Saturday, May 18, 2024 12:42:27 AM

The PERs are N/A or 1,000+ when it's close to $0.

This is unacceptable for the former CFO.

As I commented yesterday, he uses the Net Income instead of the Net Income Attributable to Common Shareholders, to calculate the EPS.

Watch the Income Statements is the first thing I do when FnF post their Earnings reports. Primarily, because I want to see whether there's been Provision for Loan Losses or reserve release. Also the amount of Derivative Gains/Losses and finally, either the qoq and yoy growth in the Net Revenues.

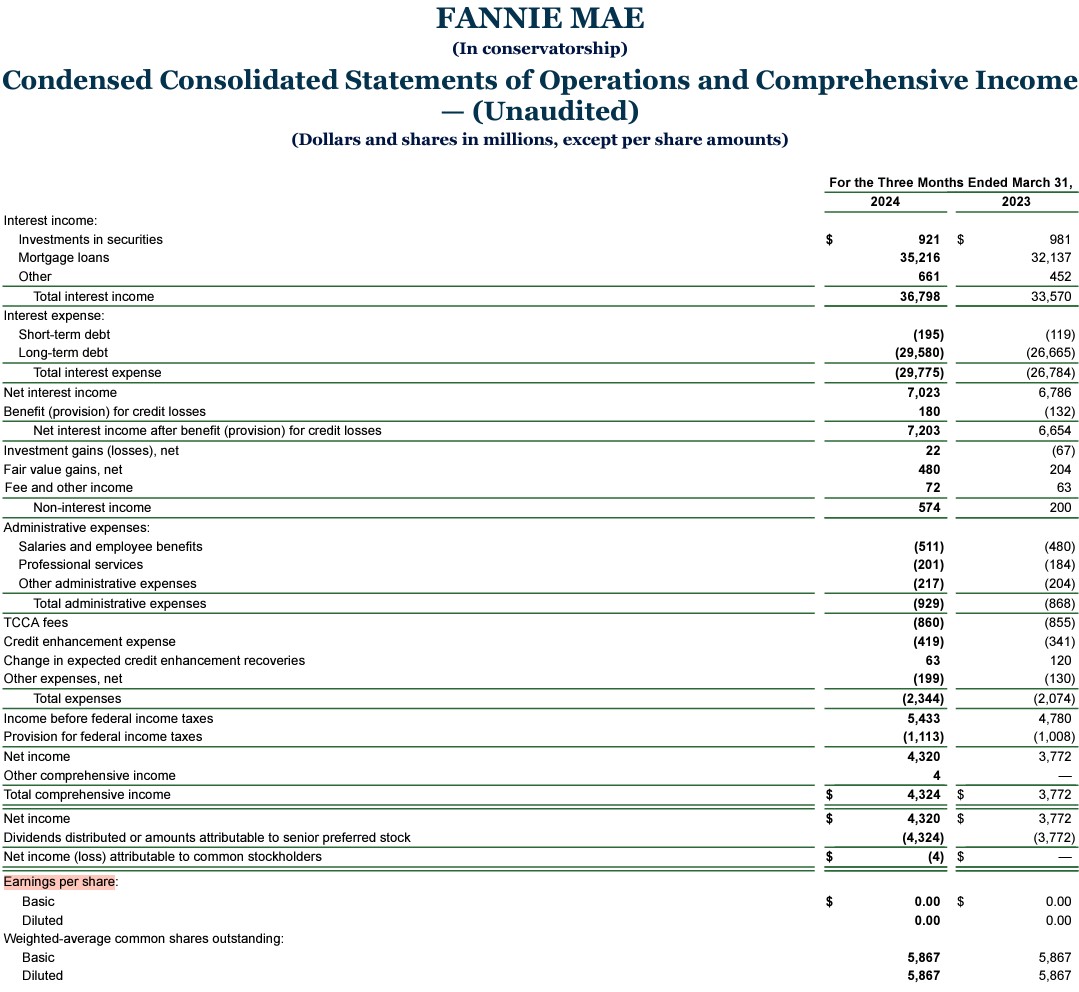

The EPS is posted at the bottom of the Income Statement. Always $0 or slightly positive or negative.

There are no excuses to not see the EPS, just knowing that the SPS LP is increased every quarter in the same amount as the Net Worth increase, and everyone should have a look to the Income Statements to see how FnF are recording this fact.

No excuses for the Bloomberg Terminal posting the KBW's EPS estimates of $3 in 2024 and 2025, outliers in comparison with the previous ones of $0. Or Guido, Pagliara's clerk, insisting on $3 EPS in this board.

We are witnessing a con operation to conceal the ongoing Common Equity Sweep with the SPS LP increased for free and its offset (reduction of Retained Earnings account), both absent from the Balance Sheets (Financial Statement fraud)

The Common Equity (Retained Earnings account) is being swept, the moment it's substituted for SPS in the Net Worth of FnF, as seen in the image with the adjusted figures.

So, these lowlifes double down on the same fraud of FnF and the FHFA of cover-up of the Common Equity Sweep.

Why is it important?

1- The Lamberth case ends: the Class Action didn't put an end to the controversy, which is one of the prerequisites in the Rule about Class Actions (let alone that the $FNMA holders were excluded).

This is why the appeal in the Wazee case, which is the first case that challenges the SPS LP increased for free (though brought in a 3rd amended complaint recently), was recently postponed to May 25th by the attorney Hamish Hume, also an attorney in the Lamberth court. He knows that he would dinamite his own case in the Lamberth case, the very moment he complains about an unsolved issue.

This is why it's being concealed. "Unsolved issue? What issue? Everything is fine! Weee!"

2- Timothy Howard conceals the ongoing Common Equity Sweep, where necessarily, the Common Equity is held in escrow, as per the CFR 1237.12. Gifted SPS LP is a capital distribution restricted. Then, we use the exception (for their recapitalization, that (c) supplements and shall nor replace or affect the Restriction on Capital Distributions by statute) to legalize this action: Common Equity held in escrow, because recapitalization means regulatory capital, not Net Worth increase with SPS.

And the key, it would uncover the Separate Account plan altogether, because it occurred the same with the dividend payments to the UST. Another capital distribution restricted and the exceptions kick off:

-Paydown of the SPS. 12 U.S. Code § 4614 (e).

-Recapitalization: CFR 1237.12.

No actual dividend was ever paid. Besides, unavailable earnings for distribution as dividend, out of Accumulated Deficit Retained Earnings accounts.

They were assessments sent to UST in the form of capital distributions, FHLBanks-1989 style.

A LOT GOING ON WITH A SIMPLE:

annual earnings per share are $2.75, making their current P/E ratio just 0.56

Cannabix Technologies and Omega Laboratories Inc. Provide Positive Developments on Marijuana Breathalyzer Testing • BLO • Jul 11, 2024 8:21 AM

ECGI Holdings Enhances Board with Artificial Intelligence (AI) Expert Ahead of Allon Apparel Launch • ECGI • Jul 10, 2024 8:30 AM

Avant Technologies to Meet Unmet Needs in AI Industry While Addressing Sustainability Concerns • AVAI • Jul 10, 2024 8:00 AM

Panther Minerals Inc. Launches Investor Connect AI Chatbot for Enhanced Investor Engagement and Lead Generation • PURR • Jul 9, 2024 9:00 AM

Glidelogic Corp. Becomes TikTok Shop Partner, Opening a New Chapter in E-commerce Services • GDLG • Jul 5, 2024 7:09 AM

Freedom Holdings Corporate Update; Announces Management Has Signed Letter of Intent • FHLD • Jul 3, 2024 9:00 AM