News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Rickards - >>> Did the Saudis Just Kill the Dollar?

BY JAMES RICKARDS

JUNE 17, 2024

https://dailyreckoning.com/did-the-saudis-just-kill-the-dollar/

Did the Saudis Just Kill the Dollar?

There’s been a lot of talk over the past several days that Saudi Arabia is ending the petrodollar deal it’s had with the U.S. for 50 years. This story has been highly exaggerated. Today I want to address the misinformation you’re seeing right now, and show you what really happened.

News services of dubious accuracy reported that Saudi Arabia had ended the petrodollar deal on June 9, after 50 years. This report was quickly followed by claims that oil would now be priced in everything from Chinese yuan to Indian rupees, Russian rubles and other currencies without strong claims to being reserve currencies.

The implication of these stories was that the U.S. dollar’s long reign as the leading global reserve currency was over. New reserve currencies would come to the fore, most prominently the BRICS planned currency.

The crypto crowd wasn’t far behind shouting that the demise of the dollar proved that cryptocurrencies were the way of the future. The internet was on fire with these and other histrionic claims.

Don’t Buy It

In fact, almost everything you just read is nonsense. There have been some very important developments in international finance and monetary policy in recent days but they’re far more nuanced and ultimately more important than stories grabbing the headlines.

As the saying goes, it’s complicated. Let’s deconstruct what’s actually going on.

The petrodollar deal was concluded in June 1974 under the Nixon administration. It was a tense time following the 1973 Yom Kippur War and the Saudi oil embargo of exports to the U.S.

I played a role in the run-up to the deal when I went to the White House to meet with Helmut Sonnenfeldt, Henry Kissinger’s most trusted aide. We discussed a plan to invade Saudi Arabia in case the Saudis didn’t agree to what the Nixon administration had put on the table.

The deal had four main parts.

The Petrodollar Deal

Saudi Arabia would price oil in U.S. dollars. Saudi Arabia would take the dollars it earned through oil sales and invest them in U.S. Treasury securities or in large bank CDs. The Treasury and the banks would lend those dollars to developing economies that would purchase equipment and agricultural products from the U.S. Finally, the U.S. offered Saudi Arabia military protections against the Soviets and regional rivals. The security agreements and the financial agreements were put into writing but have never been revealed.

The petrodollar deal was a win-win for the participants and the world. The U.S. found a reliable prop for the dollar’s reserve currency status (since other countries would need dollars to buy their own oil) and Saudi Arabia enhanced its national security.

Recycling the Saudi dollars to developing country buyers was a boost to world trade and commodity prices and helped pull the world out of the severe 1974 recession. At the Saudi’s request, the U.S. kept a veil of secrecy over the exact amount of Treasuries owned by Saudi Arabia; their holdings were lumped in with other OPEC members from the region and were not reported separately.

Did the Saudis just end the petrodollar deal as reported? Not exactly.

Less Than Meets the Eye

The deal was never a formal treaty ratified by the Senate, which would rise to the level of law. It was a non-binding executive agreement; not much more than a written handshake. It contained annual renewal provisions and could be terminated at any time by either party.

The Saudis held up their end by pricing oil in dollars and buying U.S. Treasuries. The U.S. held up its end by sending troops and repelling Iraq’s invasion of Kuwait in Operations Desert Shield and Desert Storm in 1990–91. The agreement suited both sides and so it continued.

The agreement never had an explicit “expiration date” so reports that the deal has expired are overstated. The Saudis have notified the U.S. that they’re not extending the deal, but that decision has to be put in the context of other U.S.-Saudi discussions.

The U.S. and Saudi Arabia are currently in negotiations on a new financial and security arrangement that would supersede the old petrodollar deal. The new agreement will provide that Saudi Arabia will recognize Israel as part of the broader Abraham Accords initiated during the Trump administration.

The U.S. will continue to offer security protections to the Saudis, but those will be expanded to include uranium enrichment technology. Ostensibly this technology would be used to fuel nuclear reactors but might later be used to build nuclear weapons. Saudi Arabia wants this technology because it feels threatened by Iran’s own uranium enrichment capability.

Not Much Is Different

On the financial side, Saudi Arabia would continue to price oil in dollars but could agree to be paid in other currencies, primarily euros, as is the case today. The Saudis would continue to purchase Treasury securities alongside its holdings of gold.

In short, not much would change from the current petrodollar deal except for the enhanced security guarantees.

The reason Saudi Arabia allowed the existing deal to lapse was to gain leverage in the new negotiations and because the old deal would be replaced by the new deal in all events.

The new deal will not be completed for six months, perhaps longer. It’ll be handed off from the Biden administration to the new Trump administration in January 2025 if Trump wins the election, which I believe he will.

The reason for the delay is that Saudi Arabia cannot recognize Israel until the Gaza War is over. That’ll take a few more months at least. There’s an irony there because the Trump administration created the Abraham Accords and may be the one to complete the process by including Saudi Arabia under that umbrella.

That’s a summary of what’s going on. Here’s what’s not going on…

Not a Dollar Death Blow

Oil will not be priced in rupees, rubles, yuan or other emerging-market currencies except in very small quantities. About 20% of oil purchases today are in euros and that can be expected to continue.

The new arrangement between Saudi Arabia and the U.S. doesn’t mark the end of the dollar as the world’s leading reserve currency. It doesn’t imply the collapse of the global market in U.S. Treasury securities, which a lot of people have been claiming in recent days.

The oil and dollar markets will be business as usual. Ties between the Saudis and the U.S. will be even closer because of the nuclear enrichment aspect of the new deal.

None of which is to say that there have not been important developments in international financial and monetary markets away from the Saudi situation. There have.

In particular, there were major policy initiatives announced at the St. Petersburg International Economic Forum (SPIEF) hosted by Vladimir Putin from June 5–8.

Incremental Steps

Russia announced they were working with other BRICS+ members to develop a global payments system completely independent of existing Western systems including SWIFT, Fedwire and other clearinghouses.

That’s critical because payments through Western systems are subject to seizure and interdiction, whereas payments through an independent system should be safe from Western interference.

Putin also met with Dilma Rousseff, former president of Brazil and current president of the New Development Bank, which is a de facto central bank and development lender to the BRICS+ and associated members.

That meeting was to discuss the roll-out of the new BRICS currency. It will be called the Unit and its value will be based on a weight of gold (40%) and a basket of BRICS+ currencies (60%).

The key to implementation of the BRICS currency plan is an expansion of the membership. A bilateral currency arrangement between two weak emerging markets will never be successful because there’s not much for the seller of goods to buy once it receives the currency.

But a currency union with 20 members or more using the Unit can be successful because the seller of goods can “go shopping” in many other markets and is likely to find goods or services that meet its needs. The success of the euro with 20 members and worldwide acceptance is the model for this.

The Unit won’t be launched for another year or longer although some formal announcements may come at the BRICS leaders’ summit in Kazan, Russia, this October. It’ll still take a few years to add members, build out the infrastructure and firm up some valuation issues. Still, this currency is coming.

Not a Reserve Currency

Importantly, the BRICS Unit will initially be a payment currency, not a reserve currency. Payment currency arrangements are fairly straightforward. Reserve currency status is far more difficult because it requires a large, liquid bond market; good rule of law; and an infrastructure of dealers, hedging tools, repurchase agreements, auctions and settlement procedures.

That can take 10 years or longer to put in place with rule of law perhaps being the most difficult element.

Even as a payment currency, the BRICS Unit could be used in a material percentage of global trade, giving the dollar a run for its money. The BRICS Unit doesn’t mark the end of the dollar as a widely accepted currency.

Still, in conjunction with the badly misguided weaponization of the dollar by Joe Biden and Janet Yellen it could mark the beginning of the end.

The latest Saudi action won’t destroy the dollar. The Biden administration seems determined to accomplish that all by itself.

<<<

---

Rickards - >>> Dollar Takes a “Pounding”

BY JAMES RICKARDS

JUNE 24, 2024

https://dailyreckoning.com/dollar-takes-a-pounding/

Dollar Takes a “Pounding”

You’ve probably heard that the U.S. economy is heavily “financialized.” What does that really mean? What is financialization?

It’s a big topic and not very well defined. It can refer to the dominance of financial activity over traditional business activity in goods and services. It can refer to market bubbles. It can refer to the use of financial instruments in non-traditional arenas such as warfare or political witch hunts.

In fact, it refers to all the above and more. Investors need to understand financialization in order not to be blindsided by market activity that defies fundamental analysis.

We can begin our review of financialization with a look at the role of the U.S. dollar in global transactions.

This is not a technical article detailing the plumbing of the financial system. But in considering the role of currencies in global finance, it’s important to distinguish between reserves (basically a nation’s savings account) and payments (transactions, trade, etc.).

The Dollar Still Dominates

The denomination of global reserves today is approximately:

58% U.S. dollars and 20% euros

The remaining 22% is divided among yen (6%), sterling (5%), Canadian dollars or CAD (2.5%)

And other currencies are each less than 2% (AUD, CNY, CHF).

In payments (measured in SWIFT message traffic), the U.S. dollar is about 59% of payments, with the euro at 13%, yen at 6%, sterling at 5% and yuan and CAD at about 3% each. All other currencies are less than 3% each.

The relatively larger role of the dollar in payments is due to higher oil prices and oil being denominated in dollars. SWIFT message traffic is almost exclusively interbank payments among large banks. There are many bilateral payments (for example, Russian payments to India in local currencies) that do not go via SWIFT.

There is no immediate threat to the role of the U.S. dollar in either reserves or payments.I recently debunked the fake news that Saudi Arabia has just ended the petrodollar deal that’s been in place since 1974.

Instead there’s a slow, steady erosion in the role of the dollar that could accelerate in the future. A good case study is the decline of sterling. In 1914, it was the dominant reserve and trade currency. By 1944, it had largely been displaced by the U.S. dollar as a result of Bretton Woods.

Slow Death

Today, sterling is barely a footnote in global reserves and payments. Still, that decline took 30 years (1914–1944) and continued for another 80 years (1944–2024). Major currencies don’t simply disappear overnight, but they are subject to these types of declines and gradual displacement by alternatives.

Contrary to what you hear from a lot of fringe analysts, the Russian ruble and Chinese yuan will not displace the U.S. dollar. Neither currency is widely accepted outside its home country. Those currencies have limited uses and lack large liquid bond markets, and their source countries lack a rule of law. Notions of a “gold-backed yuan” are nonsense. China simply doesn’t have enough gold.

A BRICS currency is a more likely alternative to the dollar for global payments. It won’t be issued for several more years. The BRICS are currently expanding their membership and will expand it further at their summit in Kazan, Russia in October.

That’s critical because a larger membership increases the trading zone where the currency can be used. Non-BRICS members can also agree to accept the new BRICS currency if they wish.

If you receive the BRICS currency in trade, it’s more useful if you can spend it or invest it in 20 or 30 other countries rather than just one trading partner as is the case with rubles, yuan and rupees.

This process of expanding the currency zone with new members will take a few more years, but the infrastructure is being put in place now. The development of the euro (which took eight years from the 1992 Maastricht Treaty to launch in 2000) is a good model for this.

The Great Leap to Reserve Status

While a BRICS currency will be used in trade in a few years, it will take longer to develop as a reserve currency. That requires the creation of a large, liquid bond market, which takes a legal code, issuers, dealers, settlement channels, hedging tools and much more. That process can take 10 years or longer.

What we should expect is not a sudden collapse of the U.S. dollar and the U.S. Treasury market in payments and reserves, but rather a slow, steady diminution in the role of the dollar similar to what happened with sterling after World War I.

In the short run, the main alternative to the U.S. dollar in reserve positions is not another currency, but gold. Central banks have been net purchasers of gold since 2010, reversing their status as net sellers that had prevailed since 1970.

These net purchases of gold are reflected in increases in gold as a percentage of total reserves. Gold now represents over 70% of U.S. reserves, 25% of Russian reserves and 8% of Chinese reserves.

Curiously, gold isn’t even reported in the IMF’s official reserve asset reports, despite the fact that the IMF itself owns over 1,000 metric tonnes of gold. Gold has the added attraction of being a physical, non-digital asset that cannot be frozen or seized by the United States.

The Weaponized Dollar

The most conspicuous example of financialization is the use of financial sanctions in warfare. This might better be called the weaponization of the dollar. U.S. sanctions against Russia have failed badly (as I predicted in 2022) to the point that the Russian economy is now outperforming the U.S. economy by every important metric. The U.S. hasn’t learned its lesson and is moving to more dangerous methods.

The U.S. froze Russian assets (about $300 billion in U.S. Treasury securities) at the start of the war in Ukraine. Now the U.S. is moving to steal those assets. This plan was recently unveiled on June 13 at the G7 summit in Apulia, Italy.

Russia will retaliate by seizing over $300 billion of Western assets still in Russia. Since the Russian assets are mostly in custody at Euroclear (about $200 billion), Russia can sue Euroclear for wrongful conversion in Russia-friendly jurisdictions where Euroclear has offices including Dubai and Hong Kong.

Euroclear has about $40 trillion in assets under custody. With a court judgment in hand, Russia could proceed to freeze and seize Euroclear assets on a global basis. This could throw the global financial system into complete chaos.

Financialization in its many forms is no longer a sideshow. It has become the main event in many arenas. Investors need to follow developments closely in order not to get caught in the political and military crossfire.

You need to take cover.

<<<

---

The growing rift between India and China is good news for the US, and will help throw a wrench into BRICS (see article previous post). Other good news this year is that Argentina decided not to join BRICS, and the Saudis have also apparently put the brakes on their plans to join. Also, distrust between India and China has been noted as a key obstacle in developing the BRICS gold linked currency, which has been delayed.

So good news for the US. Now, if we can somehow drive a wedge between China and Russia (the Kissinger strategy), the US might prolong its dominant global position for some time. The 'unipolar' world that the US enjoyed in the decades following the collapse of the Soviet Union is gone, but hopefully (for us) the sun doesn't set on US Empire too quickly.

Imo, what the US needs to do is to use 'the carrot' side more, and try to outcompete China's Belt + Road strategy. The reason so many countries have been gravitating to join BRICS is that China has been helping them build infrastructure --> roads, powerplants, etc. In particular, along with Russia, China is building nuclear powerplants in many emerging countries, which is a huge draw for these countries to ally with China-Russia-BRICS.

The US needs to move away from only 'the stick' (war, sanctions, de-Swifting, etc), and use 'the carrot' more. That's the way to win back the developing countries of the world to the US side. How these countries decide to align themselves will determine the future of the US.

---

>>> Third term for Modi likely to see closer defense ties with US as India's rivalry with China grows

Associated Press

by DAVID RISING and ASHOK SHARMA

6-7-24

https://www.msn.com/en-us/news/world/third-term-for-modi-likely-to-see-closer-defense-ties-with-us-as-india-s-rivalry-with-china-grows/ar-BB1nMmRe?cvid=3eb38174dbf5497ee68dc3a8df607ad9&ei=54

NEW DELHI (AP) — Fresh from declaring victory in India's election, Prime Minister Narendra Modi offered few details on the agenda for his third term, but went out of his way to underline he would continue to focus on raising the country's military preparedness and clout.

That should come as good news to the United States and its other allies, as they focus increasingly on keeping China’s sweeping maritime claims and growingly assertive behavior in the Indo-Pacific region in check.

"The government will focus on expanding defense production and exports,” Modi told a crowd of supporters at his party's headquarters after election results came in. He spoke of his plan to increase security by lowering India's dependence on arms imports. “We will not stop until the defense sector becomes self sufficient.”

Defense cooperation with the U.S. has greatly expanded under Modi, particularly through the so-called Quad security grouping that also includes Australia and Japan.

It’s a two-way street, giving the U.S. a strong partner neighboring China, which Washington has called its “pacing challenge,” while strengthening India’s defense credibility against a far more powerful rival.

"India is currently a frontline state as far as the Americans are concerned,” said Rahul Bedi, a New Delhi-based defense analyst. “The Indian navy is a major player in the Indian Ocean region.”

The defense relationship was also at the top of U.S. President Joe Biden's agenda when he congratulated Modi on the election results

In a call, “the two leaders emphasized their deepening the U.S.-India comprehensive and global strategic partnership and to advancing their shared vision of a free, open and prosperous Indo-Pacific region,” the White House said.

It added that National Security Advisor Jake Sullivan would soon travel to New Delhi “to engage the new government on shared U.S.-India priorities.”

It was about a year into Modi's second term when India's defense focus took a sharp turn toward China, when troops from the two nuclear neighbors clashed in 2020 in the Galwan Valley in the disputed northern border region of Ladakh and 20 Indian soldiers were killed.

"China really is India's long term strategic challenge, both on the border and in the Indian Ocean as well,” said Viraj Solanki, a London-based expert with the International Institute for Strategic Studies.

"This has resulted in a number of defense partnerships by India shifting, or just focusing on countering China's growing influence in the Indo-Pacific region,” he said.

Beijing has a close relationship with Pakistan, India's traditional rival, and China has been increasing defense cooperation with India's neighbors, including Nepal and Bangladesh, as well as the Maldives and Sri Lanka.

"China is really trying to engage more with these countries and develop its own influence and presence,” Solanki said. “I think that is a concern for New Delhi and something that will lead to increased competition in the Indian Ocean over the next few years.”

In congratulating Modi on the election results, Chinese Foreign Ministry spokesperson Mao Ning said that a “sound and stable ” relationship between India and China was “in the interest of both countries and conducive to the peace and development of the region."

She also added that China stood “ready to work with India,” but her comments were significantly more muted than the Foreign Ministry's remarks on Modi's last win in 2019 — before the border fight. At that time, the Foreign Ministry called the two nations “important neighbors” and said China wanted to "deepen political mutual trust, carry out mutually beneficial cooperation and push forward the closer partnership between the two countries.”

Modi has always governed with his party in the majority, but after a lackluster performance in the election will now be forced to rely on coalition partners, and will face a stronger and invigorated opposition.

The main opposition Congress party is unlikely to challenge Modi's defense reforms, but has been critical of how he has handled the border issue with China and may pressure him on that front, Bedi said.

"Modi has not been entirely truthful, or very economical with the truth as far as the situation in Ladakh is concerned,” he said. He referred to a Defense Ministry document that was published online, and quickly removed, which had suggested Chinese troops entered Indian territory during the 2020 confrontation.

“The opposition, I am sure, will raise questions and ask the government to come clean on what the real situation is.”

Under Modi's program of military modernization and reform, his government has sought to grow the private defense manufacturing sector, a space previously occupied solely by the government-run organizations, and has eased foreign direct investment regulations to try and encourage companies to establish themselves in India.

In a flagship project, the country launched its first home-built aircraft carrier in 2022, part of a plan to deploy two carrier battle groups to counter China’s rising maritime power.

Much of India's military equipment is of Russian origin, and delays on delivery and difficulties of procuring spare parts due to Russia's invasion of Ukraine has also provided impetus for India to diversify defense procurement, looking more to the U.S., France, Israel and elsewhere, Solanki said.

As it seeks to strengthen ties with India, Washington has agreed to a deal that will allow General Electric to collaborate with Hindustan Aeronautics to produce fighter jet engines.

Speaking at the Shangri-La defense conference in Singapore last weekend, U.S. Defense Secretary Lloyd Austin said the countries were also co-producing armored vehicles.

“The relationship that we enjoy with India right now is as good or better than our relationship has ever been,” he said. “It's really strong.”

<<<

---

Rickards - >>> $27,000 Gold

BY JAMES RICKARDS

MAY 13, 2024

https://dailyreckoning.com/27000-gold/

$27,000 Gold

I’ve previously said that gold could reach $15,000 by 2026. Today, I’m updating that forecast.

My latest forecast is that gold may actually exceed $27,000.

I don’t say that to get attention or to shock people. It’s not a guess; it’s the result of rigorous analysis.

Of course, there’s no guarantee it’ll happen. But this forecast is based on the best available tools and models that have proved accurate in many other contexts.

Here’s how I reached that price level forecast…

This analysis begins with a simple question: What’s the implied non-deflationary price of gold under a new gold standard?

No central banker in the world wants a gold standard. Why would they? Right now, they control the machinery of global currencies (also called fiat money).

They have no interest in a form of money they can’t control. It took about 60 years from 1914–1974 to drive gold out of the monetary system. No central banker wants to let it back in.

Still, what if they have no choice? What if confidence in command currencies collapses due to some combination of excessive money creation, competition from Bitcoin, extreme levels of dollar debt, a new financial crisis, war or natural disaster?

In that case, central bankers may return to gold not because they want to, but because they must in order to restore order to the global monetary system.

What’s the Proper Gold Price?

That scenario begs the question: What is the new dollar price of gold in a system in which dollars are freely exchangeable for gold at a fixed price?

If the dollar price is too high, investors will sell gold for dollars and spend freely. Central banks will have to increase the money supply to maintain equilibrium. That’s an inflationary result.

If the dollar price is too low, investors will line up to redeem dollars for gold and then hoard the gold. Central banks will have to reduce the money supply to maintain equilibrium. That reduces velocity and is deflationary.

Something like the latter case happened in the U.K. in 1925 when it returned to a gold standard at an unrealistically low price. The result was that the U.K. entered the Great Depression several years ahead of other developed economies.

Something like the former case happened in the U.S. in 1933, when FDR devalued the dollar against gold. Citizens weren’t allowed to own gold, so there was no mass redemption of gold. But other commodity prices rose sharply.

That was the point of the devaluation. Resulting inflation helped lift the U.S. out of deflation and gave the economy a boost from 1933–1936 in the midst of the Great Depression. (The Fed caused another severe recession in 1937–1938 with their customary incompetence.)

The policy goal obviously is to get the price “just right” by maintaining the proper equilibrium between gold and dollars. The U.S. is in an ideal position to do this by selling gold from U.S. Treasury reserves, about 8,100 metric tonnes (261.5 million troy ounces), or buying gold in the open market using freshly printed Fed money.

The goal would be to maintain the dollar price of gold in a narrow range around the fixed price.

What price is just right? This question is easy to answer, subject to a few assumptions.

$27,533 Gold

U.S. M1 money supply is $17.9 trillion. (I use M1, which is a good proxy for everyday money).

What is M1? This is the supply that is the most liquid and money that is the easiest to turn into cash.

It contains actual cash (bills and coins), bank reserves (what’s actually kept in the vaults) and demand deposits (money in your checking account that can be turned into cash easily).

One needs to make an assumption about the percentage of gold backing for the money supply needed to maintain confidence. I assume 40% coverage with gold. (This was the legal requirement for the Fed from 1913–1946. Later it was 25%, then zero today).

Applying the 40% ratio to the $17.9 trillion money supply means that $7.2 trillion of gold is required.

Applying the $7.2 trillion valuation to 261.5 million troy ounces yields a gold price of $27,533 per ounce.

That’s the implied non-deflationary equilibrium price of gold in a new global gold standard. Of course, money supplies fluctuate; lately they’ve been going up sharply, especially in the U.S.

There’s room for debate about whether a 40% backing ratio is too high or too low. Still, my assumptions are moderate based on monetary economics and history. A dollar price of gold of over $25,000 per ounce in a new gold standard is not a stretch.

Obviously, you get around $12,500 per ounce if you assume 20% coverage. There are many variables in play.

The Fundamental Model

This model is also straightforward. It relies on factors we learned about in our first week of Intro to Economics — supply and demand.

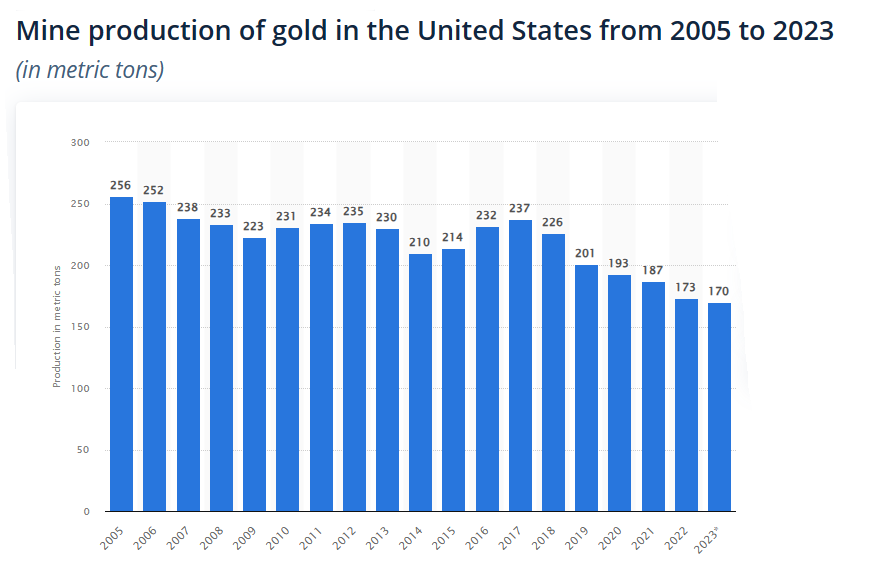

The most significant development on the supply side is the decrease of new mining output. As the chart shows below, mine production of gold in the U.S. has been decreasing steadily since 2017.

image 1

These figures reveal a 28% decrease over seven years, at the same time gold prices were rising and miners were motivated to expand output.

That’s not to argue that the world has reached “peak gold,” (output could expand in future for a variety of reasons). Still, my contacts in the mining community consistently report that gold is becoming more difficult to source and the quality of newly discovered ore is low-to-medium at best.

Flat output, all things equal, tends to put a floor under prices and to support higher prices based on other factors.

The Demand Side

The demand side is driven largely by central banks, ETFs, hedge funds and individual purchases. Traditional institutional investors are not large investors in gold. Much of the demand from hedge funds is conducted in derivatives such as gold futures.

Derivatives generally don’t involve physical delivery of gold. They involve “paper gold” that far exceeds the actual, physical gold supply. It’s this paper gold market that accounts for volatility in the gold market, not gold itself.

Meanwhile, central bank demand for gold has surged from less than 100 metric tonnes in 2010 to 1,100 metric tonnes in 2022, a 1,000% increase in 12 years. Central bank gold demand remained strong in 2023 with 800 metric tonnes acquired through Sept. 30.

That puts central bank gold demand on track for a new record. There’s no sign of that demand slowing in 2024.

Overall, the picture is one of flat supply and increasing demand, mostly in the form of official purchases by central banks.

A Math Lesson

Finally, a bit of elementary math is helpful in understanding how the dollar price of gold can move past $25,000 per ounce in the next two years. For this purpose, we’ll assume a baseline price of $2,000 per ounce (although gold has been in the $2,300 range lately with no signs of falling back to the $2,000 level).

But for our purposes, we’ll keep it simple.

A move from $2,000 per ounce to $3,000 per ounce is a heavy lift. That’s a 50% increase and could easily take a year or more. Beyond that, a further increase from $3,000 to $4,000 is a 33% increase: another large rally. A further gain from $4,000 per ounce to $5,000 per ounce is a further gain of 25%.

But notice the pattern. Each gain is $1,000 per ounce, but the percentage increase drops from 50% to 33% to 25%. That’s because the starting point is higher while the $1,000 gain is constant. Each $1,000 jump represents a smaller (and easier) percentage gain than the one before.

This pattern continues. Moving from $9,000 per ounce to $10,000 per ounce is only an 11% gain. Moving from $14,000 per ounce to $15,000 per ounce is only a 7% gain. Gold can move 1% in a single trading day, sometimes 2% or more.

As an extreme example, a move from $99,000 per ounce to $100,000 per ounce is about a 1% move. Those $1,000 pops get even easier as we approach my calculated gold price of $27,533.

The lesson for you as an investor is to buy gold now.

As prices continue to rally, you’ll get more gold for your money at the outset and high-percentage returns as gold rallies from a lower base. Toward the end of the long march past $25,000 per ounce, you’ll have bigger dollar gains because you started with more gold.

Others will jump on the bandwagon, but you’ll already have a comfortable seat.

<<<

---

SDR, US Dollar, war, overpopulation, and more -

1) Covid as a race-specific bioweapon to weaken China.

While this would have made a lot of sense, it turned out to be incorrect. When Covid originally appeared in late 2019, one potential scenario was that it was a US bio engineered virus targeting Asians, with the goal of weakening China. This would make a lot of sense to the US/Western globalists, since in their view they desperately need to halt / reverse the rise of China and BRICS. So they simply 'do in' China with a race specific bioweapon. But it soon became apparent that Covid is not race-specific, so this proposed scenario was obviously incorrect. It's not impossible that the virus was intended to be race-specific, but the Deep State scientists had bungled the job, but except for that distant possibility, we can reject the 'Covid as a race specific bioweapon' hypothesis.

2) Covid as the first step in a larger process, with the goal of global population reduction.

The bigger picture that may be emerging is that Covid was merely the first step in a longer process, with population control vaccines to be the main thrust. It's no secret that the globalists have long had an obsession with overpopulation, so the use of a vaccine for population control, or series of vaccines, makes a lot of sense. This approach would be ideal since the perpetrators (global elites) can avoid the effects themselves by simply not getting the vaccine. In this case, Covid was simply the justification for the government to get vaccine mandate power. So Covid was engineered to be like a bad case of the flu, just serious enough to be hyped into justifying national vaccine mandates, and ultimately global vaccine mandates (coming May 2024 vote on the WHO's global mandate authority).

Once in place, a future vaccine (or series of vaccines) can be mandated globally, and in these will contain the population control agent. By then, compliance with the mandates can also be enforced by the CBDCs that are being rolled out worldwide.

3) Variation on Jim Rickards' 'Ice-9' scenario which -- a) derails Chiina and BRICS expansion, b) restores the waning US dollar reserve system, with possible supplementation by the SDR of the IMF, and - c) gets population reduction rolling

With de-dollarization and the rapid expansion of BRICS, the hegemony of US/West is increasingly on the ropes. So a new version of Covid is released that severely disrupts the global economy, thus impeding the move away from the dollar reserve system, and the SDRs of the IMF can also be rolled out as the co-savior, in some combination of US dollar system and SDRs. This brings the world back into the fold of a financial system controlled by the US/West.

4) As strategic vehicles, Covid and vaccines are put on the back burner, replaced by War -

War is increasingly used in desperation to retain US global hegemony. Europe wants to gravitate away from the US in favor of China-Russia-BRICS, so the Ukraine war is launched. Saudi Arabia and Iran decide to join BRICS, so the Middle East war is launched to derail things. Argentina joins BRICS, so they are on the hit list.

---

Rickards - Petrodollar - >>> Kissinger Created the Doomsday Deal

BY JAMES RICKARDS

DECEMBER 4, 2023

https://dailyreckoning.com/kissinger-created-the-doomsday-deal/

Kissinger Created the Doomsday Deal

As I’m sure you know by now, Henry Kissinger died last week at the age of 100. He leaves a complex legacy, which is certainly understandable because he operated in a complex geopolitical environment.

But Henry Kissinger was a master strategist and political scientist. With his recent passing, I thought I’d retell the story of one of his most brilliant plans, and explain how it relates to the demise of the dollar.

In February 1974, I was asked by Professor Robert W. Tucker of the Johns Hopkins School of Advanced International Studies to join him and four other foreign policy experts for a meeting at the White House.

At the time, confidence in the dollar was on shaky ground because President Nixon had ended gold convertibility of dollars in 1971.

The price of oil was skyrocketing, partly due to inflationary policies pursued by the Federal Reserve, and partly due to an Arab oil embargo in response to U.S. aid to Israel in the Arab-Israeli Yom Kippur War of 1973.

Saudi Arabia was receiving dollars for their oil shipments, but they could no longer convert the dollars to gold at a guaranteed price directly with the U.S. Treasury. The Saudis were secretly dumping dollars and buying gold on the London market. This was putting pressure on the bullion banks receiving the dollar.

Confidence in the dollar began to crack. Anyway, back to my meeting at the White House…

Should We Invade Saudi Arabia?

We were ushered through the security gate on Pennsylvania Avenue near West Executive Avenue, closest to the West Wing. We were then escorted to the office of Dr. Helmut Sonnenfeldt, Secretary of State Henry Kissinger’s deputy on the National Security Council.

There, we engaged in a strategy discussion. Our focus that night was debating a full-scale military invasion of Saudi Arabia.

The idea was we’d then secure their oil fields, pump enough oil to supply Western and Japanese needs and price it however we wanted. We debated the pros and cons of this plan, including potential supply disruptions and international reactions until well into the evening.

Now, it may not be covered in the history books, but a military takeover of Saudi Arabia was very much on the table. In fact, the planning was well underway. But the Nixon administration under Henry Kissinger decided to try one other approach first. And what they came up with was absolute genius.

A few months after my meeting, in June 1974, President Nixon met with King Faisal in Saudi Arabia. A month later, he sent his representatives to offer a new deal. The deal was as straightforward as it was brilliant.

Birth of the Doomsday Deal

The Saudis would agree to sell their oil only for U.S. dollars. These dollars for oil were called “petrodollars.” And the Saudis would then reinvest these petrodollars in U.S. Treasury securities and deposits in U.S. banks.

In return, the U.S. would sell advanced weapons and military hardware to the Saudis and we’d promise U.S. military support to protect Saudi oil fields and the royal family.

This would effectively guarantee the House of Saud long-term rule over the country.

The final twist was that U.S. banks would then “recycle” the petrodollars deposited by Saudi Arabia as loans to emerging markets in Latin America, South Asia and Africa.

In turn, those developing countries would purchase U.S., European and Japanese exports. That would ignite global growth. And, of course, to do that they’d need lots of oil. That meant oil demand would grow endlessly as would demand for dollars. It was the ultimate win-win.

And the 1974 “Petrodollar Accord” was born. Or as I call it, the Doomsday Deal. Behind this “deal” was a not so subtle threat to invade Saudi Arabia and take the oil by force, which I was invited to the White House to consider.

BRICS and the End of the Doomsday Deal

Now, almost 50 years later, the wheels are coming off. The world is losing confidence in the dollar again, and the cracks in the dollar are already getting larger.

It’s important to understand all of this concerning BRICS.

If you’re unfamiliar with BRICS, I’m talking about the economic alliance between Brazil, Russia, India, China and South Africa. I wrote a lot about it this past summer and fall. I explained the changes in the global monetary system that will send shock waves throughout markets.

The BRICS nations represent almost one-third of the entire global GDP. Their economies are bigger than the United States, Germany, Japan, the U.K., France, Canada and Italy combined.

And thanks to Biden’s weakness and foreign policy failures our enemies — and even our allies — are emboldened and the Doomsday Deal is cracked wide open.

The BRICS countries have been running circles around blundering Biden lately.

Blunders

Here’s a quick rundown of some of Biden’s recent failures. On Jan. 17 of this year, shots were fired when Saudi Arabia humiliated Biden and thumbed its nose at America by announcing it is considering accepting other currencies for its oil.

And that announcement opened the floodgates.

On March 8, 2023, Reuters reported another massive blow as India and Russia are now ditching the dollar and trading oil in non-dollar currencies. On March 28, Brazil and China announced an agreement to conduct all future trade transactions using their own currencies.

And it gets even worse. Even our so-called allies saw the writing on the wall.

That same day, French oil giant Total Energies announced they had bought liquefied natural gas from a Chinese oil company using the Chinese currency, the yuan.

Now, other U.S. allies like India, Pakistan and the United Arab Emirates have made deals with Russia or China to buy oil or other commodities in their own currencies.

With Biden in the White House, they’re laughing at us now.

The Beginning of a Seismic Shift

Iraq announced earlier this year they’re now trading their oil for Chinese yuan. Recently it’s only gotten worse…

In August of this year, it was announced Saudi Arabia — our old partner in the Doomsday Deal — will be joining the BRICS group of nations starting in 2024.

And more recently, China and Saudi Arabia agreed to a currency swap deal.

Our enemies were already salivating, and now with this most recent news they are ready to pounce.

In a global political economy long dominated by the petrodollar, this could be the beginning of a seismic shift.

Eventually a tipping point will be reached where the dollar collapse suddenly accelerates as happened to the British pound sterling last century.

My background inside the U.S. intelligence community, investment banks and global currency markets has shown me how smart investors could profit from the failure of the Doomsday Deal.

One of the best ways investors can anticipate this monetary earthquake is by buying gold.

<<<

---

Rickards - >>> Why’s the Dollar So Darn Strong?

BY JAMES RICKARDS

NOVEMBER 7, 2023

https://dailyreckoning.com/whys-the-dollar-so-darn-strong/

Why’s the Dollar So Darn Strong?

The dollar has been extremely strong over the past two years. This persistent dollar strength has been a mystery to many. After all, the dollar’s problems are well known.

The ratio of government debt to GDP for the United States is at a record high approaching 130% (a prudent level is considered 30%, and anything over 90% is a headwind to any economic growth at all).

The U.S. is running multitrillion-dollar deficits year after year. The Congress and White House seem in the grip of Modern Monetary Theory, which claims that the U.S. can run unlimited deficits and accumulate unlimited debt without economic harm because it can print money in unlimited quantities to finance the debt and spending.

Meanwhile, projected annualized interest payments on the U.S. national debt exceeded $1 trillion at the end of October, according to Bloomberg. The cost of debt service has doubled in the past 19 months as interest rates have risen.

This fiscal profligacy comes against a backdrop of social unrest and political dysfunction. We’re facing a presidential election next year in which one candidate, Biden, is senile and the other candidate, Trump, may be behind bars on Election Day.

Take your pick. But the dollar keeps on chugging along. How can the dollar be so strong against such a dismal landscape?

There are two answers to this question.

Answer No. 1

The first is that the dollar has its problems, but other currencies are in even worse shape. For example, the Chinese yuan is on the brink of collapse being held aloft by non-sustainable intervention by Chinese banks.

The Japanese yen is joined at the hip with the yuan because of the extent of Japanese investment in China financed by Japanese banks. With the yuan going down, the yen will go down in sync.

So that’s two major currencies with problems.

Meanwhile, Europe and the U.K. have deindustrialized under the sway of the greeniacs pushing the Green New Scam policies. Now Europe faces a winter of freezing in the dark if cold weather is extreme and Russia decides to turn off the energy taps.

Germany, the largest economy in the eurozone, is heading for recession if it isn’t already in one, and the same is true for the U.K. That’s two more major currencies facing troubles.

So yes, the dollar has its problems, but as an investor do you really prefer sterling, euros, yen or yuan?

Answer No. 2

The second reason for the dollar’s strength is much more technical and not well understood, but it’s critical to grasp. You don’t need to nail down the technical details; it’s enough that you understand the bigger picture.

It involves the so-called Eurodollar.

Eurodollars are dollar-denominated deposits held at foreign offices of major banks, and therefore fall outside the jurisdiction of the Fed and U.S. banking regulations.

The Fed actually has very little influence over the global dollar market and the exchange value of the dollar. The old currency metrics of balance of trade and moves in capital accounts are leftovers from the world of fixed exchange rates, which have been gone for decades.

What drives the dollar is the Eurodollar market, as conducted by the world’s largest banks in London, New York and Tokyo. It’s here where global liquidity and interest rates are actually determined.

The Eurodollar market needs a constant supply of depositors parking their money in offshore offices of major banks.

Right now, this market is in contraction.

Derivatives are being unwound, balance sheets are being trimmed and interbank overnight lending is being financed with collateral.

And these banks are demanding the best collateral. They won’t accept corporate debt, mortgages or even intermediate-term U.S. Treasuries. The only acceptable collateral consists of short-term U.S. Treasury bills, the shorter the better. This means 1-month, 3-month and 6-month bills.

Those are denominated in dollars, of course. In order to get the bills to post as collateral, banks have to buy dollars to buy the bills. This has created enormous demand for dollars. And that partly accounts for the strength of the dollar.

Again, it’s not important that you understand the intricacies of the eurodollar system, just that high dollar demand in the Eurodollar market is contributing to dollar strength.

The fundamental dollar shortage problem is not going away soon, and will continue to support the dollar.

What About a New BRICS Currency?

What about the prospect of a BRICS currency union and the move toward a new currency? I wrote a lot about that ahead of the BRICS Leadership Summit that took place back in August.

This new currency would be gold-linked and would displace the dollar in time as a major player in world trade.

Shouldn’t that be weakening the dollar?

After all, the prospect of a BRICS currency should pose a severe threat to the petrodollar, which is a pillar of dollar strength.

But this movement is still in its infancy and, unsurprisingly, is experiencing growing pains.

It’s not yet as unified as it needs to be if it’s going to seriously threaten the dollar. And one of those BRICS nations — India — seems to be playing both sides.

It was recently reported that India’s government is expected to reject demands from Russian oil companies to pay for Russia’s crude oil imports in Chinese yuan.

Russia currently has a surplus of rupees and is having trouble spending them. At the same time, demand for yuan has grown as Russia trades more with China.

Meanwhile, India mostly uses the dirham and U.S. dollar to pay for Russian oil imports. Basically, India is currently in a balancing act. They consider Russia an important economic ally while they consider China a geopolitical rival.

India fears popularizing the yuan will hurt its own efforts to internationalize the rupee. In fact, India was the only BRICS nation to oppose the introduction of a common currency, fearing it would benefit the yuan.

India’s refusal to give in to Russia’s demands leaves a significant role for the dollar, which is another reason to believe the dollar will retain its strength for the foreseeable future.

The Golden Ruler

Now, don’t get me wrong. I’m not saying the dollar is strong. It isn’t, for all the reasons I listed above. It’s just stronger than its competitors, and that’s why it appears strong.

Is there some way to tell if the dollar is actually getting stronger or weaker without making reference to other currencies?

Yes. The answer is gold. Think of gold as a ruler that measures dollar strength or weakness.

Gold has gained close to 10% over the past month or so. I expect gold to become much stronger, despite some temporary setbacks along the way.

Investors should consider today’s prices a gift and perhaps a last chance to acquire gold at these prices before the real safe haven race begins.

Below $2,000, gold is so cheap right now, it’s practically a steal. I strongly urge you to take advantage.

<<<

---

Rickards - >>> Something “Big and Stupid” Is Coming…

BY JAMES RICKARDS

OCTOBER 3, 2023

https://dailyreckoning.com/something-big-and-stupid-is-coming/

Something “Big and Stupid” Is Coming…

With debt levels reaching all-time highs in major developed and developing economies, and with debt-to-GDP ratios also in record territory (not including contingent liabilities such as Social Security, health care and other entitlements, which make matters worse), it seems time to consider just how nations will deal with this problem.

The debt crisis may not be imminent, but it is unavoidable. When it happens, it may present the greatest financial disaster of all time. It’s never too soon for investors to consider the fallout.

When you issue debt in a currency you print, there’s no need for default in the sense of non-payment.

You can just have the central bank buy the debt (by printing money). This is the situation today in the U.S., Japan, the U.K. and the European Monetary Union (the countries that use the euro). They all have huge debt burdens, but they all have central banks that can simply buy the debt by printing money to avoid default.

Non-Payment Is Not the Issue

There are many bad consequences to printing money and storing up debt on central bank balance sheets, but non-payment of debt is not one of them. This is the mantra of the Modern Monetary Theorists (MMT) and their thought leader Stephanie Kelton.

In my view, MMT is garbage as economic policy, but the no-default tenet is valid. George Soros says the same thing.

That said, we are well past the point where the debt can be managed with real growth. That threshold is about a 90% debt-to-GDP ratio. A 60% debt-to-GDP ratio is even more comfortable and can be managed.

Unfortunately, the major reserve currency economies are all well past the 90% ratio as are those of many smaller countries. The U.S. ratio is 134%, an all-time high. The U.K. ratio is 102%. France is 111%. Spain is 112%. Italy is 145%.

China reports a figure of 77% but this is highly misleading because it ignores provincial debt for which Beijing is ultimately responsible. China’s actual figure is over 200% when provisional debt is included.

The champion debtor is Japan at 261%. The only major economy with a halfway respectable ratio is Germany at 67%. It’s Germany’s misfortune that they are probably responsible for the rest of Europe through the ECB Target2 system.

All these countries are headed for default. But we must consider the different ways to conduct a default.

There are three basic ways to default: non-payment, inflation and debt restructuring. You can take non-payment off the table for the reason mentioned above — you can always just print the money.

The same goes for restructuring. Inflation is clearly the best way to default. You pay back the money in nominal terms, but it’s worth very little in real terms. The creditor loses and the debtor countries win.

Nice and Easy Does It

The key to inflating away the real value of debt is to go slowly. It’s like stealing money from your mother’s purse. If she has $50 and you take $40, she’ll notice. If you take one dollar, she won’t notice. But a dollar stolen every day adds up over time.

This is what the U.S. did from 1945–1980. At the end of World War II, the U.S. debt-to-GDP ratio was 120% (about where it is now). By 1980, the ratio was 30%, which is entirely manageable.

Of course, nominal debt and GDP soared, but nominal GDP went up faster than nominal debt, so the ratio fell. If you can keep inflation around 3% and interest rates around 2% and exert fiscal discipline (which we did under Eisenhower, Kennedy, Nixon and Ford), the nominal GDP will grow faster than nominal debt (due to the Fed capping rates).

If you improve the ratio by, say, 2% per year and keep it up for 35 years (1945–1980), you can cut the ratio by 70%. That’s what we did.

The key was to do it slowly (like stealing from your mom’s purse). Almost no one noticed the decline in the real value of money until we got to the blow-off stage (1978–1981). But by then it was mission accomplished.

So there are two ways to deal with excessive debt: fiscal discipline and inflation. From 1945–1980, the U.S. did just that. If you run inflation at 3% and interest rates are 2%, you melt the real value of debt. If you exert fiscal discipline relative to GDP, you decrease the nominal debt-to-GDP ratio.

We did both.

The reason the debt-to-GDP ratio is back up to 134% is that Bush45, Obama, Trump and Biden ignored the formula. Since 2000, fiscal policy has been reckless so the formula doesn’t work. The problem isn’t really “money printing” (most of the money the Fed prints just comes back to the Fed as excess reserves, so it doesn’t do anything in the real economy).

The problem is that nominal debt is going up faster than nominal GDP, so the debt-to-GDP ratio goes up. This dynamic will be made much worse by the huge increase in interest rates over the past 18 months.

You can’t borrow your way out of a debt crisis. We have also been unable to generate much inflation. Inflation ran below 2% for almost all of the 2009–2019 recovery.

Japan Writ Large

Looking at the global picture, it’s important to understand that Japan is just a bigger version of the U.S. They don’t have fiscal discipline and they can’t get inflation to save their lives. The only way out for Japan is hyperinflation, which will come but not yet.

Japan can probably keep the debt game going for a while. The crash will come when the currency collapses. When I started in banking, USD/JPY was 400. Those were the days!

A debt crisis is on the way. Something big and stupid (in the words of the brilliant analyst Stephanie Pomboy) is coming from policymakers to address the issue. But the solution won’t be a policy and it won’t be a plan. A crisis will just happen almost overnight and seem to come from nowhere.

But it will come.

<<<

---

>>> The BRICs Go For Gold

Forbes

by Nathan Lewis

Jul 16, 2023

https://www.forbes.com/sites/nathanlewis/2023/07/16/the-brics-go-for-gold/?sh=5b386765eb35;

After months of debate about various currency and commodity baskets, a Russia- and China-led consortium has apparently settled on using gold as the basis of a planned new international currency system separate from the US dollar and euro. As recently reported by state-funded Russia Today, an upcoming meeting of leaders from Brazil, Russia, India and China in August may include the formal introduction of the new initiative.

This would be similar to the Bretton Woods meeting in 1944, where, after the floating currency chaos of the Great Depression, a new gold-based international currency architecture was laid out. The centerpiece was the US dollar, which in turn would be linked to gold at $35/oz., its gold parity since 1933. This laid the foundation for two decades of peace, prosperity, and fixed exchange rates, which sadly came to an end when the US dollar was floated from its golden anchor in 1971.

Since then, various governments have attempted to move back toward an international arrangement based on gold. In 2019, Malaysia's prime minister Mahathir Mohammad proposed a Pan-Asian currency based on gold. "At the moment we have to depend upon the U.S. dollar but the U.S. dollar is also not stable. So the currency that we propose should be based on gold because gold is much more stable," Mahathir described. This too mirrored the Bretton Woods debates, where John Maynard Keynes' "bancor" proposal, which amounted to a global floating fiat currency, was abandoned in favor of the gold-based U.S. dollar at the heart of the system.

In 2009, Libya's Muammar Gaddafi proposed a Pan-African currency, the gold dinar, echoing the gold dinar coins of the Arab Caliphates that once ruled North Africa. But, unrest in Libya in 2011 put an end to such ambitions.

Also in 2009, the head of China's central bank, Zhou Xiaochuan, wrote: "An international reserve currency should first be anchored to a stable benchmark and issued according to a clear set of rules … [Its] adjustments should be disconnected from economic conditions and sovereign interests of any single country. The acceptance of credit-based national currencies, as is the case in the current system, is a rare special case in history."

Although Xiaochuan did not say how these goals might be achieved, we can assume it would be done exactly the same way that Mao Zedong ended hyperinflation in China in 1950: By fixing the yuan to gold.

In Moscow, leading intellectual Sergey Glazyev recently proposed a "Gold Ruble 3.0," referencing the gold-based rubles of both the Czarist era, and then the Soviet Union. Russian media reported that Russia and Iran are in talks to establish a gold-based cryptocurrency for international trade.

All of this rumbling may have come to nothing, if not for the outbreak of hostilities in Ukraine. This was immediately followed by the isolation of Russia from the entirety of the Western financial system, including US and EU banks, and the SWIFT system for international bank payments. The Russian government was ready to make interest and principal payments on its euro-based bonds, but it literally could not do so. To add both insult and injury, roughly $600 billion of foreign reserves, held in custody in the US and EU, were "frozen," and likely to be confiscated.

This was a wake-up-call to all governments worldwide that held dollar or euro foreign reserves, or used the SWIFT banking system. The time had come to set up alternative arrangements.

This would also require a degree of independence from the International Monetary Fund. Although the IMF was set up at Bretton Woods in 1944 explicitly to reinforce the system built around the golden dollar, by 1978 that mission had become obsolete. In a 1978 revision to its Articles, the IMF allowed governments to link their currencies' value to anything "other than gold" (Article IV, Sec. 2a). The IMF itself would follow "the objective of avoiding the management of the price, or the establishment of a fixed price, in the gold market." (Article V, Sec. 12a) In other words, the IMF banned the gold standard among all member countries. The effect was to maintain the floating fiat dollar's primacy in international affairs.

Today, a "gold standard" proposal comes with a cloud of fallacious ideas, having to do with the "balance of payments" and other odd notions. It is best understood as simply a means to stabilize currency value. Today, many countries' currencies are linked to the euro, including Bulgaria, which uses a euro currency board. A gold standard system is the same basic idea, but using gold instead of a floating fiat euro. All of today's electronic payment systems would remain the same.

This was the principle that all of the Western World (and actually the Eastern World as well) followed for the past 600 years since the Renaissance. It worked very well. Gold was indeed tolerably stable in value, in the short and long term — stable enough that countries that stuck to it suffered no ill consequences as a result. They may have suffered for other reasons: Mao's Great Leap Forward (1958-1962) resulted in mass starvation, even though the yuan remained linked to gold. But, gold never failed to serve its role as a reliably stable standard of value.

"The only adequate guarantee for the uniform and stable value of a paper currency is its convertibility into specie [gold or silver] — the least fluctuating and only universal currency," said President James Madison, the primary author of the US Constitution. Today, much of the world wants a basis for their currencies that is stable in value, and also "universal" — that is, something everyone can agree on. Just as at Bretton Woods in 1944, there is only one thing that meets this need, and we all know what it is.

(--> GOLD baby !! But what happens to the value of my Treasuries, gulp)

<<<

---

>>> Global public debt hits record $92 trillion - UN report

by Jorgelina do Rosario

Reuters

July 12, 2023

https://www.msn.com/en-us/money/companies/global-public-debt-hits-record-92-trillion-un-report/ar-AA1dLyzw?OCID=ansmsnnews11

LONDON (Reuters) - Global public debt surged to a record $92 trillion in 2022 as governments borrowed to counter crises such as the COVID-19 pandemic, with the burden being felt acutely by developing countries, a United Nations report said.

Domestic and external debt worldwide has increased more than five times in the last two decades, outstripping the rate of economic growth, with gross domestic product only tripling since 2002, according to the Wednesday report, released in the run up to a G20 finance ministers and central bank governors' meeting July 14-18.

Developing countries owe almost 30% of the global public debt, of which 70% is represented by China, India and Brazil. Fifty-nine developing countries face a debt-to-GDP ratio above 60% - a threshold indicating high levels of debt. (US debt/GDP is 130%!!)

"Debt has been translating into a substantial burden for developing countries due to limited access to financing, rising borrowing costs, currency devaluations and sluggish growth," the UN report added.

Furthermore, the international financial architecture made access to financing for developing countries both inadequate and expensive, the UN said, pointing to net interest debt payments exceeding 10% of revenues for 50 emerging economies worldwide.

"In Africa, the amount spent on interest payments is higher than spending on either education or health," the report found with 3.3 billion people living in countries that spend more on debt interest payments than on health or education.

"Countries are facing the impossible choice of servicing their debt or serving their people."

<<<

---

BRICS currency in August - >>> Rickards Drops Bombshell

BY JAMES RICKARDS

JUNE 6, 2023

https://dailyreckoning.com/rickards-drops-bombshell/

Rickards Drops Bombshell

On Aug. 22, about 2½ months from today, the most significant development in international finance since 1971 will be unveiled.

It involves the rollout of a major new currency that could weaken the role of the dollar in global payments and ultimately displace the U.S. dollar as the leading payment currency and reserve currency.

It could happen in just a few years.

The process by which this will happen is unprecedented, and the world is unprepared for this geopolitical shock wave.

This monetary shock will be delivered by a group called the BRICS.

The acronym BRICS stands for Brazil, Russia, India, China and South Africa.

This play for global reserve currency status by the BRICS will affect world trade, direct foreign investment and investor portfolios in dramatic and unforeseen ways.

The most important development in the BRICS system concerns the expansion of BRICS membership. This has led to the informal adoption of the name BRICS+ for the expanded organization.

There are currently eight nations that have formally applied for membership and 17 others that have expressed interest in joining. The eight formal applicants are: Algeria, Argentina, Bahrain, Egypt, Indonesia, Iran, Saudi Arabia and the United Arab Emirates.

The 17 countries that have expressed interest are: Afghanistan, Bangladesh, Belarus, Kazakhstan, Mexico, Nicaragua, Nigeria, Pakistan, Senegal, Sudan, Syria, Thailand, Tunisia, Turkey, Uruguay, Venezuela and Zimbabwe.

There’s more to this list than just increasing the headcount at future BRICS meetings.

If Saudi Arabia and Russia are both members, you have two of the three largest energy producers in the world under one tent (the U.S. is the other member of the energy Big Three).

If Russia, China, Brazil and India are all members, you have four of the seven largest countries in the world measured by landmass possessing 30% of the Earth’s dry surface and related natural resources.

Almost 50% of the world’s wheat and rice production as well as 15% of the world’s gold reserves are in the BRICS.

Meanwhile, China, India, Brazil and Russia are four of the nine highest-population countries on the planet with a combined population of 3.2 billion people or 40% of the Earth’s population.

China, India, Brazil, Russia and Saudi Arabia have a combined GDP of $29 trillion or 28% of nominal global GDP. If one uses purchasing power parity to measure GDP, then the BRICS share is over 54%. Russia and China have two of the three largest nuclear arsenals in the world (the other leader is the United States).

By every measure — population, landmass, energy output, GDP, food output and nuclear weapons — BRICS is not just another multilateral debating society. They are a substantial and credible alternative to Western hegemony.

BRICS acting together is one pole of a new multipolar or even bipolar world.

When the new currency launch is announced in August, the currency will not fall on an empty field. It will fall into a sophisticated network of capital and communications. This network will greatly enhance its chances of success.

The BRICS are also developing an optical fiber submarine telecommunications system that would connect its members. It is being developed under the name BRICS Cable. Part of the motivation for BRICS Cable is to foil spying by the U.S. National Security Agency on message traffic carried through existing cable networks.

What’s behind this quest to ditch the dollar? In no small part the answer is U.S. weaponization of the dollar through the use of sanctions.

On numerous occasions from 2007–2014, I warned U.S. officials from the Treasury, Pentagon and intelligence community that overuse or abuse of dollar sanctions would lead adversaries to abandon the dollar to avoid the impact of sanctions.

Such abandonment would lead to the diluted potency of sanctions, unforeseen costs imposed on the U.S. and eventually to the collapse of confidence in the dollar itself. These warnings were mostly ignored.

We have now reached the first and second stages of this forecast and are dangerously close to the third.

For years, the U.S. has used sanctions to punish nations like Iran. But the sanctions the U.S. and its allies imposed on Russia after it invaded Ukraine last year went far beyond previous sanctions regimes. They were unprecedented.

Many other nations began to conclude that they could be next if they run afoul of the U.S. on certain issues. And that fear has greatly accelerated the push to opt out of the dollar system entirely.

This desire is not limited to current targets such as Russia but is shared by potential targets including China, Iran, Turkey, Saudi Arabia, Argentina and many others.

The BRICS+ present a realistic effort to de-dollarize global payments and eventually global reserves.

For years, I’ve argued that the dollar would remain the world’s leading reserve currency for longer than most people think.

But below, I show you why a new BRICS+ currency could greatly accelerate the demise of the dollar as the world’s leading reserve currency.

How could it happen so much faster than I previously thought? Read on.

The Coming Shock to the Global Monetary System

By Jim Rickards

The global desire to move away from the dollar as a medium of exchange for international trade in goods and services is hardly new. The difference today is that it’s gone from a discussion point to a novelty to a looming reality in a remarkably short period of time.

Dubai and China have recently concluded an arrangement whereby Dubai will accept Chinese yuan in payment for oil exports from Dubai. In turn, Dubai can use the yuan to buy semiconductors or manufactured goods from China.

Saudi Arabia and China have been discussing similar oil-for-yuan arrangements but nothing definitive has yet been put in place. These discussions are made complicated by Saudi Arabia’s long-standing petrodollar deal with the U.S. Still, some progress along these lines is widely expected.

China and Brazil have recently reached a broad-based bilateral currency deal where each country accepts the currency of the other in trade. Meanwhile, there’s a growing strategic relationship between China and Russia as the two superpowers jointly confront the United States. In the trading relationship between the two nations, Russia can pay in rubles for Chinese manufactured goods and other exports while China pays in yuan for Russian energy, strategic metals and weapons systems.

Yet all these arrangements may soon be superseded by a new BRICS+ currency, which will be announced in Durban, South Africa, at the annual BRICS Leaders’ Summit Conference on Aug. 22–24.

The currency will be pegged to a basket of commodities for use in trade among members. Initially, the BRICS+ commodity basket would include oil, wheat, copper and other essential goods traded globally in specified quantities.

In all likelihood, the new BRICS+ currency would not be available in the form of paper notes for use in everyday transactions. It would be a digital currency on a permissioned ledger maintained by a new BRICS+ financial institution with encrypted message traffic to record payments due or owing by participating parties. (This is not a cryptocurrency because it is not decentralized, not maintained on a blockchain and not open to all parties without approval.)

The latest information from the BRICS working groups is that this basket valuation methodology is encountering the same problems that John Maynard Keynes encountered at the Bretton Woods meetings in 1944.

Keynes initially suggested a basket of commodities approach for a world currency he called the bancor. The difficulty is that global commodities included in any basket are not entirely fungible (there are over 70 grades of crude oil distinguished by viscosity and sulfur content among other attributes).

In the end, Keynes saw that a basket of commodities is not necessary and that a single commodity — gold — would better serve the purpose of anchoring a currency for reasons of convenience and uniformity.

Based on the impracticality of commodity baskets as uniform stores of value, it appears likely that the new BRICS+ currency will be linked to a weight of gold.

This plays to the strengths of BRICS members Russia and China, who are the two largest gold producers in the world and are ranked sixth and seventh respectively among the 100 nations with gold reserves.

These and related developments are frequently touted as the “end of the dollar as a reserve currency.” Such comments reveal a lack of understanding as to how the international monetary and currency systems actually work.

The key mistake in almost all such analyses is a failure to distinguish between the respective roles of a payment currency and a reserve currency. Payment currencies are used in trade for goods and services. Nations can trade in whatever payment currency they want — it doesn’t have to be dollars.

Reserve currencies (so-called) are different. They’re essentially the savings accounts of sovereign nations that have earned them through trade surpluses. These balances are not held in currency form but in the form of securities.

When analysts say the dollar is the leading reserve currency, what they actually mean is that countries hold their reserves in securities denominated in a specific currency. For 60% of global reserves, those holdings are U.S. Treasury securities denominated in dollars. The reserves are not actually in dollars; they’re in securities.

As a result, you cannot be a reserve currency without a large, well-developed sovereign bond market. No country in the world comes close to the U.S. Treasury market in terms of size, variety of maturities, liquidity, settlement, derivatives and other necessary features.

So the real impediment to another currency as a reserve currency is the absence of a bond market where reserves are actually invested. That’s why it’s so difficult to displace Treasuries as reserve assets even if you wanted. Again, no country in the world can come close to the U.S. in that regard.

But here’s where it gets interesting, and why the dollar could lose its leading reserve status much faster than previously thought.

That’s because the BRICS+ currency offers the opportunity to leapfrog the Treasury market and create a deep, liquid bond market that could challenge Treasuries on the world stage almost from thin air.

The key is to create a BRICS+ currency bond market in 20 or more countries at once, relying on retail investors in each country to buy the bonds.

The BRICS+ bonds would be offered through banks and postal offices and other retail outlets. They would be denominated in BRICS+ currency but investors could purchase them in local currency at market-based exchange rates.

Since the currency is gold backed it would offer an attractive store of value compared with inflation- or default-prone local instruments in countries like Brazil or Argentina. The Chinese in particular would find such investments attractive since they are largely banned from foreign markets and are overinvested in real estate and domestic stocks.

It will take time for such a market to appeal to institutional investors, but the sheer volume of retail investing in BRICS+-denominated instruments in India, China, Brazil and Russia and other countries at the same time could absorb surpluses generated through world trade in the BRICS+ currency.

In short, the way to create an instant reserve currency is to create an instant bond market using your own citizens as willing buyers.

The U.S. did something similar in 1917. From 1790–1917, the U.S. bond market was for professionals only. There was no retail market. That changed during World War I when Woodrow Wilson authorized Liberty Bonds to help finance the war.

There were bond rallies and Liberty Bond parades in every major city. It became a patriotic duty to buy Liberty Bonds. The effort worked, and it also transformed finance. It was the beginning of a world where everyday Americans began to buy stocks, bonds and securities as retail investors.

If the BRICS+ use a kind of Liberty Bond patriotic model, they may well be able to create international reserve assets denominated in the BRICS+ currency even in the absence of developed market support.

This entire turn of events — introduction of a new gold-backed currency, rapid adoption as a payment currency and gradual use as a reserve asset currency — will begin on Aug. 22, 2023, after years of development.

Except for direct participants, the world has mostly ignored this prospect. The result will be an upheaval of the international monetary system coming in a matter of weeks.

<<<

---

Ever closer to CBDC, cashless society - >>> India's culling of its 2000-rupee notes is driving hoarders to realty and gold

Quartz

by Mimansa Verma

May 22, 2023

https://finance.yahoo.com/news/indias-culling-2000-rupee-notes-084500521.html

India has witnessed a spurt in demand for gold since the Reserve Bank of India (RBI), last week, announced that the 2,000-rupee currency notes will be pulled out of circulation.

These high-value notes must be deposited in bank accounts or exchanged for other denominations by Sept. 30, the RBI declared on May 19. It has set a deposit limit of Rs 20,000 per day starting tomorrow (May 23).