News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

cash4

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The target and this movement has always been AMC and not APE or Adam, how did you guys derailed and forgot what it is all about ?

Do you think for a minute that Antara Capital will ever be proud to own a stock in their portfolio named APE ? LMFAO They will dump at the 1st sign of profit.

APE has officially switched to Fat Pig. While APE shares are making Antara rich, AMC is dropping like a rock, talk about slight of hand switcheroo, everyone is distracted by APE, LMFAO.

APE stock is the new Pump and Dump unfolding right before your eyes. EOD it will close below $1.20

So did Antara Capital for $0.66 PPS from yours truly Adam Aron, millions of it BTW, they are up over 300% already, LMFAO.

I suggest you take your profits cause they will take theirs EOD to celebrate a nice Christmas Day.

Adam sold APE shares to Antara Capital for $0.66 PPS, now Antara is pushing APE above $2 so they can cash out for millions in profit.

Antara is already up 300% in their investment in just 2 days.

Adam could've pulled that deal when APE was trading at much higher prices and make out like a Bandit, instead he screwed all APES further, sell your APE and buy AMC, AMC stock is the one below $5 now and hurting.

You mean Vote yes, if you have no brain.

AMC;s debt is $5 Billion, that debt will never be paid, and it is much easier to short from a higher price than it is to short a penny stock.

AMC down 10% premarket, great job Adam. A sweet Merry Christmas from your favorite Jewish CEO, LMFAO

From a Meme stock to a Laughing stock, 8% down Premarket.

You guys read only what you want to believe and give the worst advice, it says black on white that Adam diluted $2 bil since 2021, it was never shorts it was Adam the guy you worship so much, and he also says that he will continue to dilute APE, between him and Antara another 200 mil untop of 100 mil already diluted.

"AMC is raising the $110 million via the sale of millions of APE units to Antara Capital, Antara will also exchange $100 million in debt"

The reason they have spiked the price on APE shares yesterday, so they can dilute at a higher price.

Now he wants a Reverse split and that destroyed AMC share value by 1 dollar yesterday.

You see it , he says it and you tell me that I do not understand ?

Are you for real ?

AMC can't even break $5 and stay there, you're day dreaming.

The squeeze happened,but not like you think, they squeezed every penny out of your pocket, you see it and still do not believe it.

Adam sold $2 bil worth of stock since 2021. He destroyed the stock and every APE along with it.

They won't cover shit, they exercise their Puts and short it more, Puts made them Trillionaires because of Adam's incompetence.

Adam played everyone like a violin, sell your APE and buy AMC, vote against the proposal and vote him out, that is a move he won't expect, he plans to dilute more APE shares.

"AMC is raising the $110 million via the sale of millions of APE units to Antara Capital, which is also an AMC debt holder. Antara will also exchange $100 million in debt due in 2026 for around 90 million APE units"

AMC’s meme-stock sales are approaching its total valuation

Published: Dec. 22, 2022 at 5:18 p.m. ET

By Bill Peters

comments

https://www.marketwatch.com/story/amcs-meme-stock-sales-are-approaching-its-total-valuation-11671747492?mod=newsviewer_click

Theater chain’s market capitalization stands at $2.56 billion as it looks to add to more than $2 billion in share sales since the beginning of 2021

AMC announced a $110 million equity capital raise on Thursday.

AMC

-7.36%

APE

+75.18%

GME

-3.65%

AMC Entertainment Holdings Inc. is selling another $110 million in stock, adding to a total that has already exceeded $2 billion since the theater chain got swept up into meme-stock madness and approaching the stock’s total market capitalization.

Shares of AMC AMC, -7.36% fell as much as 22% on Thursday, hitting their lowest intraday prices since March 2021, after the company announced plans for its latest equity capital raise. Executives also said they hoped to hold a shareholder vote on a 1-for-10 reverse split on AMC’s common stock, as well as a proposal to boost the allowed number of AMC common shares to permit the conversion of AMC’s preferred equity units — or APEs APE, +75.18%, a reference to the nickname for the retail traders in the meme-stock universe — into common stock.

The price of AMC’s APE units jumped 75.2% to $1.20 on Thursday. AMC shares closed with a 7.4% decline at $4.91.

Even before the $110 million equity raise announced Thursday, AMC had sold $2.04 billion in stock since the beginning of 2021 and the dawn of the meme-stocks era that that launched the movie-theater chain, GameStop Corp. GME, -3.65% and others into the stratosphere.

See also: What can we expect from meme stocks AMC, GameStop and Bed Bath & Beyond in 2023?

That total does not include $159.1 million in stock sales that took place in the fourth quarter of 2020, before shares began to spike in January 2021. Including those sales with the others completed since the beginning of 2021 — $1.611 billion in common-stock offerings and $425 million in convertible shares — and adding the figure from Thursday’s announcement, would push the total even closer to AMC’s total market capitalization. The company’s market cap stood at $2.56 billion at Thursday’s close, according to Dow Jones Market Data.

AMC is raising the $110 million via the sale of millions of APE units to Antara Capital, which is also an AMC debt holder. Antara will also exchange $100 million in debt due in 2026 for around 90 million APE units. That swap, AMC said, would reduce AMC’s outstanding debt by $100 million.

Chief Executive Adam Aron said on Twitter that the move put the theater chain “in a much stronger cash position.”

Aron has tried to find ways to increase AMC’s share count and sell more shares — a move the company resorted to after pandemic-related shutdowns left the movie-theater industry on life support. After investors resisted calls to increase the allowed share count last year, Aron introduced the APEs as a way to continue to sell equity without increasing the share count.

Now, investors will be asked to vote to allow AMC’s board to increase the share count so that APEs can be converted into normal shares. They’ll also vote on whether to allow AMC to roll out a 1-to-10 reverse stock split, and whether to give the company the right to sell more shares instead of just APEs.

“Also, APEs worked exactly as intended to let us raise needed cash, buy back debt, explore M&A,” Aron continued on Twitter. “But a huge discount in APE market price vs. common stock must be addressed. We’ll hold a shareholder vote. It’s time to convert APE preferred into AMC common to eliminate that discount.”

See also: AMC thought about buying some Cineworld theaters, but it went nowhere

He added that a “company as distinguished as AMC shouldn’t let Wall Streeters wishing us harm drive us to being a ‘penny stock.’ So in the shareholder vote, you also can consider a 1:10 reverse stock split. Simple arithmetic, if approved, the share count goes down so share price goes up.”

So far this year, AMC stock is down 82%. The company has not reported a quarterly profit since the COVID-19 pandemic began, and has reported cumulative net losses of more than $6.5 billion since the beginning of 2020.

Analysts tracked by FactSet on average expect AMC revenue to hit its highest level since the beginning of the pandemic in the fourth quarter — $1.21 billion. But they’re still projecting a loss of roughly $124 million in the period.

Adam turned this stock into a penny stock, nobody else Everyone should sell their APE shares and buy more AMC and vote against the proposal and vote him out.

Adam sold his portfolio in the $20's range. all he is doing with a Reverse Split is to raise the ceiling higher for a even bigger drop.

By converting APE into AMC it tells me that he diluted all the APE shares he had and he cannot raise funds anymore unless he places all shares into one big pile and then keep diluting it all at once, do not fall for this evil dude, he has no interest to make anyone a dime in profit.

On Thursday he put out news that he is in negotiations to purchase more theaters out of bankruptcy, and the stock took off almost approaching $6, once he saw that by 2 pm he put out another PR stating that negotiations are off the table and the stock stayed flat all day, only to destroy more value with an idiotic proposal the very next day.

$6 Calls expiring this Friday are doomed because of this Evil prick, right before Christmas.

Time for APES to use their voting power and take Aaron off the Throne, he is a sellout that betrayed everyone, he has no reason for a reverse split, other than the fact THEY got to him, Aaron owns Puts only and he might as well just work for Citadel. IMHO.

Sell your APE shares and buy more AMC shares

$EXPR borrow interest rate increasing..

Express, Inc.: My Latest Liar's Poker Bet (Rating Upgrade)

https://seekingalpha.com/article/4563888-express-inc-my-latest-liars-poker-bet

Dec. 12, 2022 7:38 AM ETExpress, Inc. (EXPR)AVYA, CSSE, CVNA, GME, REVRQ9 Comments

Summary

Express reported very poor Q3 FY 2022 results and indicated Q4 FY 2022 results would be similarly challenging.

Despite the really poor second half FY 2022, Express signed a transformative deal with WHP Global, that will result in pro-forma debt moving from $211 million net to $31 million net.

As a result of this WHP Global deal, I've moved from long time bearish to tactically bullish and got long at $1.38 (in pre-market on December 8, 2022).

The short thesis, at least in the near term, has been defused!

This idea was discussed in more depth with members of my private investing community, Second Wind Capital . Learn More »

IMG_2478.jpg

Vincent Besnault

We have a lot of ground to cover here, so if I can pull this off, you're in for a good read. Let's start with the title of today's piece: Express, Inc. (NYSE:EXPR): 'My Latest Liar's Poker Bet'. This should naturally lead you ask what was my most recent game of Liar's Poker. Well, I'm glad you asked. And just to be clear, I only selectively play Liar's Poker. It is a really difficult game to play well. The last time I played Liar's Poker and wrote a small mini series of articles, here on Seeking Alpha, was on Carvana Co. (CVNA). Back then, Carvana shares were trading in the low $20s to mid $20s, the stock was highly shorted, and the Twittershpere and stock whispers were calling for an imminent bankruptcy. I was told, unequivocally, that Carvana would file bankruptcy on or before September 30, 2022.

To just to be clear, on the timing, as timing is everything on these one month to three month Liar's Poker bets, the Carvana mini series was written from June 21, 2022 - July 21, 2022.

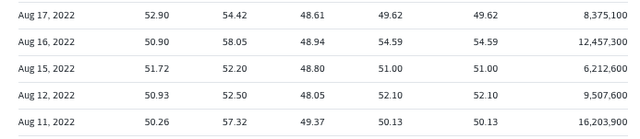

And just to set the record straight, enclosed below, I provide the time and sale data, on Carvana, at times of article publications, and then captured the subsequent rally that topped out when Carvana shares hit $58, on August 16th.

On June 21st, Carvana shares moved from $25 to as high of $32.37 and closed at $23.11, on June 29th.

On July 21, 2022, the date of the final piece, in the series, Carvana shares closed at $28.21.

From August 11, 2022 - August 17, 2022, Carvana shares traded north of $50 per share, eventually peaking at $58.05, on August 16, 2022.

My long winded point here is that Carvana was a much more difficult contrarian and shorter term Liar's Poker bet (three months in this case), given its very elevated balance sheet leverage and associated interest expense service requirements. The company needed to hit all green lights coming home, as it turns out, the rally in rates, when the 10YR yield moving under 3%, in August 2022, proved fleeting. Making matters worse, and then macro conditions worsened and used car prices tumbled. So instead of hitting all green lights, they hit a few green lights and then mostly red lights.

Later in a piece, as an observer of short squeezes, I'm going to discuss a few other short squeezes. The point I'm driving home here is that shorting companies with $100 million to $150 million market capitalization is at best bad risk management and at worse kind of crazy.

Let's Talk Express

On the morning of December 8, 2022, Express, Inc. reported very poor Q3 FY 2022 results. Q3 FY 2022 Adj. EBITDA was negative $14.5 million and Adj. EBITDA for the first nine months of FY 2022 was $17 million, down from $38.9 million, in the comparable period.

Express, Inc.'s Q3 FY 2022 10-Q

Express, Inc.'s Q3 FY 2022 10-Q

There is simply no sugar coating it, these were very poor results, with comps down 8%, and gross margins down 540 Bps (from 33.2% to 27.8%). Also, SG&A was up $9.5 million in Q3 FY 2022 compared to Q3, last year. On the Q3 FY 2022 conference call, management admitted that they misgauged the macro headwinds, citing a highly promotional competitive landscape coupled with a few fashion misses in the women's business.

The Q4 Outlook

The Q4 outlook is forecasted to continue the Q3 FY 2022 weakness. And as Q3 FY 2022 results marred the year, management took down its full year guidance.

Seeking Alpha / Express, Inc.'s Q3 FY 2022 Earnings Release

Seeking Alpha / Express, Inc.'s Q3 FY 2022 Earnings Release

During the analyst Q&A section, of the Q3 FY 2022 conference call, Tim Baxter, Express, Inc.'s CEO encapsulated management's pivot in Q4 FY 2022 and into early FY 2023. He noted that they will get inventory back in-line and entering FY 2023, Express will be in a much cleaner inventory position. Again, though, they expect Q4 FY 2022 to be very tough and incorporated that into guidance.

Absolutely, Jay. So, the outlook that we provided for 2022 clearly indicates that we're seeing the same behavior in the fourth quarter from the consumers that we saw in the third quarter. And so that is slightly different than our expectation. Coming into the fall season, our previous outlook we did expect to see improvement in the fourth quarter based on Omicron and the impact of that last year and all sorts of other factors.

The macroeconomic environment and the consumer sentiment that I described earlier, spending less on discretionary categories like apparel, and looking for deep-deep discounts that still seems to be in play in the quarter. And I would say the discount side of that is even more in play in the fourth quarter as it is typically a more promotional quarter anyway. Thinking, you know going forward, we have not shared an outlook for 2023, yet we will do that when we share our fourth quarter results, but we are approaching 2023 with conservatism, particularly in how we're buying merchandise.

And we have a great go to market process that as the supply chain challenges and bottlenecks have, sort of evened out, we're going to be able to get back into chase mode, which is something that works very, very well for us. So, we are testing things right now in the southern part of the country that will influence product we chase into for the [indiscernible] first quarter and the second quarter. So, we're going to approach it with conservativism and we have the mechanisms and the ability to chase into trends as we see consumer behavior rebounding.

That said, with the supply chain set to get significantly better, in FY 2023, they don't need to carry as much inventory or absorb the once sky high container costs of second half calendar 2021 through first half calendar 2022. Also, as there is a lag between when the inventory is ordered and when it sells through, at retail (with the higher associated cost of vintage 2022), this will be a gross margin tailwind for FY 2023.

Next, let discuss Express, Inc.'s debt.

The Debt, as of October 29, 2022

A $290 Million Revolver (11/26/2027) SOFR +165 to +185 Bps

On November 28, 2022, Express announced that they refinanced and termed out its capital structure. This consists of a Revolving Credit Facility getting increased from $250 million to $290 million, at a lower rate, and with a maturity date of November 26, 2027. In case you are wondering, the rate of interest rate is now SOFR +165 to +185, which is a slight decrease from the previous terms of LIBOR +200 Bps to +2.25%.

As you can see, as of October 29, 2022, $144 million was drawn on the revolver.

A $90 Million Term Loan (11/26/2027) SOFR +750 Bps

As part of the refinancing, the term loan was reduced from $140 million to $90 million. The maturity dates mirrors the revolver and terms are SOFR + 750 Bps. As of October 29, 2022, this was fully drawn.

Express, Inc.'s Q3 FY 2022 10-Q

Express, Inc.'s Q3 FY 2022 10-Q

Just to be crystal clear, whenever you refinance first and second lien debt, the bankers are well aware, at least directionally of the current quarterly results and near term outlook. Lenders aren't in the business of getting blind sided, otherwise they wouldn't be around and won't be able to weather different economic cycles. Therefore, I would argue that lenders were apprised, at least directionally, of the underwhelming Q3 FY 2022 results and management's tepid expectations for Q4 FY 2022, and assumed similarly tough trends when they agreed to refinance the debt at favorable terms.

The Elephant In The Room - WHP Global

When we are playing Liar's Poker, I had to be thorough and get into the weeds in the above sections, as I wanted to 1) established that Express, Inc.'s Q3 FY 2022 Adj. EBITDA and Q4 FY 2022 Adj. EBITDA outlook is uninspiring and 2) so we talk about the real elephant in the room - the transformative WHP Global deal!

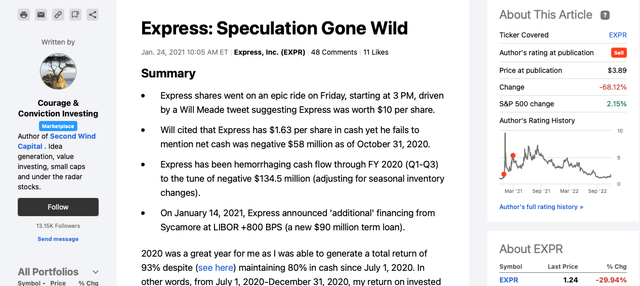

To be crystal clear, I've been negative on Express, the stock, since its two meme spikes of Q1 FY 2021. I even wrote this bearish article, on January 24, 2021, when Express was trading at $3.89.

Since then, on multiple occasions, when Express was trading at around $3 per share, I've been pitched the long case on Express. I have had zero interest whatsoever in owning Express as I just didn't see the bull case and I didn't love the valuation per se.

So let the record show, until December 8, 2022, I've been neutral to bearish on Express and had zero long exposure here. Lo and behold, and despite the really poor Q3 FY 2022 results (and subsequent weak Q4 FY 2022 outlook), I actually got long Express shares, at $1.38 (in pre-market), on December 8, 2022. The reason was simple - the WHP Global deal is transformative and completely destroys the short thesis, at least over the near term. In other words, I would argue that prior to this deal, the shorts had a valid short thesis (although shorting stocks with a sub $100 million market cap. seems a bit reckless). However, the WHP Global deal has defused the short thesis!

The Deal

When the deal closes, WHP global is buying 5.4 million newly issued shares at $4.6 per share ($25 million) and then paying $235 million for a 60% stake in a newly formed joint venture. The new JV owns global intellectual property rights of the brands. Express retains a 40% interest in the JV.

When the deal closes, WHP Global wires Express, $235 million and then Express pays $60 million, the first year royalty payment, to the JV. The next payment won't be due until Q1 FY 2024.

Express, Inc. December 8, 2022 Investor Deck

Express, Inc. December 8, 2022 Investor Deck

(Source: Express, Inc. IR Deck)

In addition, once the funds are received, the $90 million term loan will be paid off.

To be crystal clear, post deal, and including the TL breakage fee, Express corporate will have $114 million of cash, a $145 million revolver, and only $31 million of net debt!

You can like or dislike the deal all you want. The shorts can say the 3.25% royalty rate is too high (yet Express owns 40% of it). That doesn't matter! At least in the near term, the short thesis has been completely defused!

Express, Inc.'s December 8, 2022 Investor Deck

Express, Inc.'s December 8, 2022 Investor Deck

Next, and I want to discuss what I would argue is a bunch of outright propaganda on the Twittersphere. Some people, folks probably short, have suggested the lenders won't somehow sign off on the WHP Global deal.

Let's think this through.

On a pro-forma basis, post deal, the $95 million TL gets paid off, including breakage fee (hmm...I wonder why there was a breakage fee in this newly refinanced TL) and Express now has $114 million of cash. Secondly, if you look at EXPR's balance sheet, the company has $422 million of inventory, at quarter end Q3 FY 2022. With a difficult macro backdrop, on the Q3 FY 2022 conference call, management noted their short term focus was getting inventories in-line and well positioned entering FY 2023. Positively, an improved supply chain (both velocity and cost) means they don't need to hold nearly as much inventory. Arguably, $100 million of excess inventory gets permanently converted to cash, providing lenders with more comfort. Lastly, it is my understanding that Express expects to receive a $53 million tax refund from the CARES act on or around Q1 FY 2023.

Quite frankly, if anyone knows anything about how a capital structure works, the ABL or Revolver always sit at the top of the credit stack. With Express' balance sheet transformed, what is the risk to the first line lenders? Yes, you could make a point that a second lien lender might object to the new royalty terms, but that piece of capital structure is eliminated once the deal closes.

Express Q3 FY 2022 10-Q

Express Q3 FY 2022 10-Q

And just one other point to consider. I would argue Yehuda Shmidman is a reputable businessman, and the back that he is indirectly backed by Oaktree and Howard Marks, solidifies that view. The notion, that Yehuda somehow entered into this transaction as a backdoor way to take over Express in bankruptcy is unfounded and incendiary Twitter babble! Yet, sadly, that is the world we live in. The shorts will simply make stuff up if it suits them. Therefore, you need people like me to take on those arguments and point out how ridiculous they are, in the public square, as sunlight is a good disinfectant.

The Stock Price

Express shares have been a wee tad volatile. Initially, Express shares reacted favorably. As on December 8, 2022, when the 9:30am bell rung, Express shares leapt to $2.03, hit an intra-day high-water mark of $2.14 and closed at $1.77 per share. 74 million shares, or more than 100% of Express, Inc.'s total share count changed hands. And in case you're wondering, as of November 26, 2022, Express only had 68.3 million total shares in existence. The next day, Express shares opened lower, had a brief rally, and then very persistent and uniform selling took hold. It was as if the stock was being walked lower. I've been doing this a long, long time and my hunch is that the shorts shorted the heck out of Express shares, on Friday. It is highly, highly unusual for a stock to trade up so much on what the market perceives as good news and then literally fall out of the sky, as if it was shot down. The only logical explanation is aggressive short selling, at least in my view.

Yahoo Finance

Yahoo Finance

Other Short Squeezes

Nothing for nothing, over the past five years, I've spent a lot of time fascinated trying to understand and follow short squeezes. It is my version of torpedo chasing.

Incidentally, enclosed below and on April 26, 2020, I wrote this GameStop Corp. (GME) article. So although it is impossible to bat thousand, in this wild and high stakes game, I've had a lot of at bats, and am fairly well versed when it comes to short squeezes and understand the conditions that create a good setup.

Seeking Alpha

Seeking Alpha

Likewise, I want to draw readers attention to three recent short squeezes. All three squeezes occurred to companies when their market capitalization were low in absolute and market capitalization terms. Also, one company actually filed bankrupt, one narrowly avoided a bankruptcy through a take under, and the other is likely to file.

On June 16, 2022, Revlon, Inc. (OTCPK:REVRQ) filed for bankruptcy. Days before the filing, Revlon shares tanked from the mid $4s to as low at $1.08, on June 13, 2022. On June 16, 2022, the day of the actual bankruptcy filing, Revlon shares kissed $1.25 and then rebounded to $1.95, by the closing bell. By June 22, 2022, Revlon leapt from that $1.25 (June 16, 2022) low and actually hit a high-water mark of $9.89.

Revlon is Exhibit A on why don't short stocks with sub $100 million market caps.

Revlon's Stock Price (Yahoo Finance)

Revlon's Stock Price (Yahoo Finance)

Moving along, let's discuss Chicken Soup for the Soul Entertainment, Inc.'s (CSSE) take under of Redbox. As we don't have precise time and sales data, as Redbox has been delisted, post transaction, I'm going provide relative numbers, going off of memory. On May 11, 2022, CSSE announced it's take under of Redbox.

The deal priced implied an equity value for Redbox of $0.65, on the day of the deal announcement. Lo and behold, over the ensuing weeks, as a big short squeeze gather paced, and Redbox shares hit a pinnacle of roughly $18 per share!

Seeking Alpha

Seeking Alpha

RedBox is Exhibit B on why you just don't short $2 stocks!

Finally, to round out our recent list of wacky short squeezes, let's consider Avaya Holdings Corporation (AVYA). Avaya can only be described as a Greek tragedy. The company provided guidance earlier in the year and then dramatically cut that guidance. The management team got the boot and a very high level of debt and interest coverage burden crushed the stock.

Prior to the sudden business collapse, Avaya had roughly 86 million shares outstanding. Lo and behold, and despite being in dire straits, financially, AVYA shares squeezed from an August 9, 2022 closing price of $0.61 to a high of $2.30, on September 6, 2022!

Avaya's Stock Price (Yahoo Finance)

Avaya's Stock Price (Yahoo Finance)

Putting It All Together

Post closing, Express will have transformed its balance sheet via this WHP Global deal. The company will pay off its expensive term loan, should be able to convert approximately $100 million of excess inventory into cash, and still expects a $53 million CARES act refund, in Q1 FY 2023. Lastly, the company's revolver was not only refinanced, it was increased, extended, and at modestly better terms.

If bankrupt Revlon can squeeze massively, Redbox moved up 9X during its epic short squeeze, and even Avaya bounced nearly 4X, off the trough, who in their right mind is shorting Express at $2 per share, let alone sub $1.50 per share?

The short thesis has been completely defused by the WHP Global news and on November 28, 2022 its debt was just termed out and refinanced at favorable terms!

In closing, this long time Express bear has flipped to tactically bullish here. Admittedly, Q3 FY 2022 results and Q4 FY 2022 guidance left much to be desired. That said, at $1.24 per share, that really doesn't matter, as the balance sheet safety, on a pro-forma have shifted from weakness to strength. This is the elephant in the room. So, if you like swimming in the high risk/ high reward waters then I would argue Express is a great tactical and Liar's Poker bet, at any price under $1.50.

Second Wind Capital is a value oriented investment service with a strong recent track record of exceptional outperformance. The focus is mostly small cap value and special situation equities. From January 1, 2020 - November 30, 2022, the flagship account has compounded at 43% per year.

Way to oversold, time to go back up, it almost reached the 52 Week low of $1.04. Load up

$EXPR.

$EXPR Short sale restricted for 2022-12-12

https://www.shortablestocks.com/?EXPR

Fee Rebate Available Updated

3.45% 0.37% 2500000 2022-12-12 09:30:04

3.45% 0.37% 2500000 2022-12-12 09:15:03

3.45% 0.37% 2500000 2022-12-12 09:00:03

3.45% 0.37% 2500000 2022-12-12 08:45:03

3.45% 0.37% 2500000 2022-12-12 08:30:04

3.45% 0.37% 2500000 2022-12-12 08:15:03

3.45% 0.37% 2100000 2022-12-12 08:00:04

3.45% 0.37% 950000 2022-12-09 17:45:03

3.45% 0.37% 950000 2022-12-09 17:30:04

3.45% 0.37% 950000 2022-12-09 17:15:03

3.14% 0.68% 950000 2022-12-09 17:00:04

Shares Outstanding 68.27M

Shares Float 65.35M

Institutional Ownership 49.30%

Short Float 9.68%

Important Factors &Technical Analysis of “$EXPR” described below:

http://www.stocksequity.com/active-stocks/active-stock-evaluation-lucid-group-inc-nasdaqlcid-express-inc-nyseexpr/

Further, Shares of Express, Inc. (NYSE:EXPR) have seen the needle move -29.94% in the most recent session. The NYSE-listed company has a yearly EPS of $0.23 on volume of 18,007,993 shares. This number is derived from the total net income divided by shares outstanding. In other words, EPS reveals how profitable a company is on a share owner basis. The insider filler data counts the number of monthly positions over 3 month and 12 month time spans. Short-term as well long term investors always focus on the liquidity of the stocks so for that concern, liquidity measure in recent quarter results of the company was recorded 0.90 as current ratio and on the opponent side the debt to equity ratio was 0 and long-term debt to equity ratio also remained 0. The stock showed monthly performance of 12.73%. Likewise, the performance for the quarter was recorded as -10.79% and for the year was -65.75%.

Analysts’ Suggestions to keep an Eye On: In terms of Buy, Sell or Hold recommendations, the stock (EXPR) has analysts’ mean recommendation of 2.50. This is according to a simplified 1 to 5 scale where 1 represents a Strong Buy and 5 a Strong Sell. Growth potential is an organization’s future ability to generate larger profits, expand its workforce and increase production. The growth potential generally refers to amount of sales or revenues the organization generates. In the last five years, the company’s full-year sales growth remained over -3.20% a year on average and the company’s earnings per share moved by an average rate of -18.10%.

The price target set for the stock was $5.50 and this sets up an interesting set of potential movement for the stock, according to data from FINVIZ’s Research. The company has a market value of $120.80M and about 68.27M shares outstanding.

Should You Go With High Insider Ownership?

Many value investors look for stocks with a high percent of insider ownership, under the theory that when management are shareholders, they will act in its own self interest, and create shareholder value in the long-term. This aligns the interests of shareholders with management, thus benefiting everyone. While this sounds great in theory, high insider ownership can actually lead to the opposite result, a management team that is unaccountable because they can keep their jobs under almost any circumstance.

Express, Inc.’s shares owned by insiders remained 0.70%, whereas shares owned by institutional owners are 49.30%. Many value shareholders look for stocks with a high percentage of insider ownership, under the theory that when administration is shareholders, they will act in its own self-interest, and create shareholder value in the long-term.

Historical Performances to Consider:

The Stock’s performances for Monthly, weekly, half-yearly, quarterly & year-to-date are mentioned below:-

On a Monthly basis the stock was -22.57%. On a weekly basis, the stock remained -14.48%. The half-yearly performance for the stock has -51.83%, while the quarterly performance was -47.55%. Looking further out we can see that the stock has moved -77.19% over the year to date. Other technical indicators are worth considering in assessing the prospects for EQT. RSI for instance was stand at 29.64.

The Toys R Us Owner Just Made a Big Bet on Express (EXPR) Stock

EXPR stock was up more than 60% at one point on Thursday

1d ago · By Bret Kenwell, InvestorPlace Contributor

Express (EXPR) is in the spotlight Thursday, as EXPR stock was up 67% at one point on the day.

The move comes after the company reported disappointing results, missing on earnings and revenue estimates.

A new joint venture with Toys R Us parent WHP Global has EXPR stock rallying.

BUY ALERT:

EXPR stock - The Toys R Us Owner Just Made a Big Bet on Express (EXPR) Stock

Source: Helen89 / Shutterstock.com

Every investor knows energy stocks are doing well, but many may not have noticed the strong rally in retail stocks. Nowhere is that more clear than with Express (NYSE:EXPR) — at least on Thursday. That’s as shares of EXPR stock are up about 40% on the day.

Shares opened higher by 58% on the day and rallied as much as 67%. Triggering the rally was the company’s third-quarter earnings report, which was delivered before the open.

Oddly enough, the company missed on earnings and revenue expectations.

A loss of 50 cents per share missed analysts’ expectations by 21 cents a share. Revenue of $434.1 million fell 8% year-over-year and missed estimates by $17.6 million. Additionally, comparable store sales fell 8%, while gross margins dropped 540 basis points. Worse, management expects a deeper full-year loss than analysts were forecasting.

So why in the world is EXPR stock up so much?

12 EV STOCKS THAT COULD JUMP 10X, 20X, EVEN 30X

EXPR Stock Surges on New Partnership With WHP Global

The retailer is entering a strategic partnership with WHP Global in an effort to revitalize the brand. WHP Global will invest $25 million to acquire 5.4 million shares of EXPR stock at $4.60 a share. It equates to a 7.4% stake in the firm.

It’s worth mentioning Express stock closed at $1.30 a share on Wednesday. Coming into today, EXPR stock had roughly 10% of its stock sold short, as well.

Express CEO Tim Baxter had this to say on the deal:

“Our partnership with WHP will drive greater scale and profitability of the Express brand through their category licensing and international expertise and strengthen our balance sheet … We expect to accelerate our growth by acquiring multiple brands in partnership with WHP and operating them on our platform. Both of these are expected to drive shareholder value.”

The two companies will form an intellectual property joint venture, valued at roughly $400 million. WHP Global — the owner of brands like Toys R Us and Anne Klein — will have a 60% stake in the new JV, while Express will have a 40% stake.

For its 60% stake, WHP Global will invest $235 million. The companies are hoping that this “mutually transformative strategic partnership” will “advance an omnichannel platform which is expected to drive accelerated, long-term growth.”

While EXPR stock is enjoying its gains on the day, it’s still down significantly on the year. Shares are still down 44.3% this year and 50% over the past 12 months.

On Penny Stocks and Low-Volume Stocks:?With only the rarest exceptions, InvestorPlace does not publish commentary about companies that have a market cap of less than $100 million or trade less than 100,000 shares each day. That’s because these “penny stocks” are frequently the playground for scam artists and market manipulators. If we ever do publish commentary on a low-volume stock that may be affected by our commentary, we demand that InvestorPlace.com’s writers disclose this fact and warn readers of the risks.

Damn...240 K shares wall at $1,40, who's dumping so much on great news ? Unreal

Disgusting what is happening here, 24% down in one day, right after WHP Global paid $4.50 per share, $25 Milly's worth, what now...they are just sitting idle watching their investment be slashed by 1/3, how is this possible ?

How's anyone allowing this stock to drop so much after amazing news ? WTF ?

Back to 12 and back to green, I bet someone feels really stupid right about now.

200 k bid, now we're talking, someone is upset.

52 Week low is 10 cents, selling at this level is pretty dumb, this is bottomed out.

Who the hell tried to short this early at the bell ?

Not if it helps to stay with the Big Boys, in that case is good. Once you loose Nasdaq, you loose big.

Looking great Premarket, up 11%. $NUWE

Walmart needs a new CEO and fast. Every financial institution raised their target to $166, the company announced a $20 Bil buyback and the CEO turns around dumps $272 Mil worth of stock at $152 PPS and if that was not enough he makes a public statement that he will close stores due to increased theft and shoplifting just enough to bring the stock down to $149 and ruin Call options for everyone.

Who gave this dummy the keys to the Kingdom and a horn to blow in ?

https://www.cnbc.com/2022/12/06/walmart-ceo-says-shoplifting-could-lead-to-price-jumps-store-closures.html

After a record in sales on Black Friday he goes on to say this...

https://www.barrons.com/articles/walmart-stock-ceo-sales-inflation-51670441358

Please, can we get someone competent to run this business ?

$AMC trading sweet premarket let's see it above $8 today.

C'mon $AMC you looked so sexy above $8 today, HODL the line dammit !!!

How is this stock trade after hours if it was delisted to the OTC ?

I will never understand why $IMPP is not trading above $3 at least.

HODL $AMC

$BBBY just made a deal for more than $10 PPS, why is the stock dropping ? $123 Mil for 11,7 Mil shares is a pretty good deal, what am I missing here ?

TWOH May Be The HOTTEST Stock To Watch In The Food Arena As Food Prices Explode. Shares Rallied 100% In Recent Days and The Upside Potential Is Still OVER 2,700% After Gaining 4,580% Since I First Alerted The Stock In 2021!!!

Two Hands Corporation

USA: OTCPK: TWOH

CANADA: CSE: TWOH

Last Price: $0.11 | Website | SEC Filings | Latest News

Horia,

It's been a couple of years since the pandemic hit the economy and one good thing that came from it has been the ease of online grocery shopping and food delivery.

In fact, today's alert is a "Blast From The Past" as I alerted TWOH in 2021 and it's now trading at prices representing 4,580% Gains!

Excitingly, many customers prefer online grocery shopping owing to its easy ordering method, contactless and attractive payment schemes, and a safe and convenient delivery system.

To cash in on the evolving trends, giants like Amazon, Walmart, and Target have strongly emphasized on boosting their delivery capabilities with same-day deliveries to offer a seamless shopping experience.

This puts attention on an emerging player in this growing arena that could be at a supreme value right now as it takes on the massive Canadian market!

With a recent breakout of over 100%, the stock could still see stellar upside of 2,700%+!!

Delivery services for groceries and food exploded during the pandemic, and those reverberations will continue into the decade ahead.

According to a 2021 study by payment company PayPal, online spending across Canada increased by more than $2 billion per month during the pandemic—from an average of $109 per household to $178. Not surprisingly, grocery shopping was a key driver in this increased online activity.

This little-known company is tackling this monstrous Canadian market and has seen record quarter over quarter revenue growth... They have a high margin business that is scalable and offers a broad range of products. It may be just a matter of time that Wall Street fully discovers them.

With a current STAY LONG rating, a penetrable enormous market, and red-hot momentum, Two Hands Corporation (OTCPK: TWOH) has astronomical bounce potential in the QUADRUPLE DIGITS!

Two Hands Corporation

(OTCPK: TWOH)

TWOH is focused exclusively on the grocery market through three on-demand branches of its grocery businesses: gocart.city, Grocery Originals, and Cuore Food Services. All three of such branches of the Company's business share industry standard warehouse storage space and inventory. The Company's inventory is updated continuously and generally consists of produce, meats, pantry items, bakery & pastry goods, gluten-free goods, and organic items, acquired from various different suppliers in Canada and internationally, with whom the Company and its principals have cultivated long-term relationships.

TWOH - A "Stay Long" Rating Could Help Fuel a QUADRUPLE DIGIT Rally

Shares of TWOH have been moving higher in recent days, rallying from around 5 cents to as high as 13 cents this week.

Shares have already more than doubled and this could be nothing compared to what still may be on the horizon.

TWOH currently has a "STAY LONG" rating at AmericanBulls.com which can be seen below:

With a 52-week high of $3.10, the upside from current levels is still over a staggering 2,700%!

And the chart CLEARLY lays out a case for another EPIC RUN! Could we see another 1,000%+ Run comparable to the Gains of 4,580% following last year's alert?!

(CLICK HERE TO ZOOM)

An estimated one-third of shoppers buying groceries online, according to a survey. It makes sense. Why not go to a park instead of a parking lot? Grocery deliveries have made it easier than ever for people to live their busy lives and avoid unnecessary crowds.

As consumers accelerate this evolutionary stage of grocery shopping, TWOH could see immense growth opportunities ahead...

Revenues have already been skyrocketing for the company!

The food industry is ripe for growth amid strong demand and inflating grocery prices. Food stocks may rise along with inflation and makes TWOH one to put high on your radar. Consumer staple stocks tend to be defensive in bear markets as their products are always in demand.

TWOH - Two Hands to Drive and Two Hands to Deliver

TWOH is a food distribution company through three on-demand food brands, Gocart.City, Grocery Originals, and Cuore Food Services.

Gocart - an online delivery marketplace that launched last summer delivering fresh and high-quality produce, meats, pantry items, bakery & pastry, gluten-free, and organic items throughout Southern Ontario. Our line of high-quality products come from long partnerships with local and international suppliers.

Grocery Originals - a brick-and-mortar retail experience that was recently launched in Mississauga, Ontario, fully equipped with a deli, cold storage, and a stone pizza oven. We will also be offering a wide variety of fresh and specialty meals curated by Corporate Executive Chef, Grace Di Fede.

Cuore - a food import and distribution brand that operates in a wide range of channels including food service, retail chains, hotels, and restaurants. Core offerings from Cuore range from Italian themed oils, pastas, sauces, to dry packed goods, to exclusive wines, coffees, and desserts.

Key Partners

• Primo Jardin, Ontario Food Terminal, Italian Chamber of Commerce Toronto

• Manufacturers, Brands, Distributors, Logistic partners, Investors

Key Activities

• Procurement, Logistics / Distribution, Pricing

• Customer data processing, Payment Processing, Marketing & Campaigns, Digital projects

Key Resources

• Presence (new), Logistic network, Inventory, Partnership/alliances, Dedicated employee

It was last year that TWOH completed their first year of gocart.city operations with milestones that include, growing their grocery category to over 2,700 items, their customer base to over 1,000, delivery to 6 days a week and expanded their delivery area to better meet customer demand.

Grace Di Fede is TWOH's Corporate Executive Chef and brings over 18 years of hospitality and diverse culinary experience to GoCart.city, as well as international experience having worked in both The Netherlands and Italy.

Di Fede will be curating specialty recipes and meals for the online grocery marketplace, as well as our brick and mortar location set to open later this week, Grocery Originals. She will be focused on traditional, cultural dishes and diet-friendly dishes.

In addition to her culinary experience, Di Fede was awarded the Chef de Cuisine Certification (CCC), sanctioned by the Canadian Culinary Federation!

TWOH - A Paid Digital Difference

TWOH's 3rd Party Partner possesses the technology and the platform for a full digital marketing execution. They are capable of performing multi-channel advertising, Strategic SEO, with the ability to market across Google, Facebook, Instagram, LinkedIn, Display, OTT/CTV & Video.

The experience to connect with the world’s leading platforms to drive audiences to desired website and mobile app.

TWOH - A Growing Market to Zoom in On

While only 19 per cent of Canadians engaged in online grocery shopping pre-pandemic, that number had jumped to 30 per cent just one month into the pandemic and to nearly half (49 per cent) after a full year of pandemic living.

According to research firm eMarketer, the emergence of the work-from-home phenomenon was one of the key drivers, with 27 per cent of remote workers and students ordering online, compared to just 19 per cent of the overall adult population. The report said that COVID’s recent Omicron wave also damaged the in-store experience and drove more people to adopt online as their default shopping method.

“The pandemic permanently changed people’s habits as it relates to delivery. Everyone picked up this habit of getting food delivery a few nights a week; maybe getting their groceries delivered once or twice a week. What we’re seeing is that even as the world starts moving again, people are keeping that new normal. For our business, this is really positive. This trend is here to stay.”

- Lola Kassim, general manager of Uber Eats in Canada

Uber launched online grocery shortly after becoming sole owner of the now seven-year-old Latin America delivery start-up Cornershop in 2020, initially making the service available in 19 cities throughout Latin America and Canada. The launch enabled customers in Toronto and Montreal to order from retail partners including Walmart, Metro, Costco, and Rexall through the Uber app.

A 2021 study by Dalhousie predicted that the Canadian grocery industry “will look very different” from its pre-pandemic state once the pandemic recedes. Based on a survey of 10,024 Canadians, the Dalhousie study found that nearly one-quarter (22.2 per cent) of Canadians plan to buy online regularly, while ordering online for curbside/in-store pick-up is also gaining momentum.

Even though the world has almost returned to normal, in-person shopping may not be something many consumers want to return to. The convenience of delivery is just too hard to ignore.

Technavio has been monitoring the online grocery delivery services market and it is poised to grow by $631.84 billion during 2020-2024, progressing at a CAGR of almost 29% during the forecast period.

TWOH - Trading on the Canadian CSE Now!

TWOH announced in August that it had received approval from the Canadian Securities Exchange (the "CSE") to list its common shares on the CSE.

A dual listing gives TWOH even more presence in the world for investors to discover their offerings.

“As we shift to solely focus our attention on the food industry and align with our customers' needs, we are confident we will unlock the current growth potential that exists in the market.”

- Nadav Elituv, CEO of Two Hands Corporation

THE BOTTOM LINE

There looks to be no end in sight yet for the food delivery and grocery delivery space.

TWOH is in a gold mine of an arena considering how consumers are opting to stay more inside and do their shopping with ease from their computers and smart phones.

With a 52-week high of over $3, the upside potential is a beast for the stock at over 2,700%!

While the price of food and groceries is on the rise, there may be an opportunity to offset your next bill by looking at food stocks like TWOH who may be trading at a discount.

This little-known company has a current "STAY LONG" rating and has been rallying over 100% this month! Bigger gains could be imminent!

Warm Regards,

Alexander Reeves

PennyPicks.net

Still need an Online Broker to place trades?

RobinHood doesn't let you trade Penny Stocks!

etrade

Our Team HIGHLY recommends ETRADE!

IO

Home | Twitter | Disclaimer | Contact | UNSUBSCRIBE | View in Browser

Disclaimer – Always do your own research and consult with a licensed investment professional before investing. This communication is never to be used as the basis of making investment decisions and is for entertainment purposes only. At most, this communication should serve only as a starting point to do your own research and consult with a licensed professional regarding the companies profiled and discussed. Conduct your own research. This newsletter is a paid advertisement, not a recommendation nor an offer to buy or sell securities. This newsletter is owned, operated, and edited by Stellar Media Group, LLC. Any wording found in this e-mail or disclaimer referencing to “I” or “we” or “our” or “Stellar Media” refers to Stellar Media Group, LLC. Our business model is to be financially compensated to market and promote small public companies. By reading our newsletter and our website you agree to the terms of our disclaimer, which are subject to change at any time. We are not registered or licensed in any jurisdiction whatsoever to provide investing advice or anything of an advisory or consultancy nature and are therefore are unqualified to give investment recommendations. Companies with low prices per share are speculative and carry a high degree of risk, so only invest what you can afford to lose. By using our service you agree not to hold our site, its editor’s, owners, or staff liable for any damages, financial or otherwise, that may occur due to any action you may take based on the information contained within our newsletters or on our website. We do not advise any reader to take any specific action. Losses can be larger than expected if the company experiences any problems with liquidity or wide spreads. Our website and newsletter are for entertainment purposes only. Never invest purely based on our alerts. Gains mentioned in our newsletter and on our website may be based on end-of-day or intraday data. This publication and its owners and affiliates may hold positions in the securities mentioned in our alerts, which we may sell at any time without notice to our subscribers, which may have a negative impact on share prices. If we own any shares we will list the information relevant to the stock and the number of shares here. We do not own any shares in TWOH. We have been compensated $10k via wire by a third party, ACN, LLC., for this communication on TWOH. Stellar Media’s business model is to receive financial compensation to promote public companies. This compensation is a major conflict of interest in our ability to be unbiased regarding our alerts. Therefore, this communication should be viewed as a commercial advertisement only. We have not investigated the background of the hiring third party or parties. The third party, profiled company, or their affiliates likely wish to liquidate shares of the profiled company at or near the time you receive this communication, which has the potential to hurt share prices. Any non-compensated alerts are purely for the purpose of expanding our database for the benefit of our future financially compensated investor relations efforts. Frequently companies profiled in our alerts may experience a large increase in volume and share price during the course of investor relations marketing, which may end as soon as the investor relations marketing ceases. The investor relations marketing may be as brief as one day, after which a large decrease in volume and share price is likely to occur. Our emails may contain forward looking statements, which are not guaranteed to materialize due to a variety of factors. We do not guarantee the timeliness, accuracy, or completeness of the information on our site or in our newsletters. The information in our email newsletters and on our website is believed to be accurate and correct, but has not been independently verified and is not guaranteed to be correct. The information is collected from public sources, such as the profiled company’s website and press releases, but is not researched or verified in any way whatsoever to ensure the publicly available information is correct. Furthermore, Stellar Media often employs independent contractor writers who may make errors when researching information and preparing these communications regarding profiled companies. Independent writers’ works are double-checked and verified before publication, but it is certainly possible for errors or omissions to take place during editing of independent contractor writer’s communications regarding the profiled company(s). You should assume all information in all of our communications is incorrect until you personally verify the information, and again are encouraged to never invest based on the information contained in our written communications. The information in our disclaimers is subject to change at any time without notice.

Unsubscribe

This message was sent to xxxxxxxx@gmail.com from info@pennypicks.net

PENNY PICKS

PENNYPICKS

2035 SUNSET LAKE RD, SUITE B-2

Newark, DE 19702