News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

WHP03

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Only reason the stock is up is greed/swing trading... nothing fundamental; no improvements in ops, in sales, in strategy, in reduction of burn, leadership, notta. More power to those in the stock in this moment and who may benefit from brief swing higher. I hope they understand it's not moving on fundamentals and to not think 'this time it's different'. It's not. Take 15-25%, count your blessings, don't try and catch the top - and run like the lucky dog you are (if you manage to get anything good out of the swing up).

Approximately 10% increase to the float, if I am not mistaken. It would be less painful if their service revenue business was growing, and not shrinking. The resulting cashflow would be water for our dry garden.

Qtrly numbers were negative, to factual - down 15% Quarter over Quarter. It required another adjustment to full year guidance, $4.5-5.2MM. They'll need to better than average in Q4 (current qtr ending March 31) to reach MIDDLE of guide. Two years running they've reduced guidance and their track record for hitting their own guidance, without reducing guidance as they go, is poor to say the least.

Service revenue (the portion of their business that is reliable qtr to qtr) also declined 12%.

The last time the company said - it won't be necessary to raise capital (for two yrs) they raised in < 6 months. The company will raise money when they need. I'm glad to hear them say they're not going to raid the cookie jar until 2019, but raid it they will - over and over. Mathematically they MUST tap their $100MM ATM over and over to cover their significant monthly burn as they strive to bring their liver patch to market (2+ yrs out).

My position remains - their best chance at success is to land a well-heeled partner. I'd rather than 51% of something significant (a life saving liver patch company) then 100% of nothing - which is what's more likely if they feel compelled to go it alone in the long-run.

I am confident we as a society will indeed print body parts or parts of body parts that will benefit us as a whole. I am not confident ONVO is going to be one of the first, if they get there at all (I believe they will), but I am very confident it will cost ONVO $10s of millions of money they don't have today, and can't generate organically, to get a dollar size liver patch approved and on the market. I fear their next raise will be a substantial down round (although they'd be far better off with a partnership where they trade chunks of the company for access to capital and synergy), which would lead to a reverse split of at least 1:5 (by yr-end 2018).

Call me a dreamer, but I do believe ONVO possesses solid science, but the world doesn't give anyone endless amounts of time to bring a vision to life. Tech develops faster and faster every decade; shoot, every year. ONVO and their new CEO need to get off the dime soon or the barriers to entry that are inherent to them 'getting their first because they've been at it longer' will evaporate before their eyes - along with the value of years of accumulated paid in capital.

The move today was happening before the 13G filing hit the wires... IMO, the volume/price move (not exactly flaming hot) is tied more to market manipulation by speculators/MMrs who have been able to routinely pull on the emotional heart strings of 'long ONVO investors' who hope/wish every quarter for any sign the company is making good on it's previously shared vision(s).

It's not at all unusual for this stock (and countless others, who are more speculation than substance) to move in the 7-10 days prior to earnings - which typically is successful in roping long investors back into the thinking "is it different this time", "does someone know something they shouldn't going into the earnings all"?

Many investors are pulled back into the emotion, which only fuels the situation. If this is what's happening there are resistant points at 1.50, 1.59, 1.67, 1.75, 1.84 and 1.93 - with the one I think it most attainable, but also the hardest to break = $1.67.

Assuming this is just swing trading at it's usual best just prior to earnings - look out below if one is left holding the bag when the music stops. Look for a handful of unusual high volume days, a close or two above the upper Bollinger Band, and a nasty intraday reversal on really solid volume, that signals the latest trip to the bunch bowl has served it's purpose.

My view of the above is such that I only hold options at this point going into the final stretch (7-8 days) before the call. Maybe I can catch some benefit from the insanity (volatility).

For those who have been long for years - I pray that 'this time it's really different' so you all can get whole at whatever price point that may be. I hate seeing the story "The Boy Who Cried Wolf" play out with these high potential story stocks. I've lost my fair share, and then some, chasing dreams too.

Avg Buy Out Premium over 10 Yr period for Co w/Mkt Caps over $50MM = 37%

A bit dated - but lets run with this for the moment:

For the 100+ public companies acquired in 2013 with pre-announcement market caps over $50 million, the average premium to the share price a month before the announcement was 37%. [1]. Looking back over the past 10 years, the premium has also averaged 37%.

$1.40 + 37% = $1.92. That's well below the cost of a share in the last down round raise, that netted $2.50/share.

It's been my view for a long time that a buy out is the best option for shareholders. My concern is the current valuation is already 33X revenues, which is already VERY expensive for anyone an acquisition.

What is there to buy here? $4-5MM in total revenue is literally nothing. Even at today's mkt cap the company is valued at 33X revenues - who in their right mind would pay 33X revenues for a company that has missed it's own guidance two years running. Guidance wasn't put upon them - THEY set their OWN guidance and blew it in back to back years. They did this to themselves - and no one else. Really a sad situation, for employees, shareholders, and those who would benefit physically if they could only do what they say they're capable of doing.

Not sure what is worse, the former CEO who mislead shareholders (me being one of them, directly) or the current CEO who is literally a ghost at the wheel. He's running the company as if private, not public. Missing in action from the word go. You'd like to believe actions speak louder than words, since he's so silent towards shareholders - but no, there is no action. There are no words... just a share price that keeps trending lower, and lower.

Earnings are coming up very soon. Why would we think it will be any different than the last several quarters of disappointment?

This is truly a case of the boy who cried wolf... I pray they claim 2X revenue for the next 12 months over the last 12, but what's the catalyst- truly what is the catalyst. If they're waiting for their orphan drug status to drive the stock price without revenues - don't hold your breath.

Next major action, IMO in the next 3-6 months, will be a major down round raise, and by year-end a massive reverse split of at least 1:5 or 1:6. And then the entire mess will repeat.

....doing the same thing over and over and expecting a different result, well, we all know what that's called.

There is so much creativity in the world, in the science/medical/bioscience communities... it's amazing. As we've said before, no man, nor time, waits for anyone or anything (patented or not)... tick tock tick tock.

...only time will tell if they hit their guidance this year, or dramatically cut fiscal 2018 guidance 1/2 way through the 4th quarter again. IMO we know how the year is going after the Nov 2017 earnings call (Q218). And only then. Q1 won't tell us anything. The company said 1/2 half will be softer than second half. Lets see if that guidance remains intact come the Nov call... only 5 months to wait - which for those who have a 5 YR HORIZON - that's a drop in the bucket.

5 yrs is a very long time, and the same thing has been said about this company for more than 5 yrs... there are better places in the meantime to make a good ROI.

Wasn't much to like in the filing or company recorded announcement. They're basically forecasting the upper end of fiscal 2017 guidance (before they downgraded their forecast <60 days from the end of the year) as the middle range of guidance 12 months out. They're saying - the market has not adopted our solution the way we thought, so we're going to take 2 yrs to get to $6.5-8MM rather than one, and no, we're not going to grow triple digits for years to come, as we stated multiple times - until maybe fiscal 2019. They proudly stated their customers are working side by side with them to 'develop' their offering. As if that's comforting. I call that - spin. Of course I would say the same thing in their shoes - of course. But as a shareholder I don't want to here justifications for lack of revenue growth - I want to see revenue growth demonstrated.

This article puts ONVO, Facebook and Snap in the same sentence as companies who could have an Amazon like future. The article doesn't skirt the issue that much has to change for that to happen... but nonetheless - interesting to see ONVO mentioned in such a way. https://whotrades.com/feed?pinned=3813009&showMore=1&utm_source=maxsocial&utm_content=feed&frfi_id=WTFeedEmail

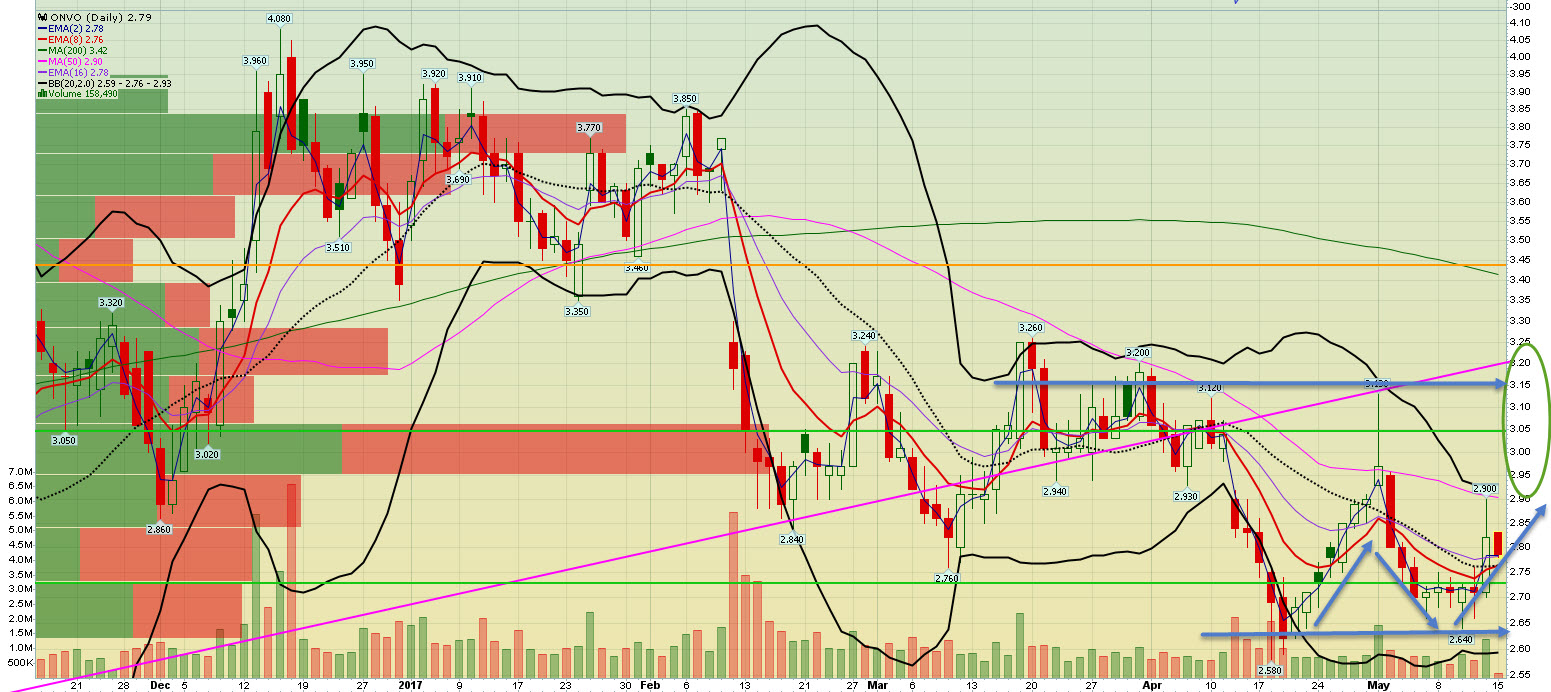

Closing above $2.85 was key. We'll see if it can get past $3.05, which appears to be the next RES line. Volume is everything at this point. I'd like to see a high 1.7 1.8+ MM share day tomorrow to show we have legs.

We need to get past $2.85 to retest the $3.15ish area... we pulled back today while IBB moved forward. That's not ideal. We'll see what tomorrow brings.

We need the company to announce they will provide Q4/Yr End Earnings, as usual, in early June. A pre-announcement will gut the stock price in my opinion.

Bill

I'd say it can do what it recently did the morning of the Univ of VA collaboration PR. It appears we had more or less a double bottom. Definite resistance above in the 3.10-3.15 range.

Pink line out of lower left corner originates @ $1.60 (multi yr low) and runs through $2.48, the low after the 2016 secondary. To retest $3.10ish we need to get past $2.85.

1.37... getting closer to your 1.40, my buy this morning @ 1.15 (trying to catch the gap fill0 was lucky.

Whoops, there is your $1.40

Could agree more....

Seems that way to me to. The new CEO's background isn't perfectly aligned to grow the tissue tox business. Seems to be more favorable towards the more expensive/highly dilutive liver patch side of the known plan. I wish they'd focus 95% of their time and energy on the tissue tox side of the business, get it to $20-30MM and then drive like crazy to be the primary supplier of 3D printed liver and kidney tissue to CROs.... THEN, and only then, increase their focus on a patch. If they're going to focus sooner than later on the liver patch... please, please, please name a well-heeled partner! I'd rather have 50% of something than 100% of nothing.

Nicely said....

The new guys is being handed a cold revenue stream, at best. I agree that revenues are everything today, tomorrow and in the future.

If by some good fortune they come in at mid-2017 guidance that will put them at roughly $682,000 in total Q4 revenues (and the company said don't look for collaboration $s). So that means, optimistically Q4 revs = Q3, which equaled Q1. Given that they indicated $500-$750K of Q4 revs will be delayed into Q1, I personally don't believe they will hit mid-guidance. I suspect their revenues will be < $500,000 in total, nearly all from service revenue. I wouldn't be surprised if <$400,000.

For the NEW GUY, that's a cold start, but there is truly nothing but UPSIDE.

I personally believe they should announce Q4 revs SOONER than later and get the BAD news out of the way. It's going to be bad, admit it, reiterate the money that was left on the table (they said $500-750K) will land in Q1, and GUIDE to NO LESS THAN 2X fiscal 2017 for fiscal 2018, as Keith and IR indicated more than once that shareholders can expect triple digit (2X) growth for years to come.

Failing to guide to at least 2X, especially if $500-750K f fiscal 2017 sales will land in Q1 fiscal 2018, will be worthy of a major backside kicking behind the barn, and associated decline in market cap.

Lots of words can be written, but in the end, it's all about revenues and more importantly rapid revenue growth. As you said, dilution is the enemy, and revenues control dilution (less capital needs to be raised and the capital that is raised will be at a higher cost per share if the company is growing). If the company is not growing - they'll still need to raise capital, but it's going to be at a lower price per share than the last round ($2.75, net $2.50). And that will be painful.

As for Mr Couch's background (patient trials)... I can see that being positive for the liver patch piece of the business... 3-4 yrs down the road. Not so sure I see the fit when it comes to tissue tox testing revenue ramp.. but I'll for now assume the board made a good decision. Mr Couch has a very steep hill to climb, and he has a 200lb backpack full of rocks on his back (large OS count, significant annual burn, company history of negative surprises, and flat QoQ rev growth for a year, assuming they hit mid-guide, but it could actually be worse).

We'll see where this goes... I won't be holding any shares at close before Q4 earnings are announced, assuming the company tells us when they're going to announce. Otherwise, I could be caught holding and I won't enjoy the impact of the news after hours or the next day, I am sure.

https://investorshub.advfn.com/uimage/uploads/2017/4/20/chprz2017-04-20_14-17-10.jpg

$2.48, the low post surprise downround secondary (when guidance was still as high as $6.2MM, and as low as $4.5MM....) is very possibly the next test.

Problems: Q4 revs will almost certainly be lower than Q3, which was lower than Q2... could be 1/2 as much as Q3. Collaboration revs are done until new contracts are signed. Founding CEO leaves at the cusp of greatness (supposedly) to pursue 'other start-up opportunities'... makes no sense. New CEO paid less than outgoing, ineffective CEO... new CEO's background unclear as to how he is 'the one' to supercharge QoQ rev growth... 2018 guidance yet to be delivered. Will Q118 revs prove that $s left on the table in Q4 (per the company's comments) truly land on the Q1 income statement? Will Q2 show rev growth over Q1 (which should be spiked with Q4 $s) or will Q2 be flat vs. the hopefully inflated Q1 results? That won't be known until Nov. Will the company wisely find a partner for the liver patch? Or will they take the 100MM share OS share count and bloat it even further to 130-150MM in order to 'go it alone' over the next 3+ yrs?

All I care about at this point is seeing proven revenue growth, from tissue services, the true near-term core business (in the next 2-3 yrs). The rest is hope, speculation, chatter.

Aether (sp?) crowd, is an odd turn of phrase, as that 'crowd' is made up for two people, the CEO and his sidekick CTO, or ah, best friend with three letters after his name (too). It takes more than a glossy product photo shots to make a company... far more. You also sorta need a product that works? You need a product that the market wants to buy, that solves real problems... something more than just a inkjet printed sign on a crumby San Fran hole in the wall building front pointing 'up'....which is from all the pictures I've seen of their so-called global headquarters quite literally all they have.

Blah blah blah... blah blah blah... whatever you say (it must be true, blah blah blah).

Blah blah blah Miji - blah blah blah Sure, whatever you say.

$ONVO Mr, Murphy's testimony runs from 24:30 to 30:00. The following link begins when he speaks:

Zacks has always been a joke on such 'recommendations'... fully automated, just gibberish. To be completely ignored, even when they say BUY BUY BUY! Worse than flipping a coin IMO.

blah blah blah, negative just to be negative... the board is by no means devoid of experience. The technology is solid, but I won't argue the dogs aren't eating the dog food at the rate that spins my or the overall mkt's wheels.

Can't argue with the logic of your suspicions...

Interesting word picture.... I am afraid it's more accurate than not. I still think the stock can be played (up and down) while the story plays out a few more quarters.

What does a good moderator do... and how does their good work translate into a stronger more desirable destination for investors? I suspect the structure of the site matters as much or more than the moderator (my experience going back 10 yrs),and the reality is there are so many more good investor sites today than there were back when I started posting here, including sites that provide a lot more value (charting, technical analysis). If others are like me - they use a mosaic of sites to paint a daily picture of the market and to color their view of specific stocks.

I like iHub for what it is - the lack of traffic/comments on this and other boards I visit is what makes iHub less useful to me than other boards I've contributed to over the years. Less traffic = less value. Why is there less traffic here? I say, there is a lot of competition that didn't exist before and iHub has not 'kept pace'.

Samsara is simply part of ONVO's supply chain (access to quality product as needed). The ultimate 'selling shoves and Levi's scenario' is exactly what ONVO is going for with their plan to be doing 10s of millions of internal tox testing to prove out the technology and ultimately become a tissue factory supplied CRO's. That's when their primary purpose in life will be to 3D bioprint tissue in mass, while building disease models and constructing/selling therapeutic tissues (i.e. liver patches).

In my mind that last aspect of their business strategy (therapeutic tissues) demands a strong financial partner, or they're going to run into major capital issues that will be highly dilutive.

We're in the crossing the chasm stage of revenue generation from tissue tox testing. It's all about 'proving the dogs will eat the dog food', and the only meaningful evidence of that will be QoQ revenue growth.

It's always about revenue growth, which is why the stock has been clobbered from 3.77 to 2.84 when they stated $500-750K of Q4 revenue will be delayed (into Q1), and fiscal 2017 was taken down from a high of $6.2MM to a low of $3.7MM (extreme ends of the guidance old and new). Assuming they hit the middle of new fiscal 2017 guidance ($4.1, the middle of $3.7-$4.5MM) Q4 revenues will be $682,000, which is lower than Q3, which was lower than Q2. That is not the right direction for a growth trend line. So Q4 will be lower than Q3, unless they blow out the upper guidance ($4.5MM).

The key for me regarding revenues is where do they come in for fiscal 2017 - and how do they guide for 2018 (min requirement is 2X 2017). As safe bet is they come in around $4MM and guide to $8MM. That's not a huge guide from the original upper end of 2017 guidance ($6.2MM), but all would show they are indeed growing revenues - just not in a way that proves (yet) there is a ravenous appetite amongst big pharma to move from animal testing to 3D bioprinted toxicity testing.

Assuming $4MM in '17 total rev and guidance to $8MM+, it does leave room for a surprise... for a change.

Not sure about the latter being accurate, but the former - yes, they're tooting their own horn, which as a shareholder I expect. The technology gains adoption through the broadcasting of such publications (and peer reviewed results).

ONVO's founder is already doing that (to produce leather)... slightly different purpose, but same neck of the woods.

http://www.modernmeadow.com/

I posted it twice because I was trying to create a new link to share on Stocktwits. For some reason ST would not let me share the original link, so I thought I'd try creating a second link and posting that over there... didn't work. No, I didn't post it twice to make a point - sorry about that!

ONVO has raised $74 million of their entitled $190 million SHELF REGISTRATION. That's 39%, leaving 61% ($116MM) to go - not $21.9MM.

Not saying $4 would be the price, but if on avg the remaining $116MM was raised at $4/share (net), that would be an additional 29MM shares added to the outstanding share count. If $3/sh it would be 38.7MM additional shares. If $5, it would be 23.2MM shares.

Here is what I received last year directly from ONVO when I asked about the Shelf Registration:

To be clear, shelf registrations speak to aggregate dollars ($), not shares. Therefore, ONVO's February 2015 shelf registration is for an aggregate $190M. Since this shelf was filed, three transactions have occurred as outlined below:

1) June 2015 equity offering - ~11M shares and $43M

2) F2Q17 ATM draw (announced in our earnings pre-release) - ~1M shares and $4.5M

3) October 2016 equity offering (based on figures in today’s 8-K) – ~10M shares and $26.5M

Taking all this together, the total draw to date (as of Nov 2016 Secondary) against this shelf registration has been ~$74M and 22M shares. All of this information is typically detailed in ONVO's 10-Q and 10-K filings.

$ONVO Updated survey results settings so anyone with the link below should be able to see all responses (and associated detail): https://www.surveymonkey.com/results/SM-7RWW7JX3/

The survey results are bullish. Yes Moo took the survey, but it can only be taken once per IP address, which is confidential to the Survey Co, Survey Monkey. Not suggesting you take or read the survey - but in summary the result are bullish as the vast majority of longs, although disappointed, rightfully so, with the delay of income, remain optimistic looking several quarters and years ahead.

ONVO has raised $74 million of their entitled $190 million SHELF REGISTRATION. That's 39%, leaving 61% ($116MM) to go - not $21.9MM.

Not saying $4 would be the price, but if on avg the remaining $116MM was raised at $4/share (net), that would be an additional 29MM shares added to the outstanding share count. If $3/sh it would be 38.7MM additional shares. If $5, it would be 23.2MM shares.

Here is what I received last year directly from ONVO when I asked about the Shelf Registration:

To be clear, shelf registrations speak to aggregate dollars ($), not shares. Therefore, ONVO's February 2015 shelf registration is for an aggregate $190M. Since this shelf was filed, three transactions have occurred as outlined below:

1) June 2015 equity offering - ~11M shares and $43M

2) F2Q17 ATM draw (announced in our earnings pre-release) - ~1M shares and $4.5M

3) October 2016 equity offering (based on figures in today’s 8-K) – ~10M shares and $26.5M

Taking all this together, the total draw to date (as of Nov 2016 Secondary) against this shelf registration has been ~$74M and 22M shares. All of this information is typically detailed in ONVO's 10-Q and 10-K filings.