News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Closed solid red on higher than avg volume (about a 50% increase in the daily avg volume).

Any gain it made- it sold off into strength each time on volume.

It's showing weakness so far IMO despite the big move to the NASDAQ.

W/o some clarity on how they're going to finance and sustain themselves, let alone fund a serious phase 2 trial which is the key to their entire plan they presented- I think they're open to the pro shorts of the Nasdaq.

Until they clarify if it's all more dilution going forward- or some other funding source, then they'll be in a position of weakness to me. If they have to do a large dilution share sale cash raise then the price will most likely come under at least temporary down pressure- which may be putting buyer's on the sidelines until clarified IMO.

They are living off of Lincoln right now (in itself dilutive) and they don't have anywhere near the cash at this point to fund a high quality, much larger FDA level phase II trial. Lincoln pretty much pays their present burn rate- but doesn't in any way fund a serious trial that I can see. The numbers don't add up.

So some key pieces of the puzzle are still missing that they need to clarify. The share offer got pulled either because of weak demand and low pricing power IMO or they have some other plan they're trying to put in place (the shelf filing is still open and good as far as I can tell).

If they have something- it'd already be announced. Public companies can't sand bag or hold back major material events- if they know and it's a done deal then it gets made public ASAP and is filed with the SEC on an 8-K or similar of needed.

Which tells me at this point- they don't have it yet, whatever it is they may be trying for. Else, it'll be back to a dilution offering, a large one IMO. Maybe they decided to try and sell the shares once on the Nasdaq hoping for a little more pricing power? They spent a bundle on up-front fees and those underwriters and legal and all to pitch that prospectus- so to just "can" it, they must have a pretty good reason? Question is- what's the plan and where's the cash gonna come from?

My 2 cents

Re: 10K

Well, the dates of the last 3 yr's filings are below- so I'd expect somewhere approx. around the same time frames. Sometimes a company is a little early with a filing, sometimes a little later. Remember, the 10-K is fully audited unlike a 10-Q so it's more complicated and expensive to do. Tomas as CEO does a lot of the 10-Q's probably to a large degree himself with some accounting firm or contract accountant assistance or whatever.

But on a 10-K filing, it's like rolling up all the 10-Q's of the full yr, getting it all put together, then it goes to the independent auditor's place (forget BHRT's auditor firm name, it's in their SEC filing- but basically a big, licensed, fiduciary duty type CPA firm that does these public traded company audits) and then they do an audit of the 10-K as Sr Mgt has prepared it (that's my understanding).

I'd guess the auditor's may make some comments or whatever and it goes back to Sr. Mgt who either agree or disagree or whatever. They then get the final document all agreed upon (probably the company SEC or stock legal counsel maybe even takes a review at it too- who knows?) - and then last step is Mr Tomas as CEO signs off on it and then the auditor's also put their name and signature to it and say something to the effect (you'll see it in the 10-K's), "We the audit firm of ABC have reviewed this filing and believe to the best of our knowledge that it's a true and accurate representation of the financial condition of company XYZ blah, blah and we also disclose blah, blah if we agree or don't agree with something". Something to that effect.

Also, the audit firm is the one then (I think) who will either insist or not to the "going concern" warning to be present or not in the filing- cause if you read all the past "going concern" warnings they will refer or state something like, "As of date XYX our independent audit firm noted the following concerns of our ability to continue as a going concern as noted in exhibit or notes section ABC, see below" or something like that. So the auditor is the one typically involved in making that "going concern" warning determination or any other financial issue "warnings" or whatever (I'd guess it's based on ratios and stuff in the "generally accepted accounting standards" these firms abide by) and then Sr Mgt I suppose agrees to include it or the audit firm probably won't sign off. Whether there will still be a "going concern" warning in this next 10-K we'll see I guess? It was still in the most recent, last filed 10-Q last qtr.

Here's the dates for prior 10-K filings:

10-K yr ended 2013:

3/25/2014

10-K yr ended 2012:

3/29/2013

10-K yr ended 2011:

4/12/2012

http://www.bioheartinc.com/Investors/SECFilings

So I'd say it looks to be about the end of March pretty much solid for about 3 yrs now. So I don't see why that would change this year? About 25 days, maybe one month away then is my guesstimate for formal 10-K release and upload to the SEC EDGAR database.

2 MILLION plus for sale on the Ask, wow !!

The selling is just not abating? Who is selling this much stock and/or for who I wonder?

Amazing IMO. The sell side pressure has been like 10 to 1 or more to buy side on many of the days of the past several weeks.

0.009 / 0.0094 (100000 x 2035000)

BMAK is sitting one level off that Ask, 10K share block at .0094 parked like always recently. They did open the spread a bit today- like they want a little "upside" on this big blog these MM's are trying to unload it looks like. These OTC MM's are just brutal IMO. Amazing.

http://www.otcmarkets.com/stock/BHRT/quote

Oh gosh, solid RED selling?

OCAT listing on the Nasdaq apparently hasn't solved all their problems I guess?

They'll still more than likely need to do a very large share dilution too, as they don't have anywhere near the funds to conduct the promised large, phase II trial. As of now they're simply living off of and keeping the lights on and door open using Lincoln for survival- but that's not serious FDA trial kind of money IMO. Also, Lincoln in and of itself is dilutive, on-going.

If this is the relatively dilution-free version on the Nasdaq, I wonder what happens if they do a large dilution deal? They're gonna need a boat load of money- and it's gonna have to come from somewhere?

Looking pretty weak in here for the big "debut" on the Nasdaq? Not sure what's creating the selling- but the buyers seem to be in short supply so far?

BMAK parked on the Ask with a 10K share block at .0094

Looks like BMAK is setting the "cap" for the day again?

Looks like BHRT ends this week as a SUB ONE CENT stock IMO. Just no real buying pressure or interest in here even at these prices it seems to me?

Nothing has been able to really bring it off bottom or the continual dropping Bid/Ask and lower lows and lower highs. Another tough week with no buying interest really at all from the decline on high volumes.

http://www.otcmarkets.com/stock/BHRT/quote

AM Bid/Ask is tilted heavy to the sell-side looks like again.

0.0085 / 0.009 (64783 x 465000)

Looking real, real weak in here at this point IMO.

Uh, all except that MSFT was PROFITABLE FROM ESSENTIALLY DAY ONE and then went on to one of the greatest company rapid growth rates, rapid rise in pure profitability in all of world biz history. MSFT became a cash printing, rapid growth machine producing a train load of millionaires (including an original early employee like a secretary) and some of the world's wealthiest billionaires the day they went public- still in the record books of world biz history.

ACTC never even had an actual "IPO" because of lack of funds or growth or a product to sell- they used the "back door" poor man's method of trading public- via reverse merging into the TWO MOONS KACHINA DOLL COMPANY of Utah straight on to the OTC market place.

OCAT is nothing of the sorts of an "early Microsoft" - not even a distant remote comparison to the history of MSFT as a business?

http://www.nature.com/news/stem-cell-research-never-say-die-1.9759

The ACTC/OCAT tale is long and sorted and to this day, some 15 plus yrs later has never produced so much as one CENT of ROI to its common shareholders nor has ever produced even one successful salable and profitable product to market and has actually lost about 98% of the value of the common stock shares, had a SEC violation or two along the way including SEC prosecutions including $millions in fines still being paid by the shareholders in final payments to this day, etc.

That is NOT a "Microsoft story" by any stretch or comparison.

Yeah typo, 5 Cents. You're correct. Great improvement. Huge first day on the NASDAQ.

But, it actually didn't make the 5 cents in the green. It traded down in after hours- a wonderful feature once a stock makes it on the NASDAQ.

It traded DOWN, RED .0101 which would be approx 1 CENT or 101/10,000ths of a dollar or down .14%. Amazingly strong first day showing, especially for the buyers at $8.39 where it spent all of probably less than a minute.

To sell-off over a $1 from it's AM peak (on a $7 stock, or almost a 15% decline off its very brief momentary peak shows weakness IMO. It sold off into any strength and very rapidly) That indicates to me it couldn't even support a good mo-mo trade at this point.

They're gonna more than likely need to dilute at some point very soon IMO to fund their proposed trials and all. If it trades this weak now, just wait till a large chunk of dilution shares are piled on and need to be sucked up in the market place. They're also diluting now for all intents and purposes as they're using and relying on Lincoln to keep the lights on and doors open.

I see continued weakness ahead IMO after today's showing.

http://www.nasdaq.com/symbol/ocat/after-hours

Quote, "OCAT finished green...even after someone tired to paint the tape in the last 30 mins and now painted after hours with 100 share ahahaha so IMO means squat With... IMO it is just that.... never really means much....

"

LOL, 5/100ths of a CENT "green". .05 "green".

Well, ole OCAT just stumbled and tripped and fell across that ole finish line "green" then I guess?

Technically, 5/100ths of a CENT to the plus side is "green", yes.

Heck of an impressive first big day on the NASDAQ. A stunning performance. 5/100ths of a CENT "green".

But it really DID NOT "finish green" on the day as claimed- as stocks on the NASDAQ can trade after-hours. And OCAT traded DOWN, RED by end of day.

http://www.nasdaq.com/symbol/ocat/after-hours

RED.

Follow

Ocata Therapeutics, Inc. (OCAT) After Hours Trading

OCAT

$7.29 last trade, 18:37 Eastern Time

DOWN 0.0101

DOWN 0.14%

Looks like the NASDAQ pro short desks and hedge fund boys already sniffed out a ripe opportunity and weak stock here IMO.

They're plowing this thing like with a bulldozer right now. Never believed for a second the myth that "shorting" ends on the NASDAQ and is only part of the OTC, etc.

If anything, IMO, the ability to get short inventory and the visibility to professional short hedge funds and similar high speed and other trading desks- probably just lit up like a Christmas tree today with a little ole OTC transfer called OCAT stepping onto the NASDAQ.

That AM spike to $8.39 lasted what- less than a minute or two, tops?

This will be lucky to even close green today the way it's stacking up now, IMO.

Quote: "Quote:

So where did $OCAT get the extra Market equity for NASDAQ Global Market listing??? IMO likely the link with the extra monies and the planned Pivotal Phase2 trials."

What? They don't need shareholder equity for the tier they chose- and that's IMO why they chose that tier.

The only requirement is $75 million "market value of listed securities" (aka their market cap) and at least $20 million market value of public held shares (In other words can't all be held by insiders, private investors etc) and a min $4 price per share and a few other tid-bits about number of MM's etc.

Shareholder equity has nothing to do with the tier they just listed on.

https://listingcenter.nasdaq.com/assets/initialguide.pdf

OCAT would most likely presently have little to no positive shareholder equity at this point from the time period of when the 10 million share prospectus/disclosures were filed (then pulled) - as they only had about $720K positive then, but would be consuming a lot of cash since then, only off-set via using Lincoln dilutive financing at this point.

NASDAQ shorts and pro MM market makers already stepping in all over it. Not surprised in the least IMO.

When a stock runs a big spike on hype like it just did- the MM's short sell on the way up to fill their orders (yes on the NASDAQ). They will then "walk it back down" to cover their own short positions for a profit. Every single time I've ever seen it. That's what MM's do, especially on fast spike moves- as they don't keep inventory on a stock to fill that much fast moving orders- so they sell it short into the spike. Cover later for a profit.

The idea the shorting and nasty MM's don't or won't exist on the NASDAQ IMO is pure myth. Some of the biggest hedge funds, the most professional shorts, the most brutal shorting and what not lives and thrives on the NASDAQ according to all I know and have read.

It's gonna be a wild ride IMO. Just "up-listing" in no way guarantees some massive price increase or inherent increase in company value IMO. I just don't see the data or historical trends to back that up?

Most "big house" short firms live on the NASDAQ, not the NYSE. Hedge fund and HFT (high frequency trading networks) were born and live on the NASDAQ.

Being encouraged not to use or set "stops" is IMO not a good idea. One can "stop out" and always buy back later- it's better than taking losses IMO.

Quote LOL: "BHRT was around this price before it went to .08 last year. I believe we only knew about 500K in revenues at that time. All the negative information being posted everyday is the same today as it was when this went up 800% last year. The only difference I can see are positives. Increased revenues, further along clinical advancements and potential partnerships. What has changed from a negative standpoint since this time last year?"

Day's low of .0082 again, right out of the gate, WOW. But I digress.

To the quote/question above-

1) And how long did it, BHRT trade and last at .08 after what was IMO a hype based run up? I believe a chart will show it lasted less than ONE DAY at the .08 price, probably actually minutes or less if memory serves me correctly. Then, within the next day or two days or so if memory serves me- it sunk by more than 50% on massive selling to about the .035 area. It then had a few more attempts to hype it/run it IMO with some "other" PR if I remember and then a "paid promotion" was used not too long thereafter ($5K at least for one month of penny promotion paid to a firm called and site called smallcapvoice) and the stock "popped" back up a bit to maybe the .06 max range one last time and then began a now nearly 12 month, steady (maybe a minor pop or two along the way perhaps) steady downtrend decline from a brief moment at .08 to now SUB ONE CENT. Whoever got caught in the .08 area or .06 area IMO more than likely got creamed for major losses. That's not an "investment" IMO but more like a split second on a Vegas slot machine or craps table to me. Again, the time at .08 was probably, literally moments - I'll pull up a historic chart and can probably measure pretty close to how many "minutes" it was actually at .08, but I believe it wasn't long at all.

2) What's changed from 1 yr or so ago to the "negative"? Well, one tiny little tid-bit might be a close to doubling of the O/S shares (especially the fully diluted share count) via massive, massive dilution via issuing over 300 million shares in approx. a 1 yr, maybe 1.5 yr max period. From SEC filings:

Around Aug 2013 the O/S share count was about 236 MILLION shares

By about March of 2014 the O/S share count hits about 420 MILLION shares

By about March of this yr, 2015 the O/S share count will more than likely pass around 700 MILLION shares, somewhere in that range (by release of next 10-K filing) as a guesstimate based on on-going, continual dilution IMO.

At some point, IMO, massive stock dilution has to have some effect on the common shares. Also, during that time period, the BOD also increased the A/S (available shares) to 2 BILLION. Which means IMO they know/knew they're gonna continue massive, massive dilution as they already had 950 million A/S available when they did that increase (apparently 950 MILLION share available was not enough to satisfy the future share dilution appetite and needs?)- apparently the BOD felt the 950 MILLION number just didn't leave um enough "cushion" zone for how rapidly the dilution would be occurring, so they upped the A/S by just a massive number of over 1 BILLION shares more.

That massive share increase was done on April 17, 2014 (NO PR about it of course, but a PR gets issued if some "award" or whatever is given to someone- but nothing about a massive increase in A/S shares, so unless one saw the SEC filing they didn't even know it occurred) And the increase was done via the "We don't need, nor do we want your vote as common shareholders" statement in a proxy "notice" (not a vote as none is ever needed) sent out that was for "information only" - saying in effect that the insiders who control all shareholder voting power (mainly via Northstar LLC's 25:1 preferred shares voting rights on 20 million shares = 500 million votes alone) that they, the "insider key shareholders had approved it" so don't bother voting, nor is your vote needed blah, blah etc. That's how the 950 million to 2 BILLION share authorization was "handled".

http://yahoo.brand.edgar-online.com/displayfilinginfo.aspx?FilingID=9926197-843-289809&type=sect&TabIndex=2&companyid=734841&ppu=%252fdefault.aspx%253fcik%253d1388319

3) And maybe just a tad possibility that the on-going, never ending use of dilutive, "convertible debt" financing deals, aka "floorless" or "toxic" by the SEC's own definition could IMO be having just a "tad" of negative down pressure effects on the common shares? Just maybe possibly? Asher used many times, Magna, Fourth Man, Daniel James used several times, KBM Worldwide to name just some of the "convertible note" financing lending firms used in the approx past 1 yr- even as recent as Oct of 2014, despite the "revenues" as they don't produce enough bottom line cash to even come close to match the spending/expenses of the business.

http://www.sec.gov/answers/convertibles.htm

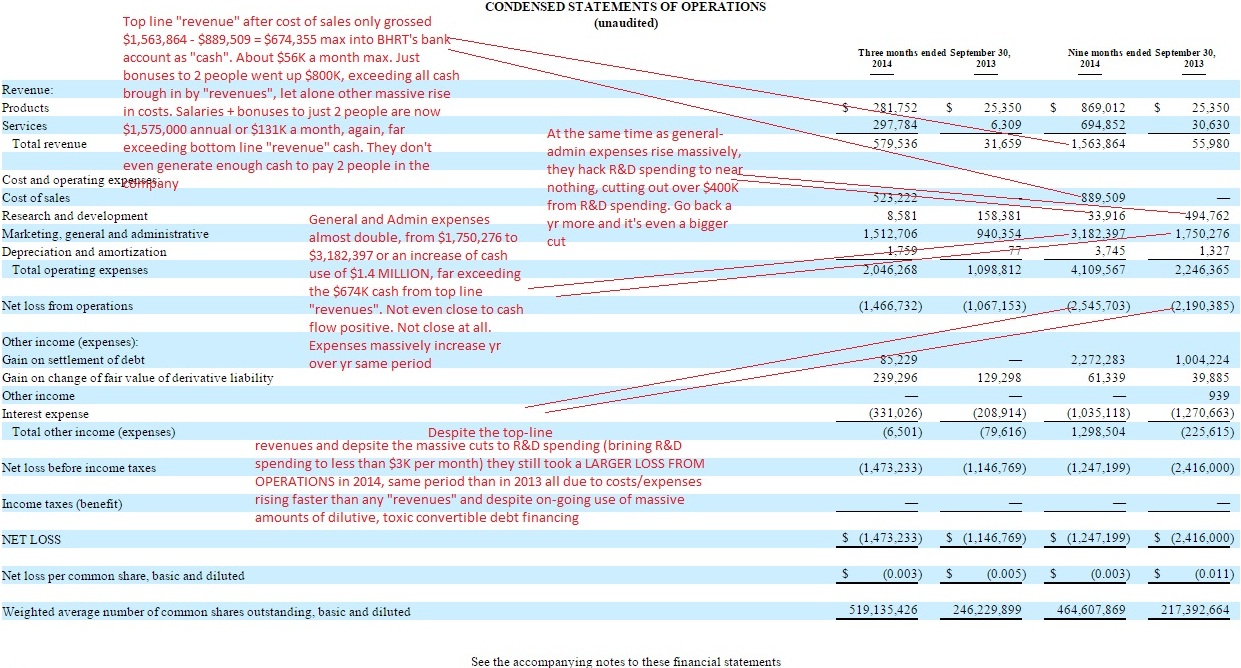

4) The continual talk of "revenues" IMO 100% fails to discuss the massive rise in the expenses/cost side that the business shows occurring on their SEC filed financial entries (also the corresponding massive CUTS to R&D spending/expenses occurring at the same time) that through Sept 30, 2014 10-Q filing have resulted in the company actually having a larger loss from operations than in 2013 (despite top-line "revenues") and left the company with only $46K total cash on-hand as of the end of the last qtr at which point they immediately inked several "convertible debt" aka toxic notes in Oct 2014 for amounts as low as $25K and $38K for survival cash (despite the claims and PR and all about "revenue) - highly dilutive notes at horrible financing terms such as share discounts of 45% and 47% (see last filed 10-Q PAGE 26 Daniel James and KBM note financing deals). Read the statement of operations on PAGE 5 to see larger losses from operations yr over yr despite top line "revenues" as expenses have grown faster than any revenue banked after cost of sales is subtracted out).

5) Same 10-Q, latest filed, still contained a "going concern" and "liquidity problems" warning from Sr Mgt despite "revenues" so not sure what has "changed" so much IMO? Their financial situation is pretty much as desperate and in poor condition yr over yr that I can see? They're living off of dilution, their expenses have massively risen despite no trials or any real R&D spending occurring (Again, page 5 last 10-Q), etc so what have "gotten better" supposedly or whatever? I personally don't see that reality reflected in any SEC filed statements? Where?

PAGE 12, latest filed 10-Q, their Sr Mgt's most recent discussion of their financial situation and how poor it is:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during nine months ended September 30, 2014, the Company incurred an operating loss of $1,247,199 and used $747,184 in cash for operating activities. As of September 30, 2014, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $10.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time.

The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern."

So those are just a few possibilities IMO, just a few maybes as to why the common shares might be in a now 10 plus month sustained downtrend? Don't know for sure- but that seems like some pretty solid data IMO, all found in the company's own SEC filings that might give a hint or clue as to why they may be where they're at now?

Oh, and the MIRROR big "phase 3 trial, FULLY FUNDED BY Bioheart" that PR and the "FULLY FUNDED" part in the PR from over 1.5 yrs ago now- well, it sorta-kinda like never actually happened either. On Jan 25th, 2015 a PR (with no real explanation given) said it, MIRROR, the big phase 3 trial is over, when for all intents and purposes IMO it never actually even took place or occurred, let alone was ever "funded" by Bioheart. Just look up the PR and SEC filing history of MIRROR- it's "interesting" to say the least IMHO. Also, no other major, key trials of there's have ever moved forwad or advanced either- while all the dilution has occurred and the convertible debt deals have been on-going, etc. Their "key trials" are now about FIVE YEARS stagnant.

Here's from the last 10-Q filing, most recent qtr, PAGE 29:

"We received approval from the FDA in July of 2009 to conduct a Phase I safety study on 15 patients of a combined therapy (Myocell with SDF-1), which we believe was the first approval of a study combining gene and cell therapies. We initially commenced work on this study, called the REGEN Trial, during the first quarter of 2010. We suspended activity on the trial in 2010 while seeking additional funding necessary to conduct the trial.

We are seeking to secure sufficient funds to reinitiate enrollment in the MARVEL and REGEN trials. If we successfully secure such funds, we intend to re-engage a contract research organization, or CRO, investigators and certain suppliers to advance such trials. We have initiated and enrolled our first patient in the MIRROR trial in 2013. The trial is very similar to the MARVEL trial but focusses on sites outside the US. We will continue enrollment in the MIRROR trial once we have secured sufficient funds."

MARVEL essentially went parked around 2009 I believe, even earlier than REGEN. So that' about 5 or 6 yrs now those trials have gone nowhere "awaiting funding" but in that period massive base pay as well as "bonuses" ($800K in "cash" bonuses just in 2014 alone) have been awarded to just two people in the company (which has about 3 to 5 full time employees total during the yrs those trials have gone nowhere - see SEC filings for any period from 2010 to today pretty much).

So maybe that's could-might be an issue too- that they really aren't apparently conducting "heart" FDA type trials anymore per their own SEC filings, then MIRROR never actually happened as hyped in a big PR campaign, etc Again, just my 2 cent thoughts on a few "possibilities" as to why maybe the common shares have come under some selling pressure?

Really not sure why- but those seem like some pretty solid possible-maybes IMO, all from the company's own SEC filings and PR and stuff they put out.

Just cause a stock "popped" for a brief moment in one year- I really don't see how that is some supposed barometer or "predictor" of what a stock will do in the next yr or especially in some near exact time frame in some future year? Everything I've read and know about stocks/markets tells me that the past does not ever "predict" the future when it comes to stocks (read the company's "Safe Harbor" statements they include in pretty much every PR or any statement or "plan" they ever talk about, how nothing in the future may ever even actually happen or occur as described and the future can't be predicted, etc)- but stock that had brief "pops" in one year don't always do it again at the very same time the next yr IMO, especially ones that are diluting constantly and using convertible debt deals nearly continuous, on-going, etc. I just don't see any connection or way to make those connections IMO?

My .009 cents worth.

Chewing through those Bid side shares. It might break the .008's as was mentioned in another post earlier. Bid/Ask both dropping today.

BMAK has now slid down the Ask into 1st position with a 10K share block at .0086, the "cap" it looks like IMO.

Looking real weak again here today IMO. Just no buying interest at all- at least not willing to pay even the Ask at these sub ONE CENT prices as they continually drop it.

Market cap just hit the round number of $5 MILLION on my screen. Holy cow.

http://www.otcmarkets.com/stock/BHRT/quote

Only about $1,200 bucks left now in the .008's. Next stop is the .007's if some more bidding doesn't materialize.

Pretty tough sledding in here fa sure.

0.0082 / 0.0086 (110000 x 10000)

"If the bulls fortress breaks .008 it could hit all time lows. IMO"

Well, as of right this moment- there's a grand total of about $4,000 bucks left in the .008's (that's dynamic and can change of course, it was only $1,200 bucks worth earlier) - but if they chew through that it's a quick drop into the .007's for sure IMO.

That big block on the Bid side just showed up- so someone maybe wants to buy a bit today but they don't wanna pay the Ask, even at well below ONE CENT.

0.0081 / 0.0089 (465000 x 87000)

(that Bid just dropped when the big block showed up; again, they want in maybe it looks like, but don't wanna pay full price today IMO)

BMAK is back, parked on the Ask w/ a 10K share block at .009. Looks to me like they're setting the "cap" for the day again.

BMAK is also sitting on the Bid side w/ a 10K share block at .0079

Interesting.

http://www.otcmarkets.com/stock/BHRT/quote

Quote: "On NASDAQ Global Market for mid-caps to large Caps. "

There is nothing in the tier of the NASDAQ "Global Market" (not Global Select) that defines a company as being a "mid-cap or large cap) company??

It's not part of the listing criteria? The only "market cap" requirement is to have $75 million in market cap- which is not by any generally accepted market definition a "mid-cap" company, it's a small cap company.

OCAT with its present market cap is a small cap company, not even close to industry-wide (for example what mutual funds use) accepted definitions of a mid-cap and certainly not remotely close to being a large cap company.

In general, and one can look this up on any major mutual fund site (Fidelity, Vanguard, or the SEC's definition, etc) - in general the dividing lines for small, mid and large cap companies are about as follows:

Less than $2 billion in market cap = SMALL CAP

Between about $2 billion to less than $10 billion in market cap = mid-cap

And in general it takes about $10 billion or more in market cap to be defined as a large cap company.

Those are industry wide, Wall Street and mutual fund easily found definitions of the approx market cap ranges. OCAT is a small cap company by all definitions.

Just a few examples:

Here is the Russel Mid-cap index fund. Not the "median market cap" for a company in that index (a well, well industry-wide recognized index) the median/avg market cap is $6.2 BILLION dollars.

https://www.russell.com/indexes/americas/indexes/fact-sheet.page?ic=US5015

Here is the S&P mid-cap fund 400 - again a major industry recognized market fund/barometer. The blend of stocks in it have market caps from the very lowest being $756 MILLION to an avg of $4.1 BILLION to a max market cap of $15 BILLION in the "mid-cap" catagory.

http://us.spindices.com/indices/equity/sp-400

By contrast, here is the S&P "small cap 600" index and its makeup and its "members" company market caps-

Lowest market cap: $92.8 MILLION

Avg market cap: $1.2 BILLION

Highest market cap: $4.5 BILLION

http://us.spindices.com/indices/equity/sp-600

Those are the market-cap ranges be considered a "small cap" by S&P and included in their 600 company "cross-sectional" index (which is exactly where OCAT's market cap is at).

OCAT is very much a "small cap" company in terms of all industry norm, generally accepted definitions I'm familiar with. At around just over $200 million in market cap- OCAT is nowhere close IMO to even being a "mid-cap" company (they're in fact in the "classic" middle area for a small cap, not a micro-cap company definition), let alone a distant close to being defined as a "large cap" company, not even distant close. They're a long ways IMO from even meeting a "mid-cap" definition at only $235 million in market cap.

Quote: "Stock manipulation of Bioheart is a serious crime. Those involved hopefully will be caught and charged. If not, they will have bad karma and nobody can escape that. IMO"

Manipulation? Karma? What??? Is there specific details on all this "stuff" (apparently serious crime stuff) - any details where one can read more about this? Wow. It sounds amazing- I mean how and where is this happening?

Or, is perhaps just MASSIVE, MASSIVE near endless amounts of common stock share dilution (by the company itself by the way) ever to blame for a declining share price? (ever?) (over 300 million shares of common stock dilution in just the approx past 1 yr see SEC filings 10-K/10-Q, and a fairly recent, self approved by insiders BOD vote to increase the A/S to 2 BILLION shares and then approx. 50 MILLION shares of dilution just in the period from Nov 2nd 2014 to about early Feb 2015 via using the share counts from the last 10-Q page 1 to the shares O/S given in the recently filed SEC "proxy vote" result document- an 8-K filing I believe it was. Does any of that EVER have any effect on the common shares I wonder? Possible maybe?)

Or, how bout the near endless and continual use of "convertible debt financing" (aka toxic, floorless or "ratchet" financing- SEC terms and words, not mine)-- just continual on-going use of dilutive, floorless convertible debt deals with firms such as Magna, Asher, Daniel James, Fourth Man and KBM Worldwide to name a few- ANY possibility "maybe" that (versus you know, the "manipulator and karma" theory thingy stuff) just any possibility that maybe that kind of toxic (again, SEC calls it that, not me) that kind of financing, on-going has any possible down pressure effect on the common share price of a OTC market, thinly traded, nano-cap (barely $5 million market cap) debt laden, "going concern" in every SEC filing going back yrs - type company? Any possible connection there at all, maybe perhaps kinda?

Here's what the SEC warns about companies who use "convertible debt" financing- the SEC IMO seems pretty gosh darn clear that it's highly, highly likely to have a "negative" as in "downward" effect on a company's common shares- that's how I read this article the SEC took the time to write specifically about use of "floorless" or what they call "toxic" or "death spiral" convertible debt financing:

http://www.sec.gov/answers/convertibles.htm

Just a small quote from the SEC article for example:

"By contrast, in less conventional convertible security financings, the conversion ratio may be based on fluctuating market prices to determine the number of shares of common stock to be issued on conversion. A market price based conversion formula protects the holders of the convertibles against price declines, while subjecting both the company and the holders of its common stock to certain risks. Because a market price based conversion formula can lead to dramatic stock price reductions and corresponding negative effects on both the company and its shareholders, convertible security financings with market price based conversion ratios have colloquially been called "floorless", "toxic," "death spiral," and "ratchet" convertibles.

Both investors and companies should understand that market price based convertible security deals can affect the company and possibly lower the value of its securities. Here's how these deals tend to work and the risks they pose:"

I mean just from reading what the SEC says- it's "possible" (besides the manipulator crime and "karma" thingy theory- just possible that's there's other reasons for this company's stock price to be under down pressure IMO)- I tend to think the SEC sorta, kinda knows their business and what they're talking about IMO, but that's just me.

From the last filed BHRT 10-Q, just as a few examples of recent "convertible debt" deals (aka floorless conversion formulas built right into them- it's right in the language of the "note") - just a few recent examples of BHRT using these deals- as they have essentially every qtr going back yrs and yrs.

Latest SEC filed BHRT 10-Q, PAGE 26:

"NOTE 13 — SUBSEQUENT EVENTS

Subsequent financing

KBM Worldwide

On October 6, 2014, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc., for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on July 8, 2015,. The Note is convertible into common stock, at holder’s option, at a 45% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts.

Daniel James Management

On October 3, 2014, the Company entered into a Securities Purchase Agreement with Daniel James Management, Inc., for the sale of a 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on October 2, 2015. The Note is convertible into common stock, at holder’s option, at a 47% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts."

I'm pretty sure that the company's (Bioheart's) Sr Mgt knowingly and willingly inked and signed up for every one of those financing deals (using convertible debt w/ reset provisions in the pricing) and every last one similar to them- cause it's in their SEC filings and I don't see anything saying they were forced to do those financing deals or any verbiage like that? I think they, BHRT, sought out those lenders and wanted to get their money from them- willing to give them as many commons shares of dilution as needed to get the cash in return for them IMO. Pretty sure that's the way it worked from reading those SEC filing details.

One can read other recent 10-Q/10-K filings and find Asher, Fourth Man and other "convertible debt" financing deals- pretty much every qtr going back for many, many yrs.

My 2 cents on the "stock manipulation" and "karma" thingy stuff (which should be reported to regulators IMO- I mean who's the manipulators? Where are they and who do they work for or how exactly do they do this "manipulation" stuff? Is the company doing any of this "manipulating" for example? This should be reported IMO. The SEC and FINRA, aka the stock market regulators has ways for reporting theories about possible stock "manipulation" taking place, but I don't think they deal in the "karma" stuff part?)

Here, here's management's own words too- about their financial condition, also from their most recent file 10-Q, "maybe" a possibility as to why maybe their stock is not hugely "in favor" right now- I mean "possible" versus the "manipulator" and "karma thingy" theory stuff-

PAGE 12, latest filed BHRT 10-Q:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during nine months ended September 30, 2014, the Company incurred an operating loss of $1,247,199 and used $747,184 in cash for operating activities. As of September 30, 2014, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $10.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time.

The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern."

Again, just my 2 cents and maybe a few other "theories" to go along with the "manipulator/Karma" thingy stuff ideas.

Quote: "What does that have to do with a companies evolving business model, products, and services? What relevance does sliding have to company leadership? Does sliding effect the developing science and does it serve the need of the public."

First off: 1.3 MILLION shares on the Ask now at .0103 and BMAK backed off a few levels. That's why it looks like they're giving it a little breathing room all of the sudden IMO- they're gonna try and unload a big block now looks like. But the Bid is weak and barely budged- they've opened the spread up a bit now, like they want to try and get a bit more on this large block they're selling for "someone".

http://www.otcmarkets.com/stock/BHRT/quote

0.0089 / 0.0103 (202000 x 1380000)

What does a falling price and continually lower highs and lower lows and falling Bid/Ask mean for a company in this condition? A LOT IMO:

When one understands how this company is being financed- which is essentially via 100% PURE, toxic, convertible debt solutions and now a Magna "credit line" facility - both of which have share discount provisions in them, and in the case of the "toxic" convertible debt are "floorless" - they'd understand that a sliding Bid/Ask on a daily basis can be devastating to the common share price and company's ability to get or raise the survival funds they're living off of.

Read any of the convertible (toxic) debt financing provisions- they all have reset conversion formulas built in- meaning the lower the share price goes, the avg share price of the past 3 or 10 or whatever number of trading days is stated in the conversion formula- then that's how the convertible debt lender gets their shares priced.

When the stock trades like it is now- the amount of dilution that can occur from a continually falling Bid/Ask can literally drive the common shares to not only 2 zeroes after the decimal, but even lower than that- as there literally becomes no limit to the dilution that can happen

Here's the SEC itself commenting on this type of toxic, "ratchet" or "death spiral" financing and what devastation it can cause to the common shares of companies who rely on it. It's called toxic for a reason- and yes, the sliding Bid/Ask has enormous implications IMO for this company's desperate financial condition right now. The lower the price drops- their ability to raise desperate cash gets that much harder and much more dilutive:

http://www.sec.gov/answers/convertibles.htm

Here are a couple of the most recent toxic financing deals done by BHRT- YES, the implication of a falling Bid/Ask makes the horrible terms on these deals that much more devastating IMO, when these firms decided to convert to dilution shares- which are coming due very soon.

Most recent filed 10-Q, PAGE 26: (ALL affected by a dropping Bid/Ask, it has HUGE implications if one understands the conversion formulas listed below)

"NOTE 13 — SUBSEQUENT EVENTS

Subsequent financing

KBM Worldwide

On October 6, 2014, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc., for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on July 8, 2015,. The Note is convertible into common stock, at holder’s option, at a 45% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts.

Daniel James Management

On October 3, 2014, the Company entered into a Securities Purchase Agreement with Daniel James Management, Inc., for the sale of a 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on October 2, 2015. The Note is convertible into common stock, at holder’s option, at a 47% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts.

Magna Equities, LLC

On October 7, 2014, the Company entered into a securities purchase agreement (the “Purchase Agreement”) with Magna Equities II, LLC, a New York limited liability company (“Magna”). The Purchase Agreement provides that, upon the terms and subject to the conditions set forth therein, Magna shall purchase from the Company, a senior convertible note with an initial principal amount of $307,500 (the “Convertible Note”) for a purchase price of $205,000 (an approximately 33.33% original issue discount). Pursuant to the Purchase Agreement, the Company issued the Convertible Note to Magna. The Convertible Note matures on August 7, 2015 and, in addition to the approximately 33.33% original issue discount, accrues interest at the rate of 12% per annum.

The Convertible Note is convertible at any time, in whole or in part, at Magna’s option into shares of the Company’s common stock, par value $0.01 per share (the “Common Stock”), at a fixed conversion price of $0.01035 per share. $40,000 of the outstanding principal amount of the Convertible Note (together with any accrued and unpaid interest with respect to such portion of the principal amount) shall be automatically extinguished (without any cash payment by the Company) under certain conditions described in the Purchase Agreement. In connection with the execution of the Purchase Agreement, the Company and Magna also entered into a registration rights agreement (the “Registration Rights Agreement”). Pursuant to the Registration Rights Agreement, the Company has agreed to file an initial registration statement with the SEC to register the resale of the Common Stock into which the Convertible Note may be converted,"

Falling Bid/Ask price has all kinds of implications for this cash poor, poor financial condition nano-cap IMO. The lower it goes- the more dilution and if trying to use the Magna "credit line" the less cash they can get "per draw" and it will cost more dilution per draw the lower the price goes.

Simple as that IMO. It's accounting 101 and all in the SEC filings.

Bid/Ask continually sliding down again, wow:

BMAK just inched the Ask down again, now to .0089

0.0084 / 0.0089 (10000 x 10000)

http://www.otcmarkets.com/stock/BHRT/quote

Only one 10K block on the Bid at .0084 and then it's down to .008

Just nothing is moving it at this point it seems? Just no buyers at all rushing in here that I can see- even at this sub 1 cent area?

Don't know why no buyers rushing in? I think this may re-visit that .007 area again real soon IMO. Just very weak here and no bid support it seems to me.

LOL, Quote: "BHRT is moving in the right direction with their plan to use what resources and science they already have as solid building blocks. Specifically their revenues are increasing. This quarters report should be very telling.

Another advantage the company has is Mr Tomas. His professionalism, intellect, passion for success, and his proven capacity for survival will move this company of the future forward and lend to ultimate success. "

Moving in the right direction? The common shares are at SUB ONE CENT near their all, all, all time lows? The common shares have lost about 99.98% of their value since going public in 2008 on the NASDAQ (de-listed less than about 1 yr later, OTC ever since) and the market cap is now barely cracking $5 million w/ current debts exceeding $10 million. If that is "moving in the right direction" and "forward" then it must be in some alternate stock universe I'm totally unfamiliar with IMO?

Quote: "Another advantage the company has is Mr Tomas......"

Based on what are all these vast claims made about CEO "Mr Tomas"? The common shares, since "Mr Tomas" took over 100% control of the company as CEO have lost about 98% or more of their value. When he took over in mid 2010 the common share price was right about .50 CENTS a share, maybe some spikes even higher. Today it's about .009 a share with a recent low of .007 (yes, 7/10th of ONE CENT) a share.

The simple math shows that to be a loss of approx 98% or more. Also, the shares have been massively, massively diluted under his tenure as CEO- from maybe 30 million max to now well over 600 MILLION share O/S by this next 10-K (a factor of 20X or more) and authorized shares increased to 2 BILLION on a sub one cent share price. The market cap has collapsed to maybe 1/3 of what it was when he began as CEO.

What "success" is that- in what business world? I'm not familiar with any CEO being deemed some wonderful supposed "success" based on those or any other of the BHRT standard, industry recognized metrics and realities for public traded stock companies (ROI, profitability, positive cash flow, cash mgt, going concern warnings in every SEC filing probably since he took over as CEO, little or no cash at any given time, some debt defaults, never re-started a single major FDA level trial since about the 2009/2010 time frame despite numerous "claims" it would happen, never inked a single "large" non dilutive "financing deal" despite numerous claims and PR that it would take place, etc, etc, etc)

Where does all this supposed "knowledge" of "Mr Tomas" come from- versus what is known via only the public available metrics and company performance and public available, verifiable info?

Makes ZERO sense to me, IMO? Not seeing it? Not seeing where one would even get the supposed "personal" type info to make those claims about him as CEO- as it's "personal" info about him and not public info of him as a company CEO based on his CEO performance metrics or what can be found based on company metrics, performance, common stock performance, the company's on-going desperate financial condition, massive on-going share dilution, etc?

I mean- how does one supposedly know "Mr Tomas'" supposed "intellect"? How is that even possible? Is there a public available IQ test they published or some other recognized metric or standardized academia or similar test that they as a company did or something and then made available to the general investing public? How does one know the "intellect" of a CEO in supposed detail?

Again, not seeing how that's even possible or even makes one iota of sense IMO?

"his capacity for survival"?? Is he on a TV show like "survivor man" or something that I missed where they test and demonstrate one's professional level "survival" skills, etc? Again, where is this public info about his "survival capacity"? How does one even measure a person's "survival capacity" - using what standard metrics or test (was it a military survival test he passed for example? Those are standardized and well recognized, but I've never seen any public, published info he passed a "survival test" that I know of?)- again, where are the public details on these wonderful, vast "claims" like "ability to survive" and all the rest?

I'd love to know where to find this public info- it's fascinating IMO.

What, QUOTE: "HUH? WELL LOOKING A THE VOL TODAY I WOULD SAY A LOT OF PEOPLE THINK THIS IT IS WORTH BILLIONS...Vol is not imaginary..... "

Well, I'd say based on the FACTS OF THE MARKET CAP, AS OF RIGHT NOW- it's not "worth billions" or even "thought" to be worth imaginary "billions"- let me check the screen.

AS OF RIGHT NOW the market cap says it's worth just about $228 MA MILLION. A tad shy of imaginary $BILLIONS, just a tad IMO.

$228 MILLION is the "value" the free market is assigning as of right now on my screen. NOT a $Billion or $Billion(s) plural- off by a factor of 5 or more.

All the best

BMAK is parked on the Ask w/ a 10K share block at .009. Looks like that's the top for now then IMO.

http://www.otcmarkets.com/stock/BHRT/quote

Only 50K or so on the Bid at .0085 (about $400 bucks worth) and then a lot at .008. Looks like maybe they're gonna try and take it back in the .008 area then today- if the past few weeks have been any indicator.

Just no buying pressure in here at all it appears- not even at these prices of sub ONE CENT.

A lot of PR and "news" and "revenue" talk and what not- but nothing has gotten it to even slightly reverse this severe 9 month plus down trend or now, even get it out of the sub ONE CENT basement?

Seems perhaps just too much dilution share down pressure maybe to overcome IMO?

Quote: LOL, "that patent is worth billions on its own .."

Funny how every patent or whatever they have is supposedly "worth" imaginary $BILLIONS alone.

Yet not ONE large funding source or non-dilutive partner or anyone else has ever stepped forward and gave um a $100 bucks worth for those imaginary $BILLIONS just sitting their for the taking? Why? Why is that?

Where's all the smart money hiding as this had gone to 5 CENTS and was 6 CENTS pre R/S on over 3 BILLION shares of dilution?

How is it they're so good at I guess hiding all those imaginary $BILLIONS in one patent "alone" - let alone all the others?

Why is their market cap what it is when they got these $BILLIONS hidden in some patent file drawer I guess?

Never been able to figure out how that works exactly? A supposed "worth" of $BILLIONS- all except the fact it's not worth $BILLIONS according to their market cap, price of their securities and no "big money" has ever come knocking looking for those $BILLIONS either? Why?

The NASDAQ "Global market" has tiers within itself- and there's also more than one "Global Market" based on suffixes. Read the wording of my sentence- it's clear what I'm stating.

https://listingcenter.nasdaq.com/assets/initialguide.pdf

Quote: "52 week highs coming tomorrow float went from infinite to finite"

WHAT? The float was "infinite"?? How does that work? "infinite" - a mathematical term that means unlimited, unmeasurable, w/o any bounds, etc?

Funny, I can go look the FLOAT OF OCAT up right now.

Here it is from Yahoo finance: OCAT FLOAT is 28.79 MILLION shares. That is NOT "infinite" - in fact it's quite "finite".

What imaginary part of OCAT float is supposedly "infinite"?? What stock ever in existence, on any market has ever had an "infinite float" when every stock to ever exist only has a FINITE number of shares issued and authorized? A stock could have 100 BILLION shares O/S and still not even be close to having an "infinite float"?

What does that even mean or is supposed to mean? It makes ZERO sense at all? There's no guarantee a 52 week high is coming tomorrow- based on what?

Aug, exactly my sentiments. They're going for the lowest tier NASDAQ global market which has no shareholder equity requirements. Just $4 a share and min market cap is all that's needed. Which tells me they never raised any capital (which we knew) and are living off of Lincoln which IMO is not enough to even begin to start any serious trials.

So I think the NASDAQ pro short hedge fund boys and others shorts will smell blood in the water if this doesn't have some real news coming quick behind it. "Maybe" good for a pop perhaps, but it'll probably be moving real fast, North or South IMO. Volatile.

I too am going to wait- wait to see what the 60 MILLION shares "available" is going to end up being in the end. If they're going to fund trials- they need a pile of money they don't have right now IMO.

Dilution and weakness on the NASDAQ will bury this just as quick as on the OTC IMO. A spike, sure- probably highly likely. Do I want to get bulldozed if they let the air out of the tire in a split second? No.

Wait and see when it gets long term stability- mainly how they going to fund and/or how much will they dilute going forward from here. Until that's answered- I think it's a roller coaster more than likely. I don't have the time right now to park in front of a screen with my finger on the sell button during the entire trading day and don't wanna get wiped for a 20% down side move or whatever if it goes that way after a spike.

Waiting for me too. My 2 cents.

LOL, "Good Volume, Holding very firm. The Revenue and Business Plan make this a winner. We could see IBC Funds LLC, A Capital etc etc step in here soon."

Yeah, right on. A falling Bid/Ask for months now on higher than avg volume and under SUB ONE CENT and a market cap barely cracking $5 million is "holding firm"???

OK, I guess?

"revenue" when exceeded by increased expenses doesn't create any "winners" IMO?? How does that work exactly? On what financial statement is that reality playing out?

BMAK spent the entire day parked on the Ask w/ a 10K share block at about .0091, capping it off. The stock is making lower highs and lower lows and one decent sell-off day will drop it back to .007 (the recent low) in a blink and maybe break the all time low of .0066.

What "fund" in what imaginary world is going to sink any money into this- unless it's a convertible debt deal (or similar guaranteed downside protection built in) that will give them total downside protection and a boat load of dilution shares too boot? IBC is just another dilutive, convertible debt lender from all I know of them- seeing them on past penny deals on I-HUB and similar.

Magna is already all over this one- why would IBC step in here now?

What's the big attempt to "try" connect IBC Funds to this now?

A bunch of conjecture about nothing IMO. No basis in fact or backing data to support any "claims" being made.

LOL, QUOTE, "Everybody is entitled to their own opinions, but not their own facts and IMO what's in the company financial statements are fact.

BUT, past quarters are history and there is a new business plan in town. Caustic borrowing was what "painfully" was required to keep BHRT alive to a point where revenue could be generated to offset the expense of moving forward. They even have a reserve (Manga) available if they would still need more.

NOW, revenue is being generated to a point in which BHRT can pay off expensive debt and pay staff reasonably for their hard, dedicated, and effective work. It will be more obvious in the coming quarterly report - facts. They will also be able to buy back diluting shares, and most important to me (an investor) give me tremendous value considering the risk I took with my money in a science and people who I am convinced will earn me returns of serious proportion."

End quote.

1) ""Everybody is entitled to their own opinions, but not their own facts"?? WHAT does that even mean? "past quarters are history"?? Wow, like things that happened prior are the PAST? There's been a "new plan" of some sort like about every 6 months IMO and per my experience- I could list all the "teams of experts brought on-board" PR links and "$20 million financing to be raised" PR that never happened and "term sheets inked" PR or "we have an agreement" or a "partnership" never heard about again- all liked in PR etc. It's nothing "new" in my opinion. Been reading the same sounding "stuff" for yrs - all as the share price continued to decline, no "big financing" ever materialized and "no major trial" ever advanced again and dilution occurred unabated at a furious rate- unending for all intents and purposes. "new plan"?? OK, sure IMO. Great. As the shares are hitting 52 week and near all time lows. OK.

2) BS to the rest- as it's does not contain "facts"

a) BHRT is not done using toxic debt? They just inked a Magna note only a few months ago- at horrible terms (face value of like $307K but BHRT only received $205K, a 33% discount- something to that effect. See latest 10-Q) I'll speculate that by this next 10-K filing, there's a very good possibility they've taken on at least one more, if not more, toxic note financing deals- for survival cash, IMO. It'll be one of the first things I check for. They also inked another series of toxic notes as recent as Oct 2014, all coming due this summer, despite "revenues"- those notes were for pittance amounts of cash like $25K and $38K etc. If this imaginary "revenues makes them cash positive now" blah, blah then WHY would they be doing toxic, floorless convertible debt notes for micro increments of cash like $25K at a time? Notes that are going to cause millions if not 10's of MILLIONS of shares of dilution at share prices like the present? Why?

b) There is a whole slew of toxic debt, aka convertible debt "notes" all coming due in the coming months- which will mean massive, massive dilution shares being issued as those notes are converted. The Magna credit line is 100% dilutive and has a share discount involved- and at these prices, mega dilutive. Again, it's not a "reserve" - BHRT said they plan to tap and use it all. What "reserve"? They don't have enough cash presently to conduct month to month operations- and that's with R&D wiped to near zero. What happens the instant they fund even the start of a phase 3 trial? Where's that cash going to come from?

c) The Magna credit line is not some "back up" line? BHRT made it 100% clear in the prospectus that they plan to tap, draw-down on all of it. BHRT has no cash or cash reserves? NONE. Where on the balance sheet are they, what page in what SEC filing? BHRT has cut R&D spending to essentially nothing (less than $3K a month per last 10-Q filing) yet they just "claimed" they're supposedly going to re-start and conduct a phase 3 level trial. They have no cash for that? They'd need every dime of that Magna credit line and then some IMO to even put a down payment on a decent, FDA quality phase 3 trial. (REMEMBER MIRROR, being "fully funded by Bioheart"??) How'd that work out? They HAD NO CASH to fund it- never did.

d) BHRT has no cash to run a share buyback program? That's comical IMO. Read the supposed "share buyback" PR. It's so loaded with "might" "if" "maybe" "possibly" "if the time is right" blah, blah, blah SAFE HARBOR same old story. It of course gives no dollar amount(s) allocated over what time period for the “possible/might/maybe/perhaps ole “share buy back ( a company share buy back will typically announce what portion/maximum amount of cash reserves may be used for the buy back and over what time frame – as in “a maximum of $1 billion over the next 12 month period” of similar wording.). The way the BRHT PR is written- if then buy no shares back or buy one shar back then the PR is true- makes no difference SEE SAFE HARBOR and every word of disclaimer that it may/might/maybe won’t happen and can be cancelled at any time no notice needed and none will be given blah, blah, blah what a surprise. (Remember ONE PATIENT ENROLLED in MIRROR PR? How much farther did MIRROR ever go after that- 1.5 yrs later? Yep.) What cash do they have to buy back shares- let alone in a quantity to even remotely make a dent in the massive on-going, continual dilution? Read the last filed 10-Q, BHRT was still, despite the big "revenue" claim- still paying common bills by issuing common stock shares- for a whole slew of things, as they HAVE NO CASH. They finished the last qtr with $46K total cash on-hand despite "revenues". Top line revenues made NO DIFFERENCE to their cash desperation situation as their expenses out grew "revenue" results- especially after the high cost of sales. Look at the gross margin last qtr- it was dismal. They banked about 10% on the top line revenue- nowhere even remotely close to enough cash to fund even their base salaries and bonuses- let alone actually run and conduct business and all the other expenses plus debt they face.

e) They're not producing any positive cash flows that could be used to pay down debts? What page of their SEC filings shows that to be true? Again, they finished last qtr with a grand total of $46K cash on-hand, and they didn't pay down any major debts using cash? They had one debt discharged as the creditor was willing to take a write-off on it. The other debt reduction was primarily via debt to equity swaps done by some insiders. They weren't paying off any major debts using any internally generated cash? It simply isn't true per their own financials? What page of a SEC filing shows that happening?

f) Again, "revenues" aren't even close to producing enough internal cash to pay even the base salaries and bonuses to just 2 people in the company. "Revenues" first have to have COST OF SALES subtracted before any cash is banked- look at the statement of operations and see what they banked versus what they spend. Also, their loss from operations is actually LARGER yr over yr for the same period of the latest 10-Q filing for 2014 versus 2013. And that's after cutting R&D by over $400K in just this yr alone, and far more over the past 2 yrs- diverting cash from R&D to pay who knows what? WHAT cash is going to fund this supposed Phase 3 "re-start" of an FDA level trial? The INSTANT that spending is added back in to their cash flow statement and statement of operations (if it ever actually is, as in they ever actually re-start and fund a phase 3 trial again, as in remember MIRROR?)- the INSTANT those expenses would hit, they'd be even more cash poor, more cash flow negative, need to tap Magna for major dilution etc. As they do not have one dime of cash reserves and even while spending a pittance of $3K a month on R&D (which does not fund any trials- LOL) they still aren't self generating even close to enough cash to pay their own bills and not using toxic borrowing to survive. Just read the last 10-Q "statement of operations" or "statement of cash flows" and then the "going concern warning", it's all their in the FACT BASED SEC filings. You know, the "facts" part.

g) "future SEC filings are going to show or prove this"? One knows already what's coming in a public traded company's future SEC filings-like they've been told insider trading information? How would anyone but a corporate Sr. Officer be able to say "what's coming" in the next 10-K filing for example? How is that possible to know?

h) LOL, "NOW, revenue is being generated to a point in which BHRT can pay off expensive debt and pay staff reasonably for their hard, dedicated, and effective work."

Revenue is NOT being generated to a point to "pay off expensive debt"?? Again, where on their accounting entries is that fantasy happening? They discharged a key debt- they didn't use cash to pay back one dime on it? There filing is loaded with inter-party "related notes" and borrowing from Peter to pay Paul, only later to pay the "new" note back with interest, etc. Northstar is still owed money and earning and being paid w/ interest- while other debts total over $10 million. Just accounts receivable last qtr exceeded $2 million w/ $46K cash on hand (essentially insolvent IMO, and their own Sr. mgt SEC filed "going concern warning" I believe backs that up). Pay staff reasonably? What "staff"?? The entire company is a few "employees" and the only ones getting richly paid are TWO, who now per the SEC filing "exec compensation table" are receiving over $1,575,000 between the two of them as the common shares have hit and are hitting, all, all, all time lows while at the same time being diluted out at an incredible pace- over 300 MILLION shares in the approx past 1 yrs and about 50 MILLION more share just from around Nov 2nd 2014 to about early Feb 2015 via looking at the 10-Q filing versus the "proxy vote" SEC filing O/S share counts and doing the math. Over a $million a yr in compensation as your common shares have lost over 98% of their value "on your watch"?? In what alternate universe is that "normal" in any company, let alone a public traded stock firm? "performance" like that isn't usually "rewarded" - it typically ends up in some people being sent packing from my experience watching what BOD's do when their common shares are nearly wiped out or experience extreme loss of value as this company has? Bonuses and large base pay increases- as the common shares have been devastated? Makes ZERO sense IMO. None. Especially when they're paying common bills by issuing dilutive shares of stock (see any 10-Q or 10-K filing "subsenquent issuances" of shares, usually at the bottom area of the filing)

So yeah, lets stick to FACTS versus made up non-facts. Totally agree.

My .009 cents worth.

Everything just explained, is IMO right there in plain accounting form- on their own SEC filing, latest 10-Q, "statement of operations" - the rising costs, the increase in loss from operations (not positive cash flow, blah, blah), the enormous rise in expenses on the general/admin expense line, the low margin on the latest qtr's top line "revenues" which means they banked hardly anything on them (cost of sales ate it all up), etc

LOL BS: "SEC filings don't lie, The CEO was given $47K in currency with the rest deferred..."

"in currency"??

PAGE NUMBER of SEC FILING and WHAT SEC FILING???

Where?

Here is the SEC EDGAR database containing EVERY SEC FILING BHRT has ever submitted to the SEC. Just pick which one and the exact page number and copy the text verbatim that shows $47K.

Also, any "deferred" supposed imaginary unpaid compensation must then be "carried on the books" as "deferred compensation" (or a very similar term) on the company's balance sheet entries (as it's now a debt/monies owed) so what page and line entry is that on also? And what is the value of that entry- for all these past unpaid amounts? Where is it being accounted for?

Company's don't get to publish "executive compensation" tables in one part of their 10-Qs and 10-K's and then just NOT PAY IT but have those monies owed just vanish? It MUST be entered on to their ledger/balance sheet and carried forward until paid. On what page of what SEC filing is that? What amounts and what line entries in what SEC filing (10-Q latest would HAVE TO include those entries- as it has the balance sheet and statement of cash flows included)

http://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001388319&owner=exclude&count=40&hidefilings=0

Would love to see it.

LOL BS QUOTE, "it came to $47K per the audited 10Q- for 3quarter. He is working for free and will only make money when the company makes money or gets bought. "

1) 10-Q' are NOT AUDITED, so that is incorrect right there. It says so right in the 10-Q, "un-audited". Only the end of yr 10-K is ever audited.

2) NOWHERE in any 10-Q, let alone the 3 qtr 10-Q does it list, say, state or anything to the effect that CEO Tomas only received a supposed $47K total in pay?? NOWHERE.

What page of the 10-Q is this imaginary statement on? What page and the exact wording? IT DOES NOT EXIST and is not "audited" which means BS right there.

Pure MYTH that this CEO is "working for free". EVERY YEAR the SEC filings have contained an executive compensation table and every yr at least since 2012 the CEO and CSO are shown receiving very large pay increases to not only their base pay rates, but also large cash bonuses. AND NOWHERE, NOWHERE in any SEC FILING does it indicate they are not being paid those BOD approved salaries and "other" compensation. PURE MYTH.

WHY would the BOD approve raises each yr and why would the company furnish a EXECUTIVE COMPENSATION TABLE, a detailed one, IN EACH SEC FILING- if those executives per some myth are supposedly not being paid yr after yr? WHY would that table be in the SEC filings and why would the corresponding expense line entry for general/Admin expenses be seen rising proportionately too? Why?

LOL QUOTE: "Biotech companies dilute don't mean they go BK LOLzzz"

A great many companies that trade on the OTC and ever reach true "penny" status, as in 50 cents or 25 cents by statistical facts do end in BK.

Passing well over 600 MILLION shares O/S on a sub ONE CENT share price- is a sign IMO that a company is in serious, serious trouble. A great deal of the most profitable and largest companies trading on the NYSE and the NASDAQ to not have that number of diluted common shares O/S. I can list 100's of them- cash generating, profit monsters with far, far less O/S shares, and they pay dividends too boot.

When a company gets to true "penny" as in SUB PENNY, like .009, .008, .007 and even .0066, with market caps like a pittance of say barely $5 million dollars, w/ essentially almost no staff (2 people plus a few others), w/ essentially no assets as in $250K total to their name against immediate debts exceeding $10 MILLION, w/ essentially no or little cash at any given time, for example as in $46K cash end of last qter (despite so called "revenues") per their last SEC filing, etc- per all market research, numerous academia studies, the SEC warnings itself, etc- a great, great numbers of companies that ever reach sub ONE CENT do in fact end in BK, a vast percentage of them. Just easily researched and easily verifiable market data FACT.

And NO, top line "revenue" per their own SEC filings has not made a difference to their cash desperation situation or lack of need to continue to use toxic, "convertible debt" financing- they did toxic notes as recent as Oct 2014, despite "revenues" as their expenses have risen faster than any bottom line revenues after cost of sales- see 10-Q filing, statement of operations. They are not generating even close to enough cash to be cash flow positive or not rely on dilution or toxic debt financing- nothing in the last 10-Q showed that to be true. Their LOSS FROM OPERATIONS is LARGER in 2014, yr over yr, for the same period in 2013 due to massive expense increases, and despite R&D spending being cut to nearly zero (less than $3K a month). $3K a month funds nothing in terms of a phase 3 trials. The INSTANT they put back in any R&D expense line costs for an actual "trial" (like MIRROR that never actually got "funded" as claimed) their cash situation will only get that much more worse. Simple as that. READ THE "financials" in the SEC FILINGS- it's all there.

From the company's own 10-Q, most recently filed, PAGE 12:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during nine months ended September 30, 2014, the Company incurred an operating loss of $1,247,199 and used $747,184 in cash for operating activities. As of September 30, 2014, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $10.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time.

The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern."

See their own financial entries- the OPERATIONAL LOSS in 2014 is going to EXCEED THAT OF 2013, despite top line "revenues" and despite over $400K being hacked out of the R&D expense line. It's right there, plain as day. They're not cash flow positive- not even close. Let alone they're not funding any phase 3 supposed "trial" right now- which would blow those expenses off the chart and put um deep, deep cash deficits, worse than even those numbers in that table below. Simple accounting realities. And their continual GOING CONCERN WARNING reflect that reality. "revenues" when exceeded by INCREASING EXPENSES change nothing when it comes to cash being generated. If one spends $1.10 or $1.25 for ever $1 generated of "revenue" they either borrow endlessly or eventually go broke- it's just that simple. It's biz 101 basics. Companies with over a $BILLION in revenues go broke all the time- Radio Shack being the most recent example. They just filed full-on BK w/ annual "revenues" of about $3.5 BA BILLION annually. Made no difference- as their "expenses" exceeded their revenues.

Look at the last 10-Q and ask why a financially healthy, cash positive company pays ordinary bills in SHARES OF COMMON STOCK??

Last 10-Q, PAGE 27:

"Subsequent issuances

On October 3, 2014, the Company issued 514,886 shares of its common stock as payment of $70,521 interest on its Northstar (related party) debt.

In October 2014, the Company issued 1,818,182 shares of its common stock in settlement of $20,000 of convertible debt.

In October 2014, the Company issued 1,293,103 shares of its common stock in settlement of $15,000 of convertible debt.

In October 2014, the Company issued 2,260,764 shares of its common stock in settlement of $18,000 of convertible debt and accrued interest of $2,120.

In October 2014, the Company issued 552,846 shares of its common stock in settlement of $5,500 of convertible debt and accrued interest of $1,300.

In October 2014, the Company issued an aggregate 2,773,549 shares of common stock for consulting services.

In October 2014, the Company issued 538,875 shares of common stock in settlement of accounts payable."

Quote: "Ok. How much is the ACTUAL amount of "cash" that Mike Tomas was given in "cash" compensation in 2014>?"

Do the math.

Here's his compensation PER THE COMPANY'S SEC FILING- cite any other information contrary to their own SEC filings. Since he got a very large raise in mid 2014 one will obviously have to use prorated calculations in their math to compute the 2013 pay rate up until mid 2014 when the large raise was given- and then compute the remaining amount for 2014 post the pay increase.

From the last filed 10-Q, PAGE 23:

"Employment agreements

On July 28, 2014, the Company’s Board of Directors approved the 2014/2015 salary for Mike Tomas, Chief Executive Officer, at $525,000 per year, beginning July 1, 2014 with an incentive bonus ranging from $150,000 to $500,000. In addition, the Board of Directors will grant Mr. Tomas options to be determined on or before June 30, 2015. The Company’s Board of Directors approved a bonus of $500,000 and options to acquire 10,000,000 shares of the Company’s common stock for ten years with four year vesting and a cashless exercise provision at an exercise price equal to the five day average closing price of the Company’s common stock as of August 1, 2014. The cash bonus may be paid in the form of a six month promissory note."

Given that raise in mid 2014, the base pay rate alone at present (THAT HE COLLECTS EACH MONTH) is:

$525,000 / 12 = $43,750 per month he receives in base pay alone since July 1, 2014. Then add in the bonus amounts etc. Simple math.

All in the SEC filings - and the "marketing, general, admin" expense line of course can be seen increasing massively at the same time as the Tomas and Comella large base pay raises and bonuses were issued- as one would expect from an accounting standpoint.