News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

#SKF: AFTER TODAY THE BANKING SECTOR IS COOKED... $12... LOAD'EM UP

$12... LOAD'EM UP

News talking massive EV sectors job layoffs, Macys closing stores, financial crisis .... is it finally time?

The FED keeps smashing the interest rate, the problem isn't going away!

I miss Rick Santelli pounding the table, telling all those that refused to listen, telling them the financials were is very bad shape.

Are we there again? Could well be!

Snagged some shares a bit ago, Scotty.

Banks going to get clobbered next week?

#SKF: HERE WE GO WAR.... $20

#SKF: LOOKING LIKE IT'S TIME AGAIN.......... $20.23

#SKF: EASY 100% GREEN COMING HERE... $22.23

BIGGER CRASH THEN 2008....!

#SKF: FIRST BAG IN THE BANK .. $18.23

Certainly looks like things may be heading in that direction. I have a short list of inverse funds in many sectors. Going in heavy when a full on downturn confirms.

#SKF: ABOUT TO BREAK OUT... $9.23

Is it time yet? Rumors have the fed raising rates in a few months.

#SKF:THE BANKS WILL FAIL UNTIL THE NEXT $TBTF BAIL OUT...1

$SILVER_TO_THE_MOON...

https://investorshub.advfn.com/boards/profilem.aspx?user=373219

https://new.reddit.com/r/Wallstreetsilver/

https://www.reddit.com/r/SilverSqueeze/

https://new.reddit.com/r/Silverbugs/

#SKF: $WTF: Rehypothecated Leverage...!

Rehypothecated Leverage: How Archegos Built A $100 Billion Portfolio Out Of Thin Air... And Then Blew Up

It's also why when the next major hedge fund implosion does happen, it will be far more catastrophic.

https://www.zerohedge.com/markets/rehypothecated-leverage-how-archegos-built-100-billion-portfolio-out-thin-air-and-then-blew

One week after the biggest, and most spectacular hedge fund collapse since LTCM, we now have an (almost) clear picture of how Bill Hwang’s Archegos family office managed to single-handedly make a boring media stock the best performing company of 2021, but then when its luck suddenly ended it was margin called into extinction, leading to billions in losses for the banks that enabled what Bloomberg has dubbed its "leveraged blowout."

Thanks to detailed reports by the Financial Times and Bloomberg, we now have the missing pieces to complete the picture of the biggest hedge fund implosion of the 21st century.

As a reminder, and as we previously discussed, we already knew how Archegos was building up stakes in its various holdings: unlike most other investors, the fund never actually owned the underlying stock or even calls on the stock, but rather transacted by purchasing equity swaps known as Total Return Swaps (TRS) or Certificates For Difference (CFD). Similar to Credit Default Swaps, TRS exposed Archegos to the daily variation margin on the underlying stock, and as such while the fund would benefit economically from increases in the underlying stock price (and, inversely, would be hit by price drops forcing it to put up more cash as margin any day the stock price dropped) it would never be the actual owner of record of the underlying stock. Instead, the stock that Archegos was long would be "owned" by its prime broker, the same entity that allowed it to enter into TRS in the first place. As such Archegos also never had any disclosure requirements, allowing it to transact completely in the dark while being fully compliant with SEC disclosure requirements - since it didn't own the underlying stock, Archegos did not have to disclose it. Simple and brilliant.

This part is important because the lack of a documented trail of ownership to Archegos is what enabled the entire Ponzi bezzle... and the staggering leverage the fund applied to its portfolio. Furthermore, well aware that there was almost no way to verify just how much of a given stock he owned, Hwang proceeded to have nearly identical positions with not one, not two but at least eight prime brokers (the final number is still being determined as more and more come out of the woodwork).

Not that Archegos prime brokers were completely clueless as to what was going on.

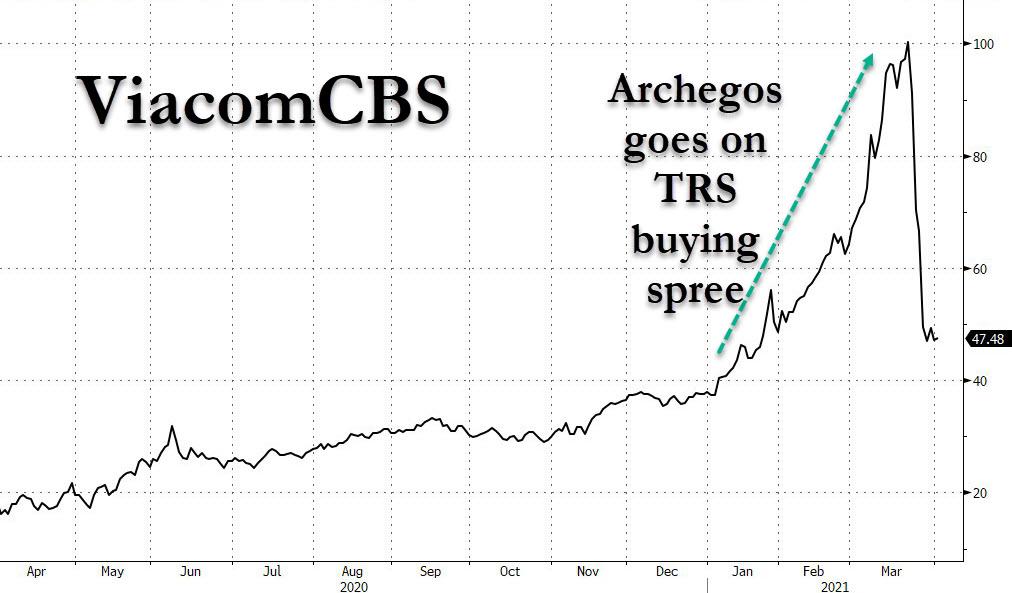

As Bloomberg reports, while much of the investing world watched in stunned silence how an "old media" company - ViacomCBS - shot up almost 300% in weeks, becoming the best performing stock in the S&P500 and prompting investors to speculate that the stock was was either undervalued, or like GameStop, or a takeover target, a handful of execs at Wall Street's top trading firms were aware of what was behind the move: it was Archegos Capital Management, who was building a massive position in ViacomCBS and a handful of other stocks... using leverage the same banks so generously offered with stock which the banks themselves technically owned!

But while banks around the world - from Goldman, Morgan Stanley and Wells in the US, to Credit Susse, UBS and Deutsche Bank in Europe, to Nomura and Mitsubishi UFJ in Japan - kept giving Hwang the leverage he needed to acquire more and more of the stock, until he became the biggest economic if not registered owner of Viacom, what they did not know - thanks to the was Total Return Swaps are structured - was the full extent of his wagers. Which were massive: he stealthily amassed $10 billion of Viacom.

Viacom was just one of many: using even more TRS and even more leverage across even more Prime Brokers, Archegos was able to place colossal wagers while avoiding the disclosures required of most investors. And so "almost invisibly" Hwang accumulated a portfolio which according to Bloomberg sources was as much as $100 billion!

Eventually, Archegos built positions in at least nine stocks that were big enough to rank him among the largest holders, fueled by a level of bank leverage that would have been unusual even for a hedge fund.

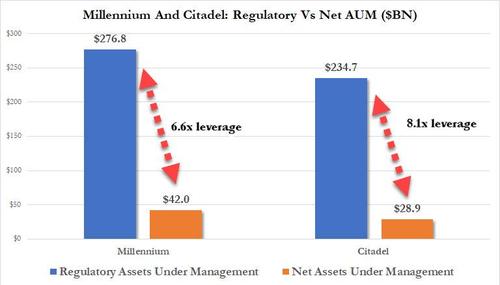

While we previously discussed the leverage aspect of Archegos strategy, here it is again: with Bill Hwuang managing approximately $10BN in assets under management, the multiple Total Return Swaps with unwitting prime brokers allowed the fund to build up a staggering $100 billion in positions, implying a huge 10x leverage. This is the kind of leverage one associated with the likes of financial titans like Citadel and Millennium, not a smallish family office which has zero downside protection (as we would eventually learn).

What is amazing about this unilateral Ponzi scheme is that it relied on what we have dubbed rehypothecated leverage: the fund never even owned the underlying stock which was layered with billions in generous Prime Broker debt, but it was Archegos' Prime Brokers who not only would own the actual stock but would also allow Hwang to add tens of billions in leverage... on an asset that they owned!

What is also remarkable is that Archegos' ponzi scheme could have continued indefinitely if only Viacom stock had i) continue to rise or ii) avoided a crash. After all, having ignited the initial upward moment, Archegos had effectively forced benchmark-tracking investors, exchange-traded funds, CTAs and other momentum investors to buy as well.

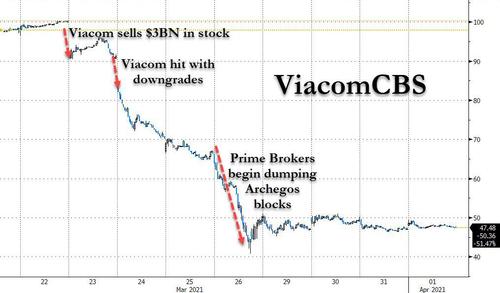

Sadly for Hwang (and his Primer Brokers) the upward momentum ended with a bang last Monday, when with its shares trading at $100, Viacom announced a $3BN stock sale, which hammered the stock, followed by a round of analyst downgrades, which sent the stock tumbling. It was at this point that Archegos was now facing tens of billions in margin calls on its VIACA Total Return Swaps from its Prime Brokers.

And therein lies the rub, because when the time came to unwind the Archegos Ponzi, the Prime Brokers' counterparty was not Archegos but other Prime Brokers. This is what led to the infamous meeting late last Thursday, where a bunch of PBs tried to reach an amicable resolution ahead of Friday's bloodbath. As Bloomberg adds, at several points during those exchanges, bankers implored Hwang to buy himself breathing room by selling some stocks and raising cash to post collateral. But "he wouldn’t budge."

As a result, Morgan Stanley and Goldman promptly started dumping blocks of stock backing Archegos TRS in the open market. In doing so the started a margin call liquidation, in which those who sold first - like Goldman, Morgan Stanley and Deutsche - would avoid massive losses, while those who waited like Nomura and Credit Suisse... would not. Indeed, we already knew that Nomura, Japan’s largest investment bank, said its losses could hit $2Bn, while losses at Credit Suisse could be as large as $4Bn according to the FT.

At this point, many questions popped up, especially (and belatedly) inside the banks themselves: as the FT reports, executives within the prime brokerage divisions of at least two banks "are being quizzed by risk managers over why they offered a business as small as Archegos tens of billions of dollars of leverage on trades in volatile equities through swaps contracts,."

As the FT further notes, echoing what we said above, while prime brokerage clients typically provide few details about their other trading activities, "executives from at least two of the six banks are investigating whether Hwang deliberately misled them or withheld vital information about mirror positions he had built up at rival banks, according to people involved in the probes."

Well, no: Archegos did not mislead anyone. He simply used (and abused) a system where - as we put it - one investor can create as much rehypothecated leverage as the investors' banks and Prime Brokers will allow him. In this case we know the number may have been as high as a mindblowing $90 billion.

Naturally, had the banks known that in a worst case scenario they would be facing other banks - since such replicated, or rather rehypothecated position would magnify the risks on each of the trades making a bank less likely to extend so much credit against them - none of this would have been possible. However, as long as everything was going up, and all of Archegos positions were pleasasntly surging nobody seemed to care... or bother to calculate just how big the downside risk was (one can thank the Fed Put for that).

One final remarkable aspect of this whole story is that this is not Hwang's first crisis. In 2012 he submitted a guilty plea on behalf of his hedge fund to a charge of wire fraud, and he resolved related civil claims of insider trading without admitting or denying wrongdoing. Archegos is the family office he formed after winding down that firm, Tiger Asia Management.

However, as if nothing had ever happened, prime brokerages immediately began lining up to help the new business. Morgan Stanley was among his early backers. Deutsche Bank signed him as a client at the urging of at least one senior executive, according to Bloomberg, "who was unperturbed by the insider-trading taint and didn’t believe Hwang had done anything wrong, according to a person familiar with that decision." Ironically, just a few years later, Hwang did something wrong and it would prove to be the biggest hedge fund collapse in post-LTCM history.

Not every bank acted like an idiot: one firm resisted the lure. Archegos approached JPMorgan sometime between 2016 and 2018 and was rebuffed, according to the Bloomberg report. At the time, JPMorgan was still revamping the equity prime-brokerage unit it had acquired with Bear Stearns during the 2008 financial crisis. "Dumb luck or not, the bank dodged a bullet."

* * *

The rest of the story is mostly known, so now what.

Well, as we first hinted and as Bloomberg reports, already regulators are dropping hints of new rules to come, with SEC officials signaling to banks that they intend to make trading disclosures from hedge funds a higher priority, while also finding ways to address risk and leverage.

Senior finance executives acknowledge that a crackdown of some form, whether on borrowing or transparency or both, is inevitable.

Amusingly, and picking up on the FT's reporting, Bloomberg also notes that while some of those firms have disclosed the financial impact of their roles in the Archegos collapse, none is willing to comment on how or why they enabled Hwang to become such a force in the market. After all what can they say: "the other guys vetted him, so we assumed he was clean"...

There are also questions whether Hwang’s counterparties knew about his relationships with other banks and the scale of the leverage he was using for what appear to be concentrated positions in a handful of companies. And - more ominously - if they did not know anything about his exposure, why the hell not? As we reported on Tuesday, JPMorgan (which successfully managed to avoid this scandal completely) estimated that the Prime Brokers facing Archegos may end up absorbing as much as $10 billion in combined losses.

Already credit rating agencies have downgraded outlooks for Credit Suisse and Nomura, citing concerns over “the quality of risk management” while activist investors are demanding better governance and would not mind if senior execs were summarily fired over this episode to restore confidence.

"Risk controls still are not where they should be," David Herro, one of Credit Suisse’s biggest shareholders, said Wednesday in a Bloomberg TV interview. "Hopefully, this is a wake-up call to expedite the cultural change that is needed in this company."

But going back to Bloomberg's original point, for all their silence the prime-brokerage units of Nomura, Goldman Sachs, Morgan Stanley, Credit Suisse and others, had clues about what Archegos was doing. These firms knew about the trades they had financed, of course, and also had some visibility into his total borrowings. And yet they didn't bother to ask about what, if any, risk management was being implemented to avoid an uncontrolled unwind. Or rather, the questions emerged only after the margin call.

What the Prime Brokers also didn't know is that Hwang was taking parallel positions at multiple firms, piling more leverage onto the same few stocks, which brings us back to our rehypothecated leverage concept which we are confident we will use much more in the coming months, especially since "unwinding a series of large, leveraged bets placed by a single account is one thing; doing so when rival banks are liquidating the same positions held by the same client is quite another."

Archegos' own "Lehman moment" came late on March 25 when Hwang’s prime brokers met again and discussed the possibility of standing down temporarily to let tensions ease, as we reported previously, but any attempt at solidarity proved short-lived: shortly after some PBs sent Archegos notices of default, clearing the way for Goldman and Morgan Stanley to dump Hwang's positions.

“Hopefully this will cause the prime brokerages of regulated banking organizations (and their supervisors) to re-assess their relationships with highly leveraged hedge funds,” former FDIC chair Sheila Bair tweeted.

A few silver linings: no one is talking about bailing out its counter-parties and hopefully this will cause the prime brokerages of regulated banking organizations (and their supervisors) to re-assess their relationships with highly leveraged hedge funds.

— Sheila Bair (@SheilaBair2013) March 31, 2021

She is, of course, wrong.

In fact, if anything we expect Prime Brokers will make leverage even easier to obtain for non-bank, hedge fund and family office clients, because the one big mistake Archegos (and its Prime Brokers) made was that it was not big and systemic enough to merit a Fed bailout. Now, if Archegos had a portfolio of $200 billion, $300 billion or more, while using Citadel's 50x leverage, now we're talking "size"... size enough for the Fed to step in and make everyone whole on the back of taxpayers... the same way the Fed bailed out Citadel, Millennium and Point72 in September 2019 during the repo crisis (as both Zero Hedge and subsequently Bloomberg, explained).

There is another reason nothing will change: hedge funds, Prime Brokers, banks - in fact the Fed itself - are all incentivized to not look at what skeletons may be found in the closet. Why? Because if the banks are forced to admit that there are more Archegos funds - and there are countless - Prime Brokers will have no choice but to sequester collateral from more clients, sparking more margin calls, leading to more stock liquidations, and resulting in even bigger investor panic. Call it a side effect of building castles on crooked foundations in an artificial, fake, Fed-supported market.

Is another market panic what the Fed wants? Or what the Biden admin wants? Of course not.

Which is why we will get a token Congressional hearing where politicians care more to hear themselves talk than listen to the answers, the banks will slap a few hands, one or two small sacrificial hedge funds will be shut down, and the world will move on, especially once Archegos is no longer on the front page of the financial media.

It's also why when the next major hedge fund implosion does happen, it will be far more catastrophic.

#SKF: THE CENTRAL BANKS ARE LOSING CONTROL...

https://www.thisismoney.co.uk/money/investing/article-9380315/Royal-Mint-customers-charged-thousands-stock-gold-bars-coins.html

#SKF: THE END OF FIAT MONEY IS NEAR.. 12.38

https://www.metalsdaily.com/

#SKF: THE TIME TO ADD IS NOW $12.38

https://new.reddit.com/r/wallstreetbets/comments/m8vb94/federal_reserve_to_end_emergency_capital_relief/

Federal Reserve to End Emergency Capital Relief for Big Banks

https://scontent.fmia1-2.fna.fbcdn.net/v/t1.0-9/163195191_10159219522749134_1946140902423842506_n.jpg?_nc_cat=105&ccb=1-3&_nc_sid=730e14&_nc_ohc=wJFuN9r1gGcAX_ousQT&_nc_ht=scontent.fmia1-2.fna&oh=da9af1be1182c0f60d1ee6d8824c6ac9&oe=607D3173

#SKF: TIME TO LOAD A FEW SHARES...

I am astounded how well this fake money printing machine has managed to keep the wheels turning. Every inverse fund is just prime pickings right now. If reality sets in one day, they all will make shareholders a lot of money. Real estate is way overdue for a massive crash as well.

Many moons ago, I went into this one at around $20 before it spiked to around $250. Looking at a far back chart, that would have been where the $4000+ peak is in early 2009. If we get a major crash and duplicate that move ....... but the dollar has to survive or you have a major gain worth nada.

I am continuously adding this and others as well buy low sell high price target is $1000 a share

I’m sure it’s going to end in tears eventually

How long can this economy last? Are the banks protected enough? Is this prime for a huge gain? Keeping a very close eye on this and other inverse funds.

HELLO! Hello ello lo ANYBODY paying attention to financials and considering going short via these inverse funds? Or are there better ways to trade short outside of straight up shorting?

A killing was made some years ago. I banked a bunch and left a lot more on the table with this one.

Weekly chart 50ma line first stop.. Might flirt with that a while as seen before.

If many millions die than we will see value loss over all imho..

be careful out there imo.

These ETFs will help you prosper in financials

Commentary: Faltering financial sector can still offer opportunity

BEND, Ore. (MarketWatch) — Locked in a confirmed bear market, the financial sector continues to lag and be a drag on major market indexes. Global threats to this important sector abound, but exchange-traded funds can offer unusual investment possibilities for our extraordinary times.

The Fundamental Edge

The financial sector is obviously a significant factor in the global and U.S. economy as “money makes the world go ‘round” and the financials are the second largest sector in the Standard & Poor’s 500 after technology. The sector’s poor performance over recent months has been troubling, to say the least, as many analysts say that a convincing economic and investment recovery cannot be sustained without financial sector participation.

However, this all-important sector faces significant risks and problems, both at home and abroad, and these negatives cast a shadow over today’s tenuous economic landscape.

In Europe, the banking problems are well documented as the euro zone grapples with the threat of sovereign debt default and the devastating impact such an event or multiple events would have on banks across the continent.

This week promises another installment in the European drama as investors respond to last week’s “stress tests,” Spanish and Italian bond yields soar, and this Thursday’s emergency summit regarding Greece’s rescue promises to be a wild and wooly affair as they struggle to avoid a Continental “Lehman event.”

Lest we think that this is just a “European problem,” the threat of “contagion” is real as major U.S. banks have exposure to European debt to the tune of billions of dollars. For example, Citigroup reported on Friday that it has $13 billion in exposure to Portugal, Italy, Ireland, Greece and Spain, or PIIGS. See: Citigroup makes progress on bad loans.

On the home front, major U.S. banks hold significant positions in U.S. Treasury debt and a default or downgrade here would almost certainly create additional negatives for financial sector performance. The top five banks in the United States (Citigroup, Bank of America , Goldman Sachs , Morgan Stanley , and J.P. Morgan Chase ) have billions in exposure to the U.S. Treasury market and so are large stakeholders in the outcome of the U.S. debt ceiling debate. See: JP Morgan, Goldman, Treasuries and default.

On the consumer front, Friday’s significant drop in the June University of Michigan Consumer Sentiment gauge to 63.8 from 71.5 casts a deeper pall on the financial sector as retail banking and real estate continue to founder. To highlight that point, J.P. Morgan’s earnings announcement included a profit decline of more than 40% in its retail banking business. See: J.P. Morgan profit rises 13%, tops target.

Finally, earnings reports last week for J.P. Morgan and Citigroup beat expectations, but both of the financial giants finished down on Friday and are down substantially year to date. Declining prices on better than expected earnings announcements are never a good or positive development.

We’ll see more earnings reports this week from big players including Wells Fargo, Bank of America, Goldman Sachs and Morgan Stanley. While we very well could see positive reports, one must keep in mind that many of these behemoths still trade far below their pre-crisis highs. For example, Citigroup closed at $38.38 on Friday compared to more than $500/share in the summer of 2007 and Bank of America, trading at less than $10/share and down from its lofty peak in the mid-fifties, today looks more like a small cap than a global giant.

The Technical Edge

As always, the charts tell the story:

In the charts of the three major banks above, we see a similar, disheartening picture. All three are below their 50-day and 200-day moving averages indicating bear market status from a technical perspective, and the two widely watched averages have also formed a “death cross,” wherein the 50-day average has crossed below the 200-day. Furthermore, declines in the neighborhood of 15% from recent highs would qualify at least as significant corrections.

To no one’s surprise, the Financials Select SPDR ETF exhibits similar patterns.

The ETF Edge

So, as the bear prowls this all important corner of Wall Street, retail investors like you and me can also use exchange-traded funds to seek profits should this dismal trend continue.

One can deploy put options on the Financials Select SPDR ETF and a technique I’ve found useful here is to buy put options that are “at” or “in the money,” and with expiration dates far in the future to partially mitigate the time decay inherent in options positions. This then becomes a trend following position using an option instead of the underlying ETF that offers increased profit potential while keeping it simple, which option trading generally isn’t found to be.

A second technique suitable for cash accounts would be to simply “short” XLF. The ETF is widely traded and liquid and so this is a very valid strategy in today’s volatile markets.

Another possibility would be to use inverse exchange-traded funds in the financial sector, which are designed to increase in value as the underlying indexes decline. These inverse funds must be fully understood as they are designed to replicate the one day performance of the underlying index and so can develop significant tracking error that can work either for or against you.

Two of the most popular inverse ETFs are (SEF) ProShares Short Financials , and (SKF) Proshares UltraShort Financials , which offers two times the inverse movement to the Dow Jones U.S. Financial Index and could be interesting for more aggressive investors.

One day, I’m quite certain that the Financial Sector will rise from the ashes like the mythical Phoenix, the firebird that rises, reborn, to live forever. In fact, I believe that in future years, the Financials will be a “super sector,” because, after all, money makes the world go around, and the Federal Reserve and European Central Bank will move heaven and earth in an attempt to ensure that the “too big to fail” banks, in fact, don ‘t fail.

But the day of the Phoenix is not today.

Instead, as we move into the lazy, hazy and sure to be crazy days of summer, opportunities abound even as the bear prowls the global economy and the crucial financial sector continues to struggle. Knowledgeable and disciplined investors need not despair, because through the flexibility and versatility of exchange-traded funds, we now have new weapons available to help us successfully navigate our uncertain and extraordinary times.

Disclosure: Wall Street Sector Selector holds positions in SKF and SEF and a put option position in XLF. Wall Street Sector Selector (wallstreetsectorselector.com)actively trades a wide range of ETFs and positions may change at any time.

It put in a double bottom and reversed direction, looks like an xlent time to jump in, especially with everything that is hitting the fan, or about too.

~ $SKF ~ Possibly going long scan results (Daily and Weekly) for for the week of March 1st 2012 - Daily and Weekly views.

Chart results for you to ponder with me.. These are technical scans only, Click next or previous at the top of the page to see my others. Twitter: @MACDgyver ---> SKF <---

Chart results for you to ponder with me.. These are technical scans only, Click next or previous at the top of the page to see my others. Twitter: @MACDgyver ---> SKF <---

Keyword: MACDscan ----> http://tinyurl.com/MACDscan

SKF made me some serious cha ching on days like today. Stayed tuned folks....more to come.

GOLDGUY111

Phase Two Of Greater Depression II Begins Now

We all know what caused the 2008 banking crisis killing Lehman and others. It was reckless lending, too low interest rates, loosy-goosy credit for consumers and most of all, instigation of derivatives by greedy bankers hungry to make billions on the quick. Now that central banks have bailed them out of their insolvency and replenished minimum capital standards by stealing TARP funds from taxpayers, we find the next LARGER MESS looming on the horizon. Governments grasping for tax income will be grubbing, and taking all at a new furious pace. Consumers that are able will simply drop-out of the system and down-size.

If you thought Lehman was fun get ready to see new price controls and acceleration of existing capital controls, with inflation that will knock your socks off. We have at least two to five more years of crash and burn in the financial markets before a new base is found. Then, toxic trade policies and old grudges open the door to a new World War, which obviously no one can afford. This is simply historical fact and not any wild forecasting by me although some may consider me crazy.

Many of the very large global banks will be nationalized and some will fold into insolvency or merger. Roughly 90% of the derivatives and real estate toxic paper trash remains hidden on banker balance sheets. Not only was the problem never fixed, they’ve been piling on more bad loans-paper at a furious pace. The Banker’s Motto is “Steal while you can. You never know when the party ends.”

Credit is the life blood of any positive economy. Yet, lending to commercial companies is almost non-existent. Further, the administration is piling on new and higher costs in health care, payroll taxes, benefit costs and SS withholding, crippling the only real source of new jobs and employment-small business. There is no strong, positive engine of growth on the horizon except precious metals and commodities trading and investing.

What few have noticed is the current inability of banks, bankers and investment banks to make any income. In a depression, income becomes paramount. Banks’ ability to earn money is diminishing on all fronts; credit cards, corporate loans, investment banking, commercial banking, real estate, and of course consumer loans for toys and stupid junk that composes 70% of the entire USA consumer spending economy. If Paulson and Bernanke had not conspired to give bankers TARP and other stolen billions, the big banks would now be insolvent.

Banks are stuck with earning a puny 1-3% on the stolen TARP funds they have invested in US Government paper. When the bond market tanks, that stolen cash is toast and so it will be with their 3% earnings. How fitting is that? Paybacks!

The losses are so beyond comprehension they simply cannot be measured due to derivatives and credit default swaps. Yes, the swaps are allegedly insured but the counter-parties simply have no hope of paying what they owe. They will be overwhelmed and the scary fall-out can only be broadly considered and not even estimated. For now, it’s all hiding in the back rooms of banks. If the mark-to-market they are insolvent.

American commercial and residential real estate is wrecked for two decades. Property ownership, banks, credit unions, title companies, loans, lender loan ownership and ability to pay are all simply destroyed.

Corporate insiders, CEO’S, presidents, and other officers have been selling gobs of stock at a rate we last heard of as 1600 to 1. That’s 1600 shares sold for each one purchased. Mr. Ballmer, chief honcho at Microsoft is dumping well over $1 billion as we speak…that is only one example. Others are selling entire companies, some taking a lifetime to build, in order to cash out and run with the money.

These people know exactly what is coming. Insurance companies thrive and live on earnings from investments they make using policy holders’ cash. If commercial real estate sinks some more, as we think it will, it’s adios income for the insurers. Further, policy holders, having paid into whole life, will cash them out to live; taking capital out of the insurance companies’ till. This further removes insurance company balance sheet cash.

The next big government taking will be to steal the pension pools of national and international corporations. This is the last remaining honeypot for government theft and has already been practiced in South America.

Those companies that are smart and can see it coming are off-shoring piles of assets, cash and investment paper to keep it away from the takers. How this can work out, lord only knows.

Individuals holding pensions and government paper will wake-up one morning to find its all been seized and piled into 30-year USA bonds, which are sinking like the Titanic. There will be no buyers and no exits for those assets. The owners could get totally wiped out. We strongly suggest you plan accordingly while being very careful. Old rules will not apply any longer. Bonds stink and they are getting stinky-er.

The real estate industry is such a tangled web of messes, the government plan (in our view) is to gather all the bad loan paper into Fannie and Freddie over the next 2-3 years. Congress gave them an open check book to buy as much garbage as possible. At the appropriate moment, the F&F’s will be forced into bankruptcy and presto, all the bad stuff goes away.

If this is true, we wonder, where does this leave the banks and home owners’? Do the banks get paid twice? No surprise to us if this happens. Would the homeowners be free and clear…interesting dilemma? Who owns the properties? Who owns the loans? How would you like to be in the title insurance business guaranteeing all the suspect properties?

The 4th quarter sales period for larger retailers, department stores and big box stores is when they make their entire year. One bad 4th quarter can take them down. We hope they have at least a decent quarter and can remain in business. Some of them after the January, 2011 returns and mark-downs will be filing bankruptcy. We forecast only a minimum of Xmas spending by Americans as a final result. By February, we’ll see who’s headed to the BK courts. Sales are mildly stronger but profits are toast on these give-aways.

We got the news today that the massive A&P grocery chain intends to file bankruptcy as early as Monday, December 13, 2010.

If the Congress fails to pass the Bush tax cut extensions before Christmas 2010, we forecast the later January, 2011 broader market selling cycle will occur before the end of December to reduce taxes.

QE2 Presents Our Largest Global Disaster.

We said years ago after the derivative mess and negative housing news came to light that Bernanke would have only one chance; and that is to print phony money and paper. This is exactly what he is doing and will continue to do until the financial system implodes.

Keep in mind the USA is the worst culprit originating digital cash and paper. China and Japan have had enough. They are sellers not buyers and further, they are beginning to produce the same problems in their own currencies and bonds. Japan’s central banker said yesterday he plans to overwhelm their system with QE2 that could make Chopper Ben’s paper dump appear to be play-school. Not too smart to say it.

System weaknesses we see are (1) A Chinese real estate bubble is popping and taking down their stock markets. Fallout from this will cause a chain reaction moving into other markets in Europe, Asia and North and South America. It doesn’t take a genius to figure out where this race to the bottom goes next. (2) First we get capital controls, price controls and then inflation. This produces some real economic pain and struggle. (3) However, the last phase is the really bad one-hyperinflation!

The first inflation phase is followed by hyperinflation and then a banking-system collapse. It’s not the end of the world as life goes on; but for millions of spoiled American brats; they will simply not be able to cope. They’re headed for major denial, and all kinds of social problems. It’s too bad it’s come to this as created by a bunch of greedy bankers and One-Worlder’s. It’s not nice to say but we wish them the worst and no mercy. They have literally destroyed our entire economic world for decades.

In the 1919-1923 European hyperinflation following WW I, hundreds of bankers and politicians were simply assassinated. (Read the book “When Money Dies” by Adam Fergusson). Could this possibly come again? We hope not but keep in mind Americans own millions of guns. When these people get very angry after being totally cleaned out, you tell me what happens next?

Most of these problems have been caused and created by the US Federal Reserve. This is a private banker enterprise not the US Government. We suggest that before all this is over, that bunch of snakes will be eliminated for good-one way or another. Never, until recently, since the birth of this gang in 1913, have there been so many responsible, authoritative calls and demands to first investigate them and second, shut them down for good. Its unfortunate the Federal Reserve born in 1913 could not have been still-born.

My beloved country and those throughout the world can manage to pass through this huge economic trauma. Our largest concern is for the freedom and liberty of America. Who will be in charge after this ends? What will be the fallout? Can we simply return to a strict U.S. Constitution and Bill of Rights? Or, will we be stuck with something much different? What happens to the dollar? What happens to other currencies?

One way or the other, I believe Americans will fight and struggle for what is fair and correct. Those that choose another path will pay the price. I am a non-violent journalist, a reporter, an analyst, a trader, and a market forecaster. I am a student of economic history and somewhat rely upon the past to forecast our present. I just wish it could be different. Buckle-up for a rough ride, use common sense and you’ll be able to manage this adventure.

Roger Wiegand

Editor Trader Tracks Newsletter

I got an odd vibe that something is going to happen in germany...

http://www.dailymail.co.uk/news/worldnews/article-1277393/We-schmucks-Europe-German-medias-verdict-anger-Greek-bailout-swells.html

You have to take a look at this if XLF doesn't take out the year high on strong volume. Scaling in now makes sense. I hate to use due, but this a due for a bounce.

FML GS.. screwing my hedge over...

short financials now...

have it as a hedge to my position in a few bank stocks...

I'm worried about banks...

they have run hard fast... and not much has changed...

we still have huge unemployment

real estate is not looking like it's going to correct as quickly as some might want... and that first time home buyer credit doesn't look like it is going to be extended.

Also the government is looking to increase capital requirements, which no matter when they will do it will cut into future profits...

ULTRASHORT FINANCIAL(NYSEArca: SKF)

After Hours: 27.24 0.08 (0.29%) 7:59PM ET

Last Trade: 27.16

Trade Time: Aug 21

Change: 1.23 (4.33%)

Prev Close: 28.39

Open: 27.74

Bid: 27.01 x 300

Ask: 29.30 x 200

NAV¹: 28.32

Day's Range: 26.89 - 27.98

52wk Range: 26.89 - 303.82

Volume: 20,161,140

Avg Vol (3m): 30,569,400

YTD Return (Mkt)²: -59.43%

Net Assets²: 1.21B

P/E (ttm)²: N/A

Yield (ttm)²: 0.44%

skf sounds real nice for today.....

Thanks for that post... gonna check with my banker friend too.. you might just be right on here...

I dont think the banks are in trouble, I think they just moved up too fast and now fear is coming back into the market, It looks like the rally is over and the trend is down for now, faz moves too fast for anything but a day trade imo. skf isnt quite as volatile.

you thinking the banks are in trouble again?

im going to go long here first pullback, possibly tomorrow,

The banks are scams, too.

Yeah but the more I watch it and play it, the more I realize its a scam along with FAS and FAZ.

|

Followers

|

13

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

429

|

|

Created

|

11/15/07

|

Type

|

Free

|

| Moderators | |||

This short ProShares ETF seeks a return that is -2x the return of its underlying benchmark (target) for a single day, as measured from one NAV calculation to the next. Due to the compounding of daily returns, holding periods of greater than one day can result in returns that are significantly different than the target return and ProShares' returns over periods other than one day will likely differ in amount and possibly direction from the target return for the same period. These effects may be more pronounced in funds with larger or inverse multiples and in funds with volatile benchmarks. Investors should monitor their holdings as frequently as daily. Investors should consult the prospectus for further details on the calculation of the returns and the risks associated with investing in this product.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |