News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

KFG Resources Ltd Q1 2015 Results(Ending July 31st 2015)

Overall it was a pretty good quarter for KFG despite the circumstances. Oil prices down 50% year over year, historic flooding that caused some wells to shut off for 45-60 of the 90 days(See end of June news release). As well, expenses increased because of new staff and new equipment needed for damaged wells, plus a few other things.

- Cash increased almost $100k

- Liabilities went down $75K

- Company made a profit even with half of the revenue from last year

- New leases in Texas signed with wells to drill before year end

- More Mississippi wells to drill

Price: $0.08

Common Shares: 50,584,144

Options/Warrants: 0

Insider Holdings: 16%

Financials

ASSETS

Cash: $1,499,459 (last quarter was $1,401,025)

Accounts Receivable: $291,245

Prepaid Expenses: $12,856

Reclamation Bond: $20,000

Property & Equipment: $932,204

Total Assets: $2,755,764

LIABILITIES

Accounts payable: $453,535

Decommissioning Liability: $243,311

Total Liabilities: $696,846 (last quarter was $765,590)

Sales

Revenue: $506,423( last year this time was $904,409)

Production: 75bopd (same as last year due to shut wells because of flooding)

Productive wells: 23 compared to 21 in 2014

Net Income: $14,563

MD&A Highlights

The Company drilled two wells in February 2015 but they were not on production until late May and June 2015. The Company has sufficient cash reserves to finance its activities for the remainder of its fiscal year. Two new wells being completed in late September 2015 should add cash flow and help lower the overall cost of production. The Company plans to participate in the drilling of two new shallow wells in north central Texas before year end, marking KFG’s entry into Texas.

Revenue from the sale of oil and gas was $395,052 for three months ended July 31, 2015, compared to $788,143 for the three months ended July 31, 2014. The decrease in revenue is a result of a price collapse in oil from $102.40/bbl to $55.33/bbl.

Management fee revenue for the three months ended July 31, 2015 was $111,371 as compared to $116,266 for the three months ended July 31, 2014. The results are comparable between periods.

Lease operating expenses were $115,515 for the three months ended July 31, 2015 compared to $79,144 for the three months ended July 31, 2014. The increase in lease operating expenses is a result of putting two wells back on production that have been shut in because of the wet weather.

General and administrative expenses for three months ended July 31, 2015 were $278,985 compared to $267,460 for the three months ended July 31, 2014. The main increase in costs is a result of hiring new staff.

Liquidity and Capital Resources

The Company’s main sources of liquidity are internally-generated cash flow from its oil and gas operations. Because KFG’s internally-generated cash flow is presently sufficient to fund its overall operating expenses, the Company will not require additional funding from equity capital markets.

KFG had cash at July 31, 2015 of $ 1,499,459. Although oil prices have collapsed, the Company, through the first fiscal quarter ended July 31, 2015, continues to generate positive cash flow. Two recent wells should help continue the trend. The Company will continue to manage its cash resources and will complete its current drilling program. In addition, the Company is increasing its inventory of projects seeking longer term leases.

Outlook

The Company’s cash position going forward will be able to finance all projects internally for the remainder of its fiscal year ending April 30, 2016. Two new wells should help the Company maintain a positive cash position. At this writing, two additional wells are planned in Mississippi this calendar year and one developmental well, weather permitting in Mississippi, as well as shallow wells in north Texas.

KFG logs, core nine feet of oil sand at Third Wilcox

2015-09-23 12:12 MT - News Release

Mr. Robert Kadane reports

KFG REOPENS PRODUCTION AT SPRINGFIELD

KFG Resources Ltd.'s subsidiary, KFG Petroleum Corp., has logged and cored nine feet of oil sand from 4,393 feet to 4,402 feet in the Third Wilcox sand. Production casing has been cemented to 4,600 feet. KFG has a 13-per-cent working interest in the well, the Stockfelt unit No. 1, reverting to a 20.25-per-cent working interest at payout. The company will report initial production tests when available.

KFG's previously announced Drouet Pool Estate well in Franklin county, Mississippi, is being completed at present, and a report on initial production should be available next week. Also, KFG has staked location for its Barnum No. 4 well in Adams county, Mississippi and will be moving in a rig to drill the well to 6,800 feet in approximately three weeks.

© 2015 Canjex Publishing Ltd. All rights reserved.

KFG drills 10 ft of McShane oil sand in Mississippi

2015-09-14 13:45 MT - News Release

Mr. Robert Kadane reports

KFG LOGS NEW FIELD DISCOVERY WELL

KFG Resources Ltd. has logged a new discovery oil well in Franklin county, Mississippi. The company's subsidiary, KFG Petroleum Corp. of Natchez, Miss., drilled the Drouet Poole Estate No. 1 well to a total depth of 6,800 feet and found 10 feet of McShane oil sand from 6,618 feet to 6,628 feet. Production casing has been set for a completion attempt. The company has a 12-per-cent working interest in the well before payout and a 24-per-cent working interest after payout.

In addition, the company is moving in to drill its Second Creek prospect in Adams county, Mississippi. The Stockfelt unit No. 1 will be drilled to a depth of 4,600 feet to test the Third Wilcox formation. KFG has a 15-per-cent working interest in the well, jumping to a 21.5-per-cent working interest at payout. At this writing, it is anticipated that two more wells will be drilled in the program, and those projects will be announced at a later date.

© 2015 Canjex Publishing Ltd. All rights reserved.

KFG Year End Results Ending April 30th 2015

Current Price: $0.08

Common Shares: 50,584,144

Options/Warrants: 0

Insider Holdings: 16%

Before reading the financial results and management discussions below, one must take into consideration that KFG had quite a good year considering the three major setbacks that occurred. Oil production, cash, and management fee's are all up year over year, but the write down of oil assets which every single petroleum company had to do made KFG show a small net loss of less than $100,000. Without the $800,000 write down, KFG would of ended the year with positive net income. Despite this, drilling will move forward next month even at these lower prices, and with several wells to do, odds of production increasing are quite good.

Three Setbacks this year:

1) Price of oil which went from $110 to $40 and this is Louisiana Light Sweet Crude

2) Historic flooding in Mississippi which stopped some production and added extra costs

3) Several wild cat wells were dry which not only increased expenses, it added no value

4) KFG's best well Craig 5 did not start pumping until after the fourth quarter ended

Financial Results Ending April 30th 2015

**My Note: All numbers are in US dollars and therefore should be converted to reflect the proper value in Canadian dollars. For example, KFG's cash position of $1.4 million USD is actually worth $1.85 million Canadian dollars as of August 28th 2015. This is essential to do considering the company is listed on a Canadian exchange.**

Producing Wells - 25 (22 in 2014)

Barrels of oil per day average - 96.02 bopd (71.79bopd in 2014) - 25% increase

Average sell price - $46.41 ($101.75 in 2014) - Down by $55.34 or 54%

*Operating cost per barrel average is $18.85 before G&A costs*

*KFG sells it's oil at LLS(Louisiana Light Sweet) pricing which is similar to Brent*

ASSETS

Cash: $1,401,025 - (2014 $1,205,750)

Accounts Receivable: $482,880

Prepaid Expenses: $13,274

Reclamation bond: $20,000

Property and Equipment: $901,766

Total Assets: $2,818,945 - (2014 $3,017,302)

LIABILITIES

Accounts Payable: 527,848

Deposits : $3,988

Decommissioning Liability: $233,754

Total Liabilities: $765,590 - (2014 $879,582)

Assets decreased year over year, but so did Liabilities.

Sales

Oil and Gas - $2,278,425 - (2014 $2,240,754)

Management Fee's - 466,674 - (2014 $419,014)

Total Sales - $2,745,099 - (2014 $2,659,768)

Total - -$84,365 - (2014 $67,467)

Revenue year over year slightly higher due to production increase by a substantial amount. However, selling oil at $46 average in 2015 compared to $101 average in 2015 made a big difference.

Expenses( 2015 - 2014)

Automotive: $96,914 - 71,902 - Increased by $25,012

Bad Debt - 0 - $2,372 - Decreased by $2,372

Depletion - $807,733 - $408,559 - Increased by $399,174 (Write down)

Dry hole & Abandonment - $118,889 - $168,065 - Decreased by $49,176

Exchange Loss - $772 - $4,802 - Decreased by $4,030

Insurance - $114,937 - $106,896 - Increased by $8,041

Lease Operations - $615,761 - $758,738 Decreased by $142,977

Office & Misc - $296,145 - $275,720 Increased by $20,425

Rent - $19,602 - $18,633 Increased by $969

Salaries & Benefits - $758,711 - $776,614 Decreased by $17,903

If you exclude the write down, remaining expenses went down $162,551 year over year. Unfortunately, every petroleum company must write down assets and take it as an expense/loss.

Management Discussion Highlights

Summary of Quarterly Results

The main difference in the last two quarters ended January 31, 2015 and April 30, 2015 were slumping oil prices in the January 31, 2015 quarter and increased depletion and amortization changes because of reserve depletions resulting from increased production, directly affecting earnings.

Liquidity and Capital Resources

The Company’s main sources of liquidity are internally-generated cash flow from its oil and gas operations. Because KFG’s internally-generated cash flow is presently sufficient to fund its overall operating expenses, the Company will not require additional funding from equity capital markets in order to execute on its business strategy for at least the next twelve months. A decline in the prices of natural gas and oil could materially and adversely impact on KFG’s ability to secure partners in drilling projects, with the result that the Company may be forced to scale back its operational activities.

KFG had cash at April 30, 2015 of $1,401,025. Oil production at Fayette is providing positive cash flow and will continue. Also the Company’s new oil revenues will provide a borrowing base in addition to the Fayette development. As of now, the Company plans to expand as cash flow permits. The Company is already experiencing new production from the Craig #5 well and all wells are back on line. During the period January 2015 – April 2015, the Company experienced bad weather and weak pricing. Two wells were drilled in February 2015, but not put on production until May 2015 because of the weather. Also the Craig #2 well and the MacNeil wells have not lined up with expectations.

Fourth Quarter

The quarter ended April 30, 2015 experienced prices at multi-year lows and wells of production that couldn’t be put back on in a timely manner. All wells are producing now but prices have reduced to the low $40 range from $60 in May, June and July 2015.

Outlook

Production at Fayette is stable and has started a slow decline. With the Dale lease back on production and new production coming off the Craig and Parker leases, KFG will have adequate internal cash flow to develop existing leases as well as support several new prospects in the coming months. Unless the price of oil collapses, the Company will generate sufficient capital to fund its requirements throughout 2016 internally.

**My Second Note: The directors Stephen Guido and Robert Kadane might not have large share positions, but they do own interests in several current and future wells. They were paid for this over 2015 and therefore it is in their best interest to make sure that every project is successful for KFG. They are paying for these wells at their own risk.**

From financials:

Included in accounts receivable from co-owners is $18,204 (2014 - $nil) due from Geronimo Corporation, a company controlled by G. Stephen Guido, an officer and Director of the Company and $19,562 (2014 - $nil) from Robert Kadane, Director and officer of the Company.

2015-08-05 12:22 MT - News Release

Mr. Robert Kadane reports

KFG OPERATIONS UPDATE

KFG Resources Ltd.'s drilling program is on hold because of high water above flood stage in the Mississippi River which affects large areas of land -- sometimes many miles away from the river. This circumstance is unprecedented in the last 75 years. The company's program will commence when conditions permit.

The company's production is stable and cash flow was positive during the first quarter of its fiscal year ending July 31, 2015. The company's Barnum No. 3 well in Adams county, Mississippi, has proved to be non-commercial and is producing 10 barrels of oil per day.

As of this date, the company has three new projects and one development well ready to drill. Two additional projects are being assembled. All projects are in Mississippi.

© 2015 Canjex Publishing Ltd. All rights reserved.

Massive insider buying on KFG: https://www.insidertracking.com/company?menu_tickersearch=KFG%2ACA%20%7C%7C%20KFG%20Resources

There's only 50,584,144 common shares with no options or warrants.

Haney, Kevin

Insider's Relationship to Issuer as Filed with Regulator: 3 - 10% Security Holder of Issuer

TransactionDate Transaction Nature # or value acquiredor disposed of Price AccountBalance

Security Type: Common Shares (Direct Ownership)

Jul 17/15 10 - Acquisition in the public market 16,000 $0.095 6,000,000

Jul 17/15 10 - Acquisition in the public market 20,000 $0.090 5,984,000

Jul 17/15 10 - Acquisition in the public market 2,000 $0.085 5,964,000

Jul 14/15 10 - Acquisition in the public market 2,500 $0.090 5,962,000

Jul 6/15 10 - Acquisition in the public market 3,000 $0.100 5,959,500

Jun 29/15 10 - Acquisition in the public market 10,000 $0.090 5,929,500

Jul 6/15 10 - Acquisition in the public market 10,000 $0.085 5,956,500

Jul 6/15 10 - Acquisition in the public market 17,000 $0.080 5,946,500

May 27/15 10 - Disposition in the public market -71,500 $0.100 5,919,500

Apr 23/15 10 - Acquisition in the public market 1,500 $0.110 5,991,000

Apr 23/15 10 - Acquisition in the public market 1,000 $0.105 5,989,500

Apr 22/15 10 - Acquisition in the public market 500 $0.090 5,988,500

Apr 22/15 10 - Acquisition in the public market 2,000 $0.085 5,988,000

Apr 2/15 10 - Acquisition in the public market 1,000 $0.100 5,986,000

Apr 2/15 10 - Acquisition in the public market 5,000 $0.090 5,985,000

Mar 26/15 10 - Acquisition in the public market 5,000 $0.080 5,980,000

Mar 24/15 10 - Acquisition in the public market 2,500 $0.080 5,975,000

Mar 20/15 10 - Acquisition in the public market 5,000 $0.085 5,972,500

Mar 13/15 10 - Acquisition in the public market 7,500 $0.080 5,967,500

Mar 11/15 10 - Acquisition in the public market 5,000 $0.085 5,960,000

Mar 5/15 10 - Acquisition in the public market 2,000 $0.080 5,955,000

Mar 5/15 10 - Acquisition in the public market 13,000 $0.090 5,953,000

Mar 4/15 10 - Acquisition in the public market 10,000 $0.090 5,940,000

Feb 27/15 10 - Acquisition in the public market 5,000 $0.080 5,930,000

Feb 12/15 10 - Acquisition in the public market 3,000 $0.105 5,925,000

Feb 12/15 10 - Acquisition in the public market 2,000 $0.100 5,922,000

Feb 10/15 10 - Acquisition in the public market 5,000 $0.105 5,920,000

Feb 9/15 10 - Acquisition in the public market 5,000 $0.105 5,915,000

Feb 5/15 10 - Acquisition in the public market 5,000 $0.105 5,910,000

Feb 2/15 10 - Acquisition in the public market 1,000 $0.125 5,905,000

Feb 2/15 10 - Acquisition in the public market 4,000 $0.120 5,904,000

Feb 2/15 10 - Acquisition in the public market 2,000 $0.125 5,900,000

Feb 1/15 10 - Acquisition in the public market 23,000 $0.120 5,883,000

Feb 2/15 10 - Acquisition in the public market 15,000 $0.110 5,898,000

Jan 30/15 10 - Acquisition in the public market 9,000 $0.095 5,860,000

Jan 30/15 11 - Acquisition carried out privately 1,000 $0.090 5,851,000

Jan 28/15 10 - Acquisition in the public market 5,000 $0.095 5,850,000

Jan 21/15 10 - Acquisition in the public market 5,000 $0.090 5,845,000

Jan 20/15 10 - Acquisition in the public market 10,000 $0.090 5,840,000

See more at: https://www.insidertracking.com/company?menu_tickersearch=KFG%2ACA%20%7C%7C%20KFG%20Resources#sthash.tetB2xlO.dpuf

KFG Financial Comparison Chart (Audited Annual Financials From 2008 to 2015)

I made this financial comparison show everyone where KFG is after years of gains and setbacks. It's been a long journey, but after much trial and error, this company has finally found the best way to grow itself. Despite low oil prices and weather trying to stop the company, this just won't happen. KFG is now a self sufficient oil junior and is more than capable of doubling or tripling its production on a yearly basis. This will inevitably increase revenue, cash position and net income which could lead to a dividend, share buyback or even takeover of the company. Please see below for a break down of every Audited Year End financial report.

KFG Year End Results in 2008

- Cash: $2.66M, Total Assets: $2.96M, Total Debt: $553K

- Revenue: $798K, Net Loss For The Year: -$64K

- Shares Outstanding: 30,874,646

- This was before the global crisis. KFG was trading around $0.15c and still raising money. Total was 25 million shares which is half of the entire O/S right now and a major cash injection. However this was done at a lower price.

KFG Year End Results in 2009

- Cash:$1.62M, Total Assets: $2.33M, Total Debt: $156K

- Revenue: $645K, Net Loss For The Year: $456K

- Shares Outstanding: 42,147,311

- Additional Funds Raised

KFG Year End Results in 2010

- Cash: $304K, Total Assets: $1.84M, Total Debt: $640K

- Revenue: $997K, Net Loss For The Year: -$1.4M

- Shares Outstanding: 47,786,580

- Additional Funds Raised

KFG Year End Results in 2011

- Cash: $1.03M, Total Assets: $2.94M, Total Debt: $834K

- Revenue: $2.9M, Net Income For The Year: $832K

- Shares Outstanding: 50,480,644

- This was a milestone year because KFG hit a string of wells(Fayette) that helped them recover from the financial crisis. Some assets were also sold and funds raised as well. The stock went back to the teen price range this year.

- Additional Funds Raised.

KFG Year End Results in 2012

- Cash: $637K, Total Assets: $2.43M, Total Debt: $439K

- Revenue: $3.5M, Net Loss For The Year: $144K

- Shares Outstanding: 50,559,191

- Despite the record profit, KFG took a major risk this year and unfortunately lost. Drilling a 100% interest Tuscaloosa well which cost the company over $1 million USD and it did not work out. This is why KFG’s strategy changed from solo wells to JV wells in multiple areas.

KFG Year End Results in 2013

- Cash: 861K, Total Assets: $2.5M, Total Debt: $430K

- Revenue: $3.05M, Net Income For The Year: $76K

- Shares Outstanding: 50,584,144(Some shares cancelled and this is the current share structure.

- This was the year where KFG started to diversify into multiple wells rather than just rely on the 9 Fayette and do a couple 100% interest wells.

KFG Year end Results in 2014

- Cash: $1.21M, Total Assets: $3.02M, Total Debt: $880K

- Revenue: $2.7M, Net Income For The Year: $67K

- Shares Outstanding: 50,584,144

- The reason why revenue went down this quarter was due to the fact that the 9 Fayette wells paid out from 75% to 59%, along with additional costs from doing other wells. However, new production was put in place to replace the lost paid out production from Fayette.

- Debt increase is based strictly on deposits from partners, not bank or payables.

KFG Results after 9 months in 2015

- Cash: $2.134M, Total Assets: $3.7M, Tot Debt: $1.07M

- Revenue: $2.27M, Net Income After 9 Months: $493K

- Shares Outstanding: 50,584,144

- If the price of oil didn’t drop 60% and weather didn’t hamper KFG’s operations (as stated in their last news release), net income would be close to $1 million USD right now. Regardless, this has not stopped KFG’s growth plans. Five to seven wells have been announced for the summer drill campaign and the company can only go forward from here.

News: KFG to drill 5-7 wells this summer

KFG Resources restarts production at all wells

2015-06-29 11:33 MT - News Release

Mr. Robert Kadane reports

KFG OPERATIONS UPDATE

KFG Resources Ltd.'s subsidiary KFG Petroleum Corp.'s Craig No. 5 well, which was put on production in May, 2015, in Adams county, Mississippi, continues to produce 100 barrels of oil per day water free. The company has a 21.5-per-cent (16.025-per-cent net) interest in the well. The Barnum No. 3 well is still undergoing production testing, although results to date are disappointing. KFG's interest in the Barnum well is 9 per cent (6.75 per cent net).

The price of crude oil in May was $60.50, bringing all production back into positive territory. All production is finally back on-line after the wettest five months in memory. A few wells were down periodically in KFG's fiscal third quarter ending Jan. 31, 2015, and in the company's last fiscal quarter ending April 30, 2015. The last well that was down is back on production this week. Weather conditions made it extremely hard to get wells back on-line in a timely fashion.

The company's drilling program should be under way in about 30 days. It is anticipated, at present, that there will be five exploratory wells, and one or two development wells in the program.

© 2015 Canjex Publishing Ltd. All rights reserved.

New article on KFG Resources from PennyStockExperts:

http://pennystockexperts.com/attractive-smart-and-relatively-wealthy-oil-operator-seeks-your-attention/

Attractive, Smart, and Relatively Wealthy Oil Operator Seeks Your Attention

Let’s face it, mainstream financial media has trained investors to think shale plays like Bakken, Eagle Ford, Marcellus et al. are the only game in town.

Now I’m no T. Boone Pickens, but I know they’re ignoring more than a few proven oil fields.

Disregarding conventional projects in favor of shale could continue to be a costly mistake for investors and operators alike moving forward.

Like a moth to a flame…

After harnessing the power of horizontal drilling, the oil industry was drawn toward hydraulic fracturing and shale like a moth to a flame. As a whole, it abandoned conventional shallow prospects, historically its bread and butter, and flew directly toward the orange yellowish glow of this newer (dare I say sexier) more controversial technique.

Easy money leads to oversupply.

Thanks to an era of easy money and $100 per barrel pricing, banks, brokers, and their clients lent to just about anyone willing to borrow. Therefore, oil operators took the money. And I guess they had to, those fancy horizontal wells don’t come cheap, each one can cost over $10 million.

As you can imagine… the bills start adding up quickly.

Thousands of wells would never have been drilled if cash from operating activities were the only funds available. Levering up ruled the day! Even sub-par outfits were able to borrow, borrow, and borrow some more, betting they could pay back lenders after oil prices continued rising.

Long story short, drilling successes contributed to an oversupplied market (we’ll save the other factoids for another day), and lots of bettors got it wrong. Nearly all shale projects need at least $60 WTI to break even, some would argue much higher, so many oil companies are now facing a life and death situation.

If we break the industry down into three groups, here’s my interpretation:

1) Those who got burned flying too close to the orange yellowish glow [bankrupt]

2) Those who levered up and are forced to run faster to stay ahead of debt collectors [borderline delinquent]

3) Those who operated during the boom expecting a bust someday [healthy, strong, and control destiny]

Which of the three would you be attracted to?

Simplicity is back in fashion.

With enough time, what’s old always seems to become new again. Conservative, conventional operators like KFG Resources (CVE: KFG) (OTCMKTS: KFGRF) and its CEO Robert A. Kadane now look like the smartest guys in the room. Bob, as he prefers to be called, has first-hand experience spanning forty years. As a youngster he watched, learned, and then helped his dad manage a small fleet of drilling rigs back when oil was 40 cents a barrel. Maybe you’ve heard or know about guys who run around in Armani suits calling themselves “oil man”? You’ll see them more frequently during the boom times

… well that’s not Bob!

Granted, marketing and promotion aren’t his strong points, just look at KFG’s website. Rough around the edges, maybe, but Bob understands the oil business and knows how to run a tight ship, and that’s most important for KFG’s long-term success. Looking for proof of concept? Prime Energy (NASDAQ: PNRG) is a $135 million dollar exchange listed company Bob built and ultimately sold before starting his next venture… KFG Resources.

KFG controls its own destiny…

With help from his team, including G. Stephen Guido of Shamrock Drilling, Bob and KFG Resources have time to think wisely and make strategic moves aimed at creating shareholder value. Unlike many of its peers, whom are weighed down by debt or already bankrupt, KFG Resources controls its own destiny.

While the industry was chasing the latest and greatest shale play(s), bidding up prices, KFG Resources stayed true to what it knows best, low-cost high return conventional opportunities, primarily in Mississippi and Louisiana.

Hold it… “Low cost high return”? Isn’t that what everyone is looking for, the kind of deal you only hear about from pitchmen, too good to be true type stuff.

Well, yes and no, please stay with me.

Hitting it where they ain’t!

To use a baseball analogy: drilling one of those fancy $10 million dollar horizontal wells into the Eagle Ford or Bakken is equivalent to swinging for the fence. You either hit a homerun or strikeout, there isn’t much room in between, success or failure.

Hitting homeruns are great! But the oil business can be less forgiving than MLB when it comes to strikeouts. Therefore, every winning baseball team (or portfolio of oil assets) needs players who get on base 30-40% of the time, and keep dry holes (strikeouts) to a minimum.

Occasionally, KFG Resources will hit a homerun, like it did recently with Craig #5, this well paid back its initial investment in just 8 weeks! But singles and doubles are also in its game plan. Inevitably, dry holes will and have occurred, but with drilling costs under $350,000 (less than 4% of a horizontal), KFG Resources should always be able to take another swing at its best geological targets.

I can assure you, Wall Street and Bay Street are overlooking KFG Resources because of its small stature, but to me that’s part of its appeal. In my experience, independent investors improve their odds of success and make more money by hitting it where the professional analysts aren’t— then selling to them at a premium later.

Bottom Line: With proved crude oil reserves of 247 million barrels, as of Dec. 2010, Mississippi exhibits strong potential for the development of oil and gas reserves. KFG Resources manages risk by working with loyal partners who co-invest; it maintains a 10%-59% interest in 26 producing wells. Additionally, it earns monthly revenue per well as operator and servicer. Finally, the metrics work, Craig #5 cost approximately $300,000 to complete, so for $65k (KFG’s 21% stake) it added 20 barrels of oil per day>>> roughly $438,000 in annual revenue at $60 per barrel>>> for KFG’s $65,000 investment! Obviously, that discovery wouldn’t move the needle for Exxon Mobil, but it’s a homerun for KFG, and with any luck it expects to hit a few more like Craig #5 this summer.

*Disclosure: author is establishing a long position in KFG Resources

KFG's Craig No. 5 well flows 98 bopd

2015-04-27 13:36 MT - News Release

Mr. Robert Kadane reports

KFG OPERATIONS UPDATE

KFG Resources Ltd.'s subsidiary, KFG Petroleum Corp., and its partners have completed the Craig No. 5 well in Adams county, Mississippi, flowing 98 barrels of oil per day, no water, on an eight-64th choke, with flowing tubing pressure of 300 pounds per square inch. The company has a 21.5-per-cent working interest in the well. Barnum No. 3 completion operations are under way. Additionally KFG is gearing up for an active summer in Mississippi with several new projects.

© 2015 Canjex Publishing Ltd. All rights reserved.

Last quarter KFG was producing at 105bopd. Including this well, the company will be closer to 130bopd since their declines are almost non-existent. Barnum 3 should add some good production, Craig 3 pays out in June, and the next several wells should give KFG the potential to double it's last quarter production numbers.

New Institution buying KFG Resources. http://dearbornpartners.com/ based out of Chicago. See the breakdown below:

Ownership - Summary : KFG Resources LtdMost Recent

Macro: Energy Free Float: 42,372,902 Filing Status:

Current Period - 14.29 %

Mid: Energy Free Float % O/S: 84% 31-Mar-2015 - 28.57 %

Micro: Oil & Gas (Exploration & Production) Shares Outstanding: 50,584,144 31-Dec-2014 - 0.00 %

Ticker: KFG-V Exchange: TSX Venture Exchange Market Cap ($MM): 3501631.000000

Investor Type

Investor Type Investors % O/S Pos Val ($MM)

Investment Managers 1 0.44 225,000 0.02

Brokerage Firms 0 0.00 0 0.00

Strategic Entities 6 16.23 8,211,242 0.59

Holding Companies 0 0.00 0 0.00

Corporations 0 0.00 0 0.00

Individuals 6 16.23 8,211,242 0.59

Government Agency 0 0.00 0 0.00

Total - All Holders 7 16.68 8,436,242 0.61

Insider Filings (As Reported)

Insider 5 16.39 8,290,900 0.00

Investor Style

Investor Style Investors % O/S Pos Val ($MM)

Core Growth 1 0.44 225,000 0.02

Location:Metro Area

Location Investors % O/S Pos Val ($MM)

Chicago & Suburbs 1 0.44 225,000 0.02

Location:Global Region

Location Investors % O/S Pos Val ($MM)

N. America 7 16.68 8,436,242 0.61

Location:Country

Location Investors % O/S Pos Val ($MM)

Canada 3 11.94 6,041,000 0.48

United States 4 4.74 2,395,242 0.13

Rotation

Rotation Investors % O/S Pos Val ($MM)

Buys 2 12.28 6,211,000 0.49

Buy-Ins 1 0.44 225,000 0.02

Position Increase 1 11.83 5,986,000 0.48

Sells 1 2.00 1,009,502 0.07

Sell-Outs 0 0.00 0 0.00

Position Decrease 1 2.00 1,009,502 0.07

No Change 4 2.40 1,215,740 0.04

Turnover

Turnover Percentage

High 0.00

Mod 0.00

Low 14.27

Concentration

Concentration

Percentage

All 16.68

Top Ten Investors

Investor Name % O/S Pos Pos Chg % Pos Chg Filing Date Filing Type Equity Assets ($MM) Investor Type Country

Haney (Kevin) 11.83 5,986,000 6,000 0.10 02-Apr-2015 Canadian Insider Data 0.49 Strategic Entities Canada

Guido (G Stephen) 2.01 1,018,740 0 0.00 16-Aug-2013 Proxy-CA 0.03 Strategic Entities United States

Kadane (Robert Andrews) 2.00 1,009,502 -50,000 -4.72 20-Feb-2015 Canadian Insider Data 0.07 Strategic Entities United States

Dearborn Partners L.L.C. 0.44 225,000 225,000 100.00 31-Mar-2015 13F 1,147.57 Investment Managers United States

Kadane (Elizabeth Jean) 0.28 142,000 0 0.00 16-Aug-2013 Proxy-CA 0.00 Strategic Entities United States

Raftery (Michael P) 0.09 45,000 0 0.00 16-Aug-2013 Proxy-CA 0.00 Strategic Entities Canada

Pople (Keith N) 0.02 10,000 0 0.00 16-Aug-2013 Proxy-CA 0.00 Strategic Entities Canada

Source: Thomson Financial

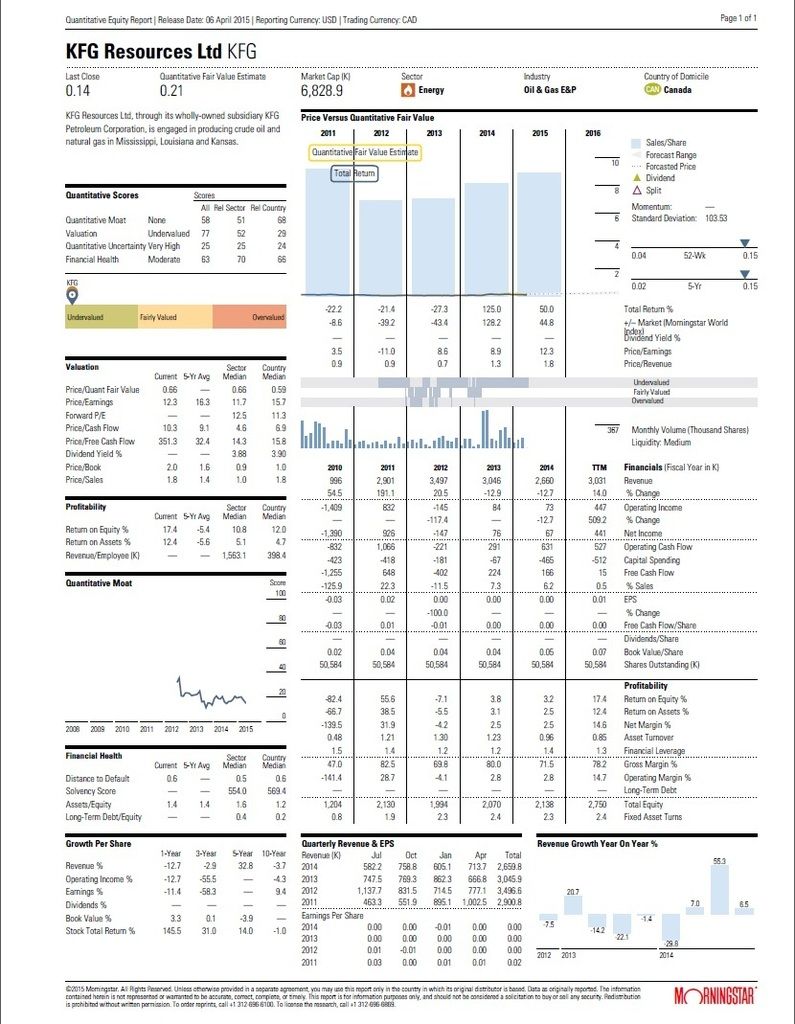

Morningstar Report: KFG Fair Value $0.21c

KFG Q3 Results Ending January 31st 2015

Note: All numbers are in US Dollars which means there should be a 20% conversion to accommodate the TSXV listed security.

Price: $0.075

Common Shares: 50,584,144

Insider Holdings: 17% or just over 8.5 million shares as per SEDI

Assets

Cash: $2,133,800 (Q2 Cash: $1,836,298) (Q1 Cash: $1,133,429) – almost 100% increase from Q1 to Q3

Accounts Receivable: $238,843

Prepaid Expenses: $39,428

Reclamation bond: $20,000

Property and Equipment: $1,250,967

Total Assets: $3,693,038

Liabilities

Accounts Payable: $464,480

Deposits from co-owners: $598,351

Total Liabilities: $1,062,831

Revenue After 9 Months

Oil and Gas: $1,938,528

Management Fee’s: $330,010

Net Income: $492,487

EPS: $0.01

My Note: Even though revenue went down due to the 50% decline in oil prices, KFG was still able to add cash to the company treasury and continue drilling despite 3 dry wells back to back. Without the two events, earnings would have been much higher for the quarter. As well, with every new producing well KFG puts online, management fee revenue will also increase on a monthly basis.

MD&A Highlights

For the nine months ended January 31, 2015, the Company had cash flow from oil and gas production of $1,469,120, compared to $1,116,992 for the nine months ended January 31, 2014. Oil production increased from 77.51 BOPD to 105.06 BOPD, and gas production decreased 1.19 MCF per day. The average price of gas increased $0.38 per MCF and the average price of crude oil decreased $15.05 per bbl when comparing the nine months ended January 31, 2015 and January 31, 2014.

Overall, the Company has recovered from giving up 25% of its interested in the Fayette Field wells at payout. Currently, with the MacNeil wells and Craig wells at payout, revenues are on a growth pattern again. The Company was able to grow just utilizing cash flow. Several new projects are in the pipeline and the Craig #3 well will payout in the next few months, increasing that revenue stream. KFG will have no problems financing growth through its internal cash flow throughout the remainder of its fiscal year ending April 30, 2015. In addition, the Barnum #2 well is on production as of mid September 2014. The Craig #4 well was recently completed as a dryhole. With the Company’s current cash position, the Company is in a good position to weather the current collapse in oil prices from about $84 in October 2014 to around $55 - $60/bbl at this writing and will still show positive cashflow. The Company’s operating cost per bbl is currently $18.85/bbl. Currently, the Company has two wells awaiting completion drilled in February 2015 – both in Adams county. The Barnum #3 well encountered the main field zone in the Parker sand at 6,400’. The Company has a 9% working interest in the well converting to a 20.55% working interest at payout. The Craig #5 well encountered the main pay zone at 1,300’ and an additional oil zone at 10,214’. The Company has a 21.5% working interest in this well. With $2,133,800 in cash, the Company is well positioned to weather the current price collapse in crude oil. KFG has a current ratio of 2.27 to 1.

During the quarter ended January 31, 2015, the Company saw a major price collapse in the price of crude oil resulting in revenues of $446,746 compared to the prior quarter’s revenue in excess of $800,000. Greatly lower costs during the period allowed the Company to limit its losses compared to the corresponding quarter ending January 31, 2014. With its cash position and lack of debt, the Company is well positioned and is not planning to cut back its exploration and development.

The Company’s main sources of liquidity are internally-generated cash flow from its oil and gas operations. Because KFG’s internally-generated cash flow is presently sufficient to fund its overall operating expenses, the Company will not require additional funding from equity capital markets in order to execute on its business strategy. A decline in the prices of natural gas and oil, could materially and adversely impact on KFG’s ability to secure partners in drilling projects, with the result that the Company may be forced to scale back its operational activities.

KFG had cash at January 31, 2015 of $2,133,800. Oil production at Fayette is providing positive cash flow and will continue to do just that. As of now, the Company plans to expand as cash flow permits. The Company is experiencing new cash flow from the Craig #1 and #2 wells, and the MacNeil #2 and #3 wells as well as having the Dale lease back on line. Also in the quarter, the Craig #3 well was completed; producing 50 BOPD and the Barnum #2 well was completed and is now producing to 80 BOPD. In addition, the Craig #1 and #2 and the MacNeil #2 and #3 have paid out causing the Company’s revenue from those wells to more than double. Even at current prices, the Company is producing positive cash flow.

In January and February 2015, the Company drilled 4 wells. Two dry holes in Franklin County, MS where the Company’s exposure was limited to 10% in each dry hole and two development wells – the Craig #5 and the Barnum #3 that are still awaiting completion due to bad weather. In the Craig #5 well, the Company has a 21.5 % working interest and it is expected to be a large source of new revenue once completed and on production. There are no plans at present to curtail the Company’s programs.

The Company is not contemplating any other transactions which have not already been disclosed. The Company continues to look at other property acquisitions and to seek joint venture partners on its properties on a regular basis.

Share Capital

The total number of shares outstanding as at January 31, 2015 and March 27, 2015, is 50,584,144. As of January 31, 2015 and March 27, 2015, there were no stock options or warrants outstanding.

Outlook

Production at Fayette is stable and has started a slow decline. With the Dale lease back on production and new production coming off the Craig and Parker leases, KFG will have adequate internal cash flow to develop existing leases as well as support several new prospects in the coming months. The Company’s outlook for the next twelve months is positive. With a current ratio of 2.27, KFG is well positioned to prosper during this period of much lower oil prices. In January and February 2015, KFG drilled 4 wells – two shallow dry holes in Franklin, Co. MS and two successful development wells in Adams Co. MS – the Barnum #3 and the Craig #5. Both wells are waiting on completion. Five new projects are in various stages of completion and are expected to be ready to drill by early summer. There is also development still to be done on the Barnum and Craig leases.

KFG shuts down Barnum, Craig operations on bad weather

2015-03-09 13:34 MT - News Release

Mr. Robert Kadane reports

KFG OPERATIONS UPDATE

KFG Resources Ltd.'s subsidiary's latest two wells -- the KFG Petroleum Corp. Barnum No. 3 and the Craig No. 5 -- are still awaiting completion. Rain, snow and ice in the past three weeks have shut down field operations. A further report will be issued when dry weather permits operations to continue. The company plans a late spring and summer drilling program with four new projects currently and two potential development wells, depending on offset well performance, all in Mississippi.

© 2015 Canjex Publishing Ltd. All rights reserved.

KFG Resources cases Barnum No. 3 well

2015-02-23 14:05 MT - News Release

Mr. Robert Kadane reports

KFG REPORTS STATUS OF MISSISSIPPI DRILLING PROGRAM

KFG Resources Ltd.'s subsidiary, KFG Petroleum Corp. of Natchez, Miss., has set production casing in its Barnum No. 3 well logging several potential oil zones in the well. A completion attempt will be made in the Parker sand at 6,415 feet (the producing zone in the Barnum No. 2 well). The company has a 9-per-cent working interest in the well until payout and a 20.5-per-cent interest thereafter.

In addition, the company has run production casing in its Craig No. 5 well to 6,400 feet to test the Benbrook sand at 6,214 feet. The producing sand on the Craig lease, the second Wilcox sand at 4,348 feet, was also present and productive significantly expanding oil reserves on the lease. KFG has a 21.5-per-cent working interest in the Craig No. 5 well. As the wells are perforated and put on production a report will follow. The company also drilled two wildcats, both dry holes, in Franklin county, Mississippi, the Seale No. 1 and the Wall No. 1, both 4,600-foot shallow dry holes. The company had a 10-per-cent working interest in both wells.

© 2015 Canjex Publishing Ltd. All rights reserved.

KFG REPORTS STATUS OF MISSISSIPPI WILCOX DRILLING PROGRAM

KFG Resources Ltd.'s subsidiary, KFG Petroleum Corp. of Natchez, Miss., has resumed its Wilcox shallow drilling program. The company is moving in on the Wall No. 1, a 4,600-foot Wilcox test, to be followed by the Seale No. 1, another 4,600-foot Wilcox test. Both wells are wildcats in Franklin county, Mississippi. KFG has a 10-per-cent working interest in both wells and, if successful, will jump to a 21.5-per-cent working interest after payout.

Also, the company is staking location to offset its Barnum No. 2 well in Adams county, Mississippi, a 6,700-foot Wilcox test. The Barnum No. 2 well has already produced 10,000 barrels, and has settled down to a rate of 70 barrels of oil per day. The Barnum No. 3 well will be drilled as weather permits, probably in early February. KFG has a 9-per-cent working interest in the Barnum lease, increasing to a 20.5-per-cent working interest at payout.

© 2015 Canjex Publishing Ltd. All rights reserved.

KFG Resources earns $611,881 in fiscal H1 2014

2014-12-30 12:56 MT - News Release

Mr. Robert Kadane reports

KFG LOGS SOLID FIRST HALF FISCAL 2014

KFG Resources Ltd.'s subsidiary, KFG Petroleum Corp. of Natchez, Miss., had revenue from the sale of oil and gas of $1,491,772 for the six months ended Oct. 31, 2014, compared with $1,129,981 for the six months ended Oct. 31, 2013. Management fee income was $220,523 for the period, compared with $211,028 for the corresponding six-month period in 2013. The company reported net income of $611,881 for the six months ended Oct. 31, 2014, compared with $238,365 for the comparable 2013 period. The company had cash on hand of $1,836,298 with total liabilities of $764,620. Current assets were $2,271,974. The company's operating costs per barrel for the six-month period ending Oct. 31, 2014, were $18.85 per barrel. Free cash flow for the period was $991,000 after all expenses.

Operationally, the Craig No. 4 well had oil shows but it was not considered commercial. KFG's drilling program for calendar 2015 will be unaffected by the decline in oil prices to date. KFG anticipates drilling activity to resume in February, 2015, with the drilling of three wells, starting with offsetting the company's Barnum Mp. 2 well in Adams county, Mississippi, and continuing with two shallow wildcats in Franklin county, Mississippi.

© 2014 Canjex Publishing Ltd. All rights reserved.

KFG Earns $612,000 on $1.7 million revenue

KFG Q2 Results Ending October 31st 2014:

Assets

Cash: $ 1,836,298 ($0.036c in cash compared to $1.14 million in July 2014)

Receivables: $403,296

Prepaid Expenses: $32,380

Reclamation Bond: $20,000

Property & Equipment: $1,222,247

Total Assets: $3,514,221

Liabilities

Accounts Payable: $726,247

Deposits from Co-Owners: $38,373

Total Liabilities: $764,620

Revenue after 6 months (2 Profitable Quarters)

Oil and gas: $1,491,772

Management Fees: $22,523

Total Revenue: $1,712,295

Total Costs: $1,100,414

Net Income: $611,881 (Net Income was $238,365 in 2013)

EPS= $611,881 / 50,584,11 = $0.012c

Wells in production: 25

Average production in Q2: 104bopd (75bopd was Q1, increase of 29bopd of 28%)

Average Price: $101 per bbl - LLS(Louisiana Light Sweet oil, premium to WTI)

COST per barrel - $18.85/bbl

Management Discussion and Analysis Highlights

The Company is a small independent energy company engaged in the development of onshore oil and gas reserves with activities concentrated in Concordia and Catahoula Parishes, Louisiana, Adams, Jefferson, and Wilkinson Counties, Mississippi and Comanche County, Kansas.

Overall the Company has recovered from giving up 25% of its interested in the Fayette Field wells at payout. Currently, with the MacNeil wells and Craig wells at payout, revenues are on a growth pattern again. The Company was able to grow just utilizing cash flow. Several new projects are in the pipeline and the Craig #3 well will payout in the next few months increasing that revenue stream. KFG will have no problems financing growth through its internal cash flow throughout the remainder of its fiscal year ending April 30, 2015. In addition, the Barnum #2 well is on production as of mid September 2014. The Craig #4 well was recently completed as a dryhole. With the Company’s current cash position and a quick ratio of 2.5, the Company is in a good position to weather the current collapse in oil prices from about $84 in October 2014 to around $55 - $60/bbl at this writing and will still show positive cashflow. The Company’s operating cost per bbl is currently $18.85/bbl.

The Company reported net income of $611,881 for the six months ended October 31, 2014 compared to net income of $238,365 for the six months ended October 31, 2013, with the increase in net income a result less operating expenses plus better prices for oil and new oil from the Craig and McNeil bases due to increased working interest in the wells as well as total overhead charges remaining virtually unchanged.

The Company reported net income of $151,781 for the three months ended October 31, 2014 compared to net income of $124,840 for the three months ended October 31, 2013, with the increase in net income a result less operating expenses plus new oil from the Craig and McNeil bases due to increased working interest in the wells.

( Barnum 2 likely reduced our net income this quarter as this was an expensive well)

During the quarter ended October 31, 2014, the Barnum #2 well was completed producing in excess of 100 BOPD. The Company has a 9% working interest in that well jumping to 16% at payout. The Company plans to offset that well in February 2015 as well as drill two new prospects. Gross income from oil sales increased 15% in spite of declining prices.

Outlook

Production at Fayette is stable and has started a slow decline. With the Dale lease back on production and new production coming off the Craig and Parker leases, KFG will have adequate internal cash flow to develop existing leases as well as support several new prospects in the coming months. Unless the price of oil collapses, the Company will generate sufficient capital to fund its requirements throughout 2014 internally. The Company’s outlook for the next six months is positive. With a current ratio of 2.97, KFG is well positioned to proper during this period of much lower oil prices. At this writing, no projects will be put off or delayed. The Company anticipates its 2015 drilling program starting in February 2015.

Share Capital

The total number of shares outstanding as at October 31, 2014 and December 22, 2014, is 50,584,144. As of October 31, 2014 and December 22, 2014, there were no stock options or warrants outstanding.

(My Notes)

Wells that are approved and still need to be drilled next year:

Fayette Well - Announced September 11th 2014

Seale Well - Announced November 5th 2014

Wall 1 Well - Announced November 5th 2014

Barnum 3 Well - Announced November 5th 2014

Wall 2 Well - Approved through Mississippi Legislature, to be announced soon

Jones Flower Well - Approved through Mississippi Legislature, to be announced soon

Craig 3 and Barnum will pay out soon which will add instant production to KFG.

This report is based on KFG's 2014 reults and does not have anything included between May 2014 until now. That means (4 wells that paid out in June, Craig 3 well + new reservoir in July, Q1 profit of $460,000 or $0.01c EPS, Barnum 2 well of 140bopd). The $0.19c NAV is exactly the same as their audited annual financials + 51-101 report that came out at the end of August(ending April 30th 2014). Then the company still has 3 wells to drill in the next 6 weeks, 2 wells in the start of 2015, and likely more after that.

Additional Insider Buying & Stock Price Near 52 Week High

The insider buying continues while the stock price flirts with the 53 week high and could break the 6 year resistance level of $0.15c. With 3 wells being worked on as we speak, positive results from all of them should drive the price well into the 20 cent range.

Haney, Kevin

Insider's Relationship to Issuer: 3 - 10% Security Holder of Issuer

Transaction

Date Transaction Nature # or value acquired

or disposed of Price Account

Balance

Security Type: Common Shares (Direct Ownership)

Nov 14/14 10 - Acquisition in the public market 60,000 $0.130 5,690,000

Nov 14/14 10 - Acquisition in the public market 150,000 $0.135 5,630,000

Nov 14/14 10 - Acquisition in the public market 15,000 $0.125 5,480,000

Nov 7/14 10 - Acquisition in the public market 25,000 $0.105 5,465,000

Nov 6/14 10 - Acquisition in the public market 15,000 $0.115 5,440,000

Nov 5/14 10 - Acquisition in the public market 20,000 $0.115 5,425,000

Nov 4/14 10 - Acquisition in the public market 35,000 $0.125 5,405,000

Nov 4/14 10 - Acquisition in the public market 5,000 $0.120 5,370,000

Oct 29/14 10 - Acquisition in the public market 40,000 $0.130 5,365,000

Oct 27/14 10 - Acquisition in the public market 55,000 $0.130 5,325,000

Oct 27/14 10 - Acquisition in the public market 80,000 $0.120 5,270,000

Oct 24/14 10 - Acquisition in the public market 50,000 $0.090 5,190,000

Oct 21/14 10 - Acquisition in the public market 40,000 $0.085 5,140,000

Oct 14/14 00 - Opening Balance-Initial SEDI Report

Good insider buying this week:

As of 11:59pm ET November 7th, 2014

FilingDate TransactionDate Insider Name OwnershipType Securities Nature of transaction # or value acquired or disposed of Price

Nov 7/14 Nov 7/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 25,000 $0.105

Nov 6/14 Nov 6/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 15,000 $0.115

Nov 5/14 Nov 5/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 20,000 $0.115

Nov 4/14 Nov 4/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 35,000 $0.125

Nov 4/14 Nov 4/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 5,000 $0.120

Oct 29/14 Oct 29/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 40,000 $0.130

Oct 27/14 Oct 27/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 55,000 $0.130

Oct 27/14 Oct 27/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 80,000 $0.120

Oct 25/14 Oct 24/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 50,000 $0.090

Oct 23/14 Oct 21/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 40,000 $0.085

Oct 23/14 Oct 14/14 Haney, Kevin Direct Ownership Common Shares 00 - Opening Balance-Initial SEDI Report 5,100,000

KFG Q2 earnings estimate

In regards to the news release today it states KFG is producing at slightly under 100bopd, so I would guess around 98bopd. Now I am not too sure as to why the number is so much lower than what was posted on the website on November 1st. Is it possible that a couple wells were shut down between Sunday-Tuesday? maybe. But either way, since we know production increased in Q2, lets redo the estimated quarterly results. I have a confirmed LLS number for August and we have the last price for September before the drop, lets use those as well.

http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=F003075773&f=M =====> $98.31 was the average price in August for LLS

http://www.petroleumnewsbakken.com/pntruncate/501597498.shtml ======> LLS was trading at $96.29 October 2nd, so September average should be at least $96

October prices dropped, but LLS is always around Brent, lets use $84 for this month

$98.31 + $96 + $84 = $92.77 or lets say $93, which is what I calculated as an average for Q2 in my previous post.

$93(per barrel average) X98BOPD X 90(Days in Q2) = $820,260 in oil revenues for the second quarter(estimate)

Then we add $120,000 for management fee's which puts us at $940,260 total revenue. Again lets use the $500,000 in expenses since it's higher than Q1 and might be due to extra costs from Craig 3 and Barnum 2.

$940,260 - $500,000 = $440,260 net income (estimate)

I'm pretty sure KFG will earn around $400,000 to $500,000 for the first 3 quarters, then in Q4 all the payouts and new wells will add significant revenue. $0.04-0.05c EPS for 2015 isstill an achievable target.

- 3 wells confirmed to do soon

- 2 wells to pay out and given their current numbers, it's an extra 20-25bopd from Craig 3 and Barnum 2

- The Franklin wells are in a new area, so results could be anywhere and could very well add new zones to

drill from.

KFG Resources to drill three wells in Wilcox

2014-11-05 07:42 MT - News Release

Mr. Robert Kadane reports

KFG REPORTS STATUS OF MISSISSIPPI WILCOX DRILLING PROGRAM

KFG Resources Ltd.'s subsidiary, KFG Petroleum Corp. of Natchez, Miss., has three projects that are drill ready before year-end 2014. In Adams county, Mississippi, the Craig No. 4, a southwest offset to the Craig No. 3 producer, will be drilled to 6,500 feet to test all Wilcox zones of interest. In Franklin county, Mississippi, the Seale No. 1, a 4,500-foot Wilcox test, and the Wall No. 1, a 4,600-foot Wilcox test, will evaluate two new areas of interest where the company has accumulated an acreage postion.

In February, 2015, in Adams county, the Barnum No. 3, a west offset to the company's Barnum No. 2 well, currently averaging close to 120 barrels of oil per day, will be drilled to a depth of 7,000 feet, testing several Wilcox zones that have produced in the immediate area. This well will be followed by additional development in Franklin county, Mississippi.

In each of the above cases, KFG will have a 10-per-cent working interest, converting to a 21.5-per-cent interest following payout of a successful project, except for the Barnum well, where the company's interest is 9 per cent.

Current net daily production is slightly under 100 barrels of oil per day before payout of the Craig No. 3 or the Barnum No. 2 wells anticipated during the first half of calendar 2015 even if the Craig No. 4 is successful.

© 2014 Canjex Publishing Ltd. All rights reserved.

Sorry everyone, an error was pointed out to me and I confirmed it. KFG shows a 74.9% working interest in Fayette, but only 59.4% of it is NET to them. So below are the re-calucations which are still good regardless.

Using the current numbers that were updated today on the website, here is what KFG's wells are producing as a whole and the net back to KFG. Fayette does not state a number, but if you look back at other financial statements, it shows production at a constant 110-120bopd from the 9 wells. For this chart I'm only using the lower amount.

Wells(name) Total Production KFG's WI(net) KFG's Cut(bopd)

9 Fayette 110bopd 59.4% 65.5bopd

2 Macneil 50bopd 20.5% 10bopd

3 Parker 90bopd 10% 9bopd

3 Craig 165bopd 21.5% & 10% 30bopd

1 Barnum 140bopd 9% 13bopd

1 Dale 25bopd 17% 4bopd

1 Miller 12bopd 4% 0.5bopd

20 Producing 592bopd - 132bopd

Average WI in all wells: 132bopd(KFG) / 592bopd(Total) = 22.3% or 22% average

Now lets see what KFG can cash flow at $80 per barrel with LLS prices right now:

132(bopd) X $80(per barrel) X 90 days(quarter) = $950,400 not including management fees.

Below is a list of wells that either have to A) Be put back online B) Need to be drilled, or C) Have to still pay out.

- Craig 3 well still needs to pay out, increasing from 10% to 21.5%

- Barnum 2 wells still needs to pay out, increasing from 9% to 20.5%

- Roundtree well shut for now, needs to be put back online

- Miller well still needs to pay out, increasing from 4$ to 18%

- 1 Fayette well to be drilled soon, as per the September 11th 2014 news release

- Craig 4 well to be drilled in December 2014

- Barnum offset in first quarter of 2015, could be 2 other potential offsets

- Several Franklin areas to drill in Q1 2015 with 3 targets ready

All information was updated November 1st 2014 as per the main page of the KFG website.

KFG Production Chart As Of November 1st 2014

Using the current numbers that were updated today on the website, here is what KFG's wells are producing as a whole and the net back to KFG. Fayette does not state a number, but if you look back at other financial statements, it shows production at a constant 110-120bopd from the 9 wells. For this chart I'm only using the lower amount.

Wells(name) Total Production KFG's WI KFG's Cut(bopd)

9 Fayette 110bopd 75% 80bopd

2 Macneil 50bopd 20.5% 10bopd

3 Parker 90bopd 10% 9bopd

3 Craig 165bopd 21.5% & 10% 30bopd

1 Barnum 140bopd 9% 13bopd

1 Dale 25bopd 17% 4bopd

1 Miller 12bopd 4% 0.5bopd

20 Producing 592bopd - 146.5bopd

Average WI in all wells: 146.5bopd(KFG) / 592bopd(Total) = 24.7% or 25% average

Now lets see what KFG can cash flow at $80 per barrel with LLS prices right now:

146.5(bopd) X $80(per barrel) = $11,720 per day X 30(days) = 351,600 per month. This does not include the management fees given to KFG per well. All in costs per well is around $30 per barrel, so very good margins even with the lower prices.

Below is a list of wells that either have to A) Be put back online B) Need to be drilled, or C) Have to still pay out.

- Craig 3 well still needs to pay out, increasing from 10% to 21.5%

- Barnum 2 wells still needs to pay out, increasing from 9% to 20.5%

- Roundtree well shut for now, needs to be put back online

- Miller well still needs to pay out, increasing from 4$ to 18%

- 1 Fayette well to be drilled soon, as per the September 11th 2014 news release

- Craig 4 well to be drilled in December 2014

- Barnum offset in first quarter of 2015, could be 2 other potential offsets

- Several Franklin areas to drill in Q1 2015 with 3 targets ready

All information was updated November 1st 2014 as per the main page of the KFG website.

KFG project information has been updated on the website. All production is current as of today. It also mentions the future wells being drilled between now and January.

http://www.kfgresources.com/project.htm

KFG Resources Ltd., through its 100% owned U.S. operations subsidiary "KFG Petroleum Corporation" owns production and holds exploration and development interests in Louisiana and Mississippi. Daily average production for the quarter ended July 31, 2014 was 75 BOPD. Average oil price received was $102 per barrel. Oil sales for the quarter ended July 31, 2014 were $788,143 and management fee income was $116,266 totaling $904,409 as compared to $582,176 in the fiscal first quarter of 2013.

Wilcox Oil Play

KFG focuses on the Wilcox formation which is a water-drive reservoir of Eocene Age prevalent in East-Central Louisiana and Southwest Mississippi. The Wilcox is a relatively shallow horizon varying between 3500 and 9200 feet in depth. There is also the deeper Tuscaloosa formation in many areas where KFG operates and when found is known to be a prolific production horizon. KFG's projects are described below.

Mississippi

Fayette Field, Jefferson County, Mississippi

The Fayette field is located 21 miles northeast of the city of Natchez. KFG has a 74.9% working interest (59.4% net) in the field. Fayette is a salt feature covering approximately 3800 acres. Past production was from the Wilcox and the Lower Tuscaloosa formations. KFG did a 3D seismic survey in 2008 and the results led to the discovery of the Spring Hill feature in June 2009. Spring Hill is fully developed with 6 producing wells. KFG has 2 other wells at Fayette including 1 small gas well. The reprocessed 3D seismic survey reveals both shallow and a deep target which KFG intends to test in the future. The Spring Hill is past the flush part of production and is in a long slow decline.

Carthage Point Field, Adam's County Mississippi

KFG drilled the MacNeil #2 well in March 2013 and a successful offset, the MacNeil #3 in October 2013. In August 2014 payout of the project was achieved and KFG's working interest increased to 20.5% from 8%. Daily production is 50 BOPD.

LaGrange Field, Adam's County Mississippi

KFG has a 10% working interest in the Parker Lease with no reversion. Four wells have been drilled - three producers and one dry hole. Combined production on the lease is 90 BOPD and it is fully developed. Also at LaGrange but in a different part of the field, KFG drilled its Craig #1 well in November 2013 followed by its Craig #2 in January 2014. Production from both wells is about 115 BOPD. A third well, the Craig #3, was put on production in July 2014 and it is currently producing 50 BOPD. The Craig #4 well has been staked and will be drilled in December 2014. The Craig #1 and #2 wells have paid out and KFG's interest jumped from 10% to 21.5% in those wells. KFG's working interest in the Craig #3 well is currently10%

Mantua Field, Adams County, Mississippi

In September 2014 the Company completed its Barnum #2 well at 6398 feet in the Parker Sand of the Wilcox. The well is currently producing 140 BOPD and will be offset in the first quarter of 2015. KFG has a 9% working interest in that well, jumping to 20.5%at payout. At this writing there appears to be three potential offsets.

Franklin County, Mississippi

There are several areas in Franklin County being leased by the Company which KFG intends to drill in the first Quarter 2015. Depths range from 4400 feet to 6800 feet. In each instance KFG has mitigated its risk by only keeping a 10% working interest and, if successful, backing in for up to an additional 16.25%. At present three of these projects are drill ready.

Louisiana

Concordia Parish, Louisiana

KFG has three leases in Concordia Parish. The Dale lease went off production in April 2013 and was returned to production in May 2014.after being shutin for a year waiting on saltwater disposal well approval. The lease is currently producing 25 BOPD from two well with an average working interest of 17%. The Roundtree lease is currently shutin, awaiting a cement squeeze to shut off a channel in the cement and the Clayton Lease, (#1 Miller) continues to produce about 12 BOPD, KFG has a 4% working interest at Clayton increasing to 18% at payout. .

Insider Buying this week:

Latest 6 months of SEDI filings for KFG by transaction date, descending [?]

amended.gif Amended Filing

As of 11:59pm ET October 27th, 2014

Filing

Date Transaction

Date Insider Name Ownership

Type Securities Nature of transaction # or value acquired or disposed of Price

Oct 27/14 Oct 27/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 55,000 $0.130

Oct 27/14 Oct 27/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 80,000 $0.120

Oct 25/14 Oct 24/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 50,000 $0.090

Oct 23/14 Oct 21/14 Haney, Kevin Direct Ownership Common Shares 10 - Acquisition in the public market 40,000 $0.085

Oct 23/14 Oct 14/14 Haney, Kevin Direct Ownership Common Shares 00 - Opening Balance-Initial SEDI Report 5,100,000

A great summary from Pinnacle Digest came out after the close today on KFG. I think this will attract some new buyers

and watchers tomorrow as this company bucks the trend of the falling oil stocks. The best juniors are the ones that can

make money when everyone else is losing money. It didn't specify, but last year KFG made $120,000 half half of the

revenue and $76 price per barrel.

http://www.pinnacledigest.com/

http://www.pinnacledigest.com/blog/pinnacle-digest/kfg-resources-jumps-50-monday

Best part at the bottom of the article:

This is all relevant, because on Monday, KFG was among the most liquid stocks on the TSX Venture. In a tumultuous environment for even the most balanced and successful oil and gas companies, KFG has found a way to climb within striking distance of its 52-week high.

Investors will need to see continued production increases and exploration upside if its market cap is to rise.

KFG Resources is representative of a junior resource stock that can still catch a bid because it has revenue and low costs. When a company earns in for a limited percentage of ownership of any given well, it mitigates its risk hugely; if the companies involved should miss on the well, they move to the next opportunity.

A junior oil and gas company can earn 10% on 10 different wells, providing it ten times the opportunity of hitting on any single well vs. being the operator and earning 100% on a single well. This is not a new strategy, but one being utilized more and more often in the junior resource sector.

Additional insider buying as per Canadian Insider:

https://www.canadianinsider.com/node/7?menu_tickersearch=KFG+%7C+KFG+Resources

Here is the progress KFG has made between August 2013 and October 2014:

August 2013 - KFG Exited 2013 with a small profit, but lost 25% of Fayette's production due to payouts.

September 2013 - KFG earned $116,000 on just $500,000 in revenue at $76 per barrel price for LLS

November 2013 - Craig 1 put into production

December 2013 - KFG earned $126,000 on $758,000 revenue

February-March - Craig 2 and Parker 2,3,4 start drilling phase and put into production

April 2014 - KFG lost $300k due to accrued income, increased costs from hiring new employees, buying new equipment and additional costs from all the new wells.

June 2014 - Four wells paid out, turning 10% interests into 20% interests, increasing KFG's production by 35-40bopd. Craig 3 and Barnum 2 started drilling

July 2014 - Craig 3 put into production. New Reservoir was found

August 2014 - KFG has net profit of $67,500 for 2013 after 4 quarters(ended April 30th)

- Total revenue at $2,659,768. Says in MD&A that all lost production was recovered and even more from a year ago.

September 2014 - Barnum well put into production at 40bopd, but 2 weeks later production increased to 140bopd.

- Fall drill program announced, 3-4 wells to complete before end of December

October - KFG earned $461,000 on $900,000 revenue. Investor acquires a 10% stake in KFG.

The October results only include 22 wells of the 24 currently production, so in Q2 which will come out in December(ending October 31) we will see additional revenue from the following:

- Craig 3 well

- Barnum well

- Full quarter of the 4 wells that paid out in June

KEVIN HANEY ACQUIRES 10% VOTING INTEREST IN KFG RESOURCES LTD

Kevin Haney of Dauphin, Man., has acquired 5.1 million common shares of KFG Resources Ltd., effective Oct. 16, 2014. Total shares held directly and indirectly amount to 5.1 million voting units, representing a 10-per-cent interest. These shares were purchased for investment purposes. Mr. Haney may purchase additional shares in the market or, alternatively, sell some or all of his holdings, depending on market conditions. It is not the intention of Mr. Haney to influence control or direction over the management of the company.

For further information, contact Mr. Haney at 204-648-4383.

© 2014 Canjex Publishing Ltd. All rights reserved.

Looked at two main Mississippi oil sites today and saw that KFG's Craig 4 well and Seale(Franklin wild cat) are licensed and ready to drill whenever the company is ready.

http://gis.ogb.state.ms.us/MSOGBOnline/

The second thing was trying to see how well KFG is performing compared to it's peer in Mississippi and Louisiana. But DrillingEdge is only upto date until June. Also keep in mind that this is total combined production of KFG and it's partners, which doesn't include Craig 3 or Barnum.

http://www.drillingedge.com/mississippi

Breakdown of areas and where KFG ranks in terms of production as of June.

Jefferson County --> KFG was the main producer in this county

http://www.drillingedge.com/mississippi/jefferson-county

Adams County --> KFG was the second main producer in this county

http://www.drillingedge.com/mississippi/adams-county

Lincoln County---> KFG was the second main producer in this county

http://www.drillingedge.com/mississippi/lincoln-county

Warrn County--->KFG isn't very active here, only one small well in this county

http://www.drillingedge.com/mississippi/warren-county

Grand total for Mississippi is 18 wells in production with 12,185 barrels produced.

12,185(barrels) / 30(days) = 406bopd.

http://www.drillingedge.com/mississippi/operators/kfg-petroleum-corporation/31500

Then the company has a few wells in Louisiana. For whatever reason though, I can't find the breakdown of where these are on this website.

http://www.drillingedge.com/louisiana/operators/kfg-petroleum-corporation/2944

Shows 3 wells with a total production of 732bopd. KFG showed 22 in the Q1 results because it included Dale, which was shutdown in this quarter as mentioned in the MD&A. Now Dale is back up and Craig 3 and Barnum 2 are producing, so total count will be 24 wells for Q2 2014.

732(barrels) / 30(days) = 24bopd

Now there are some investors wondering what will happen with the recent drop in oil prices. Well KFG is covered. One of the few articles I was able to find about Louisiana Light Sweet crude, but it has upto date recent pricing which is important since KFG sells it's oil at these prices. Like I mentioned in previous posts, my estimated average selling price for KFG in Q2 will be around $95. LLS has been trading closer to brent prices over the last couple months rather than WTI. One of KFG's many advantages in this tough oil market. Just this week the price hit a low of $90.58, so KFG is still getting $90 a barrel and with $30 cost per barrel, very profitable still. Unlike Western Canadian select, it hit a low of $74.46.

http://www.petroleumnews.com/pntruncate/501597498.shtml

At the bottom of this article

Louisiana Light Sweet, a Gulf Coast benchmark which has recently been trading near par with Brent, settled at $96.29 on Oct. 2, but by Oct. 8 it had fallen nearly $6 settling at $90.58 according to CME Group information provided by Argus. Western Canadian Select, another North American benchmark, settled at $77.86 on Oct. 2, but by Oct. 8 it too had fallen settling at $74.46.

News: Barnum well producing at 140bopd, Craig 4 to be drilled shortly

KFG's operating profit at $460,581 in Q1 2015

2014-10-01 12:27 MT - News Release

Mr. Robert Kadane reports

KFG REPORTS OPERATING PROFIT FOR FISCAL 1ST QUARTER ENDING JULY 31, 2014

KFG Resources Ltd.'s wholly owned subsidiary, KFG Petroleum Corp. of Natchez, Miss., had net income of $460,581 for the company's fiscal first quarter ending July 31, 2014, compared with $113,525 in the corresponding quarter in 2013. Gross revenue for the quarter was $904,409, as compared with $582,176 in the fiscal first quarter of 2013. The company had cash on hand of $1,133,429 and a current ratio of 2.1 to 1. There was no long-term debt.

Adams county, Mississippi

Operationally, the company's Barnum No. 2 well in the Mantua field reported initial production of 40 barrels of oil per day in mid-September. After two weeks of production, the well is now producing 140 bopd from the original perforations at 6,398 feet in the Parker sand. The well has several potential zones behind pipe. Field development will begin in the first quarter of 2015 after extensive production testing. The company's working interest in the well is 9 per cent, jumping to 20.5 per cent at payout. Additionally, the Craig No. 4 well has been staked as a southwest offset to the Craig No. 3 well in the LaGrange field currently producing 50 bopd. The company's working interest in the Craig No. 4 is 10 per cent, jumping to 21.5 per cent at payout.

© 2014 Canjex Publishing Ltd. All rights reserved.

KFG Earns $461,100US in Q1 2014, $0.01c eps

KFG Resources Ltd. Financial and MD&A Highlights for Q1 2014 Ending July 31

(Expressed in US Dollars)

Price: $0.10

Shares Outstanding: 50,584,144 with no options or warrants

Cash: $1,133,429

Accounts Receivables: $1,032,148

Prepaid Expenses: $22,922

Reclamation Bond: $20,000

Property & Equipment: $1,432,033

Total Assets: $3,640,532

Total Liabilities: $1,042,248 (All payables)

Revenue

Oil and gas: $788,143

Management Fees $116,266

Total Revenue: $904,409

Total Expenses: $444,015

Net Income: $460,100

Basic and diluted income per common share: $0.01

Now we will move onto the MD&A. Keep in mind the following:

1) 4 main wells paid out mid Q1, so only half of that new revenue was added to this quarter

2) Craig 3 was put online end of Q1, no revenue from that

3) Barnum wasn't online until mid Q2

This is why the well count only shows 21. With Craig 3 and Barnum we are at 23. Not sure why it isn't 24, maybe one well was down this quarter. Either way, the above translates to a much bigger revenue/profit for Q2 and with several wells to go it will only increase. $0.04-0.05c eps for 2014 is very realistic at this point. Even at a lower range 10 times earnings price, KFG would be at $0.40-0.50c minimum by next fall. Doesn't include additional revenue and new discoveries either.

MD&A

Overall Performance

For the three months ended July 31, 2014, the Company had cash flow from oil and gas production of $788,143, compared to $519,526 for the three months ended July 31, 2013. Oil production decreased from 86.15 BOPD to 75.07 BOPD, and gas production decreased 3.86 MCF per day. The average price of gas increased $0.87 per MCF and the average price of crude oil decreased $11.43 per bbl when comparing the three months ended July 31, 2014 and July 31, 2013.

Overall the Company has recovered from giving up 25% of its interested in the Fayette Field wells at payout. Currently, with the MacNeil wells and Craig wells at payout, revenues are on a growth pattern again. The Company was able to grow just utilizing cash flow. Several new projects are in the pipeline and the Craig #3 well will payout in the next few months increasing that revenue stream. KFG will have no problems financing growth through its internal cash flow throughout the remainder of its fiscal year ending April 30, 2015. In addition, the Barnum #2 well is on production as of mid September 2014. The Craig #4 will be drilled in mid October 2014.

The Company reported net income of $460,100 for the three months ended July 31, 2014 compared to net income of $113,525 for the three months ended July 31, 2013, with the increase in net income a result of less operating expenses plus better prices for oil and new oil from the Craig and McNeil bases due to increased working interest in the wells.

The quarter ended July 31, 2014 reflected the production of the Craig #2 well as well as payout of the Craig #1 and #2 wells increasing KFG’s working interest from 10% to 21.5% and late in the quarter the MacNeil #1 and #2 paid out increasing the working interest in those wells from 8% to 20.5%.

Production at Fayette is stable and has started a slow decline. With the Dale lease back on production and new production coming off the Craig and Parker leases, KFG will have adequate internal cash flow to develop existing leases as well as support several new prospects in the coming months. Unless the price of oil collapses, the Company will generate sufficient capital to fund its requirements throughout 2014 internally.

LEVEL 2 QUOTE

Market Maker Shares Bid Price Ask Price Shares Market Maker

105,000 0.085 0.100 5,500

25,000 0.080 0.105 10,000

50,000 0.075 0.110 19,500

5,000 0.070 0.115 15,000

40,000 0.055 0.120 60,000

10,000 0.035 0.135 50,000

100,000 0.020 0.140 20,000

264,000 0.015 0.150 50,000

200,000 0.010 0.180 11,000

300,000 0.005 0.200 212,000