News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Biobonic

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

and over 2.3 billion barrels of recoverable resource in those horizons that have flowed oil, and Alkaid #2 could add to these estimates

Random note: Flowing at 100,000 barrels a day it would take 63 years to recover the 2.3 Billion barrels

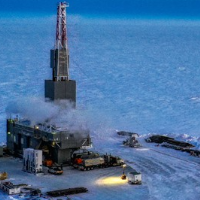

Feb 15 Theta Update

Theta West #1 - Total depth reached. Planning to flow test.

Pantheon confirms that Theta West #1 has reached total depth ("TD") at 8,450 feet having drilled through both the Upper Basin Floor Fan ("UBFF") and Lower Basin Floor Fan ("LBFF") target horizons, which are Brookian age, and having encountered approximately 1,160 gross feet of hydrocarbon bearing reservoir across both horizons combined. Data received so far indicates the reservoir quality is superior to Talitha #A, with high quality light oil encountered across the entire section. The Company is now preparing to set casing prior to flow testing within both horizons over the coming weeks.

The UBFF was encountered between 6,800 and 7,000 feet, and the LBFF was encountered between 7,450 feet and 8,410 feet depth. The top of the UBFF is located approximately 150 feet higher than pre-drill estimates. Well bore conditions in the shallower sections above the primary objective, combined with the extremely cold weather, have prevented the Company from conducting wireline operations in the open hole. However, the Company undertook Logging While Drilling ("LWD") operations which included resistivity, gamma ray, neutron density, formation density along with gas chromatography readings during drilling which has provided excellent quality data, indicating the presence of hydrocarbons in the targeted horizons some 1,500 feet structurally higher (updip) from the Talitha #A well, 10.5 miles to the southeast. Samples analysed to date by AHS/Baker Hughes, which have been contracted to undertake Volatiles Analyses ("VAS"), has also confirmed the presence of light oil within the UBFF and the top portion of the LBFF, consistent with the LWD data. AHS/Baker Hughes is yet to complete analysis of the lower portion of the LBFF.

"Billion-barrel oil fields don't come along every day. There have been very, very few ever discovered in the United States," Jamison said.

Pantheon and their shareholders could be sitting on a 12+ BILLION Barrel field.

Theta West #1 Operational Update Feb 15, 2022

Press release

Theta West #1 - Total depth reached. Planning to flow test.

Pantheon confirms that Theta West #1 has reached total depth ("TD") at 8,450 feet having drilled through both the Upper Basin Floor Fan ("UBFF") and Lower Basin Floor Fan ("LBFF") target horizons, which are Brookian age, and having encountered approximately 1,160 gross feet of hydrocarbon bearing reservoir across both horizons combined. Data received so far indicates the reservoir quality is superior to Talitha #A, with high quality light oil encountered across the entire section. The Company is now preparing to set casing prior to flow testing within both horizons over the coming weeks.

The UBFF was encountered between 6,800 and 7,000 feet, and the LBFF was encountered between 7,450 feet and 8,410 feet depth. The top of the UBFF is located approximately 150 feet higher than pre-drill estimates. Well bore conditions in the shallower sections above the primary objective, combined with the extremely cold weather, have prevented the Company from conducting wireline operations in the open hole. However, the Company undertook Logging While Drilling ("LWD") operations which included resistivity, gamma ray, neutron density, formation density along with gas chromatography readings during drilling which has provided excellent quality data, indicating the presence of hydrocarbons in the targeted horizons some 1,500 feet structurally higher (updip) from the Talitha #A well, 10.5 miles to the southeast. Samples analysed to date by AHS/Baker Hughes, which have been contracted to undertake Volatiles Analyses ("VAS"), has also confirmed the presence of light oil within the UBFF and the top portion of the LBFF, consistent with the LWD data. AHS/Baker Hughes is yet to complete analysis of the lower portion of the LBFF.

Geologist's Alaska Gamble Could Turn Into America's Next Big Shale Play

Bit of history, Great Bear Petroleum getting the asset. Story written in 2013

He shocked the industry in 2010 when he scooped up 500,000 acres of Alaska state land leases

Wish we had a Letter to Shareholders

An important aspect of receiving an FDA approval is the ability to manufacture the 'new drug' in an FDA approved manner.

Supply line backups experienced world-wide and over extended timelines has surely slowed the completion of the expansion.

On October 22, 2021, CEL-SCI announced it completed the commercial scale expansion of its dedicated current Good Manufacturing Practice (cGMP) facility in which it manufactures its immunotherapy Multikine® (Leukocyte Interleukin, Injection)*. The construction, which began in 2020, was designed to ensure it will be compliant with all requirements of the U.S. Food and Drug Administration’s (FDA) and European cGMP regulations as the facility’s production capacity has been doubled to meet anticipated market demand for Multikine once it receives regulatory approval.

The issue with providing estimated timelines is the SP decimation when it's not met.

The issue with not providing estimated timelines is the SP decimation due the 'supposed' uncertainty.

Do it once, do it right, takes time.

A rushed BLA that gets CRL'd and it's another 12-18 months added to get another shot.

Not talking about 40 somethings in the top suite.

They don't have time to rush the process.

Hold no position at present.

Here is the sticky portion of this approval process

There is one standard of care that the world follows for advanced primary head and neck cancer.

That standard of care is in the NCCN guidelines. Those are the guidelines that tell physicians what they should be administering. First treatment is recommended to be surgery and then after surgery, the doctor will decide whether to give you either radiation or radiation and chemo at the same time. We showed great benefit for those getting surgery and radiation.”

And today transaction for 3,032 put contracts with $5 strike for Jan 2022 expiry was executed.

This is what Susquehanna investment group, Simplex trading and others have been known to do.

Not claiming it was Susquehanna...

Whalewisdom

Scroll to page 6.

Kenny Nolan had a big hit song titled 'I Like Dreamin' back in 1977

Another poster has cut and paste the transcript that details what you thought you had dreamed.

Yes, it's true the staff at Cel Sci have crafted a procedure for determining who can receive Multikine prior to surgery.

Questions:

Is this a modification of SOC?

If so, what kind of approval would this modification need from the FDA?

What would the approval consist of? A clinical trial?

Does the staff have the medical expertise to tell members of the American Head and Neck Society how to change their approach?

Submit the BLA, all their trial results and when do they tell the FDA, oh by the way this will work if it's determined prior to surgery whether or not the patient will need chemotherapy.

FDA - from our understanding, the need for chemo versus just radiotherapy has been determined after the surgery. That is when the medical professionals can determine the extent of the invasion of the cancer. But your drug needs to be administered prior to surgery, and how do you determine, prior to surgery that chemo will or will not be a part of the SOC?

Do you have any trial results to back up this 'new' procedure that varies the SOC?

Just saying, it's not a slam dunk.

Is the FDA just supposed to approve an unproven change to SOC?

Current state of affairs from a blighted perspective

Trial results effective, but determining who is eligible for just radiotherapy is traditionally determined after surgery. Multikine needs to be administered as soon as NHSCC is diagnosed.

Not only does BLA need to be written to back up the improvement, they need to definitely spell out a new procedure for determining who can receive Multikine prior to surgery.

Short position rose from 8.9 to 9.7 million in the last reporting period.

They are not quietly liquidating their position.

Shorts are a well heeled group with Stat 'News' in their corner, and $$ millions at their disposal.

CVM's defense has been tweets and a well meant website.

Shorts feed on fear. And there is plenty of opportunity for fear, as the FDA approval process is shrouded.

This story isn't over, not by a long shot.

Will the BLA get accepted? Will the new procedure be convincing, convincing enough for the FDA to say Yes?

Will Stat News keep to the facts? LOL

Link to Article

From my perch, currently on the sidelines

Looks like a mis-priced Put option with August expiry.

Today's Blue light special is the $7.50 Put Option with August expiry selling for 30 - 35 cents.

A successful Sell Order will bring $30 - $35 into the account with the obligation to take shares at $7.50 if the SP falls below $7.50 and the owner of the Put wants to exercise his option.

With Put option cost 30 - 35 cents a share, Put owner only makes out if SP falls below $7.15 - $7.20.

Only two and half weeks until expiry, wonder if there's gonna be some downward SP pressure?

Appears that someone's enticing Put Option purchases...

Considering the low on the debacle day was $7.08...

Give it a try, biotechs as you know are rife with failures.

Those that short biotechs actually have a thesis that works as they have backtested it.

Predicting small cap cancer drug failure

A lot of reasons, some in the design of the trial itself, would tilt the odds in favor or failure. Small shop, limited views - meaning what got missed that will come out to bite in the readout.

CVM almost did but Dr. Talor saved the day by bringing up the idea to separate the radiotherapy group from the rad-chemo group in data gathering. (This was detailed in the Scientific presentation but not presented much in the general presentation.)

I recall Celsion in 2013 had a data readout - great idea - failed to meet significance. They didn't specify how long to administer the treatment. How does one miss that? But they did.

The shorters, for years could count on CVM to raise funds. Toxic with warrants. They got so sure of this they started to short before the annual money raise. In 2018, as the share price rose, enough warrants were exercised that the money raise wasn't needed. SP kept rising and warrants were never part of the share offering again.

So it's kinda become personal. On both sides.

What I am actually stating is the need to enroll in a remedial reading course.

Clearly the most recent presentation states the 76 are not in the OS data.

Therefore my interpretation of how ITT is understood needs refreshing.

Intention-to-treat analysis is a method for analyzing results in a prospective randomized study where all participants who are randomized are included in the statistical analysis and analyzed according to the group they were originally assigned, regardless of what treatment (if any) they received.

Would appear the 76 have been counted in the statistical analysis.

This method allows the investigator (or consumer of the medical literature) to draw accurate (unbiased) conclusions regarding the effectiveness of an intervention. This method preserves the benefits of randomization, which cannot be assumed when using other methods of analysis.

Source

From the recent Shareholder letter

Analysis methods are robust: Statistical significance was reached for the pre-specified log rank test (primary analysis) in the key intent to treat (ITT) population and supported by other populations in the study

The trial focused on a limited segment of HNSCC, the Oral Cavity.

There are segments of HNSCC that have radiation as the primary eradication approach.

ASTRO, the premier radiation oncology society in the world, 2018 Update on Radiation Treatment for Head/Neck Cancer

The total of trial participants that were administered Multikine is approx 533. We aren't told what arm the 76 that had surgery but refused any additional treatment came from. This is Stage III and IVa HNSCC, surgery alone is almost Never the prescribed treatment plan.

One could estimate that at least 2/3rds of the 76 came from the Multikine arm. That would be around 51 people, or 10% of those receiving Multikine that decided Multikine and surgery were sufficient.

Another point is these patients were Not in the radiotherapy only arm for the 14.1% increase, effectively handicapping the Multikine arm.

Something powerful was going on in the trial.

Team of Doctors detailed Guide for HNSCC patients

Well, how about that. A trial that missed it's primary endpoint.

Question?!?!

Where is the clamoring for the RESULTS?

The OS for the final readout was not provided in the PR.

The P value was not provided in the PR.

The HR was not provided in the PR.

Where is the outrage over these omissions?

Oh, only Cel Sci needs to provide those - which is totally beyond protocol.

When and how will BMY provide that data?

The company will complete a full evaluation of the data and work with investigators to share the results with the scientific community

How many other cancers will this therapy apply to in the end.

Indeed the Billion dollar question.

In 2010s Merck spend Billions in trials for Keytruda.

From a Forbes article:

stories of Permultter’s emphasis on Keytruda abound. According to one scientist, Perlmutter reportedly said, “I don’t want to wake up in five years and wish I blew another $1 billion on this drug.” Former Merck executive Reicin recalls presenting Perlmutter with a prioritized list of potential Keytruda clinical studies and asking him, based on resources, where to draw the line. “There is no line,” Perlmutter reportedly responded. “Do them all.”

This study is being done to investigate the safety, tolerability and anti-tumor activity of pembrolizumab (MK-3475) in participants with

advanced triple negative breast cancer (TNBC) (Cohort A),

advanced head and neck cancer (Cohorts B and B2),

advanced urothelial cancer (Cohort C),

advanced gastric cancer (Cohort D).

Additionally, for Cohort D, data is presented for Asian Pacific (AP) participants.

Only participants with programmed cell death-ligand 1 (PD-L1) expressing tumors were enrolled in Cohorts A, B, C and D. Participants in Cohort B2 were enrolled irrespective of PD-L1 status

Here are the shares traded totals for Jun 28, 29, 30

06/30/2021---- 15,253,170

06/29/2021------ 6,685,524

06/28/2021---- 16,245,060

Over 35 million changing hands and less than 2 million shorts covered.

Can give over 8.5 million reasons the SP might not elevate by a significant degree in the short term.

But as Clarice sang in the Rudolph story:

There's always tomorrow. For dreams to come true.

Sidelines at current. Do see it as a decent trading vehicle, just I'm not good at that.

From my perspective, which is not medically trained or schooled, what Multikine does is far superior to the 2nd line and 3rd line treatments. That said, when people are facing the end, any meds that can grant more days amongst the living can ask a very high price.

Some meds have an administer schedule of 400 mg every six weeks. (Think Keytruda) How much money does that bring in!!

Multikine got one 3 week shot, and in spite of the radiotherapy benefit, the improvement for those who also had Multikine is astounding.

Question to ask is, how did Keytruda get so many indications so quickly?

Merck bet the farm on Keytruda when they realized what it could do.

Forbes has a good article on the history: The Startling History Behind Merck's New Cancer Blockbuster.

Cel Sci didn't have the money to do what Merck did.

Will someone pick this up? IMO, someone should - it's proven.

That is the small window.

Significant percent of stage I and II indications are treated with just radiotherapy, no surgery. Bang!

What if they have discovered some biomarkers that are prevalent in determining effectiveness? Or even better, it can work across the spectrum.

Sure hope so, but being prudent would mean waiting on FDA nod.

A basic primer on Keytruda and why this is important to Cel Sci.

Merck, with Keytruda had discovered that it worked in tumors where PD-L1 overexpression is found.

In their first trials they included only patients that had this overexpression in their tumors.

In the early 2010s BMS was bigger than Merck. But Merck was able to show good results from their early Keytruda trials.

catapulting Merck ahead of BMS when the BMS drug failed in first-line therapy for lung cancer among less stringently selected patients,

while Merck succeeded brilliantly by focusing on the 30% of patients deemed most likely to respond.

On August 5, 2016, the U. S. Food and Drug Administration granted accelerated approval to pembrolizumab...The approval was based on demonstration of a durable objective response rate (ORR) in a subgroup of patients in an international, multicenter, non-randomized, open-label, multi-cohort study...This subgroup included 174 patients...The range for duration of response was 2.4 months to 27.7 months (response ongoing). Among the 28 responding patients, 23 (82%) had responses of 6 months or longer.

85% of responses lasted ≥6 months. Overall survival at 12 months was 38%.

In reflection, trial results are monumental, not only does Multikine provide lasting benefits to the radiotherapy group, the trial reveals the devastation to the immune system caused by chemotherapy. Well done sir, well done indeed

If they actually lived by that, they would never recommend chemotherapy.

For the first time ever, researchers looked at the numbers of cancer patients who died within 30 days of starting chemotherapy, which indicates that the medication is the cause of death, rather than cancer itself. The study, published in The Lancet Oncology, showed that chemotherapy treatments kill up to 50% of cancer patients in some hospitals (2).

In 2015, Prof. Holly Prigerson, along with 11 co-authors, published an important paper on the topic. They concluded that chemo given to improve symptoms actually worsened the quality of life (QOL) of many of those who received it. Patients who had a good performance status sickened. And those who already had a poor to moderate performance status did not improve. In fact, sometimes the chemo that was meant to give them relief killed them off sooner.

News Blackout

Prigerson is a professor at Weil Cornell Medical College and Harvard Medical School, and her co-authors are all professors at Columbia, Yale, Duke, Michigan, etc. Her report in JAMA Oncology created a bit of a stir in medical circles. To date, it has been referenced 200+ times in other journal articles (an indication of its impact).

Mossreport

More details

Swallowing exercises: A guide for patients with head and neck cancer

Oh, really?

This leaflet is for patients who have treatment for head and neck cancer and who are experiencing swallowing difficulties. It gives some rehabilitation exercises to help with eating and drinking. Exercises should only be used by the individual named below and under guidance from your Speech and Language Therapist.

Why do I need to do swallowing exercises?

Radiotherapy to the head and neck can cause both short and long-term difficulties with swallowing; this is known as dysphagia. Dysphagia can make it difficult to eat, drink and take your medication and you may be at risk of food, fluids or saliva ‘going down the wrong way’. If this happens it can result in choking and/or chest infections known as ‘aspiration pneumonia’.

There is the $64,000 question.

Kinda revealing my age range with that phrase!, lol

Have seen the large Pharmas get a BLA into the FDA's hands in three to four months from Phase 3 results.

I reviewed some small shop biotechs and found them taking 6 months or so, to get the BLA into the FDA. But that is a small sample size. (Too many LTFUs, LOL mikedel)

FDA granted Orphan Drug designation to Multkine.

Once the FDA 'accepts' or "receives" the BLA application:

Sponsors of an orphan drug can make use of expedited Food and Drug Administration (FDA) programs such as the Fast Track, Breakthrough Therapy, and Priority Review designations, as well as the Accelerated Approval pathway and unique grant funding opportunities, such as the Orphan Products Clinical Trials Grant program.

One of my earlier successes in biotech investing was buying Relmada in the single digits. When they announced their stellar Phase 2 results the share price skyrocketed.

Symbol RLMD - and therefore I use the moniker relmania on ST.

I will send you a msg on that platform.

Right from the FDA website

FDA undersize approval

On August 5, 2016, the U. S. Food and Drug Administration granted accelerated approval to pembrolizumab (KEYTRUDA injection, Merck Sharp & Dohme Corp.) for the treatment of patients with recurrent or metastatic head and neck squamous cell carcinoma (HNSCC) with disease progression on or after platinum-containing chemotherapy.

The approval was based on demonstration of a durable objective response rate (ORR) in a subgroup of patients in an international, multicenter, non-randomized, open-label, multi-cohort study. This subgroup included 174 patients with recurrent or metastatic HNSCC who had disease progression on or after platinum-containing chemotherapy. Patients received intravenous pembrolizumab 10 mg/kg every 2 weeks or 200 mg every 3 weeks.

Distant metastatic disease occurs in ~15% of HNSCC patients after initial definitive management.1,2,3 Patients can present in various states from a single site of metastasis and controlled local disease to widely disseminated metastases with or without local recurrence.

The biggest Pharmas in the world cherry pick

Merck and Bristol Myers Squibb developing the immunotherapies.

Merck–in effort to close what it perceived as a four- or five-year gap with BMS–opted to pursue a companion diagnostic program for the use of pembro in lung cancer patients, a decision intensely questioned not only by investors, but also by the new Merck research leadership when they joined in 2013. In the end, the companion diagnostic program was retained, and while critiqued by the Wall Street Journal as recently as March 2016, it ultimately proved to be vital, catapulting Merck ahead of BMS when the BMS drug failed in first-line therapy for lung cancer among less stringently selected patients, while Merck succeeded brilliantly by focusing on the 30% of patients deemed most likely to respond.

There are no near term catalysts, (m2011W) with shorts and algos controlling the share price movement it appears that downward is the overall trend.

The share price was moved to $6 and change on a rumor in early 2020.

Could see that level again. With funds selling before the quarter ended, new funds bought? Or are there greater percent of retail holders? Shorts with the FUD approach will have field day for months.

BLA submitted then a two month window until one finds out if the BLA application is accepted. Holding shares thru that period is fraught with danger and anxiety. Then the mid-cycle meetings and the potential for a late cycle pre-CRL letter. Or just a CRL at the end.

Shorts are busy here, on this board.

GK has waged war with the shorts and really come out on the losing end, even with good data. On another front, unless he has rock solid understanding of what shorts do and what the fails-to-deliver report really says, he shouldn't post inaccurate tweets. IMO.

He is the face of Cel Sci, today it doesn't appear elevated.

GK has been put on the defensive, clearly overwhelmed by the noise about data mining. That, being on the defensive, almost never is translated positively in share price.

I currently hold zero shares. It was a fascinating two years for me. Certainly not as profitable as I had hoped.

What should Cel Sci do now? My opinion

Hire a world class BLA application expert - announce it far and wide.

Two years ago, GK seemed a Rock Star. Get some R & R. Reset the focus on the drug, its benefits and focus like a laser on nothing else. He has charisma, a leadership style. He is not an in the trench type. Bring competent, in the trench, guys on board and let the world know, the processes going forward are in good capable hands.

Hire world class immunotherapy experts, announce the process has begun to review data for biomarkers in order to determine application in other cancer tumors.

Focus on the future success of the benefits of Multikine and all this noise today will become a distant fading memory a year from now.

Most knowledgeable people understand that.

Know exactly what you mean.

It does seem that some posters disengage their brains before posting.

when the FDA requires 900+.

Don't tell Merck - most of their Keytruda trials are under powered.

The new study involved 305 patients, who were randomly assigned to either pembrolizumab at 200 mg dose every 3 weeks for up to 35 cycles (n = 154) or platinum-based chemotherapy (n = 151). The primary end point was PFS, with OS as the secondary end point.

The median time from randomization to data cut-off was 59.9 months, and the final data cutoff was June 1, 2020. Patients in the pembrolizumab group received treatment for a median of 7.9 months and those in the chemotherapy group received treatment for a median of 3.5 months.

keep in mind that the 10% improvement was designed to be inclusive of the high risk group.

Are you privy to the SAP?

A 10% improvement in overall survival in patients treated with Multikine treatment regimen plus Standard of Care (SOC) vs. patients treated with SOC alone

Excellent recap

Appreciate the work you provided.

Now, you know there is a lot more money for pharmas for treating people than curing people.

Thanks, good to know.

Trust there will be a replay of this presentation.

One of the sticking issues I have is the different interpretation of OS improvement.

The Presentations use % increase. Division.

The Data release used improvement advantage. Subtraction.

I thought I heard Dr. Talor use the phrase improvement advantage.

Is this a major issue?

Goes to trust - been told OS improvement is determined by %.

Hard data is expressed in advantage terms.

Totally different.

Sold the remainder of everything in everyone's account during the call.

Pretty sure will be able to buy in lower.

Thank you all for being part of my journey.