mish Schneider

By: Neils Christensen | March 1, 2023

After bouncing off a nine-week low at the start of the week, the gold market is seeing some new technical buying, pushing prices to resistance at around $1,850 an ounce. According to one market analyst, this could be the start of a bigger bullish move as the Federal Reserve is unlikely to bring inflation back down to its 2% target.

In an interview with Kitco News, Michele Schneider, director of trading education and research at MarketGauge, said that if investors want to know where gold is going, they should pay closer attention to sugar prices.

The little-watched commodity is currently trading around $0.205 per pound. Last month sugar pushed to a multi-year high above $0.21. At the same time, sugar prices are up more than 120% from their 2020 COVID-19 lows.

Unlike other agricultural commodities like wheat and corn, sugar has maintained most of its gains following the global pandemic market disruptions. Schneider said elevated sugar prices indicate that inflation is not going away.

"Sugar is in everything, which means it will keep food prices elevated globally, and there is not much the Federal Reserve will be able to do about that," she said.

Late last year, food shortages of sugar, vegetable oil, rice and even bottled water in Tunisia caused fights to break out among consumers waiting in food market queues. Schneider said that supply disruptions with reduced exports from India and Russian sanctions, as its invasion of Ukraine enters its second year, could lead to higher sugar prices through 2023.

"The sugar market appears to be this underlying indication that we haven't seen the peak in geopolitical problems. We haven't seen the peak in social disruption, and therefore we haven't seen the peak in inflation," she said. "This also means we haven't seen the peak in gold and silver."

While sugar has been the quiet indicator Schneider is watching, she said it is not the only commodity that points to higher inflation. She explained that supply constraints in most industrial metals, like copper, aluminum and tin, will continue to support higher prices and will ultimately filter down to consumers, keeping inflation elevated.

Schneider said that there are already signs that gold investors doubt that the Federal Reserve will be able to raise interest rates enough to cool down inflation.

After a strong start to the year, February was gold's worst month since mid-2021. The gold market saw a sharp decline last month as interest rate expectations started to shift, with investors looking for the Federal Reserve to maintain higher interest rates for longer than initially anticipated.

However, Schneider said that despite gold's selloff, it had held critical support. She added that she expected gold prices to hold their ground at $1,800 an ounce.

"No matter how unpopular gold has gotten, its price action tells me that investors are still worried about inflation and protecting themselves," she said.

Gold's new momentum comes as market chatter highlights growing prospects that the Federal Reserve could raise interest rates to 6%. At the same time, the yield on 10-year notes has briefly pushed to 4%. The two-year yield remains at a multi-year high of around 4.8%.

Schneider also noted that despite gold's selloff, it continues to outperform the S&P 500. She said that as soon as it becomes clear that the Federal Reserve cannot cool inflation, gold will take off to new highs.

"It's going to take just one little catalyst to ignite a bigger rally in gold," she said. "Whether that is inflation as sugar prices rally or some geopolitical event, it won't take much for conditions to spiral out of control."

Although investors go back and forth over a potential recession, Schneider said that the bigger threat to the economy remains stagflation, a period of lower growth and high inflation.

"It's not about the doom and gloom. My job is not necessarily to predict but to forewarn and prepare people," she said.

Read Full Story »»»

DiscoverGold

DiscoverGold

Today's Futures Heat Map • Weakest: Lumber, Orange Juice, Coffee, Milk

By: Barchart | March 1, 2023

• Today's Futures Heat Map

Strongest: Sugar, Heating Oil, Cocoa, Copper

Weakest: Lumber, Orange Juice, Coffee, Milk

Read Full Story »»»

DiscoverGold

Look Out Below Funds Big Sellers. The Corn & Ethanol Report

By: Daniel Flynn | March 1, 2023

We kickoff the day with MBA 30-Year Mortgage Rate, MBA Mortgage Market Index, MBA Mortgage Refinance Index, MBA Purchase Index and MBA Mortgage Applications at 6:00 A.M., S&P Global Manufacturing PMI Final at 8:45 A.M., ISM Manufacturing PMI, ISM Manufacturing Employment , ISM Manufacturing New Orders, ISM Manufacturing Prices and Construction Spending MoM at 9:00 A.M.,

EIA Energy Stocks 9:30 A.M., 17-Week Bill Auction at 10:30 A.M., Cotton System, Dairy Products Sales and Fats & Oils at 2:00 P.M.

On the Corn Front massive fund selling kept the bulls at bay with a 13 ¼ cents break in yesterday’s action. The market is waiting for a dead cat bounce as the grain complex has been pummeled over the last week. Even the market will look to who can supply the global demand and exports could push US exports. At the moment US exports are dismal compared to the five-year average even discounting the surge of the export market with China. Things will change when price for feed and human consumption will dominate with tight global supplies. In the overnight electronic session the May corn is currently trading at 630 ½ which is a ¼ of a cent higher. The trading range has been 635 to 630 ¼.

On the Ethanol Front the EIA reports ethanol volumes continue to recover from the pandemic blues. The Biden administration is expected to approve a rule that would expand sales of gasoline with higher blends in certain US MIDWEST states. The rule making is not to take effect until the summer of 2024 sources said. Too little too late. The CBOT ethanol futures continue to show zero trades and open interest. Any doubt in traders mind. The pattern continues.

Read Full Story »»»

DiscoverGold

Brewing. The Energy Report

By: Phil Flynn | March 1, 2023

A global oil supply squeeze is brewing as China’s economy looks like it’s getting ready to soar. Overnight data showed the Chinese manufacturing sector saw its biggest surge in a decade and will soon erase any perception of short-term oversupply. China’s official manufacturing PMI hit 52.6 in February, and in their outlook, they are predicting even more growth in the coming months. The news initially caused oil to rally but now is pulling back as traders fear what the Energy Information Administration may say about crude supply and are even more fearful of the reaction by the Fed if China starts increasing commodity prices.

The oil supply picture short term is muddled after the American Petroleum Institute (API) showed another stunning 6.203 million barrel increase in crude supply as refinery maintenance is reducing US demand by millions of barrels a day. Yet they had better not stay in maintenance much longer as the US is exporting a record amount of petroleum products to the world as the US product supply is well below normal. The API reported drops in oil products with gasoline down 1.774 million barrels and distillate inventories down 341,00 barrels.

In fact yesterday, the Energy Information Administration (EIA) said in their monthly report that the supply of crude and petroleum products in the United States fell in December to 19.49 million bpd, the lowest since March 2021. The US refineries will have to get to work and that should add 2 to 4 million barrels a day of demand in the coming weeks and months.

On top of that, if China’s manufacturing sector does not falter it will intensify the global shortfall of distillate inventories. That will add to diesel prices and inflation and does not even raise the issue of gasoline additive shortages that are looming because of the Russia-Ukraine war.

It is also unlikely that OPEC will be able to feed this demand as Russia starts its production cut as Nigeria helped OPEC raise output even as the cartel is still below its output targets. Reuters reported that an OPEC poll showed that OPEC production was up 150,000 barrels a day but is still underproducing by 880,000 barrels a day.

The EIA also had a big downward adjustment in their previously reported oil production number. The EIA reported that US December crude production was at 12.101 mbpd vs 12.377 mbpd (revised from 12.375 mbpd) in November. That number is a concern as the Biden administration’s anti-oil policies and rising production costs are causing a pullback in US oil drillers. Rig counts are falling and costs are rising. Thank goodness at least the US is finally allowing Gulf of Mexico lease sales that were privately held up by the anti-oil Biden administration.

The U.S. Bureau of Ocean Energy Management (BOEM) will hold an oil and gas lease sale in the Gulf of Mexico in March 2023 it announced Friday. The lease sale is one of three offshore lease sales initially canceled by the Biden administration in May 2022. The Gulf of Mexico Oil and Gas Lease Sale 259 will offer approximately 13,600 blocks on 73.3 million acres in the Western, Central, and Eastern Planning Areas on the U.S. Outer Continental Shelf. The opening and reading of the bids will begin at 9 a.m. Central Daylight Time on March 29, 2023.

Of course, once you buy the lease you have to worry whether the Biden Administration will block your permission because they are the pettiest and most vindictive administration in the history of the country against oil and gas. Not only do they falsely accuse the industry of price gouging and manipulation, but their policies have also led to higher prices and more global price instability. The long-term damage from these policies will sadly be felt for years.

For oil, we must get through the EIA report. The market is sensing another crude build based on the API. Yet the focus should start to change soon as refineries will not stay down forever. You have to try to ignore the fact that the global product situation is dangerously below average even with one of the warmest winters on record in the US and Europe as far as heating degree days are concerned. Yet with China roaring back, you had better hope for a deep recession to avoid a major supply squeeze this summer.

Natural gas is trying to come back from one of its deep price dives. Freeport LNG’s progress as well as some concerns about some production cutbacks is fueling the rebound. The EIA reported that in December 2022, dry natural gas production increased year over year for the month for the 21st consecutive month. The preliminary level for dry natural gas production in December 2022 was 3,068 billion cubic feet (Bcf), or 99.0 billion cubic feet per day (Bcf/d). This level was 1.0% (1.0 Bcf/d) higher than December 2021 (98.0 Bcf/d) and the highest level for the month since 1973, when we began tracking dry natural gas production. Gross withdrawals also increased from December 2021: Gross withdrawals: 3,717 Bcf for the month, or a daily rate of 119.9 Bcf/d and A 1.0% increase compared with December 2021 (118.7 Bcf/d) The highest daily rate of gross withdrawals for the month since 1980, the earliest year in this data set. So a record.

Estimated natural gas consumption in December 2022 was 3,385 Bcf, or 109.2 Bcf/d. This level was 12.6% higher than in December 2021 (97.0 Bcf/d) and the highest for the month since we began using the current methodology for natural gas consumption in 2001. So a record.

Read Full Story »»»

DiscoverGold

Today's Futures Heat Map • Weakest: Natural Gas, Soybean Meal, Corn, Soybean

By: Barchart | February 28, 2023

• Today's Futures Heat Map

Strongest: Gasoline, Orange Juice, Lumber, Copper

Weakest: Natural Gas, Soybean Meal, Corn, Soybean

Read Full Story »»»

DiscoverGold

Agriculture Master Report

By: Bill Moore | February 28, 2023

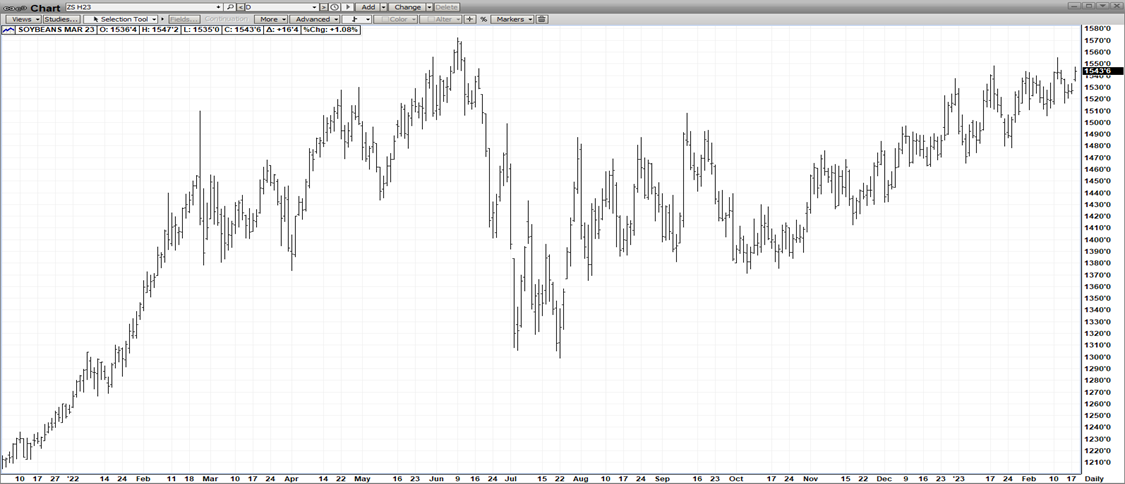

MAR BEANS

Given the recent carnage in Mar Corn (down .50) & Mar Wht (down 1.00) since mid-Feb & considering the record bean Brazilian Bean crop, Mar Beans have held up remarkably well – holding just 40 cents off their recent highs! Helping to support was the USDA OUTLOOK FORUM last week that estimated bean acreage would remain unchanged from 2022 at 87.5 MA & The Buenos Aires Grain Exchange lowered their Arg bean production to 33.5 MMT (INITIAL-48) – the lowest in 14 years! Also, the Macro Mkts scored a big down last week with THE DJI registering its biggest weekly loss of 2023! Normally a huge negative for Beans! The mere fact that Beans are holding at over $15.00 -right now -is quite impressive!

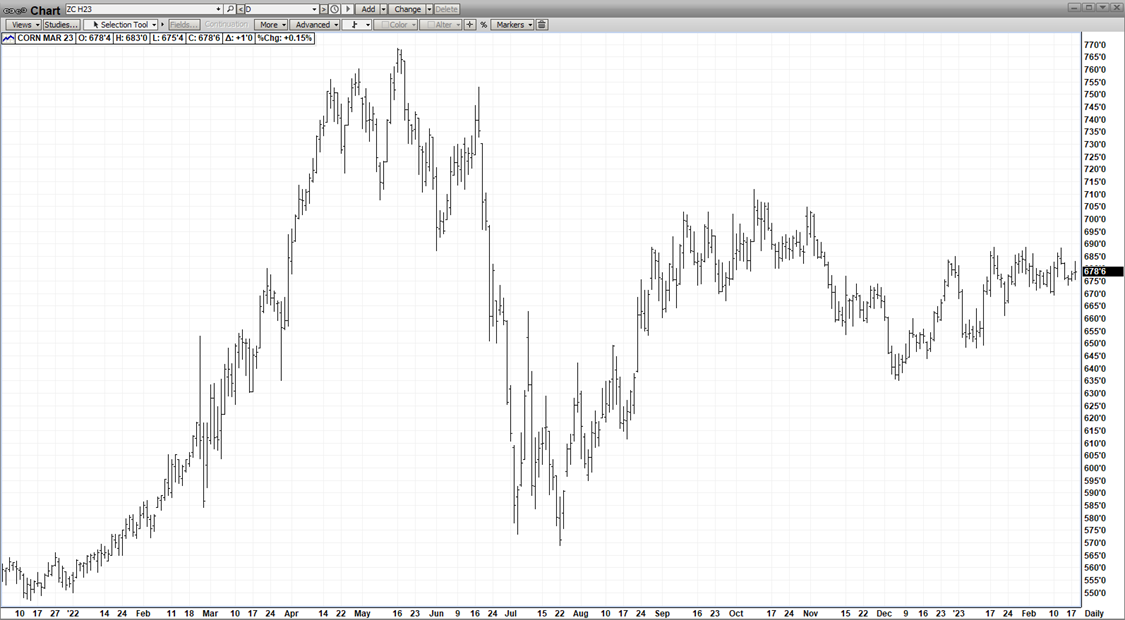

MAR CORN

Mar Corn was bludgeoned with a perfect storm of mkt events – which induced massive fund selling – resulting in a nearly 30 cent weekly drop! First was more-than-expected week-end rains in Argentina – Second, bearish #’s from the USDA AG OUTLOOK FORM including increased acres – 91.0 MA (88.6), stocks – 1887 (1267) & production – 15.08 (13.73). Finally, the Macros turned sour with the DJI down 1000 points for the week & the US Dollar up 120 points! Exports were expected to increase – even incrementally in 2023 – but that has been slow to happen so far! Still, the Corn Futures are hovering in the mid-6’s in early Feb – mostly off historically low carry-out! Should there be any additional hiccup in production from either hemisphere in 2023, May & July Corn could easily tack on .50 to .75 – especially if exports ramp up in Mar-June!

MAR WHT

In 2 week’s time, Mar Wht has experienced a free-fall – plummeting over $1.00 (8.00-694) for a plethora of reasons! The main catalyst has been Russia as they have inundated the global mkt with cheap exports from their record crop – as they attempt to finance their war efforts! Then, last week, the USDA OUTLOOK FORUM issued some higher #’s for this year’s crop – acres – 49.5 MA (ly-45.7), production -1887 MB (ly-1650) & ending stocks – 608 MB (ly-568). Also, a winter storm has helped replenish some subsoil moisture for the drought-ravaged Western Plains – finally, the Russia-Ukraine Grain Corridor Deal is expected to be renewed by Mid-March! The mkt is severely oversold now & due for an upside correction!

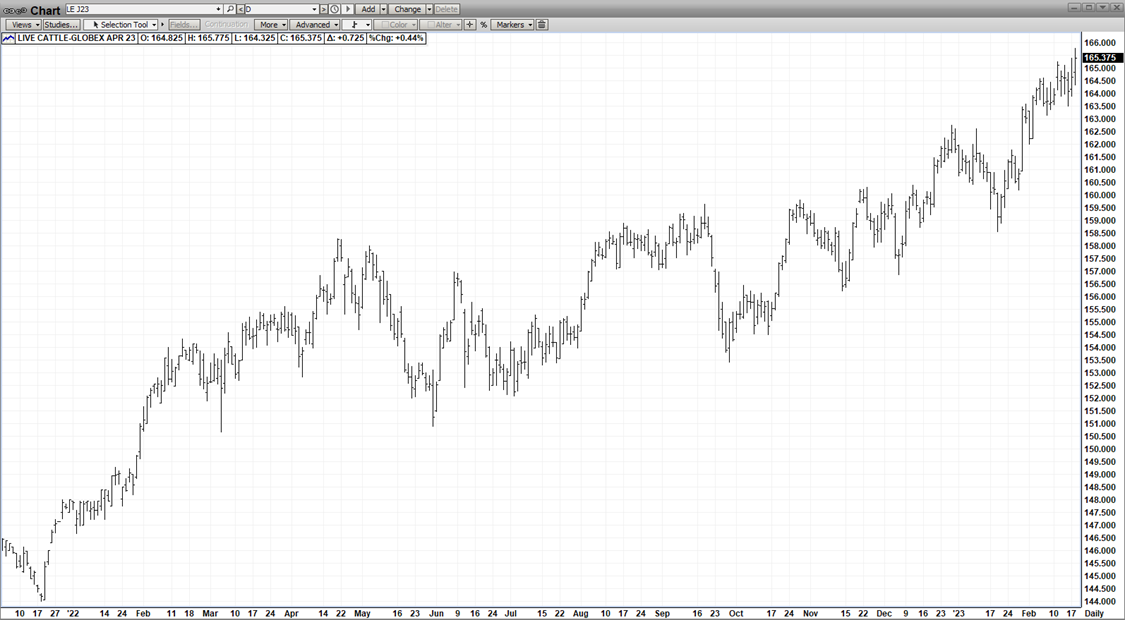

JUNE CAT

After 4 consecutive contract highs, June Cattle registered a key reversal (new highs & an outside day down) – a “tempting sell” but NOT SO FAST! Despite its really historically high level, the supply/demand fundamentals suggest a correction – not a top! The production decrease from the 4th Qtr to the 1st Qtr was the 2nd largest ever – & demand seems to be good enough to support further up! Last Friday’s bevy of livestock reports were positive – with the Cold Storage reflecting less than last month & the Cattle-On-Feed reflecting both placements & total on-feed at 96% of 2022! Currently, the only “fly-in-the-ointment” is a looming recession – which could sharply undercut beef demand!

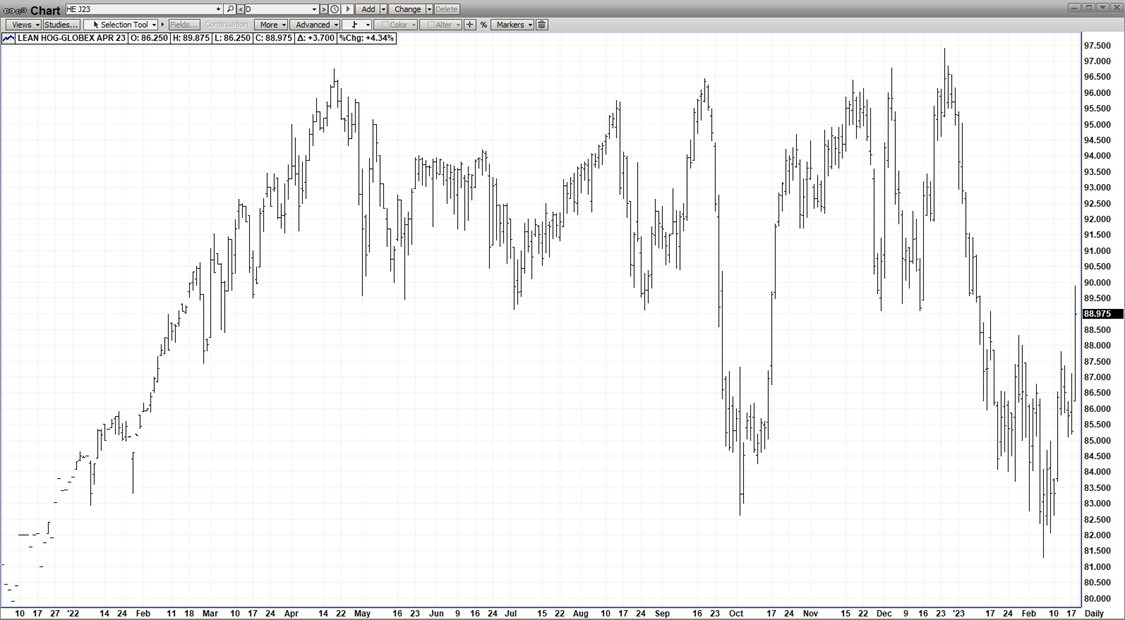

APL HOGS

Burdensome supplies continue to plague the hog complex – highlighted by the 60% jump in Pork Belly Supplies from last year 70,134 (ly-44,707) – as reflected in last Fridays monthly Cold Storage Report! The down is especially egregious when juxtaposed against a cattle mkt which makes new contract highs every 3rd day! We feel the consumer may have partially turned the tide – opting for cheap pork chops versus expensive steaks – as the futures haven’t made any new lows in 2-3 weeks. But rallying from here is another story as the massive pork supplies will probably keep the mkt just consolidating at current levels!

Read Full Story »»»

DiscoverGold

First Notice Day March Grains. The Corn & Ethanol Report

By: Daniel Flynn | February 28, 2023

We kickoff the day with Goods Trade Balance Adv, Retail Inventories Ex Autos MoM Adv and Wholesale Inventories MoM Adv at 7:30 A.M., Redbook YoY at 7:55 A.M., S&P/Case-Shiller Home Price MoM & YoY, House Price Index MoM & YoY and House Price Index at 8:00 A.M., Chicago PMI at 8;45 A.M., CB Consumer Confidence, Richmond Fed Manufacturing Index, Richmond Fed Manufacturing Shipments Index and Richmond Fed Services Index at 9:00 A.M., Dallas Fed Services Index and Dallas Fed Services Revenues Index at 9:30 A.M., and API Energy Stocks at 3:30 P.M.

On the Corn Front today we have or are rolling into May or July contracts with July being more of a market traders look to trade longer term positions. The market took on some more pressure in yesterday’s action with the spot slipping to its lowest level in 3 months. Drought conditions remain across Argentina, weather in Brazil remains favorable with spotty rains across the north central growing regions will accelerate soybean harvest and 2nd corn seedings in Mato Grosso.

Rhonda Brooks with AGWEB reports Ken Ferrie and his agronomic team conduct yield map meetings with Illinois customers this winter, They are seeing some excellent nutrient use efficiencies from the 2022 season, especially with nitrogen (N). In many cases, corn yield results were higher than farmers set goals and expectations. “At side-dressing time, our growers were raising their yield goals because of strong corn stands, which was a result of corn coming out of the ground in four-and-a-half to five days,” recalls Ferrie, Farm Field Journal Agronomist. “In most cases, pushing yield goals was the right move,” he adds. “Some growers who started with 220-bu. yield goals for instance bumped it to 240, and we adjusted the N rate accordingly.” With grain markets continuing to slide (5 sessions in a row) we may get a bounce with some short-covering but the market is trying to find support, two wildcards come into play long-term with global corn feed demand, ethanol demand and demand for human consumption which may or may not push US exports, while, the other wildcard will be Prospective Plantings March 31st. In the overnight electronic session the May corn is currently trading at 641 ¾ which is 1 ¾ of a cent lower. The trading range has been 646 ¾ to 641 ¼.

On the Ethanol Front Pro Farmer reports the Brazilian government is set to resume the collection of federal taxes on fuels this week, the Finance Ministry said on Monday, with the rate of fossil fuels higher than for biofuels. A measure to exempt federal taxes levied on fuel was launched by former President Jair Bolsonaro last year as he sought to boost his popularity by lowering prices ahead of a re-election bid. But President Luiz Inacio da Silva, who defeated Bolsonaro in October, extended the tax waiver on diesel and biodiesel until December of this year, and on gasoline and ethanol until February. The end of the waiver is seen positively by Brazil’s ethanol industry, since without taxes the biofuel loses its competitiveness against gasoline. There were no trades or open interest in the CBOT ethanol futures.

Read Full Story »»»

DiscoverGold

Russian Raking It In. The Energy Report

By: Phil Flynn | February 28, 2023

Oil is popping off Russian oil comments surrounding its production cut as a false sense of security has blanketed Europe’s surrounding victory over the global energy crisis. Gazprom Neft Chief Alexei Miller (Chairman) Alexander Dyukov in a meeting in Iran said that he predicts that oil will be in a range between $80-$110 per barrel is the predicted oil price range in 2023. He also defends Russian oil production cuts. He said that, “the world oil market is currently in surplus, he added, noting that the decision to cut oil production in Russia in March is aimed at balancing it. He also said to get ready for more volatility, so you had better buckle up.

Mr. Dyukov also is right about volatility as the oil market can’t decide if weak economic data should be bullish or bearish. Yesterday Dan Molinski at Dow Jones reported that, “US crude-oil prices are extending earlier declines, recently down 0.8% at $75.72 a barrel after a January report on US durable goods didn’t paint the rosiest of pictures for industrial activity, or more specifically the transportation sector, which accounts for two-thirds of all oil demand. The Commerce Department report showed an overall 4.5% month-on-month decline in new durable goods orders, but a 13.3% drop in new transportation equipment orders. That was due mostly to volatile nondefense aircraft and parts orders, but less-volatile motor vehicles and parts orders stayed sluggish, showing a paltry 0.2% increase in January after a 0.6% rise in December and no growth in November.

Yet previously the market was worried that the economy was too strong based on home sales and stronger than expected consumer confidence and jobs. That was a sign that the Fed wants to be more aggressive with interest rates that increased the value of the dollar. Make up your mind. This Dr. Jekyll and Mr. Hyde’s reactions to data that is too hot or too cold will soon change as the reality that demand will soon rise and supplies will fall as refinery runs and China ramps up. That is why I strongly recommend hedging before things start to heat up.

Russian oil revenues are much better than previously reported. SSRN reported that as sanctions on Russian energy were only implemented towards the end of 2022—and as global prices for oil and gas soared—Russia’s goods exports reached a record $532 billion in 2022, resulting in an all-time high trade surplus of $316 billion. Russia was able to redirect crude oil exports from Europe to alternative markets such as India, China, and Turkey with no loss of volumes, albeit at the cost of accepting discounts in a subset of markets where the EU embargo has dramatically lowered demand (i.e., shipments from Baltic and Black Sea ports). This curbed Russian oil export revenues in 2022, which would have been considerably larger without discounts. This also suggests that Russia, at least initially, chose to not reduce volumes in the face of downward pressure on prices. Surprisingly, we do not find crude oil discounts as large as those reflected in Urals prices: in the post-embargo/price cap period, the average export price for Russian crude oil stood at around $74/barrel based on our data—compared to Urals at $52/barrel.

Crude oil inventories should get their first drawdown this year and should lead to a long trend of falling US oil supply. We won’t have SPR oil to back us up much longer.

Fox Business reported that Biden’s favorite anti US oil company talking point is just wrong. Argus Media also reported that Joe Biden’s repeated claim that oil companies are sitting on 9,000 federal drilling permits overstated the backlog of unused permits, according to new data.

Oil and gas operators only had 6,650 approved but unused drilling permits on federal and tribal lands as of 31 January, according to the US Bureau of Land Management’s (BLM) latest data. The government’s tally of unused drilling permits was overstated, an error caused by a “reporting discrepancy” arising from a transition to a new database in 2020, BLM said today. The 9,000 tally became a core talking point for the White House last summer, as administration officials attempted to blame the oil industry for a spike in gasoline and oil prices at the time. Biden argued the industry was intentionally holding back on a new production as a way to inflate their own profits.

“They have 9,000 permits to drill,” Biden said last June. “Why aren’t they drilling? Because they make more money not producing more oil.” The White House said its criticisms of the oil and gas sector are still valid, even if there are fewer unused federal drilling permits than it stated before. They also stand by forcing people to get vaccinated and covering up evidence that the covid 19 virus most likely came from a lab in Wuhan China. And covering up that the vaccine actually would not stop you from getting covid as they claimed.

There is global importance of the US as a natural gas producer to the world and the reality that usage of natural gas is not going away anytime soon. Dow Jones reported that Cheniere could be included in the S&P 500. Dow Jones said that shares of Houston-based Cheniere Energy, the largest US LNG producer and the world’s second-largest operator, may be included in the S&P 500, says Cowen. “It is unclear how quickly the name could be included in the index, though the market is likely to find out March 3 when new adds are announced.

Read Full Story »»»

DiscoverGold

Grains Report: Wheat, Rice, Corn and Oats, Soybeans

By: Jack Scoville | February 27, 2023

• WHEAT

General Comments: Wheat markets were lower last week and Chicago SRW prices traded to new lows for the last year. News that USDA estimated planted area very high for the coming production and ideas that big Russian offers and cheaper Russian prices would be a feature for a while in the world market were the driving forces for the weaker prices, and price weakness could continue this week. News that Russia has launched a new offensive in Ukraine provided much of thew support this week. Russia appears to be sending three divisions across the border to fight and it looks as though this could be a major operation for the Russian army. Wire report now suggest that Russia has now committed almost its entire army to the war. Fears of deliveries of Wheat from the Black Sea will be cut significantly are surfacing again. Ideas are that both Australia and Russia are harvesting record to near record Wheat crops this year. Russia is said to be plotting a huge new invasion of Ukraine that could prevent farmers in Ukraine from harvesting Wheat and planting Corn. Russia has a large production and is undercutting most world prices in the international market. However, Russian production estimates have dropped recently. The demand for US Wheat in international markets has been a disappointment all year and has been hindered by low prices and aggressive offers from Russia. Ukraine is also looking for new business for its crops and Russia is aggressive in the world market as it looks for cash to fund the war.

Overnight News: The southern Great Plains should get mostly dry conditions. Temperatures should be below normal. Northern areas should see big snows. Temperatures will average below normal. The Canadian Prairies should see mostly dry conditions. Temperatures should average below normal.

Chart Analysis: Trends in Chicago are mixed to down with no obj3ectives, Support is at 716, 704, and 692 May, with resistance at 744, 765, and 773 May. Trends in Kansas City are down with no objectives. Support is at 825, 807, and 800 May, with resistance at 853, 862, and 866 May. Trends in Minneapolis are down with no objectives. Support is at 927, 922, and 906 March, and resistance is at 942, 947, and 955 May.

• RICE:

General Comments: Rice was lower again Friday and sharply lower for the week as the market is in a free fall from recent highs. USDA forecast a jump in production and demand yesterday with a fall in prices. Reports indicate that the farmers have been selling and ideas are that they might dump on the market if they think a big crop is coming at the end of the new growing season that is now getting ready to start in southern growing areas. Demand has been good from domestic sources. Export demand has been uneven. Demand has been an issue for the market all year. There is not much going on in the domestic market right now although mills are milling for the domestic market in Arkansas and are bidding for some Rice. Markets from Texas to Mississippi are called quiet. Demand in general has been slow to moderate for Rice for exports and solid for domestic uses.

Overnight News: The Delta should get mostly dry conditions. Temperatures should be below normal.

Chart Analysis: Trends are down with objectives of 1625 May. Support is at 1689, 1683, and 1670 May and resistance is at 1714, 1728, and 1737 May.

• CORN AND OATS

General Comments: Corn closed sharply lower last week in response to the USDA Outlook Conference that showed increased planted and harvested area and increased yields for potential production of more than 15 billion bushels and the second biggest crop on record and partly on the charts as price trends turned down and some big support areas were broken. US prices are currently very competitive with those from South America and US demand has improved because of the price differentials. Prices from South America should now remain strong as countries there concentrate on Soybeans exports, so the US has chance now to see export demand improve more than it has already. The export demand remains well behind the pace to make USDA objectives. Brazil has been hanging on for its Summer crop although losses are now being reported. The situation is now more stable in southern Brazil and northern Argentina after recent rains, but the situation in central and southern Argentina remains stressed. Argentina has suffered through some extreme drought and losses could be large. The Brazil Winter crop is harvested and China has been buying the surplus. The Summer crop and the Argentine crop is developing under stressful conditions. The next Winter crop is going into the ground in good conditions, but it has been wet so the Soybeans harvest has been delayed and the Corn planting is becoming delayed as well. There are concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. China is now moving rapidly to open the economy and allow people to move around with no lockdowns so the demand could start to improve

Overnight News:

Chart Analysis: Trends in Corn are down with objectives of 638 May. Support is at 648, 645, and 637 May, and resistance is at 660 668, and 672 May. Trends in Oats are mixed. Support is at 342, 333, and 330 May, and resistance is at 348, 358, and 361 May.

• SOYBEANS

General Comments: Soybeans and the products were a little lower on Friday and Soybean Oil closed a little lower for the week while the others closed a little higher. The market is weaker in response to the USDA Outlook Conference reports that showed planted and harvested area the same as last year and increased yields for increased production and in anticipation of the South American harvest coming to export channels in the near term. It remains hot and dry in Argentina and crop conditions are getting worse. However, weather is becoming less important now as the harvest is already underway in central and northern Brazil and will spread south soon. Sothern Brazil and northern Argentina are getting enough rain to stabilize conditions and production losses but central and southern Argentina remain very dry. Central and northern Brazil have seen harvest operations interrupted with too much rain. Soybean Meal saw strong weekly export sales as Argentina is having to withdraw from the market for Soy products sales due to the drought in the country and the fact that they have already sold a lot of Soybeans into the world market. They are now buying from Brazil. The harvest in Brazil is slowly expanding in central and northern areas. These areas have seen too much rain and the harvest has been slow. Production potential for the Brazil is called very strong even with potential problems and losses in the south. Argentine production ideas continue to drop with the drought as planting is delayed and the crops already in the ground are stressed. Ideas that Chinese demand will improve, but this could take a few more weeks as a very large part of the population now has Covid. This has delayed a robust economic return for the country.

Overnight News:

Chart Analysis: Trends in Soybeans are mixed. Support is at 1510, 1500, and 1476 May, and resistance is at 1533, 1549, and 1560 May. Trends in Soybean Meal are mixed. Support is at 474.00, 471.00, and 465.00 May, and resistance is at 485.00, 487.00, and 493.00 May. Trends in Soybean Oil are mixed. Support is at 6080, 5970, and 5900 May, with resistance at 6240, 6480, and 6440 May.

Read Full Story »»»

DiscoverGold

Softs Report: Cotton, OJ, Coffee, Sugar, Cocoa

By: Jack Scoville | February 27, 2023

• COTTON

General Comments: Cotton was higher on Friday and for the week as USDA kept with low planted area forecasts in its ideas released to the market on Thursday. Export demand was very strong when the sales report was released on Friday morning. USDA forecast a significant reduction in US planted area for Cotton in its outlook conference at about 10.5 million acres. Demand was very strong in the report last week and has been ramping up for the last couple of months. Some ideas that demand could soon increase more as China could start to open its economy in the next couple of months as Covid outbreaks should start to weaken as people get vaccinated or immune. Covid is now widespread in China so the beneficial economic effects of the opening are being delayed but these effects should start to be felt as the people there achieve immunity over the next week or two. The charts show that futures held at a test of the lows formed since November and that prices could start to move higher to the top end of the range at ab out 90 cents in the next few weeks.

Overnight News: The Delta will get mostly dry conditions and above normal temperatures. The Southeast will see isolated showers and above normal temperatures. Texas will have mostly dry conditions and above normal temperatures. The USDA average price is now 82.86 ct/lb. ICE said that certified stocks are now 1,147 bales, from 8,900 bales yesterday. ICE NY said that 0 notices were posted for delivery against March contracts and that total deliveries for the month are now 0 contracts.

Chart Trends: Trends in Cotton are mixed to up with objectives of 8740 and 9140 May. Support is at 82.90, 82.40, and 80.90 May, with resistance of 85.70, 86.90 and 87.90 May.

• FCOJ

General Comments: FCOJ was higher Friday and for the week as production remains the overriding force. The charts show that May is now challenging contract highs, but futures need to trade t about 367.00 to make new all time highs. Historically low estimates of production due in part to the hurricanes and in part to the greening disease that have hurt production, but conditions are significantly better now with scattered showers and moderate temperatures. The weather remains generally good for production around the world for the next crop including production areas in Florida that have been impacted in a big way by the two storms seen previously in the state. Brazil has some rain and conditions are rated good. Brazil continues to export to the EU and is increasing its exports to the US. Mexico is also exporting to the US. Even so, the Florida Dept of Citrus reported that inventories are still 40.6% below last year at 102.39 million pounds.

Overnight News: Florida should get mostly dry conditions. Temperatures will average above normal. Brazil should get scattered showers and near normal temperatures.

Chart Trends: Trends in FCOJ are up with objectives of 255.00 May. Support is at 235.00, 228.00, and 223.00 May, with resistance at 249.00, 253.00, and 261.00 May.

• COFFEE

General Comments: New York and London closed lower Friday in correction trading after the big rally early last week tied to higher differentials in Brazil and Vietnam caused by a lack of offers from producers in both countries. Futures finished higher for the week and could work higher again this week. Producers are not offering right now and the market wonders how much Coffee is left. Ideas of big production for Brazil continue due primarily to rains falling in Coffee production areas now. Vietnam is estimated to have veery good production this year due to a good growing season. There are ideas that production potential for both countries has been overrated. The weather in Brazil is currently very good for production potential but worse conditions seen earlier in the growing cycle hurt the overall production prospects as did bad weather last year. Vietnam is getting less rain now to aid harvet progress but volumes offered have not increased.

Overnight News: ICE certified stocks are lower today at 0.800 million bags. The ICO daily average price is now 178.96 ct/lb. Brazil will get scattered showers with near to above normal temperatures. Central America will get scattered showers. Vietnam will see scattered showers. ICE NY said that 0 contracts were tendered for delivery against March futures and that total deliveries for the month are now 572 contracts.

Chart Trends: Trends in New York are up with objectives of 209.00 May. Support is at 190.00, 187.00, and 184.00 May, and resistance is at 201.00, 205.00 and 206.00 May. Trends in London are up with no objectives. Support is at 2130, 2090, and 2080 May, and resistance is at 2210, 2250, and 2280 May.

• SUGAR

General Comments: New York and London closed lower on Friday and for the week as traders continue to factor in production losses in India and Brazil and other locations as well. Indian production is thought to be 33 million tons this year or less and the market has had to ration that supply via price. Thailand expects to export 7% more than last year. Good production prospects are seen for crops in central and northern areas of Brazil, but the south has seen drier weather. There is concern that the rainy areas will stay too wet and delay the harvest and dilute the Sugar concentrations in the cane in central areas. The harvest is active in Thailand. Australia and Central America harvests are also active. European production is expected to be reduced again this year.

Overnight News: Brazil will get scattered showers. Temperatures should average near to above normal. India will get mostly dry conditions and near to above normal temperatures.

Chart Trends: Trends in New York are mixed. Support is at 1960, 1940, and 1900 May and resistance is at 2030, 2050, and 2080 May. Trends in London are mixed. Support is at 557.00, 549.00, and 545.00 May and resistance is at 578.00, 582.00, and 588.00 May.

• COCOA

General Comments: New York and London closed mostly a little lower on Friday and for the week in correction trading as West African exporters are not offering. Wire reports suggest that exporters are currently looking for Cocoa to make good on current contracts and are not entering into new contracts right now. However, the Ivory Coast Cocoa and Coffee Council said that there will be more than enough Cocoa for export and that exporters can fix contracts. Trends have turned up in both New York and London for the longer term, but have turned mixed for the short term. Talk is that hot and dry conditions reported in Ivory Coast could curtail mid crop production, but main crop production ideas are strong. Ghana has reported a disease in its Cocoa to hurt production potential there. The rest of West Africa appears to be in good condition. Good production is reported for the main crop and traders are worried about the world economy moving forward and how that could affect demand. The weather is good in Southeast Asia.

Overnight News: Mostly dry conditions are forecast for West Africa. Temperatures will be near normal. Malaysia and Indonesia should see scattered showers. Temperatures should average near normal. Brazil will get scattered showers and near to above normal temperatures. ICE certified stocks are lower today at 5.042 million bags. ICE NY said that there were 380 notices posted for delivery against March contracts and that total deliveries for the month are now 601 contracts.

Chart Trends: Trends in New York are up with objectives of 2840 and 2860 May. Support is at 2700, 2670, and 2650 May, with resistance at 2810, 2840, and 2870 May. Trends in London are mixed. Support is at 2100, 2060, and 2040 May, with resistance at 2150, 217e0, and 2200 May.

Read Full Story »»»

DiscoverGold

Lumber- Up And Down And All Around

By: Barchart | February 27, 2023

Lumber is a critical industrial commodity that reflects the overall economy and the demand for new housing. On February 1, in a Barchart article, I highlighted the rally in lumber futures that took the price above $500 per 1,000 board feet. In that piece, I wrote, “the most recent inflation data shows the economic condition is declining. While inflation is nowhere near the Fed’s 2% target, the potential for a recession could curb the central bank’s enthusiasm for increasing short-term rates. Lumber’s price action could tell us that rates will level off in 2023, and the demand for new homes will increase.” Meanwhile, March lumber futures peaked at $533.70 on February 1, where they ran out of upside steam. While inflation data remains below last year’s high, the most recent readings were above the market’s expectations, and lumber prices have turned lower, with the March random-length lumber contract falling below $400 per 1,000 board feet.

The Fed is not likely to stop increasing rates

The January consumer and producer price index data and the latest minutes from the FOMC’s early February meeting set the stage for continuation interest rate hikes to push the Fed Funds Rate over the 5% level.

From March 2022 through early February 2023, the central bank increased the short-term interest rate from a band of zero to twenty-five basis points to 4.5% to 5.0%. The latest rate hike was only 25 basis points, but the Fed took an aggressive approach to tighten credit throughout 2022:

Source: Forbes.com

The chart shows four consecutive 75-point rate hikes from June 2022 to November 2022. The U.S. central bank is committed to returning inflation to its 2% target rate, but the economic condition remains at the highest level in decades, despite the significant credit tightening.

Meanwhile, short-term rate hikes are just one of the tools the Fed has employed. Quantitative tightening or reducing the central bank’s swollen balance sheet has put upward pressure on interest rates further along the yield curve.

The Fed follows the personal consumption expenditures price index or PCE instead of CPI or PPI. Last Friday, the PCE data for January showed a 0.6% from the prior year, which was about economists’ expectations. The inflation data tells us the Fed will increase the short-term rate by 25 or 50 basis points at the upcoming March FOMC meeting.

Random-length and physical lumber prices declined

Lumber is a primary requirement for new home building, and higher interest rates have caused the demand for new homes to decline. After reaching record highs in 2021 and 2022, lumber prices have plunged and returned to levels not seen since the global pandemic gripped markets across all asset classes.

The long-term chart shows the all-time high in the lumber futures market before 2018 was the 1993 $493.50 high. In March 2021, the price exploded to a record $1,711.20 per 1,000 board feet. After correcting to $448 in August 2021, the price took off on the upside again, reaching $1,477.40 in March 2022. Lumber reached highs in the zero percent short-term interest environment. With 30-Year fixed-rate mortgages rising from below 2% in late 2021 to over 7%, new home, and lumber demand has plunged, with the nearby March 2023 random-length lumber futures below the $400 level on February 27...

* * *

Read Full Story »»»

DiscoverGold

Today's Futures Heat Map • Strongest: Orange Juice, Natural Gas, Sugar, Platinum

By: Barchart | February 27, 2023

• Today's Futures Heat Map

Strongest: Orange Juice, Natural Gas, Sugar, Platinum

Weakest: Hard Red Wheat, Wheat, Soybean Oil, Crude Oil

Read Full Story »»»

DiscoverGold

Deliveries on Sugar/Energies/Grains/Treasuries/Canola/Metals/Ethanol

By: The PRICE Futures Group | February 27, 2023

• Tues, Feb 28th is LTD for Feb Cattle, March Sugar #11, March Heating Oil and RBOB.

• Tues, Feb 28th is FND for March MGEX Wheat, CBOT Grains, CBOT Treasuries, IFUS Canola and March Metals.

• Fri, March 3rd is LTD for March Ethanol.

Read Full Story »»»

DiscoverGold

Closing In On Spring. The Corn & Ethanol Report

By: Daniel Flynn | February 27, 2023

We kickoff the day with Durable Goods Orders MoM, Durable Goods Ex Transportation MoM, Non-Defense Goods Orders Ex Air and Durable Goods Orders ex Defense MoM at 7:30 A.M., Pending Home Sales MoM & YoY at 9:00 A.M., Dallas Fed Manufacturing Index and Fed Jefferson Speech at 9:30 A.M., Export Inspections at 10:00 A.M., 3-Month & 6-Month Bill Auction at 10:30 A.M., and Trout Production at 2:00 P.M.

On the Corn Front weather in the US and South America is another factor weighing in on the pendulum as other factors come into play with the USDA January report showing a reduction of 1.6 million acres of corn harvested in the 2022 crop and Argentina is experiencing their worst drought in 60 years. The 2023 production estimate pressured the market and the export market is doing anything but hype the bulls. We most likely will have a clearer direction after Prospective Plantings on March 31st. I still see a danger zone with food shortages with corn feed for livestock and global demand for food for human consumption. In the overnight electronic session the March corn is currently trading at 651 ¼ which is 1 ¼ of a cent lower. The trading range has been 654 to 649 ¾.

On the Ethanol Front Alexandria Chapman and Eduardo Tinti reporting for Fastmarkets Agricensus said Brazilian officials will decide on ethanol, gasoline tax exemption. A group of Brazilian officials including President Luiz Inacio da Silva will meet today in an effort to make the ethanol, gasoline market affordable. This is showing a thriving ethanol cash market while US ethanol futures remain dormant.

Read Full Story »»»

DiscoverGold

Too Hot? The Energy Report

By: Phil Flynn | February 27, 2023

Global oil markets are having a hard time determining whether they should worry about the economy. Is it too hot or too cold. Red hot inflation data in the US sent the stock market tumbling and weighed on oil even though there are signs of an increase in risk to supplies.

Over the weekend, a sign of what may be more to come, Russia cut oil flows to Poland, following through on their threat to not sell oil to any country, directly or indirectly, involved with the EU price cap. Later, Russian oil pipeline monopoly Transneft on Monday said there were no flows of oil to Poland because the paperwork for supplies in the second half of February had not been completed, Russia’s TASS news agency reported. Yet the reality is that this is Russia’s first shot across the bow and should serve as a warning to those that ideally dismiss Russia’s threat to not sell oil. It should also serve as a warning to the grain trade as well.

While the US sends record amounts of oil and gas to Europe, there are signs that because of low natural gas prices and the Biden administrations’ selling of Strategic Petroleum Reserves supplies, that US oil and gas drillers are pulling back. Reuters reported that – U.S. energy firms in February cut the most oil and natural gas rigs in a month since June 2020, with the gas rig count falling to the lowest since April, energy services firm Baker Hughes Co (BKR.O) said in its closely followed report on Friday. The oil and gas rig count, an early indicator of future output, fell seven to 753 in the week to Feb. 24. Despite this week’s rig decline, Baker Hughes said the total count was still up 103 rigs, or 15.8%, over this time last year.

There are true signs in the marketplace right now that the Biden administration’s unprecedented intervention of releasing Strategic Petroleum Reserve supplies is going to leave the market short later in the year. The market has become dependent on strategic reserve supplies like a drug addict is on drugs. It will start to be painful when they start to realize that there are no more supplies from the SPR. Losing the SPR release is like losing the 16th biggest oil producer in the world and that’s going to be felt especially when the US refiners start to come out of maintenance. The foolishness of these policies will be very apparent later in the year.

One of the most bullish factors for oil continues to be the reopening of the Chinese economy. S&P Global Platts reported that China’s small independent refineries doubled their fuel oil imports the month in February amid good refining margins and a tight supply of the alternative feedstock bitumen blend, refining, and trading sources told S&P Global Commodity Insights Feb. 27.

Read Full Story »»»

DiscoverGold

Commodities Pressured By Rising Dollar Index And Uncertainties

By: Barchart | February 26, 2023

Commodities appear severely pressured by the rising dollar index and several factors coming into play with grains, livestock, metals and energies. We follow our precise entry/exit strategies for the short-term hedger with some commentary in the Ag and Livestock sectors:

Charts - Drop us a note on Twitter @TradeGuidance or via email for a ToS Chartbook for the entire set of instruments shown above. Better yet, join us for a month and see if we can help improve your overall trading results.

In the Livestock sector:

Lean hogs stayed net green for week, but saw Friday losses between 15~ 55 cents across the front months. From Friday to Friday April hogs were still up by 75 cents. USDA’s National Average Base Hog price was 15 cents stronger to $77.68. The CME Lean Hog Index for 2/22 was 20 cents stronger at $77.73.

Pork cutout futures went into the weekend with Friday losses up to $0.45. USDA’s National Pork Carcass Cutout value was $85.35, down by 68 cents. USDA estimated FI hog slaughter for the week through Saturday at 2.375m head. That is down from 2.505 million last 2.492m head during the same week last year. The YTD total of 20.068m head is 1.3% ahead of last year’s pace.

Cattle

Monthly reports from NASS had the cattle herd numbers pegged at 11.704m head on Feb 1 for the 1,000+ head capacity feedlots. That was a tad bit over 4.1% loss YoY compared to the average estimate of -3.5%. January placements were shown at 1.932m head, a 3.6% drop YoY compared to the average 2.9% expectation. The report had 1.847m head marketed in Jan, a 4.2% increase compared to the expected 3.9% increase. USDA mentioned 1,000+ head feedlots made up 82.5% of the total inventory on Jan 1, which was up from almost 82% share last year.

In the Grains sector:

Wheat

USDA reported 339K MT of wheat was sold for export during the week that ended 2/16. That was up from 209k MT last week, as a 4-wk high led by sales to the Philippines. By class, the report had 36% of the total sale as HRS with 24% each for white and HRW. Old crop wheat commitments were 16.85 MMT, trailing last year’s 17.98 MMT pace. New crop wheat has 413,461 MT on the books as of 2/16. The European Union took 400k MT off their wheat production estimates citing multiple reasons ranging from the war in Ukraine to weather and now at 126 MMT, and among other reasons calling out low soil moisture reserves into the growing season.

Beans

Soymeal sales were 65.5K MT for the week that ended 2/16, which was below estimates. Accumulated meal commitments were 7.553 MMT as of 2/16. Soybean oil bookings for the week were shown as 755 MT of net cancelations. Soy oil commitments were just under 51K MT as of 2/16. The BAGE lowered their estimate for Argentina’s soybean crop by 4.5 MMT to 38 MMT.

Corn

USDA’s FAS reported a 20% drop in weekly corn bookings with the first sub-1 MMT booking in 4 weeks. The Export Sales report had 823k MT of sales, which was within the range of estimates, as Japan bought 312k MT (including 137k MT switched from unknown) and Mexico booked 290k MT. The old crop book numbers are lower by 40% YoY and include 14.36 MMT of shipments and 14.28 MMT of outstanding sales. For new crop corn, there is 1.563 MMT on the books as of 2/16. Meanwhile, Brazil’s 2023 ethanol output is expected to increase 5.4% citing a better sugar crop and the need for domestic production following tariff implementation on U.S. ethanol. It is estimated that over half of Brazil’s 2nd crop corn has missed the “ideal planting window” as 18.2% of Parana fields. Argentina Corn crop estimates have also seen a lowered reading.

Read Full Story »»»

DiscoverGold

Today's Futures Heat Map • Weakest: Platinum, Wheat, Copper, Palladium

By: Barchart | February 24, 2023

• Today's Futures Heat Map

Strongest: Natural Gas, Orange Juice, Heating Oil, Lumber

Weakest: Platinum, Wheat, Copper, Palladium

Read Full Story »»»

DiscoverGold

Sugar in the Red: Just a Bump or Is the Sweet Ride Over?

By: Investing.com | February 24, 2023

• Sugar in the red for Feb after rallying from end-Sept through Jan

• Sweetener gained 22% in four months; now Feb slide less than 1%

• Some analysts say output is building, and this could weigh on sugar prices

• Others predict a deeper technical slide to allow the market to ‘recharge’

After a sweet four-month ride, those long sugar are seeing red for the first time in February as good or active cane harvests in Brazil to Thailand trigger profit-taking among investors fearing higher output.

February's setback in New York-traded raw sugar futures is modest: With just two sessions left for the month, the market is off less than 1%. That too after a rally of 22% from end-September through January that came with cherry topping in the form of a six-year high of 21.82 cents a lb.

In Thursday’s trade, sugar futures front-month contract for March settled at 21.58 a lb. As of this writing, the commodity trades marginally higher, at 21.68 a lb.

So, is this slide just a bump or is the sweet ride about to end?

Sugar Daily Chart

Charts by SKCharting.com, with data powered by Investing.com

At the outset, there doesn't seem to be too much that can severely disrupt the momentum of the past four months or send the market completely in the reverse.

Yet, some analysts are cautioning that production is building. Others are citing the possibility of a further technical slide before bulls can regroup at the lower level to charge higher.

Output-wise, good progress is seen in the crop in major growing countries Brazil and Thailand, said Jack Scoville, chief crop analyst at Chicago’s Price Futures Group. He adds:

“Thailand expects to export 9.0 million tons of sugar in the current crop year, 7% more than last year. Ideas are that the market has also priced in production losses in India and Brazil.

Good production prospects are seen for crops in central and northern areas of Brazil, but the south has seen drier weather. There is concern that the rainy areas will stay too wet and delay the harvest and dilute the sugar concentrations in the cane in central areas. The harvest is active in Thailand. Australia and Central America harvests are also active while European production is expected to be reduced again this year.”

India, the world's second-largest sugar exporter, is likely to produce 34 million tonnes of the sweetener in 2022/23, down 7% from the previous forecast, a leading trade body said at the end of January.

The rally from a month ago was also helped by speculation that top exporter Brazil might also produce less if its energy policy improves ethanol's profitability.

Sugar Weekly Chart

On the charts side, sugar futures are strong enough on daily, weekly and monthly time frames to sustain their broadly bullish perspective, said Sunil Kumar Dixit, chief technical strategist at SKCharting.com.

Sugar Monthly Chart

But he also cautioned that the market could retest support at the lower 21-cent level to find energy for a push higher, adding:

“Daily chart is nearly done with momentum distribution supported by the Relative Strength Index at above neutrality of 50 while Stochastics at 77/64 are firmly positioned.

But prices could also be awaiting a break above the symmetrical triangle resistance of 21.75 cents. The alternative is a retest of support at $21.40 before uptrend resumes with targets of 23 cents and 24.10 cents.”

Read Full Story »»»

DiscoverGold

Grains Report: Wheat, Rice, Corn and Oats, Soybeans

By: Jack Scoville | February 24, 2023

• WHEAT

General Comments: Wheat markets were mostly lower yesterday on newss that USDA estimated planted area very high for the coming productiio and on ideas that big Russian offers and cheaper Russian prices would be a feature for a while in the world market. News that Russia has launched a new offensive in Ukraine provided much of thew support this week. Russia appears to be sending three divisions across the border to fight and it looks as though this could be a major operation for the Russian army. Wire report now suggest that Russia has now committed almost its entire army to the war. Fears of deliveries of Wheat from the Black Sea will be cut significantly are surfacing again. Ideas are that both Australia and Russia are harvesting record to near record Wheat crops this year. Russia is said to be plotting a huge new invasion of Ukraine that could prevent farmers in Ukraine from harvesting Wheat and planting Corn. Russia has a large production and is undercutting most world prices in the international market. However, Russian production estimates have dropped recently. The demand for US Wheat in international markets has been a disappointment all year and has been hindered by low prices and aggressive offers from Russia. Ukraine is also looking for new business for its crops and Russia is aggressive in the world market as it looks for cash to fund the war.

Overnight News: The southern Great Plains should get mostly dry conditions. Temperatures should be below normal. Northern areas should see big snows. Temperatures will average below normal. The Canadian Prairies should see mostly dry conditions. Temperatures should average below normal.

Chart Analysis: Trends in Chicago are mixed to down with obj3ectives of 704, 698, and 689 March, Support is at 733, 721, and 713 March, with resistance at 744, 755, and 760 March. Trends in Kansas City are down with objectives of 848 March. Support is at 859, 849, and 842 March, with resistance at 871, 877, and 884 March. Trends in Minneapolis are mixed to down with objectives of 900, 876 and 867 March. Support is at 902, 896, and 890 March, and resistance is at 915, 919, and 928 March.

• RICE:

General Comments: Rice was lower again yesterday as the market is in a free fall from recent highs near 1800 March. USDA forecast a jump in production and demand yesterday with a fall in prices. It looks like traders took the fall in prices to heart and tried to make it true for anytime after yesterday. Reports indicate that the farmers have been selling and ideas are that they might dump on the market if they think a big crop is coming at the end of the new growing season that is now getting ready to start in southern growing areas. Demand has been good from domestic sources. Export demand has been uneven. Demand has been an issue for the market all year. There is not much going on in the domestic market right now although mills are milling for the domestic market in Arkansas and are bidding for some Rice. Markets from Texas to Mississippi are called quiet. Demand in general has been slow to moderate for Rice for exports and solid for domestic uses.

Overnight News: The Delta should get mostly dry conditions. Temperatures should be below normal.

Chart Analysis: Trends are down with no objectives. Support is at 1666, 1652, and 1640 March and resistance is at 1699, 1723, and 1746 March.

• CORN AND OATS

General Comments: Corn closed sharply lower in response to the USDA Outlook Conference that showed inceased planted and harvested area and increased yields for potential production of more than 15 billion bushels and the second biggest crop on record and partly on the charts as price trends turned down and some big support areas were broken. US prices are currently very competitive with those from South America and US demand has improved because of the price differentials. Prices from South America should now remain strong as countries there concentrate on Soybeans exports, so the US has chance now to see export demand improve more than it has already. The export demand remains well behind the pace to make USDA objectives. Brazil has been hanging on for its Summer crop although losses are now being reported. Argentina has suffered through some extreme drought and losses could be large. The Brazil Winter crop is harvested and China has been buying the surplus. The Summer crop and the Argentine crop is developing under stressful conditions. The next Winter crop is going into the ground in good conditions, but it has been wet so the Soybeans harvest has been delayed and the Corn planting is becoming delayed as well. There are concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. China is now moving rapidly to open the economy and allow people to move around with no lockdowns so the demand could start to improve

Overnight News:

Chart Analysis: Trends in Corn are down with objectives of 651, 642, and 636 March. Support is at 654, 649, and 647 March, and resistance is at 669, 673, and 676 March. Trends in Oats are mixed. Support is at 360, 357, and 348 March, and resistance is at 375, 3782, and 389 March.

• SOYBEANS

General Comments: Soybeans and Soybean Oil were lower, but Soybean Meal closed higher. The market is weaker in response to the USDA Outlook Conference reports that showed planted and harvested area the same as last year and increased yields for increased production and in anticipation of the South American harvest coming to export channels in the near term. It remains hot and dry in Argentina and southern Brazil and crop conditions are getting worse. However, weather is becoming less important now as the harvest is already underway in central and northern Brazil and will spread south soon. Central and northern Brazil have seen harvest operations interrupted with too much rain. Soybean Meal saw strong weekly export sales as Argentina is having to withdraw from the market for Soy products sales due to the drought in the country and the fact that they have already sold a lot of Soybeans into the world market. They are now buying from Brazil. The harvest in Brazil is slowly expanding in central and northern areas. These areas have seen too much rain and the harvest has been slow. Production potential for the Brazil is called very strong even with potential problems and losses in the south. Argentine production ideas continue to drop with the drought as planting is delayed and the crops already in the ground are stressed. Ideas that Chinese demand will improve, but this could take a few more weeks as a very large part of the population now has Covid. This has delayed a robust economic return for the country.

Overnight News:

Chart Analysis: Trends in Soybeans are mixed. Support is at 1532, 1517, and 1511 March, and resistance is at 1556, 1562, and 1574 March. Trends in Soybean Meal are mixed. Support is at 488.00, 478.00, and 472.00 March, and resistance is at 501.00, 508.00, and 514.00 March. Trends in Soybean Oil are mixed to up with objectives of 6350, 6710, and 6950 March. Support is at 6100, 6070, and 5960 March, with resistance at 6360, 6520, and 6500 March.

Read Full Story »»»

DiscoverGold

Softs Report: Cotton, OJ, Coffee, Sugar, Cocoa

By: Jack Scoville | February 24, 2023

• COTTON

General Comments: Cotton was a little higher in consolidation trading yesterday. USDA forecast a significant reduction in US planted area for Cotton in its outlook conference yesterday. Futures are still showing bad demand fundamentals as the weekly export sales reports have shown moderate sales at best. Some ideas that demand could soon increase as China could start to open its economy in the next couple of months as Covid outbreaks should start to weaken as people get vaccinated or immune. Covid is now widespread in China so the beneficial economic effects of the opening are being delayed but these effects should start to be felt as the people there achieve immunity over the next week or two.

Overnight News: The Delta will get mostly dry conditions and above normal temperatures. The Southeast will see isolated showers and above normal temperatures. Texas will have mostly dry conditions and near normal temperatures. The USDA average price is now 80.12 ct/lb. ICE said that certified stocks are now 1,147 bales, from 8,900 bales yesterday. ICE NY said that 0 notices were posted for delivery against March contracgts and that total deliveries for the month are now 0 contracts. USDA said that weekly net Upland Cotton export sales were 435,300 bales this year and 11,900 bales next year. Net Pima sales were 1,400 bales this year and 0 balex next year.

Chart Trends: Trends in Cotton are mixed. Support is at 80.80, 80.50, and 80.10 May, with resistance of 83.50, 83.90 and 84.50 May.

• FCOJ

General Comments: FCOJ was higher yesterday as production remains the overriding force. Historically low estimates of production due in part to the hurricanes and in part to the greening disease that have hurt production, but conditions are significantly better now with scattered showers and moderate temperatures. The weather remains generally good for production around the world for the next crop including production areas in Florida that have been impacted in a big way by the two storms seen previously in the state. Brazil has some rain and conditions are rated good. Brazil continues to export to the EU and is increasing its exports to the US. Mexico is also exporting to the US. Even so, the Florida Dept of Citrus reported that inventories are still 40.6% below last year at 102.39 million pounds.

Overnight News: Florida should get mostly dry conditions. Temperatures will average above normal. Brazil should get scattered showers and near normal temperatures.

Chart Trends: Trends in FCOJ are mixed to up with no objectives. Support is at 234.00, 229.00, and 220.00 March, with resistance at 249.00, 253.00, and 256.00 March.

• COFFEE

General Comments: New York and London closed lower yesterday in correction trading after the big rally this week tied to higher differentials in Brazil caused by a lack of offers from producers. Producers are not offering right now and the market wonders how much Coffee is left in the country. Ideas of big production for Brazil continue due primarily to rains falling in Coffee production areas now. Vietnam is estimated to have veery good production this year due to a good growing season and less rain now as harvest expands again. There are ideas that production potential for Brazil had been overrated. The weather in Brazil is currently very good for production potential but worse conditions seen earlier in the growing cycle hurt the overall production prospects as did bad weather last year.

Overnight News: ICE certified stocks are lower today at 0.809 million bags. The ICO daily average price is now 180.91 ct/lb. Brazil will get scattered showers with near to above normal temperatures. Central America will get scattered showers. Vietnam will see scattered showers. ICE NY said that 0 contracts were tendered for delivery against March futures and that total deliveries for the month are now 572 contracts.

Chart Trends: Trends in New York are up with objectives of 209.00 May. Support is at 190.00, 187.00, and 184.00 May, and resistance is at 201.00, 205.00 and 206.00 May. Trends in London are up with no objectives. Support is at 2130, 2090, and 2080 May, and resistance is at 2210, 2250, and 2280 May.

• SUGAR

General Comments: New York and London closed higher yesterday as traders continue to factor in production losses in India and Brazil and other locations as well. Indian production is thought to be 33 million tons this year or less and the market has had to ration that supply via price. Thailand expects to export 7% more than last year. Good production prospects are seen for crops in central and northern areas of Brazil, but the south has seen drier weather. There is concern that the rainy areas will stay too wet and delay the harvest and dilute the Sugar concentrations in the cane in central areas. The harvest is active in Thailand. Australia and Central America harvests are also active. European production is expected to be reduced again this year.

Overnight News: Brazil will get scattered showers. Temperatures should average near to above normal. India will get mostly dry conditions and near to above normal temperatures.

Chart Trends: Trends in New York are mixed to up with objectives of 2040 and 2080 May. Support is at 1990, 1960, and 1940 May and resistance is at 2050, 2080, and 2110 May. Trends in London are mixed. Support is at 564.00, 557.00, and 549.00 May and resistance is at 578.00, 582.00, and 588.00 May.

• COCOA

General Comments: New York and London closed mostly a little lower yesterday in correction trading as West African exporters are not offering. Wire reports suggest that exporters are currently looking for Cocoa to make good on current contracts and are not entering into new contracts right now. However, the Ivory Coast Cocoa and Coffee Council said that there will be more than enough Cocoa for export and that exporters can fix contracts. Trends have turned up in both New York and London. Talk is that hot and dry conditions reported in Ivory Coast could curtail mid crop production, but main crop production ideas are strong. Ghana has reported a disease in its Cocoa to hurt production potential there. The rest of West Africa appears to be in good condition. Good production is reported for the main crop and traders are worried about the world economy moving forward and how that could affect demand. The weather is good in Southeast Asia.

Overnight News: Mostly dry conditions are forecast for West Africa. Temperatures will be near normal. Malaysia and Indonesia should see scattered showers. Temperatures should average near normal. Brazil will get scattered showers and near to above normal temperatures. ICE certified stocks are lower today at 5.053 million bags. ICE NY said that there were 0 notices posted for delivery against March contracts and that total deliveries for the month are now 221 contracts.

Chart Trends: Trends in New York are up with objectives of 2840 and 2860 May. Support is at 2700, 2670, and 2650 May, with resistance at 2810, 2840, and 2870 May. Trends in London are mixed. Support is at 2100, 2060, and 2040 May, with resistance at 2150, 217e0, and 2200 May.

Read Full Story »»»

DiscoverGold

Commodities’ Wild Ride: Spikes, Plunges, Re-spikes: Lithium, Lumber, Coal, Wheat, Copper, Steel, Iron Ore, Soybeans, Coffee, Corn

By: Wolf Richter | February 23, 2023

• Oh no, coffee! Commodities are not moving in lockstep.

We’re going to look at a few spectacular wild rides in commodities – but not including crude oil, gasoline, and natural gas which I discuss here separately quite a bit and in greater detail.

Lithium. Remember, just last year, the world was going to have a shortage of lithium carbonate, one of the key raw materials for EV batteries. With all the hype about supply shortages, and booming demand from manufacturers of EV batteries, the price of lithium carbonate spiked. The China lithium carbonate index, a benchmark price, exploded by a factor of 15 in two years, from CNY 40,000 per tonne in November 2020 to CNY 600,000 per tonne by November 2022. And then that was it.

New supply was being put on the map, including in Australia – makes sense at these crazy prices – and demand was strong but not that strong, and all that became clear late last year, and when the hype fizzled as it always does, the price began to plunge. At the moment at CNY 405,500, the price has plunged by 32% in two months, and is now below where it had been a year ago (all charts here via Trading Economics):

Lumber. The price of Chicago lumber futures went through epic gyrations during the pandemic, spiking by 350%, then plunging, then spiking all over again, the plunging all over again, and now it’s back where it used to be, currently at $374 per thousand board feet:

* * *

Read Full Story »»»

DiscoverGold

The Corn & Ethanol Report

By: Daniel Flynn | February 24, 2023

We kickoff the day with Core PCE Price Index MoM & YoY, Export Sales, PCE Price Index MoM & YoY and Personal Income at 7:30 A.M., New Home Sales MoM, New Home Sales, Michigan Consumer Sentiment Final, Michigan 5-Year Inflation Expectations Final, Michigan Current Conditions Final and Michigan Inflation Expectations Final at 9:00 A.M., Fed Jefferson Speech and Fed Mester Speech at 9:15 A.M., Baker Hughes Oil & Total Rig Count at 12:00 P.M., Cattle on Feed and Cold Storage at 2:00 P.M., Building Permits Final, Monetary Policy Forum and Building Permits MoM Final.

On the Corn Front a report of the Ohio toxic spill trainwreck could have been 100% preventable according to boots on the ground reports. The damage in soil and waterbeds will take years if not decades to fully recover and have acceptable readings. Any crops grown in the area will be and be carefully monitored for export, and the Ohio River locks remain closed until cleanup is underway and maybe longer. This may further disrupt barge traffic in the main arteries In the coming months sending barges to the New Orleans shipping region. We closed lower yesterday after the USDA projection for 91 million acres of corn was vied a negative for corn prices late in 2023 and selling pressure led by farmers and funds kicked into high gear. Corn bulls were not excited to see sizable supply numbers in the upcoming US crop year. However, they know that both acreage and yield numbers are far from settled. Traders will be waiting for Prospective Plantings on March 31st. In the overnight electronic session the March corn is currently trading at 654 ½ which is 5 ¾ cents lower. The trading range has been 662 ½ to 653 ½.

On the Ethanol Front production and consumption for ethanol as a transportation fuel grew significantly over the last three decades in the US before plateauing in recent years due to the pandemic. Meanwhile, the US Grains Council staff and Ethanol Advisory Team members traveled to Ottawa, Canada, from Jan31 to Feb2, 2023, to meet Canadian government officials and private stakeholders to discuss details related to the Canadian Clean Fuel Regulation released in July 2022. During this visit, the Council reiterated its enthusiasm and support for regulation and advised against further delay of clear guidance necessary for its successful implantation. Canada has been a significant growing market for US ethanol the past decade and the top destination the last three years setting racords. There were no trades or open interest in ethanol futures.

Read Full Story »»»

DiscoverGold

Give Or Take. The Energy Report

By: Phil Flynn | February 24, 2023

The Energy Information Administration (EIA) reported yesterday that US commercial crude oil inventories increased by 7.6 million barrels last week, give or take 15 million barrels or so. For the second week in a row, the EIA had a major crude oil adjustment to balance the books coming in at an astounding 2.073 million barrels a day or 14.511 million barrels. Last week the adjustment was an equaling puzzling 13.8 million barrels adjustment. These adjustments are way out of whack with historical norms and the EIA has said that typically the adjustment is less than 2% of refinery crude oil inputs. Last week crude inputs were at 15 million barrels so last week’s adjustment is closer to a 14.5% precent adjustment. Regardless, the EIA tells us that based off of that adjustment, U.S. commercial crude oil inventories are about 9% above the five-year average for this time of year. Just do not look at the SPR man behind the curtain. SPR Barrels are still 210.8 million barrels below a year ago.

The EIA also reported a surprise increase in distillate fuels which caused a big sell-off in ultra-low sulfur diesel futures before a late day incredible come back. Why the comeback? Perhaps because despite the fact that distillate fuel inventories increased by 2.7 million barrels last week, they are still 12% below the five year average for this time of year. That is not a comfortable place to be and as John Kemp of Reuters points out is a major problem.

Kemp writes that, “Global inventories of diesel and other distillate fuel oils are exceptionally low – meaning prices will surge higher again quickly if the economy avoids a recession in 2023. Inventories have risen modestly from troughs in October and November 2022 as a result of increased exports from China and the worldwide slowdown in manufacturing and freight transport. But stocks in most regions are still close to multi-decade lows and would deplete quickly in the event the manufacturing and freight cycle turns up again soon.