News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Oil has yet to bottom, WAKE UP!

Peasodos

![]()

Oil has yet to bottom, WAKE UP!

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Oil has yet to bottom, WAKE UP!

Made a nice profit, covered my shorts.

Anybody else Short CADC at the end of the day or am I crazy?

Anybody else short snapchat?

Saudi's will play Hardball, Here's Why, This translates to No deal, just like Doha

it looks like Saudi Arabia could walk away from deal entirely.

Last weekend, the Saudis pulled out of a Monday meeting between OPEC and non-OPEC countries and later cancelled the meeting altogether.

On Friday, Saudi Arabia announced that it believes demand will recover in 2017 without any OPEC intervention in the market.

On Monday, oil minister Khalid al-Falih said that Saudi Arabia’s planned production cut would be predicated on all OPEC members agreeing to “share the burden of cuts equally, and do so in a way that is transparent and has credibility with the market.” This is in contrast to traditional OPEC cuts in which the Saudis often bore the most burden.

Just before al-Falih arrived in Vienna on Tuesday, Bloomberg reported that Saudi Arabia rescinded its offer for Iran to freeze oil production at 3.8 million bpd and instead demanded a lower number – 3.707 million bpd.

Now, on the eve of the November 30 meeting, Saudi Arabia lowered that number to 3.69 million bpd (Iran’s oil output from October).

Why the sudden change? While it may seem puzzling given Saudi Arabia’s previous support for an OPEC production agreement, this is quite in line with a long tradition of tough Saudi negotiating tactics when it comes to oil policy.

A Wall Street Journal report pegs Deputy Crown Prince Mohammad bin Salman as the culprit. Its source claims, just like during the failed OPEC negotiations in Doha in April 2016, that the prince is not permitting the Saudi oil ministry to engage in any negotiations.

It's headed in that direction. Once this OPEC deal fails WTI will easily drop below $40. I do think by January last years low will get hit, maybe sooner than that. Who knows how long this oil price/Market share War can go on, maybe Allah, lol

Credit Suisse AG Announces Its Intent To Delist And Suspend Further Issuances Of Its DWTI And UWTI ETNs

NEW YORK, Nov. 16, 2016 /PRNewswire/ -- Credit Suisse AG announced today its intention to delist and suspend further issuances of the following Exchange Traded Notes (the "ETNs"):

ETN

Ticker

CUSIP

VelocityShares™ 3x Inverse Crude Oil ETNs linked to the S&P GSCI® Crude Oil Index ER due February 9, 2032

DWTI

22542D548

VelocityShares™ 3x Long Crude Oil ETNs linked to the S&P GSCI® Crude Oil Index ER due February 9, 2032

UWTI

22539T316

As part of its continuing effort to monitor and manage its suite of exchange traded notes, Credit Suisse AG has decided to delist the foregoing ETNs with a view to better aligning its product suite with its broader strategic growth plans. Accordingly, Credit Suisse AG anticipates that the ETNs will continue to trade on NYSE Arca up to and including December 8, 2016 and that effective December 9, 2016, the ETNs will no longer be listed for trading on any national securities exchange. In addition, Credit Suisse AG will suspend further issuances of these ETNs effective December 9, 2016.

Following their delisting, the ETNs will remain outstanding, though they will no longer trade on any national securities exchange. The ETNs may trade, if at all, on an over-the-counter basis. Although it is not currently accelerating the ETNs at its option, Credit Suisse AG continues to have the right to do so, as described in the pricing supplement for the ETNs (the "Pricing Supplement"), and may choose to accelerate the ETNs at its option in the future, either together on the same date or each on a separate date, including shortly after the delisting. Subject to the minimum redemption amount and other conditions, investors can continue to exercise their early redemption right with respect to the ETNs prior to, and following, the ETNs' delisting, pursuant to the terms of the ETNs as described in the Pricing Supplement. If investors wish to exercise their early redemption right, they and their broker must follow the procedures set forth in the Pricing Supplement, which can be accessed on the Securities and Exchange Commission website at www.sec.gov as follows:

https://www.sec.gov/Archives/edgar/data/1053092/000095010316017628/dp70004_424b2-a32.htm

Only the VelocitySharesTM 3x Inverse Crude Oil ETNs linked to the S&P GSCI® Crude Oil Index ER due February 9, 2032 (NYSE Arca: DWTI) and the VelocitySharesTM 3x Long Crude Oil ETNs linked to the S&P GSCI® Crude Oil Index ER due February 9, 2032 (NYSE Arca: UWTI) are affected by this announcement.

As disclosed in the Risk Factors section of the Pricing Supplement, the market value of the ETNs may be influenced by, among other things, the levels of actual and expected supply and demand for the ETNs in the secondary market. It is possible that this announcement and the delisting and suspension of further issuances of the ETNs, as described above, may influence the market value of the ETNs. For example, delisting the ETNs will remove the primary source of liquidity for the ETNs and investors may not be able to sell their ETNs in the secondary market at all. In addition, suspending further issuances of the ETNs may further adversely affect liquidity for any secondary market that may develop following a delisting. Credit Suisse AG cannot predict with certainty what impact, if any, these events will have on the public trading price of the ETNs. Investors are cautioned that paying a premium purchase price over the indicative value of the ETNs could lead to significant losses. An investor that pays a premium for the ETNs, for example, may suffer significant losses if the investor is unable to sell the ETNs in the secondary market, if the investor sells at a time when the premium has declined or is no longer present or if Credit Suisse AG accelerates the ETNs at its option. Even if investors do not pay a premium over the indicative value of the ETNs, investors could still suffer substantial losses because of the illiquidity associated in the secondary market. For instance, investors may not be able to sell the ETNs readily and may suffer substantial losses and/or sell the ETNs at prices substantially less than their intraday indicative value or closing indicative value, including being unable to sell them at all or only sell them for a price of zero in the secondary market.

In addition, as described above, Credit Suisse AG continues to have the right to accelerate the ETNs at its option in the future, either together on the same date or each on a separate date, including shortly after the delisting. If Credit Suisse AG accelerates the ETNs at its option, investors will receive the applicable accelerated redemption amount, which will be an amount equal to the arithmetic average of the closing indicative values (which will not include any premium) of the applicable ETN during the accelerated valuation period. Any investors who paid more for their ETNs (including any premium to closing indicative value) than the amount they receive upon an acceleration will suffer a loss on their investment, which could be significant. In addition, investors will not receive any other compensation or amount for the loss of the investment opportunity of holding the ETNs and investors may be unable to invest in other securities with a similar level of risk and/or that provide a similar investment opportunity as the ETNs.

UWTI below $16 wake UPPP!!!

Just look at the DXY, over 100 now. That alone is the biggest in you face indicator that oil is going to crash.

USD Breakout over 99, Oil is heading for a crash once key technicals are taken out. Wake Up!

Exactly! US production is increasing and more resilient than ever. Oil is headed for another nasty downturn this time worse than last January . Most hear don't believe me but one day they'll Wake Up!

Countdown to OPEC meeting Failure...

Just for you

Oil Is Still Heading to $10 a Barrel

Back in February 2015, the price of West Texas Intermediate stood at about $52 per barrel, half of its 2014 peak. I argued then that a renewed decline was coming that could drive it below $20, a picture/situation regarded by oil bulls as (too terrible to think about). But prices did fall further, dropping all the way to a low of $26 in February. Since then, (very simple/rough and rude) celebrated/got stronger to spend (more than two, but not a lot of) weeks flirting with $50 per barrel, a level not seen since last year. But it won't last; I'm sticking to my call for prices to (lower in number/get worse) again to $10 to $20 per barrel.

Oil Prices

Recent gains have little to do with the basics that led to the collapse in the first place. Wildfires in the oil-sands area in Canada, output cuts in Nigeria and Venezuela due to political unrest, and hopes that American liquid-related cracking and breaking would run out of steam are the first (or most important) causes of the recent spurt.

But the world continues to be full of/surrounded by (very simple/rough and rude), and American frackers have replaced the Organization of Petroleum Exporting Countries as the world's swing producers. The once-feared oil (group of businesses) is, to me, pretty much finished as an effective price enforcer. Even OPEC's leader, Saudi Arabia, is admitting/recognizing/responding to the new reality by stopping recent tries to freeze output, borrowing from banks and preparing to sell a stake in its Aramco oil company as it tries to find new sources of non-oil money/money income.

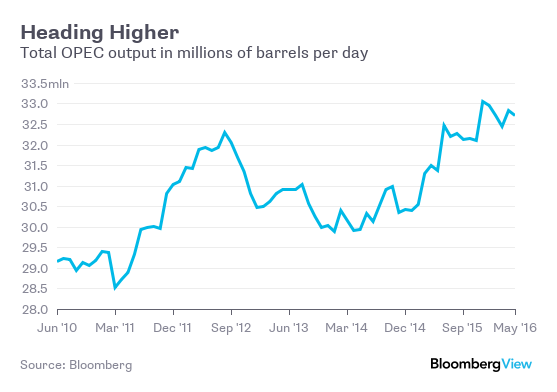

The Saudis and their Persian Gulf friends continue to play a (without hope/very upset) game of chicken with other major oil producers. (groups of businesses exist to keep prices above steadiness/balance, which encourages cheating as (group of businesses) members go beyond their given out/set aside output and other producers take advantage of inflated prices. So the role of the (group of businesses) leader, in this case Saudi Arabia, is to cut its own output, neutralizing the cheaters to keep prices up. But the Saudis suffered market-share losses from their previous production cuts. OPEC has effectively left alone (handcuffs, etc./things that slow down or hold back something), with total output flying up to as high as 33 million barrels per day at the end of last year :

Iran, freed of Punishments (from the U.S., Canada, etc.), plans to double output to 6 million barrels a day by 2020, which would make it the second-largest OPEC producer behind Saudi Arabia. Russia continues pumping to support its (process of people making, selling, and buying things) after the collapse in oil prices destroyed government money/money income and export earnings. War-torn Libya is also increasing production as best it can.

The International Energy (service business/government unit/power/functioning) (describes a possible future event) that even with a successful OPEC production freeze, if U.S. frackers cut production by 600,000 barrels a day this year and a further 200,000 barrels per day in 2017, excess supply would run at 1.5 million barrels a day until 2017. That's a continuation of the recent oversupply of 1 to 2 million barrels a day.

The price at which major producers chicken out and slash production isn't figured out by/decided by the prices needed to balance the budgets of oil producing nations, which are as high as $208 per barrel in Libya and as low as $52 per barrel in Kuwait. Nor is it the "full cycle" or average cost of production that includes drilling costs, overheads, pipelines, etc.

In a price war, the chicken-out point is the price that equals the not important cost of producing oil from an established well. Once fracking operations are set up and staffed, leases paid for, drilling happening and pipelines laid, the not important cost of shale oil for (producing a lot with very little waste) producers in the Permian (bowl/area drained by a river) in Texas is about $10 to $20 per barrel and even lower in the Persian Gulf.

What's more, fracking costs continue to fall as working well and getting a lot done improves. The number of drilling rigs operating in the U.S. continues to drop. But the rigs taken offline are mostly old up-and-down drillers that drill only one hole per (raised, flat supporting surface), while flat/left-and-right rigs -- able to drill 20 to 30 wells per (raised, flat supporting surface) like the spokes of a wheel -- more and more rule. So output per working rig is speeding up.

At the same time, worldwide money-based growth, and therefore demand for oil, is weak. China, that giant person (who uses a product or service) of oil and other (things of value), is moving/changing to services from manufacturing and (basic equipment needed for a business or society to operate) spending. Energy (using less of something) measures in the West are controlling oil demand. And (related to computers and science) advances in fracking, flat/left-and-right drilling, deep-water and Arctic drilling will boost non-OPEC supplies to as high as 58.6 million barrels per day this year from 58.1 million in 2015.

And don't forget the extremely important influence of (items that are stored and available now) on prices. After all, with worldwide output going beyond demand, the extra (very simple/rough and rude) goes into storage. And when the storage facilities are full, the (more than needed) will be dumped available to buy to the harm of prices. Cushing, Oklahoma, the delivery point for deciding/figuring out the price of West Texas Intermediate, is nearing full storage ability (to hold or do something); the same is true for the Amsterdam-Rotterdam-Antwerp area, the oil gateway to Europe. China is running out of ability (to hold or do something) for commercial and (related to a plan to reach a goal) reserves. Around the world, oil extracted from the ground (items that are stored and available now) have jumped to record levels, with a leap of 370 million barrels since January 2014.

(more than needed) oil is also being stored on ships, even though (what people commonly call a/not really a) floating storage costs $1.13 per barrel per month compared with 40 cents in Cushing and 25 cents per month in underground salt caves, like those used for the U.S. (related to a plan to reach a goal) Petroleum Reserve. What's more, as low oil prices have made shipping by train (losing money), rail tank cars are being used, with (what people commonly call a/not really a) rolling storage costing about 50 cents per barrel per month.

So what will trigger renewed price declines? Excess production will end up being dumped onto the market. Pressure from lenders on (related to money)-weak energy borrowers will force them to produce as much oil and gas as possible to service the money they owe. The likely continuing rise of the safe-safe place dollar against the types of money of developing (processes of people making, selling, and buying things) will hype the cost of imported oil -- (existing (the same) everywhere) priced in the U.S. currency -- further controlling demand. Finally, the likely slowing of worldwide money-based growth and oil demand in reaction to the U.K. decision to leave the (related to Europe) Union reinforces my (negative thinking).

An oil price drop to below $20 per barrel would be a shock similar to the dotcom collapse in the late 1990s and the subprime mortgage disaster that produced the 2008 major money-based problem -- both of which triggered (time periods where people and businesses made less money). Of course, oil prices would not stay in the $10 to $20 barrel range (for a long time--maybe forever); (time period where people and businesses made less money) would squeeze out excess energy production and prices would recover, likely to the average cost of new production. But the (lowering prices/air leaving a balloon, etc.) that might go with a worldwide money-based downturn might mean the new steadiness/balance price for oil is between $40 and $50 a barrel -- well below the $82 average in the first half of this ten years, and lower than the ideas (you think are true) in the business plans of energy producers.

Chart of what No OPEC Cut/Freeze will do to WTI:

Long term Support from February low now Resistance. Tested today!

No the self Reported numbers are higher than this.

"The Reuters survey is based on shipping data provided by external sources, Thomson Reuters flows data, and information provided by sources at oil companies, OPEC and consulting firms."

Also Angola was only lower because of a workers strike that is now over.

http://in.reuters.com/article/opec-oil-survey-idINKBN12V221

OPEC Pumps Record 34.02 Million Barrels per day in October!

http://www.bloomberg.com/news/articles/2016-11-02/oil-market-turns-skeptical-about-opec-s-ability-to-deliver-cuts

Wake Up!

Chart of Year long Support Violated

Long term support going back to the February low has been violated big time.

OPEC just hit another Record production number, Russian production Up, US production up again w/w...

WAKE UP!!!

CRUDE +9.3mm bbls

GAS -3.6mm bbls

DISTILLATES -3.1mm bbls

CUSHING +1mm bbls

I wasn't questioning you or the method, just the last part of what he said made me lol.

The Algiers accord was a surprise outcome, but looks like total baloney.

There was a massive inverse head and shoulders on the chart, but it failed hard falling drastically from the neck line and also the monthly bearish shooting star.

Good luck.

FY’16 demand line violated

October Prints Bearish Shooting Star

Hang in there, once the OPEC deal officially fails on November 30th oil will drop below $30 again by February. This time it will be worse than in 2016.

Watch the Falling Knife.

Wake Up People!

WAKE UP!!! Huge Head and shoulders pattern, just starting to break the neckline, watch out Below!

WAKE UP!!!

Libya Lifts Force Majeure at All Oil Ports, Resumes Exports

Tripoli—Libya’s National Oil Corporation (NOC) announced Thursday that it had lifted force majeure at all its oil ports and that oil exports are resuming.

NOC chairman Mustafa Sanalla, during a visit to the Libyan largest oil terminal of Zeisian, said that “NOC is in charge of the ports”.

“They are secure, and we have been in contact with our foreign commercial partners. NOC assessment teams have reported that Zeisian and Brega ports are intact,” he added

The Libyan National Army succeeded on 11 September in taking control of the four oil ports from the militias which blockaded exports since 2013 and two days later officially handed them over to NOC’s chairman.

Speaking to reporters on 13 September as he visited Zeisian oil terminals, Sanalla said “we can raise production to 600,000 b/d within four weeks and to 950,000 b/d by the end of the year from around 290,000 b/d at present”.

Sanalla said the ports of Ras Lanuf and Es Sidra were not further damaged during recent events.

“NOC is therefore lifting force majeure at all Oil Crescent ports. Exports will resume immediately from Zuetina and Ras Lanuf, and will continue at Brega, in accordance with the instructions given to me by House of Representatives and the Presidency Council. Exports will resume from Es Sidra as soon as possible,” he declared.

Force majeure is a legal term that frees a company from any contractual obligation due to circumstances beyond its control.

The latest developments are viewed by the public as an extremely positive who are mobilizing in support of the national army which has broken the stalemate around the resumption of oil exports which lasted for three years.

Force majeure is a legal protection from liability invoked when performance of a contract is interrupted due to events beyond the control of the contractual parties. Force majeure was declared at Es Sidra and Ras Lanuf in December 14, 2014. Both ports were damaged in attacks in January 2016. Force majeure was declared at Zuetina on November 3, 2015. Force majeure was not declared on exports from Brega.

Sanalla commended Libyan leaders and politicians “for choosing unity of Libya and reconciliation at this critical juncture”.

He said the developments on 11 and 12 September had “the potential to escalate, with potentially devastating consequences for the nation and our petroleum industry. Instead, we have found a shared interest in letting the oil flow, and the wisdom of that decision needs to be recognized".

http://www.tripolipost.com/articledetail.asp?c=1&i=11135&utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+TheTripoliPost+%28The+Tripoli+Post%3A+Libya%27s+News+and+Views%29

Still holding 900 DWTI.

Libya and Nigeria have the potential to bring back 800k barrels of oil online within a month.

Algiers meeting will end with no freeze or cut.

Novembers OPEC meeting will end like the last one.

I see oil headed to the low $30's before the year is over and low $20's by February.

Baker Hughes: Oil Rig Count +7 to 381

Genscape reported about 220k build in Cushing. API says 1.3m draw, oil popped. Looks like a setup for another epic dissapointment. Builds in the heart of summer driving season folks. WAKE UP.

If $34.50ish falls oil is headed to $30 and if that falls oil will make new lows for the year, at that point net longs will be rushing to the gate to liquidate and it will be a true flush out. I still expect this to all end around $21. I think mid September, during fall maintenance season is when this will all go down. We'll see...

200 day getting violated. Not much support between here and $35 once it finally breaks. Oil is going to crash come this fall refinery maintenance season, with a possible storage crisis in Cushing.

Wake UP!

Oil crashing prior to Fall Maintenance season. Genscape reported a 1.1 million barrel build yesterday. Looks like Cushing Oklahoma could experience a storage crisis this Fall. Still on target for my $21 crude oil price!!! UWTI is in for a major crash!!!

WAKE UP!!

USD 97.105

That means oil is headed much lower.

Bought 25 more DWTI on margin yesterday, 825 total.

Gasoline +1213K vs -1000K expected

Distillate +4058K vs 0K expected

Refinery utilization -0.2% vs +0.4% exp

Production up 0.7% w/w

Production up 57K bpd w/w

This time of year, should be seeing bigger draw downs in refined products, not builds.

API surveys are voluntary, whereas an accurate completion of the EIA surveys is mandatory and enforced by law.

Keeping in mind the government's rigorous standards, and that companies are compelled to report inventories to the government, the report is "theoretically more accurate," therefore EIA numbers are the only ones that matter.

A Surprise drop in refinery utilization could be the cause for the overall Build.

Philadelphia refinery cuts output as gasoline margins sink -source

U.S. East Coast refiners have cut production in recent days amid mounting concerns that a glut of supply will hammer profits even as motorists are expected to hit U.S. roads in record numbers this summer.

Philadelphia Energy Solutions was the latest East Coast refiner to clip production, reducing output by 10 percent Tuesday night at the 135,000 barrel-per-day Point Breeze section of the Philadelphia refinery complex, a source told Reuters on Wednesday.

A Philadelphia Energy Solutions spokeswoman declined to comment on Wednesday.

That news follows Delta Air Lines Inc's decision to cut production by 16 percent at its 185,000 bpd refinery in Trainer, Pennsylvania, a source told Reuters on Tuesday, citing economic and operational reasons.

The steps are unusual because refiners often run at high rates during the summer to meet gasoline demand. It also marks the second round of run cuts this year.

About 40,000 bpd has been cut on East Coast, just a small portion of the region's capacity, but the measures reflect, in part, deepening concerns about refiners' profits.

Gasoline margins 1RBc1-CLc1 have plummeted more than 30 percent in the past eight trading sessions to February lows. That spread was down nearly 6 percent Wednesday.

"The fundamental weakness in gasoline markets is being exemplified by the RBOB crack spread, which is closing in on levels which would encourage refiners to dial back on runs," said Matt Smith, analyst at New York-based oil cargo tracker Clipperdata.

Delta has since restored roughly 10,000 bpd of the cuts related to operations, a source said Wednesday, but the plant is still running about 11 percent short of capacity, the source said. Delta did not respond to requests for comment by email.

Phillips 66 has cut production in the 135,000 bpd gasoline-making unit at its Bayway refinery in Linden, New Jersey, by roughly 6,000 bpd, a source told Reuters on Wednesday, but the source said the reduction is not believed to be related to poor margins.

Phillips 66 declined to comment.

The U.S. East Coast is brimming with petroleum products, with inventories of gasoline at 72.5 million barrels as of last week, substantially above the five-year average.

The 135,000 bpd Point Breeze section of the Philadelphia refinery runs lighter, sweet crudes, like that from the Bakken shale of North Dakota and from the North Sea.

Source

http://www.reuters.com/article/usa-refinery-cuts-idUSL1N19S0M6

If EIA confirms any Build tomorrow WTI is in for a shellacking. API has been unreliable last few weeks, so we'll see...