News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Yes, but battle of analysts

deutsche has 13.00 target, wedbush 25.00

lool

MK

Not too shabby

22.88 now from 16.00ish, better qrtly

very nice

MK

Did you see this?

http://finance.yahoo.com/news/groupon-adds-credit-card-terminals-140759498.html

Groupon (GRPN) announced the addition of credit card terminals to the company’s existing payments suite for local businesses. Local businesses have three options to implement Groupon’s payments service on a credit card terminal: configure an existing Verifone (PAY) and Ingenico device; purchase a Verifone vx520 from Groupon for $150 with no monthly contract or fees; or rent a Verifone vx520 to own for $15 per month for 12 months.

Lol, looks like

I am posting to myself here

which is fine w me

this has been a good trader

MK

Shhhhhhh, don't scare it, lol

20.55

very nice now

MK

19.66 now from under 16.00

nice little atm

MK

New lo 15.34 on 6/14 some insider

buy after at 15.75

moving up a little now

MK

Payment solutions for iPod touch 5, iPhone 5 and iPad mini: VeriFone’s PAYware Mobile e315 and e335! Check out what these newest members of our PAYware Mobile family of solutions can do:

Accept All Forms of Payment: PAYware Mobile e315 and e335 meet both ISO 14443 and ISO 18092 standards, utilizing the latest technology so you can accept contactless and NFC payment applications, such as mobile wallets. Also, lower your total cost of ownership with an integrated EMV Level 1 and 2 approved smart card reader, allowing you to offer your customers a variety of payment options on one device.

Integrated Barcode Imager: Capture all 1D and 2D barcodes as well as still images and video. The embedded scanner provides unmatched flexibility for many applications, allows for quick price checks and improves inventory management productivity.

Charging Efficiencies: Available for both the iPad mini and iOS 5 devices, VeriFone’s smart charger simultaneously charges up to five PAYware Mobile devices, ensuring that you never lose power during crucial sales time. The perfect solution for the fast-paced enterprise setting.

Learn how the new and innovative PAYware Mobile e300 Series can work for your retail environment

Anyone who has snapped the jack off of their Square reader in the audio jack of their iOS device knows this is a far better solution. Even Verifone's e100 budget model is more retail hardened than Square. GO PAY

From 18.00 to 23.00 plus was nice

may have to wait a little more before re entry this time

looks like more weakness ahead

MK

23.80 better

MK

22.70 from 18.00 nice

MK

New EMV-Capable, Portable and Mobile Payment Solutions

Last night at the ETA 2013 Meeting and Expo (Booth #230), VeriFone Systems, Inc., introduced new countertop, portable and mobile payment systems and mobile POS software designed to meet the unique business needs of acquirers and ISOs.

The need for future-proof solutions continues to grow as EMV migration looms, consumer interest in mobile wallets and alternative payments increases, and merchants look to leverage the power and flexibility of mobility inside and outside the physical store. VeriFone is committed to delivering EMV and NFC-capable solutions that meet the unique needs of each channel partner, and the evolving needs of their merchant customers.

Clickhere to see the new EMV-capable, portable and mobile payment solutions VeriFone is introducing at this year's show.

It's now time for technical setup for this stock to break through resistance!!! This week will be big.

Das' Da' Point! Long or short, all positive.

PAY

technically an obvious potential gap fill .. I do not mind being long this one ..

More like a "CYA." That's why they filed it. Keep the dogs at bay. But it is not indefinite. At some point they will have to disclose the material. I'll be out by then ;)

$PAY filed a Confidential Treatment Order today, wonder what that is about?

http://yahoo.brand.edgar-online.com/default.aspx?companyid=658618

PAY

knives paying off here so far ..

News is that CEO is stepping down. Shares jumped to 22.25 after hours. C'mon $25!!!

20.99 nice from 18.00

reported today, got upgrade tgt 28.00

will hold unless something funky happens

MK

PAY

WEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE

eom

And so the recovery begins!

It should be up from here

I tried the same thing and got out before losing too much. This will come around. The company is still profitable, for crying out loud. Yesterday was a panic dump that will yield good opportunity fairly soon.

$PAY Daily Chart - Go Long For a 10% Gain Target ... Give it a One Dollar Stop Tp Protect Yourself pic.twitter.com/Cagwzh6yLP

I hear ya.. i got nailed on the bounce play after hours. Made some of it back and kept giving it back the more I played it. Shame on me. Worst loss in a while.

PAY Da lower da betta

Music to Da Ghost's earzzz

Aired dirty laundry yesterday ....... it's out there now .. everyone and their mother downgraded it today . Capitulation is inevitable IMHDGO .

after dat ... weeeeeeeeeeeee time .. .

Take em '

dive dive dive dive hehe

Da lower da betta

Take em

lol your getting short sells here?

how many shares?

Under $10 next week ... time to short ...MORE !

holy crap hitting 18.2s

it will bounce and will recover back to low 30s by next quarter results IMO

I played 'catch the falling knife'. However, in this type of market, this approach does not work. The market sentiment, imo, has turned negative. If it were still Tuesday of this week, my strategy may have worked. It did not so I've positioned myself to come back and fight another day. Good Luck.

It will bounce but most times 2 days so buy in thirds or forths

No bounce. Took my losses, licked my wounds, and moved on.

PAY

this is looking like a ridiculum opportunity ..

knives ! WEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE

i think its a play at these premarket levels

Purchased in the pre-market at $20.50. Seems overdone to me. Nothing really stands out as support on it's chart. $16 might be a target. We'll know soon enough!

Might drop below $21 on news imo.

$PAY news:

http://www.nasdaq.com/article/verifone-announces-preliminary-financial-results-for-the-first-fiscal-quarter-of-2013-20130220-01300

seems a bit overdone here at 28.35 but could test the 27s should be the bottom

It is, looking to buy back in around Friday most likely

this is getting attractive down here at 28.7 on watch

BTW is that your target?

will watch earnings might get some shares after market

|

Followers

|

10

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

135

|

|

Created

|

04/06/11

|

Type

|

Free

|

| Moderators | |||

Paymentus Holdings (PAY) has filed to raise $200 million in an IPO of its Class A common stock plus $50 million in a concurrent private placement, according to an S-1/A registration statement.

The firm provides bill payment software to companies and their customers worldwide.

PAY is growing impressively while producing earnings and free cash flow, so the IPO is worth a close look.

Redmond, Washington-based Paymentus was founded to develop a cloud-delivered payment technology stack for financial institutions and other businesses to provide omni-channel payment services with customers.

Management is headed by founder, Chairman and CEO Dushyant Sharma, who was previously co-founder of Derivion, a SaaS electronic billing company.

The company’s primary offering features include:

IPN - Instant Payment Network

Engagement

Presentment

Empowerment

Payment

Intelligence

Paymentus has received at least $30 million in equity investment from investors including Accel-KKR and Ashigrace LLC.

The firm seeks relationships with billers via a direct sales and marketing model and with no development or implementation fees required.

In 2020, the firm's platform generated more than 195 million transactions from a network of over 1,300 billers representing 16 million customers.

Sales and Marketing expenses as a percentage of total revenue have dropped as revenues have increased, as the figures below indicate:

| Sales and Marketing | Expenses vs. Revenue |

| Period | Percentage |

| Three Mos. Ended March 31, 2021 | 8.9% |

| 2020 | 10.6% |

| 2019 | 11.9% |

(Source)

The Sales and Marketing efficiency rate, defined as how many dollars of additional new revenue are generated by each dollar of Sales and Marketing spend, has increased to 2.8x in the most recent reporting period, as shown in the table below:

| Sales and Marketing | Efficiency Rate |

| Period | Multiple |

| Three Mos. Ended March 31, 2021 | 2.8 |

| 2020 | 2.1 |

(Source)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

PAY’s most recent calculation was 38% as of March 31, 2021, so the firm is close to meeting this metric, per the table below:

| Rule of 40 | Calculation |

| Recent Rev. Growth % | 33% |

| EBITDA % | 5% |

| Total | 38% |

(Source)

Management reported that its net dollar revenue retention rate for both 2019 and 2020 was greater than 117%.

A figure of over 100% indicates the company is generating additional revenue from the same cohort of customers, showing strong product/market fit and an efficient sales & marketing process, so Paymentus has performed well in this regard.

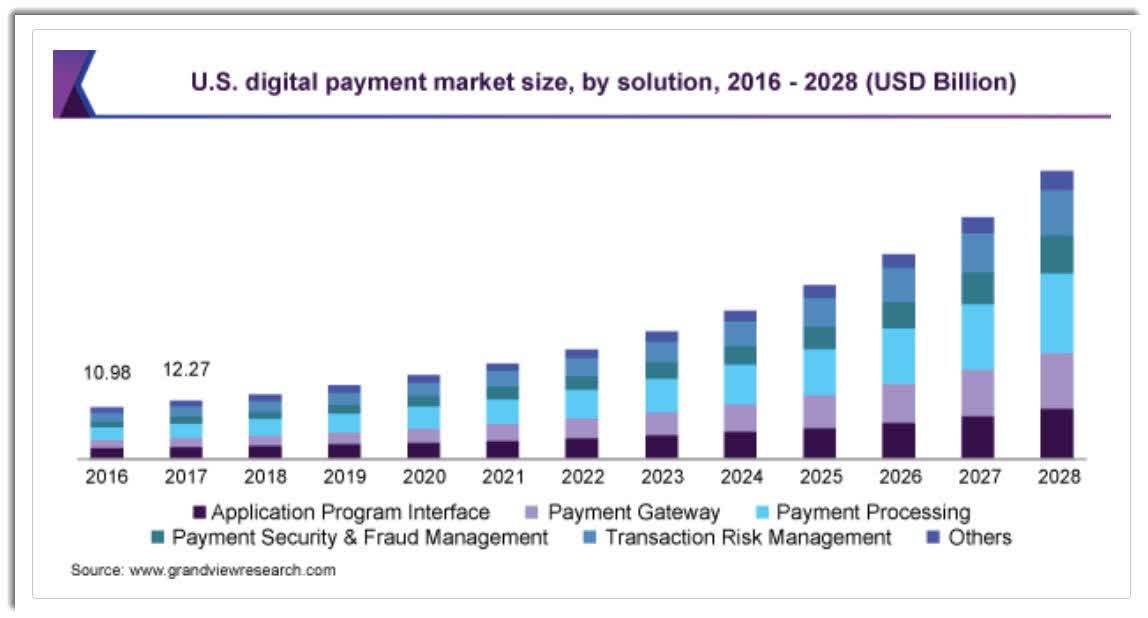

According to a 2021 market research report by Grand View Research, the global market for digital payments (as a proxy) was an estimated $58.3 billion in 2020 and is expected to reach $241 billion in 2028.

This represents a forecast very strong CAGR of 19.4% from 2021 to 2028.

The main drivers for this expected growth are continued high adoption of smartphones, growth in e-commerce and rising internet penetration and adoption of online payment technologies.

Also, the chart below shows the historical and projected U.S. digital payments market by solution type, from 2016 to 2028:

Major competitive or other industry participants by type include:

Legacy solution providers

Internal financial institution systems

Phone-based payments

Paymentus’ recent financial results can be summarized as follows:

Growing topline revenue, at an accelerating rate of growth

Increasing gross profit but reduced gross margin

Growing operating profit and net income

Uneven but upwardly trending cash flow from operations

Below are relevant financial results derived from the firm’s registration statement:

| Total Revenue | ||

| Period | Total Revenue | % Variance vs. Prior |

| Three Mos. Ended March 31, 2021 | $ 92,222,000 | 32.5% |

| 2020 | $ 301,767,000 | 28.0% |

| 2019 | $ 235,778,000 | |

| Gross Profit (Loss) | ||

| Period | Gross Profit (Loss) | % Variance vs. Prior |

| Three Mos. Ended March 31, 2021 | $ 27,547,000 | 32.6% |

| 2020 | $ 92,627,000 | 24.4% |

| 2019 | $ 74,434,000 | |

| Gross Margin | ||

| Period | Gross Margin | |

| Three Mos. Ended March 31, 2021 | 29.87% | |

| 2020 | 30.69% | |

| 2019 | 31.57% | |

| Operating Profit (Loss) | ||

| Period | Operating Profit (Loss) | Operating Margin |

| Three Mos. Ended March 31, 2021 | $ 4,853,000 | 5.3% |

| 2020 | $ 18,428,000 | 6.1% |

| 2019 | $ 18,371,000 | 7.8% |

| Net Income (Loss) | ||

| Period | Net Income (Loss) | |

| Three Mos. Ended March 31, 2021 | $ 2,278,000 | |

| 2020 | $ 8,525,000 | |

| 2019 | $ 9,000,000 | |

| Cash Flow From Operations | ||

| Period | Cash Flow From Operations | |

| Three Mos. Ended March 31, 2021 | $ 7,177,000 | |

| 2020 | $ 35,620,000 | |

| 2019 | $ 17,511,000 | |

(Source)

As of March 31, 2021, Paymentus had $49.6 million in cash and $45.4 million in total liabilities.

Free cash flow during the twelve months ended March 31, 2021, was $22.3 million.

Paymentus intends to raise $200 million in gross proceeds from an IPO of its Class A common stock, offering 10 million shares at a proposed midpoint price of $20.00 per share.

Investors have indicated a non-binding interest to purchase up to $60 million of Class A shares in the IPO.

Existing investor Accel-KKR has agreed to purchase $50 million of Class A shares in a concurrent private placement and at the same price as the IPO.

Class A common stockholders will be entitled to one vote per share and Class B shareholders will receive ten votes per share.

The S&P 500 Index no longer admits firms with multiple classes of stock into its index.

Assuming a successful IPO, the company’s enterprise value at IPO would approximate $2.3 billion, excluding the effects of underwriter over-allotment options.

Excluding effects of underwriter options and private placement shares or restricted stock, if any, the float to outstanding shares ratio will be approximately 8.62%.

Management says it will use the net proceeds from the IPO as follows:

We intend to use approximately $57.4 million of the net proceeds from this offering to redeem all of our issued and outstanding shares of Series A preferred stock (including accrued dividends), substantially all of which are held by AKKR and our founder and chief executive officer. We intend to use the remainder of the net proceeds from this offering and the concurrent private placement for general corporate purposes, including working capital, operating expenses and capital expenditures. Additionally, we may use a portion of the net proceeds to acquire or invest in businesses, products, services or technologies. (Source)

Management’s presentation of the company roadshow is available here.

Listed bookrunners of the IPO are Goldman Sachs, J.P. Morgan, BofA Securities, Citigroup, Baird, Nomura, Raymond James, Wells Fargo Securities, Fifth Third Securities, PNC Capital Markets, AmeriVet Securities and C.L. King & Associates.

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] | Amount |

| Market Capitalization at IPO | $2,319,584,740 |

| Enterprise Value | $2,269,945,740 |

| Price / Sales | 7.15 |

| EV / Revenue | 7.00 |

| EV / EBITDA | 115.98 |

| Earnings Per Share | $0.08 |

| Float To Outstanding Shares Ratio | 8.62% |

| Proposed IPO Midpoint Price per Share | $20.00 |

| Net Free Cash Flow | $22,255,000 |

| Free Cash Flow Yield Per Share | 0.96% |

| Revenue Growth Rate | 32.52% |

(Source)

As a reference, a potential partial public comparable to PAY would be Fiserv (FISV); below is a comparison of their primary valuation metrics:

| Metric | Fiserv (FISV) | Paymentus (PAY) | Variance |

| Price / Sales | 5.16 | 7.15 | 38.6% |

| EV / Revenue | 6.58 | 7.00 | 6.3% |

| EV / EBITDA | 19.46 | 115.98 | 496.0% |

| Earnings Per Share | $1.28 | $0.08 | -93.8% |

| Revenue Growth Rate | 19.1% | 32.52% | 69.89% |

Paymentus is seeking public investment to redeem its Series A preferred stock and for its corporate expansion plans

The firm’s financials indicate increasing topline revenue and at an accelerating rate and growing operating and net profits.

Free cash flow for the twelve months ended March 31, 2021 was a reasonable $22.3 million.

Sales and Marketing expenses as a percentage of total revenue dropped as revenue has increased; its Sales and Marketing efficiency rate rose to 2.8x.

Additionally, the company’s Rule of 40 metric performance nearly cleared this hurdle and its dollar-based net retention rate was an impressive 117%, for both 2019 and 2020.

The market opportunity for providing legacy financial billers with modern software solutions is significant and the firm should enjoy very positive industry dynamics in its favor, especially after the COVID-19 pandemic and its effects on increasing consumer adoption of digital technologies.

Goldman Sachs is the lead left underwriter and IPOs led by the firm over the last 12-month period have generated an average return of 25.8% since their IPO. This is a mid-tier performance for all major underwriters during the period.

One risk to the company’s outlook is that it relies on U.S. Bank and JPMorgan Chase along with a payroll solutions provider (among others) to refer new billers to its platform, so if any of these referral relationships were to end, it may negatively impact the firm’s growth trajectory.

As for valuation, compared to much larger and diversified Fiserv, the IPO appears reasonably valued, as FISV is growing revenue more slowly although producing higher EPS.

Paymentus appears to be growing impressively due to its focus on modernizing the biller space while producing earnings and free cash flow, so the IPO is worth consideration.

Expected IPO Pricing Date: May 25, 2021

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |