News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Bootz

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Piper Jaffray: 80 million iPhone 5s sales are already "in the bag"

In a survey of 400 consumers, 65% said they expected their next phone to be an iPhone

FORTUNE -- In a note to clients issued Tuesday, Piper Jaffray's Gene Munster reported the results of his annual cell phone survey. The key takeaways:

Asked what phone they were going to buy next, 65% said an Apple (AAPL) iPhone, 19% said a Google (GOOG) Android, 6.5% said "not a smartphone," 6% said "I don't know," and 2.5% said a Research in Motion (RIMM) Blackberry.

51% of respondents who planned on making the iPhone their next smartphone (whether current iPhone users or not) said they were waiting for the iPhone 5.

94.2% of iPhone users plan to buy an iPhone for their next phone, improving upon last year's rate of 93%. If you throw in half of the 2.9% of iPhone owners who were still unsure, the re-buy rate rises to nearly 95.7%.

Android phones were measured at a re-buy rate of 60%, up from 47% last year. "While the improvement is a positive sign," Munster writes, "Android is still losing 33% of current users to the iPhone. We also note that 38% of Blackberry users expect to switch to iPhone."

Asked to put a dollar value on their current phone, iPhone owners' answers averaged $313, more than $100 higher than the device's subsidized price. Android and Blackberry phones had value averages of $220 and $219, respectively.

Shown unlabeled scale drawings of an iPhone and a Droid Razr Maxx, 56% preferred the phone with the smaller screen, which makes one wonder why Apple would want to increase the iPhone 5's screen size, as rumored.

"The iPhone represents 50%+ of Apple's revenue," Muster points out, "making Apple future largely reliant on the success of the iPhone."

But he's not worried. Given the better than 94% re-buy rate and the 51% of all phone owners waiting for the iPhone 5, Munster estimates that more than half of his projected 170 million iPhone sales for fiscal 2013 are already, as he puts it, "in the bag."

The survey gathered responses from 400 people in the U.S. (Minnesota, New York, California) and Asia (China, South Korea). Among them, 348 owned smartphones, 51 owned feature phones, and one didn't own a cell phone of any sort.

You could have made good (as in easy) money over the last five years in particular by shorting MSFT every time it went above $30.

Penny Stockers! Quit Spamming!

It's just going to get deleted.

And you know who you are.

And that has what to do with market cap?

OH MY! Trouble Looming?

Of course, the desktop isn't a particularly hospitable place for touch-screen-based users either. Although I’m not sure which is more awkward -- using Metro on a desktop PC or using the desktop from a tablet -- both are pretty tedious and rarely the experience you're looking for.

To play devil's advocate, I'll at least point out that the Apple approach -- two different systems, Windows for PCs and Metro for devices -- would have failed mightily had the software giant gone that route. Microsoft is not Apple, and it never will be. And if you accept that a coming generation of iPads and iPad-like devices is reforming the market for general-purpose computing devices, then this Apple-like plan would have pitted this new Metro business against Windows internally at Microsoft. And the only thing worse than watching Microsoft get out-maneuvered by Apple would be watching it commit ritual suicide by pitting a fictional Metro team against Windows.

Windows 8, like it or not, is thus Microsoft's best chance. It gives the company a platform that's at least unique -- I mean, seriously, could you imagine Apple foisting this two-headed hydra on customers? -- and retains all of the compatibility of the past while aiming Windows squarely at the future. But as is so often the case with Windows, its biggest strength is also its greatest weakness, and by trying to please all possible customer types, Microsoft might have just created a system that is perfect for none.

Those who believe that tablets are the future will find a simpler and purer system in the iPad. And those who believe that the PC is where it's at and always will be might be turned off by what they see as the unnecessary tabletization of Windows. Fortunately, it's not like Microsoft has much competition in that particular market. But that's the issue: Traditional PCs might soon be in the minority compared with other computing devices.

The worry, simply, is that Microsoft's quest to create a no-compromises version of Windows that answers all needs might have resulted in something that is very much a compromise. Turning Microsoft's own marketing lingo against it is cheap, I know. But that's the fear. And it sits at the heart of a debate that won't quiet down anytime soon.

http://www.winsupersite.com/article/windows8/windows-8-industry-inflection-point-142482

Yes, Beavis...

And the HPQ board is here:

http://investorshub.advfn.com/boards/board.aspx?board_id=786

Looks like they could use your help!

Maybe as a Moderator?

And btw...what did that have to do with MSFT?

Just asking.

Why would there be big drop, all things considered, unless there's a big drop in the market itself?

OH MY! MSFT's market cap now half AAPL's?

$273B vs $566B?

You could look it up.

OH MY...MSFT Fudging Phone Speed Tests?

http://www.electronista.com/articles/12/03/26/incidents.show.windows.phone.comparisons.stacked/#ixzz1qE3JQBiz

The only two words you need to know about that article:

Rob. Enderle.

Offhand, I can't think of any so-called Apple "analyst" or commentator who's been more consistently wrong about Apple than Enderle.

Why he has even a shred of credibility left is beyond me.

Apple trading halted, resumes

By Philip Elmer-DeWitt March 23, 2012: 11:53 AM ET

A circuit breaker kicked in after high-frequency trades from BATS triggered a flash crash

The hearts of Apple (AAPL) traders stopped briefly at 10:57 a.m. Friday when the company's share price, which had opened the day at $600.49 suddenly plummeted 9.4% to $542.80.

The rapid fall triggered a circuit breaker and trading was halted for five minutes. When it resumed, Apple was down 3% to $597.58.

The source was quickly traced to a flurry of high-frequency trades issued by BATS Global Markets, one of the largest high-frequency computer-driven trading platforms. BATS operates two exchanges which together account for 10% to 12% of all U.S. equity trading on a daily basis.

Most observers wrote the incident off as an error -- a so-called "fat finger" trade caused by someone hitting the wrong key.

But there have been a rash of such trading anomalies lately, and they can wreak havoc on a stock as volatile as Apple.

As it happens, the Wall Street Journal reported earlier in the day that the Securities Exchange Commission was investigating the high-frequency exchanges -- including BATS -- as part of a broader probe into whether the new trading platforms are using their high-speed links to the major stock exchanges to gain an unfair advantage.

"As part of this effort," the Journal reported, "the SEC is looking at communications between exchanges and high-frequency trading firms. Investigators are examining whether firms collude to limit competition or manipulate markets, according to a person familiar with the matter."

http://tech.fortune.cnn.com/2012/03/23/apple-trading-halted-resumes/?utm_source=twitterfeed&utm_medium=twitter

Estimates for Apple’s second fiscal 2012 quarter

MAR 21, ’12 3:43 PM

Horace Dediu

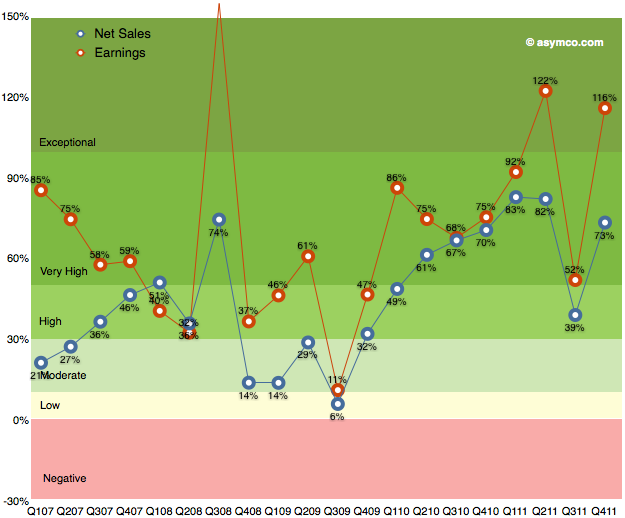

As the chart below shows, the last quarter (fourth calendar 2011, first fiscal 2012) was robust with 116% earnings growth and 73% net sales growth. I’ve heard many superlatives used to describe it. It is certainly exceptional but it was not as good as the second calendar quarter of 2011.

Sales grew faster both in CQ1 and CQ2 of 2011 and earnings grew faster in CQ2. It was in many ways a return to normality due to the iPhone returning to 133% revenue growth after the lull of the transitional third quarter.

Now it’s time to consider the current quarter. It’s already quite late in the quarter to make predictions, but I waited to hear some data about the iPad. The iPad remains a difficult product to forecast. Mainly because it is a new category and the pattern of growth takes a long time to establish. We’ve only had three quarters where y/y growth could be measured. Sales growth has been 180%, 146% and 99%. Unit growth has been 183%, 166% and 110%.

These rates have been higher than the average iPhone growth rates (average of which was 100% in units and 108% in revenues over the calendar 2011). Indeed, the average iPad growth rate so far seems to be 150%.

Is it sustainable?

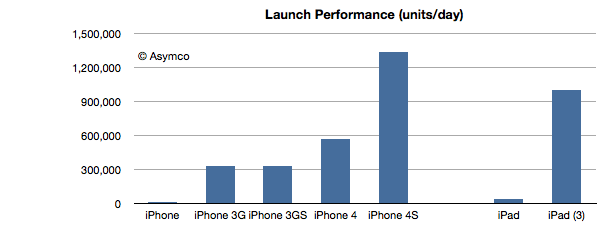

The answer from this latest launch seems to be yes. The following chart shows the launch performance of the various iOS devices whose launch performance has been announced.

The growth in launch performance between iPad 1 and iPad 3 is a factor of 28. iPad third generation had broader distribution but the volume boost from first generation is enormous. This implies a vastly improved production ramp. As the product remains supply constrained, the most important indicator of performance is production throughput.

So given this data on the iPad and the ongoing broadening of the iPhone distribution network, here are my first quarter estimates (with y/y growth in parentheses):

iPhone units: 37.3 million (100%)

Macs: 4.7 million (25%)

iPads: 12.2 million (160%)

iPods: 7 million (-22%)

Music (incl. app) rev. growth: 40%

Peripherals rev. growth: 25%

Software rev. growth: 10%

Total revenues: $42.7 billion (growth: 73%)

GM: 44.7%

EPS: $12.0 (88%)

This earnings value would imply a trailing twelve months’ EPS of about $40.7. At $600/share the P/E would be 14.7. Cash and equivalents will probably increase to $108 billion.

http://www.asymco.com/2012/03/21/estimates-for-apples-second-fiscal-2012-quarter/

Apple’s dividend and share re-purchase plan: the impact on cash growth

MAR 19, ’12 4:25 PM

Horace Dediu

Today Apple announced both a dividend and a share re-purchase plan which, when combined, will consume 45% of Apple’s current US cash reserves.

The dividend will be $2.65/share/quarter and the buyback will cost $10 billion over three years. The dividend will therefore cost about $2.5 billion per quarter (starting next quarter) and the re-purchase will cost about $833 million per quarter (starting next fiscal year).

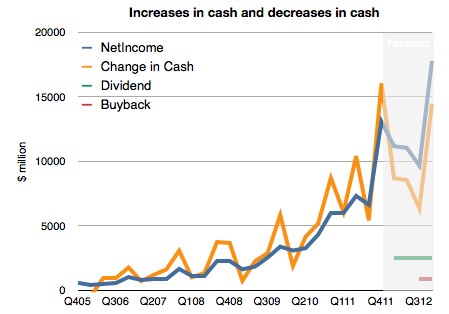

However, note that Apple’s cash has been growing far more quickly. It increased by $16 billion last quarter or $37 billion over the last year. This rate of increase is itself increasing.

To illustrate, I prepared the following chart. It shows historic net income, change in cash and a forecast of the costs of the new uses of cash and future net income (based on my estimates).

I made an assumption that future cash growth will equal net earnings minus costs for the new dividend and share re-purchase. What we should see is that the previously tight coupling between increase in cash and earnings will remain but that there will be a negative offset by $3.333 billion each quarter. In other words, cash will increase but at a slower rate.

This means Apple’s total cash should still grow by more than $35 billion this year.

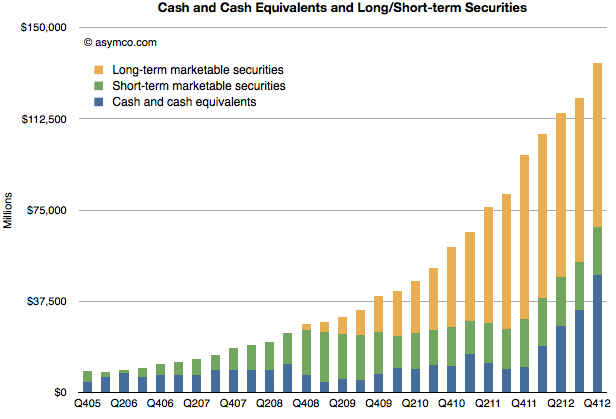

That would result in the following, more subdued, total cash trajectory (for simplicity, I assumed all added cash would be in cash and cash equivalent accounts)

http://www.asymco.com/2012/03/19/apples-dividend-and-share-re-purchase-plan-the-impact-on-cash-growth/

IPhone Sales Could Outpace Estimates, Too

Last update: 3/20/2012 7:46:56 AM

7:46 (Dow Jones) It's not just the strong iPad sales figures released late Monday, hours after the dividend and stock-buyback news, that Apple (AAPL) investors should keep mind of, says Sterne Agee. "Supply-chain checks indicate stronger-than-expected uptake in iPhone, with China Telecom added as a carrier and 21 countries added for the 4S." As such, the investment bank projects 28M iPhones having been sold this quarter--up 2M from its prior view--as it also boosts iPad estimates for calendar 2012 and EPS and revenue targets for this FY and next. In that light, Sterne Agee joins the stampede of investment banks boosting stock-price estimates, going to $740 from $620.

Yes, 3 Million Sold. Not first week, though, first weekend.

Notes of interest from Apple's dividend & stock buyback conference call

By AppleInsider Staff

Published: 09:02 AM EST (06:02 AM PST)

Following Apple's announcement on Monday that it will pay a quarterly dividend of $2.65 per share as well as initiate a $10 billion share buyback program, executives from the company participated in a conference call with analysts and investors.

Apple Chief Executive Tim Cook noted that even though the company sold 37 million iPhones last quarter, it represented less than 9 percent of all handset sales. "The potential for iPhones is enormous."

On the launch of the new iPad: "It just keeps getting better." 55 million iPads sold to date, but no sales figures on the new iPad given.

Apple still has less than 6 percent PC market share as the Mac continues to grow.

"We are innovating an incredible pace."

Apple is also investing in distribution around the world. "We don't see ceilings to our opportunities," Cook said.

All of this has led to Apple amassing a "substantial amount of cash." This has led to increased research and development, acquisitions, new retail stores, building out of infrastructure and more. "You will see all of these in the future," Cook said.

"We are going to initiate a dividend and share repurchase program. We have thought very deeply and very carefully about our cash balance. We will continue to invest in the business."

Innovation remains the most important focus at Apple, and Cook said the new program won't make them lose sight of that.

The new program is expected to broaden Apple's investor base by attracting new investors that don't currently own Apple stock.

Cook said they plan to review the program periodically.

Chief Financial Officer Peter Oppenheimer said Apple has been "very disciplined" with its cash. In fiscal 2011, its cash increased by $31 billion, with $21 billion coming from abroad.

Apple wants to maintain the flexibility to take advantage of investment opportunities that present themselves.

None of Cook's unvested RSUs will participate in dividends, at the CEO's request.

"We remain very confident in the future of our business, are extremely enthusiastic about the opportunities that lie ahead, and look forward to executing our plans to initiate a dividend and share repurchase program," Oppenheimer said.

Apple's cash plan: 3 options

By Philip Elmer-DeWitt March 19, 2012: 6:16 AM ET

Most likely scenario: ongoing dividend. Less likely: special dividend or stock buyback

In a note to clients issued Sunday night, less than 12 hours before Apple's (AAPL) scheduled conference call, RBC Capital's Mike Abramsky laid out his thoughts about what Tim Cook is likely to do with Apple's excess cash: (I quote)

Ongoing Dividend. In the most widely expected scenario, Apple may offer a $10/share ongoing annual dividend (implies a payout that is a slight premium to peers), which equates to $9.4B or 25% of our F12 FCF [free cash flow] estimate, slightly above other tech leaders (MSFT, IBM, ORCL, INTC, QCOM, CSCO, HPQ) that pay out dividends at 21% of FCF. A $10/share annual dividend equates to 1.7% dividend yield, inline with other tech leaders (1.8%).

Two Other Scenarios:

Special Dividend. We estimate Apple could declare a $60/share special one-time dividend, inline with Microsoft's 2004 special dividend (58% of cash). Following the ex-dividend date, shares are likely to drop by the value of the one-time dividend.

Share Buyback. Assuming Apple deploys the same amount of cash (25% of FCF) instead on share repurchases vs. an ongoing dividend, we estimate Apple could repurchase 16M shares annually.

Impact. An ongoing dividend and/or special dividend or share buyback signals a new phase for Apple, one of less rapid, but still above-peer growth and margins. Distributing some of its large cash balance back to shareholders addresses an overhanging issue which has weighed on valuation (13x FTM P/E (including cash) or 11x FTM cash-adj P/E vs. peers at 17x). Additionally, a dividend will appeal to some shareholders for whom a dividend is a requirement, bringing new buyers into the name.

WEBCAST @9 a.m. EDT: http://events.apple.com.edgesuite.net/123pijhbsdfvohbafv19/event/index.html

So they're having a conference call in the morning to announce that they're not doing anything with the cash stash after all?

Not likely.

Apple Touches $600, what is Next?

It sounds like a broken record, another day, another new high for Apple’s (NASDAQ: AAPL) stock. After crossing $400 on December 23, $500 on February 13, and $550 on March 12,Apple touched the $600 mark in pre-market trading this morning— though it pulled back in early regular trading. Apple is still trading well above its 200, 100, and 50-day moving averages, gaining roughly 65 percent for the last 12 months compared to an almost 7 percent gain for Google (GOOG), a 10 percent gain for the overall Nasdaq100 (NASDAQ:QQQ), and a 40 percent decline for Hewlett-Packard(NYSE:HPQ).

The iPad Reviews Are In: Faster, With an Outrageous Display

Connie Guglielmo

Forbes Staff

AAPL Target Raised to $710

Canaccord Genuity

Contributor

Apple, Steam Pad, and the New Wave of Game Development

Erik Kain

Contributor

Apple’s stock has benefited by the last profit report that exceeded analysts’ estimates by a wide margin, easing of concerns over leadership transition after the loss of its legendary founder Steve Jobs, and the introduction of new products. In the meantime, both Apple and Google have been gaining market shares against Research in Motion (NASDAQ:RIMM) and Nokia(NYSE:NOK)—Apple has been particularly strong in Asia, where it maintains the unquestionable leadership against its peers. What is next?

As we did write in a previous piece, Apple’s stock rapid ascend has fueled a wave of robust forecasts that call for Apple to reach $600, $800, even $1000 that hype investor expectations feeding into a speculative frenzy that parallels similar predictions for Cisco Systems (NASDAQ:CSCO), and Hewlett-Packard(NYSE:HPQ) back in the late 2000. We all know how that frenzy ended. That’s why we aren’t going to join in the chorus.

Instead, we should point out that even after this big run up, Apple trades at a Forward PE (fye Sep 24, 2013) of 11.54. This means that the stock is still inexpensive compared to Google and the Nasdaq100. Apple is firing on all cylinders, with its Mac products gaining in popularity among corporate users, and its iPhone 4S gaining popularity in Asia-Pacific, where Apple has a huge room to grow, both in the short-term and in the long-term; and still has a host of new products on the pipeline to capture and captivate its customers’ imagination.

Long on AAPL

Forbes

Laize, you're spinning a broken record.

You don't like AAPL as an investment play.

We get it already.

More Details on the Piper Jaffray Note: Big Estimate Revisions

Barron's:

MARCH 15, 2012, 10:17 A.M. ET

Apple: Piper Ups Target to $718 on Higher iPhone, iPad Share

By Tiernan Ray

Piper Jaffray’s Gene Munster this morning reiterated an Overweight rating on shares of Apple(AAPL) and raised his price target to $718 from a prior $670, to account for upwardly revised growth rates for the smartphone and tablet markets.

Munster now sees Apple shipping more units, but also maintaining higher share of those markets than he previously thought.

Munster now expects Apple to sell 189 million iPhone units in calendar year 2013, up from a prior 162 million estimate, representing 23% market share, year over year, up from a prior expectation for just 20%. That’s out of a total projected market for 804.6 million smartphones in 2013. Munster sees Apple holding a third of the market by 2015, with 385 million iPhones sold.

On the tablet side, Munster now sees Apple’s iPad losing only minor share in 2013, versus a former expectation for a 12% loss.

Munster estimates Apple may sell 86.5 million iPads in calendar 2013, up from a prior 75.5 million estimate, and 44% higher than 2012's number. That would give Apple 60% of the tablet market, versus his prior estimate for 52% share. That’s out of a total of 143.9 million tablets in 2013.

By 2015, Apple may still have 60% of the market, with 176 million iPad units sold.

Munster raised his 2013 estimate to $189.5 billion in revenue and $48.90 per share in profit, up from $176.99 billion and $45.79.

Munster’s price target increase represents the latest in a series of analysts joining The 700 Club: As I wrote yesterday, Canaccord Genuity’s Mike Walkley raised his target to $710 andMorgan Stanley’s Katy Huberty increased hers to $720. The average price target on the Street now is $609.84, according to Factset Research Systems.

Too funny!

Can I borrow one?

So IT hates the iPad, eh?

ChangeWave survey: New iPad roils the business tablet market

Planned sales of competing tablets were falling even before the new iPad was revealed

Click to enlarge. Source: ChangeWave

This was supposed to be the year that Apple (AAPL) started losing market share in the rapidly growing tablet market.

That may be happening among consumers, if you count the Amazon's (AMZN) Kindle Fire as a full-fledged tablet. But there's no sign of it happening in the enterprise.

In fact, a ChangeWave survey of 1,604 business IT buyers conducted in February -- even before the new iPad was revealed and iPad 2's price was cut -- found that more than one in five (22%) planned to buy tablets for their users in the next three months, and that 84% planned to buy Apple iPads. That's the highest level of corporate iPad demand ever recorded in a ChangeWave survey, up 7 percentage points from November's survey.

The list of companies whose corporate market shares appear to be headed south reads like a also-rans who's who, including Samsung, Amazon, HP and Asus. See chart below:

ChangeWave is a division of 451 Research.

Cook's sale appears to be tax related.

From AppleInsider:

Cook's shares vested last Saturday after a two year waiting period. In March 2010, the executive was awarded 75,000 restricted stock units "in recognition of his outstanding performance in assuming the day-to-day operations" of Apple while Jobs was on medical leave to recover from a liver transplant. When the first half of the shares vested last March, Cook immediately sold off the batch, netting $7.02 million after taxes.

This year, Cook's tax bill for the second half of the shares came out to $9.44 million. He opted to pay by surrendering 17,322 shares at a stock price of $545.17.

Translation: I am soooooo sorry I didn't buy any Apple shares when they were cheaper!

Put another way: your Apple hatred has cost you and your IT buddies big bucks.

Now have a nice day.

Apple 2012 Q2 Results - 4 Reasons To Be Optimistic

March 12, 2012

Apple (AAPL) is expected to report its fiscal Q2 2012 results the last full week of April. We are just about 3 weeks away from the end of the quarter and this is usually the time the analysts start revising their estimates. This article presents some of the positive catalysts in this quarter so far and arrives at a fair EPS and PPS.

China Telecom: China Telecom (CHA) is the third largest telecom provider in the most populous country. CHA recently started selling iPhone 4s and the pre-orders were of the usual Appl-e-pic proportions. The demand has been greater than expected, with more than 200,000 pre-orders. One may recall CEO Tim Cook's enthusiasm about China sales during Q1 2012 earnings call.

The New iPad: The new iPad was launched on March 7th amidst high expectations. As with any Apple launch, the initial reports weren't so positive. But Philip Elmer-DeWitt, one of the most respected Apple analysts, reports otherwise. Remember, a key factor during 2011 Q4 miss was the launch of iPhone 4s. People waited for 4s to be launched in Q1 2012, affecting the numbers for Q4 2011. But with the new iPad, the news and the launch happened in the same Q2 2012 quarter. In essence, the lost sales in iPad 2 would be more than compensated by the sales of the new iPad.

Kindle "Fired": Though not many see the Kindle Fire as a threat for Apple's iPad, there is no doubt Amazon (AMZN) sells quite a few units that would otherwise go to Apple. But now, with the price cut of iPad2 (available from $399), Kindle Fire's share of the pie should get smaller. Thinking what difference a $100 price cut would make? Check this out and remember, the survey is about non-iPad buyers and 20% is a good number there.

The (100) Billion Dollar Question: This is a cheat and not directly related to Q2 results. However, one of the most positive things to come out this quarter was on the non-product side. Thankfully, Tim Cook and co shot down all questions about meaningless acquisitions with the cash. Tim Cook's handling of the various public appearances (addressing the Foxconn issue in particular) convinces that he is in total command and will lead the company his way, not the way Steve Jobs would have, while retaining Apple's basic culture of "think different". And that is a big relief to the share holders. (Perhaps to Steve Jobs as well)

A look At The Numbers: Analyst estimates for Q2 currently is at 9.48/share and as stated above, the number will likely be revised as we head closer to the results. Going by Apple's last 4 quarters (Simple Moving Average), the company has beaten the estimates by 20% (including the "miss" in Q3). That would give us a Q2 EPS of 11.37 and last 4 quarters EPS of about 40/share. Applying today's fair trailing PE of 15.5; we arrive at $620/share. That is a good 13% gain from Friday's close price of $545.

Although, the technical indicators suggest Apple has been overbought and has been on a parabolic run, the fundamental growth is still incredible and augurs well for the shareholders.

Disclosure: I am long AAPL.

http://seekingalpha.com/article/426391-apple-2012-q2-results-4-reasons-to-be-optimistic?source=feed

Several free photo Apps today only...

iPhone and iPad:

http://lifeinlofi.com/

You're welcome!

Apple: Price Targets, Estimates Going Up on New iPad

By Tiernan Ray

Shares of Apple (AAPL) are up $3.54, or 0.7%, at $534.23 the morning after the company introduced its latest iPad model to the world, as well as a revamped “Apple TV” set-top box.

The praise from the Street is more or less unanimous, as it was with the early reviews, yesterday afternoon.

This morning, price targets are going up today in several corners, and estimates, in some but not all cases.

Mind you, some analysts had held off on raising price targets for months, and the stock had steadily crept up to the levels they were at, so some targets seemed ripe for an increase.

The mean target price on the Street is $594, according to Factset Research.

Bill Shope, Goldman Sachs: Reiterates a Buy rating, while raising his price target to $660 from $600, after raising his estimates to $152.38 billion in revenue this year and $42.52 in EPS, up from a prior $148.26 billion and $40.36. “Significantly, we believe the new iPad and the lower price point for the iPad 2 will enable Apple to continue its momentum and tablet market dominance, and we continue to expect rapid installed base growth in 2012 and beyond.”

Mark McKechnie, ThinkEquity: Reiterates a Buy rating, while raising his price target to $600 from $550, writing that “The launch follows the “tech playbook” of offering more functionality at a given price point.” The LTE capability in the new device should lead to an LTE iPhone later this year: “We view a new iPhone model, presumably the iPhone5 as a much more important catalyst on the horizon. Our industry checks suggest uncertain timing around the July-September time frame. Shipment of an LTE-based iPad adds confidence to our call for an LTE- based iPhone5 which we expect to also come in a thinner form factor.”

Shebly Seyrafi, FBN Securities: Reiterates an Outperform rating and raises his price target to $730 from $650, after increasing his calendar 2012 iPad shipment forecast to 61.2 million units from a prior 56.2 million. While the iPad “met many expectations,” it didn’t meet all of them, leaving out support by Sprint-Nextel (S) among carriers, and support for Apple’s “Siri” natural-language assistant, Seyrafi notes. Seyrafi raised his estimate for this fiscal year to $158.47 billion in revenue and $42.53 per share in EPS from a prior $156.29 billion and $42.09 per share.

Barron's

AAPL: FYQ2 Upside Even Before New iPad, Says ITG

By Tiernan Ray

Analyst Tony Berkman with boutique research house ITG Investment Research this afternoon offers up the view that Apple (AAPL) is on track to beat the consensus $35.15 billion for the fiscal Q2 that ends this month, likely turning in $37.3 billion, with some benefit coming from sales of the iPhone starting with China Telecom (CHL) tomorrow, without counting any sales from the new iPad, unveiled yesterday.

Apple may ship 31.3 million iPhones this quarter, with 1.2 million of that inventory filling, writes Berkman, and he sees particular strength in China, as “as China Unicom (CHU) has benefited tremendously from the launch of the 4S.” China Unicom has been the sole licensed carrier for the iPhone prior to Telecom starting to sell the device.

For the iPad, Berkman is modeling 10.2 million units, but he expects “considerable upside” to that number when including units sold for the new model, which comes to retail on March 16th.

Berkman thinks Apple may sell 4.35 million Macs this quarter, a 15.7% rise, with improving trends in Europe and other foreign markets.

Apple shares today rose $11.30, or 2%, to $541.99.

http://blogs.barrons.com/techtraderdaily/2012/03/08/aapl-fyq2-upside-even-before-new-ipad-says-itg/?mod=BOLBlog

"It's the best display I've ever seen. Anywhere, period. And it makes a meaningful difference to the experience -- it's not just a spec."

http://gdgt.com/discuss/ipad-3rd-gen-first-impressions-169l/

It's amazing what can be done with a touch screen these days:

http://www.apple.com/ipad/from-the-app-store/apps-by-apple/iphoto.html

Video of today's presentation...

http://events.apple.com.edgesuite.net/123pibhargjknawdconwecown/event/index.html

They're going to sell every one they can make, for starters.

$600+ by the end of the year.

Yes, it is. And Apple's gonna sell so many of those suckers it won't be funny.

Simple then, isn't it? Don't buy one.

More live view options...

http://tech.fortune.cnn.com/2012/03/07/how-to-monitor-todays-ipad-event-from-your-computer/

Live coverage for today's event...

http://live.arstechnica.com/Event/Apple_iPad_3_Event

Apple Chart...

Shanghai court sides with Apple in iPad trademark dispute, sales to continue

By Sam Oliver

Published: 07:35 AM EST (04:35 AM PST)

Apple can continue to sell the iPad in Shanghai after a local court sided with the company in a trademark dispute over ownership of the "iPad" name.

Apple's victory over Proview, which for years sold a different product with the name "I-PAD," was confirmed by a source with direct knowledge of the ruling to Reuters on Thursday. The Shanghai Pudong New Area People's Court made the decision quickly after a hearing was held on Wednesday.

At that hearing, Apple argued that a ban on iPad sales would be a negative for the nation of China. A lawyer representing Apple said that Proview has no products or customers, while Apple has "huge sales in China," and therefore prohibiting sales of the iPad would "hurt China's national interest."

Proview has contended that it owns the rights to the iPad name, and seeks to halt sales of Apple's hot-selling tablet in China. Though Thursday's ruling was a major setback for Proview, the company had previously had some minor successes in having a small number of iPad units pulled from shelves in a handful of cities.

Apple bought the right to use the iPad name from one of Proview's Taiwanese affiliates, but officials at Proview believe that was an unauthorized transaction, and the company has sought as much as $2 billion from Apple to use the iPad name. Apple, however, believes that Proview is not honoring up the original deal that was struck between the two companies.

Thursday's ruling was particularly significant for Apple because the company has three major flagship stores in Shanghai. A loss there would have barred sales of the iPad from some of its most heavily trafficked retail locations in the world.

Though the Shanghai victory is significant for Apple, it still faces challenges from Proview elsewhere. The company has even gone as far as to ask the Chinese government to block exportation of the iPad, which would effectively bring global sales of the device to a halt.

http://www.appleinsider.com/articles/12/02/23/shanghai_court_sides_with_apple_in_ipad_trademark_dispute_sales_to_continue.html