News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

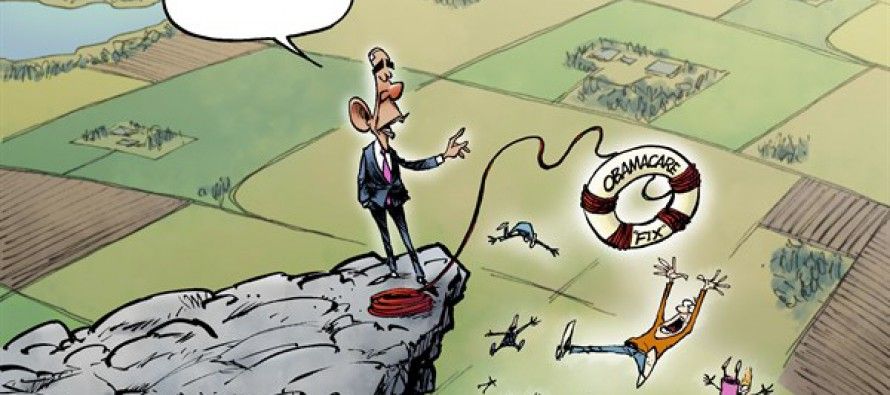

It is going to be an important debate point for the president hopefuls. Increasingly divisive too.

Leave it alone...You can't help stupid.

You are an easy mark. Congrats ;)

all you gotta do is learn the truth rather than the lies of the communist fake media.. Your account would be 10x bigger, but than again, why am I wasting my time with someone who likes to be lied to.?.... Here I will help you out. http://www.judicialwatch.org/document-archive/

I know plenty of Secret Service agents and they all said the same thing... obama and hillary were both created by the CIA... But you wouldnt know this type of knowledge. You are a new yorker where stupidity is a moral.

Thinking..., the NSA, National Security Agency, as well the Secret Service, should be alerted to your beliefs about President Obama.

WTF? what kind of a dysfunctional comment is that?

Explain why you are not Locked Up ?

Study: Deductibles Skyrocketing Under Obamacare

By Sean Moran

9 Aug 2018

Deductibles continue to rise under Obamacare, according to a study released this week.

Average health insurance deductibles and the number of Americans with high-deductible health insurance plans continue to rise under the Affordable Care Act (ACA).

High-deductible plans require Americans to pay more out of pocket for their medical expenses, including medical expenses and hospital procedures.

In 2006, 11.4 percent of private sector employees had a high-deductible plan compared to 2016. Now, 46.5 percent of Americans have a high-deductible plan. Roughly half of the workers with a high-deductible plan get an employer contribution to a health savings account (HSA) or a health reimbursement arrangement (HRA).

Small businesses tend to offer high deductibles more often than larger corporations. At the smallest companies, about two-thirds of workers did not have the option of a plan without a high deductible and did not receive an employer contribution from an HSA or HRA.

Premiums have continued to rise under Obamacare, as well.

The Centers for Medicare and Medicaid (CMS) released a report in July sh0wing that average Obamacare monthly premiums increased by 27 percent in 2018, which was even higher than 2017’s 21 percent rate hike. In May 2017, a Department of Health and Human Services (HHS) report found that average health insurance premiums doubled since 2013.

Meanwhile, roughly 30 million Americans continue to go without health insurance. In 2012, the Congressional Budget Office (CBO) predicted that Obamacare exchange enrollment would increase by nine million by 2016. In reality, only 400,000 Americans signed up on the Obamacare exchange, which is 96 percent lower than the CBO’s estimate of Obamacare exchange growth.

To combat the increasing costs of health care under Obamacare, the Donald Trump administration released a rule in August that expanded short-term, limited-duration health insurance plans. Short-term plans may cost approximately a third of the cost of an Obamacare plan.

The average monthly premium for a short-term plan in the fourth quarter of 2016 was $124 per month, while an unsubsidized Obamacare plan costs $393 per month. Trump also released a rule that expanded Association Health Plans (AHPs), which would allow businesses and associations to band together and offer Americans more affordable health insurance options compared to Obamacare.

Sen. Rand Paul (R-KY) lauded the expansion of AHPs and short-term health insurance in October as the “biggest free-market health care reform in a generation.”

https://www.breitbart.com/big-government/2018/08/09/study-deductibles-skyrocketing-obamacare/

US Healthcare: Beyond the Ability of Cosmetics To Hide Its Ugliness

Steven Brill on Obamacare

More Breast and Prostate Cancer Deaths Under Obamacare

Latest statistics show that former President Barack Obama was wrong — horribly wrong — when he had Obamacare cut the number of mammograms and PSA tests allowed.

It turns out that these were not superfluous, unnecessary tests after all.

A New York Post Op-Ed by health care expert Betsy McCaughey of the London Center for Policy Research noted that cutting the number of tests allowed has led to later diagnoses and more serious outcomes for patients of both breast and prostate cancer.

The consensus in the medical community — before Obama — was that women over the age of 40 should have annual mammograms.

But in 2009, Obama’s Preventative Services Task Force cut back the recommendation to mammograms every two years, starting at age 50.

And the panel cut back on its payments for more frequent testing.

Now, Dr. Elisa Port, chief of breast surgery at Mount Sinai Hospital in New York, has reported that women who accepted the recommendation and only got mammograms every other year were more likely to be diagnosed with later-stage cancer, more likely to need mastectomies and chemotherapy, and more burdened with cancer that spread to their lymph nodes.

Likewise, Obama’s panel recommended against annual PSA tests for men to detect prostate cancer.

The panel said that for each man found to have prostate cancer, the PSA test showed five more with false positives.

But it turned out that it was worth the inconvenience and added anxiety.

In the years since the Preventative Services Task Force recommended the discontinuation of annual PSA tests, more men have been diagnosed with prostate cancer and at later stages.

And last year, McCaughey wrote, “the Annals of Internal Medicine showed that PSA tests reduce prostate-cancer deaths by almost one-third.”

The Obama task force has now dropped its decision to reduce PSA tests.

Over the next few years, we can expect gloomy data just like this to show us how fatuous and naive Obama was being when he claimed Obamacare was only cutting unnecessary tests and procedures that we didn’t really need in the first place.

https://www.westernjournal.com/dick-morris-more-breast-and-prostate-cancer-deaths-under-obamacare/?utm_source=Email&utm_medium=patriotupdate&utm_campaign=dailyam&utm_content=libertyalliance

THIS IS WHY OUR GOVERNMENT SHOULD NOT BE IN CHARGE OF OUR HEALTHCARE!

Trump tried to repeal or repair Obamacare but he can't do it without the support of the Congress and Senate and we know the RINOS are against him and there is no across the aisle support.

It is a miracle that he was able to get his tax bill passed.

He should fulfill his promise on this

Nearly 22,000 ‘truly needy’ people died waiting for Medicaid under Obamacare

President Barack Obama’s biggest legislative “accomplishment,” and a major part of his legacy, is the Affordable Care Act, also known as “Obamacare.” While it was hailed as a remedy to the supposed health care crisis, it ended up being one of the worst scams ever perpetrated on the American people.

Now the true cost of Obamacare is becoming known—and that cost is being measured in not just dollars, but human lives. A new study by the Foundation for Government Accountability (FGA) found that nearly 22,000 “truly needy” Americans have died while languishing on Medicaid waiting lists — even as Medicaid expansions under Obamacare enrolled millions of able-bodied people.

Obamacare Penalizes the Truly Needy

Obamacare was sold to Americans on the premise helping the needy get medical coverage. As recently as late 2016, liberal media outlets were still touting the benefits of Obamacare while claiming that then-presidential candidate Hillary Clinton was the better presidential candidate in part because she would uphold the controversial act.

And yet, people with critical needs still aren’t getting the help they need.

Skylar Overman, an Arkansas girl born with a rare condition that requires full-time care, waited for over 10 years on a Medicaid waiting list to get the help she needed — and as of last fall, she’s still waiting, even as Arkansas expanded Medicaid to enroll nearly 300,000 people.

According to the FGA study, the home and community-based waiver services program, or HCBS, allows states to extend Medicaid services to people who might otherwise be institutionalized. HCBS recipients include people like Skylar, who have “severe intellectual disabilities, traumatic brain injuries, spinal cord injuries, and mental illnesses, among other debilitating conditions.”

Under the program, people who would qualify for a nursing home or another long-term care institution can instead receive needed services at home or on an outpatient basis. As FGA explains:

Benefits for these vulnerable individuals can include homemaker or home health aide services, personal care, adult day health care, habilitation, respite care, day treatment, psycho-social rehabilitation services, clinic services for individuals with chronic mental illness, and more.

However, states can also limit enrollment — and after the cap is reached, applicants are placed on waiting lists. Some wait for years, even decades.

Medicaid Expansion Diverts Funds

Under Obamacare, many states opted to expand Medicaid in 2016, spending billions to enroll “a new class of able-bodied adults,” while at the time, these same states had nearly 250,000 needy people on their HCBS waiting lists. As the FGA study authors point out:

While Obamacare did not create these waiting lists, it is increasing the likelihood that truly needy individuals will never get the help they need by diverting billions of dollars to able-bodied adults.

In Maryland, nearly 300,000 more able-bodied adults signed up for Medicaid under the Obamacare expansion, 103% than the program could hold. Meanwhile, 8,495 Maryland residents died while waiting on the state’s HCBS waiting list.

In Louisiana, over 450,000 people have been enrolled under the Medicare expansion. But over 5,000 people died while still waiting for HCBS services.

Overall, nearly 22,000 people have died while still waiting for services, according to records from a dozen states obtained by the FGA. But since some states don’t keep records of waiting list deaths, the real number is likely even higher.

How Can This Be?

Obamacare was designed to help the needy—at least that’s what Americans were told. Now, billions of dollars are being spent to provide coverage for healthy Americans — and the needy are still waiting for help.

President Donald Trump has said he would repeal Obamacare and “develop a great new health care plan.” He faces an uphill battle, but unless he can fulfill that promise, more Americans will die while waiting for help that isn’t coming.

https://www.conservativeinstitute.org/healthcare/22000-died-medicaid-obamacare.htm?utm_source=boomtrain&utm_medium=automated&utm_campaign=ci1&utm_source=boomtrain&utm_medium=automated&utm_campaign=ci1

Report: 3.2 Million Americans Will Drop Obamacare for Association Health Plans

By Sean Moran

1 Mar 2018

A study from Avalere Health released on Wednesday found that 3.2 million Americans will leave Obamacare for more affordable options such as Association Health Plans (AHPs), thanks to President Donald Trump’s executive orders on health care.

Dan Mendelson, president of Avalere Health, said, “Consumers are always looking for a new low-cost health insurance option but migration of healthy people to a new product will ultimately take a toll on what is presently being sold in the market.”

AHPs are health insurance pools sponsored by an industry, trade, or professional association that provides health coverage to their members.

President Trump signed an executive order in October that expanded AHPs, as well as short-term limited-duration insurance plans to offer Americans more affordable options compared to Obamacare.

“This will cost the United States government virtually nothing and will provide people great, great health care,” Trump said in October.

Avalere found that by 2022, one million Americans would move out of the Obamacare individual market to join AHPs, and 2.2 million people would drop out of the small-group market to join an AHP as well.

The study also revealed that Americans would experience drastically lower health premiums through AHPs compared to Obamacare.

AHPs would be roughly $2,900 lower per year compared to the small-group market and $9,700 lower per year compared to the individual market.

Avalere cites that the lower average premiums in AHPs mostly result from a healthier insurance pool due to “risk selection,” and less generous offerings.

Chris Sloan, senior manager at Avalere, explained, “The proposed rule would lead to millions of individuals and small businesses shifting into a new form of coverage, likely reducing their premiums, but leading to higher premiums in the markets they leave behind.”

President Trump argued last week that, “Piece by piece by piece, Obamacare is being wiped out!”

Sen. Rand Paul (R-KY) praised the action last October as “the biggest free-market reform of health care in a generation.”

http://www.breitbart.com/big-government/2018/03/01/report-3-2-million-americans-will-drop-obamacare-for-association-health-plans/

***Does it really matter...Same crap..Different day.. :+O

I see your handle is 'Past and present' so I'm wondering if you have something newer than 2013...?

NASCAR fans! WIN IHUB SUBSCRIPTIONS

ENTER NOW, FIRST RACE IS THIS SUNDAY!

Feel free to join us on the Monster Energy Board for our NASCAR contests.

https://investorshub.advfn.com/A-Monster-Energy-Nascar-Challenge-3206/

We run a main season long contest for the 36 regular season races--simple format of picking 3 cars/race each week...prizes awarded at the end of the season!

we also run 2 side contests:

1. The Playoffs--consists of the 10 playoff races

2. our non-points contest--consists of the 5 NASCAR non-point events.

Non-points contest starts Sun Feb 11th and the main contest starts with the Daytona 500 Sun Feb 18th!

Boogity Boogity Boogity!!

Two countries, one insurance plan: San Diego workers find medical care in Tijuana

A patient receives dental care at the SIMNSA outpatient medical center in Tijuana near the San Ysidro Port of Entry. Many of the patients are San Diego workers on a cross-border health plan licensed by the state of California.

An electrician from San Diego, a hotel food services employee from Serra Mesa and a golf course groundskeeper from Oceanside all found themselves among the dozens of patients at the same Tijuana medical facility on a recent weekday morning.

One came for a therapeutic massage and to fill a prescription, another to see a nutritionist, the third to have his adolescent son’s persistent cough checked out.

Although their jobs are in the United States, their health care is in Mexico.

On this rainy January morning, the workers and their dependent family members have converged at an eight-story building just yards from the U.S. border.

Patients come to SIMNSA for everything from dental care to medical tests to physical therapy to consultations with specialists—all covered under SIMNSA’S cross-border health plan.

Nobody here is complaining about crossing the border; in fact, many of them prefer it this way.

The co-pay for a doctor’s visit is typically $7, a fraction of what they would pay in the United States, and there are no out-of-pocket deductibles on the plan. Many are Baja California residents or have family members on the plan who live in Mexico.

Amid uncertainty over the future of U.S. healthcare, large numbers of U.S. patients continue to cross to Mexico for medical appointments. Mexico’s lower costs have long offered alternatives for U.S. uninsured patients or those in search of elective procedures not covered by their plans.

A smaller but growing number of insured workers from San Diego and Imperial counties are also seeking health services in Baja California through two Mexican plans overseen by the state of California.

Geared to Mexican nationals and their dependents who work in San Diego and Imperial counties, the plans spell savings not only for patients, but employers: SIMNSA says its premiums are 60 to 70 percent lower than those of comparable U.S. health plans. Its network includes 400 physicians, 200 of them employed full time.

The aim is to “provide affordable, quality health care for the region,” said Frank Carrillo, the 73-year-old founder of SIMNSA, the oldest and largest of two Mexican insurance providers that are licensed by the state of California. “You can make a doctor’s appointment at 11 p.m., that’s why people come over here. Not only for affordability, but for accessibility.”

Among SIMNSA’s subscribers is María Teresa Contreras, a 68-year-old Barrio Logan resident insured through her husband, who works setting up banquets at at a La Jolla hotel.

“Over there, the doctor just checks you, gives you medicine and it’s time to go home,” said Contreras, seated in a recliner as she received ozone therapy. The treatment was not offered by her former U.S. health plan, but is available at SIMNSA for patients diagnosed with ailments such as diabetes, rheumatism and arthritis.

Shara Shapiro, 40, who lives in Serra Mesa and works in food service at a hotel in La Jolla, said she paid $90 every two weeks for a U.S. health plan before switching to SIMNSA three years ago at the recommendation of a colleague.

Now, she’s paying $20. “It’s much cheaper, I get better service, and I don’t have a huge co-pay to see a specialist,” she said.

A plan limited to the California-Mexico border

California is the only state on the U.S.-Mexico border that allows such cross-border plans. Of the two HMO plans licensed by the Department of Managed Care, the smaller and newer plan is MediExcel, which started in 2012.

Based in Tijuana’s Río Zone at the private Excel Hospital, MediExcel’s plan last year saw its enrollment grow by 35 percent last year, and currently counts some 10,000 enrollees, said executive vice-president Jim Arriola.

He concedes these plans are not for everyone: “If somebody doesn’t want to go to Mexico, it doesn’t matter how much they’re going to save, they’re not going to pick a cross-border plan,” Arriola said.

Since SIMNSA became licensed in 2000, the company says more than 500 U.S. employers have chosen to offer SIMNSA as one of the options for their workers. Among the plan's direct subscribers are employees of the Hotel del Coronado, General Dynamics in National City and Barona Casino.

Enrollees can receive care at five different SIMNSA outpatient centers in Mexicali, Tecate and Tijuana, with the largest facility within easy walking distance of the San Ysidro Port of Entry. The hours are 8 a.m. until midnight on weekdays, with shorter hours on weekends.

The plan provides for U.S. emergency and urgent care. For major surgeries and other procedures not offered directly by SIMNSA, the plan contracts with other Tijuana providers.

SIMNSA counts close to 50,000 direct enrollees, but has expanded its pool of potential patients by 80,000 through agreements with two U.S. plans — HealthNet and Anthem Blue Cross — that allow members access to medical care in Mexico through SIMNSA, said Christina Suggett, the chief operating officer. In addition, more than 10,000 people receive discounted care at SIMNSA through the purchase of a membership card, Mexsalud.

One of SIMNSA’s oldest clients is Local 30, the hotel and hospitality workers’ union in San Diego. Of 3,500 members on health plans, about a third are enrolled in SIMNSA, said president Brigette Cummings. Members who enroll in SIMNSA health plans pay no fee—the entire cost is covered by the employer.

“For people willing to cross the border, it’s an excellent option,” Cummings said. “The co-pay is cheaper, the medicine is cheaper.” But there are other advantages as well, she said: the extended hours allow participants to make appointments without having to take off from their jobs and the location in Mexico allows care for dependents in Mexico who are unable to cross to San Diego for treatment.

From field workers to hotel workers

The founder and driving force behind SIMNSA is Frank Carrillo, a Mexican-born immigrant who as a boy helped support his family selling popsicles by the border in Tijuana--at the very spot where SIMNSA’s medical building now rises.

He was 16 years when his family moved to the United States. While the others went to work in the fields, Carrillo stayed behind in Los Angeles, “painting cars, construction, whatever came along.”

He earned a GED, joined the U.S. Army, and after receiving an honorable discharge returned to civilian life and found work in sales for a health plan. After rising through the ranks, Carrillo struck out on his own as a consultant, helping companies get HMO licenses in California.

From there, he went to work for the Teamsters, overseeing the union’s agricultural worker health program in the state of California, setting up health care contracts with providers on both sides of the border, as some of the farm workers lived in Mexico.

He saw an opportunity in setting up cross-border healthcare networks for Mexicans who cross to work in San Diego. “I saw service workers living in Mexico and working in San Diego, and I said to myself, the same thing I did for farm workers, I can do for these workers.”

His newest project is a 120-bed, $120-million bi-national hospital being planned around the medical tower. Carrillo expects the first phase consisting of an emergency room and 30 beds will be completed this year, with the finished project set for opening in 2020.

SIMNSA and Scripps Health in 2016 announced they would be joining forces on the project, with Scripps acting as consultant, but a final agreement was not reached. Carrillo said he is moving forward, undeterred in his vision.

“I’m one of those immigrants who realized the American Dream,” said Carrillo, a dual U.S. and Mexican citizen who lives in Chula Vista’s East Lake. “When people say, ‘You can’t do it,’ I do it. My hunger comes from being an immigrant.”

Limited enrollment

Though Americans for decades have come south for a broad range of medical medical care, the concept of a cross-border health plan sanctioned by authorities both in the United States and Mexico is relatively recent. The 1998 passage of an amendment to the Knox-Keene Health Care Service Plan Act, which regulates managed care in California, opened the door to “Mexican prepaid health plans.” These are plans that are licensed in California to offer employer-sponsored group plan contracts to Mexican nationals legally employed in San Diego and Imperial counties and their dependents, no matter what the nationality.

The legislation's sponsor, Steve Peace, was then a Democratic state senator representing San Diego’s South Bay, and says Hispanic staff members first put the issue on his radar. “They came to me and said, ‘this is crazy, you have people living in Mexico and in some cases living in the South Bay, they are being forced to get medical care that is more expensive,” north of the border.

The option for insured workers to receive care in Mexico came on the heels of the signing of North American Free Trade Agreement, a period when “there was a lot of expectation that economic relationships were going to strengthen on both sides,” said Arturo Vargas Bustamante, a professor at University of California Los Angeles’ Fielding School of Public Health and a former official in Mexico’s health ministry.

But for all the flurry of initial interest, the expectations of high enrollment have fallen short, Vargas said. A 2008 article co-authored by Vargas cited “legal, cost and geographic limitations” as the main obstacles to expanding enrollment. The plans are limited to employers in San Diego and Imperial counties and exclude “self-employed people who might be interested in buying less costly coverage in Mexico,” the article stated.

Today, the California Department of Managed Care licenses only two Mexican prepaid health plans: the SIMNSA Health Plan and the MediExcel Health Plan. Both say they are compliant with the standards of the Affordable Care Act, and both are reporting growth.

“Many of the new members we’re getting were previously uninsured,” said Arriola of MediExcel. A big issue for low-wage earners in California is obtaining coverage for dependents, he said, and by selecting lower-cost cross-border plans, workers are able to enroll family members who previously did not have coverage.

While many San Diego service workers have found low-cost insurance under these plans, they are not the only U.S. option available to those employees willing to cross to Mexico for medical care.

The Western Growers Association offers one of the largest health plans to agricultural workers in California through its assurance trust plan; as part of their choices, enrollees can receive some or all of their care in Mexico through a proprietary network of contracted medical providers in Tijuana, Mexicali and Algodones in Baja California and San Luis Río Colorado in Sonora. According to the association, some 15,000 enrollees are receiving at least some of their treatment in Mexico.

http://www.sandiegouniontribune.com/news/border-baja-california/sd-me-simnsa-tijuana-20180108-story.html#nws=true

No deal to avert government shutdown after Trump-Schumer meeting

Supreme Court to rule on Trump travel ban

Olympian Aly Raisman wishes for Larry Nassar to have 'a life of suffering'

They call it a non profit. Seems to me a lot of people were making a HUGE profit for pushing papers and BS!

Yet, those of us with REAL SKILLS who have something to make the world a better place struggle not to be taxed out of our home in Washington State where the constitution doesn't exist as they make up their own laws here!

New Mexico Obamacare Co-op Boasted Six-Figure Salaries and now is Insolvent!

New Mexico Health Connections, one of the four remaining nonprofit Obamacare Co-ops, did not inform its customers in June that it was insolvent and its entire board had resigned, The Daily Caller News Foundation has learned.

It also never told its customers the nonprofit paid its executives up to $450,000 in annual salaries.

The nonprofit, one of 24 Co-op’s originally set up under Obamacare, was supposed to provide affordable health insurance to individuals, predominantly low-income citizens. The demise of the New Mexico Co-op means that only three are fully functioning.

The New Mexico Co-op boasted extraordinarily high six figure salaries per year like many other failed Obamacare nonprofits, according to a DCNF review of its 2015 tax filing Form 990 with the Internal Revenue Service.

Dr. Martin Hickey, the nonprofit’s CEO, received a $450,000 salary, according to its 990. It is unclear what his compensation was in 2017 when the Co-op notified the state insurance superintendent it was insolvent.

All 12 of the nonprofit’s top staff received six-figure salaries, according to its tax filing. Joining Hickey was Chief Medical Officer Dr. Mark Epstein who received an annual salary of $413,000, Chief Operating Officer Anne Sapon who received $342,000, and Primary Care staffer Frances Torres who received $318,000.

The New Mexico Co-op burned through $77.3 million in federal loans awarded by the Obama administration’s Centers for Medicare and Medicaid in 2012. The nonprofit was “bleeding about $20 million in red ink a year,” an Albuquerque Journal editorial noted.

Customers first learned in September the Co-op was facing financial difficulties. It announced an agreement to sell its small and large business policies to a for-profit company called Evolent Health for $10 million in cash.

The deal meant the insolvent nonprofit would continue serving individual customers – its most vulnerable and poorest customers. About 22,000 customers were affected.

The nonprofit’s dire financial straits were so severe its total capital and surplus were $3.5 million even after the infusion of $10 million, according to its Sept. 30 financial filings as reported by the Journal last December.

Co-op customers also weren’t informed that their insurer was insolvent and its board had resigned until after the Obamacare “open enrollment” period for 2018 had expired.

Under New Mexico law, that state can take over insurers that face financial distress. Yet, the state did not assume control of Health Connections after the resignation of its board last June, according to the Albuquerque Journal. Instead, it allowed True Health to take over the two smaller divisions and permitted the individual market customers to remain in the cash-strapped nonprofit.

Hickey, the highest paid Co-op executive, left the nonprofit and joined True Health, Evolent’s subsidiary. True Health did not respond to a DCNF inquiry about his current compensation.

Sapon, in a Linked-In posting in the first week of 2018 attempted to claim the co-op wasn’t facing any financial distress.

“The nonprofit’s leadership have continued NMHC is happy to announce that, contrary to rumors that have been circulating, the company is in a great financial position for the coming year,” she wrote. “We look forward to continuing to serve our members with the same high levels of care, expertise, and compassion that we have been providing for the past four years. We wish you a healthy and happy 2018!”

“We all wanted the company to succeed, but we were effectively insolvent in June,” said Diane Denish, a Co-op board member and New Mexico’s lieutenant governor under Democratic Gov. Bill Richardson in an interview with the Journal on Jan. 9.

Other insurance companies are facing significant losses because of the nonprofit’s insolvency. The largest creditor is Presbyterian Healthcare Services, which is owed $7.6 million. Blue Cross Blue Shield of New Mexico said Health Connections will likely owe it several million dollars.

http://dailycaller.com/2018/01/10/exclusive-insolvent-new-mexico-obamacare-co-op-boasted-six-figure-salaries/?utm_medium=email

They can't get the mail to you but people want health care like Canada. LOL!

Not a laughing matter though for the people in Canada who die waiting to be seen.

But hey in the states entitlement with no responsibility behind it is the key to being a good PC follower of blind leading the blind!

Is health insurers prepared for repeal of the Individual Mandate clause? Here's a round-up of the sector's past performance.

Yet, what do you hear the socialist cry for in the states? Free health care!

Free to die before u get it!

Canada’s health-care wait times hit new record—21.2 weeks

VANCOUVER—Wait times for medically necessary treatment hit a new record in 2017 and eclipsed 20 weeks for a second year in a row, finds a new study released today by the Fraser Institute, an independent, non-partisan Canadian public policy think-tank.

The study, an annual survey of physicians from across Canada, reports a median wait time in 2017 of 21.2 weeks—the longest ever recorded.

By comparison, Canadians waited 9.3 weeks in 1993 when the Fraser Institute first reported wait times for medically necessary elective treatments.

“Excessively long wait times remain a defining characteristic of Canada’s health-care system,” said Bacchus Barua, associate director of health policy studies at the Fraser Institute and author of Waiting Your Turn: Wait Times for Health Care in Canada, 2017.

The study examines the total wait time faced by patients across 12 medical specialties from referral by a general practitioner (i.e. family doctor) to consultation with a specialist, to when the patient ultimately receives treatment.

Among the provinces, Ontario again recorded the shortest wait time at 15.4 weeks—nearly four months—and New Brunswick recorded the longest wait time (41.7 weeks).

For the fifth year in a row, British Columbia saw an increase in wait times with the median hitting 26.6 weeks—the longest ever measured in that province. Alberta also experienced its longest wait time ever at 26.5 weeks this year, and wait times in Quebec also crossed the 20 week mark for the first time since 2003.

Among the various specialties, national wait times were longest for orthopedic surgery (41.7 weeks) and neurosurgery (32.9 weeks) and shortest for medical oncology (3.2 weeks).

“Long wait times are not a trivial matter—they can increase suffering for patients, decrease quality of life, and in the worst cases, lead to disability or death,” Barua said.

“It’s time for policymakers to consider reforming the outdated policies that continue to contribute to long wait times in Canada.”

LMAO ... How true, how very true!!!

i thought the worst bill in the history of congress was BILL CLINTON !

I know people who go there on vacation and get their dental work done at the same time. What they save on this joke we call health care here pays for their vacation.

SP500 opening heat map 85% green, 15% red.

$2,830 Appendectomy in Mexico, $33,000 USA

November 30, 2017

I might feel safe in a USA operating room than a Mexican, but.....

My son had an attack of appendicitis late Saturday night. I knew that the Obamacare inflated prices for surgery in the U.S. would be ridiculous and that the service would likely be impersonal, involve long waits, and be nerve-wracking.

I have friends in the medical field so I inquired just for grins. The price for the latest routine appendectomy in my area was, my jaw dropped, $43,000. I read on-line that the average cost for an appendectomy in the U.S. is $33,000. I am not near some of the great direct-pay medical facilities in the U.S. like the Surgery Center of Oklahoma, but I am near Mexico. I chose that option since I have often utilized foreign medical and dental facilities in the past and find the service and prices to be outstanding.

The main first-rate hospitals in this part of Arizona are run by the Catholic Church. They, of course, operate under the constraints of Obamacare and other onerous U.S. rules and can’t offer pure free-market rates. So, they are pricey along with all the others.

I opted for the nearby private Catholic hospital in Mexico driving past a Catholic hospital in the U.S. en route. I also drove past the state run socialist hospital in Mexico which of course has deplorable service and doesn’t serve Americans anyway. Most of the private hospitals in Mexico have great service, modern equipment and procedures, and affordable prices. You can actually have extensive conversations with surgeons and the rest of the medical staff. They are very patient, respectful, and understanding. We arrived on a Sunday morning. This counted as an emergency after-hours visit. The fees listed below are higher because of the Sunday call-out for surgical personnel and the extra fee for the emergency room doctor that could have been avoided if I had come during normal business hours.

The emergency room doctor immediately made an assessment of my son and ordered lab work. A decision was made to perform an emergency appendectomy. The hospital called up all the necessary staff to conduct the procedure. Despite it being a Sunday, the full operating room staff was there within half an hour: Two surgeons to conduct the laparoscopic procedure, an anesthesiologist, and surgical nurses. The chief surgeon made his own assessment upon arrival and said the appendectomy was needed. He said that he would make us a CD of the operation which they always record for their records.

My son was checked into a private room with private bath and satellite TV awaiting his surgery. The surgical staff was prepped and ready to start within an hour-and-a half of our arrival. The appendix was ruptured, so extra precautions were taken to clean and flush the abdominal cavity. Since the appendix was ruptured, the chief surgeon said that my son should stay two days to receive intravenous antibiotics to prevent the development of peritonitis.

The main purpose of this article is to break down the cost of surgery at a private hospital in Mexico. It doesn’t really matter what facility you go to or what city you are in. The costs will be similar. I don’t have exclusive knowledge of some special secret hospital. If you don’t know where to go, then cross the border at your nearest crossing point and ask a taxi driver to take you and your loved one to a private hospital. You don’t need to know your way around. There are always taxis right near the border crossings. Try to get over the gringo fear that everyone will rip you off in Mexico and just go for it. Also, you can pay your bills with dollars or with your debit/credit card.

Below are the itemized costs for an appendectomy in Mexico with complications. It is higher because of the emergency attention on a Sunday. The hospital stay was for 48 hours in a private room where my wife was allowed to spend the nights with my son sleeping on a couch in his room. This cost would have been significantly less if we hadn’t incurred emergency fees and if the appendectomy had not involved complications which required a longer stay and more medication. Despite all that, I though the total price of $2,830 dollars was very reasonable.

David Hathaway is a former supervisory DEA Agent. He is a cowboy and aficionado of Latin America where he has lived and traveled extensively. He is a homeschooling father of nine children and maintains the website charityendureth.com.”

https://www.lewrockwell.com/2017/11/david-hathaway/2830-appendectomy-in-mexico/

Senate Republicans just repealed the Obamacare mandate in historic vote

December 2, 2017

Replacing and repealing Obamacare (particularly its individual mandate) has been a priority for the Trump administration and conservatives all over the country for the past year. The toxic legislation may finally be on its way out.

Senate Republicans have included, as part of their tax-cut bill, a number of provisions that will weaken Obamacare and end the individual mandate — a major step toward eradicating the unpopular law in its entirety, according to The Hill.

Sen. John Barrasso (R-Wyo.) commented on the achievement, stating, “Families ought to be able to make decisions about what they want to buy and what works for them — not the government.”

The Senator lambasted the tax penalties bundled with Obamacare that have hurt so many Americans. “I believe if people don’t want to buy the Obamacare insurance, they shouldn’t have to pay a tax penalty to the IRS,” Barrasso said.

A Long Way to Go

There are still legislative hurdles to overcome before we’ll see the Republican tax plan take effect. The bill must, for example, be reconciled with prominent House legislation that doesn’t currently support or address the repeal of Obamacare’s individual mandate.

The most recent tallies indicate that no Democrats (in either chamber) are in support of the tax bill. Some cite uncertainty, claiming that the wholesale repeal of the mandate without a replacement waiting in the wings could negatively affect the health of millions of Americans. Others, in all likelihood, are using the opportunity to be adversarial with their votes.

To bridge the partisan gap, moderate Republicans have shown an interest in working with Democrats to proactively shield the American public from damages they may incur as a result of rapid changes to the insurance market.

In Support of the Bill

The president, alongside several prominent Senate conservatives (such as Tom Cotton, of Arkansas), is an ardent supporter of the legislative changes.

It’s easy to see why — the Congressional Budget Office posits that a repeal of the individual mandate would lift $300 billion in subsidies off the shoulders of taxpayers over the course of the next decade.

Over the summer, three Republican Senators — John McCain (R-Ariz.), Lisa Murkowski (R-Alaska.), and Susan Collins (R-Maine.) — sided with the Democrats, casting their votes in opposition of an Obamacare repeal. They appear to be in favor of the updated legislation.

While there is no certainty as to the fate of the GOP’s reinvigorated tax legislation, it does appear to have momentum, and seems to carry with it enough support to potentially become law — a long-overdue death blow to Obamacare.

https://www.conservativeinstitute.org/healthcare/senate-gop-repeals-mandate.htm

Yep. Other clowns only spoke up once they saw the public speaking about it. No morals. No leadership. Just PC Race Victim cards being played down at the Cess Pool!

Sen. Patty Murray has already proven herself to be an idiot libtard!

She has remained silent on the resignation of Seattle Mayor Ed Murray in Sept. after it was revealed he sexually abused teenagers (boys) decades ago.

If Obama had not doubled the national debt the past eight years then President Trump would not be stuck dealing with another of his messes.

Fraud must be halted - HUD, Medicare, Medicaid, IRS, SS Disability, and the list goes on. Billions have been lost to fraud.

If Obama had not doubled the national debt the past eight years then President Trump would not be stuck dealing with another of his messes.

Fraud must be halted - HUD, Medicare, Medicaid, IRS, SS Disability, and the list goes on. Billions have been lost to fraud.

Congressional Budget Office: Options for Reducing the Deficit

The overall due balance of the US federal government now surpasses yearly Gross Domestic Product (GDP). This level has traditionally attested challenging in other nations. The main driver of the balance is a federal budget shortfall that now surpasses $1 trillion annually. Regardless of predictions of ominous consequences, the shortfall and due balance have not been regulated, as initiatives to make meaningful cutbacks -- counting plans created by the dual-party Bowles-Simpson and Domenici-Rivlin groups -- have thus far become vulnerable to internal strife in the political procedure (Matthews, 2013). The following excerpt exhibits a method to abolish the yearly shortfall, stabilize the federal budget, and lessen federal due balance.

By decreasing federal agencies’ expenditures for FEHB premiums for workers (who also become Medicare recipients) and their dependents, the decision to implement the premium-sharing structure would decrease elective expenditures by a projected $27 billion from 2019 through 2026, on condition that appropriations were decreased to mirror those lesser charges. The decision also would lessen obligatory expenditures for FEHB by $32 billion for the reason that the Treasury and the Postal Service would make lesser payments for FEHB premiums for persons who receive annuities and postal workers (CBO, 2016).

Ultimately, the CBO projects that beginning in 2019; the decision would cause some FEHB members to withdraw from the program and incomes for employees (including Medicare recipients) will also be influenced by the decision. However, CBO assumes that the net adjustment would be negligible. Some of the individuals who became uncovered by insurance plans would pay fines to the government, as the ACA stipulates. That surge in incomes would be roughly counterbalanced for the reason of modifications that would occur in the number of individuals with employer insurance and modifications in the charges of that health plan. Those modifications would influence the share of complete payment that takes the shape of taxable earnings and incomes and the share that takes the shape of nontaxable health benefits; taxable payment would surge for some individuals and lessen for others (CBO, 2016).

On the other hand, a benefit of this decision is that it would upturn registrants’ motivation to select lower-premium health coverages: If they had chosen health coverages that surpass the voucher amount, they would pay the entire supplementary charge. For the same purpose, the decision would reinforce price competition amid health insurance coverages partaking in the FEHB program. For the reason that registrants would pay no premium for health insurance coverages that does not exceed the value of the voucher, insurers would have a specific incentive to suggest such health insurance coverages (COB, 2016).

Furthermore, the US is challenged with an increasing forthcoming percentage of debt to Gross Domestic Product that, if permitted to remain, would have severe adverse consequences for the American economy. However, policy modifications can upturn the size of the forthcoming Gross Domestic Product and reduce the forthcoming budget shortfalls. Comparatively small drops in forthcoming yearly shortfalls could reverse the growing percentage of national due balances to Gross Domestic Product. Those yearly shortfall drops could be best accomplished by slowing the development of Medicare (Feldstein, 2016).

References

CBO. (2016 December).Options for Reducing the Deficit: 2017 to 2026.CBO. Retrieved from https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/52142-budgetoptions2.pdf

Feldstein, M. (2016). Dealing with long-term deficits. American Economic Review, 106(5), 35-38. doi:10.1257/aer.p20161004

Matthews, R. B. (2013). A "modest" proposal to balance the federal budget. Journal of Applied Business Research, 29(3), 669.

Investigators Are Taking A New Look At Two Of The Russians In The Trump Tower Meeting

Investigators are taking a fresh look at two of the Russians involved in the June 2016 Trump Tower meeting because of a secret rendezvous they had earlier this year, possibly to coordinate their stories.

According to the Associated Press, congressional investigators are interested in a coffee meeting held in June in Moscow between Rinat Akhmetshin and Ike Kaveladze, two of the Russians who attended the June 9, 2016 Trump Tower meeting with Natalia Veselnitskaya, a Russian attorney who was lobbying against the Magnitsky Act, a sanctions bill.

Akhmetshin is a Russian-American lobbyist and former Soviet military officer who worked closely with Veselnitskaya and Fusion GPS founder Glenn Simpson on the anti-Magnitsky consulting project. Simpson was working on the infamous Trump dossier at the same time.

(RELATED: Here’s What We Know About Rinat Akhmetshin)

http://dailycaller.com/2017/07/14/heres-what-we-know-about-the-suspected-ex-soviet-intel-officer-who-attended-trump-tower-meeting/

Kaveladze is the U.S. representative for the Agalarov family, the real estate tycoons who have done business with the Trumps.

Akhmetshin asked Kaveladze for the meeting, he has told congressional investigators. According to the AP, the Beltway-based political operative told congressional investigators this week that he contacted Kaveladze to discuss coming forward about the Trump Tower meeting ahead of news reports.

The New York Times broke the story of the meeting on July 8.

The Moscow meeting has raised the question of whether Akhmetshin and Kaveladze sought to coordinate their stories regarding Trump Tower, which was attended on the Trump campaign side by Donald Trump Jr., Jared Kushner and then-campaign chairman Paul Manafort.

(RELATED: Ike Kaveladze Identified As 8th Trump Tower Meeting Attendee)

The eighth person to attend the Trump Tower meeting has been identified as Ike Kaveladze, a real estate executive who was implicated in a possible money laundering scheme in the U.S. nearly two decades ago.

http://dailycaller.com/2017/07/18/8th-person-in-trump-tower-meeting-has-been-identified/

Investigators have obtained text messages between Akhmetshin and Kaveladze that could shed light on their motives, according to the AP.

Scott Balber, a lawyer for Kaveladze and Veselnitskaya who has previously represented Donald Trump, denied that story coordination was discussed.

Akhmetshin has already reportedly appeared before a grand jury being used by Special Counsel Robert Mueller as part of his investigation into Russian interference in the presidential campaign.

Mueller — like congressional investigators — is looking into whether the meeting constituted collusion between the Trump campaign and Russian operatives or whether it was an attempt by Russians to infiltrate an unwitting Trump team.

Veselnitskaya and Trump Jr. s hat it was an innocuous and fruitless.

Trump Jr. accepted the meeting after being emailed by Rob Goldstone, a publicist who works for the Agalarov family. Goldstone said that a “Russian government attorney” — later identified as Veselnitskaya — would be offering dirt on Hillary Clinton.

Trump Jr. accepted, saying “If it is what you say I love it.”

Veselnitskaya discussed the Magnitsky Act but offered no information on Clinton, she and Trump Jr. have said.

But Veselnitskaya did take a four-page memo into the meeting that contained research compiled by Simpson, the Fusion GPS founder. The document contained one mention of Clinton but largely focused on the Magnitsky Act.

It was revealed earlier this month that Simpson and Veselnitskaya were together just before and just after she and Akhmetshin attended the Trump Tower meeting. But Simpson told the House Intelligence Committee this week that he was unaware that Veselnitskaya was meeting with the Trump campaign. He also said that he did not know that his research was being taken into the meeting.

Questions have been raised about whether Christopher Steele, the former British spy who wrote the dossier, had been told about the Trump Tower meeting. Steele was working for Fusion GPS, who in turn was working for the Clinton campaign and DNC to investigate Trump.

Simpson also told the House Intelligence Committee that he was unaware that Veselnitskaya had provided his research to Yuri Chaika, the Russian government’s prosecutor general. The Daily Caller was told that Simpson expressed regret in his House interview that his work product fell into Kremlin hands.

Veselnitskaya worked as a consultant to Chaika, who is close to Russian president Vladimir Putin.

Simpson began working with Veselnitskaya in 2014. Multiple sources have told The Daily Caller that Simpson has known Akhmetshin for more than a decade, stretching back to the oppo researcher’s time as a reporter at The Wall Street Journal.

http://dailycaller.com/2017/11/18/investigators-are-taking-a-new-look-at-two-of-the-russians-in-the-trump-tower-meeting/?utm_medium=email

“Policy of the People”- 80% of Obamacare Mandate Paid by Sub $50K Households

Barack Obama ran as a hero for the common American, promising “hope and change” for the nation’s downtrodden.

It’s no surprise that his signature legislation, Obamacare, was also marketed as an amazing benefit for the middle class and poor Americans.

However, a new report reveals that Obama’s true legacy should actually be taking money out of the pockets of average Americans in one of the rawest deals since Bernie Madoff.

According to Forbes contributor Ryan Ellis, the individual mandate that is at the center of Obamacare actually hits working-class families the hardest.

“The mandate is a tax which punishes those who can least afford it,” Ellis wrote.

He looked at the breakdown of who actually pays the individual mandate surtax, which is the penalty that kicks in if a person doesn’t purchase government-approved health insurance. What he found was shocking.

“According to the IRS, some 6.7 million American families pay Obamacare’s individual mandate surtax, forking over $3 billion annually to Uncle Sam merely for exercising their right not to purchase an unaffordable Obamacare plan,” Ellis wrote.

“It turns out most of these taxpayers are solidly in the middle class. The great majority of them (80 percent) actually make less than $50,000 per year. This is perhaps the most regressive tax we have on the books today.”

Around 5.3 million Americans who earn under $50,000 annually were forced to pay the mandate penalty, which averaged about $340 per person.

Yes, average citizens are being charged hundreds of dollars for the right to not buy expensive insurance. So much for the “Affordable” Care Act.

Sen. Steve Daines, a Montana Republican, did a similar analysis of the numbers, and came to the same conclusion: Individuals and families making under $50,000 are the ones being burdened by the mandate.

What would happen if the mandate and its penalties were dissolved? Contrary to the doom and gloom spread by Obamacare’s proponents, the sky probably wouldn’t fall.

“Ending the individual mandate surtax will not cause anyone to lose their health insurance,” Ellis argued. “It will merely stop punishing people who choose not to buy expensive insurance with a surtax they cannot afford, either.”

During the push to pass Obamacare, Democrats and Obama himself waved away the penalty or surtax as something that middle-class people didn’t need to worry about.

That penalty, they insisted, would be for rich Americans who were wealthy enough to cover their medical expenses out of pocket, or who wanted some exotic insurance plan that didn’t meet the Obamacare requirements.

Like so much — dare we say all? — of Obamacare, the promises turned out to be lies. It was snake oil sold by Democrats who were desperate for a political win.

Nobody disputes that America’s health care system can be improved, but Obamacare was not the way.

Like so much of his agenda, Obama’s Obamacare legacy is falling apart.

https://conservativetribune.com/obamacare-mandate-hits-middleclass/?utm_source=Email&utm_medium=patriotupdate&utm_campaign=dailypm&utm_content=libertyalliance

You seeing whats going on in Washington state with murry saying trump is sabotaging obamacare? LOLOLOLOL!!!!

She reminds me of a penny stock ceo who lies so many times they begin to believe their own lies.

Tell me murry ............... What was there anyone could do to the obamafraud mess that could make it any worse?

How do you sabotage a plan that a third grader could tell you the numbers won't work.

Did you not hear 8 months ago rates were going to sky rocket here?

Of course you did.

But the dumb ass sheep in this state can't think for themselves so they believe your CRAPOLA!

Brutal: Many Iowans Are Living Through an Obamacare Horror Story -- and, No, it's Not Trump's Fault

It's easy to predict how Democrats will respond to negative Obamacare headlines in perpetuity -- especially since Donald Trump's (legally-compelled) cessation of illegal "stabilization" funds.

Trump's uncertainty and 'sabotage' caused these problems, they'll squeal, side-stepping their own culpability for passing a terribly broken law that was failing badly long before Trump was ever elected.

Republicans' inability to fulfill fundamental repeal-and-replace promises does mean that they own a sizable portion of the ongoing mess, but Obamacare was a partisan scheme that was passed and implemented exclusively by one party.

As the failing law continues to unravel, citizens in Iowa have been especially adversely affected, as chronicled in a devastating Politico story. Real people. Real, ongoing harm:

Iowa’s individual health insurance market is in chaos—with competition disappearing and prices skyrocketing...That’s a lesson tens of thousands of Iowans have learned over the past four years as the state’s individual health insurance market has imploded, with insurers fleeing the market because of big losses.

With Obamacare’s fifth open-enrollment season kicking off on Nov. 1, the consequences are playing out across one of America’s most politically influential states as residents struggle to maintain coverage.

Just one insurer, Medica, is willing to sell Obamacare plans in Iowa for next year—and it plans to raise premiums by an average of more than 50 percent.

Thousands of Iowans, particularly those who make too much money to qualify for financial assistance, are likely to find that monthly premiums for 2018 are less comparable to a cellphone bill and more like a mortgage payment.

The Iowa Insurance Division predicts that the number of individuals enrolled in coverage will decrease by at least 25 percent next year...

Iowa is not alone in having a disastrous insurance marketplace. Arizona, North Carolina and Tennessee have had similarly dysfunctional exchanges, with paltry competition and soaring premiums.

Nearly half the counties in America have just a single insurer willing to sell coverage on the Obamacare markets.

Truth bomb after truth bomb, starting with the critical context that these issues have deteriorated every year since the law went into effect.

Over that time period, average premium increases on Obamacare's federal exchange have ballooned by 105 percent.

To drive this point home once again, rates and costs have been spiking, and battered insurers have been abandoning the marketplaces under heavy losses for years.

These phenomena all pre-date Trump's presidential announcement, nomination, election, and post-January policy moves.

Republicans and Democrats may manage to apply some sort of bipartisan bandaid "fix" for carriers regarding the cost sharing subsidies (CSRs), but even if the deal includes a handful of positive reforms, it won't rectify the law's fatal flaws. This should be screamingly obvious, but because of Democrats' new "Trump's fault" talking point, it must be repeated every time this issue arises: Obamacare fell apart while the Obama administration was unlawfully paying out the CSRs, and continued to unravel back when everyone expected Hillary would win and continue propping up the wheezing law. Speaking of a compromise, what's the likelihood that something gets hammered out and passed? Mitch McConnell says he'll bring a cross-aisle pact to the floor...if a certain someone signs on:

Senate Majority Leader Mitch McConnell said Sunday he'd be willing to bring bipartisan health care legislation to the floor — if Trump makes clear he supports it. A proposal by two senators - Republican Lamar Alexander of Tennessee and Democrat Patty Murray of Washington - would extend for two years federal insurance payments that Trump has blocked, in an effort to stabilize insurance markets. But Trump has offered mixed signals, alternately praising and condemning the effort - confusing Democrats and Republicans alike.

Asked whether he would bring the bill to the floor, McConnell said on CNN's "State of the Union" that he was waiting "to hear from President Trump what kind of health care bill he might sign." "If there's a need for some kind of interim step here to stabilize the market, we need a bill the president will actually sign. And I'm not certain yet what the president is looking for here, but I will be happy to bring a bill to the floor if I know President Trump would sign it," the Republican said. He added of Trump: "I think he hasn't made a final decision."

I'll leave you with a piece Matt highlighted yesterday. Democrats are fracturing over single-payer healthcare, a top litmus test of the left-wing base that is worrisome to more mainstream Democrats who are concerned about the plan's towering fiscal and political risks. Here's an Obama administration alum torching the BernieCare craze in the New York Times:

The crusty Vermont independent wants to be a senatorial pied piper for Democrats. He has made his proposal into a kind of litmus test for who is a “good Democrat,” inveigling 16 of his colleagues — more than a third of Senate Democrats — into endorsing it. A goodly number of those senators are presidential hopefuls, leaving their prospective campaigns open to attack from Republicans salivating to capitalize on an idea that has historically been a political graveyard. Remember Hillarycare? As a centrist Democrat, I’m scared to see my party pulled into positions that are both bad politics and dubious policy. And I’m disappointed that few of our party’s moderates are willing to resist the freight train coming at us from the left..Yes, recent polls seem to indicate rising support for single payer.

But when factors like whether taxes would be raised or the Affordable Care Act would be repealed are introduced, the consensus swings to opposition. Spellbound Democrats should also consider the fate of past single payer proposals. In Sanders’s home state of Vermont, a single payer plan was abandoned after an analysis found that it would require a near doubling of the state budget (and increasing taxes similarly).

In Colorado last November, a whopping 80 percent of voters rejected a universal plan, again over taxes and costs. And for similar reasons, California recently shelved a single-payer proposal.

These are strong warnings from someone who sees the peril in store for a party that embraces a radical healthcare scheme that makes Obamacare look like free-market child's play.

The public is split evenly on "Medicare for all" (side note: Medicare is on a rapid path to insolvency), but when huge tax increases and the cancellation of all private, employer-based plans are introduced in polling questions, opposition soars. And even if you ignore all of those flaws, are Americans interested in NHS-style, unaccountable, scandal-plagued government rationing and long delays for care? The harsh truth is that despite the Republican Party's embarrassing incoherence and political failures vis-a-vis replacing Obamacare, the Democrats keep demonstrating why they simply cannot be trusted on healthcare.

https://townhall.com/tipsheet/guybenson/2017/10/25/obamacare-update-n2399591?utm_source=thdailypm&utm_medium=email&utm_campaign=nl_pm&newsletterad=

The spin machine has been turned on!

Health Insurance Rates Skyrocket 31 Percent in Pennsylvania After Obamacare

Pennsylvania is set to see its health insurance premiums skyrocket by an average of nearly 31 percent in 2018, according to the state’s acting insurance commissioner.

Even though rate hikes have been de rigueur under Obamacare, acting Insurance Commissioner Jessica Altman tried to blame the astronomical increase on Republicans and the Trump administration.

“It is with great regret that I must announce approved rates that are substantially higher than what companies initially requested,“ Altman said in a news release. “This is not the situation I hoped we would be in, but due to President Trump’s refusal to make cost-sharing reduction payments for 2018 and Congress’s inaction to appropriate funds, it is the reality that state regulators must face and the reason rate increases will be higher than they should be across the country.”

According to The Washington Free Beacon, there are only five health insurers participating in Pennsylvania’s state marketplace next year. While the average increase in premiums for those insurers will be 30.6 percent, some were approved for much higher hikes.

Capital Advantage Assurance Company, one of the individual market participants, got a 49.2 percent rate increase through. UPMC Health Options received a 41.15 percent rate increase and Geisinger Health Plan got a rate increase slightly higher than the state average, at 31.28 percent.

The Pennsylvania Insurance Department claims that “(r)ates reflect estimates of future costs, including medical and prescription drug costs and administrative expenses, and are based on historical data and forecasts of trends in the upcoming year.

“The Department considers these factors, as well as factors such as the insurer’s revenues, actual and projected profits, past rate changes, and the effect the change will have on Pennsylvania consumers.”

(The department avoids mentioning “Obamacare” by name, but anyone following the news knows why rates are going up.)

According to the Pittsburgh Post-Gazette, 85,000 individuals on the exchanges in Pennsylvania will be affected by the higher rates, while the other 426,000 who use it won’t see increases due to subsidies.

While the Insurance Department blames the Trump administration for the massive increase over the projected rate increase of 7.6 percent, let’s face facts: This isn’t the first state to miss its Obamacare rate increase goals.

Last year, the Free Beacon points out, the Obama administration predicted double digit rate hikes across the board on the exchanges.

“Nationwide, average Marketplace premiums for 2017 are increasing more than they have in the past two years,” the Obama administration said at the time. “For the median HealthCare.gov consumer, the benchmark second-lowest silver plan premium is increasing by 16 percent this year, before taking into account the effects of financial assistance.”

While Pennsylvania might want to blame the Trump administration, the Kaiser Foundation noted that these rate increases are mostly to do with the fact that insurers are experiencing massive losses on them.

We doubt this will be the last state to see massive rate hikes, and we doubt it will be the last to blame it on the Trump administration. The fact is that Obamacare is a failing program, and the sooner it’s eradicated, the sooner we won’t have to see these rate hikes.

https://conservativetribune.com/health-insurance-pennsylvania/?utm_source=Email&utm_medium=minutemennews&utm_campaign=dailypm&utm_content=libertyalliance

Another great question. I mean, it's the panacea, isn't it?

Many of those 500+ wounded in the Vegas massacre say they have no insurance and have set up GoFundMe sites.

The question must be asked, why didn't all those young and healthy people have Obamacare??

They can't wait to spend more of your tax payers money on a system they know won't last so what did I receive from Washington state yesterday?

An email stating they now have a mobile app to find a health care provider.

Yep, you really need to use your cell phone to do that process.

Any of these clowns ever look up the word stewardship?

Do they have a clue what that word means?

Our system is so broke but spending other people's money matters not to them got to justify their job.

Makes me sick.

Top Hospitals Opt Out of Obamacare

https://health.usnews.com/health-news/hospital-of-tomorrow/articles/2013/10/30/top-hospitals-opt-out-of-obamacare

SORRY, WE DON'T TAKE OBAMACARE

https://www.nytimes.com/2016/05/15/sunday-review/sorry-we-dont-take-obamacare.html?mtrref=duckduckgo.com&gwh=1F9858CFD606A8E0FE8D5A5241D5E2A9&gwt=pay&assetType=opinion

Top Hospitals Won’t Treat Obamacare Patients

Thank you, Mr. Obama, for a Marxist plan guaranteed to force doctors into retirement (if it is permitted) as the demands of an ever-increasing number of patients are ignored.

https://www.westernjournalism.com/top-hospitals-wont-treat-obamacare-patients/

Got Obamacare, can't find doctors

Terri Durheim and her family now have health insurance, thanks to Obamacare. What they don't have are local doctors and hospitals who will take it.

This worries the Enid, Okla., resident since she has a teenage son with a serious heart condition. They now have to find a pediatric cardiologist in Oklahoma City, more than an hour away.

And if there's an emergency ... "obviously we'd have to pay out of pocket and go here in town, but that defeats the purpose of insurance. I'm truly grateful we have insurance. It's reasonable and affordable, but it's not doing me a lot of good," said Durheim, who just had to drive 90 minutes to Stillwater, Okla., for a CAT scan for herself. "It's so frustrating."

Like Durheim, many Americans who've enrolled on the Obamacare exchanges are realizing they have access to a relatively limited set of doctors and hospitals. In many areas, the largest hospitals are not participating and many doctors are not accepting the coverage.

http://money.cnn.com/2014/03/19/news/economy/obamacare-doctors/index.html

Nation’s elite cancer hospitals off-limits under Obamacare

WASHINGTON — Cancer patients relieved that they can get insurance coverage because of the new health care law may be disappointed to learn that some of the nation’s best cancer hospitals are off-limits.

An Associated Press survey found examples coast to coast. Seattle Cancer Care Alliance is excluded by five out of eight insurers in Washington state’s insurance exchange. MD Anderson Cancer Center says it’s in less than half of the plans in the Houston area. Memorial Sloan-Kettering is included by two of nine insurers in New York City and has out-of-network agreements with two more.

http://nypost.com/2014/03/19/nations-elite-cancer-hospitals-off-limits-under-obamacare/

ObamaCare Cancer Patients Losing Hospital Coverage

Hundreds of cancer patients who belong to a failed ObamaCare health insurance co-op could soon have no coverage for their continued hospital treatment, the New York Post reports.

Health Republic Insurance of New York, which has lost $130 million dollars in 18 months, was the only ObamaCare exchange insurer contracted with the Memorial Sloan Kettering Cancer Center in Manhattan.

250 Health Republic members receiving care at Sloan Kettering need to find a new insurer by November 15 that the hospital takes or prepare to shoulder the cost themselves. New York is forcing their carrier to close shop at the end of this month for losing so much money.

http://dailycaller.com/2015/11/08/obamacare-cancer-patients-losing-hospital-coverage/

Second class patients... sorry we don't take Obamacare!

A McKinsey study shows Obamacare insurers lost money in 2014 and the losses doubled in 2015.

Amazingly, the study concludes there’s nothing to worry about because “30 percent of insurers nationwide were profitable.”

Meanwhile, outright refusals to accept Obamacare mount. “Sorry, We Don’t Take Obamacare” is now a frequent response.

The New York Times tells the sad tale of an increasing number of “Sorry, We Don’t Take Obamacare” responses to those seeking medical assistance.

http://talk.baltimoresun.com/topic/271352-second-class-patients-sorry-we-dont-take-obamacare/

Top Hospital Kicks Obamacare Patients Out on Their Butt

A Watchdog.org study of the top-tiered hospitals found they’re not easily accessible to the Obamacare insurance exchange participants. For example, in Ohio, the Obamacare exchange includes a dozen insurance companies – yet the state’s premier hospital, the Cleveland Clinic, accepts only one of those dozen firms.

https://www.westernjournalism.com/top-hospital-kicks-obamacare-patients-butt/

A Dozen Hospitals Are Laying Off Staff and Blaming Obamacare. Don’t Believe Them.

Hospitals tend to be among the largest employers in their communities — which means that any individual decision to lay off staff can have an outsized local impact. And taken together, a dozen recent announcements seem to paint an especially dire picture for hospitals (and their communities) around the nation.

For example, NorthShore in Illinois says it will lay off 1% of its workforce. The staffing cuts “ensure NorthShore remains well positioned to deal with the unprecedented changes brought on by the Affordable Care Act,” according to a memo from the health system’s chief human resources executive.

And California’s John Muir Health is offering staff voluntary buyouts ahead of ACA implementation. “We’re being paid less, and we either stick our head in the sand or make changes for the future so patients can continue to access us for their care,” according to John Muir spokesperson Ben Drew.

When Obamacare was being debated in Congress, its opponents tried to tar it with a deadly label: “the job-killing health law.” So is the ACA finally living down to its sobriquet?

Not exactly. While the recent news makes for provocative headlines, the devil’s in the details — and the financial reports.

A Closer Look at Industry Pressures

It’s clear that something is shifting in the hospital market. After years of employment growth, hospitals’ hiring patterns have largely leveled off. Collectively, organizations shed 9,000 jobs in May — the worst single month for the hospital sector in a decade.

https://californiahealthline.org/news/a-dozen-hospitals-are-laying-off-staff-and-blaming-obamacare-dont-believe-them/

Obamacare: Fewer options for many

Nationally the marketplaces offer tens of thousands of different policies with a wide variety of coverage, but Harte has noticed many have one thing in common: They cover a narrow network of doctors and hospitals.

That narrower network comes as particularly bad news for the residents of Concord, New Hampshire.

Concord's one hospital won't accept any policies offered by the marketplaces. To see a doctor, specialist or primary care provider affiliated with the hospital, patients on these Obamacare plans will have to pay out of their own pocket. The closest in-network hospital is in Manchester.

"Can you imagine having to go 25 miles away to Manchester to get access to a health care provider that is covered by your insurance?" Harte asked. "Right now, Concord is one big black hole of health care for people buying these plans."

http://www.cnn.com/2013/10/29/health/obamacare-doctors-limited/index.html

If You Can't Go to Cedars-Sinai Anymore, Is It Obamacare's Fault?

At Cedars-Sinai Medical Center in Los Angeles, originals by Picasso and Warhol hang in the hallways. The deluxe maternity rooms—three-bedroom, two-bath suites with views of the city—rent out at nearly $4,000 a day. It’s the place where Madonna got hernia surgery and Jodie Foster had her baby. The Hollywood Reporter once called it “the medical world’s most glam facility.”

But a group of Angelenos is about to lose access to Cedars, because, starting January 1, their insurance companies will no longer cover treatment at the hospital. Infuriated, some of these people insist that Obamacare is to blame. And the truth is: They’re not exactly wrong.

To keep prices down, insurers are sending patients only to the doctors, clinics, and hospitals that have agreed to accept lower reimbursements.

Anthem Blue Cross and Blue Shield of California, two of the state’s largest insurers, wanted bigger discounts than Cedars was willing to give, however. As a result, patients who want fully covered access to Cedars have only one option left: a health maintenance organization, called Health Net, with a relatively small network of doctors.

https://newrepublic.com/article/115991/obamacare-insurance-plans-cedars-sinai-hospital-limits-many

How Forest Park Medical Center buckled under Obamacare

https://www.dallasnews.com/opinion/commentary/2017/05/11/forest-park-medical-center-buckled-obamacare

Forest Park Medical Center Fort Worth shuts down MAY 25, 2016

Forest Park Medical Center Fort Worth was shut down late Tuesday and most of its employees laid off as Texas Health Resources wraps up its purchase of the bankrupt doctor-owned, luxury hospital on the city’s west side.

Forest Park hospital’s outgoing managers shut down operations on Tuesday because they expected the sale to close, said Jeff Prostok, one of their bankruptcy attorneys. He said he now expects the deal to be completed Wednesday, opening up a new chapter for the facility.

“We are ceasing operations. We are in a layoff situation,” Prostok said. “We thought it (the sale) would happen yesterday and it will happen today. We let the folks go because there really wasn’t anything for them to do. We didn’t want them around doing nothing.”

Court records show that the Forest Park facility employed 175 people, including 115 full-time employees and 60 part-time employees.

http://www.star-telegram.com/news/business/article79793337.html

San Antonio's Forest Park Medical Center building sells at foreclosure

No other parties bid at the auction, which was held on the grounds of the Bexar County Courthouse.

The property has essentially been mothballed since the hospital’s operator, Forest Park Medical Center San Antonio, closed on Oct. 15 because of financial troubles. It attributed its closing partly on insurance companies that would not enter into contracts with it.

http://www.mysanantonio.com/business/local/article/San-Antonio-hospital-sells-at-foreclosure-6863287.php#photo-9218937

Mayo says the U.S. government does not pay enough to cover the cost of care.

More than 3,000 patients eligible for Medicare, the government’s largest health-insurance program, will be forced to pay cash if they want to continue seeing their doctors at a Mayo family clinic in Glendale, northwest of Phoenix, said Michael Yardley, a Mayo spokesman.

The decision, which Yardley called a two-year pilot project, won’t affect other Mayo facilities in Arizona, Florida and Minnesota.

Obama in June cited the nonprofit Rochester, Minnesota-based Mayo Clinic and the Cleveland Clinic in Ohio for offering “the highest quality care at costs well below the national norm.” Mayo’s move to drop Medicare patients may be copied by family doctors, some of whom have stopped accepting new patients from the program, said Lori Heim, president of the American Academy of Family Physicians, in a telephone interview yesterday.

“Many physicians have said, ‘I simply cannot afford to keep taking care of Medicare patients,’” said Heim, a family doctor who practices in Laurinburg, North Carolina. “If you truly know your business costs and you are losing money, it doesn’t make sense to do more of it.”

https://ayfs.wordpress.com/2010/01/01/mayo-clinic-refuses-to-accept-medicare-what-happens-to-obamacare-when-the-doctors-refuse-to-accept-the-low-government-pay/

Covered California unplugs most top hospitals from patients

President Obama has been claiming that people can keep their favorite doctors under the Affordable Care Act. But anyone who wants a premier hospital in California better do some homework before signing up.