News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

>>> Tanzania orders gold dealers to reserve 20% for purchase by central bank

Reuters

September 28, 2024

News Africa Gold

https://www.mining.com/web/tanzania-orders-gold-dealers-to-reserve-20-for-purchase-by-central-bank/

Tanzania’s mining regulator has ordered all mining firms and traders exporting gold to allocate at least 20% of the commodity for sale to the central bank to bolster the bank’s move to diversify its foreign reserves.

The central Bank of Tanzania (BoT) began buying gold from local traders and miners in the last financial year that ended in June to boost its reserves amid depreciation pressure on the local currency, the shilling.

In the 12 months to June, the central bank bought 418 kg of gold to beef up its reserves and in the current financial year it intends to buy 6 metric tons of gold.

The regulator, the Tanzania Mining Commission, said late on Friday in a statement that the directive will take effect effectively on Oct. 1 as part of a newly enacted mining law.

Miners and traders, according to the statement, will be required to submit the reserved gold to two major mineral refineries, Eye of Africa Ltd in the capital Dodoma and Mwanza Precious Metals Refinery Ltd, located in the lake city of Mwanza in the north of the East African country.

“All payments will be done according to the Bank of Tanzania arrangements,” the statement said, without providing details on rates.

Tanzania’s foreign exchange reserves stood at $5.29 billion at the end of July, sufficient to cover 4.3 months of projected imports of goods and services.

<<<

---

Check out this graph showing the amount of precious metals derivatives held by commercial banks. It started moving up in 2019-21, and then exploded ~10 fold higher in 2022. These derivatives holders include JP Morgan, Citigroup, Goldman Sachs, etc, and their sudden interest in precious metals coincided with gold's big rise in recent years. The chart below only goes to 2022, but the extremely high level of precious metals derivatives held by these banks has apparently continued -

>>> And that trend in precious metals has continued. According to the most recent OCC report, in the first quarter of 2024, federally-insured banks held $438.60 billion in precious metals contracts. That figure is at least 12 times greater than the amount the same banks held in precious metal contracts in any quarter from 2007 through 2018. <<<

Full post - https://investorshub.advfn.com/boards/read_msg.aspx?message_id=175130195

---

Palladium - >>> Montana miner to lay off hundreds due to declining palladium prices

Associated Press

September 12, 2024

https://finance.yahoo.com/news/montana-miner-lay-off-hundreds-225135256.html

NYE, Mont. (AP) — The owner of the only platinum and palladium mines in the U.S. announced Thursday it plans to lay off hundreds of employees in Montana due to declining prices for palladium, which is used in catalytic converters.

The price of the precious metal was about $2,300 an ounce two years ago and has dipped below $1,000 an ounce over the past three months, Sibanye-Stillwater Executive Vice President Kevin Robertson said in a letter to employees explaining the estimated 700 layoffs expected later this year.

“We believe Russian dumping is a cause of this sharp price dislocation,” he wrote. “Russia produces over 40% of the global palladium supply, and rising imports of palladium have inundated the U.S. market over the last several years.”

Sibanye-Stillwater gave employees a 60-day notice of the layoffs, which is required by federal law.

Montana U.S. Sens. Steve Daines, a Republican, and Jon Tester, a Democrat, said Thursday they will introduce legislation to prohibit the U.S. from importing critical minerals from Russia, including platinum and palladium. Daines' bill would end the import ban one year after Russia ends its war with Ukraine.

The south-central Montana mine complex includes the Stillwater West and Stillwater East operations near Nye, and the East Boulder operation south of Big Timber. It has lost more than $350 million since the beginning of 2023, Robertson said, despite reducing production costs.

The company is putting the Stillwater West operations on pause. It is also reducing operations at East Boulder and at a smelting facility and metal refinery in Columbus. Leadership will work to improve efficiencies that could allow the Stillwater West mine to reopen, Robertson said.

The layoffs would come a year after the company stopped work on an expansion project, laid off 100 workers, left another 30 jobs unfilled and reduced the amount of work available for contractors due to declining palladium prices.

<<<

---

>>> Gold skyrockets as stars align for Fed rate cuts

Reuters

September 13, 2024

by Anushree Ashish Mukherjee and Swati Verma

https://finance.yahoo.com/news/gold-rallies-record-high-us-032818493.html

(Reuters) - Gold prices powered higher on Friday, beating record levels, as a boost in bullish momentum fueled by optimism that the U.S. Federal Reserve is on the brink of trimming interest rates was catalyzed by fund inflows and a drop in the dollar.

Spot gold was trading at record levels, up 0.9% at $2,582.04 per ounce by 1:45 pm ET (1745 GMT).

U.S. gold futures settled 1.2% higher to $2,610.70.

Gold market bulls are locking in bullion prices surging to fresh records, with a milestone of $3,000 per ounce coming into focus, fired up by monetary easing by major central banks and a tight U.S. presidential election race.

The stars are aligned in favour of the gold and silver market bulls as the European Central Bank lowered its main interest rate this week, the Fed is likely to lower it next week and tame U.S. inflation data, Jim Wyckoff, senior market analyst at Kitco Metals, said.

Markets fully price a rate cut next week, with a 57% chance of 25-bps U.S. rate cut and a 43% chance of a 50-bps cut, the CME FedWatch tool showed. This would be Fed's first rate cut since 2020.

"The market is still expecting the Fed to cut interest rates by around 100 basis points by the end of the year, i.e. rates would have to be cut by 50 basis points at one of the two remaining meetings after September," Commerzbank analysts said.

"It is therefore likely due to these aggressive interest rate cut expectations for the coming months that the gold price is rising."

Further driving interest in bullion, the dollar fell on Friday to its lowest level this year against the Japanese yen. [USD/]

Global physically backed gold exchange-traded funds saw a fourth consecutive month of inflows in August, the World Gold Council said last week.

Holdings of the world's largest gold-backed ETF SPDR Gold Trust were at their highest levels since early January on Thursday. [GOL/ETF]

From the technical point of view, the Relative Strength Index currently at 69 suggests that the gold price is approaching the "overbought" territory, starting at 70.[TECH/C]

Palladium rose 2% to $1,067.43 and has surged about 17% so far this week.

Spot silver rose 2.3% to $30.61 and platinum added 2.4% to $1,000.57.

<<<

---

DD....$PRECIOUS METALS - $Gold Breaking Out vs Commodities (Top Chart) As US Dollar Weakens (Bottom Chart)

$GOLD MINERS NEWS - $Gold now has a historical breakout vs US CPI. A very bullish chart for precious metals.

$Gold Has Also Broken Out vs CPI

The inflation-adjusted $gold price having a 44-year break out has absolutely massive implications going forward…

$15,000 GOLD Soon! Prepare for the BIGGEST $Gold & $Silver Rally in 50 Years - John Rubino

Money Sense

Goldman - >>> Investors should 'go for gold' as Fed rate cut looms, Goldman says

Yahoo Finance

by Ines Ferré

Sep 3, 2024

https://finance.yahoo.com/news/investors-should-go-for-gold-as-fed-rate-cut-looms-goldman-says-155551358.html

Investors should "go for gold" as the precious metal's stellar run isn't over, Goldman Sachs analysts said in a research note.

On Tuesday, gold futures hovered above $2,515 per ounce. The precious metal is off its all-time high touched last month but still up nearly 22% year to date, making it the world's second-best-performing asset behind crypto.

"Our preferred near-term long is gold. It remains our preferred hedge against geopolitical and financial risks, with added support from imminent Fed rate cuts and ongoing EM central bank buying," wrote Goldman Sachs analysts on Sunday.

The firm maintains a 2025 target of $2,700 per ounce and issued a "long gold" recommendation.

Purchases by central banks, which hit a record in the first quarter of 2024, have been one of the biggest drivers of the precious metal's rise this year. BofA analysts estimate gold has now surpassed the euro to become the world's largest reserve asset, second only to the US dollar.

Geopolitical risks such the Israel-Hamas war and Russia-Ukraine conflict, as well as signals from the Federal Reserve of a September rate cut amid signs of a slowing labor market, have also buoyed prices.

"We're seeing gold being used as an uncertainty hedge," said Tom Bruni, head of market research at Stocktwits, in a recent episode of Stocks in Translation.

Global physically backed gold ETFs have now seen inflows three months in a row as Western investors pile into gold, with North American activity outpacing Europe and Asia in July, according to the latest World Gold Council data.

In the near term, traders may be wondering if gold will succumb to a historically negative trend for assets this month. The yellow metal has declined every September since 2017, according to Bloomberg data.

Analysts expect the commodity's next catalyst will come when the Federal Reserve meets this month following a week of fresh labor data and a crucial monthly jobs report on Friday.

"Gold prices continue to hover at around $2,500/oz with focus primarily on the size of the expected upcoming Fed rate cut later this month," wrote JPMorgan analysts in a note on Tuesday.

As of early Tuesday, traders were pricing in a 31% probability of a 50 basis point cut instead of 25 basis points, per the CME FedWatch Tool.

<<<

---

>>> Why gold is outperforming nearly everything so far this year

Yahoo Finance

by Jared Blikre

Aug 28, 2024

https://finance.yahoo.com/news/why-gold-is-outperforming-nearly-everything-so-far-this-year-100022695.html

Gold futures have been surfing record highs, with Monday's prices hitting $2,555.2 per ounce, sending the value of a 400 troy ounce gold bar to $1,022,080.

The yellow metal has forged meteoric gains this year, emerging as the world's second-best-performing asset next to crypto. Its 23% year-to-date gain edges out the megacap-loaded Nasdaq Composite — itself up a healthy 18%. (A proxy for the crypto market writ large, the Bitwise 10 Crypto Index Fund (BITW), is up 47% this year.)

According to BofA Global Research, gold funds just absorbed the largest inflows in four weeks, attracting $1.1 billion. Yet, the broader trend has actually seen $2.5 billion in outflows year to date, suggesting that underlying strength is coming from outside traditional fund flows.

Central banks — especially those of developing countries — have been buying the barbarous relic at a record clip. According to the World Gold Council, central banks have purchased 290 tonnes in the first quarter alone, beating out the prior Q1 record from 2023 and setting CBs on a path to record gold purchases in 2024 that are estimated to easily eclipse 1,000 tonnes.

"Not only is the long-standing trend in central bank gold buying firmly intact, it also continues to be dominated by banks from emerging markets," wrote the Gold Council.

In that regard, Turkey tops the buy list this year with 30 tonnes purchased in the first quarter — lifting its gold reserves to 570 tonnes. China bought 27 tonnes in Q1, making it the 17th consecutive quarter of purchases and also bringing its holdings to 2,262 tonnes. Other notable purchasers include India, Kazakhstan, the Czech Republic, Oman, and Singapore.

The central bank buying spree has solidified gold's status as a reserve asset. According to BofA, gold has now surpassed the euro to become the world's largest reserve asset second only to the US dollar, representing 16% of the reserve pool.

The precious metal’s performance can be attributed to its unique position as a real asset with one of the lowest correlations to stocks across asset classes, making it a safe haven from market swings and inflation.

According to Tom Bruni, head of market research at StockTwits, in a recent episode of Stocks in Translation, "We're seeing gold being used as an uncertainty hedge."

Bruni also emphasized gold's appeal to traders due to its price action. "With gold breaking out above its 2011 highs, it's drawing significant attention from trend followers and technical analysts alike."

Investors looking for deep, liquid gold markets have a robust choice of futures markets, ETFs, and gold miner stocks and ETFs, which tend to be even more volatile than the underlying metal.

"The volatility in gold prices has made it a prime trading vehicle, whether through gold ETFs or mining stocks," said Bruni.

BofA separately highlighted how this latest gold rally isn't like the other advances this century, offering a tantalizing glimpse of future bullish potential.

The bank noted this is the third major gold advance in two decades, yet "households have missed this rally." The first two rallies — from 2004 to 2011, and from 2015 to 2020 — attracted big fund flows into gold ETFs. But over the last year, gold bullion and gold miner ETFs have shed $6.4 billion in assets, according to Bloomberg data and Yahoo Finance calculations.

But if last week's large gold inflows were to gain momentum, that trend could signal a perfect storm of retail, institutional, and central bank gold buying is brewing. Why?

Bruni said it best: “Gold is kind of one of these things that operates on vibes."

<<<

---

Precious metals have historically been a safe haven during economic downturns. For instance, gold prices surged during the 2008 financial crisis and the recent pandemic. Finding reputable dealers is crucial in this market. I've had positive experiences with APMEX and Bold precious metals. What tips do you have for buying precious metals? How do you determine the best times to sell?

>>> Gold prices slide as dollar regains ground; Copper walloped by China fears

Investing.com

Jul 18, 2024

https://finance.yahoo.com/news/gold-prices-slide-dollar-regains-013512650.html

Investing.com-- Gold prices fell sharply in Asian trade on Friday, dented by a mix of profit-taking and as speculation over a potential Donald Trump presidency and stricter U.S. trade policies favored the dollar.

Among industrial metals, copper prices steadied on Friday but were nursing steep losses amid scant cues on more stimulus measures from top importer China, as the country grapples with slowing economic growth.

Spot gold fell 0.9% to $2,423.89 an ounce, while gold futures expiring in August fell 1.2% to $2,426.45 an ounce 01:05 ET (05:05 GMT).

Gold tumbles from record highs

Spot prices were now trading about $50 below a record high hit earlier this week, facing some profit-taking after a strong melt-up over the past seven days.

Initial strength in gold was driven chiefly by growing optimism over interest rate cuts in the U.S., with traders seen pricing in an over 90% chance the Federal Reserve will cut rates by 25 basis points in September, according to CME Fedwatch.

While these bets still remained in place, the dollar found some strength this week from unexpectedly strong jobless claims data, which showed the labor market- a key consideration for the Fed to begin cutting interest rates- remained resilient.

Speculation over a second term for Trump- after the former president saw a massive boost in popularity in the wake of a failed assassination- also benefited the dollar, on bets that Trump’s protectionist policies could direct more capital back into the country.

Other precious metals also sank on Friday, tracking gold’s decline. Platinum futures fell 0.5% to $976.60 an ounce, while silver futures slid 1.6% to an over two-week low of $29.762 an ounce.

Copper nurses steep losses on China jitters

Copper prices steadied on Friday but were nursing steep losses this week on growing uncertainty over top importer China.

Benchmark copper futures on the London Metal Exchange rose 0.3% to $9,411.0 a tonne, while one-month copper futures rose 0.3% to $4.280 a pound.

Both contracts were down between 4.7% to 7% this week.

Losses in copper were initially sparked by weaker-than-expected Chinese economic growth data for the second quarter.

Reports that the U.S. was considering stricter trade restrictions against China also dented sentiment towards the country, as did speculation over a second term for Trump.

Additionally, the Chinese Communist Party’s Third Plenum, which began earlier in the week, yielded scant cues on more stimulus measures from Beijing. While officials did vow to provide more support, they did not offer any details on the planned measures.

<<<

---

Rickards - >>> $27,000 Gold

BY JAMES RICKARDS

MAY 13, 2024

https://dailyreckoning.com/27000-gold/

$27,000 Gold

I’ve previously said that gold could reach $15,000 by 2026. Today, I’m updating that forecast.

My latest forecast is that gold may actually exceed $27,000.

I don’t say that to get attention or to shock people. It’s not a guess; it’s the result of rigorous analysis.

Of course, there’s no guarantee it’ll happen. But this forecast is based on the best available tools and models that have proved accurate in many other contexts.

Here’s how I reached that price level forecast…

This analysis begins with a simple question: What’s the implied non-deflationary price of gold under a new gold standard?

No central banker in the world wants a gold standard. Why would they? Right now, they control the machinery of global currencies (also called fiat money).

They have no interest in a form of money they can’t control. It took about 60 years from 1914–1974 to drive gold out of the monetary system. No central banker wants to let it back in.

Still, what if they have no choice? What if confidence in command currencies collapses due to some combination of excessive money creation, competition from Bitcoin, extreme levels of dollar debt, a new financial crisis, war or natural disaster?

In that case, central bankers may return to gold not because they want to, but because they must in order to restore order to the global monetary system.

What’s the Proper Gold Price?

That scenario begs the question: What is the new dollar price of gold in a system in which dollars are freely exchangeable for gold at a fixed price?

If the dollar price is too high, investors will sell gold for dollars and spend freely. Central banks will have to increase the money supply to maintain equilibrium. That’s an inflationary result.

If the dollar price is too low, investors will line up to redeem dollars for gold and then hoard the gold. Central banks will have to reduce the money supply to maintain equilibrium. That reduces velocity and is deflationary.

Something like the latter case happened in the U.K. in 1925 when it returned to a gold standard at an unrealistically low price. The result was that the U.K. entered the Great Depression several years ahead of other developed economies.

Something like the former case happened in the U.S. in 1933, when FDR devalued the dollar against gold. Citizens weren’t allowed to own gold, so there was no mass redemption of gold. But other commodity prices rose sharply.

That was the point of the devaluation. Resulting inflation helped lift the U.S. out of deflation and gave the economy a boost from 1933–1936 in the midst of the Great Depression. (The Fed caused another severe recession in 1937–1938 with their customary incompetence.)

The policy goal obviously is to get the price “just right” by maintaining the proper equilibrium between gold and dollars. The U.S. is in an ideal position to do this by selling gold from U.S. Treasury reserves, about 8,100 metric tonnes (261.5 million troy ounces), or buying gold in the open market using freshly printed Fed money.

The goal would be to maintain the dollar price of gold in a narrow range around the fixed price.

What price is just right? This question is easy to answer, subject to a few assumptions.

$27,533 Gold

U.S. M1 money supply is $17.9 trillion. (I use M1, which is a good proxy for everyday money).

What is M1? This is the supply that is the most liquid and money that is the easiest to turn into cash.

It contains actual cash (bills and coins), bank reserves (what’s actually kept in the vaults) and demand deposits (money in your checking account that can be turned into cash easily).

One needs to make an assumption about the percentage of gold backing for the money supply needed to maintain confidence. I assume 40% coverage with gold. (This was the legal requirement for the Fed from 1913–1946. Later it was 25%, then zero today).

Applying the 40% ratio to the $17.9 trillion money supply means that $7.2 trillion of gold is required.

Applying the $7.2 trillion valuation to 261.5 million troy ounces yields a gold price of $27,533 per ounce.

That’s the implied non-deflationary equilibrium price of gold in a new global gold standard. Of course, money supplies fluctuate; lately they’ve been going up sharply, especially in the U.S.

There’s room for debate about whether a 40% backing ratio is too high or too low. Still, my assumptions are moderate based on monetary economics and history. A dollar price of gold of over $25,000 per ounce in a new gold standard is not a stretch.

Obviously, you get around $12,500 per ounce if you assume 20% coverage. There are many variables in play.

The Fundamental Model

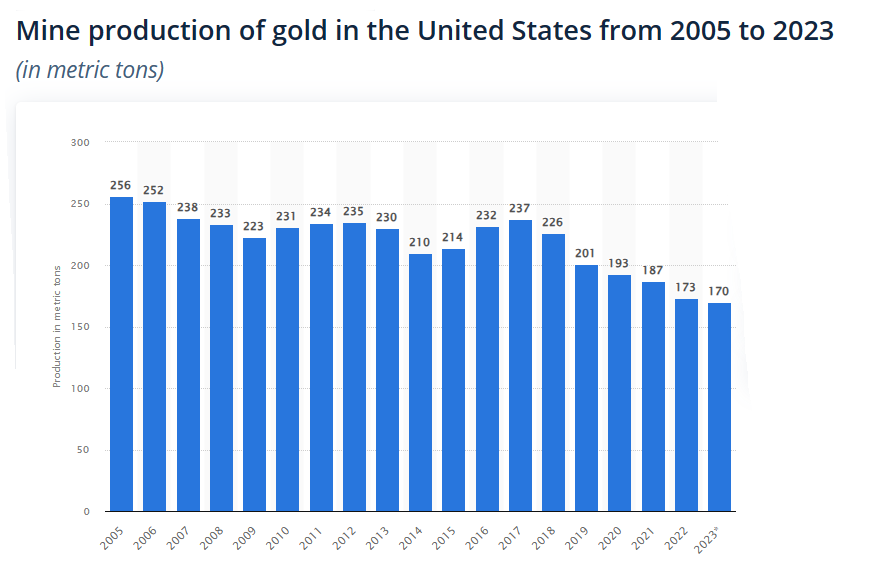

This model is also straightforward. It relies on factors we learned about in our first week of Intro to Economics — supply and demand.

The most significant development on the supply side is the decrease of new mining output. As the chart shows below, mine production of gold in the U.S. has been decreasing steadily since 2017.

image 1

These figures reveal a 28% decrease over seven years, at the same time gold prices were rising and miners were motivated to expand output.

That’s not to argue that the world has reached “peak gold,” (output could expand in future for a variety of reasons). Still, my contacts in the mining community consistently report that gold is becoming more difficult to source and the quality of newly discovered ore is low-to-medium at best.

Flat output, all things equal, tends to put a floor under prices and to support higher prices based on other factors.

The Demand Side

The demand side is driven largely by central banks, ETFs, hedge funds and individual purchases. Traditional institutional investors are not large investors in gold. Much of the demand from hedge funds is conducted in derivatives such as gold futures.

Derivatives generally don’t involve physical delivery of gold. They involve “paper gold” that far exceeds the actual, physical gold supply. It’s this paper gold market that accounts for volatility in the gold market, not gold itself.

Meanwhile, central bank demand for gold has surged from less than 100 metric tonnes in 2010 to 1,100 metric tonnes in 2022, a 1,000% increase in 12 years. Central bank gold demand remained strong in 2023 with 800 metric tonnes acquired through Sept. 30.

That puts central bank gold demand on track for a new record. There’s no sign of that demand slowing in 2024.

Overall, the picture is one of flat supply and increasing demand, mostly in the form of official purchases by central banks.

A Math Lesson

Finally, a bit of elementary math is helpful in understanding how the dollar price of gold can move past $25,000 per ounce in the next two years. For this purpose, we’ll assume a baseline price of $2,000 per ounce (although gold has been in the $2,300 range lately with no signs of falling back to the $2,000 level).

But for our purposes, we’ll keep it simple.

A move from $2,000 per ounce to $3,000 per ounce is a heavy lift. That’s a 50% increase and could easily take a year or more. Beyond that, a further increase from $3,000 to $4,000 is a 33% increase: another large rally. A further gain from $4,000 per ounce to $5,000 per ounce is a further gain of 25%.

But notice the pattern. Each gain is $1,000 per ounce, but the percentage increase drops from 50% to 33% to 25%. That’s because the starting point is higher while the $1,000 gain is constant. Each $1,000 jump represents a smaller (and easier) percentage gain than the one before.

This pattern continues. Moving from $9,000 per ounce to $10,000 per ounce is only an 11% gain. Moving from $14,000 per ounce to $15,000 per ounce is only a 7% gain. Gold can move 1% in a single trading day, sometimes 2% or more.

As an extreme example, a move from $99,000 per ounce to $100,000 per ounce is about a 1% move. Those $1,000 pops get even easier as we approach my calculated gold price of $27,533.

The lesson for you as an investor is to buy gold now.

As prices continue to rally, you’ll get more gold for your money at the outset and high-percentage returns as gold rallies from a lower base. Toward the end of the long march past $25,000 per ounce, you’ll have bigger dollar gains because you started with more gold.

Others will jump on the bandwagon, but you’ll already have a comfortable seat.

<<<

---

Wow, silver hit 29.99, so it could be the fun is just beginning. A lot of momentum building, and I'm thinking a blast up to 33 - 35 might be in the cards for the nearer term (?) Then a consolidation that establishes 30 as the new 'floor'. Just a guess, but that would replicate what gold has already done.

With silver, there is an incentive for the globalist ghouls to keep the price down, since silver represents a significant input cost for solar panels. But for now it looks like the market forces are in the driver's seat :o)

The surge in the old meme stocks this week suggests a return to 'risk on' investing could be underway, at least for a while. The main 3 stock indices all put in new highs today. RSIs for the S+P 500, DJIA, and Nasdaq are currently - 69, 69, 67, so closing in on the 70 overbought level. But I figure with luck the current momentum continues into next week, barring any news flow that derails the party.

---

Rickards - >>> AI, Gold and Nuclear War

BY JAMES RICKARDS

APRIL 16, 2024

https://dailyreckoning.com/ai-gold-and-nuclear-war/

AI, Gold and Nuclear War

So-called artificial intelligence (AI) is taking the world by storm. Meanwhile, gold has shot up like a rocket over the past couple of months.

In mid-February, gold was trading at $1,990. Two months later, gold is trading above $2,400 — a $410 gain in just two months.

So here’s a question:

Is there a connection between AI and gold? It seems like an odd question. But as it turns out, the answer is yes. And surprisingly, there has been for decades. It involves the Cold War between the U.S. and the Soviet Union.

In the early 1980s, the KGB was deeply concerned about the possibility of a nuclear first strike by the United States. At the time, Yuri Andropov was head of the KGB.

Andropov’s fear of a nuclear first strike by the U.S. was based in part on the 1980 election of Ronald Reagan and Reagan’s plan to install Pershing II intermediate-range missiles in Europe.

Those missiles could be armed with nuclear warheads and could strike the Soviet Union within minutes of being launched. This put Soviet nuclear forces on a hair-trigger alert. They adopted a “launch on warning” posture.

This means that as soon as credible evidence of a planned first strike was discovered, the Soviet Union would launch its own first strike to avoid destruction of its forces.

The irony was that the U.S. had no actual plans to launch a first strike, but the Soviet Union didn’t know that. Reagan’s speeches about the “evil empire” did nothing to calm Soviet concerns.

AI and Nuclear Readiness

In response, the Soviets developed a primitive (by today’s standards) AI system called VRYAN. That’s a Russian acronym for: sudden nuclear missile attack.

VRYAN took about 40,000 military, economic and political inputs and computed the relative strength of the Soviet Union compared with the United States expressed as a percentage output. The model used a value of 100% for equivalence of the USSR to the U.S.

The Soviet leadership was comfortable that the U.S. would not launch a nuclear first strike if the USSR could maintain a value of 60%, although they viewed 70% as providing a more comfortable margin.

A VRYAN output of 40% was considered the critical threshold at which the U.S. might feel it could launch a first strike with acceptable risk that the Soviets would not be able to mount a successful second strike.

VRYAN output values were in steady decline in the dangerous period from 1981–1984 (in 1984, the VRYAN output had declined to 45%).

The VRYAN AI system relied on by the KGB and the Soviet Politburo was an important factor in the Soviet decision in 1981 to vastly increase intelligence collections aimed at detecting U.S. preparations for a first strike.

Close Call

This intelligence collection effort was complicated to the point of extreme danger by the fact that the U.S. and NATO were conducting a war game in late 1983, code-named Able Archer 83. This war game was to practice a nuclear strike on the Soviet Union.

It turned out that the U.S. was rehearsing a nuclear first strike at the same exact time that the KGB was looking for evidence of a nuclear first strike. Able Archer 83 provided the KGB with more than enough reason to suspect the U.S. was indeed preparing for a first strike under cover of a war game.

VRYAN’s AI output on relative U.S. strength was compounded by massive U.S. intelligence failures regarding Soviet intentions. U.S. intelligence analysts assumed that the future would resemble the past, and that Soviet alerts were really propaganda designed to halt the U.S. deployment of Pershing II intermediate-range nuclear missiles in Europe.

U.S. intelligence analysts were also guilty of what’s called mirror imaging: the belief that because you know your own intentions, your opponents must share your view. In this case, the U.S. assumed that because they had no intention to launch a first strike, the Soviets must have understood that intention and would therefore have no cause for concern.

In fact, the Soviets had the opposite view based in part on VRYAN AI output.

The world came extremely close to World War III and a nuclear holocaust as a result of this sequence of events and misperception of intentions. It was only when one U.S. general decided not to escalate in the face of Soviet first strike preparations that both sides deescalated, and the crisis eventually receded.

The information above wasn’t fully understood by either side at the time of the escalation. On the U.S. side, it wasn’t until the 1990 publication of a study entitled The Soviet War Scare by the President’s Foreign Intelligence Advisory Board (PFIAB) that something like the full story was revealed.

Nuclear War Threats: Good For Gold

This study was originally classified above TOP SECRET. (Most citizens assume that TOP SECRET is the highest level of classification. But there are secret access codes that limit circulation of certain documents even among those cleared with TOP SECRET access.

In the case of The Soviet War Scare, those restrictions had the code names UMBRA, GAMMA, ININTEL, NOFORN, NOCONTRACT, ORCON. I can’t discuss my own TOP SECRET clearances, but I can inform you that very few intelligence operatives would have been able to view the PFIAB report based on those restrictions.

So what does all this have to do with gold?

Buried inside The Soviet War Scare was this passage about the U.S. assessment of KGB collection requirements related to a potential nuclear war:

VRYAN Collection Requirements – Throughout the early 1980s, VRYAN requirements were the No. 1 (and urgent) collection priority for Soviet intelligence… They were tasked to collect:… monitoring of the flow of money and gold on Wall Street as well as the movement of high-grade jewelry, collections of rare paintings and similar items. (This was regarded as useful geostrategic information.) (Emphasis added)

And there it is! The U.S. assessed that the KGB tracked the movement of gold as a leading indicator of nuclear attack.

I didn’t find this completely surprising. From 2004–2010, I was co-director of a CIA effort called Project Prophesy that looked at capital markets activity as an early warning of an enemy attack.

Gold was one of the valuable assets that was on our list of items to track. The idea was that if a general or political leader had advance information about an attack, they’d convert their wealth to gold in safekeeping in order to financially survive the fallout.

The bottom line is that this intelligence reporting and AI system are not ancient history. Today, the world is closer to nuclear war than at any time since the Able Archer scare in 1983. Gold is once again on the move, having risen from $1,830 per ounce on Oct. 5, 2023, to over $2,400 today. That’s a 31% gain in six months.

Is this a coincidence? Hardly. A close correlation of huge gains in gold with serious threats of nuclear war is exactly what one should expect.

Unfortunately, those threats of nuclear war are not going away soon. One need only look at the Iranian attack on Israel this past weekend and the possibilities of further escalation.

There are also situations in Ukraine, Russia, NATO, Gaza, the Red Sea and the Suez Canal revealing that the world is a more dangerous place than it has been for decades.

That’s bad news for the world but good news for gold investors. The rally we’ve seen in the past six months is just getting started.

<<<

---

>>> Why Are Gold Bar Sales Surging at Costco?

The New York Times

by Rebecca Carballo

April 11, 2024

https://www.yahoo.com/news/why-gold-bar-sales-surging-175059774.html

Alongside its $1.50 hot dog and soda combo, gallon tubs of mayonnaise and value packs of socks, Costco, the warehouse retailer, has been selling gold bars since October.

Now, Costco is selling up to $200 million worth of gold and silver each month, according to an analysis from Wells Fargo.

Online forums and Reddit threads have cropped up where customers give one another advice on how to purchase the bars before they sell out.

“I’ve gotten a couple of calls that people have seen online that we’ve been selling one-ounce gold bars, yes, but when we load them on the site, they’re typically gone within a few hours,” Richard Galanti, Costco’s executive vice president and chief financial officer, said in an earnings call in September.

Costco started selling gold bars in October.

Costco is now selling one-ounce, 24-karat gold bars, according to its online store. The bars can be purchased only by members, and the price varies based on market rates. As of Thursday, the bars were sold out for members online, but The Wall Street Journal reported that shoppers purchased them for around $2,000 in December.

Costco has also been selling silver coins, advertised as 99.9% pure silver, since January, according to an analyst report from Wells Fargo.

People buy gold in times of turmoil.

The precious metal has set a series of records as it surged to $2,350 per troy ounce, up roughly $300 since the start of March.

Buying gold becomes more common in times of economic turmoil. Although the U.S. economic outlook has improved and inflation has slowed, it remains higher than the targets from the Federal Reserve, said Sadiq S. Adatia, the chief investment officer for BMO Global Asset Management. And on Wednesday, a key inflation rate was revealed to be stronger than expected.

Investors have said they were puzzled about the rally.

Geopolitical concerns could also be a factor in an increasing interest in gold, Adatia said. There has been more interest in gold since Ukraine’s currency collapsed after Russia’s invasion, he said.

For those looking to purchase gold for the first time, Costco provides familiarity and ease, Adatia said.

“They make it convenient,” he said. “People can physically go in and pick it up and that’s it, versus opening up an account and buying gold shares.”

How much is Costco profiting from this?

Probably not too much.

Given its pricing and shipping costs, it’s likely a “very low profit business at best,” analysts with Wells Fargo wrote in a note to clients on Tuesday.

Costco sold more than $100 million of gold during its first quarter, or the three-month period ending on Sept. 30 last year, Galanti said on a December earnings call. However, those sales have likely grown since then and may now be running at $100 million to $200 million per month, which could increase its sales figures by 1%.

“The reason that we looked at this is that it’s becoming a larger contributor to sales for them,” said Edward Kelly, managing director of equity research at Wells Fargo. “It’s not that $100 or $200 million a month is a lot for Costco, but it’s new business and they didn’t have that business last year.”

In the three-month period ending on Dec. 31, Costco’s e-commerce sales grew 18% compared with the same period a year earlier, driven in part by demand for the precious metals, Galanti told investors on an earnings call in March.

Investing in metals can be volatile.

The Commodity Futures Trading Commission has urged caution when buying gold because precious metals can be highly volatile.

“Like other commodities, precious metal prices rise as demand goes up, so when economic anxiety or instability is high, the people who typically profit from precious metals are the sellers,” the agency said in a statement.

The commission likely puts that warning out to signal that it is not a guaranteed investment, said Larry Tentarelli, chief technical strategist for Blue Chip Daily Trend Report. He recommends the average person invest 3% to 5% of their assets in gold.

<<<

---

Goldman recently came out bullish on gold (previous post), so that's a factor in the current move, and another is that Wall Street often bases its decisions on TA / charts, and this big breakout is attracting attention. I figure numerous 'macro' factors are also at work, including the growing US debt bomb, the BRICS plans for their own gold linked currency to compete with the US dollar, etc. As we know, central banks have been piling into gold for years, so global demand grows and mining output has lagged.

So the 'stars + planets' are finally aligning to produce the big breakout. The professional 'gold bugs' are always bullish, and have their reputations and livelihoods wrapped up in the bullish side, via newsletters, book sales, etc. But it looks like gold's appeal is broadening, and some of the Bitcoin crowd might also be switching over to gold. Seeing gold being sold at Costco, and selling out within hours, may have also attracted some attention. And anyone who follows TA / charts couldn't miss the extremely bullish chart pattern that had developed.

Based on the charts, this move is probably just beginning. But as you said, the big question is when does the suppression mechanism kick in? If gold is allowed to run up too much it could reinforce an inflationary vibe and thus work against the Fed's goals. So we'll see how long the party lasts, but so far it's been fun :o)

---

>> silver <<

Silver also coming to life :o) Looking at the SLV chart, as with gold there is a quasi 12 year cup + handle (bullish), with the 3 year 'cup' having a quasi inverted head + shoulders (also bullish). It's much less classic than on the gold chart, but is easier to see now that silver is climbing. Also the 'neckline' on the silver chart is sloped, where gold's is flat and thus more 'classic'.

Anyway, looks like silver is playing catch up to gold. There is also a potential motivation for price suppression with silver, since it represents a key input cost for solar panels. Therefore keeping silver prices lower helps keep solar cost competitive with traditional types of energy. Not sure how much price suppression of silver has been going on in recent years, but like gold. it does seem to have peculiar 'smack downs' at times.

---

>>> Gold: The Everything Hedge

By Jim Rickards

https://dailyreckoning.com/goldilocks-is-gonna-get-it/

Gold is trading at $2,211 per ounce this afternoon. Since its interim low of $1,832 per ounce on Oct. 5, 2023, gold has posted a 21% gain. That’s in less than six months. Almost half of that gain occurred in the one-month period from Feb. 11 to March 11.

That overall gain is especially impressive considering gold had been stuck in a fairly narrow range of $1,650–2,050 for the past two years. That’s a range of about 10% above and below the midpoint of $1,850. Starting from the high end of that range, gold traversed the entire range to the upside and beyond in just one month.

Now, any reference to “gold prices” is an interesting one. If you treat gold as a commodity, then the price per ounce measured in dollars is one way to think about price.

On the other hand, if you think of gold as money (as I do) then the dollar price is not really a price — it’s a cross-rate similar to euro/dollar (about $1.08 today) or dollar/yen (about 152 today). When analysts say the “price” of gold is $2,211 per ounce, I think of that data as showing the gold/dollar cross-rate = $2,211.

That’s useful because there are two sides to a cross-rate. While most analysts say that gold has rallied from $2,000 to $2,211 per ounce, it is just as valid and perhaps more useful to say that the dollar has crashed from 1/2,000 per ounce to 1/2,211 per ounce.

In this analysis, gold is constant (by weight) and the dollar gets stronger or weaker relative to gold. All of the recent market action points to a weaker dollar.

This mode of analysis also solves another market riddle. Given huge U.S. budget deficits, unprecedented levels of U.S. national debt, slow growth, rising unemployment and persistent inflation, how is it possible that the dollar has been so “strong” lately?

The answer is that it’s only been strong relative to the euro, yen, sterling and some other reserve currencies and as measured by certain dollar indexes (DXY, Bloomberg, etc.) composed of baskets of currencies (but not gold).

But that’s often because those other currencies are issued by countries with debt and growth problems even worse than the U.S.’ Those currencies dropping against the dollar have the look and feel of a good old-fashioned currency war.

It’s only when you use gold as your metric that the real weakness in the dollar becomes apparent, as it should. In effect, certain currencies are weakening against each other but all currencies are weakening against gold.

Returning to the “higher gold price” frame, there are a number of reasons for this trend. The first factor is simple supply and demand. Mining output and recycled gold have been about flat for the past eight years running between 1,100 metric tonnes and 1,250 metric tonnes per year.

At the same time, central bank demand for gold has surged from less than 100 metric tonnes in 2010 to 1,100 metric tonnes in 2022, a 1,000% increase in 12 years. Central bank gold demand remained strong in 2023 with 800 metric tonnes acquired through Sept. 30, 2023. That puts central bank gold demand on track for a new record in 2023. There’s no sign of that demand slowing in 2024.

Constant output with surging demand by central banks does not by itself explain the recent surge in gold prices, but it is a contributor. Importantly, continued strong demand by central banks puts a floor under gold prices. This sets up what we describe as an asymmetric trade where downside is limited but upside is open-ended.

The second factor driving gold prices higher is the need for hedging. This is not the same as inflation hedging. It covers a larger list of risks including geopolitical risk, risks of escalation in the Ukraine and Gaza wars, Houthi efforts to close the Red Sea and Suez Canal, increasing risks of war with China and the intrinsic risk of a senile president of the United States.

As the list of risks grows longer and potentially more dangerous, the need for a hedging asset such as gold that does not rely on any nation-state for its value increases. I call gold the everything hedge.

Finally, gold prices are being driven higher by U.S. threats to steal $300 billion in U.S. Treasury securities from the Russian Federation. Those assets were legally purchased by the Central Bank of Russia as part of their reserve position.

The actual securities are held in custody in digital form at European banks, U.S. banks and the Brussels-based Euroclear clearinghouse. Only about $20 billion of those Treasury securities are held by U.S. banks; the majority are held by Euroclear. Those assets were frozen by the United States at the outbreak of the war in Ukraine.

Freezing assets means the Russians cannot collect interest or sell or transfer the assets or pledge them as collateral. Asset freezes are used frequently by the U.S. including in the cases of Iran, Syria, Cuba, North Korea, Venezuela and other nations. Often the assets are frozen for years but ultimately released to the owner as happened in the case of Iran after 2012.

Now the U.S. wants to go further and actually seize the assets, which may be viewed as outright theft under international law. The U.S. proposes to use the $300 billion to finance the war in Ukraine. European entities have expressed considerable uncertainty about this plan but the U.S. has maintained the pressure and wants to complete the theft before the June and July summits of G7 leaders and NATO members.

If the U.S. steals these assets, Russia will likely confiscate an equivalent amount of industrial and commercial assets located in Russia and owned by German, French, and Italian interests among others.

The bottom line is that if U.S. Treasury securities are not a safe investment, then securities of Germany, Italy, France, the U.K. and Japan are no better. The only reserve asset free of this kind of digital theft is gold. Nations are beginning to diversify into gold in order to insulate themselves from digital confiscation by the collective West.

Finally, there’s an interesting bit of math here, which I’ve explained in the past that shows each $100 per ounce increment in the price of gold is a smaller percentage gain because the denominator is larger.

That makes each $100 milestone ($2,400, $2,500, $2,600) easier to reach than the one before. People don’t really notice this; they just focus on the dollar amount of the gains. But this explains how price rallies gather crazy momentum.

All of these trends — flat output, rising central bank demand, hedging, protection against digital confiscation and simple momentum — will continue. Based on those trends, one would expect the gold price rally to continue as well.

The trend is gold’s friend.

<<<

---

Goldman likes gold - >>> Gold’s 'record march higher set to continue,' Goldman says

Yahoo Finance

Ines Ferré

March 25, 2024

https://finance.yahoo.com/news/golds-record-march-higher-set-to-continue-goldman-says-164325765.html

Gold’s roughly 8% month-to-date rally has room to grow with the precious metal poised to hit $2,300 an ounce by year-end, according to Goldman Sachs analysts.

On Monday futures gained to trade as high as $2,182 an ounce. The precious metal is considered a safe haven during times of geopolitical tensions and when interest rates decrease. Last week, the Federal Reserve continued to signal that it would lower interest rates three times this year.

The Fed meeting “reinforced the market’s (and ours) expectations that three cuts are likely this year, lending renewed support to gold to test and surpass March’s earlier record high,” wrote a team of analysts led by Samantha Dart.

Goldman Sachs analysts upgraded their average gold price forecast for 2024 from $2,090 to $2,180 per ounce, targeting a move to $2,300 by the end of the year.

The analysts forecast gold prices in the near term will move toward another consolidation phase, barring any geopolitical surprise. However, “a substantive retracement lower will likely also be limited by resilience in physical buying channels,” wrote Dart, citing Chinese imports of the precious metal.

“Nonetheless, in the midterm we continue to hold a constructive view on gold underpinned by eventual Fed easing, which should crucially reactivate the largely dormant ETF buying,” wrote Dart.

Bullion's price increases have been disconnected from recent outflows seen in gold-related ETFs. Strategists believe investors have been rotating money into bitcoin ETFs as the token roared toward new highs earlier this month.

Central banks have been buying up gold at historic levels, helping to drive up demand over the past couple of years.

Adjusted for inflation, gold hit a record in 1980 when it hit $850 per ounce, which would equal almost $3,200 in today's dollars.

<<<

---

The world's central banks still own a huge amount of gold, so they obviously see it as having value.

Derf, >> what gold is used for any more <<

Yes, that's the problem with owning gold since other than jewelry, its only real use historically is as money or backing for money. A tiny amount is used in electronics, but it's negligible. So the question is when will gold return to be a backing for money, ala the Bretton Woods system or something similar? The world's central banks still own a huge amount of gold, so they obviously see it as having value. The new BRICS currency being set up will reportedly be linked to gold, and once operational this could force the dollar and euro into a similar arrangement to remain competitive.

Jim Rickards recommends having 10% of one's investible assets in gold. It's tough to sit in gold when you can get 4-5% in Treasuries or the money market, so it's a dilemma. The timeline for the BRICS gold-linked currency has slipped, but with the US debt now parabolic, I figure it makes sense to at least have something in gold. Silver also seems logical since it usually follows the gold price loosely, and also has many industrial uses, in solar panels, etc. But as the saying goes - 'everything in moderation' :o)

Forbes article -

>>> The BRICs Go For Gold

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=172356566

---

Yes, copper is needed. Much like silver used to be a necessity for video equipment.

I don't know what gold is used for any more.

>>> Why Costco is selling gold bars and silver coins

CNN

by Nathaniel Meyersohn

March 7, 2024

https://finance.yahoo.com/news/why-costco-selling-gold-bars-173244588.html

Costco locked in $1.50 hot dog-soda loyalists. Now, it’s chasing a different clientele: precious metal investors and collectors.

Costco recently started selling silver coins for the first time, finance chief Richard Galanti told CNN.

The company is selling 25-count tubes of 1 oz. Canada Maple Leaf Silver Coins online for $675. The front of the coins features a maple leaf, and King Charles III is on the back. The coins are non-refundable, and members can purchase a maximum of five.

Costco is trying to replicate its recent success with gold bars. It began selling $2,000 gold bars online in September and sold more than $100 million worth of the bars last quarter.

But Costco’s move is more about marketing than just about increasing sales. After all, not many people are actually stashing away gold bars in their homes.

It’s selling precious metals to try to reinforce its “treasure hunt” brand image where it peppers its stores with unexpected, limited-time items to keep shoppers coming back.

“We try to create an attitude that, if you see it, you ought to buy it because chances are it ain’t going to be there next time,” Costco’s founder once said. “That’s the treasure-hunt aspect. We constantly buy that stuff and intentionally run out of it from time to time.”

Costco is also selling precious metals as they become more valuable. Gold prices have notched record highs this week. Silver futures are up 21% in the past year.

Precious metal prices have gone up because investors are betting that the Federal Reserve will cut interest rates in the back half of the year.

Gold and silver are considered to be one of the most resilient investments. When interest rates fall, holding income-paying assets (like bonds) becomes less appealing than owning the precious metals. When interest rates are low, falling or — as in this case — expected to fall, demand for Treasury bonds ebbs, and precious metals, which don’t pay out any interest, become relatively more attractive.

Some investors also believe them to be a hedge against inflation, wagering that they will hold their value even if it begins to surge, even though metals face price fluctuations like any other commodity.

Costco’s success in selling the metals comes as the company continues to report strong profits from the pandemic in 2020, when customers rushed to stores to load up on groceries and household staples. Millions of first-time customers signed up for club memberships during the pandemic and have held on to them, pushing Costco’s member rolls to all-time highs.

Shares of Costco (COST) have rallied 60% over the past year.

Costco reported quarterly earnings Thursday. The company’s sales at stores open for at least one year increased 5.6%, but fell short of analyst forecasts.

Costco said inflation was roughly flat during the quarter, which allowed it to reduce prices on some items.

Galanti told analysts on a call Thursday that Costco cut reading glasses, for example, from $18.99 to $16.99 and cut a 48-count of batteries from $17.99 to $15.99.

<<<

---

Derf, With copper, a few years back I had an ETF (CPER), but it ended up causing problems at tax time. Using SCCO and other mining stocks seems like a good approach.

One thing with miners in general though is the geopolitical risk. With periodic leadership changes in these countries, it can result in problems like nationalization of the mines, etc. Historically there's a lot of 'payola' that goes on to buy off the local politicians. There's also the increasing environmental rules to contend with.

But copper is a 'must have' for the 'electric everything' paradigm, so it seems like a logical area for investors. The longer term SCCO chart has been volatile, but overall looks pretty decent. I see they recently lowered their dividend by 20%, though it's still a nice yield.

---

More on SCCO - >>> Decoding Southern Copper Corp (SCCO): A Strategic SWOT Insight

GuruFocus Research

March 1, 2024

https://finance.yahoo.com/news/decoding-southern-copper-corp-scco-050928095.html

Insightful analysis of Southern Copper Corp's strengths, including its vast copper reserves and robust production capabilities.

Examination of potential weaknesses, such as dependency on energy prices and supply chain vulnerabilities.

Exploration of opportunities in the context of the global shift towards clean energy and copper's critical role.

Assessment of threats including environmental regulations and market volatility.

On February 29, 2024, Southern Copper Corporation (NYSE:SCCO) filed its annual 10-K report, providing a comprehensive overview of its financial performance and operational strategies. As an integrated producer of copper and other minerals, SCCO operates mining, smelting, and refining facilities in Peru and Mexico. The company's revenue for the fiscal year ended December 31, 2023, totaled $9,895.8 million, a slight decrease from the previous year, primarily due to lower metal prices and sales volumes. Despite this, SCCO managed to increase copper production by 1.8% and molybdenum production by 2.3%. However, net income attributable to SCCO saw an 8.1% decrease, settling at $2,425.2 million. These financial metrics set the stage for a detailed SWOT analysis, providing investors with a clear picture of SCCO's market position and future prospects.

Strengths

World-Leading Copper Reserves and Production: Southern Copper Corp boasts the largest copper reserves globally, positioning it as a top player in the industry. Its significant scale of operations across Peru and Mexico, as highlighted in the 10-K filing, ensures a steady production of copper, molybdenum, zinc, and silver. In 2023, SCCO's copper mine production increased by 1.8% to 2,008.4 million pounds, demonstrating its robust production capabilities. This strength is not only a testament to the company's resource wealth but also to its operational efficiency and expertise in mining and processing.

Strategic Market Positioning: SCCO's market positioning is strategic, with its operations spread across key geographic locations in The Americas, Europe, and Asia. This diversified market presence helps mitigate regional risks and capitalizes on global demand for copper and other metals. The company's long-standing presence in the industry, since 1952, and its listing on both the New York and Lima Stock Exchanges further reinforce its market credibility and investor confidence.

Weaknesses

Energy and Resource Dependency: SCCO's operations are heavily reliant on fuel, electricity, and water, which constituted approximately 29% of its total production cost in 2023. Fluctuations in energy prices and potential shortages of water supply pose significant risks to the company's cost structure and operational continuity. The 10-K filing acknowledges these vulnerabilities, indicating that any disruptions in the supply of these critical resources could adversely affect production and expansion opportunities.

Supply Chain and Operational Risks: The global shipping industry's current challenges, including port congestion and container shortages, present risks to SCCO's supply chain. The company's reliance on third-party energy resources and potential delays in product transportation could impact sales agreements and operational efficiency. Additionally, the need for political risk insurance, which SCCO does not intend to obtain, could expose the company to unforeseen geopolitical risks.

Opportunities

Increasing Demand for Copper in Clean Energy Transition: The global push towards clean energy and electrification presents a significant opportunity for SCCO, given copper's essential role in these technologies. The company's commitment to responsible production practices and certifications under international standards aligns with the increasing expectations for sustainable copper sourcing. This positions SCCO favorably to capitalize on the growing demand for environmentally responsible copper production.

Expansion and Diversification: SCCO's exploration activities in Argentina, Chile, and Ecuador, as well as its existing operations, offer opportunities for expansion and diversification of its mineral portfolio. The company's ability to leverage its vast reserves and operational expertise could lead to increased production, new market entries, and enhanced revenue streams in the future.

Threats

Market Volatility and Price Sensitivity: SCCO's financial results are susceptible to fluctuations in metal prices and global economic conditions. The 2023 decrease in net sales was influenced by lower copper and zinc prices, highlighting the company's sensitivity to market volatility. Such economic uncertainties and potential downturns could adversely affect demand for SCCO's products and, consequently, its revenue and profitability.

Environmental Regulations and Legal Challenges: The mining industry is subject to stringent environmental regulations, which can impose significant costs and operational constraints. SCCO's operations, particularly in Peru, face stricter environmental rules that could impact the company's ability to operate efficiently. Additionally, the lack of certain types of insurance coverage for environmental damage or hazards could expose SCCO to legal and financial risks.

In conclusion, Southern Copper Corp (NYSE:SCCO) exhibits a strong foundation with its vast copper reserves and strategic market positioning. However, it must navigate the complexities of energy dependency and supply chain risks. Opportunities in the clean energy sector and potential for expansion present promising avenues for growth. Nonetheless, market volatility and stringent environmental regulations pose significant threats that SCCO must address proactively. By leveraging its strengths and addressing its weaknesses, SCCO can capitalize on emerging opportunities while mitigating the impact of potential threats.

<<<

---

Derf, With SCCO, it looks like China is cutting their production (article excerpt below), so SCCO and FCX are way up today. Nice move :o) -

>>> Copper and Miner Shares Jump After China Output Cut

Wall Street Journal

by Bob Henderson

3-13-24

https://www.wsj.com/livecoverage/stock-market-today-dow-jones-03-13-2024/card/copper-and-miner-shares-jump-after-china-output-cut-N6dm8hihs8R9lQZOIZBZ?siteid=yhoof2

Copper futures and shares of mining companies popped Wednesday after some of China's smelters agreed to cut production.

Copper futures for March delivery gained 3.25% to close at $4.05 a pound, their highest settlement value in nearly 11 months. Shares of diggers Freeport-McMoRan and Southern Copper were recently up 7.9% and 11%, respectively.

The production cuts were reported by Reuters, which said China's top smelters agreed Wednesday to reduce production at some loss-making plants to cope with a shortage of raw material...

<<<

---

Geez you've got a ton of boards!!!

So, while I tell people buying gold is awful, last August I put some money into copper via $SCCO.

Today it's up 10%! What's up wit dat?

>>> The world’s appetite for solar panels is squeezing silver supply

Bloomberg News

July 3, 2023

https://www.mining.com/web/the-worlds-appetite-for-solar-panels-is-squeezing-silver-supply/

Changes to solar panel technology are accelerating demand for silver, a phenomenon that’s widening a supply deficit for the metal with little additional mine production on the horizon.

Silver, in paste form, provides a conductive layer on the front and the back of silicon solar cells. But the industry is now beginning to make more efficient versions of cells that use a lot more of the metal, which is set to boost already-increasing consumption.

Solar is still a fairly small part of overall silver demand, but it’s growing. It’s forecast to make up 14% of consumption this year, up from around 5% in 2014, according to a report from The Silver Institute, an industry association. Much of the growth is coming from China, which is on track to install more panels this year than the entire total in the US.

Solar is a “great example of how inelastic demand for silver is,” said Gregor Gregersen, founder of Singapore-based dealer Silver Bullion. The solar industry has evolved to become much more efficient with using smaller amounts of silver, but that’s now changing, he said.

The standard passivated emitter and rear contact cell will likely be overtaken in the next two to three years by tunnel oxide passivated contact and heterojunction structures, according to BloombergNEF. While PERC cells need about 10 milligrams of silver per watt, TOPCon cells require 13 milligrams and heterojunction 22 milligrams.

At the same time, supply is starting to look tight. It was flat last year, even as demand rose by nearly a fifth, figures from The Silver Institute show. This year, production is forecast to increase by 2% while industrial consumption climbs 4%.

The trouble for silver buyers is that cranking up supply is far from easy, given the rarity of primary mines. About 80% of supply of the metal comes from lead, zinc, copper and gold projects, with silver a by-product.

And in an environment where miners are already reluctant to commit to large new projects, lower margins in silver compared with other precious and industrial metals mean positive price signals aren’t enough to crank up output. Even newly approved projects could be a decade away from production.

The result is a strain on supply so significant that a study from the University of New South Wales forecasts the solar sector could exhaust between 85–98% of global silver reserves by 2050. The volumes of silver used per cell will increase and it could take about five to 10 years to bring them back to current levels, according to Brett Hallam, one of the authors of the paper.

Chinese solar companies, however, are actively exploring using cheaper alternatives like electroplated copper, though so far results have been mixed. Technologies that use cheaper metals are now sufficiently advanced, and will soon be put into mass production once silver prices surge, according to Zhong Baoshen, chairman of Longi Green Energy Technology Co., the world’s biggest panel manufacturer.

Silver is currently trading at about $22.70 an ounce. It’s dropped around 5% this year, but is well above where it was before surging in 2020 as the pandemic buoyed demand.

“Substitution will look more interesting when silver’s at say $30 an ounce as opposed to $22 to $23,” said Philip Klapwijk, managing director of Hong Kong-based consultant Precious Metals Insights Ltd. and one of the authors of the silver institute report. There won’t be a “doomsday scenario” where we run out of silver, but “the market will restore an equilibrium at a higher price,” he said.

<<<

---

>>> Goldman says ‘shine is returning' for gold as investors ramp up bets on rate cuts

by Jenni Reid

CNBC

November 27, 2023

https://www.nbcchicago.com/news/business/money-report/goldman-says-shine-is-returning-for-gold-as-investors-ramp-up-bets-on-rate-cuts/3287739/

...Analysts at Goldman Sachs said in a note Sunday on the metals outlook for 2024 that gold's "shine is returning."

"The potential upside in gold prices will be closely tied to U.S. real rates and dollar moves, but we also expect persistent strong consumer demand from China and India, alongside central bank buying to offset downward pressures from upside growth surprises and rate cut repricing," they said.

Bank of America analysts, meanwhile, said in a Sunday note that the commodities team's base case was for gold to appreciate from the second quarter of 2024 as "real rates are pushed lower by the Fed cutting."

<<<

---

>>> Costco's Gold Bars Are Selling Out 'Within A Few Hours'— Here Are 3 Other Ways To Invest In The Yellow Metal

Benzinga

by Jing Pan

Oct 12, 2023

https://finance.yahoo.com/news/costcos-gold-bars-selling-within-152139775.html

Everyone knows you can leave Costco Wholesale with a cart brimming with oversized tubs of peanut butter, a TV larger than your living room wall and enough toilet paper to last a decade. But did you know that the warehouse chain sells gold bars, too?

Costco has started selling 1-ounce gold bars. You can choose from two variations: a 1-ounce gold PAMP Suisse Lady Fortuna Veriscan bar and a 1-ounce gold bar from Rand Refinery.

Both types are available online only and are limited to two per member. They are nonrefundable.

Given that gold bars aren't really a typical grocery list item, you might think that they'd linger unnoticed on Costco's website. But demand has been surprisingly strong.

During Costco's latest earnings conference call, Chief Financial Officer Richard Galanti said, "I've gotten a couple of calls that people have seen online that we've been selling gold — 1-ounce gold bars. Yes, but when we load them on the site, they're typically gone within a few hours, and we limit two per member."

Costco's website indicates that both bars are out of stock as of Oct. 10.

Why Do People Hoard Gold?

People own gold for various reasons — the yellow metal has served as a store of value for thousands of years.

Unlike fiat money, which can be produced in unlimited quantities by central banks, the precious metal has inherent scarcity, making it a hedge against inflation.

At the same time, gold historically has been recognized as a safe-haven asset, providing investors with a hedge against economic uncertainty and geopolitical risks. In times of political unrest, wars and other crises, the yellow metal has often been sought as a refuge, given its global recognition and value.

These days, there are plenty of ways to gain access to the metal — and you don't have to be a member at Costco to do it.

Investing In Gold

The most direct way to own gold is by purchasing physical bullion. While Costco's gold bars might be out of stock — and sell out quickly when they are in stock — there are other reputable online dealers and platforms where you can readily acquire the precious metal. Your local bullion shop may also carry various gold coins and bars.

Second, rather than owning the metal directly, you can also invest in companies that mine it. By buying shares in gold mining companies, you're essentially placing a bet on the company's ability to profitably mine and sell gold. This method introduces the complexities of stock investing, such as assessing a company's management, mining costs and overall financial health. While this method could be more volatile than direct gold ownership, it offers the opportunity for potential dividends and capital appreciation.

In addition, investors can also invest in exchange-traded funds (ETFs) that specialize in gold. These funds track the price of gold and trade on stock exchanges so it's easy to buy and sell them. If you want to get gold exposure in your portfolio without worrying about storage or authenticity, gold ETFs deserve a serious look. However, it's essential to be aware of any associated fees or expenses, which can eat into potential returns.

<<<

---

>>> Silver coins, promised profits, and an empty vault: How a silver dealer’s slow theft of investors’ precious American Eagle coins ended in a $146m fine

Fortune

by Eleanor Pringle

July 4, 2023

https://finance.yahoo.com/news/silver-coins-promised-profits-empty-115839138.html

Hundreds of depositors who handed millions to a silver dealer in exchange for precious minted coins were told their vaults were actually empty following an investigation by the U.S. Commodity Futures Trading Commission (CFTC).

Two firms run by precious metals dealer Robert Higgins have been ordered to pay out $112.7 million to the victims of an alleged complex fraudulent scheme, and $33 million in a civil monetary penalty.

The investigation into Higgins and two connected companies began last year.

According to a statement from the CFTC, between 2014 and 2022 Higgins conducted a fraudulent silver leasing scheme via two companies: Argent Asset Group LLC (Argent) and First State Depository Company, LLC.

The scheme

The plot, sold to customers as the 'Maximus Program', offered to pay owners of silver coins a lease fee in exchange for Argent's use of the commodity.

The payments were on a "scale" and would increase or decrease depending on how many of their coins the client was willing to offer.

The coins were either already owned by the customers, or could supposedly be purchased through Argent, and were apparently in storage at a vault owned by First State Depository Company in Delaware.

Customers were also told their investments were guaranteed and fully insured.

Coins such as these—silver American Eagle dollars—are often purchased by investors who want to see something tangible for their money, as opposed to government bonds or stocks.

People buy the coins because—although they only have a $1 face value—they are made up of 99.9% fine silver, and thus hold their value as a precious metal as opposed to as a currency.

The bullions are also produced by the U.S. Mint, which guarantees their authenticity and are minted—or stamped—in limited numbers to guarantee their rarity. Currently, uncirculated silver 1oz coins from the 2023 release can be bought for $76 each. (actually $32)

The clients were also under the impression they had an eye on their income from the coins, as they were sent monthly reports from the company which prosecutors allege "falsely indicat[ed] that the assets remained safely stored at FSD."

Vanishing coins

Court documents show that vast quantities of the coins apparently stored at the FSD facilities simply did not exist.

Documents published on June 20 reveal that accountants from Baker Tilly attended the vault to conduct an inventory check and found that nearly $113 million in client and customer assets were missing.

"In some instances, they found empty boxes at FSD with a customer’s or client’s name on it, or boxes that did not contain metal but instead held an “IOU” of sorts—a piece of paper stating the quantity of metal that should have been stored there," the document seen by Fortune continues.

It goes on to add that in some customer cases no records had been kept at all—not even an empty box with their name on it.

Further inventories seen by Fortune show that Baker Tilly had expected to find around 1.2 million Silver American Eagle coins and instead discovered just under 380,000.

Likewise, the accountants also expected to find 11,125 Gold American Eagle coins and discovered just 1,936.

As a result, attorneys for the CFTC allege that the defendants "misappropriated" the coins, either using or selling them for their own benefit.

The CFTC also claims that some customers who had paid for more bullions never got them, with the parties instead pocketing the cash.

The CFTC's director of enforcement, Ian McGinley, said he was committed to "rooting out fraud" in the precious metals market.

However, the body cautioned that although the damages had been awarded to customers there is no guarantee they will get the funds back as the defendants may not have enough assets.

Customers looking for updates on the case will be able to find them on the First State Depository Company website which has been taken over by administrators.

Representatives for Higgins did not immediately respond when approached by Fortune for comment.

<<<

---

>>> US puts sanctions on gold firms suspected of funding Russia's Wagner mercenaries

Reuters

By Daphne Psaledakis and Humeyra Pamuk

June 27, 2023

https://www.msn.com/en-us/money/markets/us-puts-sanctions-on-gold-firms-suspected-of-funding-russias-wagner-mercenaries/ar-AA1d7Hxq

WASHINGTON (Reuters) - The United States on Tuesday imposed sanctions on companies in the United Arab Emirates, Central African Republic and Russia, accusing them of engaging in illicit gold dealings to fund Russia's Wagner Group mercenary force.

The U.S. Treasury Department in a statement said it slapped sanctions on four companies connected to the Wagner Group and its leader, Yevgeny Prigozhin, and said the illicit gold dealings fund the militia to sustain and expand its armed forces, including in Ukraine and Africa.

"The Wagner Group funds its brutal operations in part by exploiting natural resources in countries like the Central African Republic and Mali. The United States will continue to target the Wagner Group’s revenue streams to degrade its expansion and violence in Africa, Ukraine, and anywhere else," the Treasury's Under Secretary for Terrorism and Financial Intelligence, Brian Nelson, said in the statement.

The U.S. State Department said that any action against Wagner was unrelated to an aborted mutiny last weekend.

Wagner has fought in Libya, Syria, the Central African Republic, Mali and other countries, and has fought the bloodiest battles of the 16-month war in Ukraine. It was founded in 2014 after Russia annexed Ukraine's Crimea peninsula and started supporting pro-Russia separatists in Ukraine's eastern Donbas region.

Central African Republic-based Midas Resources SARLU and Diamville SAU, UAE-based Industrial Resources General Trading and Russia-based Limited Liability Company DM were hit with sanctions in Tuesday's action.

Washington also imposed sanctions on Andrey Nikolayevich Ivanov, a Russian national the Treasury accused of being an executive in the Wagner Group and said worked closely with senior Malian officials on weapons deals, mining concerns and other Wagner activities in the country.

<<<

---

Franco-Nevada Corporation - >>> A Canada-based streaming and royalty company. It has a diversified portfolio, with agreements tied to gold, silver, the platinum group metals (PGMs), iron ore, and oil and gas. In the third quarter of 2022, 55% of its revenue came from gold.

https://www.fool.com/investing/stock-market/market-sectors/materials/gold-stocks/