News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

CAZFF: Caza Shares were consolidated on a 560,000,000- to-one basis, resulting in every pre-consolidation Caza Share not held by Talara Opportunities V, LP becoming a fractional share to be cancelled in exchange for a cash payment based on the number of pre-consolidation Caza Shares held. Holders of Caza Shares, other than Talara Opportunities V, LP, are entitled to receive USD $0.00481 in cash.

FINRA deleted symbol:

http://otce.finra.org/DLDeletions

Well, I know what I know and I am not afraid to ask questions about what I don't know. LOL!! Again, thanks for your perspective.

Thank you for your open nature, it may mean more to me than some realize.

The point of being a moderator, for me, is to offer something by way of perspective. I don't ever presume to know what will happen. Instead, I try to make sense out of elements that may recognize patterned behaviors affecting a particular company's stock. This is why I tried to steer you towards something more akin to what could become "your own individual investment system," as it were.

One thing is for certain:

Caza got into serious trouble due to unforeseen circumstances. However--- isn't it the responsibility of every company to protect its stock's integrity and be prepared for the worst? I think so.

It's easy to look at moves to recapitalize beleaguered companies and assume, "Hey, that's a good thing, isn't it?" The problem with it is that we don't know the terms of engagement. Caza may have sold its soul with shareholders not likely to know or comprehend the impact of terms until it is too late to back away.

I'd hate to see you lose out, thinking this is a great opportunity---on the strength of a major move on Caza's part when it may have sold its future to a company with death spiral thoughts in mind.

If anything in this missive has you befuddled, let me know. I'll help.

It is always an honor to be asked for help!

By the way---two of my aggressive picks are NGL and SDLP. They are not without risks but I like the patterns I see in each. I hold 11,000 units of NGL and 4,000 of SDLP, having added 500 to the latter. Should you be interested in either, check with me for reasonable entry points as today's prices are higher than I expect they'll be a week from now. My advice would be to jot down the prices on each trading day---and do this for awhile until you feel confident of what you might expect. NGL is extremely volatile and demonstrates it via its frequently large swings. SDLP has been beaten up something awful but many investors see huge upside. Me too!

Len

I will defer to your better informed judgment and hold off and watch how this plays out. That will cost me nothing. LOL!!

Thanks for you opinion. As I said, oil is not something I know a whole lot about. After reading your profile, I respect your knowledge about the oil industry.

Thanks for taking the time to give me a heads up.

In my opinion it would be irresponsible to invest in CAZFF given the lack of info surrounding Talara. The PR points to the expectation of significant dilution but it's really the lack of clarity that makes this a sucker bet for the foolish. Solid investment must be founded on real attributes, not merely super cheap shares that will probably go nowhere good.

I'm with you on SDLP, holding 3,500 units and hoping for more.

The infusion of cash to pay off creditors. About 97% of the stock is now held by the company that paid $46 million to bail them out. A couple of positives there. Seems they have oil, decent revenue to stay afloat, now that the debt is paid off and the monthly interest is not dragging them down. And as part of the deal, the former debt holder also had to relinquish all rights to some of the working wells, which should also increase revenue.

Again, those distressed oil producers that can survive this drop in oil prices might be worth buying cheap right now. IMO.

Also liking SDLP, another that you are aware of. Especially with the dividend payout, although most recently reduced, still a nice DIVI (51%).

I see too much turmoil in it. Sound investments arise from a company's discernable behaviors instilling confidence. I see none of this. What has you feeling confident?

I'm just now thinking of buying some of this. I am a neophyte when it comes to oil companies, but it seems that today's survivors will provide a nice ROI when oil bounces back.

Glad I'm out. Never looked back.

Check this out......

http://www.bloomberg.com/press-releases/2015-12-24/caza-oil-gas-announces-closing-of-us-45-5-million-equity-financing-with-talara-opportunities-v-lp-and-debt-restructuring

Looks like CAZA will be a survivor.

Agreement is in order here as I had an identical experience. I sold half several weeks ago and noticed there'd been a dance of sorts around the effective selling price---but not including my offer. I sold the balance yesterday out of disgust.

The problem isn't the company, unfortunately.

Can Caza come back? I had to sell out back on Oct. 2nd when the stock

price could not hold above the 20 and 50 day EMA's for the second time.

Now, it looks really quite dire and the volume on the US exchange is

nearly non-existant. 57,500 shares traded today. It's odd too, as

the low of the day shows .07 and that happened when I had a bid in to

buy at .1175 and didn't get the fill - yet somehow the price dropped

to .07 then mysteriously was at .1195 just moments later.

With that kind of action - I decided to pull my bid.

Seems like it is being totally manipulated and doesn't appear to be on

the up and up at all.

http://www.cazapetro.com/index.php?id=74&url=http://feeds.mwnewsroom.com/article/rss?id=1877942

I'm posting the fully realized drilling update (above link)below for your convenience:

Caza Oil & Gas Announces Results of Initial Well at Broadcaster

HOUSTON, TEXAS--(Marketwired - Sept. 18, 2014) - Caza Oil & Gas, Inc. ("Caza" or the "Company") (TSX:CAZ)(AIM:CAZA) is pleased to announce an excellent result on the initial Broadcaster well and provide a drilling update on wells at Lennox and Marathon Road. Lennox is a Company operated property, and Broadcaster and Marathon Road are non-operated properties.

Broadcaster Property, Lea County, New Mexico: The Broadcaster 29 Fed #3H horizontal 3rd Bone Spring well (the "29-3H well") reached the intended total measured depth of approximately 15,818 feet in the targeted 3rd Bone Spring Sand interval and was subsequently fracture stimulated in 40 stages beginning on September 7, 2014. Under controlled flowback the producing rates are steadily increasing, and the well produced at a 24 hour gross rate of 2,621 barrels (bbls) of oil equivalent, which is comprised of 2,062 bbls of oil and 3.36 million cubic feet of natural gas, on September 16, 2014. The well was producing on a 46/64ths adjustable choke at 1,850 pounds per square inch flowing casing pressure. This is a very strong well, and the Company anticipates a higher peak rate to be achieved in the coming days. Once a peak rate is achieved, the market will be updated accordingly. Facilities are already in place on the property, and both oil and natural gas are flowing to sales. Caza currently has a 25% working interest (approximate 17.63% net revenue interest) in the Broadcaster 29-3H well and the Broadcaster Property.

The Broadcaster Property is a 320 acre tract adjacent to the Company's West Copperline Property, which also comprises 320 acres. In addition to the producing 3rd Bone Spring pay interval, log data from the 29-3H well indicates the presence of oil and natural gas across the same potential pay intervals present at West Copperline, which include: the Brushy Canyon, Avalon Shale and 1st and 2nd Bone Spring Sand intervals. This is favorable for future development across the property. Management believes the deeper Wolfcamp formation on the property is also prospective for oil and natural gas.

Lennox Property, Lea County, New Mexico: The Lennox 32 State Unit #4H horizontal Bone Spring well (the "32-4H well") is currently drilling ahead at approximately 15,289 feet measured depth to an intended total measured depth ("TMD") of approximately 15,740 feet. The Company anticipates reaching TMD today and has scheduled the fracture stimulation for October 6, 2014. Caza currently has a 50.00% working interest (approximate 38.98% net revenue interest) in the 32-4H well and the Lennox Property.

Marathon Road/Lynch Property, Lea County, New Mexico: The operator has moved the rig onto the location and is preparing to commence drilling operations on the Marathon Road 15 OB Fed #1H horizontal Bone Spring well. This well is a direct offset to the very successful Marathon Road 15 PA Fed #1H horizontal Bone Spring well, which had an initial 30 day average of 1,974 Boe/d gross, consisting of 1,721 bbls of oil and 1.52 MMcf of natural gas. Caza currently has a 14.7% working interest (approximate 12.5% net revenue interest) in these wells and the Marathon Road Property.

W. Michael Ford, Chief Executive Officer commented:

"This is an exceptional result at Broadcaster, and we are pleased to report the news to our shareholders. As stated previously, frac technologies continue to improve in the Bone Spring Play without a material increase in cost. When using these technologies to tailor fracs for specific reservoir characteristics, as in this case, the results can be impressive.

We are on schedule and close to reaching total measured depth on the Lennox well and look forward to reporting the results of the scheduled frac in October.

The Company's next operated well is currently the Gramma Ridge 27 State #4H horizontal Bone Spring development well, which should commence in October. We are also pleased to see operations have commenced on the second Marathon Road well and anticipate operations to commence on the next Broadcaster well in late Q4 2014."

Ordinarily I'd be inclined to agree with you but not this time. If we take a look at why oil is dropping, we can come up with a number of explanations. But I'm noticing a couple of other things.

The crack spread defines the range of opportunity available to processors. Refiners, in particular, are caught in the crossfire when the crack spread drops precipitously as has been the case for more than a year running. On top of this we've been hearing of government led moves to relax certain rules that would surely affect a refiner's bottom line. However, I've yet to see anything definitive along this line. That said, I'm not seeing renewed interest in the refining end. And without that particular catalyst, I think the trend will not suddenly become our friend.

What this means to me is that certain things must turn around if we're to find domestic oil exploration, lifting, gathering, processing and marketing behaving as though meaningfully incentivized. I'm not seeing a case for trying to explain Caza's share price drop when we know that oil is dropping. And we also know that this situation is hardly the exception in the o & g arena.

In short, CAZFF represents an extraordinary opportunity for us at this moment in time because it is so very capable of unusually great operational results. On top of that, it's suffering along with others caught in the downdraft produced by ongoing tax-related issues affecting the refining side. There will be repercussions whenever the refiners are challenged. In no way does this reflect on Caza other than to acknowledge that the road to riches is often fraught with debris amassing from unrelated wars. The wise investor looks past this, grabs a beer and a hotdog and burps while waiting for the air to clear.

As to price weakness, isn't there some sort of overhead supply. Seems that the SA Advisory mentioned a financing that involved them selling stock. I also look for a simple answer and oil down $10+ in past month or so hasn't helped one bit.

T

M&M's make for great candies but they don't speak to me when it comes to my managing my finances. Many investors prefer to fix blame for disappointment on the actions of others. I don't see conspirators in the wings of this theater. Instead, I recognize that stocks are "realized futures." By that I mean that stocks represent accumulated results of businesses plying their trades in view of the public. And that public is willing to pay the entrance fee so as to participate in the offering.

Caza goes up today, drops tomorrow. So? Is this anything new? Daily I'm witness to gyrations both large and small in my twenty or so holdings. An alarmingly contrasting price point has me looking for news explaining the abrupt change. Absent anything newsworthy, I realize that there will be no simple explanation forthcoming, not yet, anyhow. It begs the question: Am I a victim of the process or of myself?

Each of us does as he/she is commanded by personal style and background experiences. Yet we also reflect patterned behaviors, some of which occasionally cry for change in implementation. Today, by way of an example, I asked my realtor if I'm being an jerk by holding out for a better price on the property I want. This is an important question we all might ask of ourselves as it may bring us to a more sophisticated stage of development as traders. Sometimes we repeat patterns not necessarily in our best interest. Inviting opinion from others can help immensely.

As for filling the gap? I think we tend to expect patterns to repeat yet it's often the non-repeating event that becomes the best winner. It is not written anywhere that gaps must fill! This is a figment in a person's imagination in a quest to feel in control of an investment program without hard & fast rules.

Something to think about, maybe?

MY CONCERN after watching the MM's manipulate the price of this stock the

past few weeks. Looking at the opening pricing, I believe that the

MM's could manipulate this all the way back down to fill the gap at

.2091

WE NEED SOME BUYERS !!

BTW, Had that order in for MOST OF THE DAY

and .294 was NEVER FILLED - That's promising.

I'm tired of the SLIDE here. I will keep

buying !!

I think it is because the volume is low and there are a few MM's who

are just playing with the EMA's. I just put in an order to test this

theory. I put my buy order in just above the bid.

1,000 shares for .294 - and no more playing around has happened since.

EDIT UPDATE:

We'll see. Now there are 3 bids above me.

I think I am on to something !!

EDIT UPDATE AGAIN:

Those 3 bids were filled, mine has not been

filled but not showing up on Level II. But

it appears they don't put on Level II unless

minimum of 2500 shares.

Here we are on Monday, the start of a new and fresh week. The overall market is strongly higher with the DOW up 153 yet we of Cazaland are down. How can it be?

Well, it certainly couldn't have been due to disappointment over production numbers just recently released as they were breathtakingly spectacular. So, then, what can it be?

I submit the greatest deterrent lies in our stock trading out of AIM and not our home-grown NASD or NYS. I think it's just a matter of time before this is "repaired" and we get to participate in a dual listing. It's very costly to bring about but if the company wants to bring in megabucks for expansion purposes, it is the way to go. It is one way to guarantee easy and ready access to information the serious investor will need before plunking down a considerable cash outlay.

Meanwhile, I added a few shares this morning as I'm convinced it will prove to be money in the bank, as they say. Now holding 35,000 shares and will likely continue adding on the cheap as opportunities arise.

Good luck to all!

Thanks for your guidance. This is to be a project for me this weekend and I'm looking forward to seeing it from the inside.

Thanks, too, for bringing up agora.com as it might offer something I've not been finding.

And thanks to you for even asking. You might be surprised to find that many investors hold back from asking. No, I take that back---unless you were in the brokerage business strictly on the wholesale side, you'd know as well as anybody that the tendency is to hide truths, especially on the retail side of things. Anyhow, I'm constantly learning, challenged by the challenges affecting others. It pushes me to rethink anew---sort of like trying to develop a play within a play where the surface plot is anything but the ruling force within.

Moderating on the CVR Refining board, I was asked this week about how to handle events (fire and multiple injuries affecting four employees). Investors weren't factoring in the one month shutdown for more than 20% reduction in throughput announced via CEO guidance---all this to occupy a full third of Q3's (forward) production. Further complicating things is the steady rise in unit value IMMEDIATELY following going ex-dividend a few days ago.

Is it crazy? Of course it is. I suggested board participants weigh the above items and ask themselves what might keep them committed cash-wise, given that cash flow will be necessarily impacted hugely. One would think that businesses do not operate solely for the sake of altruism without a thought as to the bottom line.

After I made my concluding remarks at the board, I had to admit to myself and later to them that I was a fool to ignore what I knew to be true---and I promptly sold the balance of my positions.

This gets more interesting in light of the fact that units have risen at all, in light of the devastation visited upon the company. It looks to me like there's an artificial support system in place that is buoying things in the absence of sound business fundamentals. This morning I awakened to the thought that Carl Icahn very likely has something to do with this. And at some point a plug will be yanked and many will drown in pain.

All this to say that opportunities to guide another seem to enrich us all in the end. When explaining the 3 P's, I always wonder what path to take for it can be explained in different ways. So I try to become my own student for that moment and look for the simplest, most focused way to present something to an audience not necessarily versed in the subject. The better I get at this, the wiser I become in my own dealings.

We're fortunate to have you here as a participant. Something I'm hoping will become the topic of the moment at some point has to do with recognizing market activity as a feeding ground spawning foraging on the part of investors. Frenzied moments ensue when feasts and famines surface. For now, I'll say I'm loving the fact that we have another resident professional knowledgeable in some of the ways of the stock market. Others have made their way towards center stage and this makes all of us richer for the shared experience.

Will look at Falcon and get back to you. At first glance I'm disturbed by the crazy low volume. But the "F" tag following the symbol (for those new to this) indicates that the company is domiciled out of this country. Notwithstanding, the tag also means that we can trade the stock easily. The pink status is for trading convenience and does not suggest this could be a sleaze outfit at all. I should emphasize that the pink designation enables us to place our trades through electronic means allowing us to enjoy discounted trading fees. However--- we are not seeing the whole trading picture with respect to volume.

The primary depiction of trading volume is in Ireland.

If you have the time, take a look at HENC. These two companies embody a few items of commonality. Hmmmmmmm.......

I'm enjoying this!

Disclaimer: I have no position in HENC.

jugs, thanks for lesson one. I am a little versed in the 3 P's from having invested in Falcon Oil and Gas past 6-8 years. Marc Bruner of Ultra Petroleum fame started FOLGF and has subsequently retired. But when I first got involved they were talking about the huge reserves at the Mako Trough in Hungary. They have yet to bring anything out of the ground, but have a JV in place which looks promising. They also have millions of acres in the Beetaloo in Australia where they just signed(should be finalized any day now)a JV with two large companies. And, they have a very nicely located spread in South Africa, next to Chevron, I believe. So the potential is there, but it is a matter of getting it out of the ground. My mistake was getting involved before any actual production. It popped just after I bought in because of a JV with Exxon in Hungary but went way down after they failed to get any worthwhile results and pulled out. If you have the time, take a look and see what you think. It may be at a point where investing now would make sense. Thanks for taking time to educate us on energy investing. Have a good weekend all.

T

So this is your first foray into O & G? That's exciting to me for there is so much about energy trading if only for the incredible possibilities that might turn up at any time.

Let's tackle something you bring up as it relates directly to not only this particular company but actually any company drilling for hydrocarbons. The subject is the three P's:

In oilfield parlance we assign prospectivity values to three stages of presumed value. Thus we recognize each by awarding a name or title representing what one could logically expect to uncover, assuming drilling in that particular area or zone.

When assigning such names or identifiers, we make use of seismic for starters. Previous drilling in that specific area or adjacent areas can be extremely illuminating. Core samples tell us a great deal about soil conditions as well as the presence of material suggestive of the presence of hydrocarbons, be they in place now or formerly so as in the case of oil migration. Much of this will become clearer as we move forward, below.

The Three P's:

POSSIBLE

This is how we may view an area thought to hold oil, gas or both, based on a number of possibilities but lacking concrete evidence. This is where the dreamers among us find ourselves trapped in often pie-eyed wishful thinking. I, personally, refuse to even consider buying shares in a company whose leased lands have been assigned the single P value. I'm too old for that level of risk as such hydrocarbon systems will often take many years before there can be a meaningful start towards development. Add in the three to five years typical to bring found oil to market and even then---where's the infrastructure to support it?---and you get the idea. Worst of all is the lack of proof supporting even the mere possibility of oil in place.

PROBABLE

Here is where things can get dicey. Say you've got a lease with a few working wells. You pick up an adjoining lease, assuming this lease will compare favorably with the other one. But it may not be the case. A hydrocarbon basin may hold millions of barrels of oil but knowing where to sink the drill bit is crucial. There are up-dip situations indicating there was oil at some point but if it's "migrated" because there were no "seals" containing dome-like structures to prevent the outflow, then you're out of luck and also oil.

Seismic will usually help define the level of probability of there being discoverable oil in place (OIP) but without 3-D seismic and extensive work performed by very highly trained petroleum engineers, all bets are off. And even if not, there's the question of prospectivity as in:

Assuming there's oil, will it be enough to assure us of the commercial viability BEFORE drilling? After all, we're talking about million of dollars here, whether onshore or offshore. Still, many companies will take the gamble in the belief they are more talented, luckier or patient.

PROVED

Proved reserves are held to be the most desirable yet I know from firsthand experience that even these reserves can fall through the cracks. Seismic, both 2-D and 3-D, can illustrate where oil should be. 2-D refers to two dimensions as in length and width. 3-D provides that most desirable third dimension---depth.

Again, only the drill bit will truly prove the presence of what we'reseeking. Core samples will bring up mud from well beneath the earth's surface and this will feel oily, smell oily and probably taste about as bad as last week's fish fry. But even the sharpest geophysicists will happen upon subtle differences contrasting from their prior experiences. As a result, they may fail to accurately predict the future. I've never met a dumb geophysicist, rest assured. But life is full of anomalies. When we're focused on substance usable only after lifting it out of the ground, we're dealing with nature, birthing place of the very seeds of nature that spawned us and all that comes of us.

The study of oil in place can be incredibly tantalizing.

For those who care to understand more about this, let me refer you to Robert Bearnth. Google should have some good stuff. Also, Neil Moore. /six years ago, Bob was honored as the world's leading geophysicist, credited with no less than six major discoveries. Neil, his partner and long time friend, is the electrical engineer who first figured out how to conduct seismic research from the back end of a boat, trolling through waters with "geophones" attached to an array of wire lines. He used as many as twelve of these instruments, recording responses electronically, arising from exploding tiny charges well beneath the sea. By interpreting differences in pitch and times of decay, it was possible to determine the nature of and viscosity of material thought to be oil.

My really great fortune was to have had these two giants as my personal friends and teachers. They'd been reading my energy-related articles in blogs for years and hired me to run their company's investor relations department. I've never known better, more upstanding, outstanding and honest men than these two, now departed.

This is a lot to digest, I know. And it will likely lead to many questions. That's fine with me so long as it helps someone here to possibly find an interesting and profitable place on which to hang a hat. I know I have been extremely fortunate.

Final point: Where does this attach meaningfully to Caza Oil?

jugs, iilhabela, et.al., just for full disclosure, while I was a stockbroker for 20 years, never had I purchased an O&G, nor gold/silver company in that time. In past couple years I am making up for that lack of exposure. I may have mentioned in a past post that I found Caza from a free newsletter, SAAdvisory.com. The guy there is very astute when it comes to O&G plays. That led me here and now I am excited about LNREF. I have owned ZPTAF since the high $2's thanks to SA Advisory, along with MAUXF. I am still trying to figure out how to value oil plays what with cash flow EBITDA, EPS, market cap and different P values for oil in ground, etc. Very confusing. Thus I try to get around to different boards and gleam what I can. I am thankful for you guys sharing your ideas and methodology for valuations. The stockhouse board has some good posters also. Forgot to mention FOLGF and PTAXF. Look forward to more analysis on results from those of you who have been around the block a couple times. Still don't know what multiples to put on cash flow and EBITDA.

T

Your apology will not be accepted here! You're doing great, really.

There's a point or two I would make regarding debt and/or debt financing/refinancing:

The company expects shortly to be self-sustaining. What this comes down to is that through internal operations we may/might expect that soon, capital expenditures will be financed internally(read that: cash flow positive sufficient to carry the company towards profitability without further borrowing, dilution or debt management issues).

When I look over a company's quarterly or annual numbers, the first thing I need to find out is the directional bias evident in its production revelations. There is ALWAYS a bias in evidence, hidden or deliberately exposed. I need to see yoy (year over year) improvement and nothing less. Comparing Q1 of 2013 with Q1 of 2014 is part of it. Seeing reduced debt obligations is surely part of it. But for me, it's all about a diminishing stream of fresh debt being contrasted by increasing cash flow which, once free of historical encumbrances, should become profitable. Strictly on a net-back basis, we're talking about positive cash flow.

Next, I look at bottom line expansion. How much new acreage has been added? What is the nature of associated prospectivity? What is the status of completed seismic? 2-D? 3-D? Infrastructure available to manage new production hoped to come on line?

There's much more but I needn't clog the airways here as I know others have much to say. One thing is for sure: The results so far are truly outstanding, imo. I doubt it will be long before our shares receive the respect due.

We're listening, so speak up, folks!

Just woke up here. I have glanced over the numbers. It appears to me

that Caza is hitting every proposed figure that they have placed forward

and that they are following their business model to extract the most

production that they can. And, they continue to plan ahead.

Now after I wake up. I need to see what the debt is. From a previous

NR they had paid ahead to Yorkville but I am not sure how much more debt they hold: On July 21, 2014, the Company announced that it had voluntarily prepaid all amounts owing under its $4.3 million convertible unsecured loan (the "Loan") made available by YA Global Master SPV Ltd., an investment fund managed by Yorkville Advisors LLC ("Yorkville"). The prepayment amount of $1,676,777 terminated the Loan between the Company and Yorkville.

Anyhow, I am still new to the company and haven't ventured too deeply in all of the financials - MY BAD.

Huge! Looks like Mike Ford has really got the company going in the right direction!!!

Thank you for telling us how you respond. I hope others chime in as well. This is how we can build important perspectives with respect to this particular company and its stock.

What, in particular, impresses you? There are clues on the surface and beneath, as well. Sharing some of these personalized reactions can be beneficial to us all.

Looking forward to hearing more from you!

Wow. Fantastic results.

Our quarterly numbers are out. There is much to take in so, rather than invite disarray, I'm posting numbers from the production side. As others here contribute, the overall picture will change, providing a broader view from which we can glean value. I'm looking forward to an enriching discussion.

******************************************************

Press Release: Caza Oil & Gas Announces Second Quarter Results and Provides Operational Update

Caza Oil & Gas Announces Second Quarter Results and Provides Operational Update

HOUSTON, TEXAS--(Marketwired - Aug. 14, 2014) - Caza Oil & Gas, Inc. ("Caza" or the "Company") (TSX:CAZ)(AIM:CAZA) is pleased to provide its unaudited financial and operational results for the three-months ended June 30, 2014.

Unaudited Second Quarter Financial Results

-- Caza's revenues from oil and natural gas sales increased 489% to

US$6,286,049 for the three-month period ended June 30, 2014, from

US$1,067,991 for the comparative period in 2013. This also represents a

quarter-on-quarter increase of 37% compared to US$4,591,507 in Q1 2014.

-- Adjusted EBITDA increased to US$3,269,495 for the three-month period

ended June 30, 2014, as compared to an adjusted EBITDA loss of

(US$824,891) for the comparative period in 2013. This also represents a

quarter-on-quarter increase of 65% compared to US$2,139,210 in Q1 2014.

-- Caza's oil and natural gas liquids (NGL) production increased 495% to

65,823 bbls for the three-month period ended June 30, 2014, from 11,059

bbls for the comparative period in 2013. This was also an increase of 47%

from 44,724 bbls in Q1 2014.

-- The Company's oil and NGL production has increased to 78% of the

Company's combined oil and natural gas production in Q2 2014 from 54% in

Q2 2013.

-- Caza's natural gas production increased 100% to 111,016 Mcf for the

three-month period ended June 30, 2014, from 55,626 Mcf for the

comparative period in 2013.

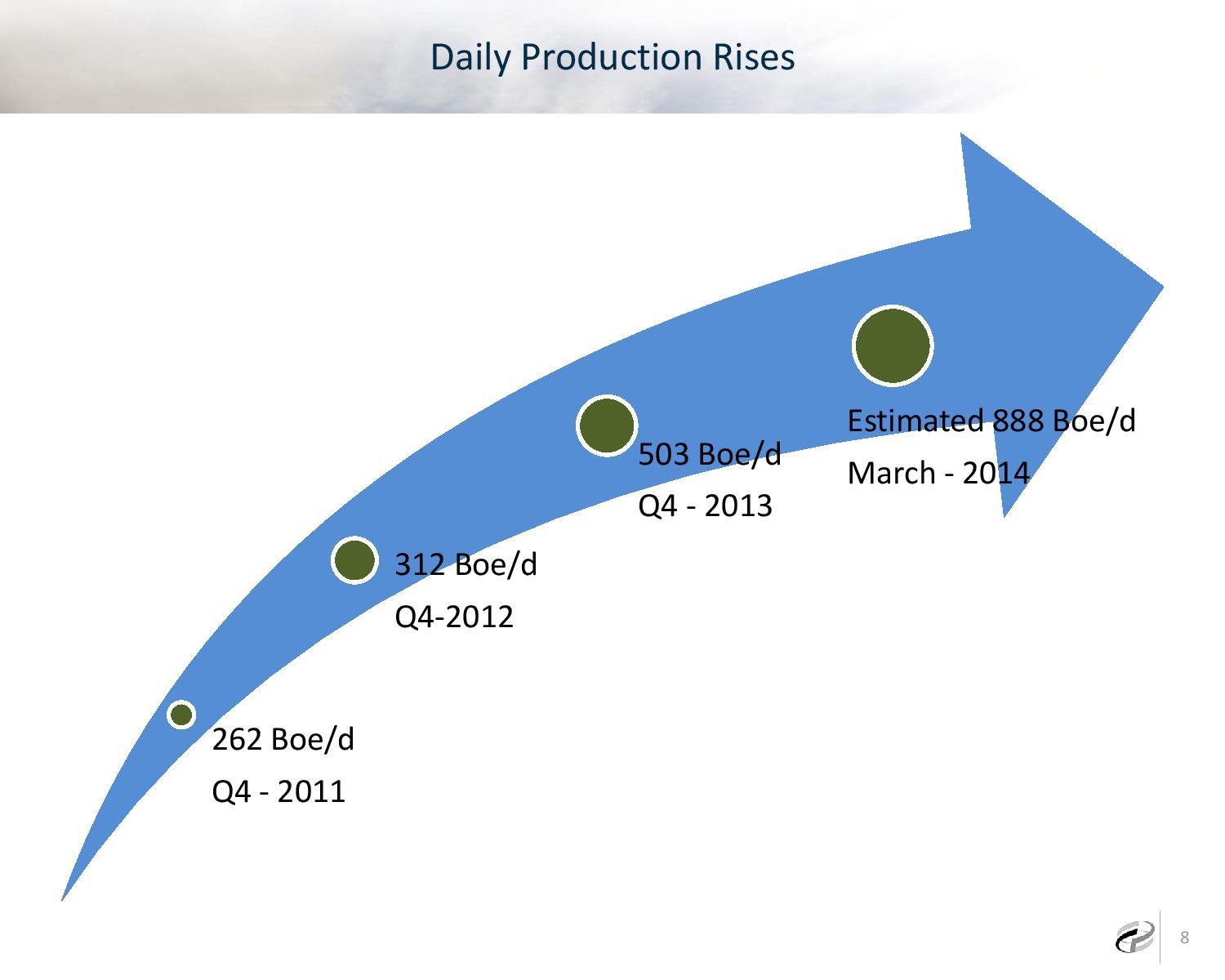

-- Average net production volumes increased 320% to 937 Boe/d for the

three-month period ended June 30, 2014, from 223 Boe/d for the

comparative period in 2013, and have since increased to an average of

1,315 Boe/d during the month of July 2014. The Company's net aggregate

production for the month of July was 40,776 Boe, which is currently ahead

of the Company's forecast.

Taking a brief look at your other two picks, I see something I like in each. Our focus here is a bit lighter than will customarily be found on boards devoted to specific stocks, so while it might not be best for all readers and contributors, I think we can at least pay lip service to stocks other than Caza.

As of tonight I am a moderator for this board. It is an honor to contribute anything I can. I know we're all here to profit from a market fraught with changing metrics yet we are probably driven by certain items we have in common with others. A few of these might be of interest here:

1. Industry cannot move forward without energy. Banking difficulties may be as sand thrown into a motor's gas tank but energy drives everything.

2. Energy is one of the most highly manipulated industries because of the above. This makes it more difficult to establish a mentally meaningful baseline from which to operate when trading.

3. Unquestionably, there is money to be made by trading energy. To do this effectively, we need to recognize the impact of seasonality on any energy company in which we invest. Seasonal changes force cyclicality issues to take front seats when analyzing such stocks.

4. Best of breed isn't a phrase we hear in stock parlance when examining energy companies engaged in oil and gas exploration yet it fits surprisingly well. CAZFF is definitely one of those I'd label best of breed for a number of reasons. Rather than delve into these now, I'll say simply that this is the stuff of analysis that could serve all of us on this board. Through our shared analysis we stand to grow in competence and character.

I salute all contributors here!

Jugs, thanks for update. I was just looking at chart and see what you mean.

T

Thanks again Len !

I have been adding shares slowly but surely. Actually got some more today after selling some of my shares I have in another small OTC PTRC. I only sold about 20% of what I had there after a decent profit...while the rest ride.

I am not in the position to invest too much at the moment.

I have my money in these 3:

CAZFF

LBSR

PTRC

And will add to each of them a little at a time with each paycheck.

I remain hopeful on all fronts.

Thanks again,

Greg

Thank you for your kind words. However, I should have added something by way of a caveat earlier:

CVR Refining (CVRR) will likely drop considerably from today's opening price because of a fire announced last week. It occurred around the day after the stock went ex-dividend so it wouldn't affect Q2 but will most definitely do so when it becomes time for the Q3 payout. As a consequence, I sold off my position entirely today.

Reflecting on it more carefully to be of help to you and any interested others, I realized how short-sighted I'd been. After all, there are huge expenses usually accompanying refinery fires and/or explosions. And in this instance there were four injuries as well. This is really frightening stuff in my mind and it will take money to resolve---lots of it.

Most likely I'll restore the position when positive guidance comes out from the General Partner. Meanwhile, I figure it's just a matter of time before units tank, possibly into the $21 range, well down from the $25+ just days ago. Understood, of course, units are currently represented with the 96 cent distribution removed as per SEC mandate. It makes little sense to place value on a stock equal to that of a week earlier after stating that its production will be seriously impacted by a fire and injuries going forward.

Bottom line: I believe it would be a silly mistake to start a position in CVRR at this time.

Very good post. Thanks for info and a couple of ideas to look into. Very much appreciated.

T

We're right in the middle of the year's slowest months when it comes to prizing oil-related fuels. Globally speaking, February is held to be the most difficult of all, when coldest temperature extremes are most likely happenstance and snow/ice storms are commonplace. In addition to this, there's plenty of storage already in place with significant lead time prior to any perceived need to revise utilization schedules.

Long story short: We are in the yearly slump time right now. Things will show signs of perking up around the middle of next month when energy traders scramble to lock up hedging contracts several months ahead of expected seasonal shifts in available supply.

Every year I scout for opportunities to make use of the above. This week I've been considering adding more shares but feel 33,000 shares should be enough.

You might look at another stock in the same business: Lonestar Energy LNREF. It's generally thought to spread out risks although both CAZFF & LNREF tend to move in parallel motion for the most part. Today, for example, both are higher whereas previously, both moved seemingly in lockstep.....down-wise, of course.

There are many of us energy-oriented investors enjoying regular income from MLPs such as NTI and CVRR. These trust-like structures cost more up front but fill a need for those in search of income. The point here is that there are numerous ways in which to make use of seasonal affectation. Hi-yield income producers present one.

Let me know how you make out if you decide to explore this.

Indicator's are bottomed out, but I am somewhat baffled at the lack of

buying at these levels. Anyone else out there have any answers on the

stagnant buying pressure and or selling pressure ?

The chart is looking ugly - but it is totally bottomed out on the

Stoch's and MACD - I'm buying more RIGHT NOW !

Not sure when the pps will reflect the true value - but going in for

more now.

It's great they've had success, but when will the pps start to reflect the progress? Any upcoming catalysts?

Very smart indeed!

I keep buying more each paycheck. WAYYYY Undervalued at the moment.

"CAZ has had 17 successful wells in a row."

Me too! The stock is in a funk at the moment but this is how things go at this time of year. Winter is well behind us but the energy market tends to gear up at least three months before the new wintery season is upon us. It's about the crush brought on by threats of unmanageable cold weather conditions. Thus, Middle to late August tends to perform as lead month and starts showing more aggressive personality when it comes to E & P's. That said, my bet is that CAZFF will be in fine fettle come November. I won't be selling shares any time soon.

This may explain what is going on here as it appears to be the most complete presentation I've found thus far. While it points specifically to Caza, it may be prudent to consider that another E&P in a similar area is also doing dramatically well---Lonestar Oil and Gas (LNREF).

I'm the moderator for this particular stock message board (LNREF). As such, I wish to alert potential investors to charges added to stock purchases that remain above and beyond the usual commissions charged. These are fees forced on brokerages and labeled transaction fees. Ostensibly these are transfer agent fees. However, I'm not happy with that explanation as there's wide variance in the amounts levied for such fees. Please visit the board before finding yourself mercilessly charged unexpectedly.

Back to CAZFF:

Headline & BriefHeadlines Only

.

Caza Oil & Gas Announces Excellent Well Result and Provides Operational Update

2:01a ET July 21, 2014 (Market Wire) Print

Caza Oil & Gas, Inc. ("Caza" or the "Company") (TSX: CAZ)(AIM: CAZA) is pleased to announce another excellent result for the second 3rd Bone Spring well drilled on its West Copperline Property, and to provide an update on drilling activities at Gramma Ridge and Broadcaster (West Copperline) properties, all of which are located in Lea County, New Mexico.

West Copperline Property: The West Copperline 29 Fed #4H horizontal Bone Spring development well (the "4H well") reached the intended total measured depth of approximately 16,015 feet in the 3rd Bone Spring Sand interval and was subsequently fracture stimulated beginning on July 1, 2014. Under controlled flowback the producing rates have remained steady, and the well produced at a peak 24 hour gross rate of 1,598 barrels (bbls) of oil equivalent, which consists of 1,220 bbls of oil and 2.27 million cubic feet of natural gas on July 16, 2014. The well continues to clean up and is producing on a 24/64ths adjustable choke at 2,650 pounds per square inch flowing tubing pressure. Facilities are already in place for the sale of oil and natural gas on the property.

Caza is now producing four wells on this property on two contiguous 160 acre tracts comprising the west half of Section 29. The West Copperline 29 Fed #1H and #2H wells are producing from the 2nd Bone Spring Sand, and the West Copperline 29 Fed #3H and #4H wells are producing from the 3rd Bone Spring Sand. All four are very strong wells and demonstrate the significant upside provided by stacked pay sands in the Bone Spring Play. There are still two remaining 160 acre tracts to be developed at West Copperline in the east half of Section 29. The wells on the east half will be operated by a third party and called the Broadcaster wells.

Notwithstanding production from the 2nd and 3rd Bone Spring Sand intervals in the West Copperline wells, log and core data were also obtained across the Brushy Canyon, Avalon and 1st Bone Spring Sand intervals in these wells. The data indicates the presence of oil and natural gas across each of these intervals, which is favorable for future development on the property, including the non-operated Broadcaster wells in the east half of the section. Management believes the deeper Wolfcamp formation on the property is also prospective for oil and natural gas.

Caza currently has a 62.5% working interest (approximate 47.69% net revenue interest) in the West Copperline wells.

Broadcaster Property (West Copperline non-operated): The Broadcaster 29 Fed #3H horizontal 3rd Bone Spring development well, is currently drilling ahead in the vertical section at approximately 10,800 feet. The operator is preparing to begin drilling the lateral section to a total measured depth of approximately 15,824 feet in the 3rd Bone Spring Sand interval. This well is a direct offset to the Company's operated West Copperline Fed 29 #1H and #3H wells, which have each delivered very strong results.

Caza currently has a 25% working interest (17.63% Net Revenue Interest) in the Broadcaster Fed 29 #3H well and in the east half of Section 29 containing approximately 320 acres.

Gramma Ridge Property: The Gramma Ridge 27 State #2H horizontal Bone Spring test well (the "27-2H well") reached the intended total measured depth of approximately 14,650 feet in the 2nd Bone Spring Sand interval on July 12, 2014. The 27-2H well reached total measured depth six days ahead of schedule and is scheduled to be fracture stimulated beginning on July 27, 2014. This well is a direct offset to the Company's highly successful Gramma Ridge 27 State #1H well (the "27-1H well"), which is currently producing from the 3rd Bone Spring Sand. Encouraging results from log and core data obtained from the 2nd Bone Spring Sand interval in the 27-1H well were determining factors in the decision to drill and test the 2nd Bone Spring Sand in the 27-2H well, which also exhibited favorable results from log and core data obtained across the 2nd Bone Spring Sand interval.

Caza currently has a 52.5% working interest (approximate 40.82% net revenue interest) in the Gramma Ridge 27 #1H and 27 #2H wells.

W. Michael Ford, Chief Executive Officer commented:

"This is another excellent result at West Copperline and continues the Company's success in the Bone Spring Play. As we drill additional wells in the play, we continue to refine our operations. This has resulted in efficiencies that have allowed us to drill wells faster and cheaper, which improves the economics of each well. We have also begun to tailor our fracs to fit specific reservoir characteristics with improved results. These subtle changes continue to increase our success and cost efficiency in the play, which creates additional value for the Company and our shareholders.

We're also happy to have reached total measured depth on the operated Gramma Ridge 27-2H well ahead of schedule and to be participating in the first Broadcaster development well offsetting Caza's West Copperline wells. We look forward to updating the market in the coming weeks once these wells have been completed."

Headline & BriefHeadlines Only

.

Caza Oil & Gas Announces Excellent Well Result and Provides Operational Update

2:01a ET July 21, 2014 (Market Wire) Print

Caza Oil & Gas, Inc. ("Caza" or the "Company") (TSX: CAZ)(AIM: CAZA) is pleased to announce another excellent result for the second 3rd Bone Spring well drilled on its West Copperline Property, and to provide an update on drilling activities at Gramma Ridge and Broadcaster (West Copperline) properties, all of which are located in Lea County, New Mexico.

West Copperline Property: The West Copperline 29 Fed #4H horizontal Bone Spring development well (the "4H well") reached the intended total measured depth of approximately 16,015 feet in the 3rd Bone Spring Sand interval and was subsequently fracture stimulated beginning on July 1, 2014. Under controlled flowback the producing rates have remained steady, and the well produced at a peak 24 hour gross rate of 1,598 barrels (bbls) of oil equivalent, which consists of 1,220 bbls of oil and 2.27 million cubic feet of natural gas on July 16, 2014. The well continues to clean up and is producing on a 24/64ths adjustable choke at 2,650 pounds per square inch flowing tubing pressure. Facilities are already in place for the sale of oil and natural gas on the property.

Caza is now producing four wells on this property on two contiguous 160 acre tracts comprising the west half of Section 29. The West Copperline 29 Fed #1H and #2H wells are producing from the 2nd Bone Spring Sand, and the West Copperline 29 Fed #3H and #4H wells are producing from the 3rd Bone Spring Sand. All four are very strong wells and demonstrate the significant upside provided by stacked pay sands in the Bone Spring Play. There are still two remaining 160 acre tracts to be developed at West Copperline in the east half of Section 29. The wells on the east half will be operated by a third party and called the Broadcaster wells.

Notwithstanding production from the 2nd and 3rd Bone Spring Sand intervals in the West Copperline wells, log and core data were also obtained across the Brushy Canyon, Avalon and 1st Bone Spring Sand intervals in these wells. The data indicates the presence of oil and natural gas across each of these intervals, which is favorable for future development on the property, including the non-operated Broadcaster wells in the east half of the section. Management believes the deeper Wolfcamp formation on the property is also prospective for oil and natural gas.

Caza currently has a 62.5% working interest (approximate 47.69% net revenue interest) in the West Copperline wells.

Broadcaster Property (West Copperline non-operated): The Broadcaster 29 Fed #3H horizontal 3rd Bone Spring development well, is currently drilling ahead in the vertical section at approximately 10,800 feet. The operator is preparing to begin drilling the lateral section to a total measured depth of approximately 15,824 feet in the 3rd Bone Spring Sand interval. This well is a direct offset to the Company's operated West Copperline Fed 29 #1H and #3H wells, which have each delivered very strong results.

Caza currently has a 25% working interest (17.63% Net Revenue Interest) in the Broadcaster Fed 29 #3H well and in the east half of Section 29 containing approximately 320 acres.

Gramma Ridge Property: The Gramma Ridge 27 State #2H horizontal Bone Spring test well (the "27-2H well") reached the intended total measured depth of approximately 14,650 feet in the 2nd Bone Spring Sand interval on July 12, 2014. The 27-2H well reached total measured depth six days ahead of schedule and is scheduled to be fracture stimulated beginning on July 27, 2014. This well is a direct offset to the Company's highly successful Gramma Ridge 27 State #1H well (the "27-1H well"), which is currently producing from the 3rd Bone Spring Sand. Encouraging results from log and core data obtained from the 2nd Bone Spring Sand interval in the 27-1H well were determining factors in the decision to drill and test the 2nd Bone Spring Sand in the 27-2H well, which also exhibited favorable results from log and core data obtained across the 2nd Bone Spring Sand interval.

Caza currently has a 52.5% working interest (approximate 40.82% net revenue interest) in the Gramma Ridge 27 #1H and 27 #2H wells.

W. Michael Ford, Chief Executive Officer commented:

"This is another excellent result at West Copperline and continues the Company's success in the Bone Spring Play. As we drill additional wells in the play, we continue to refine our operations. This has resulted in efficiencies that have allowed us to drill wells faster and cheaper, which improves the economics of each well. We have also begun to tailor our fracs to fit specific reservoir characteristics with improved results. These subtle changes continue to increase our success and cost efficiency in the play, which creates additional value for the Company and our shareholders.

We're also happy to have reached total measured depth on the operated Gramma Ridge 27-2H well ahead of schedule and to be participating in the first Broadcaster development well offsetting Caza's West Copperline wells. We look forward to updating the market in the coming weeks once these wells have been completed."

Thank you Bypp - that is even better than the one I had found.

Much appreciated !!

Looking good, glad I am invested here.

They put out a press release actually. That's why it's up.

|

Followers

|

4

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

103

|

|

Created

|

10/14/10

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |