News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

1) Nothing in your reply contradicts anything that I said. The company has no chance of being profitable based on selling products; the only way Drex can get any ROI (aside from his salary and prior "interest") is to sell it. Given they don't have any unencumbered physical assets and are saddled with unprofitable meh product, the distribution network looks like the only viable asset.

2) At no point did I mention AB - no clue where that tangent came from. Monster acquired CANarchy to be able to break into the beer brewing/distribution space, not AB.

The current world-wide energy drink market is roughly 60 billion a year with a CAGR of 7-9% per year.

1% of 60 billion is 600 million.

Not sure if this company can execute a business plan, but 1% seems achievable with a couple of Rockstar Execs. on board!

That is the most confused analysis I've ever read.

Firstly, MSLP "already" has an Amazon partnership (basically stocks Combat Crunch at Amazon distribution centers for drop shipment) so the recent PR is immaterial as Combat Crunch sales have declined to less than $4m annual through ALL SALES CHANNELS. These new liquid products will fail as well after the initial channel stuffing.

Secondly, Anheizer Busch went on a feeding frenzy of craft beer breweries. AB didn't acquire them because the small breweries HAD a significant distribution network but the exact opposite. To expand the small breweries distribution network and PROTECT current AB brands PRICING in a series of local markets. 95% of all beer on the grocery stores aisles are owned by just TWO companies and these companies acquire to simply protect price. This has nothing to do with MusclePharms product or markets or even business model.

As for the two former Rockstar employees, they were "let go" during the acquisition as they were non essential and brought nothing to the table.

With MSLP, they are on temporary independent contracts that I've shown will provide no value to shareholders as ANY and ALL sales they may be able to provide are subject to the onerous gross commission scale. Besides Ryan only pivoted to this in response to the complete fallout of capital raising and the fact his personal capital was depleted (see personal home property tax delinquent).

It's his Hail Mary and the amazing YOY decline in MSLP sales (now down over -70% since Ryan became CEO) is the exact OPPOSITE of what any acquirer would be looking for. Ryan's immense dilution and hence WW lawsuits have positioned those two parties to square off in bankruptcy court auction.

Between this and today's PR, it seems apparent that they are developing the distribution network as their primary product - not any of the actual consumables.

Drex's employment contracts have long been predicated on his ability to sell the company. They clearly can't run a profitable enterprise, and their product offerings are rehashes of the multitude of comparables already choking the marketplace. What they can do (with their crack team of former Moster execs) is build a stem-to-stern supply chain that could be leveraged by another company (with the resources and management to be successful) looking to break into a new market.

Ironically, Monster themselves did this by acquiring CANarchy Craft Brewery Collective in January, giving them instant access to the Western US microbrewery market. Be looking for the next 4loko any day now.

Tried the green apple this weekend ..pretty good! The wrap on the can looked nice, but needs a tad perfecting near the lip of the can.

Tried the green apple this weekend ..pretty good! The wrap on the can looked nice, but needs a tad perfecting near the lip of the can.

$MSLP MusclePharm Announces Third Quarter 2021 Financial Results

Press Release | 11/15/2021

Company Continues Focus on Controlling Operating Expenses with 21% Decline in Third Quarter 2021

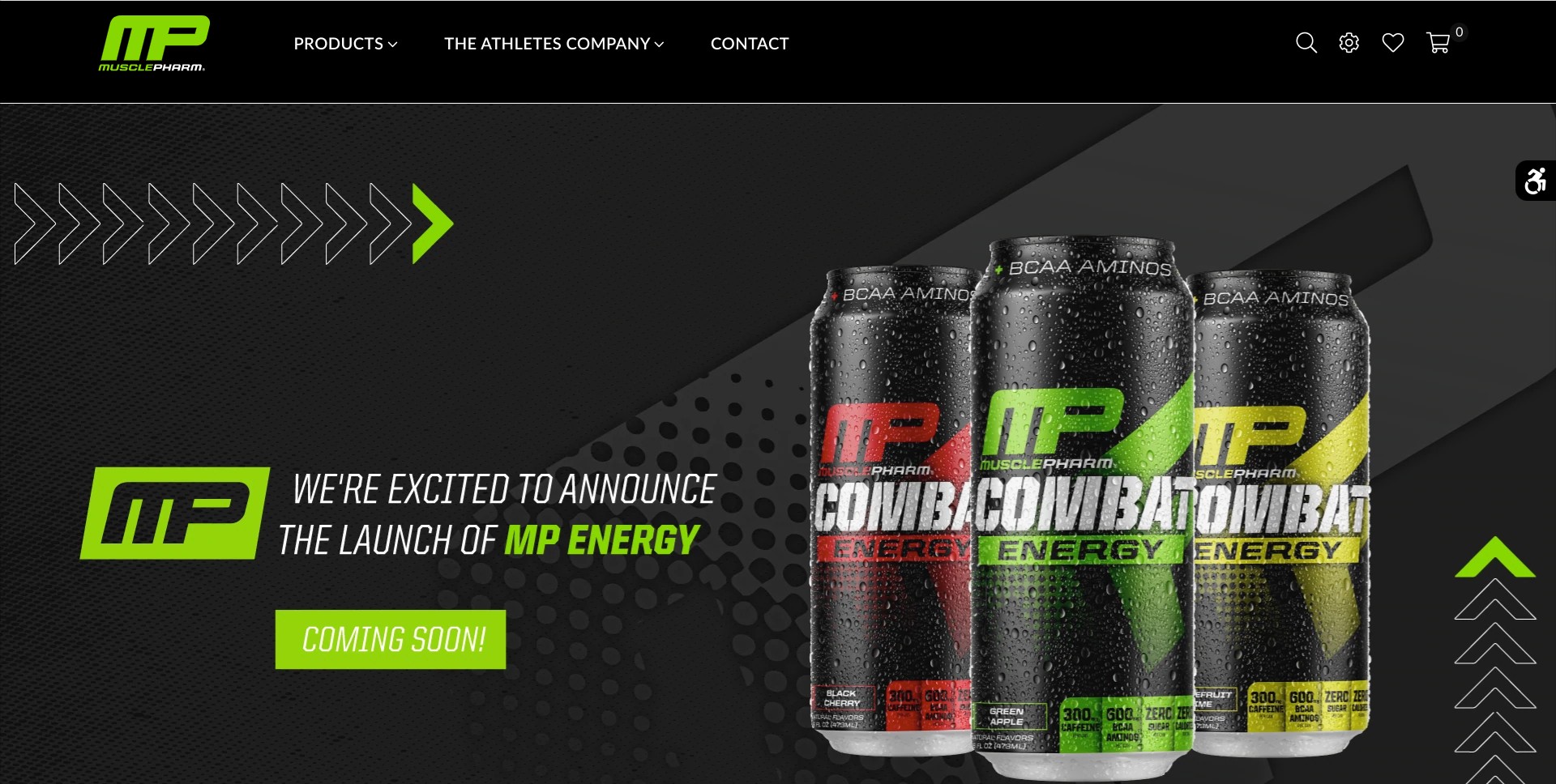

First Production Run of MP Combat Energy Successfully Sold 100%; $30 Million of Annual Sales Expected in 2023

Company Expects Sequential Revenue Growth in Fourth Quarter 2021 from

New Product Formulation and MP Energy Drink Line

LAS VEGAS, Nov. 15, 2021 (GLOBE NEWSWIRE) -- MusclePharm Corporation (OTCMKTS: MSLP), a global provider of leading sports nutrition & lifestyle branded nutritional supplements, today reported financial results for the third quarter and nine months ended September 30, 2021.

Mr. Ryan Drexler, the Chairman of the Board of Directors and Chief Executive Officer, stated, “Sales and margins in the third quarter were impacted by supply chain shortages which were mitigated by our continued focus on operating expense reduction. We are excited to launch a new and improved formula that delivers improved taste and mixability to consumers of two of our top selling products, Combat 100% Whey and Combat Protein Powder, to begin shipping this month. This new product formulation, along with the continued production of the MP Energy drink line, is expected to drive sequential revenue growth in the fourth quarter of 2021. Also, as mentioned on our second quarter earnings call, we brought on T.J. Dillashaw for marketing and business development and have already seen a significant impact on our business through the formation of marketing partnerships that will support our expected fourth quarter revenue growth.”

Mr. Drexler continued, “In addition, our recent $7.0 million senior secured notes offering has us well positioned to capture market share in the functional energy drink segment, and we believe we can grow the business to $30.0 million in annual sales starting in 2023.”

The following are key financial highlights for the period. Reconciliations of certain GAAP to non-GAAP measures are provided later in this press release.

Third Quarter 2021 Financial Highlights

? Revenue, net was $12.0 million.

? Gross margin was 0.2% due to increased protein and freight costs.

? Operating expenses were $3.5 million.

? Net loss was $(3.9) million.

? Loss per share was $(0.12).

? Adjusted EBITDA was $(2.8) million.

Nine-months ended September 30, 2021 Financial Highlights

? Revenue, net was $40.0 million.

? Gross margin was 14.7% due to increased protein and freight costs.

? Operating expenses were $10.8 million.

? Net loss was $(6.1) million.

? Loss per share was $(0.18).

? Adjusted EBITDA was $(3.6) million.

Non-GAAP Financial Measures

Within this press release, the Company refers to a non-GAAP financial measure (Adjusted EBITDA) which has a directly comparable U.S. GAAP financial measure (net (loss) income). EBITDA is defined as net (loss) income excluding interest, net, income taxes and depreciation and amortization. Adjusted EBITDA, in addition to those amounts included in EBITDA, is further adjusted for items such as stock-based compensation, gain on disposal of property and equipment, and (gain) loss on settlements.

Adjusted EBITDA is provided so that investors have the same financial data that management uses to assess the Company’s operating results with the belief that it will assist the investment community in properly assessing the ongoing performance of the Company for the periods being reported and future periods. The presentation of this additional information is not meant to be considered a substitute for measures prepared in accordance with U.S. GAAP.

Conference Call Information

The Company will host a conference call to discuss its operating results today at 1:30 pm Pacific Time (4:30 pm Eastern Time). Investors interested in accessing the live call can dial (800) 667-5216 from the U.S. and International callers can dial (303) 223-2688. A telephone replay will be available following the event and can be accessed by dialing (844) 512-2921 from the U.S. and International callers can dial (412) 317-6671; the conference ID is 21999197.

There will also be a simultaneous, live webcast with the ability to ask questions of management on the Investor Relations section of the Company’s website at www.musclepharm.com. The webcast will be archived for 30 days.

Forward-Looking Statements

This communication contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended, relating to our business and financial outlook, which are based on our current beliefs, assumptions, expectations, estimates, forecasts and projections. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “projects,” “intends,” “predicts,” “potential,” or “continue” or other comparable terminology. Such forward-looking statements only speak as of the date of this press release and the Company assumes no obligation to update the information included in this press release, except as required by law. Statements made in this press release that are forward-looking in nature may involve risks and uncertainties. Accordingly, readers are cautioned that any such forward-looking statements are not guarantees and are subject to certain risks, uncertainties and assumptions that are difficult to predict, including, without limitation, risks relating to consumer spending may decline or that U.S. and global macroeconomic conditions may worsen resulting in reduced demand for the Company’s products, risks relating to changes in consumer preferences away from the Company’s offerings, risks relating to the effectiveness and efficiency of the Company’s advertising campaigns and marketing expenditures, including existing brands and the launch of new brands, which may not result in increased revenue or generate sufficient levels of brand name and program awareness, risks if the Company becomes subject to health or advertising related claims from its customers, competitors or governmental and regulatory bodies, and risks relating to increased competition from other nutrition providers. As a result of these various risks, our actual outcomes and results may differ materially from those expressed in these forward-looking statements.

This list of risks, uncertainties and other factors is not complete. We discuss some of these matters more fully, as well as certain risk factors that could affect our business, financial condition, results of operations, and prospects, in our Annual Report on Form 10-K for the fiscal year ended December 31, 2020 and in subsequent reports we file from time-to-time with the SEC, which are available to read at www.sec.gov. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable as of the date made, expectations may prove to have been materially different from the results expressed or implied by such forward-looking statements. Unless otherwise required by law, the Company also disclaims any obligation to update its view of any such risks or uncertainties or to announce publicly the results of any revisions to the forward-looking statements made in this press release.

About MusclePharm Corporation

MusclePharm® is an award-winning, worldwide leading sports nutrition & lifestyle company offering branded nutritional supplements. Its portfolio of recognized properties include the MusclePharm® Sport Series, Essentials Series, and recently-launched Natural Series, as well as FitMiss™ – a product line designed specifically for female athletes. MusclePharm® products are available in more than 100 countries globally, with its Combat Protein product lineup being the company’s most popular.

Contact:

John Mills, Managing Partner

ICR, Inc.

646-277-1254

John.Mills@Icrinc.com

MusclePharm Corporation

Consolidated Statements of Operations

(In thousands, except share and per share data)

Three Months Ended Nine Months Ended

September 30, September 30,

2021 2020 2021 2020

Revenue, net $ 11,971 $ 16,085 $ 40,000 $ 49,309

Cost of revenue 11,942 11,073 34,102 34,504

Gross profit 29 5,012 5,898 14,805

Operating expenses:

General and administration 2,453 3,586 7,609 11,001

Selling and promotion 1,012 623 3,195 2,100

Impairment of intangible assets - 167 - 167

Total operating expenses 3,465 4,376 10,804 13,268

Income (loss) from operations (3,436) 636 (4,906) 1,537

Other (expense) income:

Loss on settlement obligation - - - (87)

Interest and other income (expense), net (465) (456) (1,144) (1,539)

Gain on settlement of payables - 518 - 518

Income (loss) before provision for income taxes (3,901) 698 (6,050) 429

Provision for income taxes 32 20 40 64

Net income (loss) $ (3,933) $ 678 $ (6,090) $ 365

Net income (loss) per share, basic $ (0.12) $ 0.02 $ (0.18) $ 0.01

Net income (loss) per share, diluted $ (0.12) $ 0.01 $ (0.18) $ 0.01

Weighted average shares used to compute net income (loss) per share, basic 33,386,200 33,008,189 33,134,933 32,746,147

Weighted average shares used to compute net income (loss) per share, diluted 33,386,200 49,097,595 33,134,933 48,835,553

MusclePharm Corporation

Consolidated Balance Sheets

(In thousands, except share and per share data)

September 30, December 31,

2021 2020

(Unaudited)

ASSETS

Current assets:

Cash $ 384 $ 2,003

Accounts receivable, net of allowances of $1,033 and $3,407 at September 30, 2021 and December 31, 2020, respectively 7,332 7,488

Inventory, net 1,589 1,032

Prepaid expenses and other current assets 1,538 1,341

Total current assets 10,843 11,864

Property and equipment, net 7 13

115 356

Operating lease right-of-use assets 271 474

Other assets 75 295

TOTAL ASSETS $ 11,311 $ 13,002

LIABILITIES AND STOCKHOLDERS’ DEFICIT

Current liabilities:

Obligation under secured borrowing arrangement $ 6,090 $ 7,098

Line of credit - 743

Operating lease liability, current 446 381

Convertible notes with a related party, net of discount 5,329 2,872

Accounts payable 18,770 14,719

Accrued and other liabilities 6,928 6,194

Total current liabilities 37,563 32,007

Operating lease liability, long-term - 343

Other long-term liabilities 3,561 5,071

Total liabilities 41,124 37,421

Commitments and contingencies (Note 9)

Stockholders’ deficit:

Common stock, par value of $0.001 per share; 100,000,000 shares authorized, 34,261,821 and 33,980,905 shares issued as of September 30, 2021 and December 31, 2020, respectively; 33,386,200 and 33,105,284 shares outstanding as of September 30, 2021 and December 31, 2020, respectively 32 32

Additional paid-in capital 178,955 178,261

Treasury stock, at cost; 875,621 shares (10,039) (10,039)

Accumulated deficit (198,761) (192,673)

TOTAL STOCKHOLDERS’ DEFICIT (29,813) (24,419)

TOTAL LIABILITIES AND STOCKHOLDERS’ DEFICIT $ 11,311 $ 13,002

MusclePharm Corporation

Consolidated Statements of Cash Flows

(In thousands, except share and per share data)

Nine Months Ended

September 30,

2021 2020

CASH FLOWS FROM OPERATING ACTIVITIES:

Net Income (loss) $ (6,090) $ 365

Adjustments to reconcile net loss to net cash (used in) provided by operating activities:

Depreciation and amortization of property and equipment 9 130

Amortization of intangible assets 240 240

Bad debt expense 326 174

Gain on disposal of property and equipment - (176)

Gain on settlement of payables - (518)

Inventory loss provision 1 (115)

Stock-based compensation 694 206

Issuance of common stock to non-employees - 116

Impairment of operating lease right-of-use assets - 167

Changes in operating assets and liabilities:

Accounts receivable, net (169) (572)

Inventory (557) 3,347

Prepaid expenses and other current assets (197) 36

ROU and other assets 423 429

Accounts payable and accrued liabilities 2,856 (1,259)

Net cash (used in) provided by operating activities (2,466) 2,570

CASH FLOWS FROM INVESTING ACTIVITIES:

Purchase of property and equipment (3) (4)

Proceeds from disposal of property and equipment - 220

Net cash (used in) provided by investing activities (3) 216

CASH FLOWS FROM FINANCING ACTIVITIES:

Repayment to line of credit (528) (2,452)

Payments from line of credit 2,192 -

Proceeds from secured borrowing arrangement, net of reserves 38,247 32,762

Payments to secured borrowing arrangement, net of fees (39,255) (34,289)

Proceeds from shareholder's loan 49 -

Proceeds from issuance of Paycheck Protection Program Loan - 965

Repayment of finance lease obligations - (54)

Proceeds of notes payable 145

Repayment of Notes payables - (165)

Net cash (used in) provided by financing activities 850 (3,233)

NET CHANGE IN CASH (1,619) (447)

CASH — BEGINNING OF PERIOD 2,003 1,532

CASH — END OF PERIOD $ 384 $ 1,085

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION:

Cash paid for Interest $ 1,153 $ 522

Non-GAAP Adjusted EBITDA

In addition to disclosing financial results calculated in accordance with U.S. GAAP, this press release discloses Adjusted EBITDA, which is net loss adjusted for stock-based compensation, gain on disposal of property and equipment, (gain) loss on settlements, interest and other expense, net, depreciation of property and equipment, amortization of intangible assets, impairment of operating lease right of use asset and provision for income taxes.

Management uses Adjusted EBITDA as a supplement to U.S. GAAP measures to further evaluate period-to-period operating performance, as well as the Company’s ability to meet future working capital requirements. The exclusion of non-cash charges, including stock-based compensation, gain on disposal of property and equipment, depreciation of property and equipment, amortization of intangible assets, and provision for income taxes, is useful in measuring the Company’s cash available for operations and performance of the Company. Management believes these non-GAAP measures will provide investors with important additional perspectives in evaluating the Company’s ongoing business performance.

The U.S. GAAP measure most directly comparable to Adjusted EBITDA is net income (loss). The non-GAAP financial measure of Adjusted EBITDA should not be considered as an alternative to net income (loss). Adjusted EBITDA is not a presentation made in accordance with GAAP and has important limitations as an analytical tool and should not be considered in isolation or as a substitute for analysis of our results as reported under GAAP. Because Adjusted EBITDA excludes some, but not all, items that affect net income (loss) and is defined differently by different companies, our definition of Adjusted EBITDA may not be comparable to similarly titled measures of other companies.

Set forth below are reconciliations of our reported GAAP net loss to Adjusted EBITDA (in thousands):

For the For the For the For the

Three Months ended Three Months Nine Months ended Nine Months ended

30-Sep-21 30-Sep-20 30-Sep-21 30-Sep-20

Net Income (Loss) $ (3,933) $ 678 $ (6,090) $ 365

Non-GAAP adjustments:

Stock-based compensation 386 27 694 206

Gain on disposal of property and equipment - (165) - (176)

(Gain) loss on settlements (94) (518) (265) (518)

Interest expense 683 632 1,800 1,715

Depreciation of property and equipment 3 24 9 130

Amortization of intangible assets 80 80 240 240

Impairment of operating lease right of use asset - 167 - 167

Provision for income taxes 32 20 39 64

Adjusted EBITDA $ (2,843) $ 945 $ (3,573) $ 2,193

The Q3 Highlights

Total Revenue: $11.97m

Cost of Goods Sold: $11.94m

Before any operating expenses, MSLP is selling its product for the same price it pays from suppliers.

Considering Amazon channel is retail money, MSLP actually wholesales it's product to Costco and such at a LOSS before any actual expense except Cost of Goods from its suppliers (who are being stiffed for payment)

Total Revenue declined -25.5% most recent Q compared to Q3 last year.

Q3 2020 revs $16.1m

Q3 2021 revs $11.9m

Declines are accelerating.

Remember when CEO Brad posted $52m in rev in a SINGLE QUARTER? CEO Ryan is posting less than that number for the ENTIRE YEAR!! Easy math. CEO RYAN -75%.

Here are the headline metrics from Q2 to Q3

Balance sheet

Total Assets: Q2 $10.9m Q3 $11.3 So an increase of $400k but

Total Liabilities: Q2 $37.2m Q3 $41.1m

Liabilities exploded $4m the past 90 days despite Assets essentially flat.

MSLP suppliers were stiffed an additional $2m NET this Q over Q2. Mind you this $2m is in ADDITION to the stiffing suffered last Q by suppliers.

Additional net borrowings of nearly $2m from the shylocks at 25%-200% interest this Q as well.

MSLP lost -$4m the past 90 days on just $11.9m in Total Sales.

Metrics must be horrific

for MSLP to not file the required 10-Q for Q3.

I'm certain more suppliers were stiffed, more shylock debt taken on and the continuation of the fraud but Ryan can't figure out a way to massage it without not reporting until the Q4 "Senior Debt Offering" (haha) can obscure the facts that occurred in Q3. Simple Ponzi activity

Wow!! Just from the call as the 10q is not filed yet.

Cost of Goods Sold (COGS) before any expenses is 99.8% of Total Revenue. That is what happens when your suppliers cut you off for non-payment.

Another -$4m loss.

Total Revenues are down to $12m so MSLP is losing $.33 cents for every $1.00 in sales even AFTER slashing any bricks and mortar business location, distribution channel, massive payroll layoffs, selling every asset down to the paperclips.

HYPE the new product while not discussing they have given away 17.5% commissions each to TWO former Rockstar employees. That is 35% commission on the gross margin in addition to $20,000 a month salaries to each as well with no minimum sale requirements. I won't mention the 3m shares awarded to the two as that is just piling on.

Trust fund babies in business pretending in Hollywood.

Oh, I almost forgot....hiring TJ Dillashaw the Drug Cheat coming off a 2 year USADA suspension has been hired to the do the marketing for MSLP. That is even worse than MSLP hired Michael Vick the dog killer as in an endorsement deal right as that tragedy was occurring. What a train wreck.

$MSLP MusclePharm to Announce Third Quarter 2021 Financial Results on Monday, November 15, 2021

Press Release | 11/10/2021

CALABASAS, Calif., Nov. 10, 2021 (GLOBE NEWSWIRE) -- MusclePharm Corporation (OTCMKTS: MSLP), a global provider of leading sports nutrition and lifestyle branded nutritional supplements, announced today that the Company will report its financial results for the third quarter ended September 30, 2021, after the market closes on Monday, November 15, 2021.

The Company will host a conference call to discuss its operating results on Monday, November 15, 2021, at 1:30 pm Pacific Time (4:30 pm Eastern Time). Investors interested in accessing the live call can dial (800) 667-5216 from the U.S. and International callers can dial (303) 223-2688. A telephone replay will be available following the event and can be accessed by dialing (844) 512-2921 from the U.S. and International callers can dial (412) 317-6671; the conference ID is 21999197.

There will also be a simultaneous, live webcast with the ability to ask questions available on the Investor Relations section of the Company’s website at www.musclepharm.com. The webcast will be archived for 30 days.

About MusclePharm Corporation

MusclePharm® is an award-winning, worldwide leading sports nutrition and lifestyle company offering branded nutritional supplements. Its portfolio of recognized properties include the MusclePharm® Sport Series, Essentials Series, and recently-launched Natural Series, as well as FitMiss™ – a product line designed specifically for female athletes. MusclePharm® products are available in more than 100 countries globally, with its Combat Protein product lineup being the company’s most popular.

Contact:

John Mills, Managing Partner

ICR, Inc.

646-277-1254

John.Mills@icrinc.com

Took 'em a few days, but it looks like they got it back up and running.

$MSLP MusclePharm adds former Rockstar Energy executive to MP beverage team to lead product development and marketing for two new Performance Energy drinks

Press Release | 10/29/2021

CALABASAS, Calif., Oct. 29, 2021 (GLOBE NEWSWIRE) -- MusclePharm Corporation (OTCMKTS: MSLP), a global provider of leading sports nutrition and lifestyle branded nutritional supplements, today announced a partnership with former Rockstar Energy executive, Jason May. Mr. May will join the MP beverage team currently headed up by Joey Cannata, another long time Rockstar Energy veteran. The MP beverage team will be launching two fully functional energy drink lines, MP Combat Energy and FitMiss Energy, and Mr. May will be responsible for building out the national marketing strategy for both lines. MP Combat Energy will launch in the fall of 2021 in three flavors: Grapefruit Lime, Green Apple and Black Cherry and FitMiss Energy will launch in early 2022, also with three flavors.

Mr. Ryan Drexler, the Chairman of the Board and Chief Executive Officer of MusclePharm, stated, “We have an incredible beverage team of top industry veterans, now strengthened with the addition of Mr. May, and are very confident their arsenal of expertise will be instrumental in our ability to succeed in the energy category. We have received over $1.0 million in pre-production sales for MP Combat Energy and are excited to bring this incredible product to the market beginning this fall, followed by our FitMiss line early next year.”

Mr. Drexler continued, “I’m confident that this will be the ultimate partnership as we work to fully leverage MusclePharm’s legacy brand heritage with our MP beverage team’s industry contacts, and I know these first three energy flavors are only the beginning of an exciting new venture. Over the next twelve months our goal is to cement our position in this every-growing category by expanding our product line with the introduction of additional SKUs. As we move forward, and as MusclePharm’s growth continues to attract great talent, I passionately believe we’ll see that we are just scratching the surface of MusclePharm’s true potential.”

“As a marketer I cannot think of a stronger brand than MusclePharm in Sports and Fitness better positioned to enter, and succeed, in the energy category. MusclePharm’s leading brand position and deep roots in nutrition channel distribution provides MP Combat Energy a clear and decisive winning proposition,” stated Mr. May. “I very much look forward to working with the MP beverage team, led by Mr. Cannata, to roll out top shelf product offerings backed by world class initiatives in digital, experiential, and channel marketing. Mr. Cannata and I have a long and successful history and I consider myself fortunate to have the opportunity to work closely with him again. When you combine Mr. Cannata’s distribution contacts and pedigree with my marketing and product development expertise you have a winning combination and the makings for a very successful beverage venture.”

Forward-Looking Statements

This communication contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended, relating to our business and financial outlook, which are based on our current beliefs, assumptions, expectations, estimates, forecasts and projections. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “projects,” “intends,” “predicts,” “potential,” or “continue” or other comparable terminology. Such forward-looking statements only speak as of the date of this press release and the Company assumes no obligation to update the information included in this press release. Statements made in this press release that are forward-looking in nature may involve risks and uncertainties. Accordingly, readers are cautioned that any such forward-looking statements are not guarantees and are subject to certain risks, uncertainties and assumptions that are difficult to predict, including, without limitation, risks relating to consumer spending may decline or that U.S. and global macroeconomic conditions may worsen resulting in reduced demand for the Company’s products, risks relating to changes in consumer preferences away from the Company’s offerings, risks relating to the effectiveness and efficiency of the Company’s advertising campaigns and marketing expenditures, including existing brands and the launch of new brands, which may not result in increased revenue or generate sufficient levels of brand name and program awareness, risks if the Company becomes subject to health or advertising related claims from its customers, competitors or governmental and regulatory bodies, and risks relating to increased competition from other nutrition providers. As a result of these various risks, our actual outcomes and results may differ materially from those expressed in these forward-looking statements.

This list of risks, uncertainties and other factors is not complete. We discuss some of these matters more fully, as well as certain risk factors that could affect our business, financial condition, results of operations, and prospects, in reports we file from time-to-time with the SEC, which are available to read at www.sec.gov. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable as of the date made, expectations may prove to have been materially different from the results expressed or implied by such forward-looking statements. Unless otherwise required by law, the Company also disclaims any obligation to update its view of any such risks or uncertainties or to announce publicly the results of any revisions to the forward-looking statements made in this press release.

About MusclePharm, Inc.

MusclePharm® is an award-winning, worldwide leading sports nutrition and lifestyle company offering branded nutritional supplements. Its portfolio of recognized properties includes the MusclePharm® Sport Series, Essentials Series, and recently-launched Natural Series, as well as FitMiss™–a product line designed specifically for female athletes. MusclePharm® products are available in more than 100 countries globally, with its Combat Protein product lineup being the company’s most popular.

Contact:

John Mills, Managing Partner

ICR, Inc.

646-277-1254

John.Mills@icrinc.com

Yeah......

Ryan had to decide where to the allocate few funds available due to stiffing all the suppliers (who have now cut him off). Either a haircut for himself or renewing the $20 Godaddy URL.

Since he will be looking for a new job soon, the haircut was probably the most pragmatic decision.

http://www.musclepharmcorp.com (their "investor relations" site) is down.

sounds about right...

Conversion price is fixed (for 5 years) regardless of all the yada yada yada you are attempting to assess to this specific financing vehicle. Do the math and you get a ~400% APR on this 180 day deal. I didn't read all the terms nor did you as they have not been released. I don't need to as I know what these deals are and what they were designed to accomplish by the financier.

This entire Soprano's style street money deal shows you exactly desperate Ryan is as all his suppliers are cutting him off for non-payment. MSLP owes over $30m in overdue invoices and can't get inventory.

All the hard assets have been sold and all the Accounts Receivable have been sold via Crossroads and Prestige at their 25% shylock rate.

This "energy drink" thing is just a desperate "pivot" like a gambler who has lost everything at the table is borrowing street money for a "Hail Mary" even the though the vig is too exorbitant to ever recover.

When does Joe C sue for his unpaid 17.5% gross commission if any significant cans ever sell which they won't. Joe knows this and is why he was able to leverage Ryan's desperation into a $20k a month SALARY deal that has no minimum sales requirements on Joe's part.

MSLP's only viable sales channel is the Protein Powder tubs at Costco and that is why sales have fallen over -70% under his "grand plan" and lack of any funds/willing suppliers to take credit are prohibiting him from filling this channel.

One thing I'm unclear on with this scenario: how can the warrants be used to cover a squeeze? The PR notes specifically that they were issued as 'restricted warrants' - thus if converted, they would yield restricted shares. Given that the holding period for removing the legend doesn't start until consideration has been rendered, they would retain the restriction for at least 6 mos. after conversion.

Thanks for the correction on the term (I just gave it a cursory glance and now the APR is ~400% cost of the funds), but.....

the stock is FREE based on the strategy I posted previously. The warrants never need to be converted to profit on 14m shares of stock warrants using a short strategy and are protected against any short squeeze by triggering the conversion if that highly unlikely event occurs.

This financing arrangement is proof that a position has already taken place and there are a minimum of 14m shares to play with....all on the downside hence the recent -75% slide in equity price the preceeded this "Press Release".

Thanks for the correction on the term (I just gave it a cursory glance), but.....

the stock is FREE based on the strategy I posted previously. The warrants never need to be converted to profit on 14m shares of stock warrants using a short strategy and are protected against any short squeeze by triggering the conversion if that highly unlikely event occurs.

This financing arrangement is proof that a position has already taken place and there are a minimum of 14m shares to play with....all on the downside hence the recent -75% slide in equity price the preceeded this "Press Release".

Agreed that this note is pretty horrible...even worse - the term is only 6 months:

The principal amount of the Notes will be due on April 13, 2022.

Each warrant entitles the holder to purchase one share of common stock at an initial exercise price of $0.78 for a period of five years from the date of issuance

and for the naive

The 14m warrants are the kiss of death in these instances, just like what proceeded GNC's bankruptcy.

GNC was still profitable but had expiring bonds that needed to either be rolled over by existing financiers or new bond issue before the expiration date on the old bonds. If I remember correctly the old bonds had an 8% interest rate (compared to MSLP's 29.9% interest rate).

The existing (convertible) bond holders refused to extend the maturity date and forced the company into bankruptcy despite $2B in revenue and bottom line profit.

Why did they do this? Defies logic, no?

Because bond holders near always protect their investment by shorting the stock in which they hold convertible bonds.

Do the math.

GNC was trading at $30 for instance when you become a convertible bond holder. Short it at $30 and any downward price is profit. If the stock skyrockets or experiences a short squeeze, you are completely protected by the conversion price, therefore you have the bonus equity supply to cover your short. BTW, that never happens. Nearly every instance of the equity goes to ZERO as these junk shylock financing arrangements are to allow the insiders and others to liquidate off the radar in dark pools or other arrangements.

Don't forget (as SLC recently posted), tomorrow is the day Ryan's convertible price is set on the ~$3m emergency injection required when MSLP ran out of cash when all the suppliers cut him off and sued him.

AND DON"T OVERLOOK the fact that in Ryan's latest 29.9% "financing" deal that is actually a ~200% cost, the financier required HALF of the 29.9% statutory interest payment UPFRONT even though it is only a 365 day term. Wow.

Can't get a credit card Ryan?

MSLP just "borrowed" $7m and has to pay a $1.15m placement "fee" for the borrowings AND 14% interest due in 365 days AND 17.3m free "shares". So essentially MSLP just borrowed 12 months worth of money for ~29% interest (intentionally structured as the statutory limit of the land) and additionally $13m worth of free stock to lender.

That is over 200% APR interest for just 365 days!!!!!!

Pure crazy. That is worse than any payday loan company would offer.

NutraBlend, who "was" MSLP's largest supplier officially cut Ryan off from any more purchases as he stiffed them again even after the pre trail settlement.

With the cost of funds to operate at over 200% interest before any "real" operating expenses or commissions, how does MSLP make a profit?

GEEZE..WHY DID ALL THE NEWBIES LEAVE? HEE!-HAW!

Desperate? lolzzzzzzzz

Nice short! You’re obviously very proud! Wall Street is next for you.

NO ONE GIVES A CHIT! LOLZZZZZZZZ

thanks for the thoughts...

A few interesting notes about Drex's most recent Form 4:

1) Although the $2,457,549 note was nominally converted 08/13/2021 - squarely in the middle of a flurry of PRs about all of the "good" stuff that was happening - the Form 4 wasn't filed until 08/17/2021. There has been only one PR fluff piece since then, and Madcow went to great lengths to point out how illusory that news was.

2) The Conversion stipulates that the price will be determined on 10/15/2021 - two full months after the deal was done (while the Company was trading in the $1.40-1.50 range).

3) Since 08/13/2021, MSLP PPS has fallen by nearly 50%, and continues to drop on a near daily basis. As noted, the Company has been dead silent during much of that time.

Now, I'm not blaming Drex - it is entirely possible (likely) that there is simply no good news to report.

However, a cynic might say that continued silence by the company while PPS drops like a stone benefits him more than anyone else (save maybe Madcow, who is as dedicated of a short as I have ever seen). Wouldn't it be an amazing coincidence if there was suddenly a report of wonderful news (early report of a profitable quarter, major deal closed, maybe a potential buyer) on 10/16/2021?

Ouch.......maybe see a doctor about that drip, drip............

Sorry you lost money again!!!!!!! lolzzzzzzzzzzzzzzzzzz

Drip drip drip...down she goes...where she stops nobody knows!

Now let's look at track record.

MSLP did $177m in annual rev under CEO Pyatt.

MSLP now does ~$50m world wide under CEO Ryan and domestic sales have fallen to $9m a Q or ~$36m annual run rate and still falling.

Every "great new deal" under Ryan has fallen through and failed.

Remember Combat Crunch and natural/organic line in every Krogers and Sprouts?

Thud.....

Remember the Natural/Organic Line period? That was supposed to be a $1B product by now.

Thud.....

There is nary a mention any more. I haven't heard a single peep anywhere of the MSLP organic plant based line that they hyped by hiring "rockstar" influencers and experts poached from successful corporations. Remember the Frito Lay exec?

Thud.....

Costco is basically the only sales channel that MSLP has and accounts for over 50% of sales and that is basically the big tub of protein powder which is the most saturated and margin sensitive product in the sector unless you are Optimum Nutrition who owns the entire supply chain including the whey.

Costco was Brad's baby that Ryan inherited and the only line Ryan hasn't run completely into the ground despite the huge sales declines at Costco too under Ryan.

Remember the entire GNC Wall Display that was going to drive the stock to $100 a share (these words are quotes from the same posters here that are now hyping the energy line)?

Thud......

Fitmiss?

Thud......

Energy Sport and Energy Sport Zero? They were going to be Gatorade killers remember?

Thud.....

And also.....

Joe C is not a salesman. He simply had connections with a few local independent beverage distributors.

This is no guarantee there will be any sales much less $30m on a product with no customers and targeting women in the supplement energy business.

I don't see too many women drinking Rock'star'. They are at 'Star'bucks tho!!!!

Joe made a few telephone calls and a local distributor in Denver agreed to carry a product when MSLP gets one but in no way guaranteed any sales.

This is the extent of the MSLP and Joe C joint venture that has guaranteed Joe a salary of over $500,000 (guaranteed $20,000 month salary already being paid) over the contract and 17.5% of the gross margin before any expenses other than cost of product from supplier.

All this for Joe to make a few phone calls to former associates of a handful of local specialized bev distributors.

Don't forget that Joe C was also awarded ~1m shares in a stock option grant too!

Sorry shareholders.

Who is going to manufacture the MSLP energy drink? Ryan can't even pay his current product suppliers and has re-stiffed his largest supplier even after the settlement pretrial.

MSLP is out of cash and sold every liquid asset they ever had on the books. They are now borrowing $1m every few weeks at 25% interest rate just to pay a few of the bills.

Ryan can't even afford to loan the company $1m as he is broke. He couldn't even pay his residential property tax on own house until well after the due date.

Now Ryan is forced to borrow $1m at 25% from the Shylocks.

Wouldn't a credit card even be a better deal for shareholders?

This is a joke.

Just assume there are any sales. Let's do some simple math.

$1m in sales and COGS is say .65 cents = $350,000 gross margin

Out of that $350k, Joe gets 17.5% or $61,250

That leaves $288K and the Shylocks get 25% interest on the whole $1m because Ryan has to pay Joe upfront and we still haven't calculated the business costs.

Interest expense is $250,000. That leaves.....

......$38K left on every $1m in sales. Now subtract Joe's $20k a month salary.

We are already in the red and haven't applied a single business expense yet.

We have calculated ZERO other expenses other than cost from manufacturer, Joe's cut off the top and the interest on the purchase order capital.

There is no scaling cost potential as the costs above are fixed to every dollar invested in the product.

But you forgot the kicker....

Ryan has already begun paying his Energy drink guy Joe C a salary of $20k a month right now AND Joe gets 17.5% off the gross margin before any expenses of every dollar of MSLP energy drink sold. Sounds like a great deal for Joe, but what about MSLP and its shareholders? Looks completely desperate as Joe doesn't have to sell a single can and makes over $500,000 in compensation for himself and then gets 17.5% of gross margin on every can sold.

Joe C knows the energy drink sector is completely saturated and he said the market he is targeting is for women.

Remember FitMiss?

That went over like a fart in church.

MSLP has been in the energy drink business since 2014. Has it overtaken Gatorade yet like many contributors here said would happen then?

$1MM in pre-orders, expecting to hit $30MM in 2023. Drex is betting heavily on the energy drinks...

https://www.musclepharmcorp.com/prviewer/release_only/id/4837040

How many Quarters of these declines before Revenues hit ZERO?

YOY Quarterly Revenue (sales) have fallen over -33%.

Quarterly Sales fell -$4.5m Year over Year ($13.5m crumbles to barely $9m in most recent Q)

With only $9m in Quarterly Sales generated in Q2 (and declines in freefall, you do the math. - another $4.5m and so on doesn't leave much from $9m.

The Sales decline percentage is exploding even using Ryan historical standards of -20% declines YOY since his appointment as CEO. Now sales are off -$33% and freefalling at nearly double the rate.

Now consider there is ZERO cash on hand and over $37m in Accounts Payable Due. Ryan is borrowing a million dollars every couple weeks on a 180 day term from prestige at an APR of ~25%. These new loans began in June and are occurring every few weeks and even disclosed continuing in August. Now several million has been borrowed that this 25% APR.

YES....you read that correctly. After you calculate the 15% interest and the accommodation fee of 1-2% and the stock grants to the shylock lender you get an APR of ~25% total cost of borrowing now additional millions of cash in $1m increments every few weeks from Prestige so the bank account is not overdrawn.

With Sales crashing and debt service exploding at now %25 APR recent cost of desperation funding, how much longer before the inevitable?

The White Winston case where the judge ordered Ryan to disclose in discovery certain MSLP financial documents and initially fined Ryan $1,500 for refusing, subsequently ordered a new deadline for disclosure and was not impressed by Ryan refusing to submit the financial documents again!

Is Ryan afraid of criminal liability? Fraud!!!

The judge this time ordered Ryan to pay White Winston's to date legal fees in just this one of the cases which amounts to ~$100,000 and that payment was required immediately.

Maybe Ryan can challenge his future cell mate in another rigged BJJ match like his past performance with Magny if things keep playing out they way they look like.

And don't look now...

Nutrablend who sued MSLP for Million$ of unpaid invoices and Ryan settled right before trial calling for 3 years of 6 figure a month payments and a minimum monthly purchase order has been stiffed again.

Personally I don't feel sorry for Nutrablend. Just look at what happened to Capstone when they were stiffed for over $10m!!!!!!

Nutrablend clearly never read the Scorpion and Turtle Folktale or if they did should have listened to Trump when he said if you owe the bank $3m they own you; if you owe the bank $3b you own them.

Q3 is off to a roaring success /s

How desperate is Ryan personally for money? Clearly Ryan is tapped out as a lucrative 15% annual interest ($75,000) and a 1% "accomodation fee" (another easy $10,000) and nearly 20,000 "free shares (another ~$40,000) is too rich for his blood for a 6 month loan. 180 days is too far out for Ryan remaining assets or lackthereof.

Ryan can't dig $1,000,000 out of his sofa to get back $1,125,000 in 180 days?

The tax assessor on Ryan's residence found out Ryan is not all that liquid any longer.

Direct quotes from the Q2 '21 10Q

On July 26, 2021, Prestige advanced the Company $1 million with a six month term and a 15% interest rate. In addition, there was an accommodation fee equal to 1% of the amount advanced plus 18,750 stock options.

As a result of our history of losses and financial condition, there is substantial doubt about our ability to continue as a going concern.

Just like I said......

$8m in "shylock" borrowings this Q just to stay afloat and Assets declined by another -$3m. Prestige and Crossroads (the shylock lenders) now hold almost 100% of the value of the Asset side of the Accounting Balance Sheet!!!!!!!

There are now ZERO unattached Assets (hocked them all to the shylocks) left and over $30m of Accounts Payable still on the books!!!!!!!!!

No cash on hand. More fake accounting by not paying bills due before the Q2 cutoff in order to not show a negative balance. Stiffing more suppliers.

Want proof? Sales declined significantly and Accounts Payable went up significantly! Ponzi scheme 101

Revenue (Sales) continues to decline to new low despite Q1 and Q2 historically being the strongest Qs of the year.

Down another ~15% just this Q over last Q (not year over year but every 90 days declining!!!!!!)

The lawsuit against MSLP by White Winston is not going well for Ryan despite his fraudulent attempt to transfer 875K shares of treasury stock to a broker dealer for this fake window dressing trading unless he is using his own shares for this purpose to dupe unsophisticated fanboy investors.

At least Ryan was able to beg, borrow or steal enough capital to pay his severely delinquent property tax bill before they foreclosed on his personal residence. Ryan is continuing to use MSLP as his personal piggy bank at the expense of shareholders and suppliers.

Multimillion dollar annual salary and stock awards are surely earned by vitamin boy whose daddy's trust fund baby's only credit is "Pimp; A Story of My Life"

Not kidding....just look https://www.imdb.com/name/nm3573940/

Says the guy who magically appears and starts slamming the company.

Yikes........nasty MMs all over the place shorting.....lolzzzz

SLC

You repeated exactly what I wrote earlier. There was no reason for the IRS to dismiss the charges against the company in order to maintain potential leverage the IRS could use to compel MSLP corporate to cooperate against the actual targets but since the targets are all in settlement negotiations including asset forfeiture, the IRS allowed the SOL to run out. It is akin to locking up a compelling witness until the actual targets or defendants are convicted.

But back to the real corporate fraud. MSLP has still not paid Millions$ of past due AP or legal judgements including nearly all of its suppliers, $1.7m+ to Thermolife, $1m+ to Manchester City FC, etc....and in the face of continuing revenue decline that will render satisfaction impossible. MSLP's own fraudulent financials show another YOY -20% decline in revs currently.

MSLP annual revs pre Drexler were $180m

MSLP current annual revs are ~$50m and have never declined LESS than -20% YOY since Drexler took over.

$MSLP MusclePharm Closes Potential $7.3 Million Liability with IRS

Press Release | 07/26/2021

CALABASAS, Calif., July 26, 2021 (GLOBE NEWSWIRE) -- On April 6, 2016, the Internal Revenue Service (“IRS”) selected MusclePharm Corporation’s (OTCMKTS: MSLP) 2014 Federal Income Tax Return for audit and, as a result, proposed certain adjustments with respect to the tax reporting of certain of the Company’s former executives’ 2014 restricted stock grants. On April 4, 2017, MusclePharm received a letter from the IRS asserting back taxes and penalties of approximately $7.3 million dollars owed for the 2014 restricted stock grants. MusclePharm submitted a formal protest disputing the matter on several grounds and has been pursuing this matter vigorously through the IRS appeals process. On June 29, 2021, an IRS Appeals Officer confirmed that the tax matter had exceeded the applicable statute of limitations and was deemed closed from any further assessment by the IRS.

About MusclePharm Corporation

MusclePharm® is an award-winning, worldwide leading sports nutrition & lifestyle company offering branded nutritional supplements. Its portfolio of recognized properties include the MusclePharm® Sport Series, Essentials Series, and recently-launched Natural Series, as well as FitMiss™ – a product line designed specifically for female athletes. MusclePharm® products are available in more than 100 countries globally, with its Combat Protein product lineup being the company’s most popular.

Contact:

John Mills, Managing Partner

ICR, Inc.

646-277-1254

John.Mills@Icrinc.com

It's really not a matter of the IRS "allowing" the corp to escape liability due to the SOL; it's a statutory requirement. More likely is that the IRS chose to pursue the individual cases and allow the SOL to expire WRT the corp.

YIKES!... Pretty nasty stuff... thanks for the update!

If you are not aware of what of just a fraction of the allegations were:

MSLP officers (mostly Brad Pyatt) secretly leased a private jet for personal use somewhere around $100k a month.

Brad and others jettisoned to 5 diamond resorts in Cabo San Lucas, Mexico and other locales booking suites costing $1,000s a night and playing golf with greens fees of $300 and $400 a round, countless spa treatments in addition to purchased things such as premium golf club sets, Louis Vuitton luggage sets, expensive jewelry, Cash ATM withdrawals for 10s of thousands of dollars at a time that the proceeds were never disclosed, etc....all for themselves personally yet paid with corporate funds in addition to the unreported and secret stock options.

There were private country club memberships that had 5 or 6 figure initiation fees in addition to the monthly dues.

That just scratched the surface of the personal piggy bank mentality that still exists at MSLP.

This is what initiated the IRS audit. The IRS is currently in active proceedings targeting Pyatt and et al and recent disclosures have stated all the targets are currently in settlement discussions thus MSLP release.

Nothing logical dealing with a SKANK of a CEO here.....lolzzzzzzzzzz

|

Followers

|

357

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

80868

|

|

Created

|

02/02/10

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |