News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

ERHClongtimer

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

What ERHC's neighbor in Block 11B is doing re: seismic, etc.:

Adamantine commits to well and seismic in Gatome basin

By Barry Morgan 12 July 2012 22:59 GMT

They are wasting no time getting the ball rolling in their block. - LT

Peter Thuo's thesis (ERHC's Central/East Africa technical consultant)

Stratigraphic, petrographic and diagenetic evaluation of Cretaceous/Paleogene potential reservoir sandstones of western Turkana, Kenya. Implications on the petroleum potential of northwestern Kenya.

This is quite an exhaustive study, encompassing 138 pages.

The different basins observed in the Northern and Central Kenya Rifts – Lotikipi/Gatome, Lokichar/North Kerio, Kerio and Baringo – all offer a good to very good reservoir potential.

Prior to early retirement from the NOCK in 2011, Dr. Thuo served as Exploration Team Leader, leading the Exploration and Production department. In addition to sitting on the National Fossil Fuels Advisory Committee, which negotiates terms of the Production Sharing Contracts, Dr. Thuo had extensive experience working as a senior geologist and geochemist in the NOCK.

As has been noted by a number of other posters, no doubt ERHC will hire a capable, experienced contractor to do the seismic for them.

In fact some seismic work has already been done for the Lotikipi Plain, and has enabled some geophysical modeling to be done: http://www.geosoft.com/resources/goto/AndrewL-online-seminar-2011-09-27

The technical analyst (Andrew Long) who prepared the presentation above made these further comments:

Further surveys would certainly add to the dream situation for Long, too. “I do not know NOCK’s intentions, but there are several geophysical methods that could be employed with the money available,” he says. “There have been tremendous developments in seismic survey methods over the last 30 years, we are sure better resolution is possible. A seismic resurvey, shot with lower frequency sources to penetrate the basalt and yield the low frequency structural information of underlying strata would help further constrain the gravity data available.”

In tandem, he would add a dedicated airborne survey, flown for the purpose of basin definition to assist the seismic interpretation. “Airborne gravity gradiometry may also yield better structural definition as exemplified in its use in other onshore East African basins that have proven very successful in defining graben structures, for example in Uganda,” he says. “A detailed airborne gravity survey would enable 3D modeling and hence the gravity contribution of the basalt sequences could be better defined and removed to yield residual gravity response.” Furthermore, he doesn’t entirely discount the magnetic method. “Although the susceptibility variation of the basalts are poorly understood, and believed to be difficult to map, the interpretation would only increase confidence.”

And finally, rounding out the dream would be a ground MT survey that may help define the basalt thicknesses. A strong bonus of course would be some exploratory wells, which would provide invaluable constraints to the seismic and potential fields modeling.

http://earthexplorer.com/2011-08/Exploring_the_East_African_Rift_System.asp

http://earthexplorer.com/2011-08/EarthExplorer-Issue1-2011.pdf (print version)

Tryoty, my comments were not about your post, but rather, augmenting your thoughts. My intent was to highlight the ridiculousness of the original poster's assertions.

It seems many are working hard to find any negative angle they can to undermine the accomplishments made by the company.

Sorry if it seemed directed towards you. - Longtimer

Tryoty, from an armchair quarterback's perspective, I agree with you that the placement via Rodman & Renshaw seemed like a deal with the Devil. The terms were certainly not very favorable to current shareholders, at face value. Wonder who was the brainchild of that deal?! But maybe it was necessary to secure some of the things that have happened recently; who knows.

In any case, that placement highlights the advantage of floating a "rights offer" to current stakeholders in the company. They are more likely to invest in a company they already have a vested interest in (and perhaps at better terms for the company--and consequently better for all shareholders, vis-à-vis the R & R deal), especially if there are to be some gratuitous terms (favorable warrants) involved (as was the case with the placement via R & R). How much better to reward current shareholders for upping their investment in the company than some opportunistic, greedy broker/dealer and their client(s).

I surely hope ERHC has this in mind with the proposed increase in authorized shares. I have to believe Offor would not stand for anything less, with his substantial stake in the company. And that makes me think it might be better to save some dry powder if those favorable terms materialize.

But it's anyone's guess at this point. - Longtimer

P.S.: It has been claimed by some that there would be an increase of 3 billion shares; but that is simply not true. The most that could be issued in new shares is 2.25 billion. And I am pretty confident that no where near that number will be issued anytime soon.

Whew! Someone is working overtime trying to throw as negative a slant as possible on a much-sought-after block in Kenya.

Why, from the comments, you would think shooting seismic in such areas had never been done before. Maybe ERHC should contact NASA about getting the plans for the Curiosity Mars rover in order to explore their block.

Someone's true colors are really showing! But it does provide entertainment. LOL - LT

Thanks, manuel, have now turned that feature (sounds) off!

Ah, so that's where that annoying clip kept coming from! It was about to drive me crazy, so I muted my laptop speaker.

I thought it was one of the IHub ads or IHub itself that was playing it.

Please don't do that again. }:^{

Excellent rebuttal, Tryoty. Hard to deny clear logic and facts.

Some suffer from severe myopia when considering where ERHC is now, where it came from, and the huge obstacles that were thrown in its path, which limited its options.

But things are really starting to roll now. Let's hope management is able to keep the momentum up. And with some cash, I think they will. - Longtimer

Yes, farrell90 posted about the pipeline, and maps are here:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78495388

Yep, and it looks like the South Sudan/Kenya pipeline will run right through ERHC's Block 11A:

arnim, vielen dank for posting the article about the joint venure between STP and Bluesky FLNG. The following in the list of objectives caught my eye:

- Manage and implement the technology solution for FLNG Bluesky gas extraction;

- Provide FLNG solution Bluesky Corporation to neighboring countries, including the joint development zone Nigeria - S. Tome and Principe Exclusive Economic Zone and Sao Tome and Principe;

- Research, drilling and installation of underwater pipelines, including the services of expert in the field of research and drilling;

Taiwan’s shipping firm TMT invests $2bn-4bn in LNG business

ICIS News : 22-May-12 07:20

By Pearl Bantillo

SINGAPORE (ICIS)--Taiwanese shipowner TMT is investing $2bn-4bn (€1.6bn-3.1bn) in building a complete liquefied natural gas (LNG) supply chain solution that is expected to come on stream in 2015, banking on the strength of global energy demand, the company’s top executive said on Tuesday.

The investment covers the re-designing of one of its huge vessels into a floating production storage and offloading (FPSO) unit, which will extract natural gas from the ocean and convert it into liquid, for shipping out to customers in Asia, TMT CEO Nobu Su said in an interview with ICIS.

“We try to offer solutions – from the ocean to the market,” said Su.

TMT’s FPSO is expected to have the capacity to process 1m-1.5m tonnes of natural gas, he said.

The company’s investment would also cover the building of four to six LNG vessels that would support the FPSO in transporting the liquefied gas to its end-market and convert it back into gas form via a floating storage and regasification unit (FSRU).

“Our solution is gas to gas. Normally you have somebody who either transporting LNG, sell LNG, or who can produce gas. But nobody is in the full chain like us,” said Subroto Banerji, who is in charge of the FLNG project under TMT.

TMT’s first FPSO will be deployed offshore in west Africa, in the natural resource-rich Gulf of Guinea, near the island country of Sao Tomei & Principe.

The company has signed a memorandum of understanding (MOU) with the island republic in March this year to collaborate and tap into the country’s natural energy resources.

Su, who is currently in Singapore, said TMT is in talks with Singapore’s Keppel Corp as a potential long-term buyer of LNG, and possibly a strategic investor in the project.

The company currently has no partner in its LNG project, Su said.

Once its FPSO unit becomes operational in 2015, the shipping firm is looking at serving the south and southeast Asian markets from its strategic location in west Africa, Su said.

“Since we are going to do it from west Africa, I think the biggest market would be, logically, India, it has a huge population and it is closer,” said Su, also citing Indonesia and Singapore as potential markets.

He estimates global LNG demand to grow at an annual rate 20%, but this is largely dependent on the supply situation. Current world demand for LNG is currently pegged at 280m tonnes/year, Su said.

TMT has a fleet of about 45 vessels, eight of which are called whales that can be converted into FPSO units.

“Basically, the [FPSO] design, we can copy to eight ships,” the TMT CEO said.

“If the demand is there, we can put eight units and get our capacity to 12m tonnes,” said Banerji.

Depending on the success of this venture, the company may consider listing its business unit Bluesky FLNG Corp, which is in charge of the LNG project, Su said.

The Taiwanese shipping firm generates an annual revenue of about $1bn, according to So.

Nobu to convert VLOO to FLNG

2012-03-27 09:01:50

Creative Taiwanese shipowner Nobu Su expects to put one of his eight very large ore oilers (VLOOs) into Hyundai Heavy Industries later this year for conversion into a floating liquefaction (FLNG) unit; LNG-FPSO.

Recently Nobu’s Today Makes Tomorrow (TMT) announced it had signed a memorandum of understanding (MOU) with the government of Sao Tome & Principe off Central Africa to develop a FLNG project using flare gas from oil-drilling operations.

Nobu plans to create its Octopus 8 FLNG unit in a reverse-engineering job on his 319,869-dwt VLOOs, which he has dubbed “Whales”, at a cost of over $1bn.

Engineers Black & Veatch and membrane containment-system designer GTT have been working on the design.

The TMT chief says the concept design for what would be a 1.5-million-tonne-per-annum (mtpa) unit is virtually complete, leaving the way open for field-specific work to begin.

The result would be a five-tank unit with a turret mooring system capable of achieving speeds of 17 knots, which Nobu claims will offer great stability. He estimates construction work will take around two years.

He is confident that Octopus 8 will be the first FLNG unit in operation.

“We already have the hull so we are doing the interior design, whereas others are building from scratch,” he said. He acknowledges that the yard would prefer to build a new one but says the VLOOs, which are currently trading ore and oil or are idling, were built at Hyundai so the yard knows them well. He says the first could be in place by the end of 2014 or early 2015.

He says the next step will be to start marketing the LNG, which he sees as going to Asia. He says the company already has buyers pencilled in and will sign MOUs with them “very soon”.

He has yet to disclose the details of his so-called “Squid” LNG shuttle tanker, which would be used to serve Octopus 8.

He reveals that these vessels will be of around 170,000-cbm to 180,000-cbm capacity and that the current breed of LNG carriers cannot load and discharge in mid-ocean but he claims Squid will be able to do this.

Taiwan Shipping Firm Eyes FLNG

Thursday, May 31, 2012

Summary

A Taiwan-based shipping firm is looking to liquefy stranded natural gas in the Gulf of Guinea off West Africa through floating LNG (FLNG) technology. A 1.5 million ton/yr FLNG unit, the Octopus 8, will be built, with production expected to start in early 2015, TMT Group Founder and Chief Executive Nobu Su told International Oil Daily Tuesday.

Japanese Nobu Su of TMT plans innovative LNG-FPSO

>> Global: Taiwanese shipowner Nobu Su, the CEO of family-owned Today Makes Tomorrow (TMT) shipping company, formerly know as Taiwan Maritime Transport, plans to offer a fleet of floating liquefaction (FLNG) units (LNG-FPSOs) to the market. The plan comprises the conversion of TMT’s fleet of eight Very Large Oil/Ore Bulk Carriers (VLOOs), using a new design that aims for ‘zero motion’ and ‘zero sloshing’.

The floater has been named “Octopus8” in reference to the number of conversion candidates.

He would leave the 319,869-dwt, 2010 and 2011-built vessels’ existing tanks in situ and fit an LNG Mark III-type containment system into them to give the world’s first triple-hull FLNG unit, Nobu says. He is currently working on the design and proposals for this together with Gaztransport & Technigaz (GTT), France’s membrane-type system designer. Further Nobu said he is prepared to undertake the first hull conversion on TMT’s account and plans to put the first vessel into the yard for the work next year.

The company is also working with Hyundai Heavy Industries (HHI) on the conversion project. HHI already built the VLOOs for TMT. A yard official claims that technically the work is possible.

However, the company will seek customers to design and build the units’ topsides, as Nobu said. The result would be a 340-metre by 60-metre unit that would have capacity to produce around 1.5 million tonnes per annum (mtpa) of LNG, store 175,000-cbm of product and process condensate.

By the end of 2012 so Nobu believes together TMT and GTT can finalise the tank containment design and if a customer comes forward to add the topside, a unit could be ready by 2014. Front-end engineering and design (FEED) work for the floater is already being undertaken by a Singapore-based company, as he added.

Just catching up on the preliminary 14A filing news and resulting discussion. As an ERHC shareholder of 13+ years, I'd like to share my thoughts:

1. It comes as no big surprise to me (nor should it to any shareholder) that ERHC is laying the groundwork for a possible means of new funding. They operate in a cash-intensive industry. Needing funding is academic.

2. A filing does not necessarily mean the proposal will be executed. It could be a contingency plan in lieu of other funding not materializing or taking longer than expected (e.g., EEZ farm-in money). Better to have a plan in place and actionable than to wait until things get dire.

3. I like the idea of a rights offering, if they must issue new shares to raise cash; it's the best possible option management can offer existing shareholders. (It's sad that some current investors would not be able to participate, but better some dilution of ownership than a cash-starved, non-functional company.) I believe SEO will fully subscribe to any rights offering made; that would guarantee a minimum 43% success rate to the offering.

4. Management has demonstrated that they are serious about enhancing shareholder value, adding the Chad and Kenya blocks recently. (I like the little nugget Homeport posted yesterday here.) And it sounds like they are not stopping at those two blocks. This takes money, but as the saying goes, nothing ventured nothing gained.

5. I don't think they would issue all 2.25 billion shares immediately. For round numbers, let's say they double the number of shares outstanding at 10 cents a share. That would raise about 75 million dollars and would provide a nice cushion of cash. And that would leave 1.5 billion shares issuable at a later time at possibly higher share prices.

6. I would not discount more good news around the corner that might make for an opportune time for issuing new shares.

7. I do not like the idea of creating a preferred class of stock.

8. We haven't been told any details about the company's plans yet, so the rational thing to do would be to wait and see what they have in mind.

Certainly appreciate the balanced comments on this topic in the following posts:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78422399

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78425949

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78425991

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78429336

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78429581

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78440771

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78440804

- Longtimer

Midtier, please post facts to substantiate your statement below...

But doing that would be in direct contradiction to Ntephe's policy of never disclosing anything to shareholders or potential investors unless you are forced to do so. - http://investorshub.advfn.com/boards/read_msg.aspx?message_id=78136788

Midtier, you say...

I will say flat out that I did not invest in this company for gas because the ROI on that is a small fraction of what you would get with an oil or condensate discovery.

Here's an 10/2011 update from Griffiths Energy showing all the prospects and leads in their Borogop & Doseo blocks:

As you can see, there are MANY more leads shown here than in the earlier image of the blocks we had. Makes you wonder what may be just north of these in ERHC's blocks.

Here is an image showing the seismic previously done by Esso:

Notice some of the seismic lines extend north into ERHC's BDS 2008 block.

Here's the complete presentation: http://griffithsenergy.com/i/pdf/ppt/GEI_Presentation.pdf - Longtimer

And then we have the likely West Polaris contract extension:

Petroleum Africa

West Polaris May Extend West Africa Stay

Date: Tuesday, June 5, 2012

Seadrill reported that it is in advanced discussions for a new five-year contract for the drillship West Polaris. This new agreement will start in direct continuation of the existing assignment which is scheduled to be completed in October.

The drillship is currently contracted to France’s Total for work offshore West Africa. Total used the West Polaris to spud a well in the Nigeria and Sao Tome and Principe Joint Development Zone’s Block 1 in March.

The potential contract revenue for the five-year period is valued at approximately $1.16 billion, with a final agreement expected in July.

http://www.petroleumafrica.com/en/newsarticle.php?NewsID=13680

You say

I would expect at least one additional well per block. I would like to stick it out and and see the results of the 2nd phase

Hmmm... if that's your point of view, Midtear, then could you tell me why you stay invested in ERHC. You must have some compelling reasons why you're still holding on, in view of your assessment of the JDZ. I'd like to hear them.

TOB (& Julius), that was exactly my point. ERHC looked to be in a really tough situation before the JDZ PSC signings and managed to come up with some really amazing contract terms and funds. The "going concern" qualifier on their financial statements is ancient history now.

As I concluded my post...

"Rather than fret and wring my hands, I am going to wait and see what develops within the next year. I like what ERHC has accomplished this year, and I'm optimistic that they will be able to capitalize once again on the opportunities they have created."

Thanks for making my intent clearer, TOB. - Longtimer

TOB, just an update on OPL 247: Both Total and Chevron have relinquished that block.

Please see http://www.ng.total.com/media/acreage_portfolio/acreage_portfolio_tucn_Jul2012.pdf

But Total still has a huge amount of acreage in the area north of the JDZ. - LT

Midtier, I think the dwindling cash balance is a concern to all of us, and beyond a doubt, ERHC management is keenly aware of it too. After all, it's their jobs that are on the line.

Yet, they keep pressing on with new acquisitions and commitments. So surely they have a plan or see the opportunity to get more funding in the near future.

The alternative is to continue to wait on the JDZ, which we all know, has not yet panned out to expectations and may be years away from producing income, if ever. So they are creating opportunities elsewhere. The alternative is to become paralyzed into inaction.

Don't know if you were around then, but before ERHC got the farm-in money from the JDZ blocks, every financial statement had a "going-concern" statement and things looked very dire. But ERHC was able to negotiate PSC terms (twice over, no less) that were far beyond expectations. I know, because I've been a shareholder for a long time. And yes, Peter was with the company then.

So, rather than fret and wring my hands, I am going to wait and see what develops within the next year. I like what ERHC has accomplished this year, and I'm optimistic that they will be able to capitalize once again on the opportunities they have created. - Longtimer

Maybe not, but that's a very cynical way of looking at things.

I think most board readers want neither extreme, only that the truth be expressed in a realistic way (whether positive or negative).

And it is one thing to express one's opinion about a matter; it's another to constantly barrage a board with the same negative comments over and over again on the same topic. It gets to the point that it is personal spam.

Hi, it would be great if a board member could be ostracized (kicked off a board) like they could in ancient Athens: http://en.wikipedia.org/wiki/Ostracism

For example, if say over 50% of active board members for the last 30 days voted off a member, then he/she would be automatically banned from the board. (Maybe you would want to have a minimum active member count, e.g. 10 members, before enabling this for a board.) It would be a way for boards to self-police themselves from disruptive posters and stealth bashers. After all, when a board becomes dominated by these types of posters, people start abandoning the board, and your page-view counts go down.

Please give us this capability, and set IHub apart from all the rest of the message boards!

Thanks,

Longtimer

TOB, I heartily agree that a "highly qualified exploration geologist and geochemist" that just recently retired from Kenya's NOC would know much more about the prospectivity of Block 11A in Kenya than a former accountant.

This graphic from the Africa Oil update (thanks redinvest) clearly shows that the Cretaceous Rift System dips well into ERHC's Block 11A, and the Tertiary Rift System is very close by, if not in, the block. And it's nice to see that this same Cretaceous Rift System has yielded 6 BBO in Sudan to-date.

So ERHC's acquisition of Block 11A is really good news. - LT

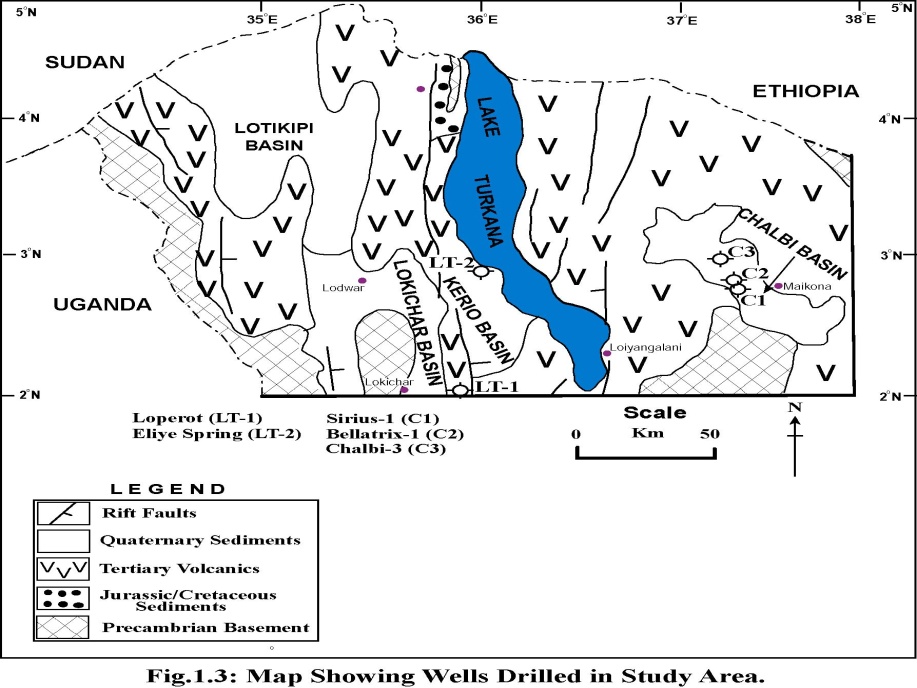

Blocks 11A & 11B are in Kenya's Tertiary Rift Basin, more specifically the Lokitipi Plain or Basin:

Here's some geological information for the area, as it relates to oil and gas exploration:

http://www.earthexplorer.com/2011-08/Exploring_the_East_African_Rift_System.asp

http://www.epgeology.com/page.php?p=kenya-rift-basin

Exploration as of December 2011

Great followup work, S1!

Looks like we have a definitive answer (if all goes well with ERHC's PSC signing).

I think we are both on the same page as far as ERHC's block in question being the onshore block of 11A, not the offshore L-11A, which is held by Anadarko.

Baz, did you check out the PDF in this post?:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=77215871

Slide 16 clearly shows Block 11A as CAMAC's on the map, and the text says "Block 11A still pending PSC". The map shows Block L-11A as Anadarko's, which is corroborated by this news release: http://www.total.com/en/about-total/news/news-940500.html&idActu=2820 (see last paragraph)

What is a little confusing is at the top of the slide the block is referred to as L11A, but the footnote attached to it says, "Kenya Block 11A has been provisionally awarded and is pending final execution of Production Sharing Contract between CAK and Kenyan Government." L11A is a typo.

The big question is, has CAMAC lost their award in the meantime (since the June 25th presentation), and has ERHC picked it up? Or has ERHC farmed in? I don't think we can conclusively say at this point, but I'd like to be proven wrong. - LT

Thanks, HP.

I try to keep tabs on the board, but don't always have time to post. Still a shareholder. - LT

Perhaps you're right, 2IRAs. Didn't look at CAMAC's financials. I agree, if ERHC got the whole block, it gives them more options. ERHC doesn't need a cash-poor partner.

As you say, hopefully the details will become clear soon. - LT

2IRAs, according to CAMAC's June 25 GHS 100 Energy Conference presentation, Block 11A was still pending a PSC agreement:

http://www.camacenergy.com/documents/CAMAC_ENERGY_GHS_100_2012_Final-1.pdf (See slide 16.)

So, it seems much more likely to me that ERHC farmed into the block rather than acquiring it.

CAMAC is listed on the NYSE Amex; they seem like a pretty solid company. See slide 4 for its organizational structure. Kind of reminds one of some of the ideas ERHC has floated in the past. - LT

CAMAC is a U.S.-based Nigerian firm, so no doubt that had a bearing on ERHC's apparent entry into Block 11A:

http://newnigerianpolitics.com/2012/02/25/us-based-nigerian-firm-wins-kenyan-oil-blocks/?calendar=2012-05

Could this be barter deal? 15% of Block 11A in exchange for a percentage of ERHC's Chad Block(s) for CAMAC? - LT

Kenya Block 11A

It appears CAMAC is the main licensee of this block. According to this operational update on 5/9/12, the company will be operator of the block with a 75% interest, with the Kenyan government holding 10%, and "the remaining 15% will be held by a local partner."

The company goes on to say, "The award is subject to negotiation and signing of a formal Production Sharing Contract for each block, which is expected to be completed during the second quarter of 2012."

You'll notice none of the news reports say that ERHC acquired Block 11A, but rather that it signed a PSC for the block. The timing of the news reports fit the time frame spoken of above, so perhaps the reality is that ERHC farmed in with a 15% interest on Block 11A. This would reduce the outlays required by ERHC for the block, as opposed to an outright acquisition. - Longtimer

TOB, this is a very significant find! Thank you for your research!

Griffiths Energy's Doseo/Borogop Concession directly abuts ERHC's BDS-2008 Block, as can be seen by comparing these two maps:

Noteworthy Details:

1. Both the Maku and Tega discoveries are only about 5 km S of ERHC's BDS-2008 Block.

2. The Kibea discovery looks to be only about 25 km SE from ERHC's BDS-2008 Block.

3. If Griffiths Energy lays the proposed pipeline, ERHC may be able to tie into it for any producing wells developed in the southern part of its BDS-2008 Block, reducing development costs.

(See this larger view of Griffiths' blocks to see just how close these discoveries are to ERHC's block.)

Here is what Griffiths says about these discoveries:

Doseo/Borogop Concessions

On January 19, 2011, the Company's wholly-owned subsidiary Griffiths Energy (Chad) Limited executed the Doseo/Borogop PSC with the State. The Doseo/Borogop PSC provides the Company with the exclusive right to explore and develop oil and gas reserves and resources in the Borogop and Doseo blocks in southern Chad, covering an area of approximately 22,206 square kilometres (the "Doseo/Borogop Contractual Zone"), subject to the terms and conditions of the Doseo/Borogop PSC. Doseo/Borogop is the largest area covered by a PSC.

Eleven wells were drilled in lands covered in the Doseo/Borogop PSC by previous operator, resulting in four discoveries at the Kibea, North Sako, Tega, and Maku fields. All four of these discoveries were tested by the previous operator but not placed on production. As a result, extensive well records exist for all wells drilled, all of which are required to be provided by the State to the Company. The well records indicate that these discoveries tested from 500 bbl/d to 2,200 bbl/d of medium and light sweet crude oil per well, and often had multi-zone potential.

None of the prior testing conducted by the previous operators involved artificial lift and little to no stimulation was used. The Company plans to conduct feasibility studies on all four of the discoveries to determine the commerciality of the discoveries.

(Link)

Doseo/Borogop Concession update

The Borogop and Doseo blocks cover approximately 22,414 km2, the largest PSC by area held by Griffiths Energy. The Company continues to conduct sub-surface and surface development and infrastructure feasibility studies to determine the optimum commercial development of the four discovery fields. This work is being completed in conjunction with the overall prospect evaluation and ranking work being undertaken by the Company's exploration group. The studies began in the fourth quarter of 2011 and are scheduled for completion in the second quarter of 2013.

Of particular interest in the Doseo block, the Kibea-1 discovery well has net oil pay in the C, D and E reservoirs. The E sands alone have 88.4m of net oil pay identified from logs, of which 75m were perforated by the previous Operator, resulting in oil test rates up to 2,200 barrels per day of 33-34° API oil. Based on these results, Griffiths Energy is planning to develop this field and believes that the recoverable volumes will be of sufficient quantity to anchor the major pipeline required to bring this field on production. This same pipeline will also provide the infrastructure necessary to develop discoveries made from the extensive exploration inventory of prospects in the Doseo/Borogop concession.

(Link)

Latest articles regarding Benoy-1

These are the latest articles I could find with comments on OPIC's Benoy-1 well. Doesn't seem as though anything has happened yet to diminish their initial findings.

The Taipei Times

Gas prices to rise NT$0.2 a liter, first raise in six weeks

Mon, Aug 22, 2011

In related news, CPC said on Friday it planned to invest more in its exploration well Benoy-1 in Chad, after crude and natural gas were discovered earlier this year.

The Benoy-1 well — which could yield 9,800 barrels of oil and 35,000 cubic meters of natural gas per day — is the largest overseas exploration the company has conducted at a single well over the past 40 years, CPC said.

“Over the next three years, CPC plans to invest NT$2 billion [US$68.98 million] and apply for subsidies from the government’s petroleum fund for more research and exploration work to better understand the field’s economic efficiency,” the company said in a statement.

www.taipeitimes.com/News/biz/archives/2011/08/22/2003511320

Taipei Economic and Cultural Representative Office in the United States

CPC aims to lift Taiwan energy self-sufficiency by 2015

Post Date: 2011/7/15

To bring Taiwan’s energy self-sufficiency up to 10 percent by 2015, state-run CPC Corp. will invest US$1 billion annually to acquire new oil fields and increase overseas energy exploration, the company said July 14.

Amid soaring oil prices and diminishing supplies worldwide, Taiwan must pursue greater energy independence, CPC said, citing Bureau of Energy statistics showing that imported energy accounted for 99.25 percent of the nation’s total consumption in 2009.

The company’s exploration budget for this year is NT$5.3 billion (US$184 million). In February in the Republic of Chad it made its largest find of oil reserves in 40 years, the Benoy-1 well, which is expected to generate 9,800 barrels of crude oil and 35,000 cubic meters of natural gas per day.

CPC said the Chad deposit could eventually produce more than 100 million barrels of oil, while other acquisition plans in Africa and Australia could add reserves equivalent to 200 million barrels.

Since it began oil exploration programs outside the country in the 1970s, CPC has developed oil fields in Ecuador, Indonesia and the U.S., with total daily output of 12,000 barrels of crude oil and 1.04 million cubic meters of natural gas.

The company added that it will use overseas private investment corporations to extend its exploration, extraction and production activities to more countries, including Australia, Libya and the Republic of Venezuela.

http://www.taiwanembassy.org/US/form.asp?ctUnit=113&spec=contactus&mp=12

CIOME Chad 2011 Newsletter

Prolific Oil & Gas Discovery by CPC in Chad

June 2011

Taiwan’s state-run CPC Corporation has discovery a new oil and gas reserves in Chad. The CPC spokesman said these new reserves could potentially help it generate revenues of up to $1.6 billion over two decades.

The newly discovered reserves from the Benoy-1 well on Block I, potentially have a daily production of 9,800 bpd of high quality light crude oil and 1.2 Mmcf/d of natural gas. CPC said that this was one of its most successful discoveries in 40 years of international exploration.

http://www.cubicglobe.com/ciome2011/CIOME2011NEWSLETTER.pdf

Africa Energy Intelligence

Fanfare for CPC's First Find

Feb 23, 2011 – Taiwan's national oil company has trumpeted its first discovery in Chad but its excitement may be premature. The chairman of Taiwan's China Petroleum Company (CPC), Chu Shao-Hua, which operates three blocks in Chad, announced that a well on the BCO II [sic] block had struck oil. The block in question lies in the Benoy region around 50 km northwest of the producer fields in the Doba basin. Paul Chen, vice president in charge of exploration for the international branch of CPC Overseas Petroleum & Investment Corp (OPIC), talked of potential output of 9800 bpd and 35000 cu.m./d of gas. However, sources at Chad's oil ministry say the announcement is highly premature. Only one well, Benoy 1, has been drilled on the block. In 2010, another well located on BCOIII proved disappointing. OPIC operates the three licenses with a 70% stake alongside the government's 30%. Production from OPIC's blocks as well as that from the China National Petroleum Corp (CNPC) could well take over eventually from the Doba basin. The operators on the latter, Exxon, Petronas and Chevron, haven't succeeded in curbing the decline of the fields which now produce only 110000 bpd after just seven years. ...

Nice find, kingpin!

Here's a flyer produced by ERHC from that link that gives some nice details about their Chad interests:

http://www.ezdataroom.com/pdf.php?id=253

Looks like Chari Ouest III will be their first target. Notice the mention of OPIC’s Benoy-1 discovery. - Longtimer