News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

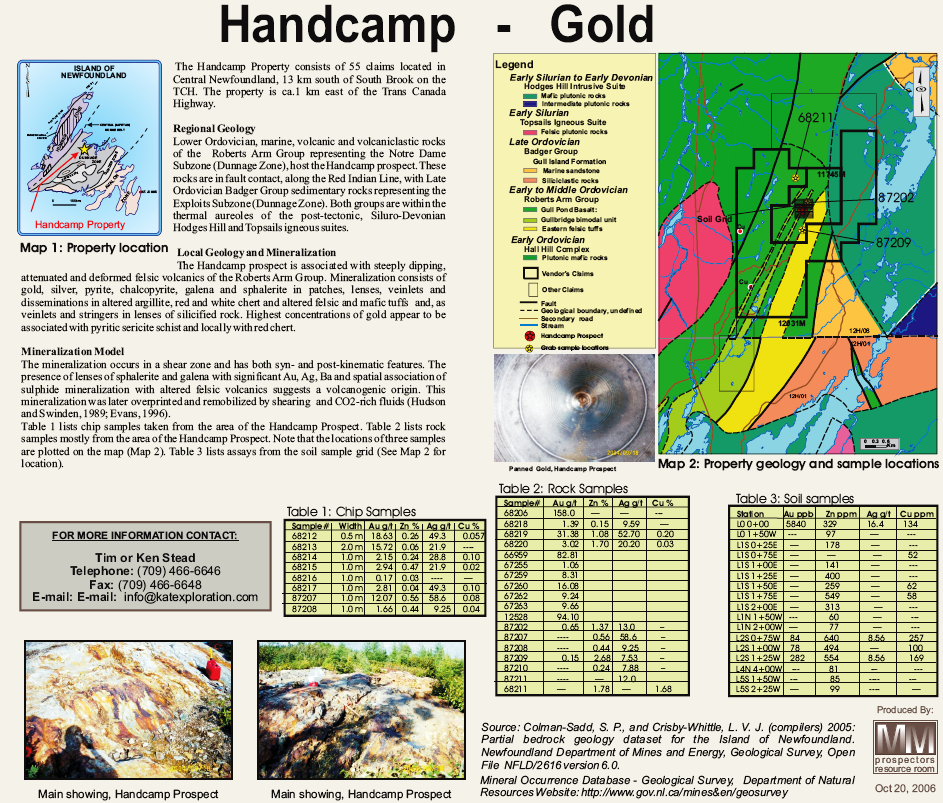

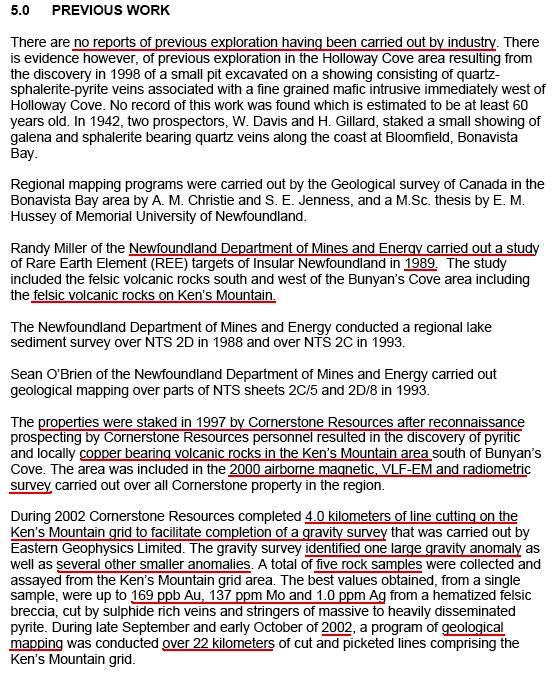

"...SABRE GOLD ANNOUNCES PRELIMINARY ECONOMIC ASSESSMENT FOR THE COPPERSTONE MINE

June 20, 2023

PDF Version

Vancouver, June 20, 2023 – Sabre Gold Mines Corp. (TSX: SGLD, OTCQB: SGLDF) (“Sabre Gold” or the “Company”) is pleased to announce it has completed a Preliminary Economic Assessment (“PEA”) on the 100% owned Copperstone Mine (“Copperstone” or “Project”) in Arizona, USA. The study has resulted in robust post-tax economics which, due to pre-existing infrastructure on surface and underground, result in both low initial capital and an overall low capital intensity ratio on a per ounce basis. The project benefits from its significant tax assets and recently reduced royalty encumbrance while also having potential for resource expansion and further exploration success.

The Preliminary Economic Assessment supports a high-grade gold underground mining operation at Copperstone producing an average of 40,765 payable oz gold per year for just over a 5-and-a-half-year mine life. Sabre Gold management worked with Hard Rock Consulting, LLC (“HRC”) to complete the PEA, which included comprehensive reviews of the construction, operations and costs, to provide confidence for potential project commencement and completion within budget and schedule. Trade off studies will continue on initial capital items and initial earthworks will commence as soon as the Company moves towards a formal construction decision. The Company will also continue to have discussions with potential providers of initial construction capital.

In accordance with National Instrument 43-101, the Company has engaged HRC to complete a technical report in support of the PEA, which will be filed on SEDAR within 45 days of this news release. The Company notes that mineral resources are not mineral reserves as they do not have demonstrated economic viability. The Company notes that a preliminary economic assessment is preliminary in nature, it includes inferred mineral resources that are considered too speculative geologically to have economic consideration applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the preliminary economic assessment will be realized.

The PEA base case assumes a gold price of $1,800 per oz and the PEA also presents project sensitivities using a range of spot gold prices between $1,600 to $2,000 per oz. All currency references herein are in US$.

Highlights from the Preliminary Economic Assessment

Consistent Production – Models an underground mine operation that will process 198,000 tonnes of ore at 544 tonnes per day (“tpd”) over the 5.6-year mine life (“LOM”).

Excellent Payback Period – The mine plan sequences the high-grade portions of the resource in early years to optimize grade and cash flow resulting in a payback period of less than 2 years and generating nearly $90m in after-tax cumulative undiscounted cash flow.

Low Initial Capital – Significant site infrastructure, such as pre-existing tailings and processing facilities, surface buildings and rehabilitated underground development allow for reduced upfront construction cost and low initial capital per payable gold ounce produced over the LOM.

Fully Licensed and Permitted – Permits are in place for initial construction and subsequent operation of the project as well as the necessary water and surface rights. Minor modifications required for the revised mine plan and flow sheet as a result of the PEA will be addressed as required in the coming months by the Company...."

https://www.sabre.gold/sabre-gold-announces-preliminary-economic-assessment/

BRAVO!

https://www.benzinga.com/pressreleases/23/06/32919152/sabre-gold-announces-preliminary-economic-assessment-for-the-copperstone-mine

https://www.cnbc.com/2023/06/20/gold-listless-as-investors-hunt-for-fed-rate-clues.html

Sabre Gold GM Talks About Preparations to ReOpen Copperstone GOLD Mine in Arizona

"... VP General Manager Sid Tolbert recently spoke to Global Stocks News’ CEO Guy Bennett about SGLD’s plans to re-start the Copperstone Gold Mine in Arizona...."

".... Sabre Gold holds 100% interest in two near-term North American gold producers: the fully permitted Copperstone gold mine located in Arizona, USA, and the Brewery Creek gold mine located in Yukon, Canada, both of which are former producers.

https://www.sabre.gold/

Management intends to restart production at Copperstone followed by Brewery Creek in the near term.

In the following video, VP General Manager Sid Tolbert talks with GSN’s Guy Bennett about current operations at the Copperstone Gold Project in Arizona...."

https://www.thenewswire.com/press-releases/1AwGFo4bJ-sabre-gold-sgldv-gm-talks-about-preparations-to-re-open-arizona-gold-mine.html

Sid Tolbert, this was an informative and a revealing interview and as an investor in Sabre Gold Mines; I'm pleased to learn that contract miners will be working on the mine for the foreseeable future.... for obvious reasons that you clearly stated. Bravo!

Did somebody say katx this is the original BIRDMAN BOB anybody here I know

"... Giulio T. Bonifacio, President and Chief Executive Officer of Sabre Gold, stated: "Sabre Gold continues to make significant progress at Copperstone in preparation of startup with progression to full production in the near term which now only remains subject to project funding. Definition drilling and results to date are continuing to show very good grade and continuity while adding further confidence to our updated geological model and our detailed mine plan. Estimated project capital for the restart of Copperstone remains in line with previous estimates as we continue to advance discussions with project lenders as well as other key stakeholders with an update on project funding to be provided in Q2-2022"

https://www.juniorminingnetwork.com/junior-miner-news/press-releases/1254-tsx/sgld/116358-sabre-gold-provides-copperstone-project-update.html

COPPERSTONE MINE UPDATE

In addition to the recently completed definition drilling at Copperstone, significant progress has been made with detailed mine planning, process engineering and mine-rehabilitation. These efforts are a continuation of earlier work completed to prepare the fully permitted mine for start-up and progression to full production.

A comprehensive detailed mine plan and production schedule was completed by Mine Development Associates in Reno, Nevada that defines stopes and production areas for the initial five years of mine-life. In addition, all capital and operating expenses were reviewed by way of further detailed engineering and have been incorporated into an updated discounted cashflow model. The mine plan indicates annual production of approximately 40,000 to 45,000 ounces per annum while demonstrating favorable economics which includes future expected conversion of additional resources based on the open extent nature of both the Copperstone and Footwall zones.

Due to limitations of underground development, drilling platforms and the geometry of the gold bearing shear zones Sabre intends to drill several years in advance as it advances underground development ahead of the underground mining areas. Years 5 to 13 are scheduled to produce from areas that currently have inferred resources and yet un-delineated extensions of the existing resources. The cash flow model includes the required excavation of drill platforms as operational headings advance and the associated drilling required to identify, confirm and define mineable areas. Updated capital and operating expenses were reviewed and incorporated into a discounted cashflow model.

Further engineering and refinement were completed on the processing facility that will incorporate a Whole Ore Leach process followed by Merrill-Crowe recovery and onsite refining. Plant lay-out and flowsheets with associated capital and operating cost estimates were completed. Engineering is estimated at 60% completion with flowsheets and plant lay-out complete. Concurrently, metallurgical testing is in final stages, indicating excellent gold recovery. Final metallurgical tests will provide data to confirm the equipment sizing and operating costs.

Mine rehabilitation continued with significant progress made in the majority of areas that will be mined in the first several years of mine life. Small Mines Development have been engaged and are nearing completion of 1,674 linear feet of rehabilitation that included robust ground support and enhancement of mine dewatering systems. The rehabilitation completes a series of efforts to ensure safety standards and readiness for full scale mining production.

The technical information in this news release has been reviewed and approved by Michael Maslowski, CPG, a qualified person as defined by National Instrument 43-101 and is employed by the company as its Vice President, Technical Services & Exploration...."

https://www.stockwatch.com/News/Item/Z-C!SGLD-3210987/C/SGLD

GREAT UPDATE !https://finance.yahoo.com/news/sabre-gold-provides-copperstone-project-130000560.html

Expecting KATX type run from CATA.. CEO is honey hole hunting in Indonesia.. Has had people on the ground over there for quite some time checking out gold properties..

TWDL 100k shares bought on the ask. Mid-Oct geo report due for "Yellow Jacket" followed by "Blue Jacket" in Nov.

TWDL

CNYC summary – 9-28-11 (avg. $.225)

TSX – CNC

OTC:BB – CNYC

Canyon Copper Corp (CNYC.OB)

1199 West Pender St., Suite 408

Vancouver, BC V6E 2R1

Phone: 604.331.9326 / 888.331.9326

Fax: 604.684.9365

URL: www.canyoncc.com

Email: info@canyoncc.com

IR: Robert Meister, Phone: 1.888.331.9326 x-231 / 1.604.331.9326 x-231 / info@cayoncc.com

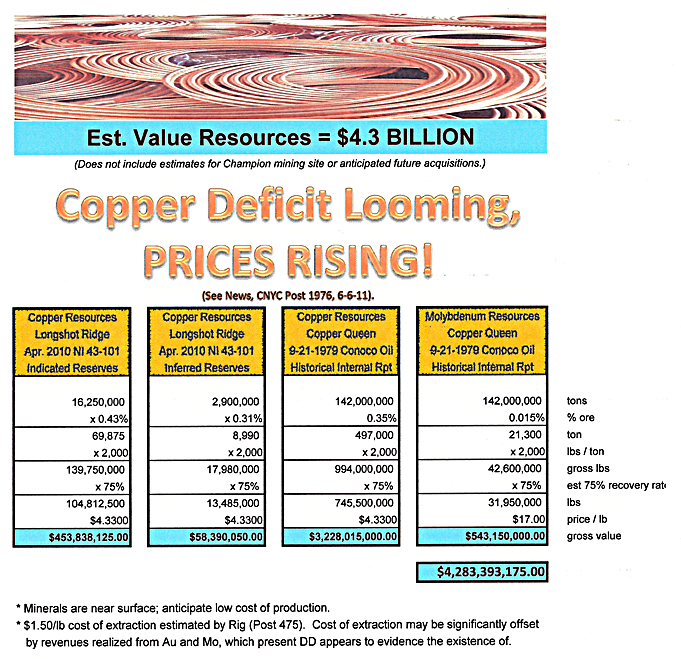

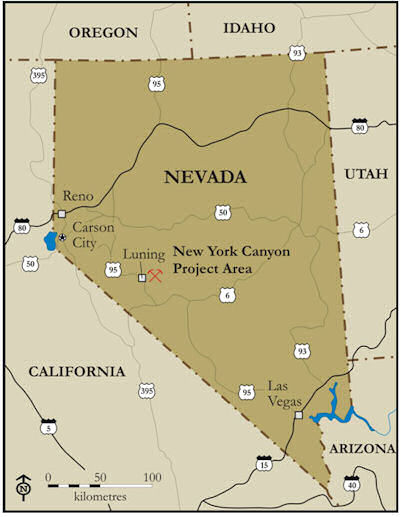

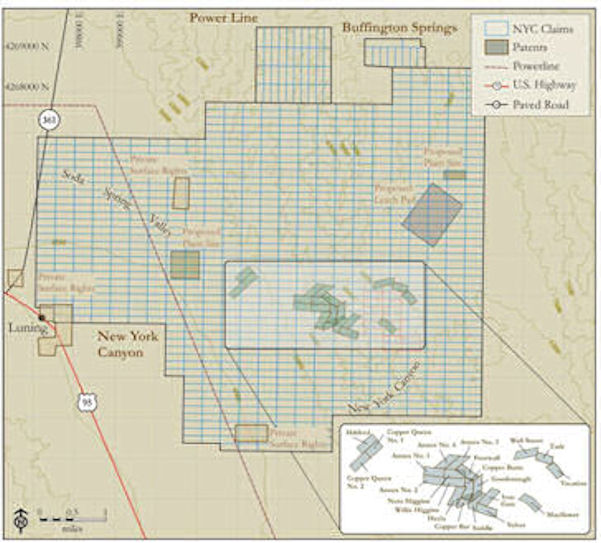

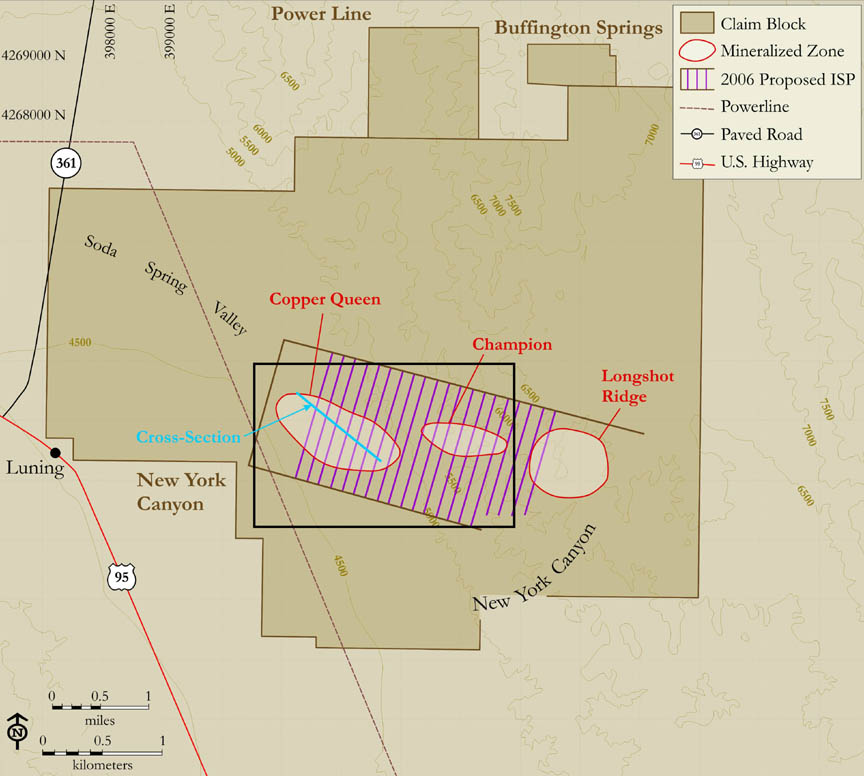

A resource exploration company with a well-advanced copper (both Oxide and Sulphide) and Molybdenum project. The Property lies within the famous Walker Lane Structural Belt of western Nevada, in Mineral County, Nevada, near the town of Luning. Canyon Copper holds a 100% interest in over 1,300 plus mineral claims (21 patented claims and 1,332 unpatented claims) representing approximately 27,000 acres.]

Immediate Corporate Objectives:

-- Develop a bulk tonnage Copper and Molybendum property in a 5km x 3 km mineralized belt.

-- Aggressive drill program to expand current NI 43-101 resource.

-- Acquisition of neighboring properties with significant resources.

-- Aim to establish a 2 billion lb. copper / molybdenum/gold resource and become a near-term producer.

MARKET CAP ~ $20,436,240 ($.33)

SHARE STRUCTURE (8-3-11):

Authorized Shares = 74,785,143

Outstanding Shares = 69,396,934

Held by Insiders = ~ 85%

Options Outstanding = 3,548,434 $0.27

Float = 15,800,000

AWAITING:

1. Marketing campaign targeting brokerage houses in Canada.

2. 3-5 drill units on site.

3. Hiring of new geologist for site management.

4. Property reassessment of core samples for value.

Revise Longshot Ridge resource estimate incorporating re-assayed values of 2006 drill & systematic road cut samples.

5. Apply for permit to dril on & around Longshot Ridge & adjacent copper oxide targets.

5. Apply for permits to drill Copper Queen & Champion target areas.

5. Assess potentials of copper oxide systems similar to the Longshot Ridge at the nearby Power Line & Buffington mine workings.

5. Initiate further work on metallurgical testing & environmental base line studies for Longshot Ridge deposit.

5. Pre-feasibility study.

6. Feasibility study.

7. Production (not restricted by season changes).

8. US uplisting to AMEX.

9. Acquisition of neighboring properties w/ significant resources around existing site in near future.

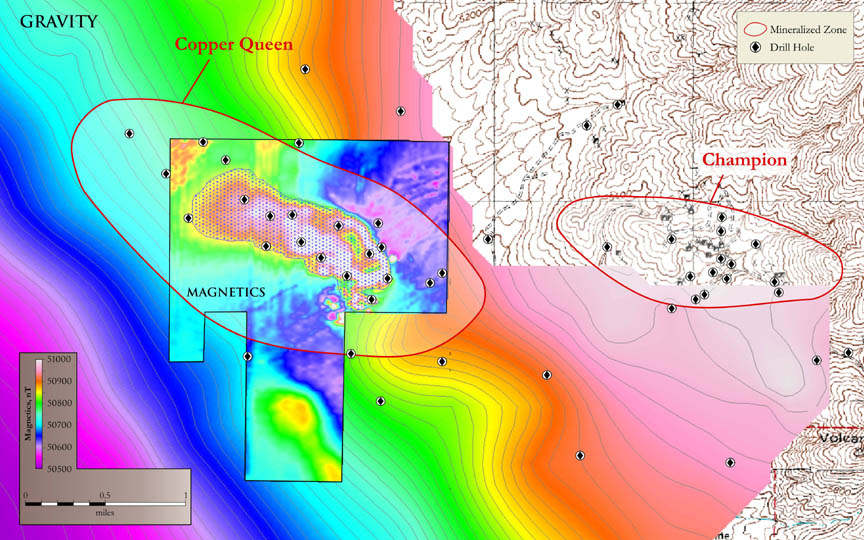

____Location of CNYC Project Area in Nevada____________Map of CNYC Claims: 1,353 mineral claims, 27,000+ acres

Identification 3 Primary Mining Zones: 1,353 mineral claims, 27,000+ acres

1. COPPER QUEEN – on the west.

Has no exposed mineralization at surface, but contains Cu sulfide skarn at depth and an incompletely confirmed Cu-molybdenum sulphide porphyry system at greater depth.

2. CHAMPION – in the center.

Numerous widespread exposures of copper skarn mineralization, both in surface outcrop and abundant old mine workings.

Picture of Copper Queen and Champion Mineralized Zones

3. LONGSHOT RIDGE – on the east.

Numerous widespread exposures of copper skarn mineralization, both in surface outcrop and abundant old mine workings.

Majority of recent exploration efforts have been focused on extensive oxide Cu skarn mineralization at this location.

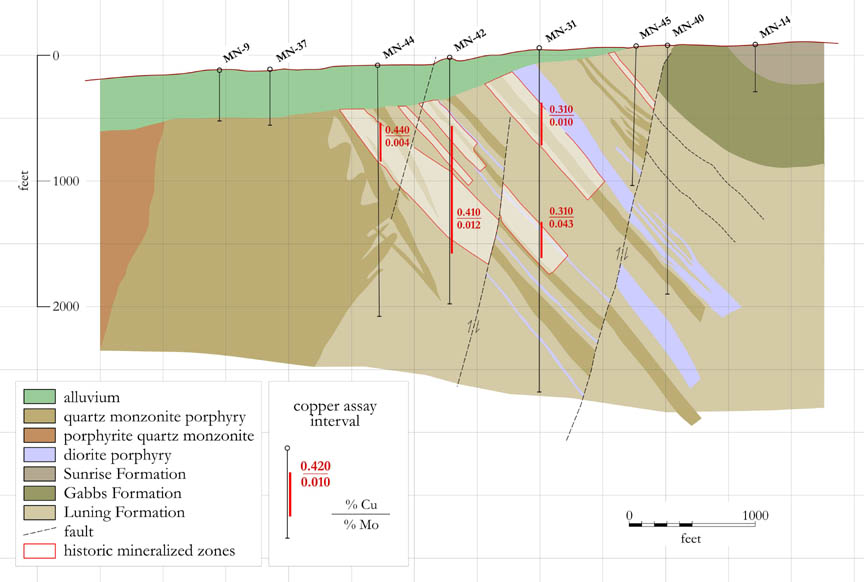

Formation: The Cu mineralization and associated alternation here at Longshot are projects of an extensive Cu-rich skarn system formed in carbonaceous sediments of the Luning, Gabbs and Sunrise Formations. Small amounts of Cu occur also in stockwork veinlets in felsic porphyry intrusive sills and dikes. The Cu mineralization consists almost entirely of secondary copper minerals, principally malachite, axurite, chrysocalla, and copper wad, in order of abundance. Additionally, some Cu-rich limonite (goethite) has been reported.

Deposit centralization: About 90% of the Longshot mineralization is within the 2 upper units of the Gabbs Formation. Drilling reveals that the strongest, thickest, and most continuous mineralization occurs in a NE-trending zone, 200’ W x 1300’ L, which is crossed by 2 NW-trending structurally-controlled high-grade zones, each about 100’ W and from 400-700’ L.

3-D Video of Cu Occurrence at Longshot Ridge – IMPRESSIVE -- http://www.canyoncc.com/s/NYCLongshot.asp?ReportID=439242

2004 Drilling Results, Longshot Ridge

-- Completed 2 diamond drill holes on Longshot: Drill hole 04-01 intersected 193’ of 0.547% Cu (from 20’ – 213’) including 50’ of 0.827% Cu (from 80’ – 130’). This hole ended in strong Cu mineralization.

-- Drill hole 04-03 was a vertical hole drilled to a depth of 43’. While drilling the hole, it was recognized that previousl drill holes in the vicinity had encountered significant mineralization at the contact of the overlying oxidized Gabbs Formation and the underlying Luning Formation, and this hole was extended to test this target. This drill hole (04-03) intersected 370’ of 0.314% Cu (from 25’ – 395’) including 140’ of 0.549% Cu (25’ – 1.65’.) and 35’ of 0.709% Cu (70’ – 105’).

Picture of Longshot Ridge drilling hole 04-03 and Copper Oxide Cores

Picture of Longshot Ridge

Site Picture

Site Picture – Core Drilling

PRINCIPALS:

Anthony R. Harvey, CEO, COB

Member of Advisory Board, Audit Committee and Disclosure Committee

Benjamin Ainsworth, President, Secretary, Director

Member of Disclosure Committee

Kurt Bordian, CFO, Treasurer

Member of Disclosure Committee

James Yates, Director

Over 25 years experience in mineral exploration and has served as director and officer of several public mining companies, such as ESO Uranium (TSX-V: ESO), and Nevada Geothermal power, Inc. (TSD-V: NGP).

Bryan Wilson, Director

Over 18 years varied career in fields of mining exploration and dvpmt, and 12 years in fin’l svcs.

Chris Broili, Project Mgr., NY Canyon Exploration project

Member of Disclosure Committee

HISTORICAL:

9-28-11 – 10K

-- CNYC has funding for proposed exploration program and continued operations ($1,090,000) for next 12 months, which includes 2011 – 2012 unpatented claim maintenance fees and monthly payments on patented claims, re-assay 2006 Longshot Ridge drill pulps, metallurgical sampling + testing, environmental base line study work, geological mapping.

-- Anticipates continuing to rely on sale of common & loans to continue funding business operations, incl. dilution, for Phase II.

9-12-11 – Listed by Stock Catalysts

7-15-11 – Canyon Copper completes Brokered Private Placement + Final Tranche of Non-brokered Private Placement.

Also made available on Canadian News Wire.

-- Brokered PP – issued 2,164,071 units @ CDN $.035 = $757,425.

-- Non-brokered PP – issued 857,142 units @ CDN $.035 = $300,000.

-- Warrants 1,510,606 @ CDN $0.50.

-- Brokered Warrants exercise restriction on transfer 11-14-11; to 1-13-13.

-- Non-brokered Warrants exercise restriction on transfer to 11-9-11; to 1-8-13.

-- May accelerate expiry date of warrants if CNYC’s shs close at price = $0.50 for 10 consecutive days providing 30 days notice of acceleration.

-- MGI Securities commission CDN $45,445; issued non-transfer options to purchase aggregate of 129,844 units @ CDN $0.35 per unit to selling group members.

7-11-11 -- Form 4

On 7-8-11, ARH Mgmt, Ltd. (CEO Anthony R. Harvey company) acquired 857,142 common @ $0.36 = $308,571.12.

Warrants (right to buy) 428,571 common @ $0.52

5-26-11 – Statement of Changes in Beneficial Ownership of Securities

5-17-11 – 8K – Milton Datsopolous resigns as member of Board of Directors

No disagreement with company.

5-16-11 – 8K – Unregistered Sale of Equity Securities, Fin’ls., + Exhibits

Reports non-brokered foreign Private Placement of May 11, 2011.

5-14-11 – Financials – March 31, 2011

5-12-11 – News – Canyon Copper Completes First Tranche of Non-Brokered Private Placement

5-11-11 – Non-Brokered Private Placement (rpt’d. in May 16, 2011 8K)

1. Issued 3,206,602 units @ $0.35 CDN per Unit = $1,112,310.70 CDN.

2. Each unit consists of 1 sh common stock (“Share”) and ½ share non-transferable purchase Warrant (“Warrant”).

3. Each whole Warrant entitles the holder to purchase an add’l Share of the Corporation at a price of $0.50 CDN / Share until November 10, 2012.

4. Company may accelerate expiry date, the accelerated expiry date w/b 30 days after the Company sends out notice of acceleration.

5. Company did not engage in a distribution of this offering in the US.

6. Share issuance represents the first tranche of the Company’s previously announced non-brokered foreign PP offering. Proceeds of offering w/b used to fund the Company’s exploration program on the New York Canyon Project, as well as for gen’l working capital and corporate purposes.

7. Also issued 142,857 units @ $.035 CDN per Unit for total proceeds of $50,000 CDN to a director of the Company.

5-10-11 – 10Q – March 31, 3011

4-6-11 – 8K – Conditional Approval to List as Tier 1 Mining Issuer

4-4-11 – News – CNYC Announces Conditional Approval to List on TSX Venture Exchange

3-4-11 – Telecon – Rigatoni interpretation of telecom w/ CEO, Anthony Harvey

-- He was hired to come in + clean up company; he fired all previously involved; company did a reverse to clean out bad management.

-- He has 50 years in mining business.

-- He has put 19 mines into production.

-- He has put 3 oil and gas projects into production.

-- He has worked on projects in 15 countries.

-- Just based on 43-101 report, they have a big property with huge potential.

-- Conoco did the original drilling and he bought all the data.

-- He said they increased the acreage and now think, hypothetically, they have 1.5 billion lbs of Cu and that would have been proven out with additional drilling to become accurate.

-- He knows institutions who own stock, and they won’t be selling for a long time, in his opinion.

-- Expecting listing at any time in Canada, rated Tier 1 upon application. No guarantees.

-- Potential future financing done for small amount, maybe 2.5 mil. Much higher than current stock price (IMO).

2-12-11 – Financials – Q4 2011

2-9-11 – 10Q – Q4 2011

1-31-11 – 8K – Regulation FD Disclosure, Fin’l Stmts + Exhibits

1-27-11 – News – Canyon Copper Announces Private Placement + Sponsorship Engagement Letter w/ MGI Securities, Inc.

1-27-11 – News – CNYC Announces Brokered Private Placement Offering of Units

http://biz.yahoo.com/e/110131/cnyc.ob8-k.html

1-21-11 – 8K, Entry into MDA, Regulation FD Disclosure, Fin’ls.

http://biz.yahoo.com/e/110121/cnyc.ob8-k.html

1-19-11 – News – CNYC Announces Private Placement Offering of Units

http://finance.yahoo.com/news/Canyon-Copper-Corp-Announces-iw-300850032.html?

11-29-10 – 8K, Entry into MDA, Amendments to Articles

http://biz.yahoo.com/e/101129/cnyc.ob8-k.html

11-24-10 – News – CNYC Announces Effectiveness of 79-for-100 Reserve Stock Split

http://finance.yahoo.com/news/Canyon-Copper-Announces-iw-1342808054.html?x=0&.v=1

11-15-10 – News – CNYC Corporate Overview

http://finance.yahoo.com/news/Canyon-Copper-Announces-iw-1342808054.html?x=0&.v=1

11-1-10 – 10Q

http://biz.yahoo.com/e/101101/cnycd.ob10-q.html

10-28-10 – News – CNYC Announces Approval for 79-for-100 Reverse Stock Split

Reverse split done in order for its capital structure to conform to capital structure requirements of TSC Venture Exchange, decreasing authorized capital of common stock from 166,666,666 shs (par $.00001/sh) to 131,666,666 shs ($.000001/sh), and issued and O/S common stock reduced from 78,39066,666 shs ($.000001/sh), and issued and O/S common stock reduced from 78,39,307 shs to 6,928,343 shs.

http://biz.yahoo.com/e/101101/cnycd.ob10-q.html

10-13-10 – 8K, Entry into MDA, Fin’l Stmts + Exhibits

http://biz.yahoo.com/e/101101/cnycd.ob10-q.html

9-28-10 – 10K, Annual Report

http://biz.yahoo.com/e/100928/cnyc.ob10-k.html

8-25-10 – 8K, ? of CPA, Fin’ls + Exhibits

http://biz.yahoo.com/e/100825/cnyc.ob8-k.html

5-31-10 – News – CNYC Announces NI 43-101 Indicated + Inferred Resources on Longshot Ridge Copper Skarn Deposit at New York Canyon Project

http://biz.yahoo.com/e/100825/cnyc.ob8-k.html

4-6-10 – NI 43-101 Technical Report on New York Canyon Project, Nevada

http://sedar.com/GetFile.do?lang=EN&docClass=24&issuerNo=00027554&fileName=/csfsprod/data107/filings/01576633/00000001/v%3A%5CCanyonCopper%5CSEDAR%5C0003217_tech_May6_2010%5Cfiled%5CCanyonCopper_TechReportmay6.pdf

CAVEAT: The entirety of the above was compiled by and contains opinions of this user, and is not to be relied upon. Do your own due diligence.

TWDL

Expecting geo reorts from RJ Johnson PG/CEM Mid-Oct and Nov

Low float 34 million

Book value .34

http://www.otcmarkets.com/stock/TWDL/news/TWDL-Signs-Agreement-With-Geologist?id=34275&b=y

TWDL

Thanks for your due diligence Bio.

There are 2 sites that suggest KATX is a buy:

http://ih.advfn.com/videos/stock-chart/katx-annotated-video-chart_galbd0T8PgE

http://americanbulls.com/StockPage.asp?CompanyTicker=KATX&MarketTicker=OTC&TYP=S

Good luck to KATX investors.

SFEG is a junior producer, stock is at $1 now, should trade up from here in a big way. $10 should be easy, $20 is possible.

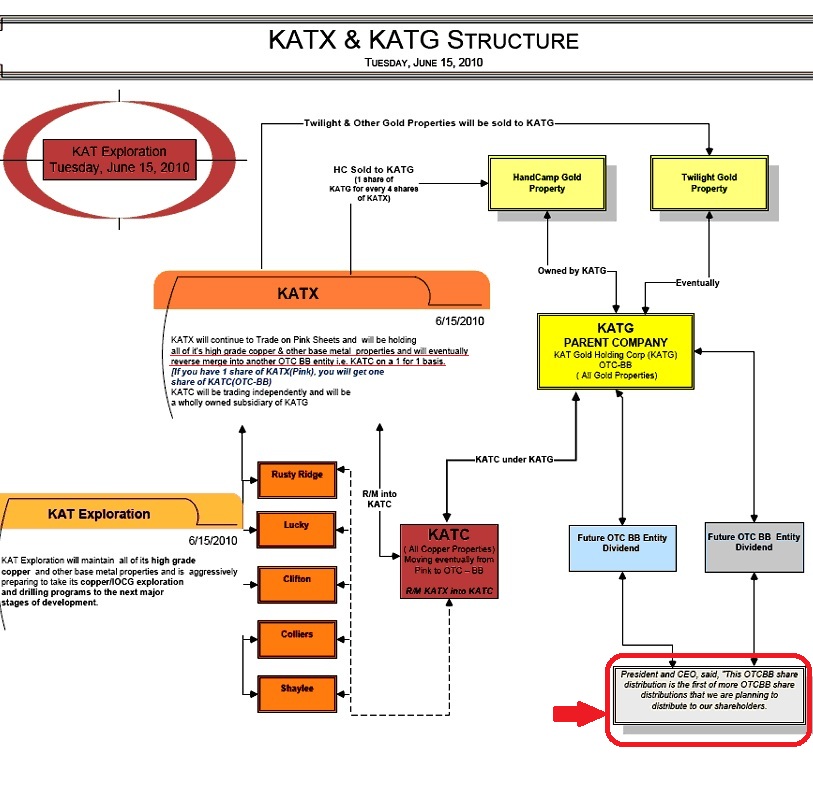

NEWS! UPDATED KATG & KATX DD AS OF August 31, 2010

NEWS! NEWS! AND MORE NEWS! LOTS OF DRILLING AND MORE SHARE DISTRIBUTIONS COMING TO KATX and KATG SHAREHOLDERS!

KAT EXPLORATION’S PRINCIPLE OBJECTIVE:

About Kat Exploration Inc

Kat Exploration's principal objective is to locate, stake, prove up and sell mineral properties to major mining companies. It is the Company's objective to take advantage of increased activity to generate numerous joint venture clients, and sales of our existing and yet to be acquired properties.

http://finance.yahoo.com/news/Kat-Exploration-Announces-pz-2721659684.html?x=0&.v=2

KATX will reverse merge into OTCBB KATC at a 1:1 ratio.

KAT Exploration shareholders will receive 1 restricted share of (OTCBB: BVIG) [now named KATG] for every 4 shares of (PINKSHEETS: KATX) owned up through the record date [July 16, 2010]...

Ken Stead, KAT Exploration, Inc. President and CEO, said, "This OTCBB share distribution is the first of more OTCBB share distributions that we are planning to distribute to our shareholders...

"KAT Gold Holdings Corporation" [KATG] will be the parent company for all future OTCBB share distributions...

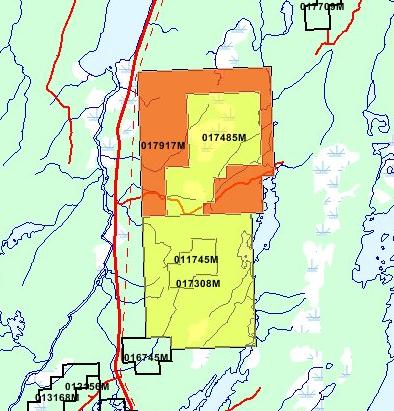

http://www.marketwire.com/press-release/KAT-Exploration-Inc-Distributes-1-4-OTCBB-Shares-BVIGOB-Provides-Update-on-Handcamp-1272825.htm

"KAT Exploration believes that because of the expected valuation that will come from its Handcamp and other high grade gold properties recently discovered that it would be better suited to position the properties within a higher market standard existing within a fully reporting OTCBB entity.

The new name for Bella Viaggio, Inc. will be "KAT Gold Holdings Corporation" that will be the parent company for all future OTCBB share distributions. The goal is to later merge (PINKSHEETS: KATX) into an OTCBB entity under KAT Gold Holdings Corporation as a wholly owned subsidiary on a 1 for 1 ratio basis."

http://www.marketwire.com/press-release/KAT-Exploration-Inc-Distributes-1-4-OTCBB-Shares-BVIGOB-Provides-Update-on-Handcamp-1272825.htm

"...Our investor's relation department felt it would be advantageous to post a Flow Chart on our web site under 'Properties,' to clarify the present structure and the future direction of the company. President and CEO Ken Stead stated, "We are working hard to build shareholder value in both of our companies and is in a process of taking all our high grade copper and other IOCG properties under KAT Exploration to the next major stages of development."

http://www.marketwire.com/press-release/KAT-Exploration-Initiates-Drilling-Program-on-Rusty-Ridge-IOCG-Property-1277037.htm

Plan of Operation

...management will initially concentrate on increasing its exploration of the Property [Handcamp] and other gold properties and, if any such other properties other than the Property are identified, seek to ascertain the value of these properties with a view to their acquisition. Management believes that further in-depth exploration on such properties, if found and acquired, is a critical factor in enhancing the Company’s ability to discover minerals, if any, at such properties. If potentially valuable sources of minerals are identified, the Company will perform a feasibility study of the properties and then seek to sell them to one or more of the major mining companies. Management hopes that this strategy will enable the Company to achieve long-term sustainable growth.

Sales and Marketing

Management believes that its customers consist essentially of other mining companies looking for properties to include in their mining and production programs. Management believes that its relationship with certain of the potential customers [its relationship w/ certain mining companies] will assist the Company in implementing its business plan.

http://www.otcmarkets.com/edgar/GetFilingHtml?FilingID=7409441

During this time, management anticipates that the Company will also be developing additional information on the Property [hence the current drill program] and any other properties it is able to acquire. If management succeeds in doing so and further believes that market prices for the minerals will justify the activity, the Company will seek to enter into joint venture arrangements with, or sell all or a part of its interest in the properties to certain parties such as major mining companies. Management hopes that the Company’s strategy will enable it to recoup its investment and generate capital to enabling it to expand its business and thus increase shareholder value.

The Company explores for gold deposits in the province of Newfoundland, Canada and has plans to expand operations throughout North America.

Management of the Company intends to focus on gold properties with a view to purchasing all or a portion of already producing gold mines, provided that the requisite financing can be obtained by the Company.

Drill rigs are not called “truth machines” for nothing. No amount of promotion or favorable press will prevent companies from being affected by negative assay results when good ones were anticipated. A selloff takes place immediately, with sophisticated players leading the way. That is why it is important for investors to understand the economic significance of drilling results, relative to the nature of the deposit being explored and where it is situated, You do not want to be the one buying when others are selling, and vice versa.

The first step to analyzing these results is to understand what grades will be economic in a typical mining operation. In general, large deposits capable of being mined by open pit will have lower cutoff grades than will deposits of the same metal that have to be mined by underground methods. For example, the Dome gold mine in northern Ontario operates an open pit with reserves grading 2.3 grams per tonne; its underground reserves grade 4.3 grams.

A 30 meter-drill intersection grading 1 gram gold per tonne, starting at 5 meters below surface, would be of economic interest if it originated from a road-accessible property in Nevada. The state has numerous low-grade deposits mined by less costly open-pit methods, whose gold is recovered by low-cost heap leaching. However, this same drill intersection would not attract much interest on a property in remote northwestern British Columbia owing to a lack of roads and other infrastructure.

A drill intersection showing 0.4% copper would be exciting in the porphyry-copper district of British Columbia, since it approaches the typical grade of the area’s large open-pit mines. In the volcanic belts of northern Ontario, where smaller, higher-grade base metal mines are the norm, the same result would merely merit more work.

Deposits with complex metallurgy will be more costly to mill, so cutoff grades rise accordingly. Off-site costs such as transportation are a major component of total production expenses. This is particularly true for gold and base metal deposits that produce concentrates, which must be shipped to a smelter for processing. Energy costs have a strong influence on a potential operation’s economics, especially when a mill must be built. As a general rule, a mineral deposit in an area where access is poor and costs are high will be less likely to make a mine than an equivalent deposit in a more developed region.

The length of drill intersections is also important, since these give an indication of the kind of mineralization present. Low-grade deposits must be large enough for bulk mining. That means low-grade drill intersections must be long — on the order of tens to hundreds of meters — to show economic potential.

Narrow intersections, on the other hand, must show high grades. A zone’s width is vital to the feasibility of mining operations, and narrow zones may simply not be economic to mine. A mineralized zone only a fraction of a meter wide could not be mined without also extracting large amounts of wall rock, thereby diluting the grade.

Core lengths quoted in press releases can also be misleading. Drill holes that cross a zone of mineralization at nearly a right angle give a better picture of the zone’s true width. Holes that are drilled at shallower angles to the mineralized zone will yield intersections with lengths much greater than the true width of the mineralization.

Keep in mind that a hole drilled to a great depth from surface will often be drilled at a very steep angle, such that if it intersects nearly vertical structures at depth, the true width will be much less than the length of the drill intersection.

There is always the possibility that the company has drilled down the dip or plunge of a mineralized zone rather than across it. This can happen, on occasion, in the early stages of an exploration project when the structure being explored is still poorly understood. A hole drilled in this way will provide no information about the width of the zone, yet the mineralized intersections may run to spectacular, but meaningless, lengths.

Lastly, it is important to consider that narrow zones of high-grade mineralization may carry an intersection. A zone only a meter wide may show a grade of 15% zinc, but a company may average that one-meter intersection with the nearly barren two meters to each side of it, reporting five meters grading 3% zinc.

http://www.miningbasics.com/why-wait-drill-results-junior-mining-company

KAT Exploration, Inc. and Bella Viaggio, Inc. Handcamp Drilling Intersects Very Encouraging Gold Mineralization at Shallow Depths

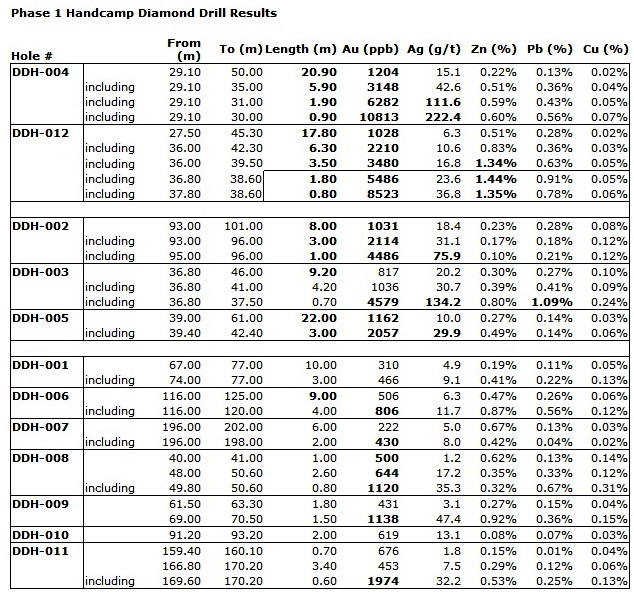

KAT Exploration, Inc. (PINKSHEETS: KATX) and Bella Viaggio, Inc. (OTCBB: BVIG) are pleased to announce that the drilling program at their Handcamp Project intersected very encouraging gold mineralization at shallow depths. Diamond drill hole DDH 004 intersected 6.3 g/t (0.18 oz./ton) gold and 111.6 g/t (3.3 oz./ton) silver over 1.9 m (1.4 m estimated true width) including 10.8 g/t (0.32 oz./ton) gold and 222.4 g/t (6.5 oz./ton) silver over 0.9 m (0.7 m estimated true width) within a wider interval grading 3.1 g/t gold and 42.6 g/t silver over 5.9 m (4.4 m estimated true width).

Diamond drill hole DDH 012 intersected 5.5 g/t (0.16 oz./ton) gold over 1.8 m (1.4 m estimated true width) within a wider interval grading 3.5 g/t gold (0.10 oz./ton) over 3.5 m (2.6 m estimated true width). Both intersections occur within an even broader mineralized zone defined by elevated gold that includes 1.2 g/t gold over 20.9 m (15.6 m estimated true width) in DDH 004 and 1.0 g/t gold over 17.8 m (13.3 m estimated true width). Three other holes (DDH-002, 003 and 005) also intersected strong gold mineralization over wide widths as shown in the summary table. The gold is typically accompanied by elevated silver, lead and zinc.

Results of the current exploration program indicate that the mineralized zone at Handcamp is outlined well by induced polarization geophysics. The current drilling program tested the mineralized zone for approximately 0.9 km along strike (trend) at 250m to 300m spaced intervals and to a maximum vertical depth of 200 m. DDH 012 is the southwestern most drill hole of the current program and is approximately 600m southwest of the main Handcamp showing. During the second phase of exploration, the mineralization in DDH 012 will be tested to depth and along strike to the northeast and southwest where the IP anomaly has been traced a further 500 m and remains open. Two other induced polarization anomalies subparallel to that delineating the Handcamp mineralized zone remain to be tested by diamond drilling. One, about 350 m to the northwest, has been traced for 1.2 km and remains open and the second is about 900m to the northwest, and has been traced for 700 m and remains open. The two anomalies are viable targets for testing in the second phase of exploration.

Trenching completed at four locations north and south of the Main Hand Camp prospect exposed disseminated sulphide mineralization in altered volcanic rock that contains anomalous gold, silver, lead and zinc concentrations over an approximate strike length of 600 m and over widths of up to 20 m in trenched rock exposures.

Ken Stead, President CEO, states, "The first phase of exploration, which included induced polarization geophysics, trenching and 1640m of diamond drilling in 12 drill holes, has now been completed on the Hand Camp Property. A second phase starting this fall is in planning and will include additional line cutting, induced polarization geophysics and diamond drilling. With data collected so far and the very encouraging results from this first phase, the company feels that this project warrants a full scale exploration program to determine the true significance of the deposit. With just four areas drilled at such wide intervals within such a large structure and the fact that we intersected gold in all 12 drill holes, we feel there is high potential for further encouraging results within this mineralized structure. Also the number of targets yet remaining to be tested outside this determined structure lends itself to a high degree of optimism that this project will be of great value to the company."

Geochemical analyses and assay data consistently and routinely return anomalous gold, silver, lead, zinc and copper values over considerable widths. As an added bonus the distribution of these elements is uniform in comparison to many gold deposits that are subject to the nugget effect enhancing the potential for the delineation of economic concentrations of polymetallic mineralization.

The Company's exploration work on the Handcamp Project is supervised by J. Wayne Pickett, M.Sc. P.Geo., a member of the Professional Engineers and Geoscientists of Newfoundland and Labrador and a Qualified Person as defined in NI 43-101. Mr. Pickett has verified that the results presented above have been accurately summarized from the official assay certificates provided to the Company.

http://www.marketwire.com/press-release/KAT-Exploration-Inc-Bella-Viaggio-Inc-Handcamp-Drilling-Intersects-Very-Encouraging-1309659.htm

Jul 29, 2010 10:25 ET

KAT Exploration and Bella Viaggio, Inc. Welcome "Senior Vice President of Capital Projects" to Board of DirectorsMOUNT PEARL, NEWFOUNDLAND--(Marketwire - July 29, 2010) - KAT Exploration Inc. (PINKSHEETS: KATX) (www.KATexploration.com) and Bella Viaggio, Inc. (OTCBB: BVIG) are very pleased to announce that J. Wayne Pickett has agreed to join the companies as a director and "Senior Vice President of Capital Projects." Mr. Ken Stead, CEO, commented that "on behalf of the board of directors, we are delighted to have someone with this caliber of a geological background to oversee all the company's projects as we move forward ever so rapidly." All present and future geologists along with field crews will work under the direction of Mr. Pickett.

Please check the link for Mr. Pickett's resume.

http://www.katexploration.com/PressReleases/Wayne%20%20Pickett%20Resume%202010.pdf

Also, on June 26th, 2010, 77 new claims were staked around the most Northern claims of the Handcamp property as more new discoveries have been found. This latest discovery is approximately 2 kms to the North of the main Handcamp showing and appears to be an extension of the latest north western anomalies recently discovered through Induced Polarization (IP). This mineralized zone contains very impressive massive sulfides and samples have been sent to the lab for gold and base metal analysis. No drilling or trenching has taken place in those new areas thus far but will be part of another drill phase as we continue to move the project forward.

See attached pictures.

Nine drill holes have been completed to date with all holes intersecting mineralization. Hole #7 tested the mineralized structure at 180 meters (612ft) down section and intersected mineralization over a width of 30 meters. This is extremely encouraging as we now know that, not only does the strike length of the mineralized structure continue for at least a minimum of 1400 meters and open at both ends, it has a minimum depth of 180 meters and also open at depth. With new mineralized structures being discovered to the west and far north, this increases the potential of the property significantly.

Results are beginning to be received from the lab and Jim Weick along with Wayne Pickett will begin the compilation of these results which will be published in an upcoming press release.

http://www.marketwire.com/press-release/KAT-Exploration-Bella-Viaggio-Inc-Welcome-Senior-Vice-President-Capital-Projects-Board-1297501.htm

KAT Exploration and Bella Viaggio, Inc. Updates Investors on Its Handcamp Drill Project

MOUNT PEARL, NEWFOUNDLAND--(Marketwire - July 22, 2010) - KAT Exploration, Inc. (PINKSHEETS: KATX) and Bella Viaggio, Inc. (OTCBB: BVIG) are very happy to inform shareholders of the ongoing first phase drill program on its Handcamp high grade Gold property.

To date six (6) holes have been completed with the seventh in progress. All six holes have intersected the mineralized zone as outline in soil sampling, Induced Polarization(IP) and trenching. The purpose of the holes was to test mineralization near surface and at depth.

All holes have been drilled at an azimuth of 110 degrees perpendicular to the northeast strike of the 1.4 km structural zone that hosts Hand Camp mineralization.

As the first two drill holes, DDH-001 and DDH-002 were located on the same setup on line 2+00 South approximately 50m west of the Main Trench Showing (Trench #1).

DDH-001 drilled at a dip of-45 degrees intersected mineralization from 68.0m to 79.0m for a total width of 11.0m (37.4ft).

DDH 002 completed at a dip of-65 degrees intersected mineralization from 93.0m to 102.5m a total width of 9.5m(32.3ft).

As the third drill hole, DDH-003 was drilled at a dip of-45 degrees on line with DDH-001 and 002, approximately 25m from the Main Trench as a check on the consistency of mineralization from surface to DDH-001 and 002. It intersected mineralization from 36.0m to 49.0m over a total width of 11.0m(37.4ft).

The fourth and fifth holes DDH-004 and DDH-005 were completed on the same setup approximately 200m north of drill line DDH-001, 002 and 003 approximately 25m west from the Main Hand Camp showing.

DDH-004 completed at a dip angle of-45 degrees intersected mineralization from 29.1m to 45m over a width of 18.9m(64.3ft).

DDH-005 drilled from the same setup at an angle of-65 degrees intersected mineralization from 39.4 to 82.6 a total width of 43.2m(146.9ft).

A sixth hole, DDH-006 recently completed at a dip angle of-45 degrees, 50m west of DDH-004 and DDH-005 intersected mineralization from 118m to 151m a total width of 33m(112.2ft) at a vertical depth of approximately 100m(340ft).

The seventh hole, DDH-007being drilled from the same setup at a dip angle of-65 has been designed to test for the continuation of this mineralization down dip at a vertical depth of approximately 120m (408ft)... at a greater vertical depth than all previous drilling.

Zone #1 where the first 3 drill holes took place still show that mineralization continues at depth and will require deeper testing to determine the true depth of this area of the structure.

Zone # 2, 200m north of zone #1, where the latest 3 drill holes took place, showed even greater width at greater depths and is now being tested by DDH-007 to see if the mineralization continues.

President/CEO Ken Stead commented "We are very pleased and excited with the drill program thus far and we look forward to the lab results determining the gold and base metal contents. One would have to understand the significances of these drills holes hitting mineralization at such depths and width, with already known gold showings on surface above the drilled areas. And taking into consideration the amount of mineralization discovered along with the limited amount of drilling in comparison to the known depth and 1400m strike length of the mineralized structure, lends itself to huge potential for the Handcamp property.

Mr. Stead further states, "Samples from most of the holes drilled thus far have been logged and sent to the lab with a request to expedite analytical results. We will let our shareholders and investment community know as soon as we have the results from the lab."

http://www.marketwire.com/press-release/KAT-Exploration-Bella-Viaggio-Inc-Updates-Investors-on-Its-Handcamp-Drill-Project-1294326.htm

KAT Exploration and Bella Viaggio, Inc. Updates on Handcamp Geophysics and Drill Project

MOUNT PEARL, NL--(Marketwire - June 29, 2010) -

...Due to the latest discoveries of several new very strong IP targets the company has decided to engage the services of another geologist and geophysicist to work along with Mr. R. James Weick on laying out a very constructive drill program. These discoveries have created a much bigger work load and latest trenching has uncovered extensive amounts of sulphides over a strike length of 700 meters.

Some of the bigger targets extend west of the grid and south of where the geophysics ended. Therefore, the company has decided to extend the latest geophysics in both of these areas as it was recommended by the geophysicist who did the interpretation of the first round of geophysics.

Ken Stead, President and CEO, stated, "The more work we do, the more new discoveries are being found, all of which causes us to take a serious look at other areas of the property too… it has been requested that the contractor leave his excavator on site because we feel very strongly that after the extended geophysics are completed there will be many other areas that will need trenching and quite possibly drilling."

Shareholders will be informed immediately upon the first turning of the drills.

http://www.marketwire.com/press-release/KAT-Exploration-Bella-Viaggio-Inc-Updates-on-Handcamp-Geophysics-Drill-Project-1283494.htm

KAT Exploration and Bella Viaggio, Inc. Commence Drilling on Handcamp Gold Property

MOUNT PEARL, NEW FOUNDLAND--(Marketwire - July 6, 2010) - KAT Exploration, Inc. (PINKSHEETS: KATX) www.katexploration.com

KAT Exploration, Inc. (PINKSHEETS: KATX) and Bella Viaggio, Inc. (OTCBB: BVIG) are pleased to inform its shareholders & investment community that drilling on the Handcamp high grade gold property has begun today.

The first selected drill targets are taking place over the exposed outcrop known as the "Main Handcamp" showing, where channel samples generated a result of 7.1 g/t gold over 28ft along the surface.

The first series of three holes will be drilled at different intervals down depth. The next series also consists of three down depth holes two hundred meters south of the first drill holes. This is a new area that was discovered during the first round of an IP survey which coincided with gold anomalies in soils. The next series of holes will be in several areas to the north where IP, soils and trenching revealed strong anomalies near surface and at depth along with heavy mineralization in uncovered outcrops. This first phase of drilling will take place within a 1400 meter strike length of a very impressive gold bearing structure.

A second round of an IP survey will be carried out North West of the grid which is showing another large anomaly open to the west. This new target is very large and requires immediate testing to confirm the magnitude and size of the target.

Mr. Dean Fraser P. Geo and a geophysicist (RDF Consulting Ltd.) have been contracted to work with Mr. R. James Weick on the Handcamp project including the second round of geophysics.

President & CEO Ken Stead: "Over the weekend meetings with both geologists and geophysicist for a complete overview of the work thus far has demonstrated some new discoveries which has shed additional light on the potential of the Handcamp project. Like all companies, when a project gets to the stage of drilling, there is always a certain amount of apprehension and uncertainty as to what it will produce. However, the results of the ongoing work have strengthened our feelings to a much higher level of excitement and anticipation."

Qualified Persons

Mr. R. James Weick P. Geo & Mr. Dean Fraser P. Geo and a geophysicist, an Independent Qualified Person as defined by National Instrument 43-101 has reviewed the drill program, supervised the preparation of the scientific and technical information and verified the data supporting such scientific and technical information contained in this news release.

New photographs of the latest trenching have been added to the KAT Exploration website exposing large mineralized zones within the 1400 meters strike length [http://www.katexploration.com/handcamp_trenching.html ].

At certain stages of the drilling program, when results have been obtained from the lab contracted to analyze the drill samples, a press release will inform shareholders of those results.

http://www.marketwire.com/press-release/KAT-Exploration-and-Bella-Viaggio-Inc-Commence-Drilling-on-Handcamp-Gold-Property-1285962.htm

KAT Exploration Discovers up to 5840 PPB of Gold in Soil Samples and 31.4 g/t Au in Outcrop at Handcamp Gold Property

MOUNT PEARL, NF--(Marketwire - March 1, 2010) - KAT Exploration Inc. (PINKSHEETS: KATX) www.katexploration.com --

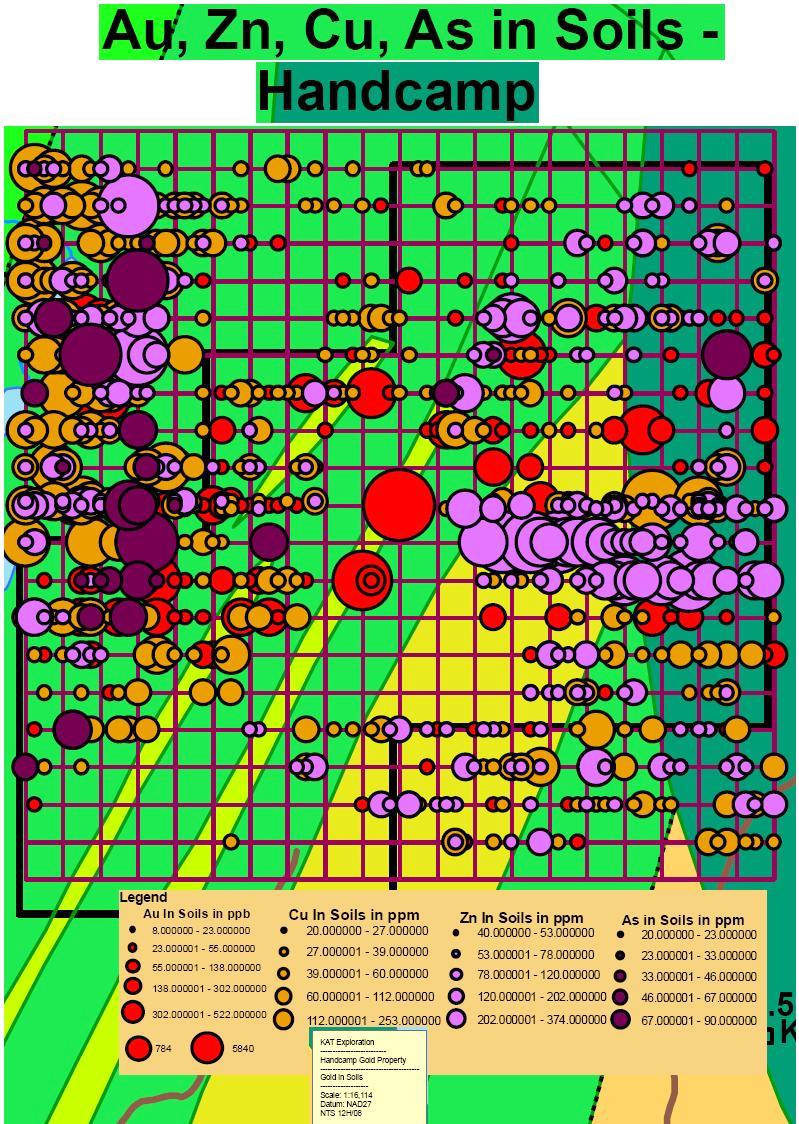

KAT Exploration is pleased to release the results of 1457 soil samples received from Actlabs in Ontario, Canada for Gold and base metal analysis. The results have shown several very impressive anomalies over certain sections of the grid which encompass less than one quarter of the overall property. Soil samples have been digitally plotted by an independent geologist on grid maps that can be viewed at KAT's website www.katexploration.com under the "Handcamp" Property.

To the SE portion of the grid lies a very strong, distinct anomaly of Zinc stretching for over 900m X 300m that would no doubt warrant intense follow up.

To the West and NW portion of the grid is a very large cluster of Copper anomalies extending beyond the western boundary of the grid . This is also very exciting as it leaves the door open for more discoveries. off the grid, yet still on the Handcamp property.

Of most interest to the company and importance to the property is the extent of Gold throughout the western, central and NE parts of the grid. In all three sections where high gold results are located in soils, rock samples have verified gold in the underlying outcrops with the central portion of the grid being particularly impressive, where soil results were as high as 5840ppb Au with 31.4 g/t Au in outcrop underneath this same area…

These main anomalies extend as much as 1 km (1000 meters) from the high grade zones where the first phase of drilling will take place. This demonstrates the significance of how widespread gold and base metals are throughout the property.

http://www.marketwire.com/press-release/KAT-Exploration-Discovers-up-5840-PPB-Gold-Soil-Samples-314-g-t-Au-Outcrop-Handcamp-1193541.htm

KAT Exploration is pleased to release the results of 1457 soil samples received from Actlabs in Ontario, Canada for Gold and base metal analysis. The results have shown several very impressive anomalies over certain sections of the grid which encompass less than one quarter of the overall property. Soil samples have been digitally plotted by an independent geologist on grid maps that can be viewed at KAT's website www.katexploration.com under the "Handcamp" Property [see one digital plot below].

http://www.marketwire.com/press-release/KAT-Exploration-Discovers-up-5840-PPB-Gold-Soil-Samples-314-g-t-Au-Outcrop-Handcamp-1124037.htm

The "Handcamp" is located approximately 33km north of Badger, central Newfoundland and 10km northeast of the old abandoned "Gullbridge" copper mine…Superimposed on the volcanogenic sulphide mineralization is epigenetic disseminated gold mineralization. The best sulphide mineralization is associated with sericite schist with veinlets and dissemination having been traced over a strike length of 1200m…Rock samples were collected over the prospected areas with numerous samples showing very significant mineral content with some gold numbers as high as 158g/t Au, 94g/t Au, 82g/t Au. along with excellent Zn, CU, Ag numbers ( massive to simi-massive sulphides ). A chip sample was cut over the main Handcamp gold showing averaging 7.1g/t Au over 8m (27ft). Due to the world interest in gold, this property will become the focus for Kat Exploration over the next years.

http://www.katexploration.com/properties.html

...Although not generally utilized commercially, deposits of schist may be a valuable commodity if they contain gemstones or metal ores. For instance, talc and mica schists in Upper Egypt have been mined for emeralds for thousands of years and have benefited various people and civilizations throughout history, including the ancient Greeks and the famous Egyptian queen Cleopatra…

Found in various locations, one of the best known examples of quartz-sericite schist occurs in Canada, where it is a source of economically important gold deposits.

http://www.olympusmicro.com/galleries/polarizedlight/pages/schistquartzsericitesmall.html

According to CEO Ken Stead: “[Handcamp] is just south of the new gold processing facility which just opened this year by Anaconda Mining. That in itself is just south of what used to be the Nugget Pond Gold Mine, which is now being operated by Crew Gold and then there’s the Duck Pond Deposit, which is being mined as a massive sulphide deposit, and is a bit to the south also."

Speculation:

Handcamp’s situation so close to existing gold mines and Anaconda Mining’s gold processing facility could make a potential JV with Anaconda a good prospect for both companies.

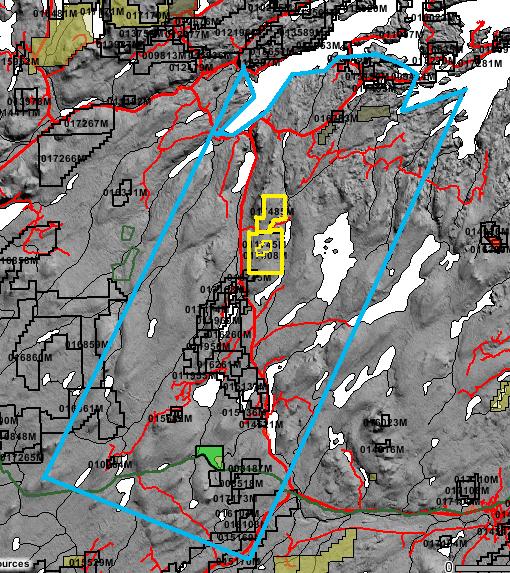

What is also of interest is the fact that Handcamp lies absolutely dead central within an area marked out by the Canadian Government as being of special interest due to its underlying geology, and was given special attention in an air survey of Canada [see next three graphics].

-courtesy of Rick-UK

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=50326084

From: Ken Stead <kstead@katexploration.com>

Subject: Re: Hi Ken QUESTION ???

To: birdmanbob4

Date: Wednesday, March 3, 2010, 3:54 PM

XXX,

Any mining company in the world would just love to get their hands on VMS, it really brings quite a bit of value to each ton of rock mined. Just to the south in the same belt of rocks that the Hand camp is in, is the "Duck Pond" VMS deposit but they do not have near the gold that we have.

Aur Resources Announces Development Decision for the Duck Pond ...

The Duck Pond deposit has proven and probable reserves of 4.1 million tonnes at an average grade of 3.3% Cu, 5.7% Zn, 59 g/t Ag and 0.9 g/t Au. ...

www.encyclopedia.com/doc/1G1-126132569.html

Ken

From: birdmanbob4

To: Ken Stead

Sent: Wednesday, March 03, 2010 6:38 PM

Subject: Re: Hi Ken QUESTION ???

...I am wondering about the mines and companies close to us are they geared to process the other minerals as well like the copper and Zinc...or am I correct in my thinking that Vale has a Processing place on the mainland that is geared best for the "Multi Mineral" thing? ...In other where is the best place to take our dirt?...

The truth will set you free!

From: Ken Stead <kstead@katexploration.com>

Subject: Re: Hi Ken QUESTION ???

To: birdmanbob4

Date: Wednesday, March 3, 2010, 4:11 PM

The Duck Pond refinery is best suited for this

Ken

From: kstead@katexploration.com

To: xxxxxxx

Subject: XXXX

Date: Wed, 3 Mar 2010 05:04:47 -0330

XXXXXXX,

Everything seems to be going as planned and we are excited with the Handcamp thus far and believe we will continue to be excited as we move forward. The Twilite will also receive a very thorough exploration program this year as well. However, where we have advanced the Handcamp to the drill stage, right now it has become our main focus and as the exploration season unfolds the Twi-lite will get due attention. Thanks for supporting us, we are working hard on your behalf.

Ken Stead

President/CEO

KAT EXPLORATION INC

O-(709) 368-9223

O-(709) 368-9224

F-(709) 368-9213

Email: kstead@katexploration.com

Website: http://www.katexploration.com

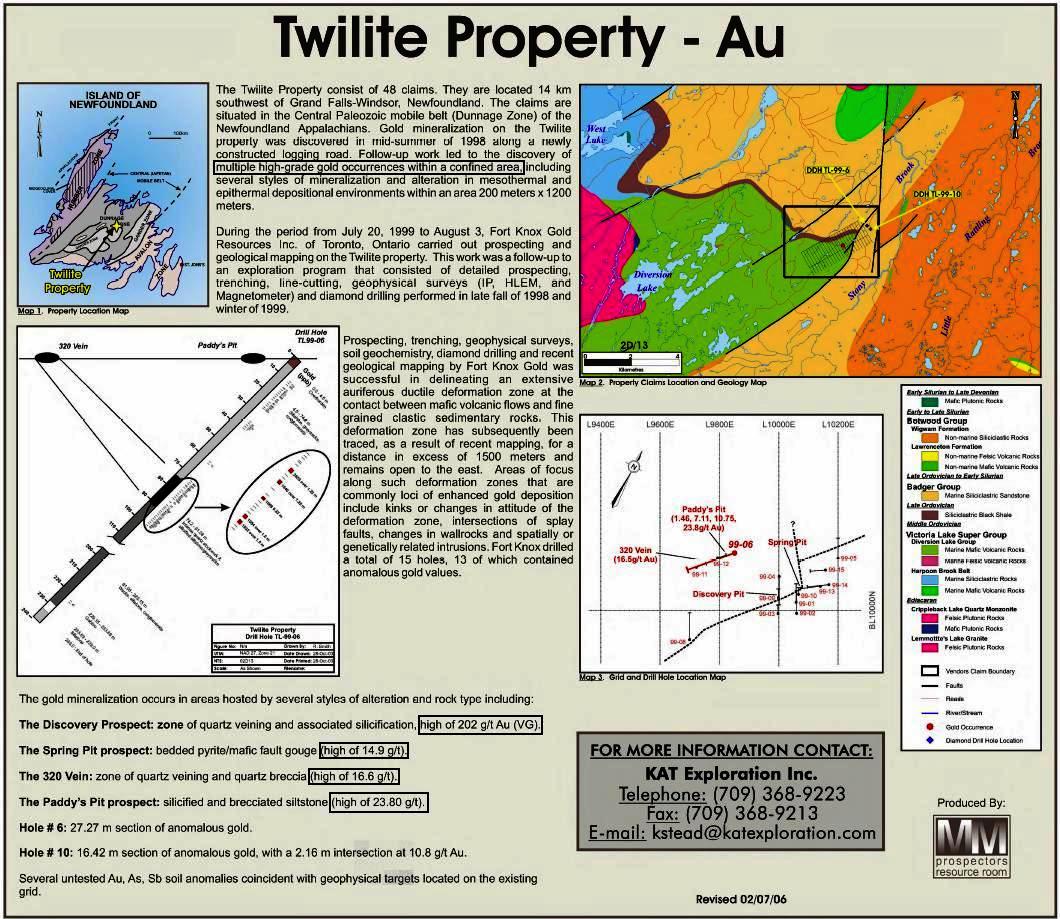

Dec 21, 2009 08:00 Kat Exploration Inc. Announces Option Agreement to Purchase 100% of the "Twi-Lite" High Grade Gold Property

MOUNT PEARL, NL--(Marketwire - December 21, 2009) - Kat Exploration Inc. ("Kat") (PINKSHEETS: KATX) http://www.katexploration.com

..."We are very pleased to have the Twi-Lite property as part of our gold portfolio. It provides us with greater opportunity to expand our position as a real gold player. The company's field crews will now build on past work and examine high priority targets which offer excellent potential for the discovery of new gold mineralization.

"Our management team believes that Twi-Lite is a highly prospective property based on strong exploration results to date, its favorable geology and strategic location," said Ken Stead, President and CEO of Kat Exploration.

http://www.marketwire.com/press-release/Kat-Exploration-Inc-Announces-Option-Agreement-Purchase-100-Twi-Lite-High-Grade-Gold-1093875.htm)

Twilite Gold Property

The Twi-lite property, lies along the western margin of the Botwood Basin, central Newfoundland, It is situated approximately 30 kms southwest of the Moosehead gold prospects and has similar potential for epithermal gold mineralization.

The two major structural elements within the survey area are NE-NNE and NW faults. These two directions are well represented within the Discovery showing and have been noted as being associated with gold mineralization. The regional depth calculations, carried out using the Source Parameter Imaging Technique indicates that two major “graben” type structures may occur within the area; one striking NW-SE along the Victoria Lake-Badger Group overlap and the other along the Badger Group-Botwood Group NE striking fault contact. Through the central portion of the area, immediately east of the Discovery showing, major N-S faults are evident on the processed magnetic maps. At the southern end these N-S structures control eastern boundary of the Victoria Lake Group and in the north they appear to form the eastern edge of the Lemotte’s Ridge Sequence.

Some results to date:

The Discovery Prospect: Zone of quartz veining and associated silicification, high of 202 g/t Au (Visible Gold).

The Spring Pit prospect: bedded pyrite/mafic fault gouge (high of 14.9 g/t).

The 320 Vein: zone of quartz veining and quartz breccias (high of 16.6 g/t).

The Paddy’s Pitt prospect: silicified and brecciated siltstone (high of 23.80 g/t.)

http://www.katexploration.com/properties.html#2

MOUNT PEARL, NL--(Marketwire - February 8, 2010) - KAT Exploration Inc. (PINKSHEETS: KATX) www.KATexploration.com would like to inform its investors that it has secured areas of interest around its Handcamp and Twi-lite properties.

The company thought it very important to stake the land packages around both these properties as gold is becoming the main interest amongst exploration companies today.

A total of 5,311 acres was staked around our Handcamp property along with 5,805 acres around the Twi-lite property.

This will now allow the company to carry out larger exploration programs in both these areas in a quest to extend the present gold discoveries.

http://www.marketwire.com/press-release/KAT-Exploration-Secures-Large-Land-Packages-Around-Its-Handcamp-Twi-lite-Properties-1113751.htm

KAT Exploration Signs Three-Year Option Agreement Contract With Vale

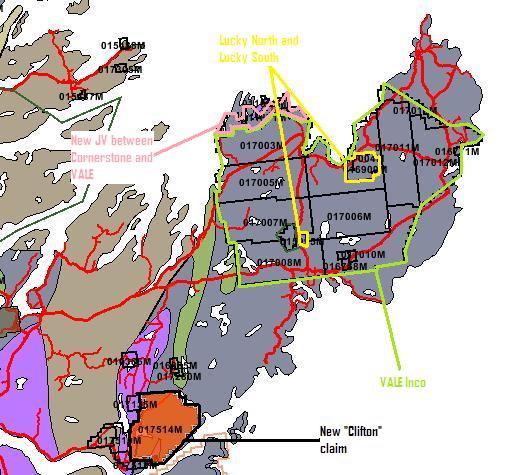

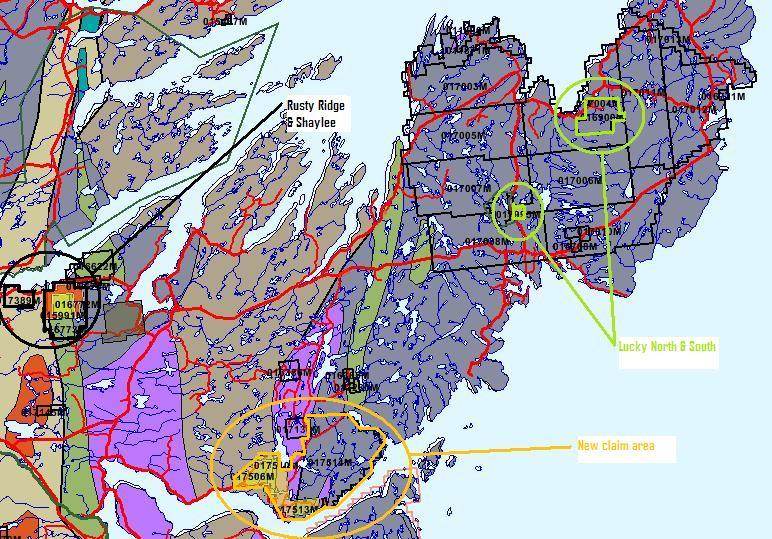

MOUNT PEARL, NL--(Marketwire - June 11, 2010) - KAT Exploration Inc. (PINKSHEETS: KATX) ("KAT") is pleased to announce that it has signed an option agreement with Vale Exploration Canada Inc. ("VEC"), a wholly-owned subsidiary of Vale S.A. ("VALE"), on its North and South Lucky copper properties on the Bonavista peninsula in eastern Newfoundland. Under the terms of the agreement, VEC has committed to an initial C$20,000 cash payment on signing and may elect to make further cash payments totaling C$75,000 over the three-year option period, and may elect to incur a minimum of C$750,000 in exploration expenditures within the option period to earn an 80% interest in the Lucky properties.

Upon VEC's exercise of the option, a joint venture will be formed to further develop the properties, with each party contributing to further approved exploration programs as per their interest. VEC will be the operator of the exploration programs during the option period.

The Lucky properties are in a geological setting with the potential for sediment-hosted stratiform copper (SSC) deposits. The Lucky properties have the potential to produce low-grade, large tonnage copper deposits similar to those of the Zambia copper belt.

Ken Stead, President/CEO of KAT, states, "The very fact that a company of Vale's caliber has enough interest in the area and sees enough potential in the Lucky properties to warrant an option with KAT, leaves us very excited. We are very pleased to be exploring these copper properties with Vale and look forward to bringing them to their full potential."

The Lucky properties are located on the Bonavista Peninsula in eastern Newfoundland, and are accessible by well-maintained roads, allowing for exploration programs to be carried out fairly quickly and comfortably.

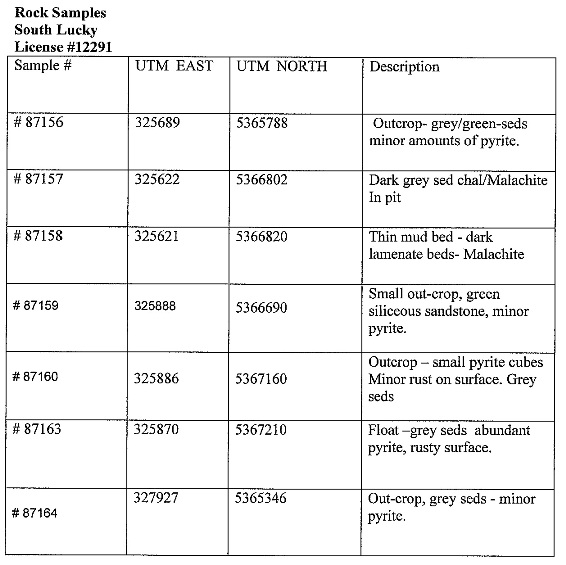

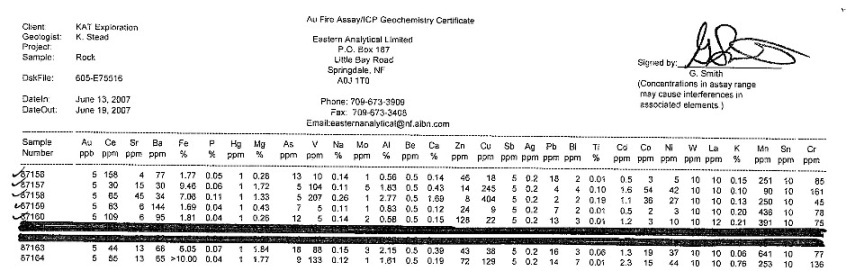

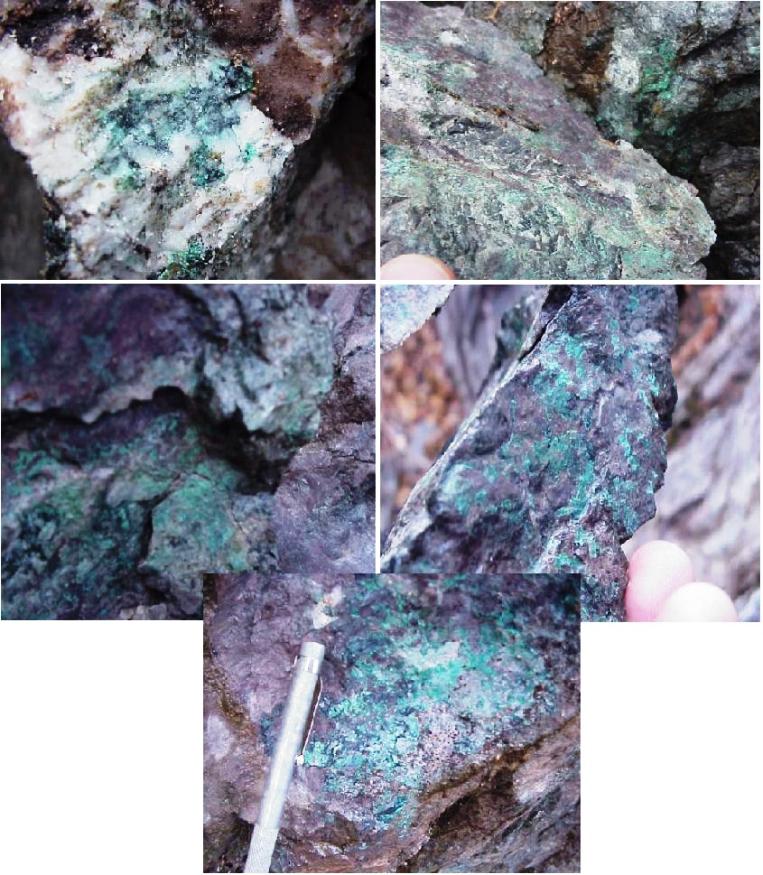

Copper mineralization is quite visible in an old pit near a gravel road with impressive malachite staining along with chalcocite strata bound within the more sandy beds of the sediments with assay results of 2.5% Cu in the more concentrated areas. The most recent discovery was on our North Lucky property where well-disseminated chalcopyrite was found in exposed outcrop approximately 10km north of the South Lucky property.

About KAT Exploration Inc.

KAT Exploration's principal objective is to locate, stake, prove up and sell mineral properties to major mining companies. It is the Company's objective to take advantage of increased activity to generate numerous joint venture clients, and sales of our existing and yet to be acquired properties.

About VEC

VEC is a wholly-owned subsidiary of Vale, the world's second largest mining company by market capitalization, with its headquarters in Brazil. Vale is committed to the pursuit of sustainable growth by operating with respect for the natural environment and being an ethically and socially responsible company.

Jack Zwicker

KAT Exploration Inc.

Investor Relations

Ph 902-497-3188

jzwicker@katexploration.com

http://www.katexploration.com

http://www.marketwire.com/press-release/KAT-Exploration-Signs-Three-Year-Option-Agreement-Contract-With-Vale-1274884.htm

Posted by: siljie Date: Saturday, June 12, 2010 9:28:00 AM

In reply to: None Post # of 61799

Email response from Ken for some insights:

My QSN: First of all, I'm excited that Vale is interested! Well done, and congratulations to all of us! The PR says that VALE has paid $20,000 (and possible 75,000 for extending this 3 yrs) to own the option to JV with KATX. If Vale chooses to spend at least .75 million for exploration costs, they then own 80% of the claims, and 20% stays with KAT. My first question is, what if Vales does not choose to do this, but chooses to exercise the option to JV, what kind of terms might we be looking at, and is it better for KATX to fund the exploration ourselves, prove up reserves and get a more valuable deal?

Ken's ANS: First off, the $20K & $75K is money that is paid at the beginning of each anniversary date is just to cover the cost of administration. No major company will pay much of anything until they are pretty certain there's something there. If Vale does not complete the 3 year deal and spend .75 million (which would take them to a feasiblity study so they know there's a deposit there) then the property returns to KAT 100%. The advantage KAT has is, VALE is building a $2.5 billion refinery just to the south of the Lucky properties and need copper for process. If there is a deposit there worth mining they will not sit on it as that’s their reason for working… in such an urgent way.

My QSN: 2ndly, why has KATX agreed to give up 80% of its interests in return for this sub-million exploration cost, the exchange appears vastly disproportionate? I am not knowledgeable on the mining industry, so I'm not sure if really the 80:20 will turn out to be a really balanced exchange eventually accounting for all associated costs etc (I don't know these). And/Or perhaps it is justified to significantly sweeten the deal for VALE for subsequent dealings to work out in our favour. Please give me some insights into these.

Ken's ANS: After the 3 year option is execised then comes a feasibilty study which would cost nothing less then $50 million to which Vale will have to pay 80% of the cost. If there is not an ecomomical deposit then we've saved our money and Vale has wasted its. Also, most deals like this for a smaller company like KAT might just stand the chance of only being able to retain a 2% NSR(net smeltering royality). A copper/silver deposit such as could possibly be on the Lucky property has the potential to be valued at $5 billion and much more. That being the case KAT owning 20% of the deposit would equal in value of $1 billion for KAT, which any company would be happy to own. Therefore 20% of an economical deposit has tremendous value for a company.

I sent this today around noon time Europe, and got a reply in 45min.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=51220992

MOUNT PEARL, Newfoundland--(BUSINESS WIRE)--Kat Exploration (OTC-Pink Sheets: KATX) is happy to report that its exploration program carried out this summer on its 100% wholly owned “Lucky” Property has been a real success.

Copper mineralization is quite visible in an old pit near a gravel road and impressive malachite staining along with chalcocite is strata bound within the more sandy beds of the sediments. The horizon that contains the mineralization has been traced for approximately 8 miles with copper mineralization at a thickness of 300ft in places. Assay results of 2.5% Cu [COPPER]were discovered in the most exposed areas within this horizon. The most recent work uncovered several large areas of semi-massive to well disseminated chalcopyrite approximately 4 miles on strike from the open pit which reveals the highest copper grades to date.

This type of environment has the potential to produce low grade, large tonnage copper deposits similar to those of the Zambia copper belt.

To secure an area of interest the company recently staked 1225 acres of new land mass where some recent grab samples produced copper results of .5% along with anomalous gold.

More ground work is planned for the Northern portion of the property where the most recent copper occurrences were discovered.

In its future endeavors the company would hope to ensure non-dilutive options where the merits of the projects will fund the operations. As one of the co-founders of Cornerstone Resources Inc., who had done joint ventures with major mining companies such as Noranda, Phelps Dodge, and other major companies, Mr. Stead is quite familiar with world class mining companies and is confident in bringing their interest to Kat’s projects as they move forward. Future press releases will provide more updates to confirm more guidance on the direction of the company.

http://ca.news.finance.yahoo.com/s/23112009/34/biz-f-business-wire-kat-exploration-report-recent-discoveries-its-lucky-property.html

MOUNT PEARL, Newfoundland, July 2, 2009 (GLOBE NEWSWIRE) – Kat Exploration Inc. is pleased to announce its "Lucky" Property is ready for drilling.

http://finance.yahoo.com/news/Kat-Exploration-Announces-pz-2778940824.html?x=0&.v=1

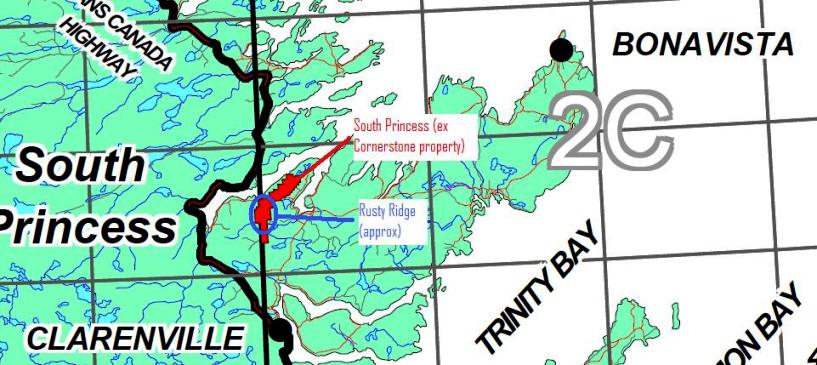

Jun 16, 2010 09:50 ETKAT Exploration Initiates Drilling Program on Rusty Ridge IOCG Property

MOUNT PEARL, NL--(Marketwire - June 16, 2010) - KAT Exploration Inc. (PINKSHEETS: KATX) www.katexploration.com

KAT Exploration is pleased to inform its shareholders and investment community that a deep drilling program on its Rusty Ridge Iron Oxide, Copper & Gold (IOCG) property is being initiated in order to test two major Induced Polarization (IP)/Magnetics targets. Application for drilling has been submitted to Newfoundland Department of Mines & Energy to carry out the work.

A Canadian geological firm with much experience in the Olympic Dam type deposits have been contracted to carry out the project under the direction of our present geologist Mr. James Weick.

The Rusty Ridge targets have been identified by an airborne survey and ground geophysics which can be viewed on KAT's website.

The coincidental magnetic IP resistivity and soil geochemical anomalies suggests potential for a body of Iron Oxide +/- Base, Precious and Rare Earth Element type mineralization, similar in style and settings to the giant Olympic Dam deposit in Australia.

The presence of a large magnetic body that appears to be intrusive into the overlying rock sequence that appear regionally altered, are variably pyritic and contain vein type fluorite mineralization and appears to suggest a magnetic origin for the mineralization.

Anomalous levels of the Light Rare Earth Elements (LREE) cerium and lanthanum, all present in Olympic Dam were not only detected in soils but also in rock samples as well in our Rusty Ridge property. In addition, the soil geochemistry also produced anomalies in silver, gold & copper.

President and CEO Ken Stead stated, "This project will be very significant for the growth of the company if the defined targets at depth prove to be a multi-mineral ore body similar to that of the Olympic Dam, or any deposit for that matter. We know the targets are very intense and now we are ready to prove what they are by means of a series of deep drill holes."

Shareholders and Investors will be kept up to date as this drill project moves forward…

http://www.marketwire.com/press-release/KAT-Exploration-Initiates-Drilling-Program-on-Rusty-Ridge-IOCG-Property-1277037.htm

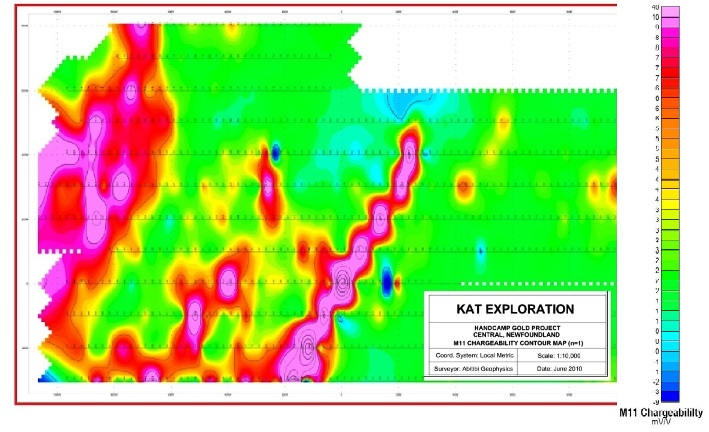

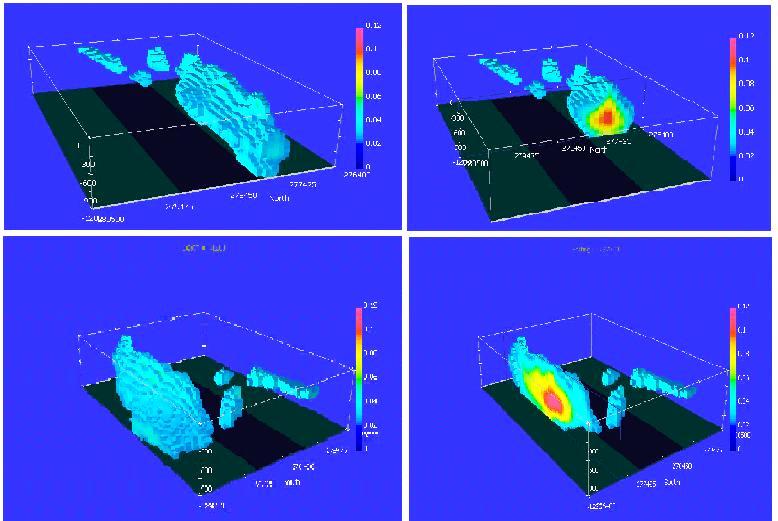

MOUNT PEARL, Newfoundland, June 15, 2009 (GLOBE NEWSWIRE) -- Kat Exploration (Pink Sheets:KATX - News; http://www.katexploration.com/) is pleased to announce that exploration on it's "Rusty Ridge"(IOCG) property was highly successful in identifying coincidental magnetic IP resistivity and soil geochemical anomalies that suggest potential for a body of Iron Oxide +/- Base, Precious and Rare Earth type mineralization, similar in style and setting to the giant Olympic Dam deposit in Australia… A recently completed 3D inversion modeling [shown below] of the airborne magnetic data show a discreet, strong magnetic anomaly underlying the Rusty Ridge area. Coincidental with this are moderate to strong IP chargeability anomalies that suggest either graphite or significant concentrations of sulphides. Graphite can be for the most part eliminated as the rocks are terrestrial, not marine meaning that conductive argillaceous rocks would not be expected in this environment.

Anomalous levels of the Light Rare Earth Elements (LREE) cerium and lanthanum, all present in Olympic Dam (and others), were not only detected in soils but also in rock samples. Other rare earth elements such as Yttrium(Y), Niobium(NB), Zirconium(ZR) along with Uranium, were all detected in both soil and rock samples. In addition, the soil geochemistry also produced anomalies in silver, gold and copper.

The host rocks for most of the mineral occurrences and the unit overlying the most intense portion of the magnetic anomaly is a brecciated, hematitic felsic volcanic rock, locally with veins of purple fluorite and disseminated pyrite.

This property has already generated a lot of interest from mining companies and is being offered as a Joint Venture (JV) project.

http://finance.yahoo.com/news/Kat-Exploration-Announces-pz-2721659684.html?x=0&.v=2

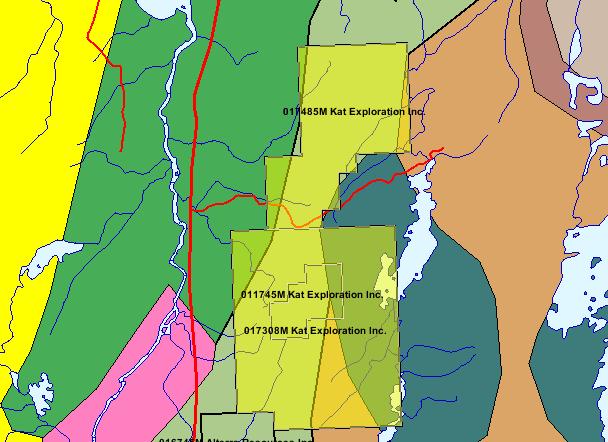

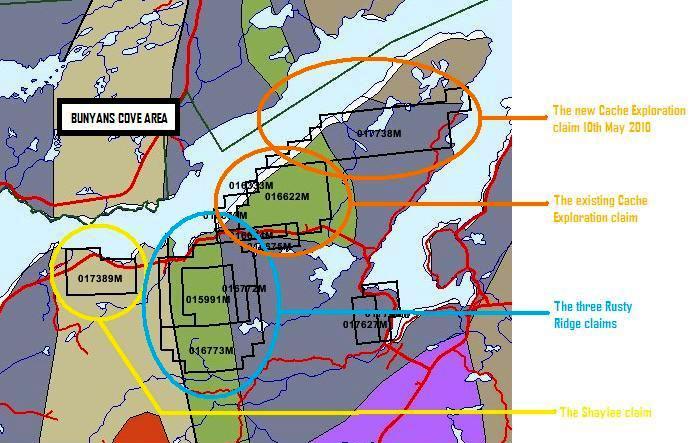

New information about Rusty Ridge and Shaylee

Here's some new stuff about the Rusty Ridge / Shaylee area. A little while ago I noted that there were some claims north of Rusty Ridge from some other companies. In fact they weren't registered under a company name but that of an individual. Anyway, I did some digging and found his email address and sent him an email. He replied and we struck up an email conversation. I now know who he is, what his company is called and what his company are doing up there.

The company is called Cache Exploration. Here's the map:

Cache Exploration is searching for... Rare Earth Elements (REE)! They are organising further exploration on their claim this summer, led by a top level, award winning independent geologist and university academic. They must be confident too, because on 10th May they doubled their claim size. I also had a chat about them with our CEO Ken Stead. He knows that area well because he has already explored it and is confident that we have the best claims staked already.

So what is important about this? To my mind what is important is that Cache Exploration believe there is enough value in that area from REE deposits alone. We have our copper at Rusty Ridge and we knew that there are REE deposits up there, but this additional DD adds to the circumstantial evidence that the REE value could be immense.

-courtesy of Rick-UK

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=50549449

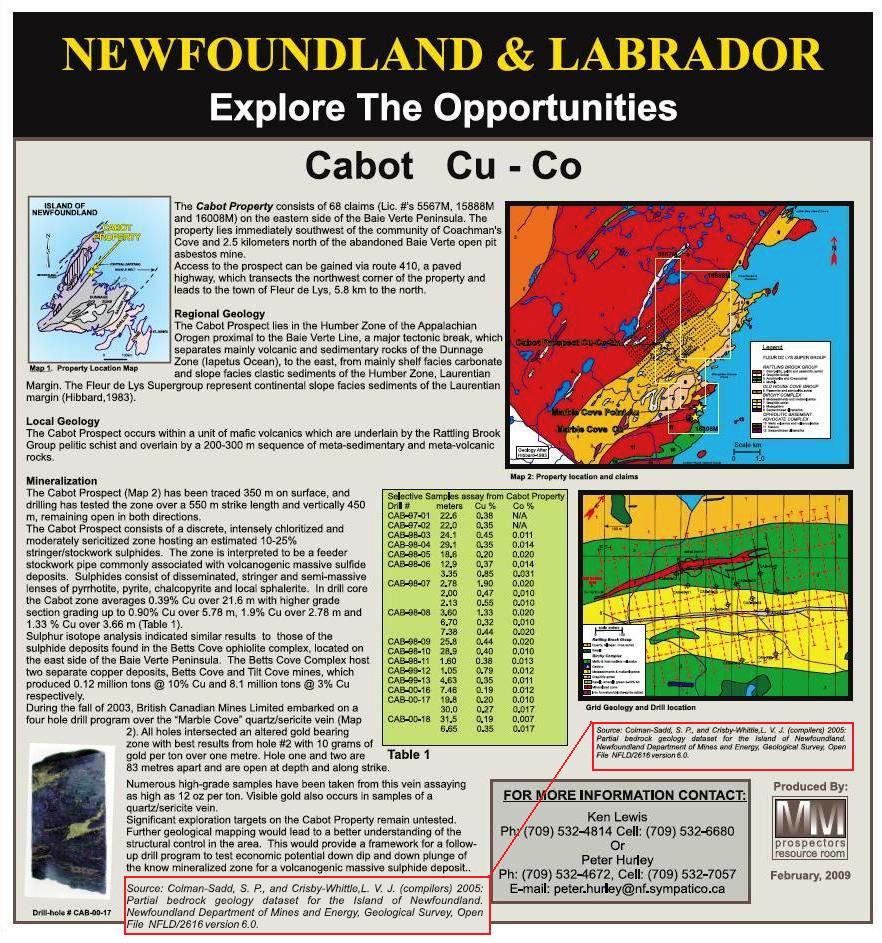

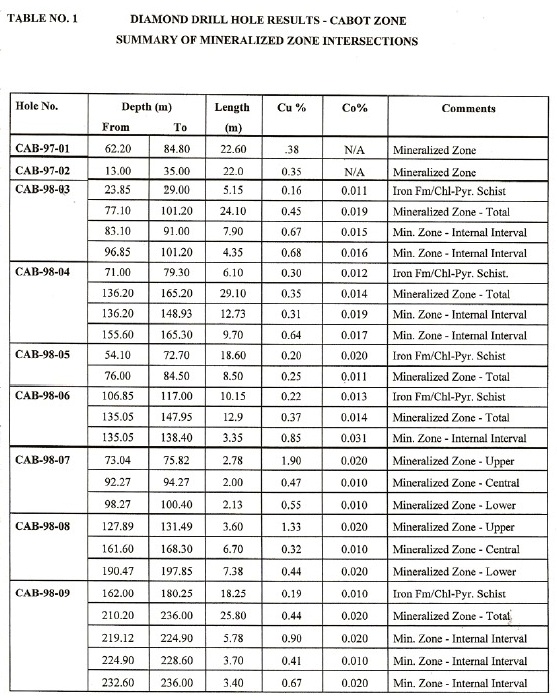

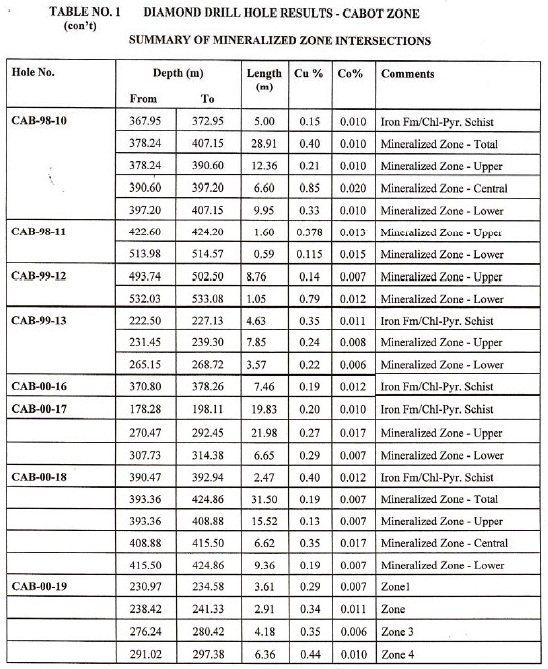

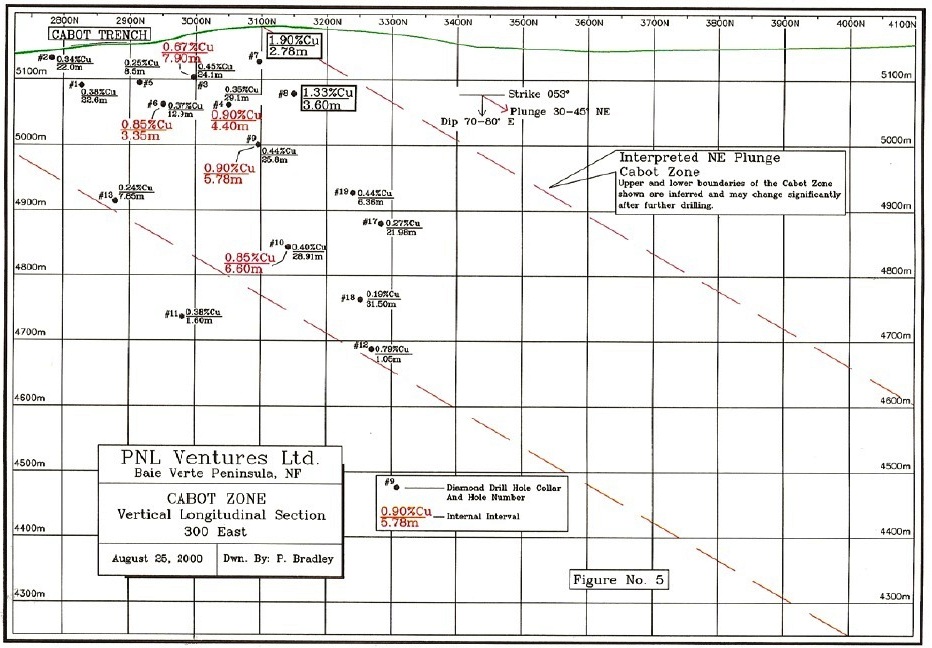

KAT Exploration Inc. Announces Option Agreement to Purchase 100% of the "Cabot" Copper/Gold Properties

July 19, 2010. KAT Exploration Inc. is pleased to announce that it has completed the signing of an option agreement with PNL Ventures Ltd, and Weyburn Investments Limited, for the Cabot properties, consisting of 138 claims in five separate licenses, located on the Baie Verte peninsula, Newfoundland.

KAT has agreed to acquire a 100 percent interest in the Cabot properties over a five-year period in consideration of total cash payments of $560,000, which includes a payment of $40,000 on signing and the remaining $520,000 over the remainder of the agreement. The agreement also includes a stock issuance of 3,000,000 shares, with 150,000 shares to be issued upon signing and the remaining 2,850,000 over the remainder of the agreement.

KAT also agrees to allocate minimum expenditure of $1.2 million over the five year term of the agreement and complete a National Instrument 43-101 on the Cabot properties.

If upon completion of a feasibility study of the Cabot Properties, KAT will pay a further four million shares, whereby it will then have earned 100% of the five licenses which make up the Cabot properties.

PNL Ventures Ltd, and Weyburn Investments Limited, will also retain a 2.5% NSR [Net Smelting Return] in which KAT Exploration has the right to purchase 1.5% of the 2.5%NSR for a total amount of $3.5 million.

Kat Exploration will be the operator of the project during the option period.

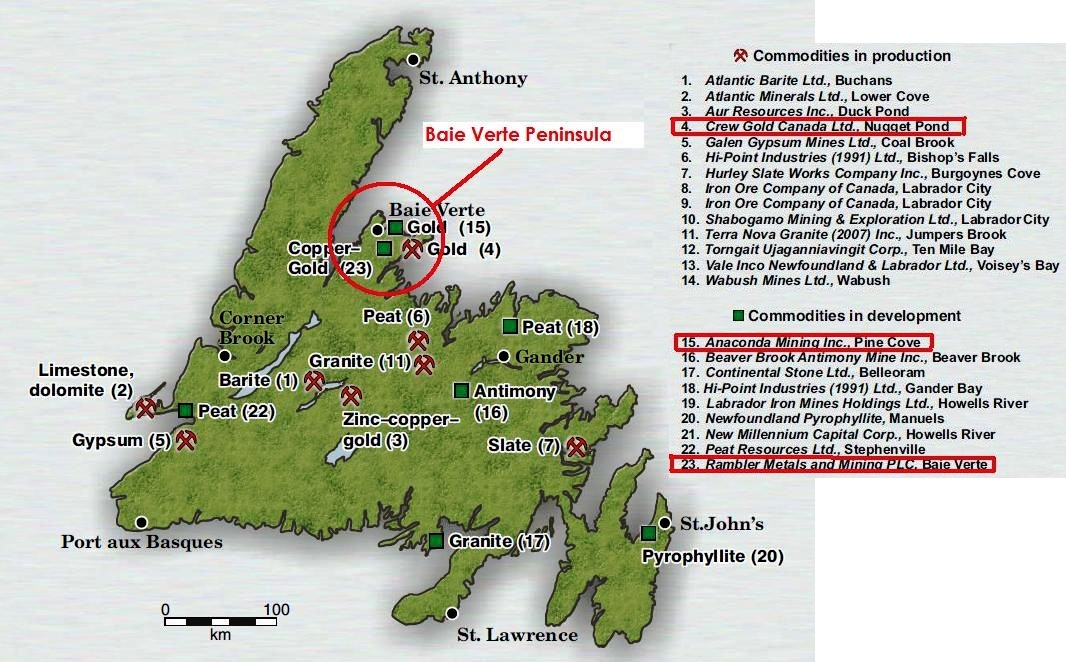

The Cabot properties are located on the Baie Verte Peninsula which is one of Newfoundland's most historic and prolific mining districts. Down through the years the Baie Verte peninsula alone has be host to numerous Copper, Gold and Massive Sulfide deposits. The "Tilt Cove" mine, the "Rambler" mine and the "Bretts Cove" mine to name just a few were all massive sulfide deposits. The "Deer Cove" mine, the "Nugget Pond" mine and the still operating "Pine Cove" mine were/are gold deposits.

The "Cabot Property," with its significant new Copper/Cobalt/Gold discoveries, is a prime example that tremendous potential still remains for new discoveries in this prolific mining region.

The Cabot zone consists of a discrete, intensely chloritized and moderately sericitized zone hosting an estimated 10-25% stringer/stockwork sulfides. The zone is interpreted to represent a feeder stockwork pipe commonly associated with volcanogenic massive sulfide deposits. The Cabot Zone had been tested with several past drill holes averaging 0.39% Cu over 21.6 meters with internal intervals grading up to 0.90% Cu over 5.78 meters. The best grade intersections over an appreciable width encountered 1.90% Copper over 2.78 meters and 1.33% copper over 3.66 meters respectively.

One mineralized zone exposed on surface, varies between 25-30 meters wide and a strike length of 700 meters. A rough calculation has indicated 18 to 20 million tons of low grade copper ore, with cobalt as a complementary mineral, together averaging approximately ½%. There are large areas of the properties unexplored with no drill testing that has the potential to increase the volume of ore significantly.

Ken Stead, President/CEO, states, "We have been in negotiations for the past several months in trying to acquire this property and very excited we've closed the deal. However, while we are excited about the Copper/Cobalt content, it's the Gold potential that is most attractive. One drill hole intersected 40 meters of anomalous gold along with one meter averaging 10 grams per ton. A number of recently discovered quartz veins have produced results of 10 grams of gold per ton with the highest reaching as high as 12 oz/ton. These are the kind of properties KAT Exploration is looking for as it continues to move forward and bring real value to its shareholders. KAT Exploration will continue to have interest in obtaining gold, copper, silver and other minerals that would prove to be substantial assets for the company. Multi-mineral ore deposits are where our focus has always been and will remain."

http://www.marketwire.com/press-release/KAT-Exploration-Inc-Announces-Option-Agreement-Purchase-100-Cabot-Copper-Gold-Properties-1292069.htm

...we have made a few new and unexpected discoveries on the RR [Rusty Ridge] during our last period of sampling so we will continue with a summer program of the same and spend some time on the Shaylee right next door.

Ken

Shaylee is a region of volcanic rock traversed by numerous faults which early indications appear to indicate contain high levels of copper. Even less is known about Shaylee than about Twi-Lite. Shaylee sits adjacent to and very nearly abutting Rusty Ridge, and was an area that Ken and Tim Stead have only very recently claimed on 11 February 2010, although they had explored the area beforehand. Shaylee has two very interesting copper anomalies, the first 1km long by 75m wide and the second 200m long by 50m wide. It’s proximity to Rusty Ridge means that KAT Exploration can include further exploration at Shaylee into its plans for exploration at Rusty Ridge, and this precisely what our CEO Ken Stead intends to do. What I also think is interesting is the idea that KAT Exploration could potentially find a JV partner for Rusty Ridge but retain the mineral rights at Shaylee, then piggyback off the work carried out at Rusty Ridge to add further value to KATX shareholders. Just an idea!

The image below shows Rusty Ridge to the right (three claim areas together) and Shaylee to the left…

--courtesy of Rick-UK

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=50326084