News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

DartmouthDan

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Obviously they lack the money to pay the State of Nevada the $1,350 that was owed in December 2017.

There are no Prax-Rx products on Amazon.

I know teenage kids who are Amazon sellers.

The BS never ends

It looks like that the officer of record with Nevada when Chen took over was Shahin Tabatabei, at 2724 Otter Creek Court, Apt 101 in Las Vegas, and that was the person served papers on along with the resident agent. So the Balaghi guy never bothered to update Nevada. The last annual report had been filed in 2012.

Been busy lately. All has come to pass as I predicted. Those that listened to me, did not lose as much money. I predicted the stock would be under a penny. I predicted that the whole Mesa Pharmacy was a scam. What happened to the $8 million in stockholder equity and the $60+ million in annual revenue? Bogus. No financial reports have been filed for 18 months. Meanwhile, despite there being no current public information, 80 million more shares were freed up and dumped into the market.

And it was announced in February that the Company has moved to Nevada in order to enjoy larger pharmaceutical facilities.To 61 Spectrum Boulevard. Does not look like there is any larger pharmaceutical facility there. They bought an existing pharmacy for $120,000, but Praxsyn only had $50,000 cash and the rest has to be paid over time. $120,000 will buy you only a very small pharmacy, with 20-30 prescriptions a day and probably less than $100,000 in revenue. And this is a public company that claims $7 million in market cap?

Not long ago I was saying the stock was going sub penny. Not hard to predict; at .0036, its going to be .0001 by year end.

case number A-15-713465-P

In the matter of the petition of Ketcher Industries, LLC

lead attorney Peter L. Chasey

The SEC let their S-1 go effective without review. Such sloppy work

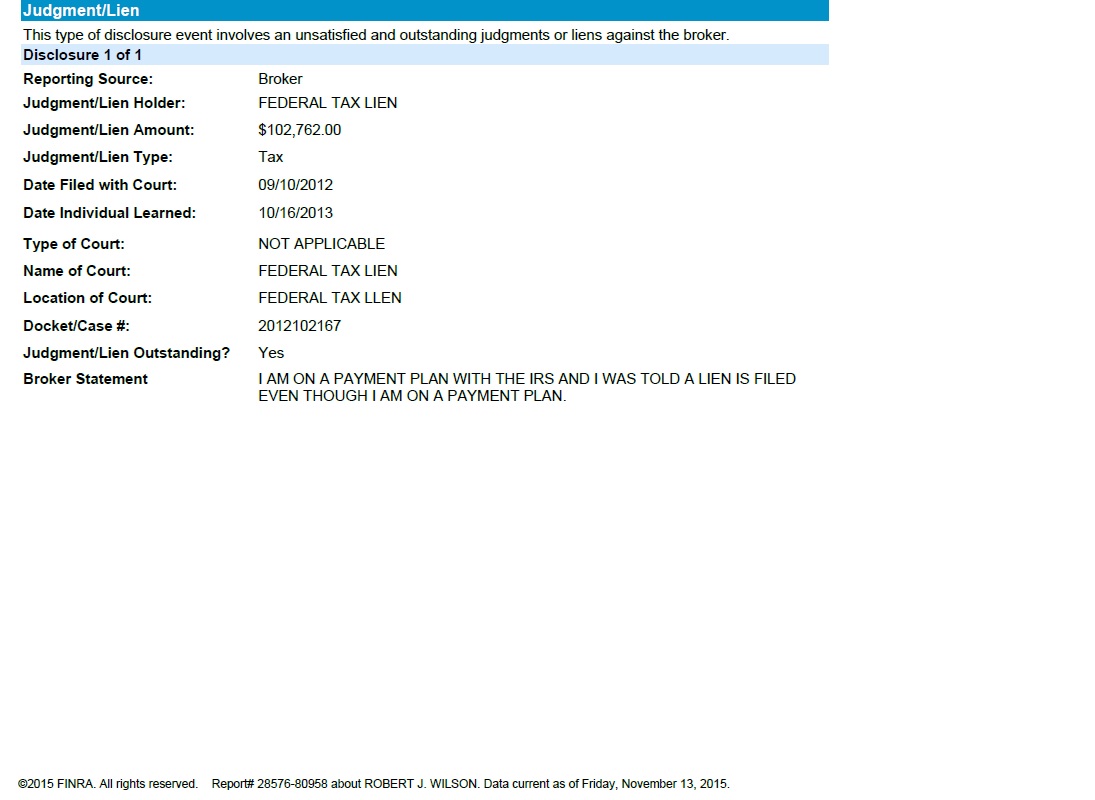

Mr. Robert J.Wilson owes some money to the IRS

$102,700. You can see it on his U-4, on Finra Broker Check CRD 1611118

And he was registered at over 25 firms. Constantly moving. A red flag as they say. And a number of disciplinary actions. My My My.

I do not know what happened but I can give you another chance

I read the motions for summary judgment and I think the shareholder group is going to lose and have to pay a lot of money.

yes they are continuing to get out of this stock asap

new company website nxtn.info

Look at this chart! PXYN just exploding! Insiders know what is happening and they continue to dump.

Series B holders who got 800 million shares, or more than half of the equity, did not pay anything for their shares, according to the 10-K. They received their shares in exchange for Advanced Access Pharmacy which was formed less than two weeks before. Ed is not being truthful in his statement.

We cannot know which of the insiders are holding and which are selling because the company is hiding the ownership of the Series D (Mesa people) and the Series B (the Advanced Access shares given out for 0)

anyway maybe some insiders are not selling yet, but others are as fast as they can

How about this one?

"The agency is still pursuing litigation against stock promoters ____ of Poland and _____ of South Africa, who allegedly made about $4.2 million off the scheme that they deposited into Panamanian accounts the SEC couldn't trace. The two promoters couldn't immediately be reached for comment and the SEC said there are no known attorneys for them. Agency officials believe they aren't in the U.S."

ps. One of the two guys did get apprehended, the other one still out there

Panama has an information exchange treaty with the US now. That is how they nailed them.

It is rumored that the other guy ended up on the bottom of the sea. All the US assets were seized and the perps left 100% penniless. Kind of what will happen here

not only did it trade at a penny that is where the dump happened today, after the 200 share paint yes a $2 trade

173 million shares issued on conversion in the first six months of the year:

During the six months ended June 30, 2015, we issued 461,894 common shares upon the conversion of a portion of a note holder’s 2012 Convertible Promissory Note. See Note 5. In addition, we issued 128,528,000 common shares upon conversion of Series D Shares and 44,200,000 common shares upon conversion of Series B Shares.

This is not a promo job this is a real company. Just look at who is involved.

Listen, nobody really buys $29 worth of stock when the ticket charge is at least $10. It makes no economic sense. And in this stock, it happens many times at the beginning or the end of the day. That points to stock manipulation. Praxsyn is a classic example. I have seen it in my litigation consulting work on stock fraud cases, and Praxsyn is following the stock manipulation program to a "T."

Actually, almost all the sales today were below yesterday's close

The stock was up for the day because someone painted the tape with a $29 order

Investopedia......"

DEFINITION OF 'PAINTING THE TAPE'

A form of market manipulation whereby market players attempt to influence the price of a security by buying and/or selling it among themselves so as to create the appearance of substantial trading activity in the security. Painting the tape is an illegal activity that is prohibited by the Securities and Exchange Commission because it creates an artificial price for a security. The term originated in a bygone era when stock prices were largely transmitted on a "ticker tape."

BREAKING DOWN 'Painting The Tape'

Two common objectives among market manipulators of painting the tape are to lure unsuspecting investors into a security, or achieve a high closing price for it.

Unusual trading volume in a security may attract investors to it. Cabals of market manipulators who have painted the tape in a security generally expect to make significant profits by offloading their holdings in it - which are usually acquired at much lower prices - to investors unaware of the stock manipulation. These investors are literally left "holding the bag" once the manipulation ceases and the stock declines steeply in price.

High closing activity attempts to create an artificial price for a security by boosting its price substantially at market close, since closing prices are widely reported in the media and are closely watched by investors. Since most portfolios and securities are valued on the basis of their closing prices, manipulators use this tactic to achieve a higher market value for their holdings rather than their intrinsic worth.

$29 paint the close today

Down 75% for the year as the "smart money" is dumping hundreds of millions of shares on the unsuspecting rubes.

huge dump at .012. look for another big dump of shares toward the end of the day. These will be shares being sold all day long but the ticket is not issued until the end of the day, so that the price does not get hit during the day.

the big dump late last week freed up money to pay for a program today.

Insiders and shell people know what the future will be, so they are selling asap. Only a couple of years of dumping left

Simple fact day after day is that the big volumes in this stock are all on the lows for the day, and the highs are low volume paints. Indicates that this is a stock that is being dumped.

Can a moderator please put this chart on the main page here?

That is what Shebanow states in his affidavit.

"Rubicon ... ['] only business interests relate to holding Praxsyn Corporation (misnamed as Praxsyn, Inc., also a Nevada corporation) stock and managing that interest. Rubicon was formed expressly to do so."

Then he states that Rubicon received "below market stock" in exchange for the monies he paid on behalf of Rubicon (paragraph 26) and also states that he has a substantial amount of Series B preferred.

So it appears that Advanced Access was only a front to issue shares to parties including Rubicon. Note, that Shebanow's affidavit says nothing about Advanced Access.

As to whether it has been Rubicon's sales or someone else's sales is unknown. But we do know that over 200 million common shares were issued on conversion of Series B and there is little reason to convert unless a holder wants to resell into the market.

LOL LMAO

Under IRC 382,

Praxsyn will only be able to take limited (the percentage is based on the long term tax exempt rate, under 3%) advantage of NOLs from 2014, because of the change in equity ownership percentages resulting from the huge increase in outstanding shares.

so if the 2014 loss is about 12.6 million, that means it can exclude about $400,000 in income using NOLs

But I understand; you did not have the opportunity to spend a semester with Noel Cunningham as I did, and Section 382 is somewhat arcane.

You are correct. I should have added s-k 403(a), which covers Rubicon.

(a) Security ownership of certain beneficial owners. Furnish the following information, as of the most recent practicable date, substantially in the tabular form indicated, with respect to any person (including any “group” as that term is used in section 13(d)(3) of the Exchange Act) who is known to the registrant to be the beneficial owner of more than five percent of any class of the registrant's voting securities. The address given in column (2) may be a business, mailing or residence address. Show in column (3) the total number of shares beneficially owned and in column (4) the percentage of class so owned. Of the number of shares shown in column (3), indicate by footnote or otherwise the amount known to be shares with respect to which such listed beneficial owner has the right to acquire beneficial ownership, as specified in Rule 13d-3(d)(1) under the Exchange Act (§240.13d-3(d)(1) of this chapter).

The Court further stated that its conclusion was supported by its reading of a June 4, 2008 letter from the Deputy Director of the SEC’s Division of Corporate Finance (due to the Court’s timing, the SEC did not have sufficient time to formally submit an amicus brief in response to the Court’s invitation that it do so). While the SEC staff letter stated that “as a general matter, a person that does nothing more than enter into an equity swap should not be found to have engaged in an evasion of the reporting requirements,” the Court found that TCI did more than just enter into an equity swap since, at the very least, it entered into the equity swaps for the purpose of avoiding the disclosure requirements of Section 13(d). The Court interpreted a statement in the SEC staff’s letter that “a person who entered into a swap would be a beneficial owner under Rule 13d-3(b) if it were determined that the person did so with the intent to create the false appearance of non-ownership of a security” as merely illustrating a specific intent that would satisfy the standard under the rule, but not as limiting the situations where the rule would apply. In light of this, the Court found that Rule 13d-3(b) applies where an investor enters into a transaction with the intent to create the false appearance that there is no large accumulation of securities that might have a potential for shifting corporate control by evading the disclosure requirements of Section 13(d) or (g) by preventing the vesting of beneficial ownership in the investor. Thus, the Court found that, under Rule 13d-3(b), TCI was deemed to be the beneficial owner of shares held by its counterparties to hedge the equity swaps.

I think you need to look at that balance sheet again.

The amount of cash is not $5 million, it is $4.8. And there is no additional $3 million or so in cash "set aside" for taxes. The $3,095,000 in accrued taxes has to be paid by June 15 (for amounts accrued by May 31) or Sept. 15. Praxsyn is just floating the money, and if it is not paid with the estimated tax bill it will need to pay a penalty to the IRS and the California FTB.

As of June 30, Praxsyn has a working capital (current assets minus current liability) deficit of $ 8 million. That means that unless it raises money, it will not be able to pay its debts when then come due. This is the definition of equitable insolvency.

If three of Praxsyn's creditors filed chapter 11 on them, Praxsyn as of June 30 would be adjudged a bankrupt.

Lets chart it out, working backwards

Date CA CL Ratio

June 30 13 million 20 million 6.5 to 1

March 31 14.5 18.9 7.6 to 1

Dec 31 11.5 14.8 7.8 to 1

Sept 30 11.7 16.4 7.1 to 1

June 30 9.1 12.6 7.2 to 1

The conclusions: the financial situation under the "preapproved" receivables is worse than under the TPS business model

AND

Praxsyn is headed for a crash.

But don't believe just me. Believe what management has to say in the June 10-Q. Substantial doubt about continuing in business unless they can raise money. If not, the doo doo will get deep, and fast.

Going Concern

The accompanying consolidated financial statements have been prepared assuming that we will continue as a going concern. During the six-month periods ended June 30, 2015 and 2014, we generated net income of $3,954,656 and incurred a net loss of $12,793,324, respectively. The 2014 net loss contained stock-based expenses and a warrant modification expense, all of which were one-time expenses, totaling $16,012,011. At June 30, 2015, we had negative working capital of $6,478,085. Historically, we have funded operations primarily through proceeds received (a) in connection with factoring of accounts receivable on a nonrecourse basis for non-pre-approved billings, (b) through issuances of notes payable, and (c) through sales of common stock. Prior to 2015, our business has been concentrated in workers’ compensation billings which were not pre-approved and for which the collection would be delayed for long periods of time depending on various factors. In 2015, we have added a significant amount of business for which billings were pre-approved by the insurance carriers. We have been, and continue to be, dependent upon a few third party marketing services and we derive almost 100% of our revenues from customers referred by these marketing services. While Management believes the addition of pre-approved billings business will improve our operating performance, we understand that we will need additional financing, including accounts receivable factoring for non-pre-approved billings, to be able to fully implement our business plan. Given the indicators described above, there is substantial doubt about our ability to continue as a going concern.

Here are some questions for PXYN Management, in light of Mr. Shebanow's Federal court affidavit Any person who, directly or indirectly, creates or uses a trust, proxy, power of attorney, pooling arrangement or any other contract, arrangement, or device with the purpose of effect of divesting such person of beneficial ownership of a security or preventing the vesting of such beneficial ownership as part of a plan or scheme to evade the reporting requirements of section 13(d) or (g) of the Act shall be deemed for purposes of such sections to be the beneficial owner of such security.

1. Why is Shebanow's "substantial" share ownership hidden? What is he trying to hide? He says he owns a substantial number of Series B. He says that in an affidavit under penalty of perjury filed in Federal court. So one has to believe that Shebanow really said it. Why isn't his share ownership and the proxy to Kurtz disclosed? Why isn't the voting agreement filed by Praxsyn, as required by law? How is it that he got Series B when the Series B was issued to the Advanced Access members? You know, the ones that had a plan to get into the pharmacy business and 16 days after organization, they received a majority of Praxsyn's equity? I don't see any pharmacy in Shebanow's background. I see a lot of penny stock investing deals, though. It looks like he got his Series B for getting the company going again. Paying its transfer agent etc or whatever. Not by starting up Advanced Access. So that means the Advanced Access "deal" was just a fake deal to get people free stock. Can you give me a reason not to believe this?

2. Shebanow agreed to restrict the conversion of his Series B preferred to under 5% of the outstanding common. This a scheme to evade disclosure under Rule 13d-3(b)? Looks very clear that it is.

3. Attached to the TPS complaint is an email dated January 13, 2013 from John Garbino to John Shebanow asking "where do we stand with the agreement?"

apparently referring to a revision of the TPS agreement

and then a return email to John Garbino dated January 13, 2015 stating "My draft is mostly done, but what I do not have are the current deal points. They were revised as of your last couple of meetings (both with and without David and Ray) and I need a written summary from you or Ed so I can mesh them up with my previous draft."

Why is John Shebanow, who has gone to some trouble to not appear as a control person, drafting the revised agreement with the company's biggest source of business? Doesn't that seem to indicate that maybe he is running the company too? That he is a control person? If you read Shebanow's affidavit you will notice he is not a literate person. There are spelling and grammar mistakes everywhere. So please don't try to tell me he is just a scrivener.

4. if it were just Garbino saying that Shebanow is the real power at Praxsyn maybe it could be discounted, but Bellevue also claims the same thing in the Arizona lawsuit. Unless you can tell me they are in league with each other, it looks pretty persuasive to me.

5. How is it that Evon Midei is the manager of the LLC Advanced Access, which received 80,000 shares of Series B Preferred, yet the 10-K does not disclose that he received or owned any shares.

6. Seems to me that if Garbino can show he was negotiating a new agreement with Praxsyn, his complaint that he was induced to give up his series D in order to get something in exchange has legs? How do you explain this away? If Garbino was such a fraud, why was Praxsyn trying to make a new deal with him?

7.Why doesn't Praxsyn come out and say who is converting stock and selling? wouldn't that be transparent?

Based on these trends, the stock will be $.002 a year from now.

Yes definitely a winner here on our hands.

Maybe you could convince the Praxsyn insiders, you know, the ones that got the stock for $0 per share through the Series B, for example to believe you? because they do not believe you, they keep on dumping and neither does anyone else believe you.

You seem to have information not known to the public. who is the "related party" who loaned the money?

Lets see what cash Praxsyn claimed it had (all based on 10-Qs)

March 2014* 819,996

June 2014 518,550

September 2014 593,251

Dec. 2014 1,222,084

Mar. 2015 1,896,910

Why did it take Praxsyn so long to repay this convertible note? It was on extremely bad terms for Praxsyn. Because Praxsyn is cash poor. Even though the June 30 balance looks good, Praxsyn still has to factor its receivables and is paying a discount of more than 50%. (they had a loss of 3.6 million on sales to factors and 3.2 million realized in cash from the sales in the 6 months ended 6/15). That is a HUGE finance rate. Why doesn't anyone want to invest in Praxsyn's (pre-approved) receivables?

because they are poor quality.

Because Praxsyn somehow manages to rip off people and as a result gets sued all the time

Because Praxsyn's accounts receivable management does a crummy job.

See where this is going? the faster they may try to "grow" the worse it gets. But they have to post revenue to support the stock dumping.

* according to the March 2014 10q, this note, dated March 5, 2014, was convertible into 260 shares of Series B stock (2.6 million shares, worth .11 per share, or $286,000. A five-fold return. Praxsyn must have been desperate for cash then. Somehow this disclosure about the conversion rights got dropped from the June 15 q disclosure.So what? what is the point of telling the truth?

8 separate judgment liens on record in Florida against good old Henry Fong. There must be a line of sheriffs in front of his house, waiting their turn.

and 5 judgment liens recorded against FFFC.

Yeah they took Henry's wedding ring too. Do you think they will let FFFC keep 420 ? No. If they have not already, Grace will start banging FFFC's bank account.

[ONE PIANO,ONE PIANO BENCH,ONE WOODEN CABINET,ONE WOODEN STAND,ONE SILVER SILVER MENS'S WATCH WITH GREEN DIAL (MARKED "ROLEX SUBMARINER")AND ONE MEN'S(TRIPLE RING)WEDDING BAND(GOLD COLORED METAL)]

in order to satisfy a certain Judgement entered in this cause on the 31st day of March, in the sum of $1,001,092.90, with interest from that date and for the costs of this levy. If not satisfied, the aforesaid property shall be sold by me according to law.

Ric L. Bradshaw, Sheriff

Palm Beach County, Florida

By Sgt. Johnny Ortiz

Court Services Bureau

Every post is numbered. Go to post 42298 and follow that thread. Or you can use the internet and look at the Palm Beach County Court records and see the actual sheriff's report online. You can also see there where the judgment was domesticated in Florida.

While you are at it, look at all the other judgments against Mr. Fong. And see the creditors are taking his deposition every few months to see what he has and what his buddies, who also have judgments against them for stock scams, have. Its all public record there.

You can look at sunbiz.org and see the judgment lien was filed in Florida

You can look at PACER and see the original case and the judgment against Fong and FFFC.

You can look in the last 10-Q of FFFC where the Grace Capital judgment is reported and reserved against. That is why FFFC is in the hole I think $11 million dollars.

You can look on the Nevada Secretary of State's website and see that FFFC is in default to the tune of $5,750.

Also you can look at a chart of this stock and see it follows the same pattern every other Fong deal has exhibited. Why would you expect him to change?

It was posted here a while back. the sheriff's report showed what had been taken from Fong to pay Grace Capital.Post 42298

Now, look at this interesting disclosure in the June 10-Q.

Why, if the company has so much cash and is doing so well, did they have to borrow $42,500 from a related party? And then not be able to repay it on time? By the way, why are we not told who this party is?

The obvious truth is that notwithstanding the big cash balance as of June 30, 2015, the company is always on the edge, hurting for cash.

On March 5, 2014, we issued a convertible note in the amount of $42,500 to a shareholder who is also a related party. The convertible note, which had a stated interest rate of 6% per annum, was to be repaid in April 2014 and became past due. At March 31, 2015 and December 31, 2014, the total principal amount outstanding for this note was $52,400. On April 10, 2015, we entered into a settlement agreement with the note holder under which we repaid this note, including all accrued interest, for a payment totaling $42,500. In connection with this repayment, we recorded a gain on extinguishment of debt in the amount of $14,359 during the three and six months ended June 30, 2015.

I don't see the company claiming 20 million in annual profits. The promoters did that on their last company and it got suspended. From the last 10-Q:

While Management believes that our new pre-approved business will greatly improve our operating performance, we understand that we will need additional financing to be able to implement our business plan. Further, due to market developments in relation to preapproved claims, we anticipate that revenues may decrease overall in the subsequent periods.

Grace Capital just took Henry's piano bench. They are also going to take the company's cash, its ownership of CFMS and 420 and anything else that comes in the door, including convertible loans. I would not doubt if FFFC goes into receivership