News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Bid dropping again- it's all the .004's now:

0.0048 / 0.0053 (120000 x 10000)

Both BMAK and CDEL are all over it this AM, with BMAK setting the "cap" at .0053 with the 10K share block. This thing isn't going anywhere IMO, except likely DOWN.

The Bid is for all intents and purposes now, a .004's proposition at best it appears. There's 1.6 MILLION shares parked at .0045 today, that would be where the share price is heading then IMO.

BMAK is for now running a "bracket" - sitting on both the Bid and Ask at .0048 and .0053 w/ 10K share blocks respectively (a wide spread) - but if BMAK pulls their "stop block" off that Bid- then it's gonna head for that big block of 1 MILLION plus shares hanging out there at .0045, that's what I think will happen more than likely

It's just the "way it is" now- with the massive, massive dilution the company has entered in to and the continual use of toxic, convertible, floorless debt deals (qty-5, FIVE new ones in just Jan/Feb and April of 2015 already, see latest SEC filed 10-K and 10-Q)

For the first time that I've seen- there's a "legit" - meaning current time stamped, actual block on the Bid at .0038 being shown by MM BKMM for 400K shares. That's how weak the Bid really is it appears.

"PR" hasn't moved or budged it a micro smidge since the 2015 free-fall really picked up steam (post signing with Magna in late 2014), the SEC filings and PR reports of "our great 10-Q" or whatever, released after the filings hasn't made any difference, the big "new plan" thingy put out in PR and in the last SEC filings (with Power Point slides and vast "projections" of revenue or whatever) hasn't budged it off its new bottom prices here, the company PR about the "share buyback program" LOL has made a dent (sorry, but it was funny when issued IMO, and still funy now to me, using dilution shares to buy-back your own dilution shares?? Never did figure out that PR, just never "got it" personally I guess?) - no big buyers or big "net buying pressure" seem to be appearing from anywhere, even at sub 1/2 CENT levels?

When the company just issued out something like 80 MILLION plus dilution shares in the first few months of 2015 (see the share count from the last 10-K to the most recent 10-Q and see how much dilution occurred), and many of those shares were steeply discounted, some being as low as about .003 maybe .0035 a piece- I just don't see what catalyst this company of a few people is possibly going to have now to over come that massive down force those dilution shares are going to put on the common share price going forward- many of the convertible debt deals "coming due" (meaning they'll be converted to even more free trading shares) all through this summer and in to Oct/Nov 2015 and even to Jan 2016, if these guys are even still functioning and a "GOING CONCERN" still by then- who knows with this share price hovering in the .004's now?

Next big leg down- which I believe is imminent IMO, given BHRT's reliance now on Magna (as well as Danial James and KBM Worldwide and Asher and Fourth Man and Vis Vires now too, etc) - I believe the next "down tranche" the next big convertible debt "conversion leg" - will run it to the .003's w/o a doubt, as it's touched .004 twice now, on extremely high volumes.

My .0048 cents or so worth, for what it's worth

RED, $6.34 and DROPPING like a space capsule on re-entry !!

It was $7.50 END OF APRIL 2015, less than 30 DAYS AGO, this means the stock is DOWN 15%, ALMOST 20% RIGHT NOW in 30 days, not "up" as has been "claimed"- NO, it's not being "bought up" by supposed "institutions" blah, blah.

Wait, it's those imaginary "big institutions" all doing "stealth" buying, LOL !!! NO, this is called SELLING, NET SELLING and NO it's not supposed "accumulation" - it's good ole, plain vanilla, NET SELLING. Simple as that.

Oh, and the entire market really just doesn't "get it"- how having almost NO CASH, and NO "big FDA quality Phase II" underway (let alone even remotely funded) and having a common share value that's DOWN, RED about 99% since it began trading public, and a history of NEVER being able to attract or raise any major, high quality capital/funds w/o using low grade dilution lenders of last resort such as Lincoln, etc

Cause you know, it just all supposedly "WORKS" when in reality- all they have after 20 yrs is a tiny Phase I under their belt- but "the market" just isn't sharp enough to figure out all the "secret sauce" stuff that's really supposedly there and all, hidden in the tall grass in stealth mode or some such myth ???

See, that THREE YEAR HISTORY- it's not actually real I guess (nor the SEC violations and prosecutions and large legal settlements paid for on the shareholder's dime or the accounting "revisions" aka sometimes called fraudulent statements/filings, etc), it's just a grand illusion and "the market" is not "getting it yet"??

Or, the market probably really just doesn't "get it"- all this "stuff" n junk that the company plasters all throughout their own SEC 10-Q and 10-K filings and in public made statements and all the rest, NO- it's just "boiler plate" supposedly and really not part of the yellow brick road fairy tale riches version and all the myths and all-

Here's a few "samples" of THEE COMPANY'S OWN WORDS, versus some myth that "cash is no problem" and they're supposedly just gonna sail on in to some "early_approval" blah, blah, blah.

Just filed OCAT 10-Q, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales FOR THE FORESEEABLE FUTURE, IF EVER. "

(What? WHY WOULD THAT BE, if their mythological "therapy" already "works"?? Why?)

OR,

PAGE 7, SAME SEC filed 10-Q, most recent:

"The Company has NO THERAPEUTIC PRODUCTS CURRENTLY AVAILABLE FOR SALE AND DOES NOT EXPECT TO HAVE ANY THERAPEUTIC PRODUCTS COMMERCIALLY AVAILABLE FOR SALE FOR A PERIOD OF YEARS, IF AT ALL. These factors indicate that the Company’s ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

(WHAT?? HOW CAN THAT BE? That's OCAT'S most recent filed SEC 10-Q?? According to MYTH they have a "therapy", RIGHT NOW, that supposedly "just works" and one can GET, NO???? So why does their 10-Q say just the opposite of the myth? The 10-Q says, "The Company has NO THERAPEUTIC PRODUCTS CURRENTLY AVAILABLE FOR SALE AND DOES NOT EXPECT TO HAVE ANY THERAPEUTIC PRODUCTS COMMERCIALLY AVAILABLE FOR SALE FOR A PERIOD OF YEARS, IF AT ALL." Something's a miss it seems. OCAT says they HAVE NO THERAPIES currently proven "that work" or "are for sale", NONE??? Why would they print that in their SEC filed 10-Q??)

Or, how bout why they're just about OUT OF MONEY when they have these mythological "therapies" that already supposedly "JUST WORK" as supposed unchallenged FACT? What? Why did they put all this other "stuff" then in their most recent SEC filed 10-Q and why did their own Lanza make statement verbatim like the ones below, ones where HE SAYS CAUTION and MORE TESTING NEEDED? When something supposedly AS FACT (which is a myth) plain old supposedly "JUST WORKS" well SHAZAM, then one doesn't say or need all the junk and stuff like below, the FACT BELOW said by the company's own Sr. Mgt and printed and signed in their own duly filed SEC documents- why, why would they say all the FACTS below:

From the highly respected science journal NATURE:

www.nature.com/news/stem-cells-pass-safety-test-in-vision-loss-trial-1.17451

Lanza doesn't say "IT WORKS"??? He says CAUTION and MORE TESTING NEEDED to "prove" anything? He didn't dispute or retract or question the NATURE article? Why? He DOES NOT EVER SAY "it works" - he says MORE TESTING NEEDED, lots more testing and lots more MONEY.

The VERBATIM article, again, from the highly respected science journal, "NATURE"-

"A company that has spent more than 20 years trying to develop treatments based on embryonic stem cells is taking encouragement from small, preliminary tests of the cells in people with progressive vision loss. If the technique continues to impress in larger trials designed to assess its effectiveness, it could become the first therapy derived from embryonic stem cells to reach the market.

A study of four patients, published in Stem Cell Reports on 30 April1, shows that injection of retinal cells derived from stem cells is safe for people with macular degeneration. The report follows similar results from a trial in 18 patients that was published last October2.

Both studies were meant to assess safety only, and neither included a control group. In the latest study, conducted by researchers in Korea and the United States, three participants were able to read 9–19 more letters further on an eye chart a year after treatment — but two of the three also gained some ground in their untreated eyes."

MORE...

"“This bodes well,” says Robert Lanza, chief scientific officer at Ocata Therapeutics in Marlborough, Massachusetts, and an author of the study. “But I think we need to interpret this improvement cautiously until more controlled studies are done.”

The sample size is too small to warrant much excitement, cautions ophthalmologist Tien Yin Wong of the Singapore National Eye Centre. “At this stage it’s hard to say if the visual improvement will be sustained,” he says. “But it’s very promising.”

Lanza speaking to a local MA newspaper-

www.telegram.com/article/20141014/NEWS/310149525&Template=printart

"We treated the last UK patients last month, and they also have not seen any safety issues related to the transplanted tissues themselves, either," Dr. Lanza said.

Advanced Cell now hopes to launch a 100-patient, phase 2 study in Stargardt's patients by the end of the year, according to Dr. Lanza.

A second, smaller phase 2 study in patients with age-related macular degeneration would follow, he said. Any treatment might not be ready for FDA approval until 2020, Dr. Lanza said."

THOSE are the "FACTS" as Lanza has stated um "on the record"- not the other myths that this is a DONE DEAL and SLAM DUNK and already "proven" to work, blah, blah, blah.

That was dated Oct 14, 2014 and the END OF YEAR phase II DID NOT HAPPEN.

Where's the BIG MONEY? Why don't they ever attract any large capital investments- especially any "high quality" money (non dilutive) or at least not cash-for-dilution-shares deals with discounts and all the rest attached to them? Why? Why is that? Why? They live on low grade dilution money and have NO WHERE NEAR the funds to get a large Phase II even started- let alone funded to completion? Why? Why is that?

It took like FIVE YEARS to get a micro sized phase I done. They've yet to even start the large and magnitudes more difficult and magnitudes more expensive Phase II trials (with control arms and placebo blinding)- why? If the phase I took about FIVE YEARS, then how long will these phase II trials take- the one(s) that were supposedly going to be fully funded and rocking and rolling by END OF 2014 and it's now almost half way through 2015 and the trial(s) are in the parking space, going nowhere and the latest Lincoln cash is dwindling down at an alarming rate. Why? Why is that?

www.sec.gov/Archives/edgar/data/1140098/000101968715001797/ocata_10q-033115.htm

Just filed OCAT 10-Q, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales for the foreseeable future, if ever. "

PAGE 7:

"The Company has no therapeutic products currently available for sale and does not expect to have any therapeutic products commercially available for sale for a period of years, if at all. These factors indicate that the Company’s ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

PAGE 7:

"The accompanying consolidated financial statements have been prepared in conformity with GAAP which contemplate continuation of the Company as a going concern. However, as of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. The ability to continue as a going concern is dependent upon many factors, including the Company’s ability to raise additional capital in a timely manner. The Company has no expectation of generating any meaningful revenues from our product candidates for a substantial period of time and must rely on raising funds in capital transactions to finance our research and development programs. Our future cash requirements will depend on many factors, including the pace and scope of our research and development programs, the costs involved in filing, prosecuting and enforcing patents, and other costs associated with commercializing our potential products. Accordingly, management’s plans to continue as a going concern contemplate raising additional capital including the prior execution of an agreement for a $30 million equity line in late June 2014, of which approximately $12.5 million remains available as of March 31, 2015. There can be no assurances that management can raise the necessary additional capital on favorable terms or at all. The accompanying financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern."

PAGE 24:

"We cannot assure you that public or private financing or grants will be available on acceptable terms, if at all. Several factors will affect our ability to raise additional funding, including, but not limited to, the volatility of our common stock and the broader public equity market, especially public equities issued by other pre-commercial biotechnology companies, and our ability to raise capital through non-dilutive transactions such as out-licenses. If we are unable to raise additional funds, we will be forced to either scale back our business efforts or curtail our business activities entirely. As of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern.

"

Most recent filed 10-K, PAGE 16:

"

Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. The timing and degree of any future capital requirements will depend on many factors, including:

"

Same 10-K, PAGE 16:

"We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

Same 10-K, PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties."

Same 10-K, PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

"

Boy, for a company with a mythological "therapy" that's PROVEN AS FACT to "just WORK" supposedly, they sure do like to plaster the GOING CONCERN WARNINGS all throughout their own SEC filings (GOING CONCERN is business speak for becoming "ill-liquid" which then leads to greatly cutting costs/spending or filing for BK)

But the myth is, that it all supposedly "JUST WORKS"??? LOL ! That OCAT is on some supposed "fast track"?? MYTH and conjecture and nothing more. The company's own SEC filings and public statement are in 100% contrast to "it just works". OCAT is fast running out of cash because NOTHING "just works" so far- and that's the reality. They're down to MONTHS worth of cash left to fund their operation and just booked another massive quarterly loss in their most recent SEC filed 10-Q and the common shares are being continually diluted and sitting near a 52 week low- in a still raging bull market.

Just FACTS versus conjecture and myths such as some "therapy" just "WORKS", LOL. In their own words, OCAT, they are YEARS and YEARS away from any "therapy" that "works" and can be sold to "human customers", IF EVER. That's their OWN WORDS.

Looks like LINCOLN just stepped back down on the SELL PEDDLE

The Lincoln, well oiled, well maintained BIG RED SELL BUTTON appears to have be working smooth after a maintenance and "breather" break it seems to me-

That's all that's going on here IMO- nothing more (and no, no "big institutional" buying is taking place, I don't believe it for a second)

This company lives and survives on PURE DILUTION and nothing more. There's a continual flow of shares being dumped into the market that must be bought up, and the price will fall if there's less buyers than the net selling volume.

The stock has been range bound by dilution and has literally GONE NOWHERE for 3 plus years- just totally DEAD MONEY FLAT to DOWN as the bull market of world history (especially for bio-techs) has passed it on by- gone, and fading now as world markets weaken and head for uncertainty everywhere. If they couldn't pitch and sell a secondary end of 2014, when the bull was raging- it's just gonna be that much harder now IMO.

A picture is worth a 1000 words they say, maybe two are worth 2000 words, who knows. Any way one slices is it- THOSE are two fugly ugly chart pictures IMO (maybe later I can get an overlay of the S&P and DOW indexes over-laid on um, to show how truly ugly those pics/charts really are in terms of DEAD MONEY)

Quote BS LOL, "Could the shorts get really in trouble? Could they loose their shorts? Is there enough shares for the shorts to cover and the institutions to buy as well?"

"loose" their shorts?? How would a short LOSE anything on this stock? It's been every short's dream stock come true, a 99% TOTAL LOSER to the common shares since it went public. If one had shorted this stock- they could have gotten filthy wealthy, unlike anyone long the stock.

WHAT SHORTS anyway? The open short interest as a percentage of float and O/S shares is noise level? How would any supposed "short" get in imaginary "trouble" or whatever?

Also, HOW does a public traded stock "run out of shares"??? The market makers MAKE A MARKET no matter what, they provide shares and liquidity no matter what- a stock can not "run out of shares", LOL !!

If anything, the MM's themselves are likely SHORTING to fill any buy orders on these little micro spikes- as that's what an MM does. When a rapid spike occurs, they short sell to fill the orders/demand, then pull the stock back later to "cover" their own positions, almost always closing out all open positions by day's end, shorting and all.

Quote, "I have met Dr. Paul Knoepfler several times at the World Stem Cell Summits and have had several of my blogs posted on his site...."

Great, but Dr. Paul Knoepfler DID NOT WRITE THE ARTICLE being referenced or discussed in my prior post (he, Knoepfler is quoted in it, among other experts/sources) - it's an AP (Associated Press) Journalist who writes for the "health" field who is the author and it was published in U.S. News And World Report among many other places (NOT on Knoepfler's blog)

"Stem cell "WILD WEST" unregulated- says AP (Associated Press) and U.S. News and World Report-"

http://www.usnews.com/news/business/articles/2015/05/18/stem-cell-wild-west-takes-root-amid-lack-of-us-regulation

That's thee U.S. News and World Report site itself (again, nothing to do with Knoepfler or his blog)

Associated Press May 18, 2015 | 9:17 a.m. EDT (that's the time and date stamp of publication citing the AP as the base source of the article)

"By MATTHEW PERRONE, AP Health Writer"

That is THEE AUTHOR signature stamp and label- and it's credited to an AP (associated press) journalist and not "Knoepfler" or his "blog"

Here's some links to the author's own pages/background on his writing (he's based out of Washington D.C., and again is a writer "on staff" for the AP, Associated Press):

http://muckrack.com/ap_fdawriter

http://bigstory.ap.org/content/matthew-perrone

https://twitter.com/ap_fdawriter

https://www.linkedin.com/pub/matthew-perrone/6/890/735

(he's got almost 9 yrs of writing for the AP specializing in "health field investigative journalism", he's not an amateur)

http://www.salon.com/writer/matthew_perrone/

Again, "Knoepfler" is just one of several sources cited in the AP written and published article, but he is in no way the author or source of it.

Once the AP (Associated Press, the single largest and oldest news and journalism source in the nation, and I believe in the world) - once they publish something and put it on the "wires" it gets picked up and re-published many, many places as they are a trusted journalism source due to their long history, level of editing skill, fact checking reputation, etc

Here is thee exact same article (and many outlets published the "video" version of the same AP article/investigative journalism piece) appearing on numerous other "news" and academic outlets (including Harvard's own website)- that obviously picked it up off the AP "wires" and re-published it:

https://hms.harvard.edu/news/stem-cell-wild-west-takes-root-amid-lack-us-regulation

http://www.foxbusiness.com/technology/2015/05/18/unproven-stem-cell-procedures-flourish-across-us-outpacing-regulation/

http://www.abcnews4.com/Clip/11506580/stem-cell-wild-west-takes-root-amid-lack-of-us-regulation

http://www.ajc.com/ap/ap/top-news/stem-cell-wild-west-takes-root-amid-lack-of-us-reg/pCfL8b/

http://www.postbulletin.com/life/health/stem-cell-wild-west-takes-root-amid-lack-of-us/article_3594deb2-37be-59e3-b032-3b711ea7103f.html

http://www.kcbd.com/Clip/11506580/stem-cell-wild-west-takes-root-amid-lack-of-us-regulation

'Unproven stem cell procedures flourish across the US, outpacing regulation' http://t.co/YmA38W50Va

— Stem Cell Foundation (@AusStemCell) May 19, 2015

AWFULLY RED RIGHT NOW, IT CAN'T HOLD EVEN $7 bucks.....

I know, this is the mythological "big institutional buying" and stealth supposed "accumulating" and all of that blah blah jazz, right?

You know, cause today the overall market is UP, but this is SOLID RED.

Yes, net buying by "big institutions" and "big accumulation" = a lower share price, in the alternative myth-market, LOL !!

Yes.

(It's still DOWN from $7.50 in only late April, only about 29 days ago, which indicates a net SELLING balance, not net "buying" or any "big accumulation", that's how the actual free markets "work")

Stem cell "WILD WEST" unregulated- says AP (Associated Press) and U.S. News and World Report-

FASCINATING article IMO. Really amazing journalism - and full of some real interesting key words about companies doing "training" and "opening clinics" etc in the highly un-regulated "WILD WEST" of the "stem cell" field- according to this journalism piece, even quoting the highly respected stem cell researcher at U.C. Davis and blogger, "Dr. Paul Knoepfler," (Knoepfler recently published a blog piece on BRHT, Bioheart)

http://www.usnews.com/news/business/articles/2015/05/18/stem-cell-wild-west-takes-root-amid-lack-of-us-regulation

http://www.ipscell.com/2015/05/bioheart-on-the-edge/

Pretty fascinating reading IMO. Real fascinating. One has to wonder if the FDA is about to step in and really start cracking their regulatory whip here real soon? Seems like a real possibility IMO.

Isn't part of the BHRT big "new plan" thingy- got a great deal to do with offering some cash for "treatment" stem cell "clinic" now on U.S. soil, in Florida? That's what's in the latest 10-Q, no? How do they do that if what they have as "treatments" are not FDA approved?

I never could figure that one out? Never made any sense to me personally? Still doesn't even more- now, after reading that U.S News and World Report/ AP Associated Press journalism piece.

http://www.usnews.com/news/business/articles/2015/05/18/stem-cell-wild-west-takes-root-amid-lack-of-us-regulation

Quoting the article:

"Unproven stem cell procedures flourish across the US, outpacing regulation

By MATTHEW PERRONE, AP Health Writer

BEVERLY HILLS, Calif. (AP) — The liquid is dark red, a mixture of fat and blood, and Dr. Mark Berman pumps it out of the patient's backside. He treats it with a chemical, runs it through a processor — and injects it into the woman's aching knees and elbows.

The "soup," he says, is rich in shape-shifting stem cells — magic bullets that, according to some doctors, can be used to treat everything from Parkinson's disease to asthma to this patient's chronic osteoarthritis.

"I don't even know what's in the soup," says Berman. "Most of the time, if stem cells are in the soup, then the patient's got a good chance of getting better."

It's quackery, critics say. But it's also a mushrooming business — and almost wholly unregulated.

The number of stem-cell clinics across the United States has surged from a handful in 2010 to more than 170 today, according to figures compiled by The Associated Press. Many of the clinics are linked in large, for-profit chains. New businesses continue to open; doctors looking to get into the field need only take a weekend seminar offered by a training company.

Berman, a Beverly Hills plastic surgeon, is co-founder of the largest chain, the Cell Surgical Network. Like most doctors in the field, he has no formal background in stem cell research. His company offers stem cell procedures for more than 30 diseases and conditions, including Lou Gehrig's disease, multiple sclerosis, lupus and erectile dysfunction.

There are clinics that market "anti-aging" treatments; others specialize in "stem-cell facelifts" and other cosmetic procedures. The cost is high, ranging from $5,000 to $20,000.

Berman and others point to anecdotal accounts of seemingly miraculous recoveries. But while stem cells from bone marrow have become an established therapy for a handful of blood cancers — and while there are high hopes that the cells will someday lead to other major medical advances — critics say entrepreneurs are treating patients with little or no evidence that what they do is effective.

Or even safe. They point to one stem-cell doctor who has had two patients die under his care.

"It's sort of this 21st century cutting-edge technology," says Dr. Paul Knoepfler, a stem cell researcher at the University of California at Davis. "But the way it's being implemented at these clinics and how it's regulated is more like the 19th century. It's a Wild West."

___

DISCOVERING 'LIQUID GOLD'

Doctors in South Korea and Japan pioneered the fat-based stem cell technique, using it to supposedly enhance face lifts and breast augmentation. For years, U.S. patients would travel to hospitals in Asia, Latin America and Eastern Europe — places where regulation is more lax than in the United States — to have these procedures as part of the international "stem cell tourism" trade.

Plastic surgeons in the U.S. quickly realized the financial potential of the fat they were already taking out of patients' bellies and backsides through liposuction — something that had been disposed of previously. Berman calls it "liquid gold."

Some early adopters have expanded into chains, offering doctors across the country a chance to join the franchise after buying some equipment and attending a seminar. These doctors sometimes appear on local TV news broadcasts, drumming up new business from patients and stoking interest from other doctors......."

Wow, simply amazing to me. Staggering amazing. This has to be on the FDA's radar IMO. I just don't see how this stuff can't be. What's fascinating to me- is many of the claims made by some of the "clinics" described in that AP article, almost match verbatim what I read on the U.S. Stem Cell Clinic web site- the company now partly owned by BHRT.

http://usstemcellclinic.com/

http://www.ipscell.com/2014/12/breaking-new-fda-draft-guidance-views-fat-stem-cells-as-drugs/

Quote right from that BHRT operated website:

"Is this procedure FDA approved?

No it is not; however our procedure falls under the category of physician’s practice of medicine, wherein the physician and patient are free to consider their chosen course of treatment. Our procedure is compliant within the guidelines listed in the FDA Code of Federal Regulations 21 Part 1271. We meet FDA guidelines by providing a same-day procedure done entirely in clinic with only minimal manipulation of a patient’s own cells which are then immediately delivered back to that patient."

Most recent filed BHRT 10-Q, PAGE 12:

"Investment is comprised of a 33% ownership of U.S. Stem Cell Clinic, LLC, accounted for using the equity method of accounting. The initial investment in 2014 and 2015 of cash and expenses paid on U.S. Stem Cell Clinic, LLC’s behalf was in aggregate of $54,714. The Company’s 33% income earned by U.S. Stem Cell Clinic, LLC of $3,966 for the three months ended March 31, 2015 (inception to date loss of $5,151) was recorded as other income/expense in the Company’s Statement of Operations in the appropriate periods and increased the carrying value of the investment to $49,563."

AND, same 10-Q filing, PAGE 26:

"US Stem Cell Clinic, LLC, (“SCC”), a partially owned investment of our company, is a physician run regenerative medicine / cell therapy clinic providing cellular treatments for patients afflicted with neurological, autoimmune, orthopedic and degenerative diseases. SCC is operating in compliance with the FDA 1271s which allow for same day medical procedures to be considered the practice of medicine. We isolate stem cells from bone marrow and adipose tissue and also utilize platelet rich plasma."

So BHRT seems to be making some "claim" that they're somehow operating this "clinic" and doing procedures and offering "treatments/therapies" using their stem cell "drugs" (the FDA has deemed stem cells to be "drugs" from all that I've read, including the FDA's own web site) doing this "stuff" on humans, on U.S. soil via some interpretation/reading of some FDA section of law- but not that the FDA has ever approved a single, actual "stem cell" whatever that BHRT is now doing? Wow, IMO. Pretty wild stuff to me- just what that AP/U.S. News World Report reporting/journalism article seems to be discussing from my read on it.

http://www.fda.gov/AboutFDA/Transparency/Basics/ucm194655.htm

http://www.fda.gov/ForConsumers/ConsumerUpdates/ucm286155.htm

http://www.ipscell.com/2014/12/breaking-new-fda-draft-guidance-views-fat-stem-cells-as-drugs/

http://www.nature.com/news/fda-s-claims-over-stem-cells-upheld-1.11082

WOW, IMO. Pretty fascinating stuff- this working seemingly "on the edge" of what the FDA says or deems legal on U.S. soil? Kinda Wild West to me, just like the Associated Press investigative journalism/medical writer article says IMO.

Is Bioheart really even pursuing FDA clinical trials for "heart stuff" any more? Really, are they? It sure doesn't seem like it to me, personally? It's been totally de-emphasized it seems in these most recent SEC filings, they have no money to fund any trials as they're nearly cash broke at any given time, and now all their "talk" and "PR" stuff and all- all seems to center around this "new' whatever "clinic" and "doctor training" and now "animal" stuff and all? Clinical trials- just doesn't even seem like a realistic possibility anymore to me and their trials they did have once, the FDA ones, are now going on 5 or 6 yrs old at least, just parked and going nowhere?

I'm not even sure what real business they're in anymore, that's my personal thoughts? Now some odd-ball part "clinic" operator/owner and "teaching physicians" branch or "division" or whatever and all this other "stuff" like "animals" now too - when the entire company is like 4 full time people probably, maybe 5 tops? I personally don't even get how all that's even possible then- supposedly running and managing and doing and funding all this "new stuff"- let alone, being an actual medical R&D clinical trials company like they at least sorta seemed to be trying to be, in the past?

Totally confusing to me- just makes no sense. But hey, that's just me.

It's about a 1/2 CENT stock looks like to me- that looks like the new "normal" here, so maybe I'm not the only one "not getting it" perhaps? Maybe? Who knows?

Is BHRT cash desperate or in a major (worse than normal) CASH CRUNCH?

They just filed two SEC Form 4's in which two BOD members bought shares direct from the company- which is essentially insider's buying shares-for-cash, aka sort of a Red-D or "exempt" sale I think it's called or something like that? As the insiders are are "accredited" and I guess "exempt" investors being insiders and large holders of shares. That's why they didn't buy on the open market I think- because it's actually to raise quick cash direct to the company's bank account it would seem to me?

Interesting- when one does the math on the two transactions, they equal essentially exactly $20K a piece, per the amount of shares and share count on the SEC Form 4. It's like they adjusted the share count to make the deals worth exactly $20K each.

Why would BHRT suddenly need $20K a piece from two insiders? They've sold small chunks of stock off many times- per the latest SEC filings. I believe it was in the last 10-Q they even sold like $5K worth in a "private" (company direct to buyer) transaction- in April 2015 I think it was.

Are they in a major cash pinch right now? Perhaps they needed cash so bad - that they couldn't wait for another Magna credit line draw-down to process or get another toxic lender deal inked in time to get the money needed for whatever their situation is? Why two $20K transactions, back to back, within days of each other? Fascinating IMO. They may be in a worse than normal cash crunch possibly/maybe ? (if that's even possible, given their extremely precarious cash position of $79K left against $2 MILLION in just accounts payable, per the last field 10-Q. They've been essentially cash broke for all intents and purposed (see any 10-Q or 10-K plastered with GOING CONCERN and LIQUIDITY PROBLEM WARNINGS plastered all throughout the documents) a long, long time now- just see any 10-Q or 10-K going back at least 2 yrs, but could this be even more desperate or something now- that they had to get two insiders to do a cash-for-shares quick financing deal? I'd expect the next 10-Q to list these two insider transactions as some sort "shares sold deal" and probably like being "exempt" Reg "D" deals or something (whatever they're called typically)- like in the past filings.

Guess we'll see- but the timing of it seems odd to me. Given that BHRT has already done Qty-5, FIVE toxic, floorless convertible debt deals in just Jan/Feb and then April of 2015 already (see the 10-K and the 10-Q, Daniel James, Vis Vires, KBM Worldwide, etc) - and then are also already making several major draw-downs on the Magna dilution credit line- I mean, they can't get cash coming in fast enough from those deal and need more insider cash funding too?

Not making sense to me?

http://www.sec.gov/Archives/edgar/data/1388319/000120677415001748/xslF345X03/ahn_form4.xml

http://www.sec.gov/Archives/edgar/data/1388319/000114544315000733/xslF345X03/murphy_form4.xml

And then, from the latest filed 10-Q, PAGE 24:

"Subsequent financing

On April 13, 2015, the Company entered into a Securities Purchase Agreement with Vis Vires Group, Inc. (“Vis”), for the sale of an 8% convertible note in the principal amount of $33,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on January 16, 2016. The Note is convertible into common stock, at Vis’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owed multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment.

On April 27, 2015, the Company entered into a Securities Purchase Agreement with Daniel James Management, Inc., for the sale of an 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on April 26, 2016. The Note is convertible into common stock, at Asher’s option, at a 47% discount to the lowest daily closing trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal at 150%, interest and any other amounts."

And

"Subsequent stock issuances

On April 2, 2015, the Company issued 11,508,100 shares of common stock in settlement of $213,904 of accrued payables to Guarantor of the Company’s loan agreement with Bank of America and Seaside Bank. (See Note 5).

In April 2015, the Company sold 540,736 shares of its common stock for net proceeds of $5,000. In connection with the stock sale, the Company issued 540,736 warrants to purchase the Company’s common stock for five years at $0.009247 per share. In In addition, the Company issued 6,869,151 shares of its common stock in settlement for services, provided, 22,053,009 shares of its common stock in settlement of $79,000 of outstanding convertible notes payable, and $2,739 accrued interest, 1,363,031 shares of its common stock in settlement of $12,635.29 related party interest on Northstar debt (see Note 8), 14,917,086 shares of our common stock in exchange of $79,075 draw down on the Magna equity line and on April 9, 2015, the Company issued 413,289 shares of its common stock in settlement as “true up” shares pursuant to the draw down on the equity line."

And then the most recent 10-K (end 2014) PAGE F-34/35:

"Subsequent financing

On January 7, 2015, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc. (“KBM”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on October 9, 2015. The Note is convertible into common stock, at KBM’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owing multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment.

On January 28, 2015, the Company entered into a Securities Purchase Agreement with Fourth Man, LLC., for the sale of an 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on January 27, 2016. The Note is convertible into common stock, at Asher’s option, at a 47% discount to the lowest daily closing trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal at 150%, interest and any other amounts.

On February 19, 2015, the Company entered into a Securities Purchase Agreement with Vis Vires Group, Inc. (“VIS”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on November 23, 2015. The Note is convertible into common stock, at VIS’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal, interest and any other amounts owing multiplied by (i) 140% if prepaid during the period commencing on the closing date through 179 days thereafter. After the expiration of 180 days following the date of the Note, the Company has no right of prepayment.

"

And

"Subsequent stock issuances

In January 2015, the Company issued 4,783,568 shares of its common stock in settlement for services, provided 14,299,567 shares of its common stock in settlement of $49,500 of outstanding convertible notes payable, and $2,981 accrued interest and 2,096,450 shares of its common stock for net proceeds of $16,118 from equity drawdown under the Magna Purchase Agreement.

In February 2015, the Company sold an aggregate of 1,443,656 shares of its common stock for net proceeds of $16,270. In connection with the stock sale, the Company issued an aggregate of 1,443,656 warrants to purchase the Company’s common stock for five years at $0.01127 per share. In addition, the Company issued 20,219,367 shares of its common stock in settlement of $132,500 of outstanding convertible notes payable and $2,520 accrued interest and 16,556,976 shares of its common stock for net proceeds of $135,645 from equity drawdown under the Magna Purchase Agreement.

In March 2015, the Company issued 6,185,432 shares of its common stock in settlement of $25,000 of outstanding convertible notes payable and $1,226 accrued interest. In addition, the Company issued 635,357 shares of its common stock as true up shares relating to the February 2015 equity drawdown under the Magna Purchase Agreement."

Just MIRED in a continual flow of dilution financing deals and massive, massive continual issuing of dilution common stock shares- but they're still going now to two insiders, for $20K a piece in cash-for-shares transactions? Really? They'd need $40K that bad?

That PR said Murphy paid .01 per share, which IMO is 100% in contradiction to the SEC filed Form-4 linked above- which says he paid .0077. If he did pay .01, then he's already DOWN 50% ON HIS MONEY as of today, as the stock traded at .005 and a day's low of .0046. That's a heck of a loss IMO to take in a few trading days, wow ! Even if he paid the .0077 (which I believe is the case as that's what the SEC filing says versus some "PR" thingy)- he's still down 20% or more on his money in a matter of days- given today's share price action.

Makes no sense to me; these recent Form-4 buys, insider's doing cash-to -the-company share purchases??

Oh, and wasn't the company supposedly going to "BUY BACK SHARES" anyway, LOL, according to the "buy back" PR announcement !! Whatever happened to that, LOL ! Now they got two directors needing to buy shares for likely cash infusions instead?

http://finance.yahoo.com/news/bioheart-board-directors-authorizes-repurchase-150000370.html

Again, none of it makes any sense IMO. I sure don't get it??

Quote, "Anent your dilution theory, do you have a firm $$cost total/patient to run all contemplated patients through Phase 2, both SMD and dry-AMD? Anyone?"

Well, read the $100 MILLION shelf offering prospectus. They made it 100% crystal clear they planned to USE and NEED ALL OF IT- and likely more.

Their first "down payment" attempt was a failed $62 MILLION secondary- so that should put in perspective how cash desperate and cash poor they are to fund even a single large phase II and get it even out of the parking spot it's in now.

Lincoln money- all it does is pay their very large overhead bloat and high SG&A costs. Just look at the loss from the last qtr, last filed 10-Q. $7 MILLION up in smoke-and that's mostly big salaries, a little R&D and basic overhead, nothing much else and not a DIME for any large clinical trial.

They're gonna need super dump trucks full of cash- and they DO NOT HAVE IT as of right now, that's the simple bottom line IMO.

LOL BS quote, "IMO they walked in with a suit case full of U.S. Currency and stated something to the extent of "I wanna buy X amount of shares at X amount price...CASH!""

Oh yeah, sure thing, LOL !! Happens all the time? If it was for more than $10K worth, it'd probably be illegal under numerous banking laws among other things, if not properly reported. A large cash transaction- would light up all kinds of red alerts at the various regulatory agencies. They have numerous checks and balances in place to regulate and track foreign "cash" transactions and other "things" that can be used for example for things like "money laundering" among any other number of potential "problem" areas when "cash" becomes involved.

Where did this myth based "cash and suitcase" thing take place? At a SEC registered, licensed, FINRA registered broker's firm? Really? Which one?

Not a chance IMO. Just nonsense conjecture to me. Why wouldn't this imaginary buyer just use a wire transfer or whatever- like every one else does? Why a "suitcase" and cash? What brand was the "suit case" I wonder?

Not likely.

Selling/Dumping off end of day- looking like?

It just doesn't hold gains- like Lincoln just hunts for a few new buyers, then unloads right back on um.

The stock that literally GOES NOWHERE, for 3 plus years. Pretty amazing- you know, with the myth of the "institutions buying" and blah, blah, blah, LOL !!

THAT is one fugly-ugly chart picture if you ask me. THEE definition and textbook case of DEAD MONEY and lost capital opportunity as the bull market of probably all world history blew right on by.

Iron, nope- no clue either.

The open today was bizzaro as I've seen - and this BHRT one is a real bizzaro one in all ways and forms, to say the least.

This thing put-on like 3 MILLION shares in what seemed like a blink after open and made a day's low of .0046, back in those .004's- but that huge block of shares seemed to be nowhere on the Level II? All the way to the .004's and then faster than a blink, BMAK came in on both sides and set the range back up to about .0053 Bid to .0057 Ask, where BMAK is now parked on the Ask with the "capping" block, as usual.

The dilution MM's "working this thing" are rumored to be the best of the best- mainly BMAK and CDEL who from my Google and I-HUB and other searches/research are pretty well established to be known as the trading desks or MM's of choice for Magna, Asher and a hand full of other convertible debt, toxic finance joints. That's what I've read via researching, I-HUB has a few boards dedicated just to these dilution MM's and how they "do what they do".

But this AM opening, wild stuff- I don't have a clue where that volume came from or what a OTC "pre-market" is or how it's even possible, let alone labeled as "cash"??

BMAK has the daily "cap" set right now at .0057 with the 10K share block, but they look like they're taking it down a notch as we speak. The MM's right now seem to want about .005 for the share price, unless of course someone wants to sell even $500 worth- then the Bid gets buried. If one wanted to unload/sell, say even a lousy $2K or $5K worth, I'd bet these MM's take it to the low .004's faster than one can spit. That's the "game" the deal as they have it set up right now IMO, from what I've been watching in the trading.

Wanna buy- one pays the full spread premium, mega wide spread some days. Wanna sell more than say $100 bucks worth, the dilution MM takes that Bid down like a lead boat anchor, faster than a blink, as of recent to the .005 area, even .004's range.

I think the next down leg, the next debt conversion or Magna "draw down" (which I'd guess is coming any day, any time here)- I'd guess that these MM's will make a down-leg to the .003's for sure. It's touched .004 two times now just recently on very high volumes. These dilution MM's run "tranches", these stair-step like patterns with lower highs and then lower lows from what I've seen and read about um. So I think the .003's get hit on this next leg- whenever it comes. If BHRT makes a "draw request" to Magna or if one of the dilution lenders converts a good size chunk- that IMO is the "event" that takes it down the next "tranche" or down-leg.

My .0055 cents or so worth, for what it's worth

LOL quote, "Sunny weather for the OCAT projections. Thanks Guy !!!"

More like made up MYTHS and PURE CONJECTURE and vast "projections" pulled from the thin air.

The ole "list" is pure nonsense IMO.

The company is bleeding cash and has missed big on their single greatest task- the big ole PHASE II trial and the associated mega large cash to fund it, the trial(s) in the spot marked PARKED.

Until that moves and moves in a big and very expensive way- all the other myths and vast "projections" don't amount to a hill of beans to me.

The common share price and continual need to rely on low grade Lincoln dilution "trickle" funding is 100% reflective of that reality IMO- it's 3 YEARS FLAT to DOWN for the common shares and they are trading today below where they were as OTC penny stinker shares.

Simple as that. Reality versus myth-ville and "projections" and fantasy.

RED, by golly. SOLID RED

MM's "gamed" the AM buyers on a little post long weekend hype and just took um to the proverbial cleaners.

"patents" aren't any good to a near cash broke company that can't even advance it's key phase II clinical trial(s) out of the PARKING SPOT??

File patents all day long- it's just money spent, as their cash line dwindles precariously near the RED LINE, DANGER ZONE and all they got is low grade Lincoln credit-card dilution bucks to fall back on.

What's changed? NOTHING really. Same old stall, delay, going nowhere fast IMO.

Little "PR" bites won't overcome the constant dilution selling- and NO, there's no myth of "big institutional buying", contrary to the "blog" that claims that to be the case. Not happening. Nope.

Dilution, constant dilution is the down pressure and lack of cash and lack of clinical trials advancing is their biggest overhang and problem they face.

To me, all else is noise until those issues are shown to be revealed and solved. If they need to sell/dump 10 million shares at say $4 bucks to raise the cash they desperately need to even remotely "begin" to get the phase II trial(s) out of park (very real possibility IMO, given the failed secondary when the market was much "hotter") - then that will be the new "reality" and set the price from there forward IMO.

AMAZING, 4 MILLION volume and day's LOW taken to .0046

But NONE of those shares were showing on the Level II??

The dilution MM's took it down for a brief crusher on several million shares as the other post pointed out (dumping YES, it appears, or covering?)? But none of it was even showing on the Level II Bid/Ask?

These dilution MM's are amazing, like beyond amazing.

Did they just cover a short at .0046 in the blink of an eye and now let-off a bit to open the spread back up to the .005 to .0057 range? What were those 3 million plus shares even? Where did they come from and where did they go?

Wild stuff on this one- real Wild West stuff here, OTC-ville free for all to me.

0.0053 / 0.0057 (53000 x 110000)

Look at that Bid/Ask now- but the shares already put in a day's low of .0046 on very high trading volume, almost as fast as the market opened?

Wild.

LOL, "PATENTS" schmatents- ANY PHASE II TRIAL(S) or large cash for those ole "patents"!!

Right back below $7, that didn't take long !

Filing patents while one's cash is fast dwindling to ZERO, except for probably going back to Lincoln to negotiate the next trickle-draw down "line", is a "big whoop" nothing IMO.

WHERE IS THE LARGE FUNDING and WHERE IS THE PHASE II rocking and rolling, as that's all that matters for them right now IMO.

All else it the "PR MACHINE" and just noise.

Everyday that passes w/o that Phase II starting, is just that much longer a delay that this thing sits. ACT/OCAT is notorious for delays and missed dates and taking YEARS to complete even the tiny trials they finally got under their belt to date. This one is already dragging on with delays- not a good sign to me. Every day it doesn't start, and start BIG, like fully underway and funded large- is that much longer there is a shadow of doubt as to what they really hold in their cards- is it a "fold" and a bust, or do they have a shot at something with efficacy and a remote chance at ever having an approved and salable product?

Just filed OCAT 10-Q, PAGE 13:

"Our ability to become profitable depends upon our ability to generate revenue. We do not anticipate generating revenues from product sales for the foreseeable future, if ever. "

PAGE 7:

"The Company has no therapeutic products currently available for sale and does not expect to have any therapeutic products commercially available for sale for a period of years, if at all. These factors indicate that the Company’s ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required."

PAGE 7:

"The accompanying consolidated financial statements have been prepared in conformity with GAAP which contemplate continuation of the Company as a going concern. However, as of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern. The ability to continue as a going concern is dependent upon many factors, including the Company’s ability to raise additional capital in a timely manner. The Company has no expectation of generating any meaningful revenues from our product candidates for a substantial period of time and must rely on raising funds in capital transactions to finance our research and development programs. Our future cash requirements will depend on many factors, including the pace and scope of our research and development programs, the costs involved in filing, prosecuting and enforcing patents, and other costs associated with commercializing our potential products. Accordingly, management’s plans to continue as a going concern contemplate raising additional capital including the prior execution of an agreement for a $30 million equity line in late June 2014, of which approximately $12.5 million remains available as of March 31, 2015. There can be no assurances that management can raise the necessary additional capital on favorable terms or at all. The accompanying financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern."

PAGE 24:

"We cannot assure you that public or private financing or grants will be available on acceptable terms, if at all. Several factors will affect our ability to raise additional funding, including, but not limited to, the volatility of our common stock and the broader public equity market, especially public equities issued by other pre-commercial biotechnology companies, and our ability to raise capital through non-dilutive transactions such as out-licenses. If we are unable to raise additional funds, we will be forced to either scale back our business efforts or curtail our business activities entirely. As of March 31, 2015, the Company has an accumulated deficit of $356.2 million, recurring losses from operations, and negative working capital which raise substantial doubt about the ability of the Company to continue as a going concern.

"

Most recent filed 10-K, PAGE 16:

"

Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. The timing and degree of any future capital requirements will depend on many factors, including:

"

Same 10-K, PAGE 16:

"We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

Same 10-K, PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties."

Same 10-K, PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

"

Boy, for a company with a mythological "therapy" that's PROVEN AS FACT to "just WORK" supposedly, they sure do like to plaster the GOING CONCERN WARNINGS all throughout their own SEC filings (GOING CONCERN is business speak for becoming "ill-liquid" which then leads to greatly cutting costs/spending or filing for BK)

But the myth is, that it all supposedly "JUST WORKS"??? LOL ! That OCAT is on some supposed "fast track"?? MYTH and conjecture and nothing more. The company's own SEC filings and public statement are in 100% contrast to "it just works". OCAT is fast running out of cash because NOTHING "just works" so far- and that's the reality. They're down to MONTHS worth of cash left to fund their operation and just booked another massive quarterly loss in their most recent SEC filed 10-Q and the common shares are being continually diluted and sitting near a 52 week low- in a still raging bull market.

Filing more "patents" as their trial just sits in the parking space and cash is fast dwindling to RED LINE urgency levels. "patents" shmatents- any CASH with those patents? NO? Then it's a big whoop about nothing IMO. More PR while the real issues and real "progress" goes nowhere fast- including the common share price.

AM Level II, BMAK has it "bracketed" on the Bid/Ask, both sides-

Looks like it's pretty much going nowhere then today IMO.

0.005 / 0.0056 (150000 x 100000)

BMAK has a 10K share block (what a surprise, eh !) parked on the Ask at .057 and is also on the Bid with a 10K share block at .0046

That looks like about it then- at least for now. The dilution MM's appear to want the shares right around .005, and are willing to only pay in the .004's it seems if anyone wants to sell much of a chunk, like more than $500 bucks or so worth- then the Bid gets dropped rapidly to the .004's, real fast.

Oh well- guess the big ole "REVISED" version the "PR" end of last week didn't cut it either? PR doesn't seem to do much with this one anymore from what I've observed since at least 2015 started, pretty much since they inked two large financing deals with Magna (The Josh Sason run hedge fund lender, see link below to excellent Bloomberg financial journalism piece on Sason and Manga), among the additional qty-5, FIVE other dilution/toxic, convertible debt, floorless deals they've already done in just Jan/Feb and April of 2015 already (see latest SEC 10-Q and 10-K Danial James, Vis Vires group, KBM Worldwide, Fourth Man, etc all hedge fund, convertible toxic debt dilution-for-cash shares deals all done in early 2015 already)

Looks to me like dilution, massive dilution runs the show on this one for now, maybe for good IMO. Like 50 MILLION plus shares of pure common share dilution- just in the period from the 10-K for 2014 to the 10-Q for Q-1 2015 and it's on-going, non stop. Many convertible debt deals coming due one after another, plus continual "draw downs" on the MAGNA credit line as already shown in the end of 2014 10-K and the Q-1 2015 10-Q.

My .005 cents worth or so

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

http://www.sec.gov/answers/convertibles.htm

http://en.wikipedia.org/wiki/Death_spiral_financing

"patents" and "PR" blah, blah- ANY TRIALS FUNDED, LET ALONE STARTED?

You know, the LATE PHASE II that has not been funded yet to any degree- nor has it even started, nor is it progressing along in any way, shape or form? Will 2015 be over before the "big phase II" even starts, meaning about 2017 at a minimum to even know anything meaningful, as in, knowing is this entire thing a bust or a "maybe" to move to the then much larger, much more expensive, much longer in YEARS phase III for a remote chance at an FDA approval- like 2021 on the "inside" now, as a best shot possible-maybe?

They are doing everything except their key mission which is obtain LARGE FUNDING and run a LARGE PHASE II complex, long, and expensive FDA quality clinical trial(s).

EVERYTHING else to me- is noise and smoke and mirrors and distraction, simple as that.

They're running down to near zero on the Lincoln low grade dilution credit-card, their secondary was a mass failure leaving them nowhere near enough cash to begin to remotely fund a large Phase II (let alone two of them) to completion - they are IN PARK and going nowhere fast to me.

Right now- all they have is trickle-in dilution money, that for all intents and purposes merely PAYS THE BASIC BILLS and OVERHEAD BLOAT (6 or 7 "C" level guys for a company of 36 or whatever total employees, LOL!! I'm not sure Apple, probably the largest market cap company on planet earth has that many "C" level managers?)- they merely pay their basic bills and limp along.

They release a 10-Q showing a massive $7 million quarterly loss w/o ONE DIME being spent on funding a large, phase II clinical trial- just merely paying the basic overhead and a small amount to an R&D budget, nearly all of it went to general and admin costs, aka salaries and overheard and bloat.

"PR" and "give talks" and "go to conferences" till the cows come home - IMO, the stock goes nowhere until they show how they're gonna raise meaningful capital (like $60 million in ONE CHUNK) and how much dilution and at how low a price they're gonna have to "give it up" to get that money- and then the stock will either plummet more (say they sell those shares at $4 ea, which would not surprise me in the slightest, given the failed secondary when the Bio-tech bull market of all history was raging, and has now cooled off considerably), or the common shares have a shot at moving out of being range bound and flat for THREE YEARS now, going nowhere, trend-less.

LOL quote, "we look forward to rewarding Dr. Murphy for his financial commitments through continuing increases in the value of Bioheart’s stock price."

What?

Man, are THEY FREAKING KIDDING? WHAT "continuing increases in the value of Bioheart's stock price", LOL !!!

The stock just made an all, all, all time NEW LOW of .004 (4/10th's OF ONE cent) only days ago, and the CEO talks as if the price has been, or is, or has EVER "appreciated" on his watch?

When Tomas took over as CEO in mid 2010, the share price was about .50 to .70 per share, aka 50 CENTS per share. (pull up any long term chart and see what the share price was in mid 2010)

http://www.prnewswire.com/news-releases/bioheart-announces-mike-tomas-appointed-ceo-97013034.html

Thus, during his tenure so far in 100% control of this company as it's CEO- the common shares have LOST, about 99% OR MORE of their value, NEVER have they "appreciated" in value from the 50 cent per share range at which he took over control of running the company.

.50 cents - .004 cents = 49.996 / 50 = .99992 x 100 = 99.99% TOTAL LOSS to the common shares while Tomas has been CEO.

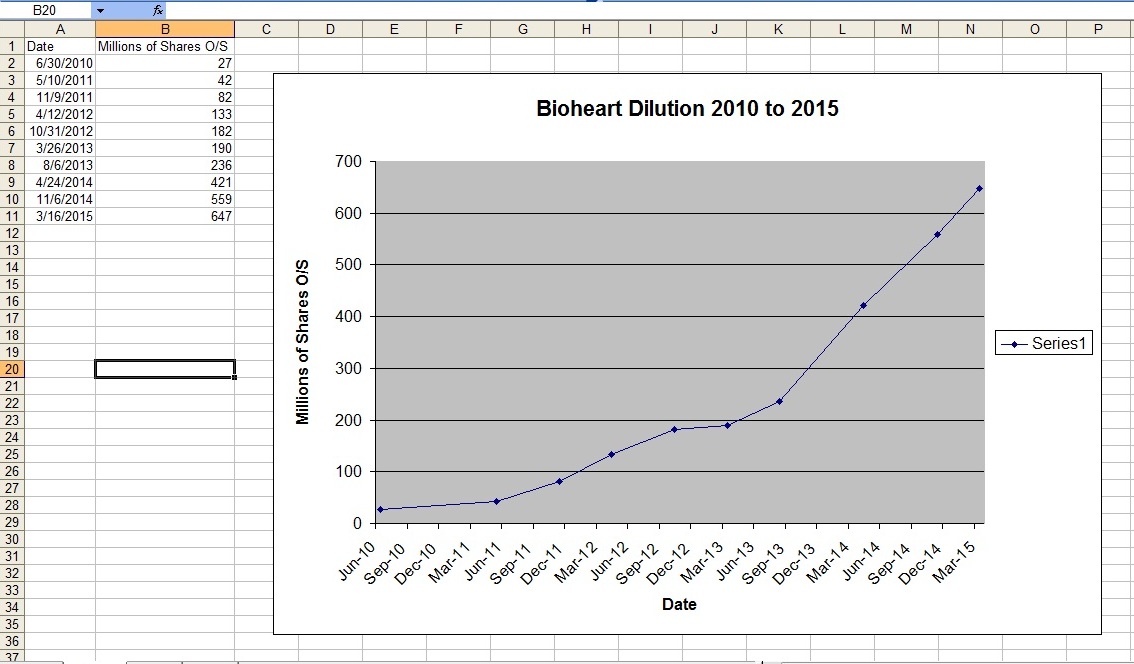

Also, there was maybe 30 million shares max O/S when he took over in 2010. Today per the last filed 10-Q, there is over 730 MILLION shares O/S- meaning massive, massive common share dilution and market cap devaluation has occurred on his watch.

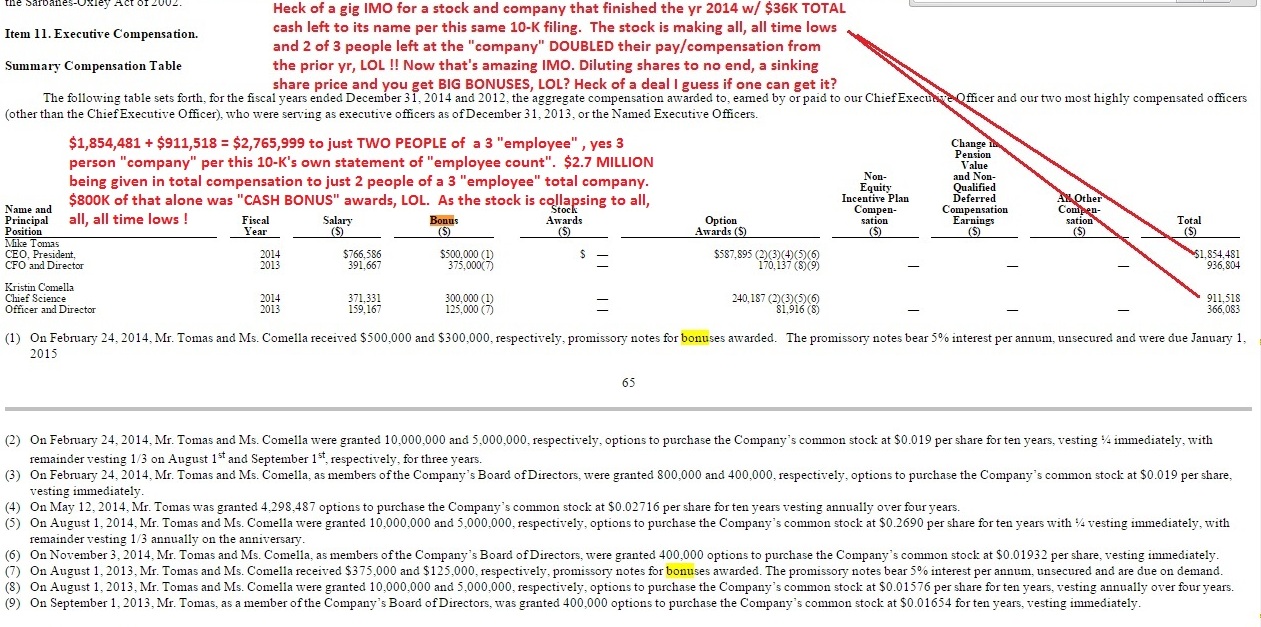

And for all that- he's for all intents and purposes, according the company's duly field SEC 10-K statements, TRIPLED his own pay package, including large "CASH" bonuses in about the past 3 yr period, a period when the stock has massively declined and hit all, all, all time LOWS.

That's page 65 of Bioheart's 2014 SEC filed 10-K. Quite amazing IMO, given the massive collapse in the price of the common shares and also the company's precariously low cash position and also continual use of toxic, floorless convertible debt deals to finance their on-going survival - qty 5, FIVE toxic financing deals being done in just Jan/Feb and April of 2015 alone already (in addition to tapping Magna continually)- See the 10-K and 10-Q (Danial James, KBM Worldwide, Vis Vires group, Fourth Man, etc)

Makes no sense to me? How can a statement in a PR be made about supposed "continually appreciating share price", LOL ??

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

As of the last 10-Q filing, it's now well over 700 MILLION shares O/S of dilution and climbing.

LOL quote, "How fast did this shareprice go to $27...? Quick? "

Well, The "share price" (shareprice) it actually NEVER went to $27 DOLLARS (the figure $27 indicates dollars per share)- as it's NEVER traded above about $7.50 dollars a share. It went public at about $5 per share (dollars) and then proceeded to lose about 99% of the common share value, reaching about 5 CENTS per share on over 3 BILLION shares of dilution- never, ever trading much above $5 dollars per share from 2005 to late 2014 when a R/S (reverse split) was done- taking the shares from the 6 CENT range, to the now approx $6 or $7 dollar range.

So, it's NEVER traded for $27 a share, ever.

A FIVE YEAR CHART- in the middle of the greatest bull market ride the world might ever see- and ACT/OCAT has literally gone DOWN to NOWHERE. DEAD MONEY as it's known "in the markets" or "on the street" and to investors in the investing world and investor's parlance.

And NOWHERE along this long and declining road that's led nowhere for all intents and purposes- did ACT/OCAT ever attract any large, non dilutive, single cash infusion investments or cash infusions or supposed "partnerships" or "JV's" or whatever, or similar. Has not happened- as money has flowed like water in the raging bull of the bio-tech explosion of probably all of world history. Nope.

Yuppers. A picture is worth a 1000 words so they say - and that chart is ONE UGLY PICTURE IMHO. Yes.

LOL LOL !! Quote, "LOL Quote in Ref. to Bluebird... It has ZERO debt ..... HUH HUH HUH OCAT has ZERO DEBT AS WELL...... HUH HUH....YUPPERS...... LOL

"

AND, OCAT IS CASH BROKE for all intents and purposes, LOL !! Really !! Yes !! Their own 10-Q says so- it's a HOOT !! $300 MILLION Bluebird COLD HARD CASH and lil ole OTC convert OCAT has the Lincoln credit card to "draw on", but ONLY in tiny, incremental "draw downs".

Most recent filed 10-K, PAGE 16:

"

Other than our arrangement with Lincoln Park, we have no sources of debt or equity capital committed for funding. Recent attempts to raise capital in the public equity markets have proven unsuccessful, and we can provide no assurance that we will be successful in any future funding effort. The timing and degree of any future capital requirements will depend on many factors, including:

"

Same 10-K, PAGE 16:

"We will require substantial additional resources to fund our operations and to develop our product candidates. If we cannot find additional capital resources, we will have difficulty in operating as a going concern and growing our business."

Same 10-K, PAGE 16:

"Our independent auditor’s report for the fiscal year ended December 31, 2014 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our current operating and capital expenses, in their report on our audited annual financial statements as of and for the year ended December 31, 2014, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties."

Same 10-K, PAGE 46:

"We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Ocata Therapeutics, Inc. and Subsidiary as of December 31, 2014, and the related consolidated statements of operations, stockholders' deficit, and cash flows for the year then ended and our report dated March 16, 2015 expressed an unqualified opinion thereon and included an emphasis of a matter paragraph relating to an uncertainty as to the Company’s ability to continue as a going concern.

/s/ BDO USA, LLP

Boston, Massachusetts

March 16, 2015"

"

Oh, now THAT IS A HOOT !! Take the latest OCAT 10-Q and count the number of times TWO VERY PARTICULAR WORDS ARE USED, "GOING CONCERN" (nice business-speak for being ill-liquid and CASH POOR, ie close to BK aka INSOLVENT aka can't pay one's bills in a timely manner when they come due as there is NO CASH arriving fast enough to match the rate at which the creditors demand to be paid and NO, it's not "boiler plate" SEC filing language, blah, blah, blah).

SEARCH HIGH and SEARCH LOW in the Bluebird Bio 10-K or 10-Q and see if the words "GOING CONCERN" ever appear- cause you know, they have $300 MILLION PLUS in cold hard cash banked, and no DEBT, LOL.

Yuppers, it's a HOOT, how many times those words GOING CONCERN appear, cause you know, cause OCAT supposedly has "no debt", LOL. They instead just have MASSIVE BILLS and enormous OVERHEAD BLOAT TO PAY but little to NO CASH at any given time, unless they can dilute and sell and dump shares hopefully fast enough to match those ole pesky bills (DEBTS) coming due. Yuppers !!

All the best, KIRK

LOL quote, "Then you don't know about Bluebird Bio and when institutions started buying it. Check it out."

Who doesn't know about Bluebird Bio???

1) It's a Nasdaq listed stock it was NEVER a straight to OTC penny stock, ever. From its beginning it was backed by a who's who of highest quality venture/risk capital investors

2) It has over $300 MILLION in cold, hard cash with ZERO debt

3) It has revenues of $25 million annual

4) They are partnered with a powerhouse CELGENE

And those are just the small points. To try and lump this in as some "case study" of institutional ownership versus OCAT, a penny stock for all intents and purposed (and a broke one at that) - is comparing apples to asparagus.

No linkage between the two at all. None.

Quote FALSE LOL, "The Biotech history, very clearly shows phase2 runs-run. OCAT had phase1 run to $27 "fact"."

NO "fact"???

OCAT "went public" via the "poor man's" way (as the company was cash broke as they've essentially always been)- via a reverse merger STRAIGHT TO THE OTC market using the guts of the TWO MOONS KACHINA DOLL COMPANY OF UTAH.

That public share price, 10 years ago in 2005 was about $5.00 per share. They have never, ever traded higher than about $5.00 per share, split adjusted. The common shares have since lost approx. 99% of their value- from $5.00 a share, to a R/S split adjusted price today of about 6 CENTS to maybe 7 CENTS. FACT.

http://www.nature.com/news/stem-cell-research-never-say-die-1.9759

The entire sorted tale of ACT/OCAT as told by the highly respected journal, "NATURE".

LOL quote, "GE HealthCare Chief Dr. Steven Minger announced to the world that he likes OCAT, preveiously ACT."

Really? Has HE PUT UP ANY BIG MONEY OF HIS OWN to finance ACT/OCAT? (non dilutive, non discounted, actual equity stake risk money?) Is he say, a 5% plus shareholder of record? Is GE a major shareholder of record- even owning so much as ONE share in OCAT?

If not, then "talk is cheap" as they say.

I "like" beer- but I've never made a large, personal risk investment in some micro brewery or whatever.

I'm sure this guy, Minger whatever, can be found "on the record" stating he finds many "companies" and "technologies" or any number of "things/stuff" as "interesting" or that he "likes them" or finds them "fascinating" or similar terms.

Big whoop. Any BIG MONEY? NO. Words and talk are free, and 100% risk free. When the guy puts a $million or more of his own money or $10's of $millions of GE's money into OCAT, then it's newsworthy to me. Else, chatter noise about nothing IMO.

Quote LOL, "Ownership of OCAT shares. From Stemvest of Icell:"

What? NO ONE KNOWS if those are "ownership" of shares or if those firms are long and holding? How? How would that be known? Most of those firms are hedge funds?

The "buy" could have been SHORT COVERING for all one knows and they might have held the stock for minutes, hours or days for all one knows?

There is no proof these firms are "long" and "holding" this stock- a filing of a Form 13 doesn't reveal that? Where and how???

Personally, I find "Icell" to be probably the number one source of wrong predictions and just plain old wrong info regarding stocks. Their track record as a little "blog" of "predictions" and what is supposedly happening or going to happen at some future date regarding companies is horrific- especially when it comes to "predicting" anything about "stem cell stocks" and especially the history of ACTC/OCAT, LOL. Just read the years and years of WRONG PREDICTIONS about ACTC/OCAT on that site (or any other stocks they cover there). The batting avg is probably zero, IMO. What have they ever predicted correctly?