News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

biomaven0

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

>>NTRP

"(p < 0.1, one-tailed)"

You don't really need to read any of the PR aside from this parenthetical.

>>So it still means the pricing now is $1 buck per share(excluding the warrants).

No - Dew is correct here. The $1 is for the combo, and even if the warrants have no intrinsic value now, they do have time value. So you have to subtract that time value from the $1 (or $0.95) for the combo to see what the implied price of the stock is. For a high volatility stock like this, a 5-year warrant at-the-money is worth something near half the price of the common.

I wonder if you can make an antitrust argument? This is effectively a "tie" albeit the same product across multiple indications rather than multiple products.

https://www.ftc.gov/tips-advice/competition-guidance/guide-antitrust-laws/single-firm-conduct/tying-sale-two-products

>>Humira pricing

I am reliably informed that a CEO of one of the competitors in the same space (RA biologics) claimed he could set the price of his rival drug at zero and it still wouldn't get on some formularies.

I can't say I fully understand the dynamics, but it has something to do with rebates and Humira having a broader label. So I could speculate that the rebates depend on hitting a minimum sales level and if you removed RA sales from Humira there would be a huge hit on the other indications.

Peter

If this tachyphylaxis argument is correct, then there is potentially another risk for AKBA/GSK - changing response to the drug over time (months not weeks). What is worse, such enzyme-linked changes tend to be quite variable across different patients. And because it is a negative feedback situation, increasing the dose further might well produce diminishing returns.

So bottom line I really don't know if this is going to be an issue for AKBA or GSK or not, but does certainly add to the risk profile. It is perhaps interesting that GSK tested very high doses of their drug before choosing one of the lowest doses they had tested for their Ph III.

Peter

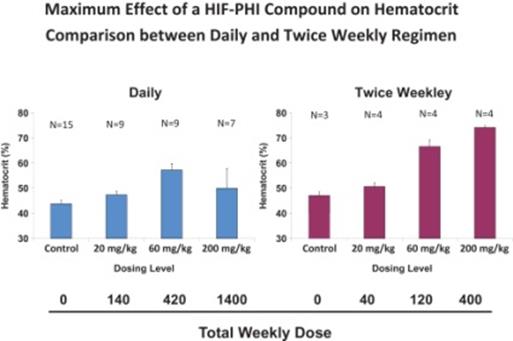

Digging up this old AKBA post because it was linked recently:

>>PS: i too was struck by the lack of dose response, but it probably has something to do w trial design such as ESA rescue, transfusion, and dose escalation after 8 weeks

So here is my big concern with AKBA drug:

Doses in $AKBA chart are 300mg QD, 450mg QD and 450 TIW. Suggests to me tachyphylaxis mechanism w/ daily dosing as $FGEN has claimed pic.twitter.com/DunX7OWQ93

— Peter Suzman (@Biomaven) April 25, 2017

The primary driver of FGEN (by far) is going to be roxadustat safety. (There is some potential volatility from their ctgf drug of course, but that's not relevant to the discussion).

If roxa has a safety issue of some sort, I'd predict it's 50:50 whether AKBA would go up or down on the news. In my book, that makes it a bad hedge.

Peter

>>True, it's not a "pure" hedge due to the possibility of a class effect that takes down both companies; however, I figure that's a pretty unlikely outcome.

No, I think it is quite plausible. Roxa has seemed very clean on obvious side effects, but some weird MACE risk is always possible. In that event AKBA would go down in sympathy. It's only if roxa exhibited some clearly idiosyncratic effect that AKBA would benefit - some DILI say. But even there the AKBA absolute dosage is way higher, so (all other things being equal) I'd say the AKBA risk is higher there too.

I posted on twitter about my concerns on AKBA dosing strategy.

Peter

Thanks.

I'm thinking of the pricing dynamics as the market matures. My sense is that JNJ would have the opportunity to cut pricing in this one segment without engendering a pricing war. So basically they could segment the market and aim at the low end. Could also market to prison populations and the like.

Any idea of the proportion of remaining US HCV patients that are in this "easy" bucket (non-cirrhotic, non-GT3)? I also assume that these are also the least likely to have already been diagnosed.

On compliance, I figure that payers might be OK with a 6-week script. Anything that increases compliance is in their interest - they don't want to have to re-treat.

Peter

>>JNJ/ACHN—3-DAA* HCV regimen has good-news/bad-news—mostly bad

So here's my question: Is it not plausible that the bulk of the yet untreated patients in the US fall in the non-cirrhotic GT1 category? My assumption is that the "tough" patients have been treated first and that the bulk of the residue constitute "easy" patients.

Thoughts? Will the market demand a pan-genotype treatment, or will patients still be genotyped and segregated into categories to be treated accordingly? If the latter, I could see a role for a 6 week treatment for the easy patients. So will JNJ take this forward?

>>Could a combination with other elements get a patent?

Yes, you could get a patent for a non-obvious combo. It wouldn't be a composition of matter patent but could still have some value. But once you are into combos, trials (and the FDA) become tougher.

There has already been one attempt at exploiting one of the marijuana pathways - the doomed anti-obesity drug rimonabant. It does the opposite of what marijuana does (it's a CB1 antagonist) and it did cause weight loss (anti-munchies!), but also caused depression and other psychiatric issues and was taken off the market after initial approval in Europe.

The problem is that cannabis is a complex mixture of natural compounds, none of which are patentable.

The same is true of tobacco actually, with many nicotinic compounds that might well have some medical efficacy. But so far companies have struck out trying to isolate and make drugs in that area.

Western medicine is focused on finding drugs that do one thing well. Many natural compounds potentially do good things across multiple areas, but the effect size is almost always small. So trials to prove efficacy are very hard, and the lack of patents makes things that much harder.

>>700 MEDICINAL USES OF CANNABIS SORTED BY DISEASE

I believe I could come up with a comparable list for curcumin or pomegranate.

Most compound that are claimed to work in everything pretty much work in nothing.

>> The “authorized generic” nomenclature is curious (and misleading) insofar as TEVA does not have authorization from GSK to sell the product, and it must be marketed as a distinct branded drug (although it is priced like a generic).

The way I read their PR, it is an authorized generic for their own branded product, not for Advair.

AZN has a standstill agreement with FGEN in place expiring at the end of 2019.

FWIW, the GLGP drug is an order of magnitude less potent than its rivals. Not a red flag, but does raise the possibility of unexpected AEs somewhat.

The INCY rejection does raise the bar here somewhat - the FDA is going to be just as picky on the next candidate.

You can read the detailed EMA analysis here:

http://www.ema.europa.eu/docs/en_GB/document_library/EPAR_-_Summary_for_the_public/human/004085/WC500223726.pdf

That's a lot more data than we get as investors in deciding whether approval is likely or not, and nothing there suggests a dosing issue that I can see.

"[A] more robust response was shown [for 4mg] regarding the prevention of structural bone damage in Study JADX, and higher remission rates were achieved for the 4 mg dose versus the 2 mg dose in the multi therapy resistant bDMARD-IR population (Study JADW)."

Peter

Interesting preclinical paper - FGEN's roxadustat dosed intermittently not only did not enhance tumor growth (as some have feared it might) but sensitized them to cisplatin:

https://www.nature.com/articles/srep45621

Here is the Weissman paper on a CD47+Rituxan combo:

https://www.ncbi.nlm.nih.gov/pmc/articles/PMC2943345/

You absolutely do get responses to rituxan with re-treatment after a relapse following initial rituxan treatment - indeed the response rate is (surprisingly) not a lot worse than with the initial treatment.

But I'm guessing that these patients were actually resistant to rituxan.

Here's a potential rationale for MRD AML being a good indication:

http://www.siliconinvestor.com/readmsg.aspx?msgid=31057031

>>only one response out of 27 pts given monotherapy

But 1/1 with MRD AML, which the company said at Cowen was the indication they currently liked best.

Some more details here - this patient relapsed after a stem-cell transplant:

http://www.siliconinvestor.com/readmsg.aspx?msgid=31056707

It's going to depend on the details of the patient, but potentially very significant in my view. I would guess that MRD with good prognosis wouldn't be enrolled in this trial to begin with.

>> In the AML cohort, one patient with minimal residual disease (consisting of 0.7% abnormal blasts at baseline) obtained a complete molecular remission after 4 infusions of TTI-621. A second marrow analysis at week 8 confirmed a complete molecular remission, the patient continues to tolerate weekly infusions of TTI-621 and remains in continued remission for 15+ weeks.

This is very good news.

>>The fusions and some of the driver mutations seem to out-compete other clones and crowd out other pathways and so they tend to be mutually exclusive with other mutations and upregulated pathways.

No sooner did I post this than I saw this LOXO PR for a glioblastoma that had only part of the tumor fusion-driven:

http://finance.yahoo.com/news/loxo-oncology-announces-proof-concept-203000489.html

The fusions and some of the driver mutations seem to out-compete other clones and crowd out other pathways and so they tend to be mutually exclusive with other mutations and upregulated pathways. So that's why they seem to be an effective "single point of attack."

Your analysis of BPMC vs. LOXO concords with mine - LOXO is going to have a much harder time identifying patients for their drug. I'll also bet BPMC's RET is going to be significantly better than LOXO's RET (which is from ARRY I believe).

>>BPMC’s BLU-285 (inhibitor of either a mutant form of KIT or a mutant form PDGFRa – although I still haven’t figured out how that was accomplished)<<

KIT and PDGFRa are structurally very similar - right next to each other (with FLT3) on the kinome tree.

Peter

I recall when Sepracor was trying to make a Xopenex asthma inhaler using non-CFC propellant. They struggled for more than a year before licensing 3M technology. And that was not a generic - the degree of difficulty for a generic inhaler that has to closely match the original is that much higher. I assume GSK also has a bunch of patents on the device that need to be circumvented.

Inhalers are really hard - it's tricky to get a reproducible dose. Lots of variables (particle size, amount of air, velocity, duration, etc.) determine how much drug gets to the lungs and how much end up in the mouth and throat. The originator can adjust the drug concentration to get the dose they want - they just need to be consistent, but a substitutable generic needs to match the original closely.

But Viagra spending stayed firm...

Interesting quote on pricing ($37k/yr) from a few months back:

REGN CEO 2/16/17: 'We want to discuss with payers and say, hey, look, we can work together. When a responsible manufacturer comes with a breakthrough product at a price that is really tied to the value delivered, and that everybody can agree on that. Then the payers have to do their part. The payers have to make sure that access, formulary coverage, it's there from the beginning. They don't have these arbitrary delays of six months or this and that. It's there from the beginning. It's not putting these subtle and not so subtle barriers. Believe me, they know every trick in the book. They know if they ask a doctor to fill out a 10-page form just how much of a barrier that is and how many prescriptions that will suppress. And what I want is, I don't want any of those shenanigans. I want coverage. I want access. I want it fair. And what I want to give you in return or in exchange is a breakthrough product at a fair and responsible price. I think that everybody wins when we set that paradigm. I think we can be the new paradigm for how pharma and the payers can actually work together to do the right thing. But it all depends on us being responsible and the payers being responsible.'

And positive reaction by Express Scripts to the pricing:

https://www.forbes.com/sites/matthewherper/2017/03/28/regenerons-new-drug-price-could-disappoint-everyone-heres-why-thats-a-good-thing/#4edfdd765db4

SM is largely driven by PDGFR, while GIST is largely driven by KIT.

Frontline KIT is handled well by Gleevec - it's only the mutations engendered by prolonged treatment that require a different drug. The BPMC drug would work well in frontline GIST driven by PDGFR, but that's a small fraction.

Yes - it's a very significant holding (mostly indirect) for me.

Blu-285 is a magic drug for advanced systemic mastocytosis. Not a huge incidence but patients will likely stay on their drug for many years and revenue should build very nicely for many years. So a very nice long-term buy and hold. Should also work well in 2nd/3rd/4th-line GIST for some patients (not frontline though). Their RET drug looks to be very good too (likely better than Loxo's).

It's in my charity portfolio on SI and I've discussed it some on twitter and SI.

Peter

>>AZN’s Tagrisso approved in China

Many people are not aware that EGFR-driven lung cancer is an order of magnitude more prevalent in China than in the US, so this is very significant.

AZN is (as best i can tell) already the biggest multinational in the Chinese prescription drug market, and is 50:50 partner with Fibrogen for roxadustat in China.

>>If XON were to spin-off more of AQB and thereby reduce its equity stake to <50% (from its current 58% stake), AQB might be able to utilize its tax-loss carryforward more effectively

You are assuming that the Sec 382 limitation goes away in that event - I do not think that is the case (at least in any straightforward manner).

Copy of my SI post on FGEN:

Nothing dramatic I heard in FGEN CC - mostly stuff we already knew.

This is a good summary:

https://twitter.com/MauriceOnTW/status/837067709561126913

And here's my humorous tweet:

LOL the $FGEN p value for efficacy vs. placebo in China Phase III:

— Peter Suzman (@Biomaven) March 1, 2017

(p<0.000000000000001)

Kyprolis is about a $800m/year product right now, and that's without any convincing trial showing superiority over Velcade. So I think this new trial should produce some growth.

Good Kyprolis result for AMGN - impacts LGND too:

Amgen (AMGN) today announced positive results from a planned overall survival (OS) interim analysis of the Phase 3 head-to-head ENDEAVOR trial. The study met the key secondary endpoint of OS, demonstrating that patients with relapsed or refractory multiple myeloma treated with KYPROLIS® (carfilzomib) and dexamethasone (Kd) lived 7.6 months longer than those treated with Velcade® (bortezomib) and dexamethasone (Vd) (median OS 47.6 months for Kd versus 40.0 for Vd, HR = 0.79, 95 percent CI, 0.65 – 0.96).

http://finance.yahoo.com/news/phase-3-head-head-trial-140000117.html

The 3% royalty LGND gets might well hit around $2/share in a year or two. And it's worth noting that any generic will very likely also need to license the captisol ingredient, so should be no patent cliff.

Peter

I commented on TRIL poster on twitter:

1/ A number of positives in new $TRIL poster:https://t.co/A1A3iqmII3

— Peter Suzman (@Biomaven) February 24, 2017

Those are obviously very good results indeed, but as you say, it is hard to know how much is their drug and how much the carbo/PD1 combo.

I could well believe a treatment like this could work.

When people get anxious, many start hyperventilating. That leads to low CO2 levels in the blood (hypocapnia) and produces cerebral vasoconstriction and less oxygen to the brain - that will typically further increase symptoms of anxiety and may well lead to a panic attack.

These patients could also likely be treated with a cheap beta blocker - that also typically stops the anxiety spiral.