News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

TMLonggun

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

http://investorintel.com/technology-metals-intel/putnam-now-on-fast-track-to-worlds-first-primary-scandium-mine/

P.S. I did not find the arguments from the "be wary" article to be very convincing, the comments at the bottom were interesting though.

Probably CLGRF will be swapped for SSRI and CRJ for SSO.

I will keep a small % of free SSO shares, the rest will go into new Claude style companies to do the junior producer multibagger run all over again.

I appreciate your posts Geo, I think it was just basically you and I here at the Claude bottom. You do such a good job I rarely feel the need to post.

Claude was great but there are lots of other great stories out there too. Buy when things look grim yet are compelling for high risk/reward. Or wait until they prove themselves (in a market that doesn't immediately care) and take the lay up.

The super easy money was already made but lots of room to run. Should be an easy 500m-1bil+ market cap in the next bull once they get running. Hope a few of you got in, I know I am a happy camper so far this year. Nothing like an instant 30+ bagger to vindicate my February conviction to buy a decent % of the company.

Take care everyone. Lots of golden opportunities hiding in plain sight!

The referenced attached report:

Now that's a "survey"!

http://www.globenewswire.com/Tracker?data=8CWllFqDjCIXyiZJ3K_JC44TO9Qniu46_bd1p4pJc8LtE4B37vclL6nrZcOgvi84eGvpuufBZbE0f6ZHyYgAioqEloVHtPuaLATqwf_fR8RpBHxEHTHLDY3lcsgN98S_ylcHJltri-83-_MOF0Aa5_GDyDfq4kkuk-eh92TkHl4=

Read the entire thing - pretty short and simple prelim report with some good pictures. Assays, more samples, drilling etc will follow up. Lots of economic minerals to go at from the surface and prove up a million ounces easily as they go along. The next few years are looking golden!

Mexus Gold US (OTCQB:MXSG) (“Mexus” or the “Company”) announced that work on the Santa Elena mine is progressing as planned. On My 24th, representatives from MarMar holdings and Mexus (JV members) held a meeting and adopted a mining plan with numerous items being discussed and agreed upon. Out of this meeting came the decision to obtain a blasting permit in the name of the JV as opposed to using a blasting contractor. The parties can control costs and manage the process more efficiently than using an outside vendor. It will take 4 to 6 weeks to obtain this blasting permit allowing time for our partner to bring in additional equipment. In the end, this property will be brought into full production faster and much larger than first anticipated.

Geologists from both companies are working at identifying and mapping additional areas of interest on the property. They’ve begun taking samples for testing shown in the attached report. Added CEO Paul Thompson, “The work being done will, I believe, help confirm Mexus’ belief that this property will produce 1,000,000 plus ounces gold equivalent. I’m extremely pleased with our JV partner (MarMar) as they have and continue to follow through with their plans for the Santa Elena. I believe that their knowledge and expertise will help make this property a major mining operation and produce outstanding returns for our shareholders.”

More Mexus pictures available on the website. (Thanks RJW/PD)

Photos added to the media gallery showing a small portion of the equipment being moved to the Santa Elena mine

05/30/2016

http://www.mexusgoldus.com/photos.php

Found under Santa Elena mine

Didn't find much on MarMar but there is a connection here somewhere. Mining is a small world.

"The mining activities at San Félix mine, are done in the claims San Félix and La Chinchi and the consolidation of the district is represented with the contracts with Mr. Marco Antonio Martínez Mora, adding the Marco and Phoenix claims with 3592.62, 4693.32 and 1498.13 has."

San Felix Report

media.globenewswire.com/cache/13013/file/21972.pdf

If he was interested in SF then Elena is a no-brainer. Not to beat a dead horse but I can't help but wonder what would have happened if SF was done with Mar instead of Atzek/SP. SF might well be an ace in the hole and another 50-50 Mar Mexus JV in the making (*some day).

Within two polarized sides the truth is often somewhere in between.

Does lode have a lot of potential? Of course, and this potential is the main reason people are here. But what most care about is that geological potential turning into a profitable mine. For the 10 years I have been here the perception is that lode has always been on the cusp of greatness, profits are always just a couple-few quarters out. Years go by and every single month that potential that shareholders love is being stolen from them via dilution. For as long as I have been here there are people who will defend lode no matter how they do, no matter much they fail, lie, or dilute. Then there are also people who bash no matter what. Both sides display a fervent religiosity that is frightening and blinds both sides to important issues.

Recent history proves that the rational course is to be skeptical, given that so much of what has been promised over the past decade did not work out favourably or as expected.

There are some compelling long arguments - history/potential of the district, value of the land, claims, and plant/equipment and the sunk capital in the property is in excess of their share price. The UG assays are VERY encouraging. If a new gold bull begins lode will do quite well. From this perspective lode looks like a good deal.

But Longs frequently ignore their biggest risk factor (aside from management) which is dilution. When I bought my first lode/gspg shares the count was at a split adjusted 5 million shares. We are now nearing ~200M for 40x dilution. Did the company value go up more than 40x as Corrado and Faber implied? Nope, we are heading towards those 07 lows.

Dilution is a fact of life for growth. As long is there is no mass dilution or toxic financing

Mexus enters into joint venture with MarMar Holdings

Mexus Gold US (OTCQB:MXSG) (“Mexus” or the “Company”) announced today that it has entered into a joint venture agreement with MarMar Holdings of Mexico at its Julio/Santa Elena property. Under the 50/50 joint venture agreement, MarMar will operate the mine and carry all costs. In addition, the company is announcing that the Julio/Santa Elena property will now be known as the Santa Elena mine.

MarMar Holdings is owned by Marco Martinez of Monterrey, Mexico. Mr. Martinez has over 40 years of experience in mining including work done at Penoles’ La Herradura open pit mine. MarMar has an extensive staff including lawyers, certified geologists, engineers, equipment operators and general labor to work the Santa Elena mine. In addition, MarMar owns equipment capable of moving up to 100,000 tons of ore a day. Certified Geologists from MarMar are already working the property and have identified additional ore bodies. The company is bringing in a blast hole drill and will do the initial shoot when ready. Initially, Mexus had planned to do a test 10,000 ton heap leach pad. This agreement changes the plan and will allow the heap leach pads and ponds to be built much larger.

Added Mexus CEO Paul Thompson, “The scale and scope that MarMar brings to this project will allow the mine to be built out much larger and much faster than we had planned. This is a great fit for Mexus and a win for our shareholders. Marco’s knowledge and experience with large mines will prove invaluable as we move forward. Between our geologist, Cesar Lemas, and MarMars’ certified geologist we’ve identified over 1,000,000 tons of mineralized material with an average value of 1.5 gram AU per ton. This material sits at the surface with an initial mining depth of 3 meters and no overburden. We know that this properties value goes much deeper than that. In addition, the certified geologists will begin a drill program that will be the basis of creating an NI 43-101. Our goal is to mirror what Penoles did just 30km south of our property and create a world class mine that will produce gold for years to come.”

http://ih.advfn.com/p.php?pid=nmona&article=71548201

Hello everyone I have been a bit busy lately so I apologize for not responding to recent messages.

As for Mexus now is a time for a celebration. Another JV that few believed was possible has now been signed, proving again the predictive merits of a common sense based approach. This JV is different than the last - production, not exploration is the focus and it should be advanced quite rapidly. The next course is to produce profitably and given what is known about the property the chance of them being able to do so is near 100% in my opinion. We have survived the difficult and risky part of the game. What's ahead? Patience and profits.

"Mexus Gold US (OTCQB:MXSG) (“Mexus” or the “Company”) announced today that it has entered into a joint venture agreement with MarMar Holdings of Mexico at its Julio/Santa Elena property. Under the 50/50 joint venture agreement, MarMar will operate the mine and carry all costs. In addition, the company is announcing that the Julio/Santa Elena property will now be known as the Santa Elena mine.

MarMar Holdings is owned by Marco Martinez of Monterrey, Mexico. Mr. Martinez has over 40 years of experience in mining including work done at Penoles’ La Herradura open pit mine. MarMar has an extensive staff including lawyers, certified geologists, engineers, equipment operators and general labor to work the Santa Elena mine. In addition, MarMar owns equipment capable of moving up to 100,000 tons of ore a day. Certified Geologists from MarMar are already working the property and have identified additional ore bodies. The company is bringing in a blast hole drill and will do the initial shoot when ready. Initially, Mexus had planned to do a test 10,000 ton heap leach pad. This agreement changes the plan and will allow the heap leach pads and ponds to be built much larger.

Added Mexus CEO Paul Thompson, “The scale and scope that MarMar brings to this project will allow the mine to be built out much larger and much faster than we had planned. This is a great fit for Mexus and a win for our shareholders. Marco’s knowledge and experience with large mines will prove invaluable as we move forward. Between our geologist, Cesar Lemas, and MarMars’ certified geologist we’ve identified over 1,000,000 tons of mineralized material with an average value of 1.5 gram AU per ton. This material sits at the surface with an initial mining depth of 3 meters and no overburden. We know that this properties value goes much deeper than that. In addition, the certified geologists will begin a drill program that will be the basis of creating an NI 43-101. Our goal is to mirror what Penoles did just 30km south of our property and create a world class mine that will produce gold for years to come.” "

Translation: We are going to be rich! I am hesitant to even do the math on 100k a day; the numbers will be so large. A 100k a day with 1g (lower than what we have) and a low recovery still is 2250 oz a day or about 750k annual. If Mexus ever produces 100-300 oz/day we will have done VERY well, let alone at many multiples of that. It doesn't matter if it imputes a $1, $5, or $25 value - it is clearly much higher than today. It will take lots of work to get there but this is highly likely to be the turning point and a low risk, high reward entry.

50% of rev or profits? Similar argument as last year. If you go back and read those posts from July I demonstrated that a low cost mine like the SE makes sense as a revenue deal, while still allowing ample profits for both sides of the partnership. Based on the wording of the PR, just like last year, leads me to believe this is a gross revenue deal. Otherwise, very simply, if we split the profits that means that Mexus has indeed paid for 50% of the production costs, which isn't what the PR says. At first pass this appears to be a MUCH better deal than the AR one but the split (50-50 instead of 80-20) and use of the word carry may imply a reimbursement and that the deal will be based on profits (and that Mar is just fronting the cash and operating costs). Either way it is still a very positive development and the SEC filing and upcoming PRs should be more clear and outline the plan going forward.

Yet after rereading the PR and rerunning some of the numbers I can only conclude that this is a 50-50 profit split and not a revenue deal.

"All mining operations will be funded by Argonaut at no cost to Mexus." 80-20

vs

"MarMar will operate the mine and carry all costs." Carrying the costs implies they will be "set down" ie reimbursed. 50-50

Does a GR deal even make sense like with the AR deal?

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=115439395

100k oz produced $1200/oz ppg 120m earnings, 50% to Mexus off the top, 60m profit, 60m to MAR - 60M (600/oz)Cost 100% to MAR - 0M profit for MAR. NOPE - This doesn't make any sense at all and only worked for the other deal because of the AR % structure.

Anyway I am very pleased with this news. Our chance of ultimate success has increased significantly.

Congrats to those that had the intelligence and confidence to add to their positions when things were at their darkest. From that darkness a new gold bull will be born and if we add that to even the low end of our Elena's capacity Mexus might very well become one of the best performing gold stocks in human history.

Well done Paul!

Old:

PEA HIGHLIGHTS:

Capital cost estimate for the Project is US$77.4 million,

Operating cost estimate for the Project is US$636/kg scandium oxide,

Oxide product volume is 35,975 kg per year,

Project Constant Dollar NPV10% is US$175 million, (NPV8% is US$217 million),

Project Constant Dollar IRR is 40.6%,

Oxide product grades of 97-99% are estimated, and

Scandium recovery estimate is 84.3%.

To the more up to date DFS:

FEASIBILITY STUDY HIGHLIGHTS:

Capital cost estimate for the Project is US$87.1 million,

Operating cost estimate for the Project is US$557/kg scandium oxide,

Oxide product volume averages 37,690 kg per year, over 20 years,

Project Constant Dollar NPV10% is US$177 million, (NPV8% is US$225 million),

Project Constant Dollar IRR is 33.1%,

Oxide product grades of 98-99.9%, as based on customer requirements,

Project resource increases by 40% to 16.9 million tonnes, grading 235ppm Sc, at a 100ppm cut-off in the measured and indicated categories, and

Project Reserve totalling 1.43 million tonnes, grading 409ppm Sc was established on part of the resource.

Looks like a very impressive project. Should be easily financed, conservative 3 year pay back on the low side of production. Super high grade reserves, about $600 million in easy pickings. 400 ppm = $800 per tonne. Scandium bonanza?

http://www.scandiummining.com/s/newsreleases.asp?ReportID=745646

George Putnam, CEO of Scandium International Mining Corp. commented:

"The Company is pleased with this very solid feasibility study result, and with the quality of the development work it represents. We now have a project plan we can execute on, and a considerably more mature development schedule on which to seek additional scandium customers. We also now have what we believe to be a financeable platform with which to engage in construction funding discussions. This accomplishment brings us a significant step closer to building the Nyngan Project and producing scandium for what we know to be numerous waiting markets."

William Harris, Chairman of EMC Metals, commented:

"Delivery of this feasibility study represents an important strategic milestone for the Company in that SCY has the first primary scandium project to complete metallurgical, engineering, and economic investigations and bring a viable feasibility study to the marketplaceSCY has the first primary scandium project to complete metallurgical, engineering, and economic investigations and bring a viable feasibility study to the marketplace, and do so in full view of both scandium investors and future customers."

"Pricing Assumptions

The price assumption in the feasibility study is US$2,000 per kilogram (kg) of scandium oxide product, as an average price covering all product sold, over various product grades. Current market pricing, such as that can be established, is substantially above these levels based on small unit quantities and varying grades. This product pricing benchmark applied in the feasibility study remains the same as was applied in the 2014 Preliminary Economic Assessment ("PEA") on this Project, and for the same reasons. In order to encourage a viable, over-subscribed and vigorous scandium market, across numerous applications, product suppliers will need to provide for adequate supply of quality product, available from trusted jurisdictions, at prices lower than product trades for today.

In addition to limited publically available price quotes for scandium oxide, the feasibility study notes two other reference points on the US$2,000/kg price assumption. The Company has an offtake agreement in place, for 7,500 kg/year (3 years), with pricing being supportive of the pricing assumption in the feasibility study. The customer is a knowledgeable alloy group, with longstanding interest in aluminum-scandium alloys. The feasibility study price assumption is also supported by a recent, independent marketing report that examines the 10 year scandium supply/demand outlook, and includes scenario-based 10 year price forecasts. The details and contents of this market outlook report will remain confidential, but select information will be included in the feasibility study. Both of these reference points support that the scandium value proposition for customers/consumers is valid at this price level."

"CONCLUSIONS AND RECOMMENDATIONS

The production assumptions in the feasibility study are backed by solid independent flow sheet test work on the planned process for scandium recovery. The report consolidates a significant amount of metallurgical test work and prior study on the Project, including important test work results completed since the PEA was generated in 2014. The entire body of work demonstrates a viable, conventional process flow sheet utilizing a continuous-system HPAL leaching process, and good metallurgical recoveries of scandium from the resource. The metallurgical assumptions are supported by various bench and pilot scale independent test work programs that are consistent with known outcomes in other laterite resources. The continuous autoclave configuration, as opposed to batch systems explored in previous flow sheets, is also a more conventional and current design choice.

The level of accuracy established in the feasibility study substantially reduces the uncertainty levels inherent in earlier studies, specifically the PEA. The greater confidence intervals around this Technical Report are achieved by reliance on significant project engineering work, a capital and operating cost estimate supported by detailed requirements and vendor pricing, plus one offtake agreement and an independent marketing assessment, both supportive of the marketing assumptions on the business.

The feasibility study delivers a positive result on the Nyngan Scandium Project, and recommends the Project owners seek finance and proceed to construction. Recommendations are made for additional immediate work, notably to win additional offtake agreements with customers, complete some optimizing flow sheet studies, and to initiate as early as possible detailed engineering required on certain long-lead capital items."

I think the tagline they use repeatedly is that they will be the largest primary scandium mine in the world, so Niocorp isn't even in the running.

Although Nio's scandium is small tonnage relative to their other ops it is a large % of their expected income. I think niobium prices have fallen a lot lately so they will hype their scandium even though it isn't correlated to their niobium geology. Just my quick BoE shows about 225m of niobium and ~200m in scandium. So that is almost 1:1 with the company's namesake.

CLQ and SCY are nearly infinitely scaleable primary scandium mines with giant, super high grade deposits at surface with low development cap ex. Nio has large capex, much lower grades, and a bunch of other hurdles to overcome so it is a matter of ease. SCY and CLQ can produce infinite scandium easily while Niocorp's scandium hopes depend on a much more complex thesis and geology. Nio might even end up the big winner depending on how successful they are at cracking the geology and mining scandium (and potentially avoiding lawsuits). How they operate in an environment of say low Nb high scandium prices would be interesting. A domestic supply for scandium in the US would be critical for defense and advanced industry and there is more than enough demand for all the first movers to produce until their hearts are content. In twenty years there will probably be operating scandium mines on most continents, but like with any mineral the highest grade deposits in the best areas will be exploited first.

Nio might even be able to bill themselves as a zero/low cost producer which is always a huge marketing boon. If scandium pays for the niobium or vice versa. I don't know how this story will end and who will be crowned the ultimate victor but the future is definitely bright for those first few companies to produce at a profit and supply a long sought after commodity to the market.

Argonaut gets rid of another premium development property for a pittance:

"TORONTO, ONTARIO--(Marketwired - Jan. 18, 2016) - Minera Alamos Inc. (TSX VENTURE:MAI) (the "Company" or "Minera Alamos") today announced that it has entered into a binding Letter of Intent (the "Binding LOI") with Argonaut Gold Inc. ("Argonaut") and its wholly owned subsidiary Durango Fern Mines S.A. de C.V. to acquire 100% of the mineral claims known as the La Fortuna Gold Project located in Durango Mexico ("La Fortuna").

"La Fortuna clearly fits our corporate growth objectives to consolidate high margin, late development stage projects with manageable capital requirements", said Chris Frostad, Minera Alamos' CEO. "This project also adds positive new gold exposure in support of our Los Verdes copper project. We look forward to providing further updates regarding our plans in the coming weeks".

"In the past ten years our current technical team has been responsible for the successful development of three similar gold projects in Mexico and Central America through to commercial production", said Darren Koningen, President at Minera Alamos. "I am confident that we can rapidly accomplish the same at La Fortuna".

Highlights:

Potential for One of Highest Grade Open Pit Gold Heap Leach Projects in the World: The current La Fortuna near surface resource grade is approximately 2 g/t gold with additional silver credits, presently excluded from the resource calculations;

Established Resource with Additional Upside Potential: Measured plus Indicated Mineral Resource of 4.8 million tonnes grading 2.0 g/t gold and containing 308,100 gold ounces (see chart below). The identified gold-silver mineralization at the La Fortuna deposit remains open at depth and along strike;

Regional Exploration Potential: Several other mineralized areas have already been identified and demonstrated via surface sampling to be gold-bearing. These provide immediate drill targets for the definition of additional gold resources;

Accelerated Path to Production: Minera Alamos will be initiating the permitting process immediately upon closing of the transaction along with the completion of a technical report outlining the path to production. It is expected that a construction decision, if deemed appropriate by management of Minera Alamos, can be made later this year (2016);

Platform for Further Consolidation: The La Fortuna Gold Project represents the first phase of what Minera Alamos intends to be a growing profile of late stage development opportunities in Mexico and the Americas.

Pursuant to the terms of the binding LOI, the Company will pay the vendor USD $750,000 on closing. An additional USD $250,000 will be paid 9 months after the closing and USD $1,000,000 will be paid upon the announcement of a construction decision. The vendor is also entitled to a 2.5% net smelter returns royalty subject to a maximum amount of USD $4,500,000. The closing of the transaction is subject to regulatory approval.

La Fortuna Resources:

Measured Category Indicated Category Measured & Indicated

Cutoff

Grade Au g/t Tonnes (000) Au g/t Tonnes (000) Au g/t Tonnes (000) Au g/t Au Oz.(000)

0.8 1,322 3.332 2,681 1.731 4,003 2.260 290.8

0.5 1,538 2.956 3,287 1.533 4,824 1.986 308.1

Notes:

Resources are as reported in the NI 43-101 compliant Technical Report titled "La Fortuna Project, Durango, Mexico, Updated Technical Report for Castle Gold" by Toren K. Olson, P.Geo. and dated November 21, 2008.

Based on a total of 127 drill holes comprising 19,400 metres, including 121 original holes (18,885 metres) plus 6 twin holes comprising 515 meters

Assays normally included silver as well as gold. However, in some cases silver values were not available and as a result of the inconsistency of this sampling resources of silver were not calculated.

To the best of knowledge, information and belief of Minera Alamos, there is no new material scientific or technical information that would make the disclosure of the mineral resources set out in the foregoing Technical Report inaccurate or misleading.

Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. There is no certainty that all of any part of the Mineral Resources will be converted into Mineral Reserves.

La Fortuna Project

The La Fortuna Gold Project includes the historic La Fortuna mine together with the surrounding concessions, totaling 994 hectares. The property is located in the northwestern corner of the State of Durango, Mexico, about 70 kilometers northeast of the city of Culiacan, Sinaloa.

Initial development of La Fortuna followed the 1884 discovery of the gold-bearing oxidized outcrop. Between 1886 and 1892 a 200 TPD gravity mill was built near the site to process the ore which was selectively mined underground. Reportedly, about 200,000 tonnes of material, grading 20 g/t was mined and processed during this period. In 1987 an 80 tonne per day flotation mill was installed in order to process the sulfide ore, operating intermittently until 1990. Reportedly, 20,000 tonnes were mined from underground and processed.

Between 1991 and 2008 numerous exploration surveys were performed which included detailed mapping and sampling of the underground workings and the drilling in the immediate La Fortuna Mine area. These programs culminated in the development of a resource block model which produced a Measured and Indicated resource of 4,800,000 tonnes at 2.0 g/t gold (308,000 contained ounces) at a 0.50 g/t gold cut-off grade as set forth above.

About Minera Alamos

Minera Alamos is a junior exploration and development company. Its flagship project is the Los Verdes open pit copper-molybdenum project in Sonora, Mexico that is currently in development."

The most cyclical industry in the world making the same mistakes over and over again like clockwork. Invest in quality during the bear and prosper in the bull or follow the herd off the buffalo jump.

Safe to say AR is out of the running (IMO) given their recent decisions and PRs. Time for someone with more vision and greed to step up.

Thanks 8!

To be clear a 10,000 t heap with a pilot test plant is not a 10k/day operation (it is 10k total) but given what we know it will be easily scale-able to the long talked about 6k/day to probably multiples of that eventually. (For an open pit mine 6k/day is pretty small.) If they prove a high recovery rate it will be expanded and the other known high grade zones can feed it at 6 or 10 or 20k a day for a year or two without getting into an insane drill program.

8 do you really think they can get 90% recovery off their heap? Thanks for keeping us appraised and correcting us when needed. Give the teacher a golden apple.

I'd multiply those numbers by .6 or .65 to get actual recovery.

"The pilot plant will start with a 10,000 ton heap leach pad. The initial expectation is 1 to 2 grams per ton Au based on our existing resource from the outcropping quartz vein system. This system had been previously sampled and was recently tested by more aggressive and encouraging geochemical follow up. The resource is near surface, economically valuable ore, with open depth potential and holds bonanza Au grades. All exploration data is being evaluated and processed to proceed with the production of a modeled economic volume of ore related to the low angle shear zone structures. These structures dominate the property and are the main bulk mining ore targets in the area."

10k at 2gr should put us around 130-150k/oz/year recovered ounces (if the pilot proves successful). Even if it only produces 6k at 1gr with low operating days and recovery this should still put us at a very profitable 40k/year or so.

If Mexus accomplishes something like this, even in a bear market, our market cap will be many, many multiples of where we sit. If a baby 6k/day operation is likely to make us wealthy and get us to 6 figures then a 10k at 2g is getting close to 200k/oz a year production and it is easy to develop with a very high IRR compared to most operating mines on this planet.

Someone will want a piece of this. Apparently at least five companies do, with more looking over the fence. Exercise some patience though, as Rick Rule would say that which is inevitable is not necessarily imminent. A deal will come and this property will be mined but it won't necessarily happen overnight. Negotiations, then contracts, then construction, and then mining.

"Cesar believes that we can have our mine operational in 45 days once we flip the switch."

I assume this means that 45 days after construction and commissioning it will take about 45 days for the first pregnant solution to flow to the plant. MC, electrowinning, carbon? Who knows, let the experts decide.

"Mexus has at least a couple years of production. A mine like my big winner Claude has had a couple years of production for 20 years. We need more drilling but finding more of the same is highly likely. We have more than enough for the short-medium term and if we mine that funding exploration for more ore for the long term shouldn't be a problem.

This alone is all we need to start:

"4,000,000 tons of ore with an average gold grade of 2.5 grams with three times as much in Silver."

4M/6k = 666 days of production

333 days = 160 771 oz even 60% recovery is still 96463 oz a year easy peasy. 100k should be the low end of a baby leach. A decent size might yield 500k a year, some of these nearby similar open pit operations do 100k t a day to our likely 6k startup. 20 x 100k for a full size op is 2million ounces produced annually. Is that likely? I don't know, probably not. At the very least it would take years of work and hundreds of millions to get there. It is possible though and all we need is the 100k baby operation to become wealthy just like GORO. 100-300k is a pretty realistic goalpost once they have been mining for a couple years. If we get even close to that we will all be wealthy.

This isn't even counting the best asset, the HG Julio underground.

Some of the neighbours are definitely watching but not all are in position to take advantage of what they see. Someone will eventually... too much gold in plain sight to ignore in the long term. "

And there is 31.1 grams (or grammes) in a Troy ounce.

There is a lot of complicated variables going on here Gene and I doubt anyone can grasp them all. There is part of this that is very logical: a speculative thesis based on the high grades of the mine, confirmed by assays, qualified geos, and casual visitors to the site. It is logical for a mining company to pursue a JV because of the operational merits of the project.

I just don't get it that a mine this rich would have such difficulties going into production, finding a strong partner, falling to a market cap of like $600 000. That does not make any sense...it just seems very illogical.

AR was here and they left. There should be a looooong line of suitors better than they ever were.

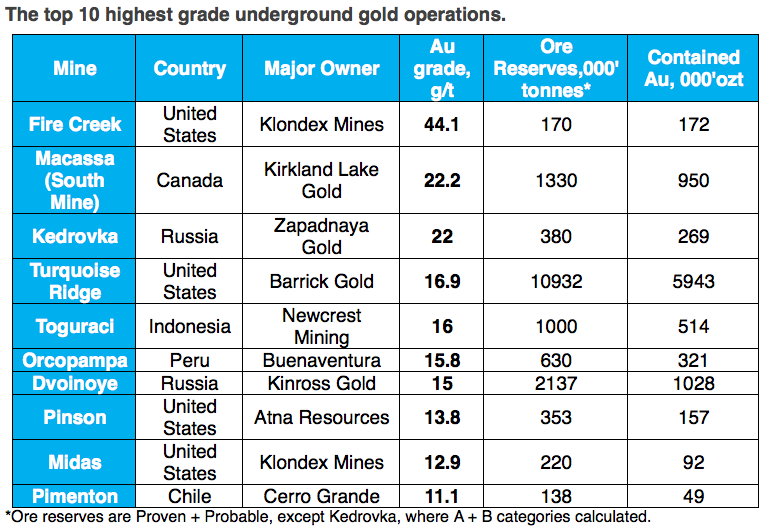

An underground mine needs higher grades than an open pit to be economic. Most of the best gold deposits on earth that were near surface bonanzas with obvious signs were mined out over the past 400 years. Those were the easy pickings. Deposits of that nature are rare in stable countries in the 21st century.

There are historic bonanzas (Comstock, Gold Rush etc) with higher grades and small pockets of minerals that are higher grade (Rubicon hit over 1000 oz/t but it was under a lake and deep with narrow widths) and loads of other examples but right now in 2016 Mexus is the highest grade development property I know of. (Obviously I am not aware of every gold mine in existence). The article I linked states that Klondex is the highest grade ug gold op with 44 g/t, the 2nd place half that and the tonnages are quite small. Mexus has no reserves but we are ahead of that or at the very least in the same ballpark. Do your own DD and draw your own conclusions.

"Santa Elena/Julio Property

Mexus’ Julio/Santa Elena property is located 54 kilometers NW of Caborca, Sonora, Mexico just West of Mexico Highway 2. This fully permitted project consists of several mining concessions totaling approximately 1340 hectares.

The Santa Elena/Julio area is dominated by a series of fissure white quartz veins where 6 important systems have been recognized. Three or four low angle shear zones are also present with important prospects in them and notable higher gold grades as bonanza pockets. The fissure quartz veins have an average width of 2.1 meters. The quartz is massive and mostly fractured, and often brecciated due to multiple pulses during deposition.

The Julio Vein extends more than 800 meters before it buries and is known for high bonanza grades which includes the underground mining site on the property and is estimated at 415,000 tons on the surface with a minimum of 5 grams per ton. There are also four shear zones recognized in the area. Shear Zone 1 is coincident with the Julio Vein and had a sample graded at 11.5 grams. Shear Zone 2 is 400 meters to the south east and parallel to the vein system 1 through 5. Shear Zone 3 contains a bonanza pocket which had sample results as high as 19 grams was graded at an average of 5.5 grams from assayed sample results. Shear Zone 4 presently contains some pits, adits and shafts and graded 2 grams from eight samples. The 6 major vein structures identified in the area south of the Julio shaft account for nearly 4,000,000 tons of ore with an average gold grade of 2.5 grams with three times as much in Silver.

The company believes, using its current drilling studies along with historical data of the Julio, that 1 ounce of gold per ton is obtainable. Past history shows that the Julio produced 2 ounces per ton gold average. "Mexus has seen assays as high as 6 ounces per ton. In addition, there is visible gold and we would expect the assays in those areas to be even higher," said CEO Paul Thompson.

The underground shaft is currently 100 feet deep with 100 feet of drift. Past assays show gold up to 6 ounces per ton. [And Ken pulled out up to 20oz/t) anecdotally]

The quartz vein is from 3' to 13' in width. Sampling from the exposed areas have assayed from .5 oz to 6 oz per ton. Mine Superintendent, Diego Guillermo Baltazar Garcia, has worked the Julio shaft in the past and believes Mexus can average 2 oz of gold per ton. The initial daily goal will be to mine 25 tons at a daily cost of $1600."

Compare that with a sub 1 gram industry average for open pit and somewhere around a 5-7 gram UG average (and the previous examples) in a rapidly depleting industry and I think we are in good shape; will average at least .75-1.5 oz/t and that puts us in 1st place - or there abouts. Even using .25 still puts us well into the top quartile and that is all that matters. It doesn't matter if we are 1st or 29th in the world. The Julio compares to bonanzas of old and we control it in the 21st century with gold above a thousand dollars. We are definitely among the highest grade development properties in the world and out of all of the juniors I follow Mexus is in first place for grade. Grade is king. This is why we will succeed and why there will be a JV... eventually.

The REAL Highest Grade Underground Mine in the World

Is Mexus among the highest grade gold mines on Earth?

Keep in mind these are reserves... but still. Our resources (probably around the indicated level) are at the minimum 3x the supposedly highest grade mine in the world. The purpose of reserves is to prove they are economic through drilling, testing, and production. Mexus does not have to do this because the variables are simple (no/low strip, super high grade, very near surface, oxide, etc.) meaning that these minerals would be economic nearly anywhere on the planet except Antarctica or the bottom of the ocean.

http://www.mining.com/the-worlds-highest-grade-gold-mines/

I think I am comfortable saying that Mexus is one of the top 10 highest grade mine discoveries in the entire world.

If a mining company is mining gold in Mexico they should care about Mexus especially in this sort of environment:

The discipline is called "speculating," very different from both gambling and investing. Big mining houses will be interested in our project because that's what they do, mine and develop projects inferior to ours at a profit. Big mutual funds are obviously not interested in a penny stock, they tend to invest on net income and other investing metrics which we don't possess. When/if we do they will come, take much less risk, and pay way more for their shares.

For those wanting to post negative opinions about Mexus you are welcome to do so just leave the personal attacks out of it and stick to messages with content. One sentence replies saying someone is wrong does very little to convince people of why.

Mexus has a few flaws and they are pretty obvious but that doesn't outweigh the potential of the company or the deposit just sitting there.

That said, good post Belgie:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=121312366

Let's just keep it real, and celebrate when it happens. It could still take a while, as the Argonaut deal took a lot longer and a lot more negotiation to complete.

It depends on whatever deal we ultimately get, its terms, how quickly it comes, and how quickly it advances a timeline to production. If we stay in limbo and gold turns down again (for hopefully the last time before it resumes its climb) then Mexus will go down as will the probability of a good deal. The opposite is true, if gold in both pesos and dollars goes up while we wait a stronger deal should be more likely.

But that is all out of our (and PT's) hands. One thing is certain though, that even at $1200 - or substantially less - Mexus makes sense as a JV/ development candidate because of the high operational margins their deposit represents to a potential suitor or partner.

I am bullish on quality juniors and miners in general. Hard to speak in specifics until we have some but I will say this: If Mexus starts mining gold at a profit its share price will be multiples of where it currently is.

Perhaps there are some more clues to the AR question many people keep asking. Did they leave because Mexus has no gold? Or is there a more likely explanation as I (and others) have suggested? Here's AR's CEO:

"Pete Dougherty, President and CEO of Argonaut Gold stated, “I am proud of what the team has accomplished. We had a record year of production as a Company. We met our production guidance for the year, even with lower grades than planned at El Castillo. At La Colorada, throughput and production exceeded expectations. We were able to increase cash on the balance sheet in the second half of the year and were only slightly down year-over-year, even after the $20 million final payment to complete the purchase of the San Agustin project. We expect to make a construction decision on this project in the latter part of 2016. We were able to negotiate key contracts and streamline the business to allow us to plan for fully loaded costs (including operating, capital, taxes and corporate administrative costs) to be less than $1,000 per ounce for 2016. This gives us tremendous leverage to a rise in gold price. Our share price did not perform as we would have liked during 2015, but with positive cash flow generation and almost no debt, we are well positioned to meet our 2016 goals and reach valuation parity with our peers.

With regards to our development projects, we are striving to ensure that all three of our development projects are shovel ready. We recently released the results of the updated PFS for the Magino project and the results make this project stand out as one of the top undeveloped gold assets in North America from a payback, IRR and NPV perspective. We are exploring ways to unlock the value of this project through responsible financing options. We submitted permit applications for the San Agustin project and have developed plans to link the project with El Castillo’s infrastructure, thereby reducing the upfront capital and improving the cost structure. We expect to make a construction decision on this project in 2016. At San Antonio, we continue to be highly active in engaging both the local communities and key officials at federal, state and local levels to create the conditions necessary to move the project forward. We are excited about the opportunities for the Company in 2016, and will continue to execute upon our commitments, to preserve our balance sheet and protect our shareholders’ investments until market conditions merit advancing the projects.”"

http://www.argonautgold.com/news_events/news/index.php?&content_id=210

Note the last sentence - not the call to create shareholder value through expansion and exploration like most miners but to preserve cash and protect (limit downside) for their shareholders. That's from the horse's mouth and he isn't playing hockey. Pretty much ends that debate (I hope)... especially if you read between the lines a little bit.

So once and for all did AR leave because Mexus is a played out scam with no gold? No, they left to develop internal properties, reduce risk (from their POV) and conserve cash until more favourable market conditions arise. If anyone wants more information call Argonaut and ask.

I bet there were a couple red faces from facepalming at Fresnillo HQ when they saw the AR deal last year. Second chances don't always come around. For them it would pittance to develop and low risk. A fair deal and we will prosper. If it is indeed a new gold bull we will prosper even more!

Why is this time different?

I guess I shouldn't have sold all my shares at .004 to shop at the gap?

More high grade assays:

LUGC15-032: 0.429 opt Au (14.72 g/t) and 1.217 opt Ag (41.73 g/t) over 37 ft. (11.3 m).

Includes 1.116 opt Au (38.26 g/t) and 2.496 opt Ag (85.55 g/t) over 7 ft. (2.1 m).

Includes 0.668 opt Au (22.88 g/t) and 1.141 opt Ag (39.13 g/t) over 8 ft. (2.4 m).

LUGC16-043: 0.384 opt Au (13.17 g/t) and 0.858 opt Ag (29.41 g/t) over 20 ft. (6.0 m).

Includes 0.473 opt Au (16.22 g/t) and 0.865 opt Ag (29.65 g/t) over 15 ft. (4.5 m).

LUGC16-047: 0.894 opt Au (30.65 g/t) and 0.280 opt Ag (9.60 g/t) over 3 ft. (0.9 m)

LUGC16-048: 0.321 opt Au (10.99 g/t) and 11.55 opt Ag (395.95 g/t) over 5 ft. (1.5 m)

Includes 0.404 opt Au (13.85 g/t) and 17.700 opt Ag (606.79 g/t) over 2.5 ft. (0.8 m)

LUGC16-048: 0.346 opt Au (11.85 g/t) and 0.737 opt Ag (25.28 g/t) over 17.5 ft. (5.3 m).

Includes 0.352 opt Au (12.07 g/t) and 0.623 opt Ag (21.34 g/t) over 10 ft. (3.0 m).

Includes 0.640 opt Au (21.94 g/t) and 0.666 opt Ag (22.81 g/t) over 2.5 ft. (0.8 m).

LUGC16-049: 0.716 opt Au (24.56 g/t) and 1.003 opt Ag (34.4 g/t) over 10 ft. (3.0 m).

http://www.comstockmining.com/news/press-releases

This quote was pretty funny too.

“We’re not going to pick the ore body up and take it somewhere else. It’s there whether we like it or not..." -John DeCooman Silver Standard’s vice president of business development and strategy.

LoL you don't say? Notwithstanding the fact that the purpose of mining is to extract the metals from an ore body and then take them somewhere else, haha.

I think that is a typo in the 3rd article. This requires 66.66% to pass. A lot can happen between now and mid May.

I agree Skanderbeg's quote there is odd. He will probably argue that the combined company will be stronger and extremely undervalued and much better able to expand and explore Claude's properties, unlocking "the true value of the company" or some such. It might even be true. SSRI also has a lot of production, contributing over 300k to Claude's 75, from this angle we have gained. These deals are hard to value, so many metrics like jurisdiction and deposit potential are difficult to pin down.

SSRI will probably be in a position to pay a dividend in short order if the deal goes through.

Timothy J. Stabosz 6,628,570 3.39%

US Global Investors, Inc. (Asset Management) 5,550,000 2.84%

PCJ Investment Counsel Ltd. 4,137,200 2.12%

Dimensional Fund Advisors LP 3,652,890 1.87%

Ruffer LLP 2,672,500 1.37%

Mackenzie Financial Corp. 2,200,000 1.13%

Hillsdale Investment Management, Inc. 1,872,200 0.96%

BMO Asset Management, Inc. 1,850,000 0.95%

Mawer Investment Management Ltd. 1,800,000 0.92%

Leleux Associated Brokers SA 1,200,000 0.61%

A revolt is more than possible. Who owns all the shares? We do. Even if this current deal falls through and no other bids emerge it has raised our profile and awareness and we will be fine in the long run.

Why did SCY go up 41%? I see no news. We are getting close to some progress PRs, which should support us. I was very surprised we pulled back as far as we did. These (upcoming) PRs shouldn't have much effect since they are known about a year in advance but the same thing has happened a few times over the years. This stock has such low visibility and a small s-base that the PRs tend to make the price rise more than I would normally expect. 11 cents for this company at this stage of development is madness of the highest order.

DFS with awesome economics coming, along with a positive EIS and more off-take agreements. Anyone selling for less than high 20s or 30s has not been paying attention to the scandium story.

Saskatchewan’s only gold mining company is the target of a friendly takeover bid by a larger precious metals extraction company based in British Columbia.

Silver Standard Resources Inc. has offered to acquire Claude Resources Inc. for the equivalent of $1.65 per share, representing a “strong” valuation of $337 million. The deal represents a 30 per cent premium on the Saskatoon-based gold mining company’s March 4 closing price of $1.27 per share, and would leave its shareholders with a 32 per cent stake in the combined company.

“In the end, this is a very good and beneficial transaction for Claude’s shareholders and I think it reflects well on the province,” Claude Resources president and CEO Brian Skanderbeg said Monday morning.

“Silver Standard recognizes Saskatchewan as a place they want to do business, and recognizes the opportunity (in the province).”

Claude Resources has discussed takeovers with several interested parties, and began “strategic discussions” with Silver Standard about six months ago, Skanderbeg said. The Vancouver-based company offers the twin benefits of “scale and liquidity,” meaning Claude Resources will be able to overcome challenges imposed by its “relatively small balance sheet,” he added.

“Now, if we have a relatively aggressive growth path and want to take Claude forward, it’s more effective and efficient to do it from a larger platform with a stronger balance sheet … That’s one of the key wins for Claude, is participation in a larger platform,” Skanderbeg said.

Founded in 1980, Claude Resources owns and operates the Seabee Gold Operation, located about 125 kilometres northeast of La Ronge. It consists of two producing mines: the Seabee Gold Mine and the Santoy Mine Complex. In 2015, the company produced a record 75,748 ounces of gold.

Silver Standard, which is headquartered in Vancouver, operates mines in Argentina and the United States, and is developing new operations in Argentina, Peru and Mexico. The company reported revenues of $375.3 million in 2015, and hopes its acquisition of Claude Resources and its Saskatchewan assets will add another dimension to its business.

“We’re not going to pick the ore body up and take it somewhere else. It’s there whether we like it or not, and we certainly like it. We have no issues with it,” said John DeCooman, Silver Standard’s vice president of business development and strategy.

DeCooman said Silver Standard would like to ramp up the mining rates at Claude Resources’ Saskatchewan mines, and the company’s history with open pit mining means it will need talent to do that. He added that combining Canada’s geopolitical climate and “good hard-working people” with capital and added knowledge “usually leads to a lot of opportunities.”

The deal has been approved by both companies’ boards of directors, but still needs to be ratified by 62.66 per cent of Claude Resources’ shareholders. Skanderbeg said the company plans to call a shareholders’ meeting in mid-May, and that he doesn’t foresee much opposition.

The takeover will result in Saskatchewan losing its only gold mining company. Skanderbeg conceded that it’s a “trade-off” when an outside company buys a local one, but said Silver Standard is committed to investing in the Seabee Gold Operation, which began operations in 1991 and has recently “turned the corner” in terms of production.

“I do think this is a net benefit to the province overall, in the sense that you have a stronger and more well financed platform to invest in the province,” he said.

http://thestarphoenix.com/business/local-business/b-c-mining-company-eyeing-acquisition-of-claude-resources-in-friendly-takeover

My other post got deleted in Ihub's weird technical difficulties this morning but the gist of it was that I will be voting no for this deal. I don't think anything under a new all time high, let alone under $2, is fair. Delaying and refusing at this point is much more likely to help us than hinder, although I have seen both happen before. Even on hostile deals (GG and Osisko for example) there is potential for increased offers from other suitors, especially once they know the window to acquire is closing. Claude will be worth 50-100% more if they just wait a year but I guess that is probably true of the combined company as well, although I'd like Claude to be solo and mature for a couple more years. Claude has been mining for decades and they are only just now getting into their groove. Either independent or as SSRI they still have an awesome property and some great assets that I want to own a piece of.

Still outperforming all the Canadian gold analysts I know of. In 2008 I made one massive purchase at .28 sold in 2011 for 2.50 then repurchased late 2014 at .22 after they turned around their operations. $1.60 makes it about a 20x in about 8 years (4 of holding). All publicly called. Compared to 0 percent rates I've done did pretty well and managed to ignore the nonsense of most of the "professionals".

Mexus will have its turn. As a non-producer it is higher risk than CRJ (you can wait for ops to begin if you want a lay up) but an explorer transitioning to a profitable producer should make CRJ's 20x look like a pittance. The wealth creating power of a good junior miner plus a little common sense for entry and exits is profound. We are at one such entry with MXSG. This story will be turned around; it is far too compelling not to.

Stay tuned. $600k in 2016 and 150M by 2018? Anything is possible as long as they start production and produce even a fraction of what is expected.

We have the gold. It will be mined. Economic minerals almost always get extracted and cyclical bear markets always reverse...eventually. Successfully speculating in these stocks is an exercise in discipline and patience. Bet on what is both inevitable and ignored and then be patient and prosper.

Take care everyone.

Full text with highlights:

SILVER STANDARD TO ACQUIRE CLAUDE RESOURCES

VANCOUVER, B.C. -- Silver Standard Resources Inc. (NASDAQ: SSRI) (TSX: SSO) ("Silver Standard") and Claude Resources Inc. (TSX: CRJ) ("Claude Resources") are pleased to announce that they have entered into a definitive agreement (the "Agreement") whereby Silver Standard will acquire all of the outstanding common shares of Claude Resources pursuant to a plan of arrangement (the "Transaction") to create a high-quality intermediate precious metals producer with assets in the Americas.

Under the terms of the Agreement, all of the Claude Resources issued and outstanding common shares will be exchanged on the basis of 0.185 of a Silver Standard common share and C$0.0001in cash per Claude Resources share, representing total consideration of C$1.65 per share of Claude Resources based on the value of Silver Standard's common shares as of the close of business on March 4, 2016. This implies an equity valuation of C$337 million for Claude Resources. The consideration represents a premium of approximately 25% based on the 20-day volume weighted average prices of Silver Standard and Claude Resources and 30% to Claude Resources' closing price of C$1.27 per common share on March 4, 2016. Upon completion of the Transaction, existing Silver Standard and Claude Resources shareholders will own approximately 68% and 32% of the combined company, respectively.

Transaction Highlights

§ Establishes a high-quality intermediate precious metals producer: Combines high-margin precious metals operations with scale and financial strength in attractive mineral belts and political regions.

§ Significant pro forma mining company: In 2016, the combined company is expected to produce approximately 390,000 gold equivalent ounces at cash costs of approximately $735 per equivalent ounce of gold sold 1.

§ Immediately strengthens financial position: Increased free cash flow generation, enhanced credit quality, and improved financial flexibility with combined cash and marketable securities of $330 million as at December 31, 2015.

§ Combines complementary technical skills: Brings safe underground and open pit mining skills together to realize portfolio growth and exploration opportunities.

§ Well positioned to pursue growth: Accelerate exploration of the +19,000 hectare Seabee property while continuing to explore Marigold in Nevada and Pirquitas/Chinchillas properties in Argentina, as well as continuing our disciplined approach to reviewing external project and production opportunities.

Paul Benson, President and CEO of Silver Standard said, "The addition of the Santoy and Seabee mine complexes to our operating portfolio demonstrates our disciplined acquisition strategy to deliver growth and value to our shareholders. Through this transaction we are adding a third high quality, strong cash flowing operation located in Canada, one of the best places in the world to operate mines. We also acquire a large underexplored land position with significant exploration upside. With financial synergies and our strong balance sheet, the combined company is well positioned to maximize value from our assets and pursue further growth opportunities."

Brian Skanderbeg, President and CEO of Claude Resources said, "This transaction provides our shareholders with meaningful ownership of an emerging Americas focused mid-tier precious metals producer. Our long-term production profile, free cash flow, strong balance sheet and significant exploration potential are a great addition to Silver Standard's portfolio of producing mines and development projects and we are excited that we can share in the growth opportunities that exist going forward. "

Benefits to Silver Standard Shareholders

§ Immediate positive free cash flow from high-margin mining operation.

§ Results in production growth with minimal capital investment and a cash flow accretive transaction.

§ Establishes an operating presence in Canada, providing further geopolitical diversification.

§ Adds underground mining capabilities to our core operating strengths.

§ Provides strong Mineral Resources to Mineral Reserves conversion opportunity.

§ Discovery potential with a large, underexplored land package underpinned by active drill programs.

§ Enhances corporate credit quality, further strengthening our balance sheet.

§ Income tax and G&A synergies with the addition of a Canadian mining operation.

Benefits to Claude Resources Shareholders

§ Results in an immediate premium of 25% based on Silver Standard and Claude Resources' 20-day volume weighted average prices on March 4, 2016.

§ Immediate premium of 30% to Claude Resources' closing price of C$1.27 per common share on March 4, 2016.

§ Provides exposure to Silver Standard's diversified project portfolio.

§ Significantly enhances financial strength and free cash flow generation.

§ Provides equity participation for exposure to future value creation and growth.

§ Increases trading liquidity and capital markets exposure.

§ Presents financial and tax synergies only realized through the combination.

§ Maintains exposure to Claude Resources' operating and exploration portfolio.

Transaction Conditions and Timing

Under the terms of the Agreement, the Transaction will be carried out by way of a court approved plan of arrangement and will require the approval of at least 66 2/3% of the votes cast by the shareholders of Claude Resources at a special meeting. The issuance of shares by Silver Standard under the Agreement is subject to the approval of the majority of votes cast by the Silver Standard shareholders at a special meeting.

Completion of the Transaction is subject to regulatory approvals and other customary closing conditions. The Transaction includes customary deal-protection provisions, including non-solicitation of alternative transactions, a right to match superior proposals and a C$12 million reciprocal termination fee payable under certain circumstances.

Full details of the Transaction will be included in the management information circulars of both Silver Standard and Claude Resources to be mailed to their respective shareholders by mid-April 2016. The special shareholder meetings of both companies are expected to be held in mid-May 2016. Upon completion of the Transaction, one Claude Resources Director will be appointed to the Board of Directors of Silver Standard.

Board of Directors' Recommendations

Both companies' Boards of Directors have determined that the Transaction is in the best interests of their respective shareholders based on, among other factors, the benefits set forth above. Each company's Board of Directors has unanimously approved the Transaction and will provide a written recommendation that its respective shareholders vote in favor of the Transaction in the management information circulars to be mailed to their respective shareholders in connection with the Transaction.

Each of the directors and senior officers of Silver Standard and Claude Resources have entered into an agreement to vote in favor of the Transaction at the special meetings of Silver Standard and Claude Resources shareholders, respectively.

Macquarie Capital Markets Canada Ltd. has provided a fairness opinion to the Board of Directors of Silver Standard. National Bank Financial Inc. and Canaccord Genuity Corp. have provided fairness opinions to the Board of Directors of Claude Resources.

So what is the combined SSRI-Claude worth? I don't know much about SSRI, so I will have to look into them to decide whether to hold or sell and redeploy when the dust settles.

Hopefully we trade above the buyout price, signalling a larger premium or perhaps a bidding war with additional suitors. Not ideal to be bought out at the bottom of the market but if the combined company is strong and lean it will probably be an excellent investment for the next gold bull. Either way we are in a great position.

"Mr. Winfield has the sole voting and disposition power over the shares of Common Stock directly owned by him. As Chairman, President and CEO of InterGroup, Santa Fe and Portsmouth, and sole manager of NC, Mr. Winfield can be deemed to have shared power with those entities to direct the voting and disposition of the shares of Common Stock owned by such entities. Thus, Mr. Winfield may be deemed to beneficially own 46,960,467 shares of Common Stock for purposes of Section 13D of the Exchange Act, or approximately 29.0% of the voting power of the Common Stock of the Issuer."

Less than I thought. His recent sales are a pittance. The only odd thing was the donation, now PRed here:

"VIRGINIA CITY, NV (March 7, 2016) - The Comstock Foundation for History and Culture (the "Foundation"), a recognized 501(c)(3) non-profit organization, today announced that it has received its first donation through a transfer of 100,000 shares of Comstock Mining Inc. common stock from Mr. John Winfield. Less than one year ago, Mr. Winfield pledged his support to the Foundation, committing 1,000,000 common shares over the next decade toward the preservation of these precious historic and cultural resources. The donations will contribute directly to the Foundation’s efforts to advance the preservation of historic and cultural resources within the Comstock Historic District."

Winfield with common stock is a good thing, puts us all in the same boat. Positive PR from the donation... other than that no comment. Time to celebrate Claude. As soon as lode starts making profits its turnaround story can/will be very similar.

Canadia-based precious metals producer Silver Standard Resources Inc. (SSO.TO, SSRI) Monday said it has agreed to acquire Claude Resources Inc. (CRJ.TO)(CLGRF.OB).

The common shares of Claude Resources will be exchanged on the basis of 0.185 of a Silver Standard common share and C$0.0001 in cash per Claude Resources share, representing total consideration of C$1.65 per share of Claude Resources based on the value of Silver Standard's common shares as of the close of business on March 4. This implies an equity valuation of C$337 million for Claude Resources.

The consideration represents a premium of approximately 25 percent based on the 20-day volume weighted average prices of Silver Standard and Claude Resources and 30 percent to Claude Resources' closing price of C$1.27 per common share on March 4.

In 2016, the combined company is expected to produce approximately 390,000 gold equivalent ounces at cash costs of approximately $735 per equivalent ounce of gold sold.

Under the terms of the Agreement, the transaction will be carried out by way of a court approved plan of arrangement and will require the approval of at least 66 2/3 percent of the votes cast by the shareholders of Claude Resources at a special meeting.

One Claude Resources Director will be appointed to the Board of Directors of Silver Standard on completion of the deal.

Macquarie Capital Markets Canada Ltd. is acting as financial advisor and Lawson Lundell LLP is acting as legal counsel to Silver Standard and its Board of Directors.

National Bank Financial Inc. is acting as financial advisor and Blake, Cassels & Graydon LLP is acting as legal counsel to Claude Resources and its Board of Directors.

Read more: http://www.nasdaq.com/article/silver-standard-resources-to-acquire-claude-resources-20160307-00200#ixzz42E1jWJ6M

Kind of disappointing but hard to knock a huge success. Congratulations everyone.

No one is going to plop down millions to start up a mine unless they are sure the ppg will stay high.

After my buddies and me beat down this stock by selling off, she will be ripe to buy back.

I may not own MXSG, but at least I'm not a commie!

[Mexus isn't being accumulated but pazoo is (as MXSG is being accumulated]

They're giving out stock like candy!

MXSG is a good investment.

How many ounces MXSG pullin out of the ground a day?

Anyone?

Anyone?

Anyone?

zzzzzzzzzzzzz...

In reality, again, reality, the company is broke and there is a reason why Argonaut walked away from this hole in the ground.

If there was money to be made here, they would have made it.

You are feeding on your own feeding frenzy, and the bottom will fall out.

You're welcome but my insight as you call it is just borrowed from others.

Everything I have learned has come from men like Don Phillips, McEwen, Rule, etc and a whole bunch of reading, observation, and personal experience. I can't even write - my teachers taught me that.

Over the years there has been lots of false starts, cryptic information, and hard to decipher geologic reports in addition to all the signals from management etc and without 8 this place would be a ghost-town. I just try and be objective and rearrange the information. I know I was not impressed with Mexus at all when I first looked at it (the cable salvage days). But times change and properties change hands, while opportunities come and go. If this venture succeeds PT and DP, along with Mexus' employees, deserve all the credit.

Sometimes this board confuses even me. Who is Tom? Am I Tom? Am I Don's son? Who knows? Decoder ring activate!

Take care everyone.

I see lots of newcomers lately and was asked to repost some DD. Please familiarize yourself with the ibox. The Mexus speculative thesis is easy to see but only if you have all the pieces.

Here's some old (but still relevant posts):

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=116279947

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=92736888

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=103085965

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=116137064

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=115160046

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=115152092

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=111271400

2015 Julio Report https://www.dropbox.com/s/bbriq1pwkphf23x/JULIOREPORT.pdf?dl=0

On this board some good posters that are worth reading are Belgie, 8, KansasCrude, and rickybobby among others. There is lots of info out there, you're just limited by the amount of reading and effort you want to put in and the capital you want to risk.

Is Mexus an insane bargain or a money pit? Time, as always, will be the final arbiter.

Very impressive assays. We all knew that the Comstock wasn't played out! High grade and long length will add up to some serious ounces - and these should be economic especially with high silver grades to help pay for production costs. Seeing an ounce per tonne is exciting compared to lode's average and cutoff.

Finding gold isn't good enough these days. We have to find economic gold like this current discovery and keep expanding. A high margin deposit like this is worth a fortune compared to what they currently have.

That is not conservative at all. In what world do you live that mining an ounce of gold (or anything for that matter) has no production costs whatsoever? Where in the history of mankind has a mine been valued in such a manner?

At best you can divide the total estimated profit per ounce by the total a/s plus a bit of dilution added for good measure.

Right now lode still loses money on every ounce. So taking $0 divided by 162M = 0.

"Hey I have a deposit worth four billion and it will only take slightly more than that to extract so please give me four billion."

Good look selling that.

With higher gold prices and lower inputs they might begin to eek out a small operational profit.

3,200,000 x $100 = 320 000 000 or under $2/share

But they can only mine 40k or so which is only $4M a year profit that will be obliterated by the rest of the development and overhead.

The UG looks promising but so did the open pit. Even if they do mine the UG at a profit it will still be a long time until all the money spent to get there is paid off.

Lode's current value estimate/opinion:

potential- nebulous, opinion, no value.

net income x10- none

Real estate- ~50M

small % of their highest grade ore that can be produced at a profit-10-20M

plant and equipment- ~40M

claims- 5-10M

Captial raised and spent- ~100M+

Market cap:80M

Lode very well may be undervalued, but not for the reasons you mention. Lode has been on the cusp of turning around for what seems like ages. When/if it does the price will rise significantly to reflect eps and the growing capacity for more of same. This is probably a low risk, high reward entry but hyping the gross value of a deposit is pointless unless it represents significant margin and lode has demonstrated the opposite thus far.

he's got a wealth of knowledge here based on my readings