By the "next ASCO", the B Phase 3 will be well under way and we may even have some early results for B-OM. And then there is the P Phase 2. The current Market Cap is extremely low and does not reflect the full value of either B or K separately. So at current price levels, I don't think bad news for K at ASCO would have a significant impact on CTIX for any appreciable length of time.

Of course agree with you, with one caveat. B derisks K as everyone says, BUT K could pull down CTIX and B if it does not work. Say trial results are ultimately disappointing for K, and we hear at next ASCO

What would CTIX be worth? Despite all we hope for with Brilacidin and B OM? The share price would be something really ugly for a long time - To infinity and beyond!

Let's pretend we are in some fantasy universe in which K is a total failure in the later phase 2 trials: how does it even occur to you that it would be presented at ASCO? For one ASCO would not accept a presentation on a failed drug and two, CTIX wouldn't be dumb enough to make the submission. So that scenario is out of the equation. But let's keep going. If K has failed but B is a success CTIX is still a revolutionary biotech company and will be worth many billions. As you stated; B has single handedly derisked CTIX. So in your scenario we are still a 10x and above return from today's levels. Why would investors and big pharma pass on owning or partnering with B just because a totally different drug in the CTIX pipeline didn't work? That makes no sense at all. I don't understand the daily chiken little "sky is falling" posts, when your scenarios are not even based in reality.

Any such discussion is well down the road as at this point, Kevetrin is a near certain success for its Phase 1 Clinical Trial Primary Outcome Measure.

Secondary outcome measure are hinting positive with the company securing Orphan Drug status and planning a Phase 2/3 for Ovarian Cancer. Without Secondary indications of efficacy, this move wouldn't make sense.

So discussion of Kevetrin having a failed trial is just not a likely event at this point. Every indication is of a successful trial, with at least two to mid stage trials to follow. Once possibly an adaptive design that can morph into a Phase 3 trial.

At that later point risk returns with new trials underway, as positive results are not guaranteed. That is the possible risk of bio-tech investing. The possible reward is a successful trial leads to many-multiples of the share price.

Should any trial ever fail there is always a hit to the share price. Right now CTIX is low risk as we are a ways from that possibility, and with all the trials starting, we should have the opportunity to re-evaluate risk at higher share prices than the currently undervalued share price. Some people take their cost basis off on a double, or quadruple, then ride free shares to compensate for risk. Others hold all for a big win or a lose. To each his own. My personal opinion is it is too early to worry about trial risk and CTIX has not yet risen to a reasonable valuation, so this discussion is premature.

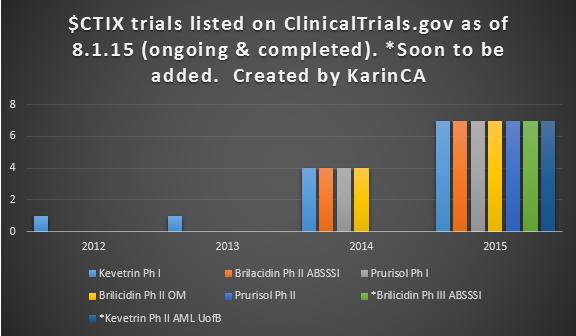

CTIX also has 3 drugs testing 4 indications, with more clinical trials planned and more drugs in the pipeline. Any one having a success brings the share price to a significantly higher valuation. So CTIX has excellent safety nets as well as excellent upside opportunity.

But of course there is always risk. There are no guaranteed emerging biotech investments that promise many multiples of profit without risk. No such thing.

But it's also important to understand biotech catalysts and risks. At the current time, CTIX has numerous catalysts and reduced risk. The only trial near wrapping up is Kevetrin, and that is a near certain success. The other trials have just started, or soon to start. So their results risk is a ways off. The real conversation currently IMO is when and if the market will wake up to CTIX's dramatic increase in clinical trials and begin a new valuation.

Say trial results are ultimately disappointing for K, and we hear at next ASCO -to infinity and beyond!

Kevetrin is a near certain Phase 1 success for the primary outcome measures. There are no disappointing results likely even possible at this point.

A Phase 1 dose escalation trial is a success in meeting its primary outcome measures. Then it's on to Phase 2 or Phase 2/3 trials, with one P2 for Leukemia (AML) already in the final start-up phase and one Phase 2/3 of Ovarian Cancer already in the planning stage. Progression to later stage trials generally means increase share price. Bingo!

So what disappointing results could we hear at ASCO next year? The answer is none. The secondary outcome measures of efficacy are not powered for statistical significance. They are more to give preliminary indications of efficacy and to guide future trials in choosing which solid tumors to focus on.

Even better, we've already have heard some positive secondary outcome measures, Ovarian cancer spleen met disappearing (complete response), stabilization of cancer and bio-markers, increase of P21 as an indication of P53 effect. Those are just tid-bits, I expect the full report to include more.

This is all good stuff, especially considering the low doses most patients have had and the infrequent dosing of this trial. With dose optimization, and PK data supporting greatly increasing the dosing frequency, that's when we start to zero in on efficacy. At Phase 2, not the current Phase 1.

So I think this concern is premature and misplaced. It is necessary to understand how these clinical trials work in terms of expectations and progression. The current Phase 1 trial looks great and the real discussion is "how great". The company is sending obvious hints with plans for a Phase 2/3 for Ovarian Cancer and attaining orphan drug status.

Once Phase 2 or Phase 2/3 is near its conclusion (or key interim evaluations if the trial design includes them), we can reasonably discuss risk of failure vs the chance of a win based upon efficacy. IMO we'll be having that discussion at a CTIX share price well above the current one.

News

News  Market Data

Market Data  Discover

Discover