News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Just a fraction of KTCarneyCorker. GSEs have real shareholders, none of them hold shares. They just make up stories, then make up friends to pat them on the back so others may follow down the wrong road. They said 10c at 30c, now it’s 1.5. They make laser focused losses in courts, shareholders gain with every case.

Kthomp, thanks for taking time to respond. Very interesting scenario, and one I tend to agree with. Gov't is going to maximize all they can upon exit. Shareholders will just have to deal with it.

Based on your thoughts about the possible scenario of converting the seniors to commons and JPS into commons, am I understanding this right?

I'll calculate JPS shares at 50% and 100% par with a low conversion to common at .25 cents per share and $2.00 per share based on your speculation.

30k JPS shares at $12.50 (50% par) = $375k

$375k ÷ .25 cents (conversion to common shares) = 1,500,000 common shares.

$375k ÷ $2.00 = 187,500 common shares

_______________________________________________

30k JPS shares at $25.00 (100% par) = $750k

$750k ÷ .25 cents (conversion to common shares) = 3,000,000 common shares.

$750k ÷ $2.00 = 375,000 common shares

Is this what could happen in the example you laid out to me? Interesting.

If Trump cinches the election in November, the euphoria could very well send the JPS close to 50% of PAR... since historically it has reached that high multiple times in the past.

I don't know about you but if your predictions is anywhere from 50-100% of PAR... I'm liquidating at least half of my position if it goes near 50% of par.

A double from 50% of PAR can be done with much less risk in another stock...

Barnum & Bailey is seeking employment, I think you would be an asset. How many ID’s you think Tightcoil and Niagra have?

That's according to Fannie Mae. There's no input from me.

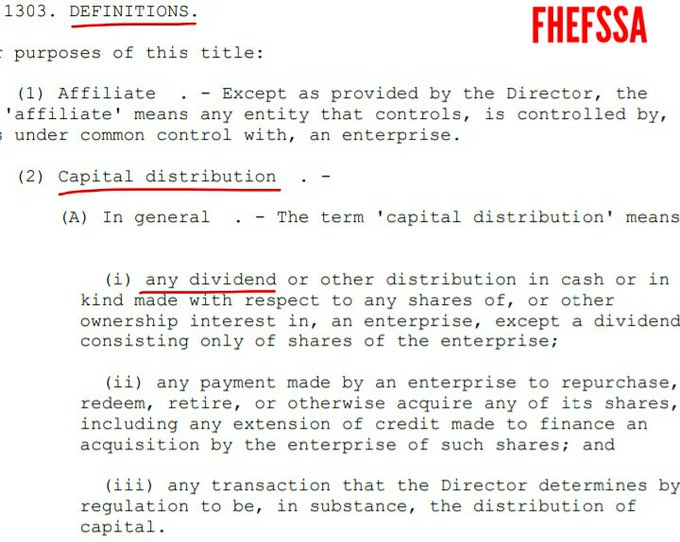

JESUS! Can't you see that dividends and today's gifted SPS LP are Capital distributions restricted?

Both number 1 in its statutory definition, just in case you haven't learnt it in a book in Finance: a dividend is a distribution of Earnings (Retained Earnings account is Core Capital) and SPS are capital stock (The Lamberth rebate is number 3, approved through the CFR1229.13 in the Final Rule of July 20, 2011)

The exceptions kicked off in order to legalize them, despite the desire of FHFA and its Hedge Funds guard to turn itself into an outlaw Federal Agency, under the FHFA-C's Incidental Power "any action authorized by the Rehab power", that states: "Restore FnF to a sound (Recap) and Solvent (reduce the SPS) condition".

◾️Reduce the SPS (U.S. Code §4614(e)): 10% and NWS dividends (it recapitalizes at the same time, as the SPS are reduced with simple cash, not with cash dividends.

◾️Follow-on plan: "(c) it supplements.....". Exceptions 1, 2, 3 and 4: For their Recapitalization: CFR 1237.12 in July 20, 2011:

Either

- Outside the balance sheets when they saw that the SPS were going be fully paid down soon (end of 2013 and end of 2014, in Freddie Mac. -Chart below-, and Fannie Mae, respectively), the FHFA needed another exception to apply the dividend payments towards (assessments FHLB-1989 style, not actual dividends).

And

- Internally, with the Common Equity held in escrow, currently in place in the 3rd phase with the SPS LP increases 1:1 Net Worth increases, as compensation to UST in the absence of dividends. It works as follows: FHFA: "Just joking! It'll be unwound. Zing!". No intention of these gifted SPS as of December 2017, to stay, due to the fact that they are already missing on the Balance Sheets ($132B). Financial Statement fraud though.

The scammers are pressing so hard playing the fool, that now they are called The Diapers Gang.

Bradford is living the American dream: to work for a renowned hedge fund manager and mess around with the retail investors 24/7, like many others.

SPS Write down means debt forgiveness, Argentina-IMF style.

There aren't SPS outstanding under the Separate Account plan.

commons up today, hooray!

in my view, they have value if the government writes down the value of its spspa.

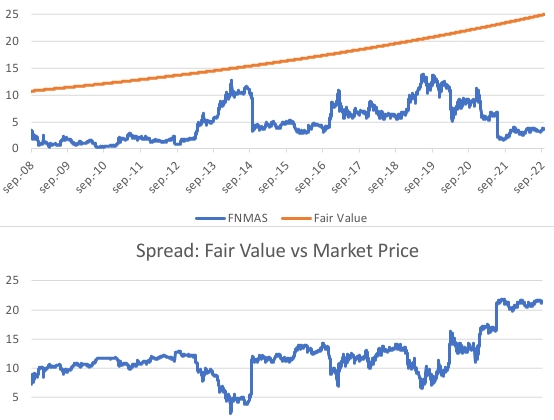

The JPS trading based on its fundamentals is shown in its fair value chart during conservatorship, under the Separate Account plan, that is, a normal conservatorship carried out secretly.

The underlying security is an obligation. A fixed-income security with a legal claim on dividend (coupon) payments and the par value. It trades close to the par value all along, depending on the market interest rates in relation to its coupon, just like a bond.

With the dividend suspended as per its contract or prospectus (at the BOD's discretion) and the statutory Restriction on Capital Distributions, it trades at a discount to par value, discounting the time period to resume dividend payments.

This is the chart with a 6% discount rate, assuming the dividend was resumed under the Table 8: Payout ratio, with the 3Q2022 results.

The JPS holders like Berkowitz are annoyed with this chart (primarily, in comparison with a common stock that trades at x times the EPS) and embarked on a con operation in the U.S. courts when they learned that the UST in 2011 required the Basel-framework for capital requirements for the release from conservatorship, but this is their fair value. JPS have this risk and this is why they get a higher dividend rate than the interest rate on similar obligations by the same issuer. He thought that he was outsmarting them, with no strings attached.

It has ended up with Mnuchin requiring, as compensation to UST, SPS LP increases (another capital distribution restricted) 1:1 Net Worth increase in FnF, so that later he requires that the same haircut for these gifted SPS, be applied to the JPS of his buddy, Berkowitz (Calabria told us in his book).

This is Regulatory Risk (Leverage ratio or Minimum Captial Level: Core Capital > 2.5% of ATA, versus 0.25% before, for the off-balance sheet obligations -MBS Trusts-.). Even an additional 25% of the Prescribed Capital Buffer is necessary (Table 8 of the Capital Rule: Payout ratio) to recover the par value.

Then, Conservator Risk. FHFA-C, in the best interests of FHFA-R, is maintaining the dividend suspension seeking "Membership cleansing", that is, fetch CET1 > 2.5% of ATA, so that the JPS (AT1 Capital) can be redeemed before the Privatized Housing Finance System is unveiled (Tier 1 Capital > 2.5% of ATA), FnF were bound for, since it was chosen for the release by the UST in 2011.

A replica of the FHFA final rule of 2016, about the expulsion of the unwanted members of the FHLBanks.

Good or bad, the companies have fundamentals and that's the stock's fundamentals.

For instance, FnF post $0 EPS every year due to the ongoing Common Equity Sweep. Then, applying a Forward Price-Earnings Ratio of 10 times, $FNMA and $FMCC Target Price for the end of 2024 = 10 x $0 2024 EPS = $0.

The S.E.C. is in charge of the well-functioning of the financial markets and thus, make sure that the stocks trade accordingly, otherwise there is stock price manipulation behind.

$GME trading at PER 1,500 times, looks more like a plot by Blackrock's Fink and Trump's former SEC chair, Clayton, now Mnuchin's lawyer in the $NYCB off market acquisition, attempting to discredit all those that claim that the stocks trade based on fundamentals, because they are the ones that have made up the concept of "tokenization of the common stocks", that is, deprive them of their value (a legal claim on all the future EPS, plus the existing Retained Earnings account) and turn them into "unbacked tokens" in order to hold up their grand scale fraud with this security.

Looks like Dr. Lye can't keep a job very long anywhere she's been.

KTcarney and kite boy posting frenzy today. Sounds like we have a good week ahead 🤣

Fight Back - Fight to Win

Fannie Mae - All the Way Go-Go-Go

Fight to Right the Wrong done to Shareholders

Protest - Complain - The Conservatorship has gone on for too long

Oh you don't own commons? I thought you did..My bad

I can see us getting screwed by the impending implosion of commercial real estate. 20 trillion dollar problem. Usually the way to handle too big to fail real estate is to punish the savers. Either inflate your way out of it, or? Sometimes I suspect that Paulson and cohorts don’t want to get money from monetizing GSE stock, rather they are going to get money by using fnf to bailout all the empty office buildings.

All the towers in LA are empty and underwater and have 4% 10 year mortgages that are all about to go into default.

I imagine that will crash everything. The banks are going to go broke.

Paulson is simply doing the same thing he did betting against the residential market, just on a larger scale in the commercial game.

All those office buildings. Not just the towers, but the 6 story office park cubes are now worthless and the banks are going to get stuck with them.

Mnuchin and Paulson will have cash after the crash and buy them cheap then sell them after the taxpayer gets stuck with bill.

Too bad it’s impossible to make them sensible residential.

I wonder what this crash is going to look like.

Anyone have ideas of how to make money on the coming commercial real estate crash?

I think that we are closer to the end than the beginning. But the spspa kind of is the problem for why i dont own commons. Either the spspa has value or the warrants/commons have value.

The FNMA chart is following a little bit behind but is making positive strides! GLTA!!

That FMCC chart is setting up nicely for a continued move upward! GLTA!!

1 week chart showing $FNMA cannot be held down much longer. #moonshot 🚀 pic.twitter.com/XpiDrISOz3

— Stankonia Capital (FTP FJB VLLC MAGA) (@StankoniaCap) May 15, 2024

FnF closed at $1.51

hopefully the start of something

FnF closed at $1.51

hopefully the start of something

FnF's enormous regulatory capital holes cannot be filled unless the SPS are written down, converted to commons, or some combination of both.

Even with that happening, FnF would have to raise capital, and no capital raise is possible with the SPS overhang currently in place.

Time to make electric homes

What? You just ignore that FnF started retaining earnings during who’s Presidency?

KThomp, you appear to have a solid, in depth understanding of FnF history as it pertains to FHFA and Treasury.

How do you see the preferreds and commons doing? I realize there are numerous possible outcomes, but I'm curious what you think.

I wish they would have wiped out shareholders in 2008.

Pre conservatorship shareholders would have sued and won but companies still gone.

I would have never bought. Imagine where my portfolio would be without this loss since 2009.

We deserve this to end and get paid dividends, etc.

WARNING: you all do know he’s a policy wonk and he’s an advisor at the Cato Institute, right? It’s 36 minutes long and you WILL be bored. He has strong opinions about agency independence, banking regulation, housing policy, he does want a combined financial regulator (at a minimum merging FHFA into the OCC), etc.

He ADMITS pushing back on the Trump Admin when they wanted him to move on the GSEs because he thought as a regulator he shouldn’t buck what he thought was the will of Congress (HERA).

If you make 4.3B in a quarter and the shares only go for around $1.50 per share. The outstanding shares are 1.16 B shares. The math to me is the made $ 3.70 per share in the quarter.

I know we are in a conservatorship.

NOBODY, I repeat NOBODY, other than shareholders, especially any Congressmen, agency official, or influential policymaker, cares about the plight of shareholders. In fact, I contend that it is counter productive to contact ANY government official seeking any relief SOLEY on the basis of an appeal to shareholder plight.

If you all love the cheerleading here more power to you, if it helps you hang in there and find camaraderie, great! As they say misery loves company, but don't be fooled for an instant that you are making a difference to the powers with the boots on your neck. You have a better chance appealing as above, through the backdoor, but for Christ's sake do it smarter!

I read the comment by 'Rule of law guy' and had a laugh. If you don't understand that the SPS aren't "fully repaid", then you shouldn't be commenting at all. And certainly TH's follow-up was just as stupid.

The two problems with trying to have the liquidation preference (LP) offset the funding commitment are:

1) As Tim said, having the funding commitment continue post-conservatorship would be very helpful compared to it disappearing. Also, the LP is valued at $220B on the government's books (as of the most recent Financial Report of the US Government), while the contingent liability of the funding commitment is at most a few billion due to the extreme unlikelihood of it having to be touched at all let alone exhausted, in the future.

2) Treasury choosing to write off the SPS rather than exchange them for commons a la AIG amounts to writing an enormous check to shareholders for no reason. Mnuchin said that it would be illegal and would result in a lot of political fallout according to Calabria's book. While LP writedown would be seen as "fair" by shareholders (though certainly not by people like Senator Warner), I don't see any reason to expect it to ever happen given all the evidence we have.

The Conservator is supposed to have a duty to "Conserve and Preserve."

Let's forget the history we all know here and assume this to be true.

So when the FHFA acts as a con-

servator, it may aim to rehabilitate the regulated entity in a way that,

while not in the best interests of the regulated entity, is beneficial to

the Agency and, by extension, the public it serves. This feature of an

FHFA conservatorship is fatal to the shareholders’ statutory claim.

How is it they can give away billion$ to low income housing when their stated duty is to conserve and preserve. I would expect they should not be allowed, legally, to give ANY of that money away. Other than being the government that nationalized the GSEs, how do they get away with this?

Translation: we are f*cked until TSY decides to play fair.

What it does mean is that if they are to do so (convert senior preferred shares to any other class) they will need another amendment.

After the jury decision, presided over by Lamberth, I want to see how they pull off yet another self-enriching act knee-capping current shareholders.

Any new amendment will be the perfect opportunity to reassess the full picture and, in light of all that has transpired, the new assessment should be quite positive for the company and current shareholders.

If you want to make an extreme click-bait statement, sure.

you state facts yet drill down to a single conclusion that only time will tell if it's true.

Shareholders have the rights associated with the Shareholder agreement. These rights do not dissolve suddenly in 2012 because of a contract between two government entities that violates the fair dealing with Shareholders. These rights travel with the shares. This is backed by the Berkley verdict.

In fact, Treasury could wipe all of the Common and JPS value based on their LP amounts.

It's also possible the leader of the free world will believe in the 5th Amendment.

The resolution of Conservatorship may include NOT further violating the covenant of good faith and fair dealing with Shareholders. IMO, this would be the smarter resolution.

but is it on the TREASURY balance sheet ? and if yes - how does it show --- as the SP value or ?

And there will soon be a ratified 2023 decision that says Shareholders do have a right to reap in the benefits of the company profits as per the shareholder agreement.

What's your point?

Yes, although this doesn't mean lawsuit/s won't be filed after the fact. They just have a near-zero chance of success.

While it's possible the 300+bn worth of SPS gets converted, it's also possible it's less than that.

The amounts CAN be altered with a pen swipe.

As I've said multiple times... I've already given you all the info I care to share. If you can reverse engineer something, good for you. If not, too bad so sad. I am under no obligation to show you my formulas nor the different scenarios.

What you want? Am I supposed to care? We have zero obligation to jump through hoops for you.

At no point did Treasury state they thought anything was illegal. Treasury is an entity, not a person. I've said this multiple times and I don't see you producing any evidence to the contrary.

There had been some calls over the course of the conservatorship for Treasury to just forgive all or part of its claim. That was a nonstarter, politically, for Treasury. Moreover, Treasury claimed that it could not legally do so.

Again, I've answered your questions multiple times. The answers are vague and not to your liking because I'm not Nostradamus.

But you are also the pot calling the kettle black.

Govt doesn’t own yet

Ackman does

Warrants were collateral

Govt has been more than paid back

FNMA & FMCC

Greeen Money Masheeeens

Navy and who? lol.

LOL there are only 2 major holders of fannie mae...

We are next.

https://on.mktw.net/3wEcOp9 Check out this article from MarketWatch - Five things to know about meme stocks like GameStop and AMC — and why they’re hot again

whoah

wait a minute

this says elected board member in the fine print?

something happening or I am just making something out of nothing?

don't answer that. LOL

SEC Filing | @FannieMae $FNMA

— José E Burgos Lugo, PA (@TheBurgosGrp) May 14, 2024

@JarndyceJ read where she’s coming from. https://t.co/MjPxqTbzUO

delta down to .06

will it get to zero or above FNMA?

it's a slow repeating pattern that I should hav replaced bets on.

how do you get 1 billion per quarter if adding 1 trillion?

i am happy that you did not show your ugly face at the open

did anyone here ask you if they have value? are you a financial analyst or something?

|

Followers

|

2308

|

Posters

|

|

|

Posts (Today)

|

18

|

Posts (Total)

|

797488

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader Patswil jeddiemack FOFreddie | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |