News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Bootz

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

$treet King, do you really need four posts to cover that territory?

Wouldn't one do?

Well, yes, that would be the "plan."

No official date yet. Current best guess seems to be Tuesday, January 24th.

Keep checking here:

http://investor.apple.com/

How do you figure that the Galaxy has "a few more apps available" than the iPad?

It's the other way around, and not likely to change anytime soon.

Oh I forgot, you are a fanboi at all cost.

Is that anything like being a Troll at all cost?

Just curious.

Apple: J.P. Morgan Lifts Ests; Sees More iPhones, Fewer iPads

J.P. Morgan analyst Mark Moskowitz this morning raised his estimates for Apple for the December quarter, reflecting a higher forecast for iPhone sales, offset in part by a reduced outlook for iPad sales. The analyst maintains his Overweight rating and $525 price target.

“Our research inputs indicate that iPhone sales remain robust, and Mac sales holding up,” he writes in a research note. “The thrust of our call is that we are increasing iPhone estimates but slightly trimming our iPad estimates. Despite the uncertain macro environment, we expect Apple to sustain above-peer revenue growth, upward-trending margins, and incremental market penetration opportunities to fend off competitive and economic challenges.”

For the quarter, he now sees revenue of $38.69 billion and profits of $9.87 a share, up from $37.26 billion and $9.45. Street consensus is $38.02 billion and $9.78. His new gross margin forecast is 40.7%, up from 40.4%; operating margin goes to 31.6%, from 31.4%.

He now sees sales of 28 million iPhones in the quarter, up from 25.3 million previously. His fiscal 2012 forecast is now 105.5 million, up 4.2 million; for 2013 he goes to 121.7 million, up 1.5 million.

For iPads, his new forecast is 13 million, down from 13.3 million. “We see no structural change to the iPad demand environment, but there has been limited uplift in build activity,” he writes. “To a lesser extent, the Amazon Kindle Fire’s better-than-expected momentum with more price sensitive consumers is a factor, too. Longer-term, we still expect the iPad’s ongoing momentum in commercial environments to accelerate.”

For the Mac, he continues to see 5.4 million units in the quarter. “Our conversations with industry participants suggest that MacBook Air momentum continues, and we do not anticipate major competition from Ultrabooks, yet,” he writes. “Also, we do not expect Apple to be impacted by the HDD shortage impacting the broader PC market as we expect whitebox makers to bear the brunt of any HDD supply shortages.”

3 Reasons Apple (AAPL) Shares Are So Cheap

Though a long-time market darling, the reality is Apple's (AAPL) stock remains one of the cheapest of the major tech names on a relative basis. Despite exactly one earnings miss in 7 years Apple now trades at 13x earnings; less than half its multiple of 32x two years ago. "It makes no sense to me, frankly," says Reuters Blogger Felix Salmon.

Perhaps most baffling to Salmon is Apple's valuation relative to other tech stalwarts. "There are four big companies on the Internet: Amazon (AMZN), Google (GOOG), Microsoft (MSFT), and Apple," he says. "Maybe Facebook when it goes public next year." And he points to Amazon which is trading at 90x earnings and questions "Why would you pay 90x earnings for Amazon when you can pay 13x for Apple?"

Salmon has answers and causes, both real and imagined for Apple's relative discount.

(1) The Law of Large Numbers: When a company has a market cap of some $350 billion dollars it simply becomes impossible to move the needle in terms of paying up. Everyone who wants Apple has managed to buy it over the last decade. The bears have been devastated. Once both sides of a trade have made up their mind about a company it's hard to get the market to change its mind.

(2) Slowing Growth: Typically a discount valuation means investors are expecting slower growth. Salmon says Apple's pipeline is robust enough to make such worries illusory. The vast majority of the world has neither a smartphone nor a Mac. This leads Salmon to believes there's "as much growth potential or more growth potential for Apple than there's ever been."

(3) Leadership: Tim Cook is by all accounts tremendously gifted from an operational side. But where Apple really excels is in product design. It's going to take years for Apple to prove that their gift for knowing what customers want before they even know they want it is legendary. The late Steve Jobs will get credit for new Apple products for years to come, making it impossible to restore faith in the Apple development machine. Salmon says Cook "still has Johnny Ives, he still has all of Apple's great design, he still has exactly the same pipeline. He still should be given some kind of benefit of the doubt."

Television and the cloud have been relative failures for Apple so far. While rumors are rampant that Apple, Google and virtually everyone else is coming out with revamp sets for next year, there are no hints at exactly what those products are going to look like. They better be good if Apple hopes to assuage the fears limiting multiple expansion.

Despite the strength of Apple's stock over the last decade it would trade near $900 if it still had a P/E of 32x. There's something going on there.

ace, and still Android is a 3rd rate experience:

http://thenextweb.com/microsoft/2011/11/13/nokia-lumia-800-the-first-device-that-would-make-me-give-up-the-iphone/

And you didn't take any of the other patents into account.

And why, pray tell, would you think they wouldn't?

If you're looking for Bloated Pig, maybe you should check out the AMZN board.

90 PE ratio?

Compare that to Apple's PE and tell me again who's bloated.

Only if you take it with you when you travel.

And the plural of PC is PCs, not PC's, Macs not Mac's.

You didn't.

The world is changing.

Get used to it.

iPad 3 could make Apple the world's top PC vendor next year

by Lance Whitney November 22, 2011 5:55 AM PST

Apple's iPad

(Credit: James Martin/CNET)

Apple is likely to outshine Hewlett-Packard as the world's top PC maker before the second half of next year, says research firm Canalys, but it'll need some help from the iPad 3.

Currently the world's second-leading PC vendor, Apple has seen its share of the market jump to 15 percent from 9 percent over just the past year. That growth is largely due to heavy demand for the iPad, which Canalys considers a personal computer.

But fourth-quarter iPad shipments in the U.S. may take a hit from Amazon's Kindle Fire and Barnes & Noble's Nook tablets, which are launching at consumer-friendly prices. As a result, Canalys believes that HP and Apple will duke it out for the top spot this quarter but that Apple will ultimately grab the lead after the iPad 3 debuts next year.

Rival tablet makers are still fighting to compete with Apple, with many starting to get the hint by selling devices at cheaper prices. The debut of Android 4.0, aka Ice Cream Sandwich, should help Android vendors as developers can finally push their existing smartphone apps to run on tablets. But the timing of updated Android operating system is less than ideal, says Canalys.

Most tablets being sold during the holiday-shopping season will still sport some version of Android 3.x. And Android hasn't been known for a speedy upgrade cycle. Savvy consumers waiting for devices equipped with Ice Cream Sandwich may actually put off purchases until next year when the newest version of Android becomes more prevalent.

Notebook sales have also provided a boost to the PC market this year, with total shipments projected to reach 211 million, a 10 percent gain from last year. Ultrabooks, which are thin, light, high-powered laptops, could spur notebooks sales over the next five years. But Canalys believes prices would have to creep down sharply.For 2011, global PC shipments are expected to reach 415 million, a 15 percent gain from last year, thanks mostly to higher tablet sales. Total tablet shipments are expected to hit 59 million for the entire year, including 22 million in the fourth quarter, says Canalys.

"The least expensive models are currently around $800, a real barrier to mass consumer uptake," Canalys analyst Michael Kauh said in a statement. "As more vendors embrace the ultrabook design, component costs should drop and mainstream consumer prices will be achieved."

The amazin' elastic iPhone 3GS

By Philip Elmer-DeWitt November 22, 2011: 7:06 AM ET

Who gets hurt most by Apple's entry into the $250-$400 mobile phone market?

In a 36-page report to clients issued Monday, a Credit Suisse team led by Kulbinder Garcha took a close look at the iPhone's price elasticity -- Econ 101 jargon for the question: "If I lower the price of my widget, how many more will I sell?"

Garcha et al.'s focus is the iPhone 3GS, which Apple (AAPL) last month began offering to its partners for an ASP (average selling price) of $325, allowing the likes of AT&T (T), Vodafone (VOD) and Rogers (RCI) to give it to customers at subsidized prices ranging from $0.99 to $0.00.

It also marked Apple's entry into what Credit Suisse believes is the sweet spot for mobile phone growth -- the $250-$400 (to carrier) price range, where Apple's competitors do most of their business.

How does this change the competitive landscape? According to Credit Suisse:

Apple has an 85% share of the $500+ market and a 50% share of the $400+ market, but nothing to speak of, before the 3GS price cut, in the $250-$400 range.

The $250-$400 slice of smartphone market is expected to grow 80% over the next four years, from 119 million to 213 million.

Apple is well positioned to capture 25% of that market, putting more pressure on competitors whose margins are already being squeezed.

HTC and Samsung are the most exposed, with a 22% and 20% share, respectively, of the $250-$400 market.

The impact, according to this report, could be most severe on Research in Motion (RIMM) "given ongoing concerns around its product portfolio."

On Monday, Credit Suisse lowered its price target for RIM from $30 to $20.

Its price target for Apple is $500. On Friday, when Garcha et al. wrote their report, Apple was trading at $374.94 with a 9.6 forward P/E they found "compelling" given the rate at which Apple's earnings are growing. The stock closed Monday at $369.01.

Amazon is a marketing gorilla and with a price of $199 they will take IPAD business away or make Apple lower the price.

No. They. Won't.

The Kindle Fire was touted as the next/newest iPad killer.

It's not.

Not by a long shot.

There's no Fire there.

Cold Water On The Kindle "Fire"

Is It Worth It?

JH: I don’t want to overcorrect for other reviewers, but I think people are giving this device—and Amazon—too much credit. I don’t think it’s a good product. I know it’s $300 less than an iPad, and I know it technically does many of the same things, but we’re not talking about laptops here.

A $400 laptop that can do most of what a $1000 laptop can do is a good value proposition, because people need laptops. They’re tools. Tablets are for leisure—for goofing around. And $200 isn’t a better deal than $500 if all you end up with is a frustrating device you don’t want to use. It’s just a waste of $200.

And I say this as a total nerd. I’ve got a lot of patience for shoddy UIs and software quirks. I’m actually a little sad for the people who preordered this thing for friends, family, or themselves. I think they’re expecting—and were led to expect—something that they’re not going to get.

GD: I’m disappointed, too, because I was expecting the device to deliver on the high-performance promise of that opening screen, and I don’t think it does. So, even at the impulse-buy price of $199, I still can’t suggest that people go out and buy this device today.

Read more: Hands-on With the Amazon Kindle Fire - Popular Mechanics

http://www.popularmechanics.com/technology/gadgets/reviews/hands-on-with-the-kindle-fire-6562321?click=pm_latest

You get what you pay for.

Did HP hire some Samsung engineers?

I mean, where else would this design have come from?

"HP Envy"

At least they got the name right.

Why would Apple want to move its prices higher on anything?

I believe you can get a 3GS iPhone now for $99 and Amazon pricing had nothing to do with that.

The Kindle Fire is not an iPad -- not even close. You get what you pay for.

With Kindle Fire you get what you pay for...

Hardware

The Fire’s hardware is plain and clunky. It’s a thick black box with zero style. There isn’t even a volume control or a physical home button, and the on/off button is a small thing hidden inconveniently on the bottom edge.

In the quest to meet the $199 price point, Amazon omitted many features common on other tablets. There are no cameras or microphone, no GPS for determining your location, no Bluetooth for headsets or wireless speakers and no included earbuds. The Fire is Wi-Fi only—it has no built-in cellular connectivity.There isn’t even an included cable for connecting to a computer, something you may want to do to get photos into the Fire, since Amazon lacks an online photo service.

There is just 8 gigabytes of memory, half the total of the base iPad or the Nook Tablet, and only about 6 gigabytes of that is available to store content. If you want to download movies, you won’t be able to fit many into the Fire.

User Interface

When I first saw it, I really liked the Fire’s user interface. Instead of screens full of icons or folders, it presents virtual shelves filled with the books, magazines, music, TV shows, movies, apps and websites you’ve used. A large one has the most recent items, with smaller shelves below it. These are for your favorite items. Across the top is a search bar and a list of categories, like Books, Music, Videos, Apps.

But I became frustrated with the interface. There’s something off with the touch calibration on the top shelf, or Carousel, which scrolls through a seemingly endless stream of items. It can be difficult to get it to stop on the item you want and it takes more pressure than it should to open the selection.

Also, you can’t configure the main screen much. You can’t reorder the top shelf, and while you can place items on the favorites shelves, they are in the order you added them, not how you like them.

http://allthingsd.com/20111115/kindle-fire-a-grown-up-e-reader-withtablet-spark/?mod=tweet

Barclays: Expect iPad 4Q Growth, iPhone Strength

By Dimitra DeFotis

On a day when Research in Motion (RIMM) added two new Blackberries to its ranks, Barclays says there’s too much fuss about the fate of Apple.

Analysts at Barclays think shares of Apple (AAPL) have more than 40% upside to their target of $555. The stock is up 2% today, or $8.29, to $387.56.

Analysts Ben A. Reitzes and Jennifer Thorwart say Apple’s market cap will rise “as it extracts more profits out of the traditional PC and mobile phone industries” and that Apple will still see sales growth in iPads, sequentially in the fourth quarter, based on supply chain patterns. Regarding share underperformance due to iPad and iPhone concerns, the duo says worries about iPad demand/build “have some merit, but are not a long-term problem and the iPhone concerns seem overblown.” To wit:

“While iPad estimates lack upside and have even some modest downside, we believe Apple still has significant holiday momentum with the iPhone, Macs and in China. Also, the jury is still out on the Amazon Fire [Amazon.com (AMZN)]. We believe the iPad still stands out as the industry standard in terms of software integration. Some of the early reviews for the Fire are less than flattering. We believe that iPad is set for a new product cycle in fiscal 2012, which will re-accelerate the category. …One thing seems universal from our extensive checks and conversations with colleagues – the iPhone demand still seems quite strong. Checks still show regular daily stock-outs of the 4S at Apple stores in the U.S. Internationally, signs show strong demand, especially in China. We believe some of the concerns around iPhone stem from order cuts for Japanese based suppliers for Flexible Printed Circuit Boards with facilities in Thailand …The real concern for iPhone may be the pace of C1Q12 builds and product momentum. Right now, based on conversations with colleagues, we expect production to fall in C1Q12 – but more in the older models than the new 4S.”

Mac Attack: Mac Sales Headed for New Record

http://finance.yahoo.com/news/Mac-Attack-Mac-Sales-Headed-allthingsd-812687914.html?x=0&l=1

By John Paczkowski | AllThingsD

The Mac is on track for another one of those “best quarters ever” — better even than the fourth quarter during which Apple reported Mac sales of 4.89 million.

The machine is on a real growth tear. New metrics from research outfit NPD show Mac sales up 19 percent year-over-year in October.

That upward trend bodes well for the company as it heads into the holiday shopping season. Indeed, extrapolating from those numbers, Piper Jaffray analyst Gene Munster figures Apple will sell between 5.1 million and 5.3 million Macs during the December quarter, accounting for about 18 percent of overall revenue for the period.

That’s year-over year growth of between 23 percent and 28 percent. Impressive. More so, considering the state of the PC market, which these days is suffering from slowing sales growth.

You'd think someone with God-given talent would have seen this coming...

Amazon's Kindle Fire no iPad: Review

Puget Sound Business Journal

Date: Monday, November 14, 2011, 5:39am PST

The reviews for Amazon.com Inc. 's new Kindle Fire tablet are coming in and, in short, prepare customers that the Fire is no replacement for Apple Inc. 's iPad.

The New York Times' review states that the Kindle Fire needs more "polish" and "its software gremlins will drive you nuts" but if your prime tablet need is for an e-reader device to read books, then "Amazon’s refined, dirt-cheap Kindle and Kindle Touch are no-brainers"

Mac see a 20% increase in sales in Europe vs -11% decline for PCs - Gartner

Apple up in Europe, despite wider PC sales decline

By Darrell Etherington Nov. 14, 2011, 6:26am PT

PC shipments were down in Western Europe, dropping over 11 percent during the third quarter of 2011 vs. the same period a year ago according to Gartner. Total shipments for the quarter were 14.8 million total, down from 16.7 million, but Apple bucked the trend and saw a nearly 20 percent increase in shipments year over year.

One of the biggest hits the market took in general was a 40 percent decline in mini notebook (including netbook) shipments. Gartner doesn’t include tablets in its PC shipment outlooks, but it’s very possible the iPad could’ve been a considerable factor in that precipitous drop. Even without the iPad included, Apple still saw a 19.6 percent growth in its computer shipments between the third quarter of 2010 and the same period in 2011. Shipments grew from 947,000 in Q3 2010 to 1.13 million in Q3 2011, and Apple’s market share jumped from 5.7 to 7.6 percent, thanks to the declining fortunes of other PC manufacturers.

A big part of Apple’s success had to do with its performance in the U.K. market, where it chalked up 21.8 percent growth overall measured against the year-ago quarter, and increased its market share from 5.7 to 7.8 percent. In the U.K., Apple also saw its biggest competition in the PC space come from the same manufacturer currently challenging it most in smartphones and tablets: Samsung. Samsung experienced a huge 39 percent growth overall in the U.K., with its share jumping from 4.7 percent to just under Apple’s at 7.3 percent.

Apple is fourth overall in sales in the U.K., but third-placed Acer saw its shipments drop by a massive 53.1 percent in shipments, so Apple could easily move up the rankings next time around if it can keep Samsung at bay. In Western Europe as a whole, Apple came in fifth, but again, Acer, which ranked second, posted a nearly 50 percent drop in overall shipments, while fourth place Dell shrank 10 percent, too.

http://gigaom.com/apple/apple-up-in-europe-despite-wider-pc-sales-decline/

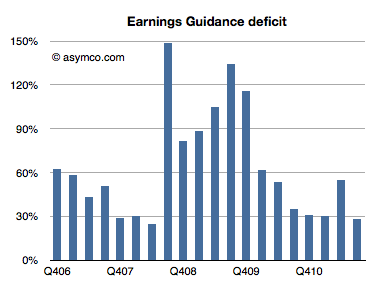

Apple’s Guidance Deficits

NOV 13, ’11 10:50 AM

Horace Dediu

Every quarter Apple’s management issues a “guidance” or forecast of their own earnings in the following quarter. Over the years, this figure has been nearly useless because not only is it not accurate, the error itself has been wildly variable. I plotted what I call the Earnings Guidance Deficit for Apple based on the formula (Actual EPS diluted – Guidance)/Guidance.

The higher the value in the bars above, the more the company underestimated (or under forecast) its performance. Note that during the recession the company routinely offered guidance at half the level they actually delivered. After the recession they returned to a more reasonable ~30% under-reporting.

The problem with this analysis is that there is such a high volatility in this factor that we can’t count on it to predict where earnings will fall. Even if we saw a range bounded at 30% to 60% the usefulness of this would be very low as that is far worse than the range that analysts can get through other means (Deagol’s accounting of analyst error). The best thing we can say is that the range seems to be bounded by 30% and 150%.

Rather than using this history for precision, perhaps it makes more sense to assume that the lower bound offers at least some limit to the possible value of next quarter’s earnings. Maybe it can give us a “sanity check” for our own estimates.

For the next quarter Apple guided $9.30 per share. If we assume a 27% “deficit” which is at the lower end of the range above then the earnings are likely to be about $11.8.

That’s equivalent to an 84% growth in earnings year/year. It would also imply $33 for the 2011 calendar year. At the current share price of $384 that implies a P/E of 11. That happens to also be the P/E for Apple at the trough of the recession in January 2009.

In other words, if the stock price does not rise (or falls) from the current level by the time earnings are reported in late January, then the P/E for Apple may drop to less than 11 on growth of 83%. That’s a sanity check all of its own.

Flash goes out swinging...

Er...singing.

Massive crowds gather in Hong Kong for iPhone 4S launch

By Philip Elmer-DeWitt November 10, 2011: 3:59 PM ET

Police were called in Wednesday to restore order after fighting broke out

Funneling line-sitters into holding pens. Image: Andrew Leyden

"I can't begin to accurately describe the scene on the walkways outside the Hong Kong Apple Store."

So begins the dispatch by Penguin Six's Andrew Leyden writing 24 hours before the first scheduled launch of Apple's (AAPL) iPhone 4S in China.

According to Leyden, police broke up a disorganized mob of 400 line sitters Wednesday night amid rising tensions and scattered fighting. On Thursday, police and security officials, using "crush barricades," forced the crowd into a series of 45 holding pens of 20 sitters each.

"It's not Apple fans at all," Leyden writes in the text accompanying the video posted below. "It's line sitters and smugglers. They'll make $100US per phone, which is a week's wages for some of these low income people. Buy 5 phones and they make a month's salary."

"I'd be shocked ," he concludes, "if the PTU Riot Police is not deployed tomorrow. Should Apple run out of phones, as it appears likely, I would not want to be anywhere near that walkway when the line sitters are told the bad news. 'Ugly' is too polite a word for that scene."

Apple: Baird Sees Q4 iPhone, iPad Units Solid

Posted by Tiernan Ray

RW Baird’s William Power today reiterates an Outperform rating on shares of Apple (AAPL), writing that his visits to retail stores “suggest strong demand” for the company’s iPhone 4S, and that it’s “too early to call” on shipments of Apple’s iPad.

Power reiterates a forecast for 27.2 million iPhone units this quarter and 15 million iPad units.

Baird is no doubt responding to the multiple rumors circulating yesterday and today about Apple cutting production of either or both devices for one reason or another.

Baird doesn’t directly address those rumors, but alludes to them, writing “Given the importance of the holiday selling season, we believe FQ1 iPad shipments are too early to call, though our checks suggest solid overall demand. We do expect the [Amazon.com(AMZN) Kindle, Nook and others to take some share, but continue to forecast strong iPad growth overall.”

AAPL: China Mobile Wants Cut Of App Store, Says Sterne Agee

Posted by Tiernan Ray

Sterne Agee’s Shaw Wu this morning reiterates a Buy rating onApple (AAPL) shares and a $500 price target, writing that “a frequent question we have gotten from investors recently is what are we hearing in terms of progress with China Mobile and the iPhone.”

Wu explains that many customers on the network of China Mobile(CHL), which doesn’t officially carry the iPhone but has 10 million subscribers using it anyway, are simply running the device on WiFior on the older 2G frequency because the iPhone doesn’t yet support China Mobile’s flavor of 3G wireless, the so-called TD-SCDMA.

Despite no official deal, our understanding is that AAPL and China Mobile remain firmly engaged. Our industry sources indicate iPhone prototypes using TD-SCDMA chip sets have been under beta test for some time. But because of the success of iPhone at China Unicom (official carrier partner) and China Mobile (using Wi-Fi), not to mention Greater China including Taiwan and Hong Kong, AAPL is apparently in no rush to produce such a model and may not do so at all. Instead, effort is being focused on developing 4G TD-LTE models.

But the actual sticking point between the companies may be that China Mobile wants some App Store revenue:

our industry sources indicate that one of the reasons why there isn’t an official deal between China Mobile and AAPL is over App Store economics. Today, AAPL does not share revenue with carriers, which has been a source of tension but also accepted. Mobile apps are becoming a very big deal in China and it is understandable why China Mobile wants a bigger piece of the action. We need to see how this plays out but what may help AAPL ironically is the lack of a carrier cut and is one of the key reasons why iOS developers make money while others don’t.

Apple shares today are up $4.97, or 1.2%, at $404.70. China Mobile shares are down 10 cents at $48.52.

Your Apple don't taste like $323, I'll tell you that.

I vote for a couple of aircraft carriers.

Aircraft carriers are really cool!

Why Siri Is a Google Killer

It’s now been a couple of weeks since Siri debuted as part of Apple’s (AAPL) 4S. The response from most people has been very positive.

However, in my opinion, Siri is tremendously under-valued. People see it as it is today, which is already the best voice recognition application in history. But people (including high-priced sell-side Wall Street analysts) fail to see where the puck is going for Siri. Siri will be vastly more improved in as little as 2 years from now. And the boundless number of applications using Siri will explode.

In the way that the January 2007 launch of iPhone set a ripple in the ocean that would eventually overtake Research In Motion (RIMM) in an all-out tsunami, I believe Siri’s launch this month spells a future crippling of Google’s business (GOOG).

Here’s why:

1. Siri works. Voice recognition has been the next big thing for 15 – 20 years. We still have these frustrating experiences when we call into check the balance of our bank account and have to shout in the phone 5 times in a row, because the application doesn’t recognize us. Siri is the best voice rec app ever — and it’s still in “beta.”

2. Siri has personality. Not only does Siri accurately recognize our voices but it has a personality to boot. It’s that personality which makes the app addictive because we start to feel over time that we truly have a personal assistant who is our friend.

3. Siri is hard to copy. For anyone who doesn’t understand voice applications, it’s easy to think that Siri will be easy to copy. It won’t. There are 2 parts to making a successful voice app: the voice rec technology which has improved a lot but is basically a commodity and the app itself, which is a combination of art and artificial intelligence. It’s that 2nd part that’s so tough to replicate and that’s why Apple bought Siri last year. It’s true Google has experience in the voice rec space and doing some simple voice apps but they do not have the personality and AI of Siri and that will be very difficult to copy — especially for a company that doesn’t sit at the intersection of the humanities and technology.

4. Siri helps own the customer experience for Apple. Dan Frommer and others have been talking about this for a long time. Siri is a new interface for customers wanting to get information. It used to be text-based input to their desktops. Then, it was thumbing it in to their mobile devices. Now, Apple is attempting to make it voice-based. They previously were attempting to Balkanize your data needs by training for you to do specialist searches for the information within apps on your iPhone. Now, they’re training you to rely for doing any task by leaning on Siri to do it for you. At the moment, most of us still rely on Google for getting at the info we want. But Siri has a foot in the door and it’s trusting that it will win your confidence over time to do basic info gathering. Siri can be potentially leveraged in other devices that Apple ships in the future like TV to become the primary way you interface with info you need.

5. Siri will vastly improve in the next 2 years based on all the data it’s amassing. This game is about where the puck is going, not where it is today. Many people only look at Siri as the application as it works today. Yet, the biggest advantage over any other voice application out there today, and the apps still to be developed, is the massive data Siri is now and will continue to collect in the next 2 years. We know after the first weekend alone, there were 4 million Siri-enabled devices out there probably collecting 1 – 2 utterances a day worth of data — all being stored in Apple’s massive North Carolina data center. All that data will allow Siri to get better and better. Think Siri has awesomely funny answers to your crazy questions now? Just wait two years. She’ll be even more your friend then, knowing you perhaps better that you know yourself in some situations. Gary Morganthaler – who was an early investor in Nuance (NUAN) and Siri — explains this in the video below:

Video at link:

http://www.forbes.com/sites/ericjackson/2011/10/28/why-siri-is-a-google-killer/

6. When Siri opens up its API to 3rd party developers, this thing’s growth and adoption will go ballistic. At the moment, Siri is in “beta” and no 3rd party app exists. But what happens when you allow developers to write Siri-enabled scripts that tie into their websites – like Yelp, OpenTable, and others? Siri will become even smarter. For users, it will become even more valuable because better and better data results will come back to it. And Apple — as happened in the iPhone and then iPad spaces — will have a huge lead in 3rd party apps tied into this powerful interface.

Ultimately, Siri is a “rich get richer” story. An amazing app today has such a head-start that it will encourage massive adoption, which will allow Scott Forstall and his team at Apple to make it even better with an enormous lead.

When I first heard about Siri, I thought about its similarities to Microsoft’s (MSFT) Kinect – creating a new form of interacting with information. Yet, it’s obviously so much more powerful and universal as an interface compared to hand-waving.

Ultimately, Siri is intended to be a Google killer. It won’t happen overnight. Research in Motion didn’t collapse after the iPhone was released in January 2007. In fact, RIM hit all-time highs 18 months after iPhone’s introduction. It’s only now — 4.5 years after its introduction — that we see how iPhone caused RIM’s slow-motion car crash. It might take that long for Siri to inflict that much harm to Google and Google has lots of cash to throw at the problem. But we might be watching the beginning of the end of Google, thanks to innocuous introduction of Siri in the 4S.

That's really rich for someone who lives and dies by The Register for their anti-Apple venom, er, news.

And we know they never get anything wrong, right?

Meanwhile, if you're really concerned -- which I don't think you are for a minute -- email the guy who did the original graph:

michael@theunderstatement.com

You're welcome.

Microsoft’s Productivity Future Vision ?

According to Gruber:

This video encapsulates everything wrong with Microsoft. Their coolest products are imaginary futuristic bullsheet. Guess what, we’ve all seen Minority Report already. Imagine if they instead spent the effort that went into this movie on making something, you know, real, that you could actually go out and buy and use today.

Hey, acie, long time no see! Wassup?

I figured you'd be busy over on the MSFT board assisting yourself moderate it, but I see there's not much going on there, so no wonder you've got time on your hands.

You're not confusing Siri (a component) with iOS 5 itself are you?

What Android phone are you using, btw?

To their credit, I understand the latest Windows phones are pretty good.

Show 'em the chart from that link, guy!

And this is the kind of stuff that adeezl loves?

December Quarter Guidance since Fiscal 2005

Guidance

F2005 21¢

F2006 46¢

F2007 73¢

F2008 $1.16

F2009 $1.21

F2010 $2.35

F2011 $4.80

F2012 $9.30

Results

F2005 35¢

F2006 65¢

F2007 $1.14

F2008 $1.82 adjusted for change in accounting rules

F2009 $2.50 adjusted for change in accounting rules

F2010 $3.67 adjusted for change in accounting rules

F2011 $6.53

F2012 Pending

Average beat of the non-adjusted quarters: 55%. Range of beat 41% F2006 to 67% F2005. F2007 and F2011 were nearly identical at 56% and 55% respectively. F2011 results came in at exactly the average (to 2 decimal points).

Should 55% beat be used as a historical reference when calculating FQ1/2012 estimates? If so, $9.30 Guidance becomes $14.40 estimate.

http://www.macobserver.com/tmo/forums/viewthread/81736/

Apple updates MacBook Pro with faster processor

Posted on Monday, October 24th, 2011 at 4:28 am. PT

Written by Jim Dalrymple

Apple on Monday updated its MacBook Pro line of notebook computers, adding faster processors and graphics cards.

The 13-inch MacBook Pro now comes with 2.4GHz and 2.8GHz processors, up from 2.3GHz and 2.7GHz in the previous models. The hard drives on these models have also been bumped from 320GB and 500GB to 500GB and 750GB, respectively.

The 15-inch models now feature 2.2GHz and 2.4GHz processors, replacing the 2.0GHz and 2.2GHz processors in the previous models. The graphics cards have also been updated in the 15-inch models — the base model now comes with an AMD Radeon HD 6750M with 512MB GDDR5, while the higher-end model has an AMD Radeon HD 6770M with 1GB GDDR5. The older models used the AMD Radeon HD 6490M and the AMD Radeon HD 6750M.

The new 17-inch MacBook Pro comes with a 2.4GHz processor and the AMD Radeon HD 6770M with 1GB GDDR5, replacing the 2.2GHz processor and AMD Radeon HD 6750M with 1GB GDDR5.

$405.77 is 8th highest close in AAPL history & $12.90 is 10th largest daily $ gain

Is that why we were only up thirteen bucks?