News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

sold today couldnt leave the good day unnoticed

will look for more on dip

whose bullish and whose bearish? beat on next earnings?

price target of $54.80, but still waiting for a little more downside back into the $27's

i think it will be good over the winter season and into the spring with nice earnings. They will beat square and will continue to bring newer technology into the market.

on watch here at 28.5

sold at 29.07

will look doe more shares in indiviudual account this week for 1%-2% move

i got 300 in ira at 27.97 i could have sold at eod for a steak dinner will look for big position in individual account tommorrow

ahhh pay bouncing missed 1% if volume increases may jump at 28.3

got down to 30.13 and then crept toward 30.50 had to leave so pulled order. Down big today I cant help but to be cautious even though I have no Idea why its down 7% even in red day this looks extremely over done

first buy order on 52 week low

looking to get back in this week on watch now

21st Century Billing & PAY Solutions

I've been following and investing in the billing and PAYment service industry since 1998.

Card swipe encryption devices add another layer of security that ernables transactions, regardless of origin, to move from A-B, in-between and through the ACH (automatic clearinghouse) without being compromised.

An iRemotePay dot com video displays Apple PDAs (personal data assistants) a sturdy clip-on card reading encryption device and cards of networking opportunity with MasterCard & Visa Logos.

21st Century PAYment methods can hone-to-perfection with help from back-office bill and PAY modular servers, enabled to adjust and re-adjust, when its discovered that transactions are being compromised. A private company called FutureX has been in business for 30yrs. PAY and others that adopt a FutureX type encryption server that can handle and process 2250 iRemotePAY transactions per second, will enabled back-office ASPs (appliction service providers) to stay globally competitive imo.

State-of-the-Art encryption, Dial-UP & Deal!

ASP42001

got a bit more return than expected but got out early

yeah I would be looking for a 1 % move then out

Well percentage wise yes lol...I dumped 99% of the shares, kept a tiny bit to always keep an eye on her lol

yeah you have to be pretty red by now

My next move...lol

Wow this thing has been gutted. May buy if the bleed continues tommorow

Anyone have a thought on after hours today. Good news? Bad news?

Not sure if it just got downgraded

Smoke and mirrors so their buddies can get cheepies IMO...Verifone is everywhere and will report solid earnings...revenues and future guidance are what investors want to see and IMO PAY will deliver...

The market has me second guessing everything, even if they have a good report it could drop with one little thing. Do you think it's going to rise? Not sure if it just got downgraded, how low it will go

You should buy on this dip IMO

Sorry, I tried to delete this, got my stocks mixed up. My bad. I was checking on this one to see if it was getting anywhere, I should have sold yesterday but it was looking better

Who upgraded it the other day? And what was that price target again????

So the other day it was upgraded and price target at 8 and today it drops this big?

Downgraded by UBS

why the droppage this am?

VeriFone to Report Third Quarter 2012 Results on September 5, 2012

Aug 1, 201208:00:01 (ET)

SAN JOSE, Calif., Aug 01, 2012 (BUSINESS WIRE) -- VeriFone Systems, Inc. (PAY, Trade ) will release its financial results for the third quarter of fiscal 2012 after the market closes on September 5, 2012.

The management of VeriFone will host a conference call to review the financial results on September 5, 2012, at 1:30 pm (PT). In addition to discussing VeriFone's third quarter results, management may provide forward looking guidance on the call.

To access the audio webcast with slides, please go to VeriFone's website ( http://ir.verifone.com ) at least ten minutes prior to the call to register. The recorded audio webcast will be available onVeriFone's website until September 12, 2012.

To hear the live conference call by phone, please dial the following numbers:

Domestic callers: 800.215.2410 International callers: +1.617.597.5410 Passcode: 1251 3850

To hear areplay of the conference call, which will be available until September 12, 2012, please dial the following numbers:

Domestic callers: 888.286.8010 International callers: +1.617.801.6888 Passcode: 8713 4846

Additional Resources: http://ir.verifone.com

About VeriFone Systems, Inc. ( www.verifone.com )

VeriFone Systems, Inc. ("VeriFone") (PAY, Trade ) is the global leader in secure electronic payment solutions. VeriFone provides expertise, solutions and services that add value to the point of sale with merchant-operated, consumer-facing and self-service payment systems for the financial, retail, hospitality, petroleum, government and healthcare vertical markets. VeriFone solutions are designed to meet the needs of merchants, processors and acquirers in developed and emerging economies worldwide.

SOURCE: VeriFone Systems, Inc.

VeriFone Systems, Inc. Investor Contact: Doug Reed, 408-232-7979 ir@verifone.com or Editorial Contact: VeriFone Media Relations Pete Bartolik, 508-283-4112 pete_bartolik@verifone.com

Are they the suppliers to Google for their contact-less trials (with Android phones?).

I mean of course the vendors who will be part of the trial not for stuff inside the phones.

Anyone know how many US point of sale systems have contact-less capabilities?

Good news on Singapore taxi contract but would like to see a big US vendor (7-eleven?) going contact-less as well.

Yes interesting stock. I am thinking of writing covered calls on PAY,... very high return.

Maybe stupid question,.. is Paypal their competition?

Thanks

This is the future of electronic payment services. It is on a major uptrend & still has tons of future value to consider. For example, Verifone Systems, Inc. is introducing NFC payment systems to society. These will enable us to purchase our products via our smartphones...just like a credit card. The future is exciting for Verifone ... it might not be full of the glamour offered by companies such as Apple, but this seems to be a pretty safe bet.

|

Followers

|

10

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

135

|

|

Created

|

04/06/11

|

Type

|

Free

|

| Moderators | |||

Paymentus Holdings (PAY) has filed to raise $200 million in an IPO of its Class A common stock plus $50 million in a concurrent private placement, according to an S-1/A registration statement.

The firm provides bill payment software to companies and their customers worldwide.

PAY is growing impressively while producing earnings and free cash flow, so the IPO is worth a close look.

Redmond, Washington-based Paymentus was founded to develop a cloud-delivered payment technology stack for financial institutions and other businesses to provide omni-channel payment services with customers.

Management is headed by founder, Chairman and CEO Dushyant Sharma, who was previously co-founder of Derivion, a SaaS electronic billing company.

The company’s primary offering features include:

IPN - Instant Payment Network

Engagement

Presentment

Empowerment

Payment

Intelligence

Paymentus has received at least $30 million in equity investment from investors including Accel-KKR and Ashigrace LLC.

The firm seeks relationships with billers via a direct sales and marketing model and with no development or implementation fees required.

In 2020, the firm's platform generated more than 195 million transactions from a network of over 1,300 billers representing 16 million customers.

Sales and Marketing expenses as a percentage of total revenue have dropped as revenues have increased, as the figures below indicate:

| Sales and Marketing | Expenses vs. Revenue |

| Period | Percentage |

| Three Mos. Ended March 31, 2021 | 8.9% |

| 2020 | 10.6% |

| 2019 | 11.9% |

(Source)

The Sales and Marketing efficiency rate, defined as how many dollars of additional new revenue are generated by each dollar of Sales and Marketing spend, has increased to 2.8x in the most recent reporting period, as shown in the table below:

| Sales and Marketing | Efficiency Rate |

| Period | Multiple |

| Three Mos. Ended March 31, 2021 | 2.8 |

| 2020 | 2.1 |

(Source)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

PAY’s most recent calculation was 38% as of March 31, 2021, so the firm is close to meeting this metric, per the table below:

| Rule of 40 | Calculation |

| Recent Rev. Growth % | 33% |

| EBITDA % | 5% |

| Total | 38% |

(Source)

Management reported that its net dollar revenue retention rate for both 2019 and 2020 was greater than 117%.

A figure of over 100% indicates the company is generating additional revenue from the same cohort of customers, showing strong product/market fit and an efficient sales & marketing process, so Paymentus has performed well in this regard.

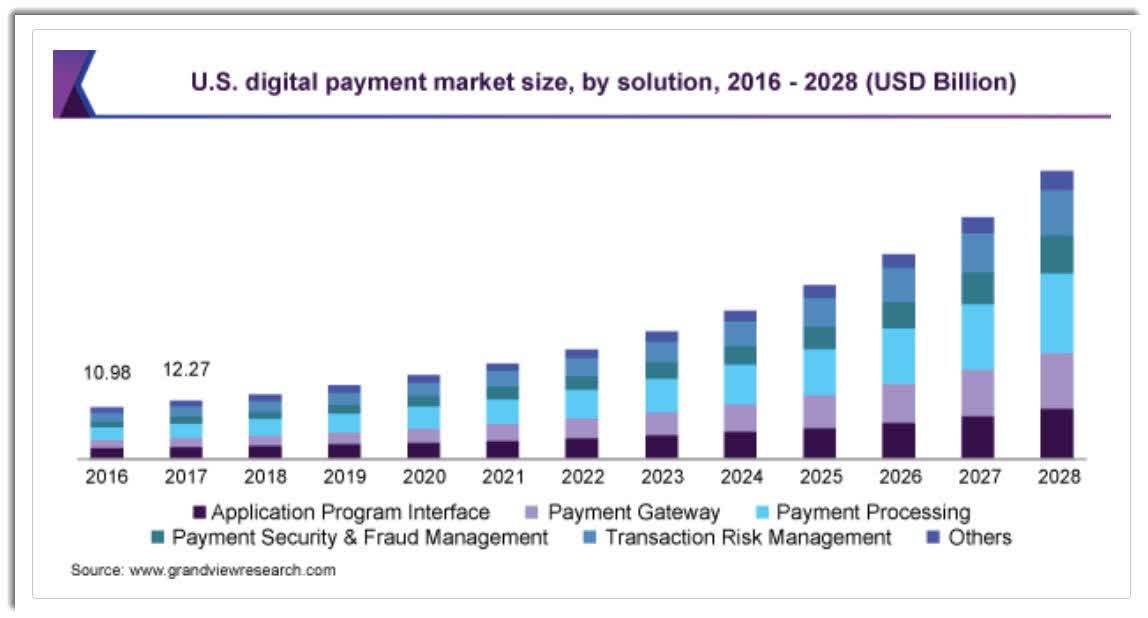

According to a 2021 market research report by Grand View Research, the global market for digital payments (as a proxy) was an estimated $58.3 billion in 2020 and is expected to reach $241 billion in 2028.

This represents a forecast very strong CAGR of 19.4% from 2021 to 2028.

The main drivers for this expected growth are continued high adoption of smartphones, growth in e-commerce and rising internet penetration and adoption of online payment technologies.

Also, the chart below shows the historical and projected U.S. digital payments market by solution type, from 2016 to 2028:

Major competitive or other industry participants by type include:

Legacy solution providers

Internal financial institution systems

Phone-based payments

Paymentus’ recent financial results can be summarized as follows:

Growing topline revenue, at an accelerating rate of growth

Increasing gross profit but reduced gross margin

Growing operating profit and net income

Uneven but upwardly trending cash flow from operations

Below are relevant financial results derived from the firm’s registration statement:

| Total Revenue | ||

| Period | Total Revenue | % Variance vs. Prior |

| Three Mos. Ended March 31, 2021 | $ 92,222,000 | 32.5% |

| 2020 | $ 301,767,000 | 28.0% |

| 2019 | $ 235,778,000 | |

| Gross Profit (Loss) | ||

| Period | Gross Profit (Loss) | % Variance vs. Prior |

| Three Mos. Ended March 31, 2021 | $ 27,547,000 | 32.6% |

| 2020 | $ 92,627,000 | 24.4% |

| 2019 | $ 74,434,000 | |

| Gross Margin | ||

| Period | Gross Margin | |

| Three Mos. Ended March 31, 2021 | 29.87% | |

| 2020 | 30.69% | |

| 2019 | 31.57% | |

| Operating Profit (Loss) | ||

| Period | Operating Profit (Loss) | Operating Margin |

| Three Mos. Ended March 31, 2021 | $ 4,853,000 | 5.3% |

| 2020 | $ 18,428,000 | 6.1% |

| 2019 | $ 18,371,000 | 7.8% |

| Net Income (Loss) | ||

| Period | Net Income (Loss) | |

| Three Mos. Ended March 31, 2021 | $ 2,278,000 | |

| 2020 | $ 8,525,000 | |

| 2019 | $ 9,000,000 | |

| Cash Flow From Operations | ||

| Period | Cash Flow From Operations | |

| Three Mos. Ended March 31, 2021 | $ 7,177,000 | |

| 2020 | $ 35,620,000 | |

| 2019 | $ 17,511,000 | |

(Source)

As of March 31, 2021, Paymentus had $49.6 million in cash and $45.4 million in total liabilities.

Free cash flow during the twelve months ended March 31, 2021, was $22.3 million.

Paymentus intends to raise $200 million in gross proceeds from an IPO of its Class A common stock, offering 10 million shares at a proposed midpoint price of $20.00 per share.

Investors have indicated a non-binding interest to purchase up to $60 million of Class A shares in the IPO.

Existing investor Accel-KKR has agreed to purchase $50 million of Class A shares in a concurrent private placement and at the same price as the IPO.

Class A common stockholders will be entitled to one vote per share and Class B shareholders will receive ten votes per share.

The S&P 500 Index no longer admits firms with multiple classes of stock into its index.

Assuming a successful IPO, the company’s enterprise value at IPO would approximate $2.3 billion, excluding the effects of underwriter over-allotment options.

Excluding effects of underwriter options and private placement shares or restricted stock, if any, the float to outstanding shares ratio will be approximately 8.62%.

Management says it will use the net proceeds from the IPO as follows:

We intend to use approximately $57.4 million of the net proceeds from this offering to redeem all of our issued and outstanding shares of Series A preferred stock (including accrued dividends), substantially all of which are held by AKKR and our founder and chief executive officer. We intend to use the remainder of the net proceeds from this offering and the concurrent private placement for general corporate purposes, including working capital, operating expenses and capital expenditures. Additionally, we may use a portion of the net proceeds to acquire or invest in businesses, products, services or technologies. (Source)

Management’s presentation of the company roadshow is available here.

Listed bookrunners of the IPO are Goldman Sachs, J.P. Morgan, BofA Securities, Citigroup, Baird, Nomura, Raymond James, Wells Fargo Securities, Fifth Third Securities, PNC Capital Markets, AmeriVet Securities and C.L. King & Associates.

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] | Amount |

| Market Capitalization at IPO | $2,319,584,740 |

| Enterprise Value | $2,269,945,740 |

| Price / Sales | 7.15 |

| EV / Revenue | 7.00 |

| EV / EBITDA | 115.98 |

| Earnings Per Share | $0.08 |

| Float To Outstanding Shares Ratio | 8.62% |

| Proposed IPO Midpoint Price per Share | $20.00 |

| Net Free Cash Flow | $22,255,000 |

| Free Cash Flow Yield Per Share | 0.96% |

| Revenue Growth Rate | 32.52% |

(Source)

As a reference, a potential partial public comparable to PAY would be Fiserv (FISV); below is a comparison of their primary valuation metrics:

| Metric | Fiserv (FISV) | Paymentus (PAY) | Variance |

| Price / Sales | 5.16 | 7.15 | 38.6% |

| EV / Revenue | 6.58 | 7.00 | 6.3% |

| EV / EBITDA | 19.46 | 115.98 | 496.0% |

| Earnings Per Share | $1.28 | $0.08 | -93.8% |

| Revenue Growth Rate | 19.1% | 32.52% | 69.89% |

Paymentus is seeking public investment to redeem its Series A preferred stock and for its corporate expansion plans

The firm’s financials indicate increasing topline revenue and at an accelerating rate and growing operating and net profits.

Free cash flow for the twelve months ended March 31, 2021 was a reasonable $22.3 million.

Sales and Marketing expenses as a percentage of total revenue dropped as revenue has increased; its Sales and Marketing efficiency rate rose to 2.8x.

Additionally, the company’s Rule of 40 metric performance nearly cleared this hurdle and its dollar-based net retention rate was an impressive 117%, for both 2019 and 2020.

The market opportunity for providing legacy financial billers with modern software solutions is significant and the firm should enjoy very positive industry dynamics in its favor, especially after the COVID-19 pandemic and its effects on increasing consumer adoption of digital technologies.

Goldman Sachs is the lead left underwriter and IPOs led by the firm over the last 12-month period have generated an average return of 25.8% since their IPO. This is a mid-tier performance for all major underwriters during the period.

One risk to the company’s outlook is that it relies on U.S. Bank and JPMorgan Chase along with a payroll solutions provider (among others) to refer new billers to its platform, so if any of these referral relationships were to end, it may negatively impact the firm’s growth trajectory.

As for valuation, compared to much larger and diversified Fiserv, the IPO appears reasonably valued, as FISV is growing revenue more slowly although producing higher EPS.

Paymentus appears to be growing impressively due to its focus on modernizing the biller space while producing earnings and free cash flow, so the IPO is worth consideration.

Expected IPO Pricing Date: May 25, 2021

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |