News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

is looking for undervalued stocks

RyGuy

![]()

is looking for undervalued stocks

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

is looking for undervalued stocks

Hope your doing well Chevy....

What angers me about this entire situation was the behavior of the executive team.

They drew down a portion of the credit facility to pay themselves bonuses prior to filing for bankruptcy. This should be a criminal case against these executives.

https://www.otcmarkets.com/filing/html?id=13131141&guid=FC53UnwS_ftC93h

All while in their previous investor presentation they painted a much rosier picture of increased revenues, paying down debt, better debt ratios, and increased profits as hedges rolled off over the next year.

Meanwhile institutional investors were dumping massively 14 days prior to the bankruptcy filing, without filing any kind of Form 4’s to reflect changes in their ownership. Insider knowledge that no one will be punished for.

This good ole boy club with executives and their sweetheart compensation packages for each other to only do this. I'm pissed at these criminals. That is essentially what they are, and they behaved no better than sleazy penny stock executives.

https://www.otcmarkets.com/filing/html?id=13173742&guid=FC53UnwS_ftC93h

I'm sorry, but ineffective management, do not warrant the salaries they command. You do not perform, you deserve no bonus.

They should have managed the business with the fiduciary duties that were intrusted in them.

$1.5 Billion in Assets

$1.2 Billion in Liabilities

$470 Million in Annual Revenues

$274 Million in Shareholder Equity.

This is what you should do as an executive of a company.

I hope this failure follows Sloan and Midget for the rest of their professional careers.

It was institutional ownership that sold to boot, and did not file the requisite forms to disclose.

Holy Crap... Totally shocking today's action to me....

WTH

Fortune 500 company and it feels like a penny stock. ARRRRGGGGHHHH

My feelings exactly... plus the executives painted a much rosier picture in their investor presentation last September.

The investment banks were dumping before the announcement into the market on inside information. Nor did they file any change of ownership forms.

Gotta say, I am a little shocked with the market behavior in regard to a sizeable pending distribution with only a few days left.

Sure feels like a concerted effort to keep NGL down.

But if I say it too much, I start to feel like I sound like a conspiracy theorist.

LOL

Zacks equity research...

Pretty much shows the valuation multiples that I have mentioned previously.

https://www.zacks.com/stock/news/372139/is-ngl-energy-partners-lp-ngl-a-great-value-stock-right-now

$NGL .39 Div declared

Payable May 15; for shareholders of record May 7; ex-div May 6.

https://seekingalpha.com/news/3453969-ngl-energy-partners-declares-0_39-dividend

.39 Div declared

Payable May 15; for shareholders of record May 7; ex-div May 6.

https://seekingalpha.com/news/3453969-ngl-energy-partners-declares-0_39-dividend

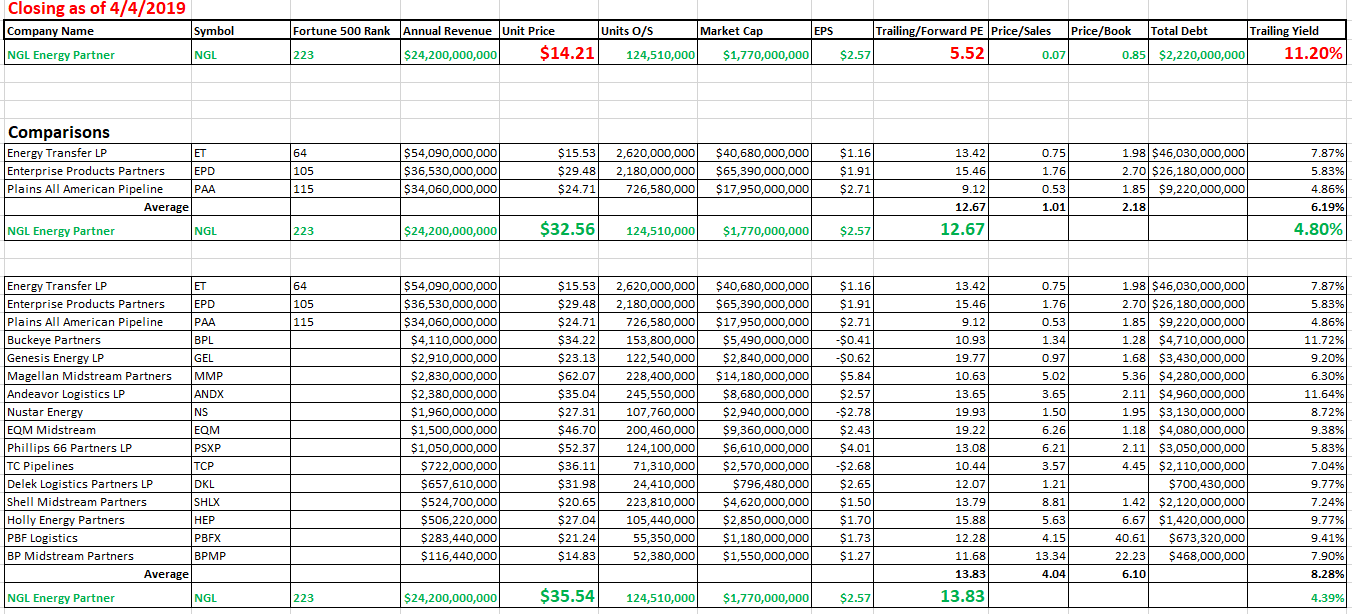

NGL should be at minimum $18.99 to $24.88 to match the average dividend yields of the other Pipeline/Transportation MLP's.

Until the better valuation average of it's peers PE/Ratio is realized of $32.23 to $35.53.

Just my opinion. But hopefully we will see the upside market correction to $19 begin soon.

@cvpayne The market has significantly undervalued $NGL. NGL has increased their leadership position in Water solutions in the Permian Basin. #223 ranked U.S. Fortune 500 company. Compared to its Pipeline/Transportation peers NGL is undervalued by close to half. Should be $24 now pic.twitter.com/FbPrhkugeM

— BigWigg (@RyanWiggins4) April 22, 2019

I would be stunned if any regular poster on this board would ask that.

Hell no...

I'm just venturing a guess that NGL's EBITDA numbers should continue to improve substantially versus the years prior with the retail propane divisions and the other non core assets that were sold, and higher margin water services added into the mix.

Yahoo shows NGL based on previous EBITDA of $486 to be at a EV/EBITDA of 8.86

https://finance.yahoo.com/quote/ngl/key-statistics?p=ngl

With improving numbers on the last Q at $596 Million for 9 months and $205 Million for the Q, I'm thinking NGL should be around $800M for the year end.

Which at current enterprise value would put NGL around 5.35 EV/EBITDA

Compared with other Pipeline/Transportation companies that would again leave substantial room for appreciation.

Company.....EV/BITDA

NGL...........5.35

EPD..........13.27

ET.............11.21

PAA..........10.81

https://finance.yahoo.com/quote/ngl/key-statistics?p=ngl

https://finance.yahoo.com/quote/epd/key-statistics?p=epd

https://finance.yahoo.com/quote/et/key-statistics?p=et

https://finance.yahoo.com/quote/PAA/key-statistics?p=PAA

Or my belief of $32 being possible.... I like Hotel's higher number $47 even better.

I wonder at what point the big oil and gas exploration and production companies will begin to start gobbling up the pipeline transport and logistics companies?

The cost to acquire NGL is chump change in comparison to the Anadarko deal.

Wow what a nice day for those shareholders! I believe our day is coming soon!

Gas prices at the pumps have been soaring over the past few weeks. I’m wondering if those prices are going to start to be reflected in further appreciation valuations of energy stocks soon.

Target $32.78. Updated Excel Spreadsheet market capitalization to show that even a double in price of NGL would not be absurd.

All of those stocks above are on the Alerian MLP screener, and are listed as Pipeline/Transportation K-1 issuing MLP's. All are considered in the same industry segement as NGL, and as you can see NGL is significantly undervalued in comparison to them all.

Here is the link to the Alerian MLP screener:

https://www.alerian.com/education/mlp-screener/

When looking at the screener, you can filter the industry segments. NGL is listed in the Pipeline/Transportion segment.

Plains GP Holdings (PAGP) probably the most likely comparable MLP in general. Yet NGL is still undervalued in comparison by a factor or 2-3 times. Also close ccomparable in the Pipeline Transportation segment is (PAA) Plains All American Pipeline.

https://finance.yahoo.com/quote/NGL/key-statistics?p=NGL

https://finance.yahoo.com/quote/PAA/key-statistics?p=PAA

https://finance.yahoo.com/quote/PAGP/key-statistics?p=PAGP

https://finance.yahoo.com/quote/TCP/key-statistics?p=TCP

https://finance.yahoo.com/quote/SHLX/key-statistics?p=SHLX

https://finance.yahoo.com/quote/PSXP/key-statistics?p=PSXP

https://finance.yahoo.com/quote/PBFX/key-statistics?p=PBFX

https://finance.yahoo.com/quote/NS/key-statistics?p=NS

https://finance.yahoo.com/quote/MMP/key-statistics?p=MMP

https://finance.yahoo.com/quote/HEP/key-statistics?p=HEP

https://finance.yahoo.com/quote/GEL/key-statistics?p=GEL

https://finance.yahoo.com/quote/ET/key-statistics?p=ET

https://finance.yahoo.com/quote/EQM/key-statistics?p=EQM

https://finance.yahoo.com/quote/EPD/key-statistics?p=EPD

https://finance.yahoo.com/quote/DKL/key-statistics?p=DKL

https://finance.yahoo.com/quote/BPMP/key-statistics?p=BPMP

https://finance.yahoo.com/quote/BPL/key-statistics?p=BPL

https://finance.yahoo.com/quote/ANDX/key-statistics?p=ANDX

Here is a list of Fortune 500 companies. Based on Revenue there is only three other MLP's larger and with more annual revenues than NGL.

http://fortune.com/fortune500/

64 - Energy Transfer

105 - Enterprise Products Partners

115 - Plains GP Holdings

223 - NGL Energy Partners

Looks like NGL is still a potential more than double in price from here. $32 here we come!

Charles Payne has responded to me in the past on companies I have mentioned to him.

It would be nice to have someone with platform clout to mention how undervalued NGL is on a platform like Fox Business.

@cvpayne wanted to show you what I believe to be a tremendously undervalued MLP in comparison to it's peers. NGL - NGL Energy Partners. Currently ranked #223 on U.S. Fortune 500 list with an 11.2% yield. To be valued with it's Pipeline Peers it should be $32 - $35 pic.twitter.com/UyajkqGKnQ

— BigWigg (@RyanWiggins4) April 7, 2019

I just realized I didn’t update the market cap formulas to show the potential MC at higher EPS metrics.

Thanks TH.

So everything here and Heaping Crappers and other analysts reports I have periodically read, it seems everyone has always complained about the misses on earnings projections. As if the executives in the past couldn’t understand their own business.

Also lower margined services.

With all that revenue their EPS is minuscule in comparison with the others. NGL’s got one of the lowest unit counts out of all of them, while the others like ET, EPD are reflecting earnings per share of a dollar or more with billions of units outstanding too.

NGL’s refocus on higher margin services, should continue to improve those numbers. We’ll get a year to see the numbers with the retail propane business and their little to no margins not attached.

Those other companies are also reflected positively in their market capitalization. The big ones being valued at $30-$50 billion.

I find great solace in these comparisons that a double for NGL still only valued them at $3.5 Billion. So all the issues mentioned above are still priced in if they were valued at similar EPS metrics.

These comparisons I think help me decide which one is the best investment opportunity for price appreciation.

JMO

-Ryan

I don’t think it will happen tomorrow. LOL......but that would be nice. I still give 8 months

If they continue improving Earnings, there should be a correction, to bring them closer to their peers. I would be ok feeling like its Christmas every day for the next 8 months. LOL

I think my point behind these valuation charts is simply that all of the others that are similar business models to NGL are all valued nearly 2 times or higher.

There is a disconnect between the market and NGL’s valuation in so many facets. Could it be because of past missed projections? That’s what I keep hearing. Hopeythey have learned their lesson in that regard.

NGL has one of the lowest total debt loads out of all of them, now since they paid down debt last year. They are one of the four pipeline MLP’s that is a Fortune 500 company. Bring on $32!

NGL Price Target $32-$35

Increasing my price target to $32-$35. I take back my $28 price prediction.

All of those stocks above are on the Alerian MLP screener, and are listed as Pipeline/Transportation K-1 issuing MLP's. All are considered in the same industry segement as NGL, and as you can see NGL is significantly undervalued in comparison to them all.

Here is the link to the Alerian MLP screener:

https://www.alerian.com/education/mlp-screener/

When looking at the screener, you can filter the industry segments. NGL is listed in the Pipeline/Transportion segment.

Plains GP Holdings (PAGP) probably the most likely comparable MLP in general. Yet NGL is still undervalued in comparison by a factor or 2-3 times. Also close ccomparable in the Pipeline Transportation segment is (PAA) Plains All American Pipeline.

https://finance.yahoo.com/quote/NGL/key-statistics?p=NGL

https://finance.yahoo.com/quote/PAA/key-statistics?p=PAA

https://finance.yahoo.com/quote/PAGP/key-statistics?p=PAGP

https://finance.yahoo.com/quote/TCP/key-statistics?p=TCP

https://finance.yahoo.com/quote/SHLX/key-statistics?p=SHLX

https://finance.yahoo.com/quote/PSXP/key-statistics?p=PSXP

https://finance.yahoo.com/quote/PBFX/key-statistics?p=PBFX

https://finance.yahoo.com/quote/NS/key-statistics?p=NS

https://finance.yahoo.com/quote/MMP/key-statistics?p=MMP

https://finance.yahoo.com/quote/HEP/key-statistics?p=HEP

https://finance.yahoo.com/quote/GEL/key-statistics?p=GEL

https://finance.yahoo.com/quote/ET/key-statistics?p=ET

https://finance.yahoo.com/quote/EQM/key-statistics?p=EQM

https://finance.yahoo.com/quote/EPD/key-statistics?p=EPD

https://finance.yahoo.com/quote/DKL/key-statistics?p=DKL

https://finance.yahoo.com/quote/BPMP/key-statistics?p=BPMP

https://finance.yahoo.com/quote/BPL/key-statistics?p=BPL

https://finance.yahoo.com/quote/ANDX/key-statistics?p=ANDX

Here is a list of Fortune 500 companies. Based on Revenue there is only three other MLP's larger and with more annual revenues than NGL.

http://fortune.com/fortune500/

64 - Energy Transfer

105 - Enterprise Products Partners

115 - Plains GP Holdings

223 - NGL Energy Partners

Looks like NGL is still a potential more than double in price from here. $32 here we come!

If DK can go from $30 to $60 in 6 months in 2018. I got a feeling NGL can go from $14 to $32 in 8 months.

Increasing my price target to $32-$35. I take back my $28 price prediction.

All of those stocks above are on the Alerian MLP screener, and are listed as Pipeline/Transportation K-1 issuing MLP's. All are considered in the same industry segement as NGL, and as you can see NGL is significantly undervalued in comparison to them all.

Here is the link to the Alerian MLP screener:

https://www.alerian.com/education/mlp-screener/

When looking at the screener, you can filter the industry segments. NGL is listed in the Pipeline/Transportion segment.

Plains GP Holdings (PAGP) probably the most likely comparable MLP in general. Yet NGL is still undervalued in comparison by a factor or 2-3 times. Also close ccomparable in the Pipeline Transportation segment is (PAA) Plains All American Pipeline.

https://finance.yahoo.com/quote/NGL/key-statistics?p=NGL

https://finance.yahoo.com/quote/PAA/key-statistics?p=PAA

https://finance.yahoo.com/quote/PAGP/key-statistics?p=PAGP

https://finance.yahoo.com/quote/TCP/key-statistics?p=TCP

https://finance.yahoo.com/quote/SHLX/key-statistics?p=SHLX

https://finance.yahoo.com/quote/PSXP/key-statistics?p=PSXP

https://finance.yahoo.com/quote/PBFX/key-statistics?p=PBFX

https://finance.yahoo.com/quote/NS/key-statistics?p=NS

https://finance.yahoo.com/quote/MMP/key-statistics?p=MMP

https://finance.yahoo.com/quote/HEP/key-statistics?p=HEP

https://finance.yahoo.com/quote/GEL/key-statistics?p=GEL

https://finance.yahoo.com/quote/ET/key-statistics?p=ET

https://finance.yahoo.com/quote/EQM/key-statistics?p=EQM

https://finance.yahoo.com/quote/EPD/key-statistics?p=EPD

https://finance.yahoo.com/quote/DKL/key-statistics?p=DKL

https://finance.yahoo.com/quote/BPMP/key-statistics?p=BPMP

https://finance.yahoo.com/quote/BPL/key-statistics?p=BPL

https://finance.yahoo.com/quote/ANDX/key-statistics?p=ANDX

Here is a list of Fortune 500 companies. Based on Revenue there is only three other MLP's larger and with more annual revenues than NGL.

http://fortune.com/fortune500/

64 - Energy Transfer

105 - Enterprise Products Partners

115 - Plains GP Holdings

223 - NGL Energy Partners

Looks like NGL is still a potential more than double in price from here. $32 here we come!

If DK can go from $30 to $60 in 6 months in 2018. I got a feeling NGL can go from $14 to $32 in 8 months.

I’m think a comparable valuation to the rest of their peers is coming... it may take the rest of the year to get there, but.........bring on $28

That’s a nice paper route.

Thanks Jugs.....

I personally find the comparisons quite staggering and to see NGL still this low. In comparison to those others NGL’s debt load is minimal.

Hopefully as NGL over the next couple of quarters continues to to show increased earnings and lower revolving credit debt and any company buybacks, we will get a lot closer to that $28 number.

Here is the Alerian MLP screener with information as of March 15th, 2019.

https://www.alerian.com/education/mlp-screener/

When looking at the screener, you can filter the industry segments. NGL is listed in the Pipeline Transportion segment. Below are all of the K-1 issuing MLP's that are in Pipeline Transportation.

The closest comparable that I can see in the Pipeline Transportation segment is PAA Plains All American Pipeline, and Plains GP Holdings. But Plains GP holdings is 1099 issuing partnership, not a K-1 issuing. Yet, NGL is still far undervalued in comparison.

https://finance.yahoo.com/quote/NGL/key-statistics?p=NGL

https://finance.yahoo.com/quote/TCP/key-statistics?p=TCP

https://finance.yahoo.com/quote/SHLX/key-statistics?p=SHLX

https://finance.yahoo.com/quote/PSXP/key-statistics?p=PSXP

https://finance.yahoo.com/quote/PBFX/key-statistics?p=PBFX

https://finance.yahoo.com/quote/PAA/key-statistics?p=PAA

https://finance.yahoo.com/quote/NS/key-statistics?p=NS

https://finance.yahoo.com/quote/MMP/key-statistics?p=MMP

https://finance.yahoo.com/quote/HEP/key-statistics?p=HEP

https://finance.yahoo.com/quote/GEL/key-statistics?p=GEL

https://finance.yahoo.com/quote/ET/key-statistics?p=ET

https://finance.yahoo.com/quote/EQM/key-statistics?p=EQM

https://finance.yahoo.com/quote/EPD/key-statistics?p=EPD

https://finance.yahoo.com/quote/DKL/key-statistics?p=DKL

https://finance.yahoo.com/quote/BPMP/key-statistics?p=BPMP

https://finance.yahoo.com/quote/BPL/key-statistics?p=BPL

https://finance.yahoo.com/quote/ANDX/key-statistics?p=ANDX

Here is a list of Fortune 500 companies. Based on Revenue there is only two MLP's larger than NGL.

http://fortune.com/fortune500/

105 - Enterprise Products Partners

115 - Plains GP Holdings

223 - NGL

Plains GP Holdings probably the most likely comparable MLP in general. Yet NGL is still undervalued in comparison by a factor or 2-3 times.

https://finance.yahoo.com/quote/PAGP/key-statistics?p=PAGP

Looks like NGL is still a potential double in price to me. $28 here we come!

Hey Pete, I was just looking at the Fortune 500 list. It looks like we were #167 in 2016.

http://fortune.com/2016/06/28/fortune-500-revenue-growth/

The most recent list appears to be 2018's numbers still.

http://fortune.com/fortune500/list/

Honestly, I don't see how 2018 numbers can be correct though, as the rankings are based on revenues.

It appears NGL has $24-26 Billion revenue, which should place them around the rank of 120 or so. Not sure why Fortune has them ranked so low.

That's just aweful.

Thanks Chevy

Thanks Maz

This falls squarely with Scott Sloan and Ryan Midgett.

Drawing additional monies from the credit facility for “Corporate Purposes” as stared in theb12/31/2018 8-K, to pay themselves absurd salary’s and bonus compensation for doing a piss poor job. They haven’t performed to deserve that money, nor have any of the directors.

They painted a more than rosey picture to investors, of reduction of debt, increased revenues, and improving cash flows, while they had this as a planned possibility.

And who was given inside information to continue to dump an enormous amount of shares at the bid over the 14 trading days prior to the chapter 11 filing.

I think that is an example form for parties with claims against the debtor to use. As nice as it would be, I don’t think it means they will be accumulating common stock.

I could be wrong though, as I was obviously wrong on their going forward concerns.

No it will not be halted. It will continue to trade, the problem is getting back what you paid for it.

Held...

I was at court hearing with my wife this morning, regarding guardianship of her mother. So of all the days for this to occur.

I am so pissed at the ineptitude of Scott Sloan and Ryan Midgett, they should rot in a cell.

Personally.... I would love to know who had, and how did they get the inside information to trade/sell on in the 14 days leading up to today...

The lying executives sure can post a rosey picture of their financial health and going forward operations....

https://www.vnrenergy.com/wp-content/uploads/2018/08/Vanguard-Presentation-August-2018.pdf

In the 14 days up to the time of this mornings release 8,042,825 in Volume....

3/29/2019 … 389,708

3/28/2019 … 770,626

3/27/2019 … 569,999

3/26/2019 … 1,170,212

3/25/2019 … 435,212

3/22/2019 … 802,231

3/21/2019 … 687,421

3/20/2019 … 814,037

3/19/2019 … 609,003

3/18/2019 … 778,953

3/15/2019 … 465,478

3/14/2019 … 181,087

3/13/2019 … 150,220

3/12/2019 … 218,638

Total... 8,042,825

Meanwhile the entire year prior 3/12/2018 to 3/12/2019 there were only 4,242,983 shares traded.

Only 4.7 Million in the float. So who had the information prior and traded and made a market on inside information.

R. Scott Sloan and Ryan Midgett deserve to never be exectives any where else again.

They haven't done anything to justify those wages and compensation to this point.

Exactly. They should make their money, when their performance and company meeting goals warrants them getting paid.

This good ole boy club with executives and their sweetheart compensation packages for each other to only do this. I'm pissed at these no good crooks.

https://www.otcmarkets.com/filing/html?id=13173742&guid=FC53UnwS_ftC93h

I'm sorry, but ineffective management, do not warrant the salaries they command.

So they drew down a portion of the credit facility to pay themselves.

https://www.otcmarkets.com/filing/html?id=13131141&guid=FC53UnwS_ftC93h

How about you manage the business with the fiduciary duties that were intrusted in you.

$1.5 Billion in Assets

$1.2 Billion in Liabilities

$470 Million in Annual Revenues

$274 Million in Shareholder Equity.

This is what you do as executive leadership.

You and me both...

This still doesn't make any sense to me.

I see the NT 10-K was filed. So it looks like they have 15 additional days.

I don't know why they would do this this.

They financials have been improving each quarter, and they were in better shape than they were than when they emerged from bankruptcy in 2017.