News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

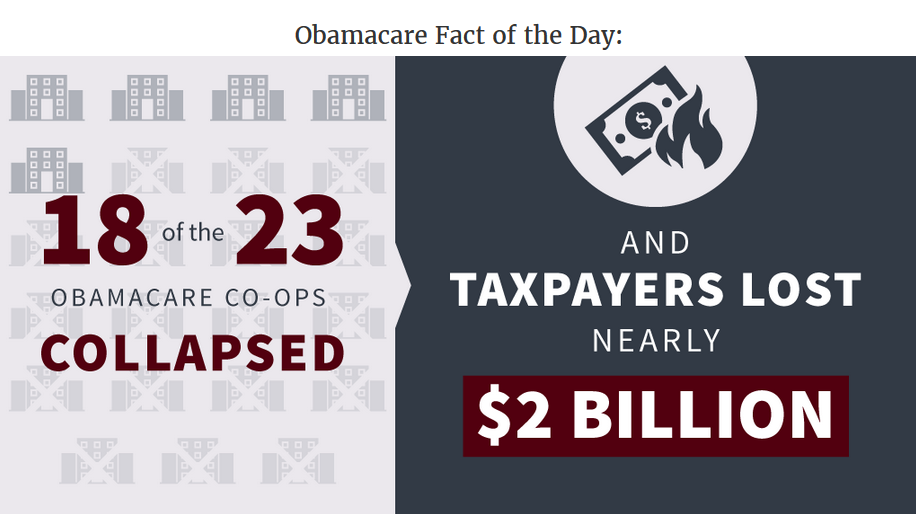

Clear and concise. Perfect.

Obama Lied. My FOURTH Health Plan Died.

Cue the funeral bagpipes. My fourth health insurance plan is dead.

Two weeks ago, my husband and I received yet another cancellation notice for our private, individual health insurance coverage.

It's our fourth Obamacare-induced obituary in four years. Our first death notice, from Anthem Blue Cross and Blue Shield, arrived in the fall of 2013. The insurer informed us that because of "changes from health care reform (also called the Affordable Care Act or ACA)," our plan no longer met the federal government's requirements.

Never mind our needs and desires as consumers who were quite satisfied with a high-deductible PPO that included a wide network of doctors for ourselves and our two children.

Our second death knell, from Rocky Mountain Health Plans, tolled in August 2015. That notice signaled the end of a plan we didn't want in the first place that didn't cover our kids' dental care and wasn't accepted at our local urgent care clinic. The insurer pulled out of the individual market in all but one county in Colorado, following the complete withdrawal from that sector by Humana and UnitedHealthcare.

Our third "notice of plan discontinuation," again from Anthem, informed us that the insurer would "no longer offer your current health plan in the State of Colorado" in August 2016.

With fewer and fewer choices as know-it-all Obamacare bureaucrats decimated the individual market here and across the country, we enrolled in a high-deductible Bronze HSA EPO (Health Savings Account Exclusive Provider Organization) offered by Minneapolis-based startup, Bright Health.

Now, here we are barely a year later: Deja screwed times four. Our current plan will be discontinued on Jan. 1, 2018.

"But don't worry," Bright Health's eulogy writer chirped, "we have similar plans to address your needs."

Riiiiight. Where have I heard those pie-in-the-sky promises before? Oh, yeah. Straight out of the socialized medicine Trojan horse's mouth. "If you like your doctor," President Obama promised, "you will be able to keep your doctor. Period. If you like your health care plan, you'll be able to keep your health care plan. Period. No one will take it away. No matter what."

Is pathological lying covered under the Affordable Care Act?

Speaking of Affordable Care Act whoppers, so much for "affordable." Our current deductible is $6,550 per person; $13,100 for our family of four. Assuming we can find a new plan at the bottom of the individual market barrel, our current monthly premium, $944.86, will rise to more than $1,300 a month.

"What's taking place is a market correction; the free market is at work," says Colorado's state insurance commissioner, Marguerite Salazar. "(T)his could be an indication that there were too many options for the market to support."

This presumptuous central planner called federal intervention to eliminate "too many" options for consumers the free market at work. Yes, friends, the Rocky Mountain High is real.

This isn't a "market correction." It's a government catastrophe.

Premiums for individual health plans in Virginia are set to skyrocket nearly 60 percent in 2018.

In New Hampshire, those rates will rise 52 percent.

In South Carolina, individual market consumers will face an average 31.3 percent hike.

In Tennessee, they'll see rates jump between 20-40 percent.

Private, flexible PPOs for self-sufficient, self-employed people are vanishing by design. The social-engineered future -- healthy, full-paying consumers being herded into government-run Obamacare exchanges and severely regulated regional HMOs -- is a bipartisan big government health bureaucracy's dream come true.

These choice-wreckers had the arrogant audacity to denigrate our pre-Obamacare plans as "substandard" (Obama), "crappy" (MSNBC big mouth Ed Schultz) and "junk policies" (Sen. Tom Harkin, D-Iowa).

When I first called attention to the cancellation notice tsunami in 2013, liberal Mother Jones magazine sneered that the phenomenon was "phony." And they're still denying the Obamacare death spiral. Liberal Vox Media recently called the crisis "a lie."

I don't have enough four-letter words for these propagandists. There are an estimated 450,000 consumers like us in Colorado and 17 million of us nationwide -- small-business owners, independent contractors and others who don't get their plans through group coverage, big companies or government employers. The costs, headaches, and disruption in our lives caused by Obamacare's meddling meddlers are real and massive.

But we're puzzles to corporate media journalists who've never had to meet a payroll and don't even know what is the individual market.

We're invisible to late-night TV clowns who get their Obamacare-at-all-costs talking points from Chuck Schumer.

We're pariahs to social justice healthcare activists and Democrats who want us to just shut up and subsidize everyone else's insurance.

And we're expendables to establishment Republicans who hoovered up campaign donations on the empty promise to repeal Obamacare -- and now consider amnesty for immigrants here illegally and gun control higher legislative priorities than keeping their damned word.

https://townhall.com/columnists/michellemalkin/2017/10/11/obama-lied-my-fourth-health-plan-died-n2393283?utm_source=thdaily&utm_medium=email&utm_campaign=nl&newsletterad=

You read articles, hear people speaking about it, but when is the last time you heard them say look we need to go after the ROOT of the problem which is why it is so expensive in the first place?

Solve those issues like tort reform, pharmacy cartel, etc.

Put a REAL system in place for all the fraud billing going on out there that you and I pay for year after year.

May not be connected to healthcare directly but go after all the frauds on disability.

The ones who are truly physically disabled most of them have the ability to work on the computer they could do so much work a month for the government billing or what ever to help out the money paid to them.

Obamacare costs projected to rise faster than inflation in next decade as enrollment declines

Obamacare premiums will rise an average of 5 percent a year over the next decade, much higher than the annual inflation rate, the government’s chief scorekeeper predicted Thursday, saying that while the 2010 health care law is stable, the government will have to pump in more money per customer to keep it running.

Enrollment is coming in far below predictions.

The Congressional Budget Office now estimates that just 12 million customers will buy insurance on the exchanges in 2027, down from the 18 million projected last year.

Overall, Obamacare is costing less than anticipated, but that’s because fewer people are enrolling, the CBO said. When figured on a per-enrollee basis, taxpayers are shelling out more, paying ever-higher subsidies to help low- and middle-income Americans afford insurance.

Within a decade, each person getting subsidized coverage will cost the government an average of $8,600, up from $5,550 this year.

Premiums are spiking because young and healthy customers didn’t sign up in large enough numbers in Obamacare’s early rounds, leaving insurers with a sicker, costlier customer base. Some plans have requested double-digit increases for two years in a row, while others have dropped out altogether.

Under President Obama’s framework, taxpayer subsidies rise with the cost of midtier “benchmark” plans, absorbing the cost for most consumers but forcing taxpayers to pony up more for the program.

“It’s a sign of a poorly designed program, but I don’t think it rises to the attention of the average taxpayer,” said Douglas Holtz-Eakin, president of the American Action Forum and former CBO director, who said bigger drivers of spending eclipse the dynamic.

The CBO said the administration is making matters worse by waffling on key decisions. Overall, premiums for benchmark plans will rise 15 percent next year alone, though they will drop in 2019 if the administration can settle the markets.

Enrollment is predicted to rise slightly next year, from about 10 million to 11 million, dampened in part by President Trump’s decisions.

“That increase in enrollment in 2018 is limited by projected premium increases due to near-term market uncertainty and by announced reductions in federal advertising, outreach, the enrollment period and other enrollment efforts, which push enrollment down,” analysts said, referring to the Trump administration’s decision to slash advertising and sign-up assistance by more than $100 million before enrollment season begins Nov. 1.

Democrats held up that part of the report as evidence that Mr. Trump is trying to sabotage his predecessor’s signature domestic achievement.

“By hindering Affordable Care Act outreach through funding cuts and creating uncertainty in the marketplace, Trump is causing premiums to increase and stifling enrollment in 2018 and beyond,” said Democratic National Committee spokeswoman Adrienne Watson.

Democrats say Obamacare is stabilizing after a tumultuous start, with insurers raising prices enough to break even or make a profit, and that public opinion is turning in favor of their 2010 signature law.

Republicans, who now control Congress, say enrollment is stalling because the public doesn’t like expensive and overly prescriptive plans in the exchanges.

Medicaid enrollment will continue to rise from 63 million this year to 70 million by 2027, with more states enticed into the Obamacare expansion.

Mr. Trump’s attempt to rally his Republican allies behind an Obamacare repeal bill fell short this year, opening the health care debate to a range of options on Capitol Hill.

Four Senate Republicans are pushing a last-ditch bill to replace Obamacare with block grants that empower states.

“They will find solutions that work better for their state than the Affordable Care Act,” said Sen. Bill Cassidy, Louisiana Republican.

From the left, a sizable number of Democrats are looking beyond Obamacare and pushing a government-run, single-payer program that they have dubbed “Medicare for all” to cover every American.

Meanwhile, a bipartisan crop of senators wants to strike a compromise that bolsters the existing program, ponying up enough federal money to prop up Obamacare’s exchanges — a win for Democrats — in return for giving states greater flexibility to shape their markets.

“To get a result, Republicans will have to agree to something that many don’t want to agree to — additional funding through the Affordable Care Act,” said Sen. Lamar Alexander, Tennessee Republican and chairman of the Health, Education, Labor and Pensions Committee. He wants to strike an agreement in the coming days so Congress can act before the end of the month.

Insurers must decide this month whether to participate in the Obamacare marketplace for 2018.

http://www.washingtontimes.com/news/2017/sep/14/obamacare-costs-to-rise-faster-than-inflation-cbo-/

Another Obamacare Tax Dead Ahead

While the GOP continues to fumble their promise to repeal Obamacare, another Obamacare tax is due to hit businesses come January 1, 2018.

Though they have not been able to repeal the Affordable Care Act because, in all honesty, they don’t really want to, they should be able to at least write a piece of legislation to stop Obamacare’s rules applying a “Health Insurance Tax” (HIT) of between 4 and 6 percent on every health plan sold in America, not including self-insurance.

Quin Hillyer writes:

Critics have urged Congress for months to use various legislative vehicles to repeal or at least delay the tax, but so far Congress has not been able to make a repeal or delay fit into any one bill.

The HIT was originally slated to take effect several years ago, but Congress delayed it several times, most recently in a government-funding bill President Barack Obama signed in 2015.

Grover Norquist of Americans for Tax Reform wrote that “Next year alone, the health insurance tax will total $12.3 billion, according to the Congressional Budget Office. Over the next decade, it will result in nearly $145 billion in higher taxes.”

Norquist further wrote: “Any [of HIT’s] costs are passed directly to small businesses that provide healthcare to their employees, and middle class families through higher premiums. The tax even impacts the care received by seniors through Medicare advantage coverage and low-income Americans that rely on Medicaid managed care. According to the American Action Forum, the tax is responsible for premiums increasing by as much as $5,000 over a decade and half of the tax will be paid by those earning less than $50,000 a year.”

Even if insurance companies don’t pass the entire tax directly through to consumers, a group of companies led by United Health publicized a study showing HIT alone would force premium hikes next year of 2.6 percent. And that’s on top of other factors causing huge premium increases in an Obamacare market struggling to stay afloat.

The GOP have once again sold the American people out just like they were doing when they took control of the House under John Boehner and just like they did when they took control of the Senate.

Instead of providing the people actual relief, they have continued to allow Obamacare to be solidified in society.

The cost on this tax alone is devastating.

Estimates are that this tax alone could cost 286,000 jobs to be lost by 2023, according to the National Federation of Independent Business and there’s not doubt it will add to the increasing numbers of insurers offering plans in each state.

This means that American citizens will pay the cost not only for the Democrats decision to shove this unconstitutional legislation down our throats but also the cost of Republicans inaction to repeal the pretended legislation that is an albatross around our necks.

While RINO Speaker of the House Paul Ryan (R-WI) says the HIT is a “bad tax,” he has done nothing to stop it. In fact, it was Ryan who passed a spending bill of over $1 trillion dollars and helped to continue the implementation and funding of Obamacare.

Ryan should just change his name to Judas because that is what he is.

With that said, until they can get their act together to do what they actually promised the people who put them into office, there does seem to be at least one or two ways Congress could keep this tax from taking effect.

According to Leslie Small:

Two recent reports commissioned by UnitedHealth estimate that the return of the tax in 2018 will increase health insurance premiums by as much as $22 billion—or 2.6%—and cost the Medicaid program $5.5 billion. Conservative groups have also petitioned Congress to repeal both the health insurance tax and medical device tax.

However, while it seems as though at least extending the moratorium would be relatively uncontroversial, that task is far easier said than done.

For one, Congress has a slew of pressing issues to attend to in September, such as raising the debt ceiling and ensuring the government is funded.

And while tax reform—another of the GOP’s main priorities—might seem like an obvious vehicle, leaders in the House have said they don’t want any such legislation to address healthcare taxes, according to Axios. Addressing the ACA’s taxes also isn’t currently on the table in the Senate’s bipartisan talks about how to stabilize the individual exchanges.

There is some hope, however, that a health insurance tax relief provision could make its way into either a stabilization package that Rep. Mark Meadows, R-N.C., and Tom MacArthur, R-N.J., are formulating, or a long-shot ACA repeal-and-replace bill championed by Sen. Bill Cassidy, R-La., and Sen. Lindsey Graham, R-S.C. In addition, the article notes that the tax could be addressed in a bill to reauthorize the Children’s Health Insurance Program in the event that gets pushed back to December.

If Congress is able to at least delay the tax again, that could help mitigate insurers’ mounting concerns about operating on the ACA exchanges next year. As a recent report from consulting firm Oliver Wyman states, continuing the moratorium would “help reduce the significant premium increases and provide more stability to the individual ACA market.”

I’m not holding my breath because I actually think a majority of Congress wants this to fail so they can be the Savior's and walk in a single payer plan, full on Socialist Medicine, something that even Donald Trump would be proud to sign into law.

http://sonsoflibertymedia.com/another-obamacare-tax-dead-ahead/

Northwell to close CareConnect

There is now a new casualty regarding the uncertainty as well as some problems inherent in the implementation of the Affordable Care Act: Northwell Health is shutting down its insurer.

CareConnect, the insurer set up by Northwell Health, has decided to shut down, after being denied a portion of its rate request and in the wake of large charges imposed on it through the Affordable Care Act and ongoing uncertainty.

The decision, which comes amid questions as to whether federal subsidies will continue and amid other persistent problems with the Affordable Care Act, is a huge blow to the state’s, and Long Island’s, health insurance market.

“It has become increasingly clear that continuing the CareConnect health plan is financially unsustainable, given the failure of the federal government and Congress to correct regulatory flaws that have destabilized insurance markets and their refusal to honor promises of additional funding,” Northwell CEO Michael Dowling said.

The New York State Department of Financial Services issued a statement regarding CareConnect’s decision to “withdraw from the New York health insurance market.”

Department of Financial Services Superintendent Maria Vullo blamed “the repeated actions of the federal government to undermine the Affordable Care Act at this time in the insurance cycle.”

She said CareConnect has decided to “begin an orderly wind down from the market,” but added that “this decision will help Northwell focus on its core mission to deliver healthcare services to New Yorkers.”

Northwell had requested a 29.7 percent hike for individuals, but was granted 23.1 percent, and requested a 19.3 percent small group hike, but obtained 15.5 percent.

“One of the underlying flaws of the law is this flawed financial methodology they use for insurers, which is why so many insurers are getting out of exchanges,” said Terry Lynam, a Northwell spokesman. “That’s what’s causing these premium increases.”

Jason Samel, head of JayMar Insurance, said the decision to close the insurer is going to have a big impact on the state’s and Long Island’s insurance market.

“With over 100,000 enrollees, CareConnect’s exit from the marketplace is going to create havoc for consumers, businesses, and brokers much the same way the shutdown of Health Republic did in the past,” he said. “I am really concerned for our Long Island community.”

Samel called this “an unfortunate pitfall of the Russian roulette” that he said President Donald Trump and the Republican party “have been playing with our healthcare system.”

The announcement came as Modern Healthcare named Northwell Health CEO Michael Dowling the 38th most influential person in healthcare – but named Republican legislators and President Donald Trump toward the top of the list.

Northwell Health earlier said the failure to obtain its full rate hike request compounded uncertainty and problems.

And Northwell Health said that the fact that it had been compelled to pay more than $100 million into what’s known as a risk adjustment pool pushed the insurer into the red.

The Affordable Care Act includes a risk adjustment system designed to compel newer insurers, particularly with healthier patients, to pay money that goes to other insurers.

The problem, Northwell Health had said, was that it was being implemented in a way that essentially imposed a huge levy on it, making it question whether it could continue offering insurance.

Northwell will be submitting a withdrawal plan to the state, but CareConnect operations will continue over the next year as it said it “works with its customers, businesses, and others to help transfer policy holders to other health plans.”

Throughout the transition, CareConnect said it will continue to pay claims and serve members, patients, and providers.

“Many of CareConnect’s more than 200 employees will continue to have jobs during this transition period, and Northwell will assist them in trying to find other suitable positions within the health system,” according to the insurer.

Even after Northwell’s decision, Vullo sought to stabilize the insurance market, saying “New York’s healthcare market remains robust and consumers across New York have real choice of coverage.”

Some other insurers sought to position themselves to serve customers who will be seeking health insurance.

“It’s likely that many of CareConnect’s 120,000 members — particularly those with small business health insurance – may look to Oscar Health as an option,” a spokeswoman for Oscar Health said.

Oscar Health just introduced a new health plan for small businesses, Oscar for Business, and was the only insurer to reduce its premiums for small businesses next year, cutting them by 3.2 percent.

She said the state “will work with CareConnect on an orderly transition to ensure that all of its members know their full options and continue to receive healthcare coverage without interruption.”

Vullo called on the federal government to “end this continued uncertainty, immediately act to protect our markets by fully paying the cost-sharing subsidies for good and not piecemeal.”

She called on the federal government to approve subsidies and faulted it for seeking to reduce the enrollment period, which she said would likely lower the number of people who are insured.

“As much as we regret having to make this decision to withdraw from the market, I continue to believe in the strategy of CareConnect, population health and the benefits that come from value-based care,” Dowling said.

http://libn.com/2017/08/24/northwell-to-close-careconnect/

Obamacare Co-Op Now in State Receivership After Exiting Obamacare Exchanges

Minuteman Health of Massachusetts and New Hampshire announced in June it was planning to exit the Obamacare exchanges next year, but now the co-op is being placed in state receivership due to a lack of capital.

The Massachusetts Commissioner of Insurance, Gary Anderson, announced that the Obamacare co-op is now under its control as the Supreme Judicial Court granted the commissioner receivership. The commissioner said Minuteman Health’s capitalization is very thin, and this action was done to protect policyholders and health care providers.

Even though the commissioner says the co-op has limited capitalization, it notes it is still solvent and has enough funds to pay all of its insurance claims.

Chris Goetcheus, a spokesman for the Division of Insurance, said that while Minuteman’s risk-based capital has been low for some time, “the commissioner had decided it had reached a point where he needed to take control of the company and make sure providers were paid.”

"It’s the normal course of business," Goetcheus said. "Policy holders will contact Minuteman as they have previously. Providers will be paid in a timely fashion. Business as usual. We will be in very close dialogue with Minuteman as we have in the months leading up to this. Effectively the commissioner is in charge of the company so we will have all the info the company has."

http://truepundit.com/obamacare-co-op-now-in-state-receivership-after-exiting-obamacare-exchanges/

https://www.bizjournals.com/boston/news/2017/08/03/minuteman-health-placed-under-state-control.html

Only the people that are paying full price or damn near it are the only ones that are gonna get hit with that. The peeps that are getting it free or damn near it will continue to get it free. I hope the peeps paying tell them to get f'd and bail.

Insurers want to hike Obamacare rates in Illinois up to 43 percent

Insurers want to raise rates by up to 43 percent for Illinois customers who receive health care coverage under the Affordable Care Act.

Among the companies seeking double-digit rate hikes on most of their plans starting next year are the three insurers that offered Obamacare coverage in Cook County this year, according to rate reviews released by the federal government on Tuesday.

More than 351,000 Illinois residents are enrolled in Obamacare, with most of them — nearly 310,000 — covered by Blue Cross Blue Shield of Illinois.

The company is anticipating rate increases averaging 38.2 percent on its BlueCare Direct plans; 14.5 percent on its Blue Precision plans; 9.3 percent on its Blue FocusCare plans, and 5.4 percent on its Blue Choice Preferred plans.

Cigna HealthCare wants a 37.7 percent increase, which would affect nearly 27,000 Illinoisans, and Celtic Insurance, the third Cook County Obamacare insurer, plans to raise rates by about 15 percent for its more than 36,000 enrollees.

Health Alliance Medical Plans, which offers Obamacare plans in central and downstate Illinois has proposed a whopping 43.1 percent rate hike.

In the rate reviews, most companies pointed to rising costs for medical services and prescription drugs as the cause of surging rates.

Also apparently factoring into the rate hikes is the precarious state of the health care system under the Trump administration. Blue Cross Blue Shield cited “a loosening on the enforcement of the individual mandate,” while Cigna highlighted doubt as to whether the federal government will keep providing subsidies to insurers that lower copayments for low-income customers.

Insurers can change their proposed increases before they go into effect on Jan. 1, 2018. State officials can recommend changes to the companies’ proposals, but they don’t have the power to alter or reject them.

http://chicago.suntimes.com/news/insurers-want-to-hike-obamacare-rates-in-illinois-up-to-43-percent/

I totally agree with you

I'm sure you're right.

She did well getting to the core of the problem leaving politics behind.

Disabled Boy’s Mom Clears The Air About Trump, Congress & Obamacare

"... very professional and frustrated ..."

The mother of the boy who became fodder for a misleading attack on President Donald Trump doesn’t care about the media fuss over a video edited to wrongly imply Trump ignored her son at a recent event.

What she cares about is getting Obamacare fixed.

As reported by Western Journalism, author J.K. Rowling was forced to apologize after using an edited video clip to falsely accuse Trump of snubbing Monty Weer during a White House event last week.

Marjorie Kelly Weer, the boy’s mother, said there is someone to blame in Washington, but it is not Trump.

“You want to know who snubbed my son? Congress snubbed my kid in D.C. when they failed to pass meaningful legislation. Everyone missed the point of why we were there in the first place. They didn’t come up with a dynamic plan and they didn’t go out and sell it to the American people. If they have a plan, what is it and where is it?” she said.

If Congress has disappointed her, the Trumps did not.

First lady Melania Trump spoke to Weer and her family on an earlier visit to the White House.

“She was very kind and very gracious,” Weer said. “She didn’t have to take time out of her busy schedule.”

After they returned home, Melania Trump sent Monty a package with 11 books, a book bag, a puzzle, candy, a stuffed bunny and a “Make America Great Again” hat.

On Weer’s second visit, she met the president.

“He came across as very professional and frustrated about what he has to work with in Congress,” she said. “He’s not what they make him out to be in the press.”

“I appreciate people trying to stand up for me and my family but even slinging mud at people like (Rowling) doesn’t move the conversation. I like action, I like movement and I like solving problems,” she said.

Weer said that when the media thought it could get a good anti-Trump story, everyone wanted to talk to her. But when it comes to her problems with Obamacare, it is a different story.

“Where was CNN when we were complaining about health care? That’s why I went with Fox News, they talked to us beforehand,” she said, adding that most media outlets “want to use my family. They saw a potential catfight between me and J.K. Rowling and I’m not giving them that.”

Monty, 3, suffers from spina bifida. Majorie Weer’s South Carolina provider became out of network in 2016, which forced her to go to Boston Children’s Hospital for her son’s yearly check-up. Then she learned that due to problems with Obamacare, the hospital might only accept in-state patients and launched a six-month battle, which she finally won, to gain access.

Weer wondered why if she could adapt and overcome every time she hit a wall, Congress cannot do the same.

“In my case, a ‘no’ can equal death. If you hit a wall, who the heck cares? It’s just a wall, you can work through the impossible. That’s the world I live in,” she said.

Weer criticized the “we can’t” attitude of Congress and said if Congress can’t do its job, the American people need to come up with solutions and push Congress to adopt them.

“We need to be a part of the discussion because it’s our health care, our money and the lives of our family at stake here,” she said. “That’s why I was in Washington. In the middle of changing diapers, I’m trying to come up with ideas that might work too.”

Weer said if this Congress can’t do the job, she will remember.

“Get your job done, or we’ll sit home in 2018,” she said.

http://www.westernjournalism.com/disabled-boys-mom-clears-air-trump-congress-obamacare/?utm_source=Email&utm_medium=PostUp&utm_campaign=WJDailyEmail&utm_content=2017-08-05

The big insurers’ troubles have led critics to raise questions about the overall sustainability of the ObamaCare model

A disproportionate number of unhealthy customers have signed up for the exchanges, which provide tax subsidies to pay for insurance, causing unbalanced risk pools for many insurers.

Molina Healthcare Pulling Out Of Two States, Raising Premiums 55% In Remaining States

Molina Healthcare announced today that the company will be pulling out of Obamacare exchanges in Utah and Wisconsin and reducing its participation in the Washington market.

The company is still considering its continued participation in other states. In those states where it does remain, Molina will be requesting a 55% increase in premiums for 2018. From the company’s press release:

We are exiting the Utah and Wisconsin ACA Marketplaces effective December 31, 2017. For the three months ended June 30, 2017, these two health plans reported a total of $127 million in Marketplace premium revenue (16% of consolidated Marketplace premium revenue), and a combined Marketplace medical care ratio of 128%.

In our remaining Marketplace plans, we are increasing 2018 premiums by 55%. The increase takes into account the absence of cost sharing reduction subsidies. Had we assumed that cost sharing reduction subsidies would be funded for 2018, the premium increase would have been 30%.

We are also reducing the scope of our 2018 participation in the Washington Marketplace.

We continue to closely monitor the current political and programmatic developments pertaining to our 2018 participation in other Marketplace states, and subject to those developments, will withdraw from 2018 participation as may be necessary.

All of this comes as Molina announced a net loss of $230 million for the second quarter. Monday the company announced plans to lay off about 10% of it’s workforce. From Modern Healthcare:

Medicaid health plan Molina Healthcare intends to lay off 1,400 employees, or 10% of its workforce, over the coming months to try to offset losses from its Obamacare exchange business, the company said in an internal memo to employees Monday…

“As part of our drive for operational efficiencies, we are simplifying our organizational structure and reducing the size of our workforce. This was a very difficult decision, and one that I do not take lightly,” White said.

Molina fired its CEO and CFO, the sons of the company’s founder, in May. Molina was considered one of the big successes in the Obamacare market as recently as last September. From the Hill:

Molina’s plans are now among the most affordable on the market. But unlike other companies that tried to attract customers in the first year of ObamaCare with ultra-cheap plans, Molina is staying profitable…

The big insurers’ troubles have led critics to raise questions about the overall sustainability of the ObamaCare model.

But Molina sees more room for his company to grow. It has already announced plans to expand this year into three more markets.

It was all going so well for Molina until it wasn’t. Now the low-cost provider is cutting staff, pulling out of at least two states and jacking up premiums by 55% in the remainder. Even without the possibility of cost-sharing reduction payments being cut off by the Trump administration, Molina would still be requesting a 30% increase in premiums. There’s no way to spin that as a success story.

http://hotair.com/archives/2017/08/02/molina-healthcare-pulling-two-states-raising-premiums-55-remaining-states/?utm_source=hadaily&utm_medium=email&utm_campaign=nl

Obamacare Deathspiral Continues

On Thursday, Health Insurer Aetna has announced that they are completely withdrawing from Obamacare in 2018.

Washington Examiner Reported: Health insurer Aetna announced Thursday that it would completely withdraw from the Obamacare exchanges in 2018, after seeing its profits soar from reducing its participation this year.

The company said during an earnings call that it was withdrawing from the exchange in Nevada, the last state it had considered staying in. Aetna was leaving the possibility open because it was applying for a Medicaid managed care contract, and the state gives extra consideration to insurers that participate in both programs.

During its second-quarter earnings call on Thursday, however, Aetna said it was not moving forward with the recently awarded contract and would be leaving the exchange as well.

"Our 2018 participation was required based on a Medicaid contract with the state," spokesman T.J. Crawford said in an email. "As a result of terminating that contract for unrelated reasons, we will not have a presence on the individual exchange in Nevada."

Aetna notified state officials about its intent to no longer participate in the Medicaid managed care program in a letter sent July 1, citing low enrollment.

"This is far less than the critical number needed to ensure a viable Medicaid plan capable of delivering quality care and competitive programs," the chief executive officer of the program wrote, citing an enrollment figure of 1,600.

Aetna's second-quarter profit jumped 52 percent, far ahead of projections, and the company plans to invest in more Medicare Advantage plans.

Aetna has been gradually withdrawing from the Obamacare exchanges. It had decided to pull out of the exchanges in other states because it lost $700 million between 2014 and 2016 and was projected to lose $200 million in 2017 despite having already significantly reduced its participation in the exchanges to only four states.

A disproportionate number of unhealthy customers have signed up for the exchanges, which provide tax subsidies to pay for insurance, causing unbalanced risk pools for many insurers. Aetna also has cited uncertainty over the future of the law and over whether it will receive federal payments as a contributing factor to its decision.

http://redstatewatcher.com/article.asp?id=88838

Estimates Show How Bad Obamacare Will Be in 2018

Republicans in Congress have failed to repeal and replace Obamacare — something they have promised the American people seven years — and President Donald Trump has made it clear he wants to take action now before more Americans suffer.

A new study from the Centers for Medicare and Medicaid Services indicated 1,332 counties in the United States — more than a third of the total — will have access to only one health insurer on the Obamacare exchanges.

The CMS also reported that 40 counties out of 3,007 in the country currently don’t have access to any health insurers on the Obamacare exchanges, according to the Free Beacon.

While Democrats are aware that Obamacare is on the verge of imploding, they have chosen to obstruct President Trump rather than help him fix a failing healthcare system plaguing the American people.

“This could represent more than 2.3 million Exchange participants that will only have one choice and may not be able to receive the coverage they need,” the agency said.

At least 27,660 Americans living in counties that the CMS projected will not have any health coverage on the Obamacare marketplaces will have nowhere to turn next year. The CMS estimated that Obamacare insurance premiums increased by an average of 21.6 percent between 2016 and 2017.

After Sen. John McCain (R-AZ) voted to keep Obamacare last week, President Donald Trump suggested allowing Obamacare implode to force Democrats and Republicans to work together to repeal and replace Obamacare.

http://conservativetribune.com/obamacare-will-devastate-nation/?utm_source=Email&utm_medium=minutemennews&utm_campaign=dailyam&utm_content=libertyalliance

When high deductibles hurt: Even insured patients postpone care

In November 2015, Tina Heck was in her garage lifting 40-pound bags of wood pellets to fuel her heating stove, when something went very wrong with her back.

“The next day, I could barely walk,” said the 55-year-old who lives on an acre of land in Nevada City, Calif., 60 miles northeast of Sacramento. The cause: a bulging disc in her lower spine, which shoots pain down her leg and makes her back stiff.

The injury wasn’t Heck’s only setback. The initial MRI, cortisone shot and doctor visit cost her $3,000 because her health plan requires her to shell out $5,000 before insurer payments kick in.

She doesn’t want to explore other treatment options because of that high deductible. Heck, who makes $68,000 a year in marketing for a nonprofit, is not willing to add more debt on top of her credit-card and mortgage payments.

“I’m in pain every day,” she said, but “it’s not bad enough to go into debt.”

The concept behind high-deductible plans was to lower premiums and reduce overall health costs by ensuring that consumers shared the financial burden of their own health care decisions. But evidence is mounting: High deductibles have actually forced people to delay care that could prevent health emergencies later or improve their quality of life.

Regardless of what happens to the Affordable Care Act, such plans are likely to become more widespread as health care costs continue to rise.

Just over half of people with health plans from their employers now have a deductible of $1,000 or more, up from 10% in 2006, according to the Kaiser Family Foundation. (Kaiser Health News, which produces California Healthline, is an editorially independent program of the foundation.)

“People who have medical problems that can be put off tend to do so much more now because of the high deductible,” said Dr. Ted Mazer, a San-Diego based head and neck surgeon who is president-elect of the California Medical Association.

Annual deductibles can amount to many thousands of dollars on some plans. Covered California bronze plans, with the lowest premiums available on the exchange, carry deductibles of $6,300 for an individual and $12,600 for a family.

A Kaiser Family Foundation survey released this year showed that 43% of insured people reported having trouble paying their deductible, up from 34% in 2015. (Kaiser Health News, which produces California Healthline, is an editorially independent part of the foundation.)

In one study by the liberal advocacy group Families USA, more than a quarter of people in high-deductible plans delayed some type of medical service such as a doctor visit or diagnostic test. And 44% of adults with high out-of-pocket expenses put off medical care, according to a nonpartisan Commonwealth Fund study.

Another recent study by researchers at the University of California-Berkeley and Harvard University found that people with high-deductible plans spent 42% less on health care before meeting their deductibles, primarily by reducing the amount of health care they received, not by shopping around for a better price.

Jonathan Kolstad, associate professor of economics at UC-Berkeley’s business school and co-author of the study, said patients dropped both needed care, such as diabetes medication, and potentially unnecessary care, such as imaging for headaches.

“Left to their own devices, people [in high-deductible plans] seem ill-equipped to make their own decisions” about what care they need, and what care they don’t, Kolstad said.

Mazer said that, in his practice, people have delayed all kinds of treatment that may not save “life or limb” but involved medical conditions that interfered with breathing or sleeping.

He said he’s had patients who needed a biopsy to determine if an abnormal vocal cord was cancerous, and they put it off because of the cost.

“I have to make the phone call and say, ‘We’re looking at a mass that may be malignant and if you put it off you’re putting yourself at risk,’ ” Mazer said. “And I’ll tell you, we’ve had people take that risk.”

Recent Republican proposals to repeal Obamacare have promoted the use of high-deductible plans by allowing people to put away more tax-free dollars into the health savings accounts that consumers use in conjunction with those plans. And experts said the proposals would also spur the growth of these plans — by cutting the subsidies available through exchanges, inducing customers to look for cheaper plans with higher deductibles.

Conservatives say insurance that promotes personal financial responsibility helps tamp down overall health costs. Hoover Institution analysts, for example, argue that high deductibles encourage patients to “choose wisely.”

But new evidence suggests that putting off care can be dangerous and, eventually, more costly to patients.

A March 2017 Harvard study found that low-income patients with diabetes who had high-deductible plans delayed visits for complications such as skin infections and pneumonia. They wound up getting more expensive care later on.

Patients may try to treat their conditions at home, or hope they go away — but if that approach fails, “they then have to seek care at the emergency department,” said Frank Wharam, a health policy researcher at Harvard Medical School and lead author of the study.

Wharam said the middle-income earners he studied didn’t suffer any adverse effects from health care choices they made in high-deductible plans, adding that more studies are needed on that group.

Sabrina Corlette, from the Georgetown University Center on Health Insurance Reforms, said that until national health policy addresses the “underlying costs of care,” patients in high-deductible plans will likely be stuck with the difficult task of figuring out what medical attention they need or can afford.

Heck said the symptoms from her back injury have changed — the pain is in a different part of the body than it was right after the injury. But she’s not even considering a trip to a nearby clinic for a new assessment. That would require another MRI, she said, which could cost at least $1,500, and it might not even help her. If her deductible weren’t as high, she’d feel “freer” to explore other health care options, she said.

For now, she’s taking a lot of ibuprofen and seeing a chiropractor.

“A lot of people get stuck in this place,” she said.

http://www.dailynews.com/government-and-politics/20170727/when-high-deductibles-hurt-even-insured-patients-postpone-care?source=topstoriesrot

Covered California announced increased rates of 12.5 percent for its 2018 health insurance plans

Anthem Blue Cross will stop selling individual Covered California health plans in the Southern California market but will still sell in parts of Northern and Central California.

Covered California on Tuesday announced that insurance rates will jump an average of 12.5 percent for next year, amid uncertainty about the future of Obamacare.

“Californians are paying about 3 percent more than they would have if not for the uncertainty,” said Peter Lee, executive director of the state’s exchange.

Additionally, Anthem Blue Cross will stop selling individual health plans in the Southern California market but will still sell in parts of Northern and Central California.

“The uncertainty is also having an impact on plan participation,” Lee said. “It’s significant. About 153,000 of their consumers will need to shop and change into 2018.”

Last year, rates increased an average of 13 percent statewide, which was much higher than in the two years before. But this time, insurance companies were left unsure if lawmakers will still move to dismantle the law, and if the Trump administration will continue making monthly payments that allow them to reduce co-pays and deductibles for low-income consumers as required by the Affordable Care Act. Later this month, Covered California will decide whether to attach an average 12.4 percent surcharge to the silver-tier plans that offer the reduced out-of-pocket costs for about 650,000 Californians.

Roughly 551,510 people in Los Angeles, Orange, Riverside and San Bernardino counties purchase subsidized plans through Covered California.

Covered California announced average rate increases of 4 percent in 2015 and 4.2 percent in 2014.

http://www.dailynews.com/government-and-politics/20170801/covered-california-announced-increased-rates-of-125-percent-for-its-2018-health-insurance-plans?source=email

15mn Americans Would Opt Out Of Obamacare If They Could – CBO

Posted on 31st July 2017 | By admin

By next year, 15 million people would opt out of the Affordable Care Act, widely known as Obamacare, if one of its key provisions – individual mandate – were repealed today, shows an estimate by the Congressional Budget Office.

Getting rid of Obamacare’s individual mandate, which imposes financial penalties on people who don’t buy insurance, would leave 15 million uninsured, according to the CBO.

The congressional body tasked with estimating the budget impact of proposed bills said by 2026 the number of uninsured as a result of repealing the individual mandate would be 16 million people.

Many Democrats have interpreted the estimates as the number of people who would be deprived of insurance as a result of the provision’s repeal. However, some analysts see it as the number of Americans who were forced into Obamacare.

“If the CBO projections are correct, there are 15 million Americans who would directly benefit from the repeal,” said Scott Rasmussen, the founder of conservative-leaning polling outlet Rasmussen Reports.

“If the individual mandate were to be repealed, many Americans might be interested in purchasing less comprehensive and less expensive coverage. The CBO has offered no estimates of how many might take advantage of such alternatives,” Rasmussen added. “It is currently illegal for insurance companies to offer less expensive plans offering less comprehensive coverage.”

Having failed to secure enough votes for a straight repeal of the Affordable Care Act, congressional Republicans are planning to put forward what they call a ‘skinny repeal.’

Not much is known about the new proposal as of Thursday morning, as Republicans lawmakers have yet to publish the text of the bill, but preliminary reports suggest that it would eliminate Obamacare’s individual and employer mandates, along with some of its taxes.

It is also expected to commit $45 billion for states to spend on opioid addiction treatment.

The Consumer Freedom amendment proposed by Senator Ted Cruz (R-Texas) or elements of it could also be included in the ‘skinny repeal’ bill that Republicans are preparing.

Cruz says his amendment would lower costs and raise individual enrollment by allowing insurers to sell cheaper plans to healthier people.

Many Democrats and some Republicans have objected to the measure, saying it would raise premiums for sicker people.

The ‘skinny’ repeal bill is “expected to accelerate health plans leaving the individual market, increase premiums, and result in fewer Americans having access to coverage,” a bipartisan group of governors, including Republicans Brian Sandoval of Nevada, Charlie Baker of Massachusetts, John Kasich of Ohio, and Phil Scott of Vermont, wrote in a joint letter Wednesday.

The CBO had previously estimated that repealing the individual mandate would raise premiums by somewhere between 10 and 20 percent – the increase would be driven by healthier people buying cheaper insurance, and the sicker paying more.

Congressional Republicans have for years pushed to repeal President Barack Obama’s signature healthcare legislation. However, with Trump waiting to sign a bill to repeal and replace Obamacare, the GOP has so far failed to unite behind one plan.

On Monday, the president scolded GOP senators who “have not done their job in ending the Obamacare nightmare.”

Trump also called Obamacare a “big, fat ugly lie,” citing as an example Obama’s 2009 statement: “If you like the plan you have, you can keep it. If you like the doctor you have, you can keep your doctor, too.”

http://unreportedtoday.com/2017/07/31/15mn-americans-would-opt-out-of-obamacare-if-they-could-cbo/

It never ends.

This countries actions 95% of the time is about buying votes, keeping votes, paying off old favors for votes, continuing each parties agenda.

We need to abolish this system start over with the constitution and no more political parties just regular people REPRESENTING the PEOPLE not BUYING the people!

Strong rope, High trees get er done!

Obamacare 40% Cadillac Tax Hits No Frills Plans Too. Like Your Plan, Keep Your Plan?

In 2010, House Speaker Nancy Pelosi urged passage of Obamacare so we could find out what’s in it. We found many new taxes, but in 2010, few worried about the Cadillac tax that was delayed until 2018. Besides, it would apply only to truly rich plans for the most elite. The numbers no longer seem so elite.

The tax applies to individual health plans worth more than $10,200 and family plans worth more than $27,500.

They are hit with a whopping 40% excise tax. Former Obamacare adviser Jonathan Gruber gloated that rising medical costs would ensure that the Cadillac tax would all but eliminate tax deductible company provided health insurance. Mr. Gruber even said President Obama was in the room when the Cadillac tax lie was created.

2018 now seems close and the Cadillac tax is looming. Many Democrats and Republicans may be curiously aligned in considering repealing it. Politico has an in-depth story on the Cadillac tax, noting that repealing it would cost $87 billion.

Even so, the 40% excise tax will clearly be a catastrophe. Rep. Frank Guinta (R-N.H.) introduced legislation to repeal it. Companies and unions must plan ahead as they negotiate benefits.

Plainly, the Cadillac name is a gross misnomer. It will apply to many benefits that are hardly elite. The sea change is enormous. Company provided health benefits have not been taxed for generations. And that is exactly what the deceptively named Cadillac tax does. It is broad too, applying to health savings and flexible spending accounts, supplemental insurance plans, and more.

Even plans that are not hit by the 40% tax in 2018 soon could be. After all, the Cadillac tax is linked to the consumer price index plus 1%. Medical and insurance costs are growing far faster, so more and more plans will be hit with the 40% each year. A survey by Mercer anticipates that one-third of employers will be hit by the tax in 2018, growing to 60% by 2022. It could be worse still.

And this is just want we know so far. It could be far worse. The IRS has already showcased how incredibly complex this tax will be, setting out approaches to the excise tax. Of all the taxes in the ironically named Affordable Care Act, none is more onerous, a whopping 40% on top of all other federal taxes. It is an excise tax, one of the most dreaded taxes there is. It sounds as if it taxes overly generous employer-provided health care plans for executives.

In reality, it seems likely to primarily hit union plans. Unions that have negotiated for generous health benefits may now wish they hadn’t. Across the board, the Cadillac tax puts pressure on employers to offer less-generous health insurance plans. The 40% tax is imposed on the cost of individual health plans above $10,200 for individuals and $27,500 for family coverage. The tax applies at a 40% rate on every dollar above those thresholds.

A reasonable response to the Cadillac tax is likely to be cutting of health insurance. Less generous coverage will presumably be provided. In large part, the result is likely to higher costs for employees, higher deductibles, and other add-ons that will harm employees. Doesn’t that go directly contrary to what proponents of the Affordable Care Act–including the President–represented? Like your plan, keep your plan?

https://www.forbes.com/sites/robertwood/2015/04/07/obamacare-40-cadillac-tax-hits-no-frills-plans-too-like-your-plan-keep-your-plan/#4899f39be0fb

How about Trump removing the labor unions exemption from Obamacare? If Obamacare is so great, why were the unions granted exemptions?

There are ACA exemptions/delays that President Obama has granted union groups.

1. In 2013, Obama excepted unions from paying fees that other large group health plans have to pay. That fee has been passed to those insured through non-union plans.

The union exemption deal will require that insurers who aren’t fully reimbursed by fees along with non-exempted self-insured employers will have to pay more to make up the shortfall. How will they make that up? How else but by passing on higher costs to their customers? The Department of Health and Human Services has confirmed that the fee for other non-exempt plans will be higher as a result.

Unions Get Big ObamaCare Christmas Present As Other Self-Insured Groups Get Scrooged

2. Under union pressure, the Cadillac Tax, a 40% tax on generous healthcare benefits was delayed to 2018 and may be scrapped altogether.

Even plans that are not hit by the 40% tax in 2018 soon could be. After all, the Cadillac tax is linked to the consumer price index plus 1%. Medical and insurance costs are growing far faster, so more and more plans will be hit with the 40% each year. A survey by Mercer anticipates that one-third of employers will be hit by the tax in 2018, growing to 60% by 2022. It could be worse still.

And this is just want we know so far. It could be far worse. The IRS has already showcased how incredibly complex this tax will be, setting out approaches to the excise tax. Of all the taxes in the ironically named Affordable Care Act, none is more onerous, a whopping 40% on top of all other federal taxes. It is an excise tax, one of the most dreaded taxes there is. It sounds as if it taxes overly generous employer-provided health care plans for executives.

In reality, it seems likely to primarily hit union plans. Unions that have negotiated for generous health benefits may now wish they hadn’t. Across the board, the Cadillac tax puts pressure on employers to offer less-generous health insurance plans.

The 40% tax is imposed on the cost of individual health plans above $10,200 for individuals and $27,500 for family coverage. The tax applies at a 40% rate on every dollar above those thresholds.

A reasonable response to the Cadillac tax is likely to be cutting of health insurance. Less generous coverage will presumably be provided. In large part, the result is likely to higher costs for employees, higher deductibles, and other add-ons that will harm employees. Doesn’t that go directly contrary to what proponents of the Affordable Care Act–including the President–represented? Like your plan, keep your plan?

https://www.quora.com/Which-labor-unions-are-exempt-from-Obamacare

Reality check: Obamacare is KILLING people right now

By J D Heyes

Monday, July 24, 2017

(please note: The underlined words are 'clickable' links when accessed via the link at the bottom of this page)

In case you haven’t noticed — and, unfortunately, far too many Americans haven’t — the Democrats have an honesty problem. Seems they can never really say what’s on their mind because if they do, if they present themselves honestly, then far fewer people would support them.

Like when they call Republican efforts to reduce the growth of federal spending harmful spending cuts. They’re not cuts, they are reductions in spending growth.

Obamacare was full of Democratic misdirection and outright lies. Take the name of the legislation enacting it: The Affordable Care Act. By any definition, Obamacare isn’t affordable for the vast majority of Americans.

We were promised that the law would reduce insurance premiums; it hasn’t. They’ve grown dramatically, even for people who qualify under Obamacare’s expanded subsidies.

We were promised that we’d have more choices; we don’t. More insurers are bailing out of the Obamacare exchanges leaving, in some cases, only one.

We were told our deductibles would go down; for most, they’ve gone up — so much so that for millions of Americans, it’s like they don’t really have anything other than catastrophic coverage. In fact, their coverage is so bad that it literally is affecting their health.

And yet, Democrats are saying that Republican efforts to repeal Obamacare and replace it with a more free market-oriented solution, promoting real choice and giving control over healthcare back to patients and providers will cause mass death. It’s simply a lie.

The Democrat-passed Obamacare is a mandate “not to get care, but to get coverage,” Sen. John Barrasso (R-Wyo.) said last year.

“And many people are finding the coverage is not at all of value to them because they can’t get care. Either…their doctors don’t take Obamacare or the deductibles are so high that they’re never able to get to the insurance,” he said.

“We’re seeing numbers in New Hampshire above 40 percent increases; in New York, above 40 percent increases; in New Mexico, where Blue Cross-Blue Shield of New Mexico pulled out a year ago, they’re talking about coming back in, but only if they can get a rate increase of over 80 percent,” he said, in reference to sky-high increases in premiums and deductibles.

This reality is affecting health outcomes. Because Obamacare-induced out-of-pocket expenses are so high, many Americans have simply stopped going to doctors for care because they can’t afford to.

Bloomberg News reported just days before the November election:

Michelle Harris, a 61-year-old retired waitress in northwest Montana, has arthritis in both shoulders. She gets a tax subsidy to help buy coverage under Obamacare, though she still pays $338 a month for the BlueCross BlueShield plan. Yet with its $4,500 deductible, she says she’s doing everything she can to avoid seeing a doctor. Instead, she uses ibuprofen and cold-packs.

Obamacare, in fact, is so bad and has so distorted the health insurance markets — making it unaffordable — that the law is literally killing people, according to some evidence.

Other evidence suggests that while Obamacare expanded Medicaid coverage to allow people to say they have insurance, their health outcomes are similar to people who don’t have any insurance at all, American Spectator notes.

None of this is lost on President Donald J. Trump, who is busy chiding Senate Republicans for dropping the ball on Obamacare repeal, contrary to their previous promises (and votes) to do so.

“Obamacare has wreaked havoc on the lives of innocent, hard-working Americans,” Trump said Monday at the White House, surrounded by families who have been hurt by the law.

He lashed out at Democrats’ demagoguery, claiming the GOP repeal will ‘kill thousands’ of Americans.

“They say death, death, death. Well, Obamacare is death,” Trump said. “That’s the one that’s death.”

Studies show he’s right.

J.D. Heyes is a senior writer for NaturalNews.com and NewsTarget.com, as well as editor of The National Sentinel.

Sources include:

TheFederalist.com

Spectator.org

CNSNews.com

Bloomberg.com

TheNationalSentinel.com

http://www.naturalnews.com/2017-07-24-reality-check-obamacare-is-killing-people-right-now.html

Trump can't control the "never Trumpers" and the RINOS. Traitors to their party!

As he should. But .................. instead of doing what he said before becoming president and TRULY fixing health care like tort reform, big pharma's drug cost scams, list goes on and on it's been the same old game.

Each party does what ever they think will get votes instead of doing the RIGHT thing.

Both parties can just go away and lets start over with the constitution, bill of rights, and a HIGH dose of COMMON SENSE!

I've had ENOUGH!

And btw ...................

The Largest Drug Cartel in the world your local pharmacies only get a fine but if you or I ripped off SCHEDULE ONE drugs the DEA would have us in prison for years. Just another example of the DEA in bed with Big Pharma!

BTW ........... Got to love it when they describe them as stolen or wait for it ........ here it comes ............. MISSING!

They actually used the word missing! Unbelievable!

Safeway to pay $3 million fine after drug thefts in Wash. spark investigation

by KOMO Staff

Tuesday, July 18th 2017

http://komonews.com/news/local/safeway-to-pay-3-million-fine-after-drug-thefts-in-wash-spark-investigation

SEATTLE - The Safeway chain has agreed to pay a $3 million penalty after a federal investigation found the company had failed to report the theft of thousands of opioid narcotic pills in Washington state and elsewhere in a timely manner.

U.S. Attorney Annette L. Hayes says the investigation began in 2014 when the Drug Enforcement Administration learned about irregularities at the Safeway pharmacy in North Bend, Wash., and another in Wasilla, Alaska.

The investigation showed that Safeway did not report the theft of tens of thousands of narcotic hydrocodone pills at the two pharmacies until months after the company discovered the pills were pilfered by employees.

Further investigation revealed a widespread practice of Safeway pharmacies failing to report missing or stolen controlled substances in a timely manner, Hayes said.

By law, pharmacies and other drug providers are required to notify the DEA of the theft or significant loss of any controlled substance within one business day of the discovery of the theft or loss.

Following the investigation, Safeway accepted responsibility for failure to report the thefts in a timely fashion and agreed to pay a $3 million penalty. The chain also agreed to implement a compliance agreement reached with the DEA to ensure such notification lapses do not happen again.

Hayes said the agreement is an important step in battling drug addiction.

“As our community struggles with an epidemic of opioid abuse, we call on all participants in drug distribution to carefully monitor their practices to stem the flow of narcotics to those who should not have them,” she said.

This is the third U.S. Justice Department settlement in the past year involving lax pharmacy controls and inconsistent adherence to DEA requirements, Hayes said.

In January 2017, the Justice Department reached an $11.75 million settlement with Costco and in July 2016 DOJ reached a settlement with Seattle Cancer Care Alliance over pharmacy control failures.

Trump blasts Obamacare

Obamacare’s Subsidies to Cost Taxpayers an Extra $10 Billion in 2017

Dec. 16, 2016

Earlier this year, the Obama administration published a report saying that a typical health insurance plan bought through Obamacare's exchanges would rise in price by about 22 percent this coming year. Administration officials responded by downplaying concerns about rising premiums, noting that most consumers would be largely insulated from those increases by the law's subsidies, which increase with the price of insurance.

The increased cost of insurance under the law, in other words, would be born by consumers rather than taxpayers. We now have a price tag showing exactly how much those higher premiums will cost the public.

The government will spend nearly $10 billion more this year, rising from about $32.8 billion in 2016 to about $42.6 billion in 2017, a 28 percent hike. The average monthly subsidy will rise from $291 per month to $367.

Those numbers come from a new report by the nonpartisan Center for Health and Economy, which used government data in combination with the organization's own subsidy estimates in order to produce the findings.

Thanks to far lower than expected enrollment, the total cost of Obamacare has come in lower than expected. But that cuts both ways, because the lower than expected enrollment is part of what's driving premium hikes. And what we see with this year's premium hikes is that the price tag of subsidizing those people who are signed up is rising rapidly—at significant public cost. Those people are only insulated from premium hikes because taxpayers are footing the bill.

And not everyone, of course, is insulated. A little more than 20 percent of enrollees in Obamacare's exchanges don't get any sort of subsidy at all, meaning they bear the full cost of any premium increases.

The report comes as Republicans have vowed to make repealing Obamacare a top priority after Donald Trump takes the White House in January. And it hints at some of the potential difficulties of repeal: Republicans in Congress have made it clear they favor a "repeal and delay" strategy in which Obamacare repeal legislation is signed quickly, but leaves the law's major components on the books for a number of years. That could accelerate the unwinding of the health insurance marketplaces, and perhaps lead to even higher premiums in the short term for those who maintain coverage under the law.

In the meantime, though, it also shows the sorts of struggles the law is having with rising costs to both taxpayers and consumers, and adds to the evidence that Obamacare in its current form cannot maintain a stable equilibrium.

http://reason.com/blog/2016/12/16/obamacares-subsidies-to-cost-taxpayers-a

I know of seven people who had cancer. All received chemo and all died. One had limited success for a couple of years but then it came back in her kidneys and that was the end.

Every one of the cancers was different, uterine, breast, 2 with colon, bone, bladder, and stomach. One friend had both breasts removed and she is still living. Four were family members, three were friends.

Right now I don't know anyone close with cancer or I would advise them to research alternatives.

Doesn't matter which party tries to fix insurance as long as both parties continue to support the scam treatment called chemo fraud will take place.

Not really sure what it takes to wake people up from the SCAM called CANCER treatment but maybe this video might help.

I been talking about it for some time now but people place Doctors up on a pedestal when if they knew the truth most Doctors, not all, but most worship money instead of treating you with GOD'S natural cures like cannabis combined with other natural products.

Problem is those natural ways of healing doesn't pay the yacht payments!

Chemo treatment is a SCAM!

Dr. Peter Glidden talks about the incredibly low success rate for chemotherapy as a cancer treatment.

Credit to ihealth ... https://www.youtube.com/user/iHealthTube

obamafraud was never looking good then or now.

A third grader could have ran the numbers and found out it was a SCAM!

Reminds me of the fools saying college should be free. Reality is a problem for so many. I asked this guy who was highly educated who heard that on the radio while I was i9n his home so if you think it should be free tell me who is going to pay for it?

He pauses ............. says I guess you are right.

Common sense doesn't grow in every ones garden.

Now with new heath care bill ..................

Problem is the republicans are placing a band aid on it instead of doing surgery and FIXING it.

The fraud alone in the medical field removing rid billing fraud, big pharma profit margins, tort reform, list goes on and on.

Same BS different day.

Both parties are about doing favors for votes and their own wealth, that list could go on and on also.

We the PEOPLE they long ago forgot. Only serve themselves.

The Congress is to debate the new healthcare bill possibly already next week and the future of Obamacare is not looking very bright. Debates are gonna be tense I think.

and that my friend would be the republicans fault....I think that is the dims plan in order to flip the blame off them they have to see to it NOTHING GOES THROUGH....that many people getting shit on could change an election

FACT: If the Republicans don't fix Obamacare there won't be any choice for millions and with premium increases again, millions more won't be able to afford it.

New York’s health insurers will request double-digit rate increases for ObamaCare policies for 2018 while debate rages in Washington on overhauling the law, analysts told The Post. New York health plans have requested double-digit rate hikes in each of the past three years.

Last Insurer in Delaware Requests Rate Hike of 33.6% For 2018

Highmark Blue Cross Blue Shield has requested a premium rate hike of 33.6 percent for 2018 to the Delaware Department of Insurance.

The state of Delaware has only two insurers participating on the exchanges this year and after Aetna announced in May that it will pull out of the Obamacare exchanges, Highmark will be the only insurer participating in the state in 2018.

NOT A PROBLEM, there were only 27,000 consumers in Delaware who purchased coverage through the marketplace.

CareFirst asked the Maryland Insurance Administration for average premium increases of 52 percent in 2018, far more than three other insurers on the exchange.

Chet Burell, president and CEO of CareFirst, acknowledged the proposed increases were large but said the carrier estimates it will have lost $600 million in the four years since it began selling plans under the law, known as Obamacare.

Anthem pulls out of ObamaCare exchanges in Midwest, fueling GOP repeal push

The nation’s second-largest health insurer announced Wednesday it plans to pull out of ObamaCare exchanges in Indiana and Wisconsin next year -- a move that fueled GOP calls on Capitol Hill to upend the law.

One Nation, Under Medicaid, With Misery and Poverty for All

In a recent study by the Kaiser Family Foundation, 24 states have a majority of births financed by Medicaid.

In other words, a majority of births in nearly half of our nation are born into poverty.

This is progress according to Progressives Socialists, the champions of big government and the architects of the disaster known as Obamacare.

So why would Socialists double down on a big government solution to a big government problem known as Obamacare? Simple. More dependency yields bigger bureaucracy. Bigger bureaucracy yields more wealth confiscation.

Wealth confiscation yields more poverty, and the vicious, Socialist experiment continues until there is equal misery and poverty for all—except for the politically-connected bourgeois.

Following in California’s Single Payer foot steps, the newly elected and appointed Socialists in Nevada passed “Medicaid for All.” According to Vox:

“Nevada, with little fanfare or notice, is inching toward a massive health insurance expansion — one that would give the state’s 2.8 million residents access to a public health insurance option.

The Nevada legislature passed a bill Friday that would allow anyone to buy into Medicaid, the public program that covers low-income Americans. It would be the first state to open the government-run program to all residents, regardless of their income or health status.”

Nevada Governor Sandoval, a moderate Republican, who championed and oversaw the largest tax increase in Nevada’s history, will have to decide by Friday, June 16th, if he will fix Obamacare and Medicaid by allowing all Nevadan residents (legal and illegal) to sign up for Medicaid!

By allowing this bill to become law, the next Kaiser study will have Nevada moving from sixth in the nation of Medicaid births to first! Progress!

Single payer healthcare system

Medicaid for All/Medicare for All is a revived plan to “fix” spiraling costs, coverage and access to healthcare. Yet, wasn’t Obamacare sold as the solution to these healthcare woes? Yes, but the sell of Obamacare relied on the stupidity of the American voter. Obamacare was sold to fix healthcare but was never designed to fix healthcare.

Obamacare was simply a political mechanism to create the bureaucracy and dependency needed to pave the way for the next Socialist leader to implement a single payer healthcare system. Who needs to rely on the stupidity of the American voter to pass a single payer system, when a near majority of states are breeding Medicaid dependents?

On the national level, Congresswoman Dina Titus (D-NV), and many other socialists, are trying to sell Medicare for All.

http://canadafreepress.com/article/one-nation-under-medicaid-with-misery-and-poverty-for-all?utm_source=newsletter&utm_medium=email&utm_campaign=jihadi_jane_lands_a_new_gig_kathy_griffin_to_entertain_isis&utm_term=2017-06-16

Oregon insurers request 17% average premium hike for 2018

Obamacare insurers in Oregon have submitted their rate requests for 2018 and those rates range from a 12% drop on some plans to a 66% increase on others. Charles Gaba at ACA signups calculates the weighted average of the requests is 17.2 percent.

Gaba also posts the letters various insurers submitted justifying their requests. Those letters contain an explanation of the factors driving the double-digit rate hikes. For instance, ATRIO opens it’s letter saying, “ATRIO’s 2016 premiums were insufficient to cover the cost of its claims, and, while the increase from 2016 to 2017 is expected to mitigate a portion of the shortfall, ATRIO believes that the calculated increase is necessary to achieve adequate rates in 2018.” In short, they lost money in 2016 and haven’t recovered.

Another Oregon insurer, BridgeSpan, has a similar justification. “The main driver of the rate change is the increasing cost of medical care,” their letter states. However, the letter also mentions another factor which Gaba highlights [emphasis his]:

“Another driver is the expectation that lower cost members are less likely to purchase coverage in 2018.”

Translation: We don’t expect HHS to actually enforce the individual mandate (or, at the very least, BridgeSpan is pretty sure that potential enrollees don’t think HHS will enforce the mandate, which amounts to the same thing…it doesn’t really matter whether they do enforce the mandate if enough people think they won’t).

These are rate requests, meaning that Oregon’s insurance commissioner will look them over and could push insurers to accept something lower before actual rates are announced.

The requested rates in Oregon are high but not as bad as those requested in a couple other states.

Earlier this month a large Obamacare insurer in Maryland requested a 59% premium increase for next year. The same insurer requested a 35% increase in Virginia. That insurer’s CEO, Chet Burrell, also described Obamacare as being in the first stages of a “death spiral.”

Connecticut has also released the rate requests it received from insurers and those averaged 24%, about the same as the national average last year.

http://hotair.com/archives/2017/05/16/oregon-insurers-request-17-increase-2018/?utm_source=hadaily&utm_medium=email&utm_campaign=nl

I'm sure you're right.

I think there will be more insurance companies dropping out for 2018.

Trump and team should just let Obummercare die.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |