News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

since I believe it is legal for Treasury to declare the SPS paid - then selling it for 1B (huge discount) to F and F would be legal

but is that approach written anywhere ?

all the articles I have read said its very hard to turn office space to rental or condo. For one thing there is way too high a ratio of space without windows. People want windows in their rooms. The economics are not easy to pencil out. In Chicago private and city money are trying to convert four major large commercial buildings to housing. It should be interesting to see how they do it

prices are supply and demand

years of insane crazy low 3-4 percent mortgages - held by owners of many houses - keeps them from offering their houses for sale. A strong (yes inflation but jobs and wage growth) economy keeps the demand high - relative to this reduced supply - even at 7% (which in historical sense is not that high)

If Treasury agrees that FnF have paid down the SPS, Treasury still owes them over $30 billion in overpayment of the 10% dividend.

I am not greedy and securities law is securities law

GOV - Treasury has every ACCOUNTING right (not moral right of common sense right) to call every penny sent from F and F to Treasury a dividend. As such in an accounting sense - the GOV can always claim all of their "investment" still belongs to them and is not paid down

IMO - the GOV can declare the investment paid down --- it just can -- AS IT IS the investor and the investor can say - you owe me nothing. DONE.

At that point I am not in a hurry to look a gift horse in the mouth. WTS and a few Billion are weights on our shoulders that still leave us that day - with at least $20 a share.

Again - GOV can argue in any court that we - equity owe them a fortune. I want - wish - hope - they call it paid off - but that is for them to do for political or economy reasons

And in what hiding spot can we find the SEC in all of this?

"the President has clearly stated that his objective is to dispose of the government's investments in individual companies as quickly as is practicable.”

See, the trick is in that last part "as quickly as is practicable". That time never has nor never will arrive.

"“The exercise price was set at the average of the stock price during the 20 day period preceding the day that Treasury granted preliminary approval to participate in the CPP program”

Why not just make the exercise price ZERO since the 100,000 shares/dollar was so terminally, laughably ridiculous. I would have bought Fannie Mae myself if the government would have sold at their so-called "exercise price".

All info is controlled these days

Paid for hire info only is allowed for the tbtf narrative to win aka steal more $ from shareholders

Agree for the most part. But why would he remove my post about the warrant repurchase. If it doesn't apply, he could just comment on it.

Treasury actually received warrants from all the institutions they "bailed out" and then allowed them to repurchase them once the SPS had been paid. Most bought back their warrants. Bank of America was one of the few that didn't repurchase their warrants. Theirs got auctioned off. Obiterdictum once provided us with a spreadsheet of the amounts received by Treasury from the buybacks and the auctions. Can't find it. I tried the Treasury website. Couldn't find it readily. Maybe others might have better luck.

He doesn't want his comments section like IHUb with all kind of accusations without backing evidences, is my guess. After all u like IHUb, he is responsible for everything happening on that page and accountable. So when you say fraud by TDY, unless you prove it with evidence, he wouldn't do it. He is just looking for intellectual discussions mostly in the comments section unlike IHUb or stocktwits etc. Not trying to downplay your comments or intellectual level, but that's my guess on His standards and policies of his comments section

When Treasury deems that the SPS has been paid, Fannie and Freddie can buy back the warrants based on previous 20 days average closing price.

Tim Howard previously took down my comment about Treasury allowing the warrant buy-back. Now he took down the one where I said they were issued fraudulently. Looks like gas lighting to me. Why is he doing it? Don't know. But I no longer trust him. Lost faith in Pagliara long time ago. Right about the time the Moelis Plan came into the picture.

Ooooh. Blind homerism?

We can do that..

very true. and paulson, berkowitz want gazillion shares for each of their pfds. not happening. moelis isn't going to be allowed to collect billions in fees either who are backed by paulson.

i am conflicted about tim. he appears to have straight line to some in the white house as he has written before so he will have connection to paulson if he becomes treasury secretary. that is a big 'if' as you know. he has filed amicus brief on behalf of hedge fund berkowitz. we have to be careful to parse out his viewpoints. i would be surprised if he is manipulating his large following after what he went through. who knows.

I agree. Practically everything they've done is illegal. The people who should speak up for the corporations (e.g. Tim Howard) are for personal reasons (possibly bought and paid for by hedge funds) suppressing any mention that the warrants are illegal. If Treasury agrees that FnF have paid down the SPS, Treasury still owes them over $30 billion in overpayment of the 10% dividend. At current prices FnF could buy back the warrants for less than $10 billion. That gives them an additional $20 billion towards their capital. Politicians can claim the profits they made from their "investment" is $301B-$187B-$30B+$10B = $94 Billion.

The reason Ackman, John Paulson and possibly Berkovitz legitimize the warrants is because they probably want to buy the warrants from the government. Ackman and Heroic it's previously made offers to buy them. And Moelis Plan was a thinly disguised plan by John Paulson to buy them cheap.

who are these 3 ? very curious

“Treasury has retained 3 asset managers and intends to use other outside consultants to assist Treasury in enhancing its process and independently assessing value of each repurchasing bank's warrants. “

interesting.. there are so many ways they can exit, completely subjective and speculative

Q: Is the number of warrants subject to reduction or adjustment?

A: Yes, a bank can reduce the number of warrants it issued to Treasury by 50% if it completes a qualified equity offering

no capital raise as it dilutes their stake

“The warrants are also subject to customary "anti-dilution" adjustments in the event of other changes to the Company's capital structure, which is designed to ensure that Treasury's interest is not "diluted" by such changes.”

what does this mean? they did in aig case.

“For publicly-traded institutions, Treasury receives warrants to purchase common shares. Treasury has not exercised these warrants.”

“The President has clearly stated that his objective is to dispose of the government's investments in individual companies as quickly as is practicable.”

isn't it then illegal for them to take warrants at $0.00001 ? or does the comment below only applies to exercise price? it is kind of unfair to take 79.9% at $0.00001 with 300 billion already taken

“The exercise price was set at the average of the stock price during the 20 day period preceding the day that Treasury granted preliminary approval to participate in the CPP program”

https://www.fhfa.gov/Conservatorship/Documents/Senior-Preferred-Stock-Agree/FNM/warrant/Fannie-Mae-Warrant.pdf

https://home.treasury.gov/news/press-releases/200962612255225533

Going to have to turn commercial business buildings into real estate I’m guessing.

I don’t think the government can rob the gse’s again.

It seems this disaster of empty office buildings should have already happened but is delayed somehow.

I have a few of questions.

1. What will happen when the obvious commercial real estate disaster happens.

The skyscrapers are 50% empty. They have a few years left on their 10yr 2% loans. The banks are going to own them and they are worth 50% of what they were.

How will this affect Fannie Mae in the economy at large? Does anybody imagine a different scenario? It seems to me as sure is nightfall day collapse is impending in all cities.

Is there a way to make money betting against commercial real estate?

2. It’s strange that the 7% interest rate hasn’t dropped home values more than it has. But I believe it will. Thoughts? I’m in LA for example and work in the film business, at least I used to, but suddenly starting a year ago all Production left Los Angeles. Everybody I know in the business is out of work. And about to sell their houses.

3. What other Trump trades are there? I think I’ve made it clear that I’m not a fan of Trump. But from the looks of the swing states the election is his to lose. I actually think the New York case is a bullshit case of selective enforcement. The 130,000 is small potatoes. Even with a conviction, I doubt that’s going to change. I was originally happy to see him going to court, but if I’m any barometer, my opinion has changed. I think his position position in the polls will be strengthened whether he wins or loses.

If he wins and is found not guilty, then the case was a nuisance case. if he loses, it looks like political persecution at worst and selective enforcement at best.

" they paid like $0.001?"

You wish! Be more free with the 0s.

"i don't like either candidate but if one of them will at least partially right this wrong I'll take him."

Sorry, one of the candidates thinks Fannie and Freddie are some of his snotty neighbors in Delaware.

Shareholders here are like those two knot-headed brothers on Oak Island. Everybody tells them to sell and move on but they know there is a treasure there . . . . somewhere.

"I think the sherwin-williams reference is

Very accurate for what the MM’s are

Doing to us. Maybe we should name them

The SW MM’s will be less irritating for you."

What the MMs are doing to us, what those in government are doing to us, and what those in the judiciary are doing to us is more readily found on a porn channel rather than a paint store!

Then how do you explain all the graffiti?

lol

Sorry I couldn’t resist

What a clown.

Golf

Why the focus on WTS that dilute equity 4:1

Should the focus be on the 200B dollars of obligation that Treasury could convert to equity ---- being say a 100:1 dilution

?

Thank you

and if GOV kills that obligation (v F and F pay cash to kill it) ---- ? can F and F then buy back for pennies the WTS

my sense - if GOV decides (Treasury) to say PAID BACK --- they will do it as ONE same step with exercise of the WTS and share ownership of 4B shares in their pocket

?????

could be

key word - given last four years he was in office (With control on Treasury and Justice all four years !!!!) - this is a trade (buy if you believe and get ready to quickly sell - if there is no real solid news in say 4 months )

Help

Those CERTAIN provisions suspended seem tiny to me - relative to CORE (95%) business

what would be seriously interesting - ? -- if anyone can find the "amendment or rule change or ?" that said keep the cash and write the IOU on ALL profit ?

Cancel the warrants

Govt Should be deemed paid back

IMO

IMO

any move at F and F ---- like second mortgages (or lending on equity - which is same but here F and F are the lender) --- or ...

likely have no impact on the economy between now and NOV

but - one move could both have impact - reduce inflation - and GAIN massive positive PR ---- for Biden now or say DJT if he wins in year one

SUSPEND THE FEE FOR ONE YEAR --- mortgage rates drop the next week by noticeable amount

HUGE PR - and take credit (right or wrong !!!) for STRONG IMPROVED F and F that can afford to do this !!!

which is why release will be done down here, below institutional prices. and Ps will be nowhere near par cause they wont go up unless commons go up. their fantasy will be gone, KTCarneyCorkerShellGamer Amateur hour will be over.

When Treasury deems that the SPS has been paid, Fannie and Freddie can buy back the warrants based on previous 20 days average closing price.

https://home.treasury.gov/news/press-releases/200962612255225533

You can't say "JPS par (stated) value" because they are two different stock values.

Par value is the value as stated in the companies' books.

Stated value is when there is no par value.

The JPS have par value, $25 or $50, not stated value.

On the other hand, the SPS have no par value and a stated value that coincides with the Liquidation Preference.

It denotes that you are clueless, as seen in your call for a swap JPS (AT1 Capital) for Common Stocks (CET1), despite that FnF have generated a whopping $433B worth of Common Equity (Retained Earnings account: CET1) that remains unaccounted for, once their Financial Statement fraud with the $132B SPS LP/offset absent from the Balance Sheet is adjusted.

Not even $1 of CET1 has been recovered by the corrupt plaintiffs and their remedies don't recover it either.

Asking for debt forgiveness (SPS written off) doesn't count. It's just too crazy.

juniors will end up with somewhere between 50% and 100% of par (stated) value via a conversion to common. Not converting the juniors makes no sense due to the CET1 capital requirement in the ERCF.

THIS IS TRUMP TRADE. Begins June, 2024.

The lowlifes target the Income Statements (EPS) and FnF and the FHFA target the Balance Sheets, where this SPS LP increased for free (First, a one-time $3B in December 2017. Then, every quarter since September 2019) and its offset, are missing.

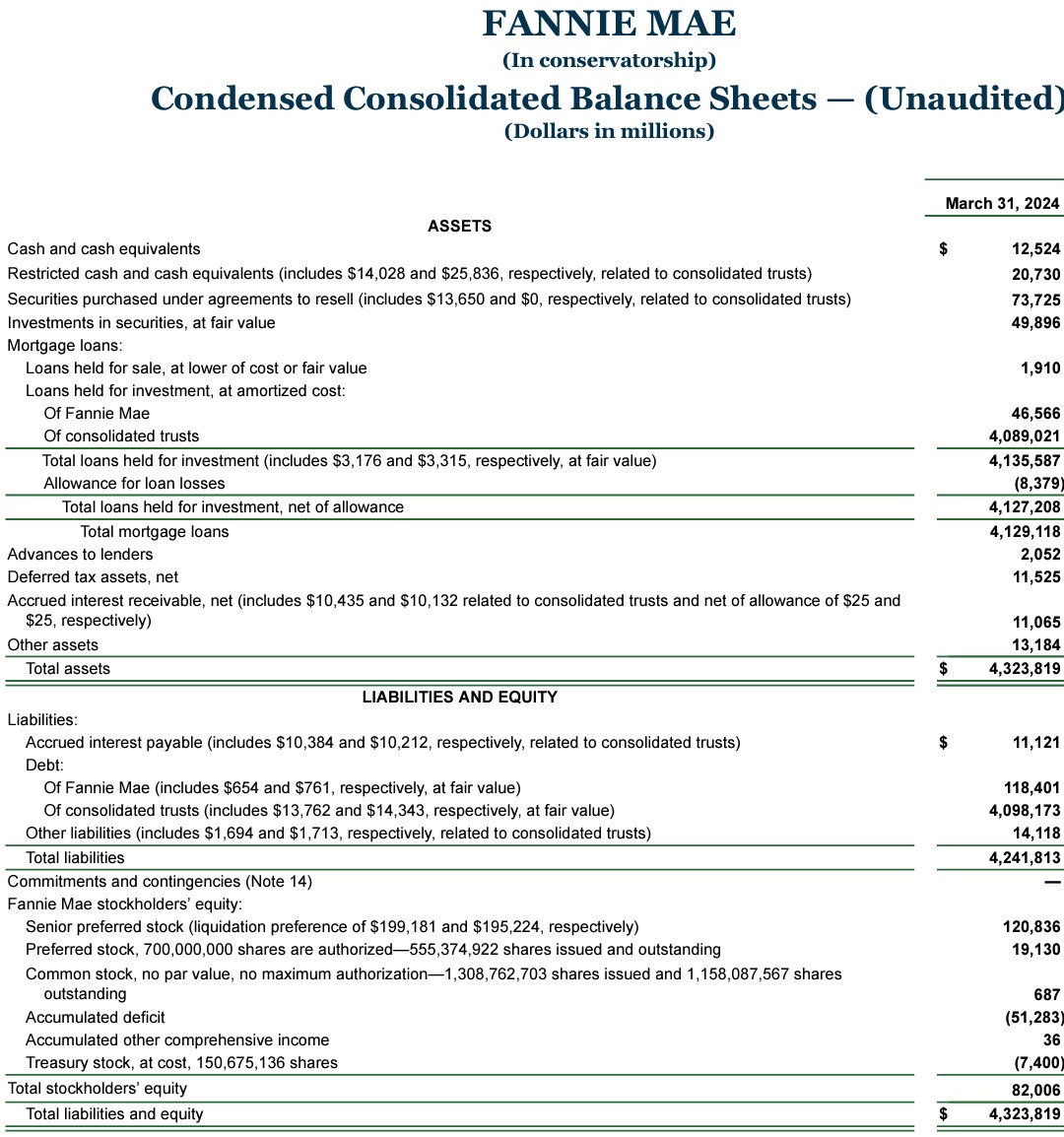

Fannie Mae posts the same SPS LP every quarter: $120.8B.

The actual SPS LP outstanding as of March 31, including the one scheduled to be increased on June 30 that must show up as well (no cash is expected to receive): $203.5B.

Hence, $82B SPS LP missing, which is the $82B Net Worth built.

These people want to meet the capital requirements with the Net Worth, which means, that it's met with the SPS handed out to the government.

Likewise Freddie Mac:

Its SPS LP is stuck to $73B every quarter. Yet, the actual SPS LP outstanding stands at $123B as of March 31, including the one scheduled for June 30.

$50B SPS LP is missing, equal to the $50B Net Worth.

FnF are building SPS, not regulatory/statutory capital.

Bill Ackman and Sandra Thompson lie: "FnF continue to build capital through Retained Earnings".

The payment of Punitive Damages will clear things up.

Howard is a fraud, the EPS is $0.

The PERs are N/A or 1,000+ when it's close to $0.

This is unacceptable for the former CFO.

As I commented yesterday, he uses the Net Income instead of the Net Income Attributable to Common Shareholders, to calculate the EPS.

Watch the Income Statements is the first thing I do when FnF post their Earnings reports. Primarily, because I want to see whether there's been Provision for Loan Losses or reserve release. Also the amount of Derivative Gains/Losses and finally, either the qoq and yoy growth in the Net Revenues.

The EPS is posted at the bottom of the Income Statement. Always $0 or slightly positive or negative.

There are no excuses to not see the EPS, just knowing that the SPS LP is increased every quarter in the same amount as the Net Worth increase, and everyone should have a look to the Income Statements to see how FnF are recording this fact.

No excuses for the Bloomberg Terminal posting the KBW's EPS estimates of $3 in 2024 and 2025, outliers in comparison with the previous ones of $0. Or Guido, Pagliara's clerk, insisting on $3 EPS in this board.

We are witnessing a con operation to conceal the ongoing Common Equity Sweep with the SPS LP increased for free and its offset (reduction of Retained Earnings account), both absent from the Balance Sheets (Financial Statement fraud)

The Common Equity (Retained Earnings account) is being swept, the moment it's substituted for SPS in the Net Worth of FnF, as seen in the image with the adjusted figures.

So, these lowlifes double down on the same fraud of FnF and the FHFA of cover-up of the Common Equity Sweep.

Why is it important?

1- The Lamberth case ends: the Class Action didn't put an end to the controversy, which is one of the prerequisites in the Rule about Class Actions (let alone that the $FNMA holders were excluded).

This is why the appeal in the Wazee case, which is the first case that challenges the SPS LP increased for free (though brought in a 3rd amended complaint recently), was recently postponed to May 25th by the attorney Hamish Hume, also an attorney in the Lamberth court. He knows that he would dinamite his own case in the Lamberth case, the very moment he complains about an unsolved issue.

This is why it's being concealed. "Unsolved issue? What issue? Everything is fine! Weee!"

2- Timothy Howard conceals the ongoing Common Equity Sweep, where necessarily, the Common Equity is held in escrow, as per the CFR 1237.12. Gifted SPS LP is a capital distribution restricted. Then, we use the exception (for their recapitalization, that (c) supplements and shall nor replace or affect the Restriction on Capital Distributions by statute) to legalize this action: Common Equity held in escrow, because recapitalization means regulatory capital, not Net Worth increase with SPS.

And the key, it would uncover the Separate Account plan altogether, because it occurred the same with the dividend payments to the UST. Another capital distribution restricted and the exceptions kick off:

-Paydown of the SPS. 12 U.S. Code § 4614 (e).

-Recapitalization: CFR 1237.12.

No actual dividend was ever paid. Besides, unavailable earnings for distribution as dividend, out of Accumulated Deficit Retained Earnings accounts.

They were assessments sent to UST in the form of capital distributions, FHLBanks-1989 style.

A LOT GOING ON WITH A SIMPLE:

annual earnings per share are $2.75, making their current P/E ratio just 0.56

was this ever unsuspended? did they ever announce further action on the capital as they say below? it says they they are building capital but we have been reading they aren't and that capital belongs to treasury as nws 2.0 ? what am i missing? unfinished business? for a reason?

FHFA and Treasury Suspending Certain Portions of the 2021 Preferred Stock Purchase Agreements

"The Enterprises will continue to build capital under the continuing provisions of the PSPAs".

"Additionally, FHFA is reviewing the Enterprise Regulatory Capital Framework and expects to announce further action in the near future."

https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-and-Treasury-Suspending-Certain-Portions-of-the-2021-Preferred-Stock-Purchase-Agreements.aspx

It absolutely baffles me that no one in restructuring from any of the major investment banks have had the common courtesy to let Tim Howard know how wrong he is about the capital raise.

"today introduced OTC Overnight, a new offering that will make OTC equity securities available for trading Sunday through Thursday between 8 PM and 4 AM eastern time"

when does this mania begin?

What a clown.

The share price isn't as important as % of equity ownership.

One $100 is equivalent to five $20 which is also equivalent to one hundred $1 bill.

and treasury can sell some of the warrants back to the companies for a nominal value. they paid like $0.001? sell it back for $0.01, that is 10x profit. lol..

tim howard today

"Midas–I want to address your question: “If a capital raise in light of all [the negative actions against Fannie and Freddie that Treasury has taken in the past] would be possible without a senior-to-common exchange, why would it not be possible with one? I can’t understand why outside investors would consider all of the above to be okay, but would see a senior-to-common exchange (which doesn’t affect these investors at all) as the final straw.”

I’ll start by repeating that a capital raise by Fannie and Freddie ISN’T possible as long as Treasury’s senior preferred stock and liquidation preference remain on their books. So where we seem to be in disagreement is over whether the way in which Treasury eliminates the seniors and the liquidation preference will make a difference in the companies’ capital-raising ability (and stock price).

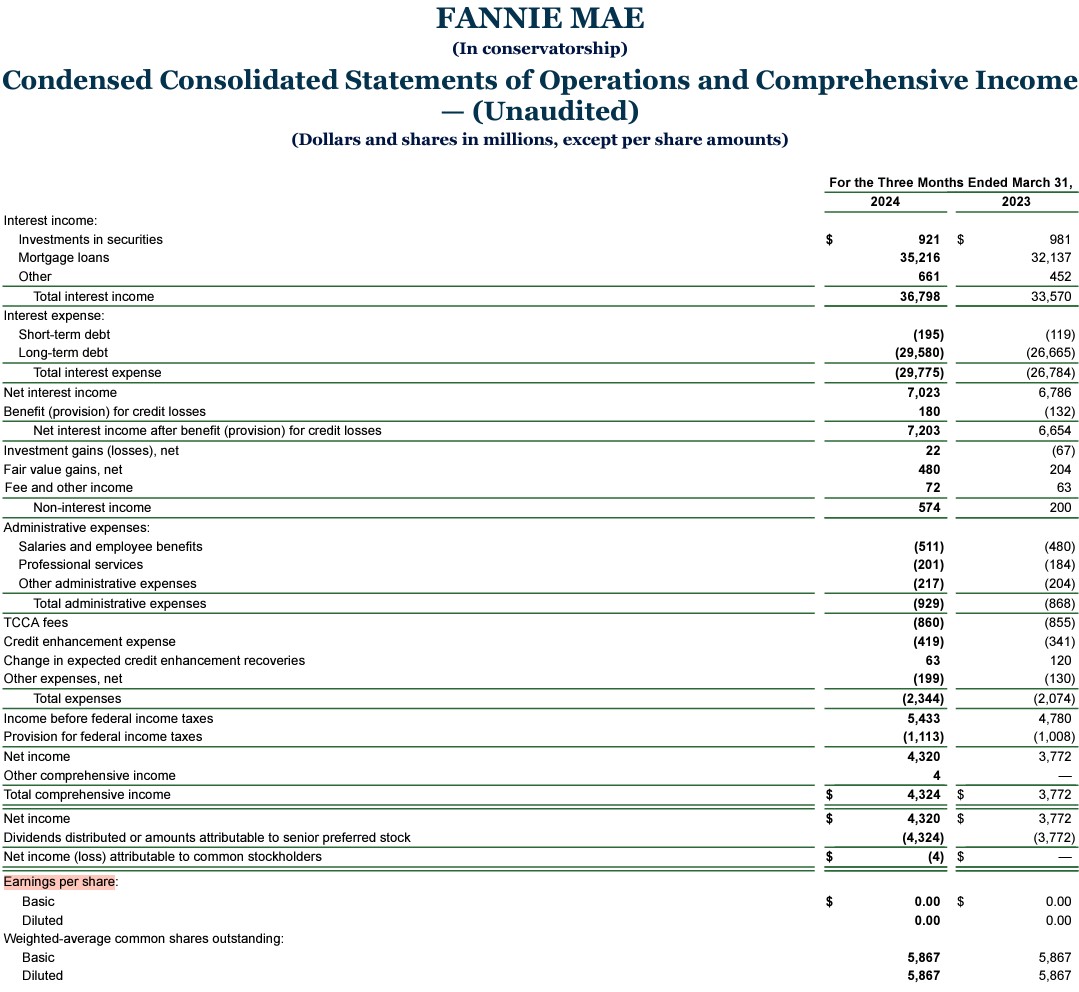

My analysis of this question starts with the facts we know: that Fannie has 5.867 billion of fully-diluted shares of common stock outstanding (assuming conversion of the warrants by Treasury), Freddie has 3.234 billion of fully-diluted shares of common outstanding, and that as of yesterday the companies’ weighted average common stock price was $1.53. Assuming sustainable combined annual earnings of $25 billion, Fannie and Freddie’s weighted average annual earnings per share are $2.75, making their current P/E ratio just 0.56, compared with about 25 times earnings for the average common stock in the S&P 500.

Why is Fannie and Freddie’s combined P/E so low? Almost certainly it’s because the only way existing (or new) common stockholders ever will get the rights to the companies’ earnings or assets is if Treasury cancels the net worth sweep (which will kick in again after Fannie and Freddie achieve full capitalization), redeems or cancels the senior preferred, and eliminates its liquidation preference. A 0.56 P/E on the companies’ $25 billion in annual earnings is the market telling us it thinks there is little chance of any of these things happening on terms favorable to common shareholders.

Treasury can change that, if it wishes. I agree with you that all of its past actions that were prejudicial against and unfair to Fannie and Freddie will have a long-lasting and possibly permanent impact on how high the companies’ P/E can be. But I also believe that how Treasury behaves toward Fannie and Freddie in the future can, and will, make a significant difference in how far above the current 0.56 times earnings, and towards the 25 times earnings multiple of the S&P 500, Fannie and Freddie’s P/E can go.

I don’t know what Treasury wants to do with, and about, Fannie and Freddie, and it’s possible that it doesn’t either. But I do think it’s true that the negative actions of prior Treasuries against the companies in the past–forcing FHFA to place them in conservatorship while still adequately capitalized, encouraging FHFA to maximize the amount of senior preferred they had to draw by loading up their income statements with anticipatory, estimated, or overly conservative non-cash expenses, then proposing the net worth sweep just as many of those non-cash charges were about to reverse and become income–were taken because Treasury (and the Financial Establishment) intended to replace the companies with some secondary market mechanism more to their liking. That’s no longer on the table. Virtually everyone now agrees that Fannie and Freddie have the best business model for the functions they were chartered to perform. For that reason, if Treasury does implicitly agree that its past actions with respect to the companies did not have the effect it had hoped for, and unwinds the most damaging elements of those activities (the net worth sweep, the seniors and the liquidation preference), I believe the market would be inclined to put a much higher value on Fannie and Freddie’s future earnings. If, on the other hand, Treasury converts the seniors to common, that would be an unmistakable affirmation that its prior anti-shareholder policies towards the companies have not changed at all, and in that instance I don’t know why their P/E would move any higher than it is now (indeed, it likely would move lower).

Again, I’m not predicting what Treasury will do, whether in this administration or a future one. But I am saying that if Treasury decides one of its objectives is to maximize the value of its current ownership in Fannie and Freddie (via conversion of the warrants), it should do so by canceling, rather than converting, the seniors."

Oh wow. No worries. We are next.

https://finance.yahoo.com/news/these-stocks-ripped-even-higher-than-gamestop-in-the-meme-rally-165649464.html

|

Followers

|

2323

|

Posters

|

|

|

Posts (Today)

|

3

|

Posts (Total)

|

801586

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader EternalPatience jeddiemack FOFreddie | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |