News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Scotts Miracle-Grow - >>> Hawthorne Looks to Strike Out on Its Own

Green Market Report

12-5-23

https://www.greenmarketreport.com/hawthorne-looks-to-strike-out-on-its-own/

The company is positioning itself to become profitable again.

Hawthorne, the hydroponic subsidiary of fertilizer company The Scotts Miracle-Gro Co. (NYSE: SMG), is looking to strike out on its own – a move that Scotts CEO Jim Hagedorn hinted at on the company’s earnings call in November.

“We’ve made progress on a range of potential solutions that should benefit shareholders and create opportunities for that business to grow,” Hagedorn said about Hawthorne at the time. “We’re in active discussions to create a leading vertically integrated cannabis company. I can’t share more at this time, but we will provide an update as soon as we can.”

Just a few years ago, Hawthorne was riding high as the cannabis industry’s mantra was bigger is better. Multistate operators were competing with each other over who could build the biggest grow facilities – and that meant lots and lots of lights.

However, the cannabis bubble burst and the business wilted. Hawthorne President Chris Hagedorn made difficult decisions to adjust to the new reality and eliminated almost a thousand jobs. He restructured debt and cut expenses.

Now the company is positioning itself to become profitable again.

Options

Green Market Report spoke with Jim and Chris Hagedorn at the MJBiz Conference last week, where the two opened up about the options being considered. Essentially, there appear to be two roads out of Scotts:

Spinning out into a separate public company

Joining forces with Riv Capital (TSX: RIV) (OTC: CNPOF), which has an investment connection with Hawthorne

“We’ve said as much publicly, but I think the interesting part of the conversation is why?” Jim Hagedorn said. “(Scotts will) keep the debt. You move it without any debt at all. So completely clean. Hundreds of millions of inventory and upward capital.”

New PubCo

Scotts could spin Hawthorne out into its own public company where it would compete with the likes of Ubi-grow, Agrify, and Grow Generation. However, these companies receive little analyst coverage, and there is concern that Hawthorne’s assets wouldn’t be recognized.

Hawthorne has engaged in considerable research, and Chris Hagedorn doesn’t want that to get lost by being lumped in with other hydroponic companies.

Riv Capital Option

Riv Capital and Hawthorne are already associated with each other. In 2021, RIV Capital Inc. signed a deal with The Hawthorne Collective, a cannabis-focused subsidiary of Scotts for the purchase of a $150 million unsecured convertible note from RIV Capital.

However, Riv Capital is best known for paying top dollar to buy New York medical operator Etain. The Hagedorns acknowledged the criticism that the deal received but maintain that the New York market still holds great promise.

Jim Hagedorn pointed out that Riv Capital is currently sitting on almost $90 million in cash, but it only has a market cap of roughly $10 million.

In Talks

“So the audience of people who we’re talking to, we haven’t had anybody yet say no. The question is how do we do this so that we create a company that you would look at and say, holy f*ck,” Jim Hagedorn said. “I sat with those guys and they were giving me big time hints that there is going to be a consolidation here that’s sort of across the board that creates the best pot company in the United States.

“There are different permutations on how to get there. And these are conversations that are live right now,” he added.

Chris Hagedorn noted that in those conversations, they’ve been told, “We see the R&D you guys do. They look at it as there’s the tax-yielding, which is exciting because everyone’s looking for tax mitigation. Hawthorne has the highest possible quality produced at the lowest possible cost.”

The pair believe that cannabis will be rescheduled next year, which will release a lot of capital into the market. And with that there’s a lot of opportunity ahead for Hawthorne.

<<<

---

Derf, With the recent inflation numbers coming in higher than expected, and analysts pushing back their Fed % pivot date from June to July or later, the interest rate sensitive sectors in particular have sold off significantly today. Oh well, so much for my 'buy small caps, REITS, utilities' strategy lol. But the CPI and PPI numbers are just for one month, so we'll see how things look in the months ahead.

Anyway, while liftoff for the % sensitive sectors might be delayed, these still seem like logical areas to be in for the next several years as % rates gradually trend lower. But the techs and growth sectors should also do well in that environment, so one solution ---> own the S+P 500 and get all sectors :o)

Btw, I see ADM is still above the 50 MA. It didn't quite reach 60 intraday, but pretty close. My solar plays ENPH, FSLR are looking weak, as these are particularly sensitive to % rates, so looks like the recovery will be delayed. I only own a few shares though.

Just curious if you are still in SMG? The chart setup does look interesting, though I figure the cannabis landscape may have to improve to really get a recovery going. Here's some info on SMG's Hawthorne unit (next post), and looks like they are working on it to become a separate company.

---

Derf, ADM left a somewhat ambiguous candlestick today. It stayed above the 50 MA, so that's good, but looks like some heavy profit taking volume in the last hour. So might go either way tomorrow, probably a modest pause / pullback (a guess), but then more upside next week? Just guessing though. I'm not an experienced trader, but did spend a year subscribed to Stockcharts.com for their online 'chart school' (Art Hill), and had a good aptitude for it, but mainly just learned the basics and never really tried it much for active trading.

With the Fed meeting next Tues + Wed, I figure the market could be somewhat subdued until that's over. I used to call Powell 'Grumpy Jerome', but after the Fed's dovish pivot last Fall he has mellowed considerably. But if he senses the stock market getting overly buoyant, he might go back toward the grumpy side, at least verbally.

But based on Nick Timiraos' articles (link below), the Fed clearly plans to start easing, the only question being when. June is most likely, but subject to the ongoing data. Timiraos is well known on Wall Street as the designated Fed mouthpiece, who is tasked with leaking Fed policy guidance to Wall Street so there are fewer surprises. The guidance is contained in his headlines, so it isn't really necessary to subscribe to WSJ for the full articles -

Nick Timiraos - Chief Economics Correspondent at the Wall Street Journal -

https://www.wsj.com/news/author/nick-timiraos

---

Derf, >> get it and move on <<

With a short term trade as the strategy, the question is how long the current bounce will last. If it closes today near the high of the day, then the current bounce might continue and get to 60-62 before a pullback (a guess). But if it leaves a bearish candlestick today, then a pullback to the 50 MA level occurs first, and then re-evaluate for another bounce. So have to play it by ear. But I'm not an experienced short term trader, so would just be winging it.

That said, if it moves up sharply in the near term, I might be tempted to book the short term profit and then try to reload after a pullback. That's what happened with SMCI -- got lucky and now have the luxury of the 1/2 free shares to hold longer term. The initial strategy wasn't for a short term trade, it only turned out that way for 1/2 of the position. It would sure be great if things always worked out that way. Btw, thanks again for your 1000 call, it was spot on and signaled the near term top and subsequent 30% retracement.

---

The amount shouldn't matter as much. If you are a poker player, having $100 in chips in a $1-2 game is the same as having $1000 in a $10-20. You still don't want to end up at zero.

Now, if you are in the $10-20 game and making a small bet, it might not matter to you.

I've always laughed at the people who only post daily on penny stock boards, then claim the money doesn't matter if they lose it. If so, why are they only posting about making money on penny stocks? It's the equivalent of broke people buying lottery tickets.

Now, once again, on ADM....I think we are both in agreement on the short term price target...but I'd like to get it and move on. I am not impressed with the future. I don't see this as slow and steady, I see this as slower....

Derf, Another way to view ADM would be as a shorter term bounce play. Today it got through the 50 MA resistance (for now), and above that is the big gap going up to 67.5. Tough to say, but it might get to 60, then pull back to re-test the 50 MA. Then if that holds it could work its way up into the gap area, maybe get mid-way into the gap, say 63-65. So a decent short term trade idea. But just a guess, and will depend upon news flow and the overall market.

With a whopping $345 at risk, I'll probably just sit with it longer term. That's one advantage to having tiny positions --> minimal Tagamet required :o)

---

From what I'm seeing in their projections, they had a huge earning year in 2022 and the stock got overextended. Now it is back in line with its very slow growth, and in fact, I see the earnings growth pretty much non-existent for the next few years. It's pretty much just a dividend growth story now....which is ok, but I think if it fills its gap, it will not break through its resistance. I'd say fair market value on this stock is between $58-62.

Derf, With ADM, I figure the recovery could be bumpy due to news flow, etc. But it's a solid company with a dominant position in its industry, so in a year or two the stock should be recovered and back on track. So the 40% haircut is just temporary, which would make this a buying opportunity. But will need to be patient.

ADM has reportedly been trying to move into higher margin areas, and management apparently linked their bonuses to the performance of that newer Nutrition Unit. But when the unit was taking too long to get rolling, they apparently tweaked the unit's numbers in order to keep their bonuses high. That's what it sounds like anyway. So not good, but I figure in a year the stock has recovered, making the current selloff a bargain for patient investors. Sounds logical, but we'll see what happens. Either way I only have a small position.

---

it's true, I've become worried.

The only thing I can see saving Wall Street is massive inflation and a screwed up government

Derf, >> AVGO <<

It's almost back to the 50 MA, so will see if that holds. But the other semis haven't pulled back as much as AVGO has. Looking at ASML, KLAC, and the Semiconductor ETF (SOXX), they are less than halfway back to their 50 MAs. So might be more downside to the pullback, but tough to say. Either way though, I figure longer term this sector should continue to be a winner. Just look at the steadiness and trajectory of AVGO's 10 year chart. The techs have merely gotten ahead of themselves in recent months, so some consolidation is needed and would be healthy.

Fwiw, I figure some of the out of favor sectors and stocks could now play catchup - small and mid caps, and some of the % rate sensitive areas like REITS and utilities could start to recover as the Fed eases this summer. The market will have a nice tailwind from the falling % rates for the next several years. So that leaves geopolitical events and the election as the main landmines lurking out there. But as the old saying goes - 'A bull market climbs a wall of worry'.

---

OK, so I bought a few hundred shares of ADM this morning. Remind me when it gets to $68.

Geez! I definitely jumped the gun on AVGO. I fear a very large retracement coming.

It did break the trend today. Maybe you should add another 6.

Derf, >> ADM <<

I have all of 6 shares, so a less than 'tiny' position :o)

---

ADM may turn into a hero for you.

Derf, I picked up a little PFE and ADM today since it looks like the bottoms 'might' be in, or close enough. Only small positions though. Both are stalwart long term type stocks at a big discount, so what the heck.

---

>>> ADM Rises After Revising Years of Internal Unit Sales

Bloomberg

by Gerson Freitas Jr.

March 12, 2024

https://finance.yahoo.com/news/adm-revises-years-internal-sales-111050920.html

(Bloomberg) -- Archer-Daniels-Midland Co. investors appeared to breathe a sigh of relief Tuesday, driving the commodity giant’s shares higher after its delayed annual report didn’t deliver the kind of bombshell financial revelations some had feared.

In its annual report, ADM revised its intersegment sales for the last three years following an internal probe into its financial reporting and disclosed a $137 million impairment charge related to its animal nutrition unit. ADM confirmed in its annual filing that the various adjustments didn’t impact overall earnings.

“ADM could have been worse,” Vital Knowledge wrote in a note after the company provided a long-awaited update on its internal investigation into its financial reporting. It also reported quarterly results, offered guidance for 2024 and announced a $2 billion share buyback, which together helped drive shares higher, it said.

Shares rose as much as 5.6%. ADM’s stock price had earlier fallen about 19% since Jan. 19, the last trading day before it disclosed the investigation.

The adjustments and charge gave investors one of their first indications of the magnitude of the scandal that had wiped out more than $7 billion in ADM’s value since first disclosed earlier this year. Overall, the adjustments “were not as significant as some feared,” analysts for Citi Research said in a note, calling the changes “relatively minor.”

In January, ADM stunned the agricultural trading and processing world when it suspended its chief financial officer, Vikram Luthar, pending a probe into accounting practices at its nutrition unit following a request for information from the US Securities and Exchange Commission. The company said little about the probe in subsequent weeks, before disclosing earlier this month that the “material weakness” it had uncovered in its internal controls wasn’t expected to have a broader impact on earnings.

“The company did not have adequate controls in place around measurement of certain intersegment sales” between its nutrition segment and other key units, Chief Executive Officer Juan Luciano said in the filing. ADM has put in place a plan to remediate this material weakness, it said. Luciano said on an earnings call that he would not take questions about the investigation.

The changes include a $31 million reduction in 2023 segment operating profit for the nutrition unit, and cuts of $68 million and $59 million in 2022 and 2021, respectively. It also restated gross revenues for the segment. In addition, it has released adjusted segment operating profit going back to 2018. The investigation covered the period between January 2018 and September 2023.

To be sure, ADM is not out of the woods yet. The company confirmed in the filing certain current and former employees have received subpoenas from the Department of Justice.

ADM has spent billions expanding its nutrition business since 2014, when it made its biggest-ever acquisition — the $3 billion buyout of European natural ingredient maker Wild Flavors — in a bid to diversify from row crop grains and oilseeds into processed products. ADM also spent about $1.8 billion to buy an animal feed maker in 2019. But the unit’s profits have failed to live up to initial expectations due to weakening demand, including for plant-based food, raising questions about ADM’s big growth bet.

In a separate filing, ADM reported fourth-quarter earnings and offered 2024 guidance. It sees adjusted earnings per share in the range of $5.25 to $6.25 per share, down 18% compared to 2023 using the midpoint of the range.

<<<

---

>>> NextEra Energy -- Fossil fuels aren't going away anytime soon, but renewable energy has steadily contributed more to America's electric grid. NextEra Energy (NYSE: NEE) is one of the world's largest green energy producers and the largest electric utility business in the United States. Growth in renewable energy has fostered big investment returns. Since going public, NextEra has beaten the S&P 500.

https://finance.yahoo.com/news/4-supercharged-dividend-stocks-buy-131600987.html

The company is also an excellent dividend growth stock. The payout has increased for 30 years, and investors get a solid 3.7% starting yield.

The best part? Its dividend growth. Management has raised the dividend by an average of 11% annually over the past five years and is guiding for 10% increases through at least this year. That makes NextEra a dividend growth stock you want to snap up whenever the price dips.

<<<

---

Pfizer - >>> 2 Dirt Cheap Dividend Stocks to Buy and Hold

by Prosper Junior Bakiny

Motley Fool

March 11, 2024

https://finance.yahoo.com/news/2-dirt-cheap-dividend-stocks-134500534.html

Dividend stocks are great for several reasons. Some use the regular payouts they offer to complement their income, whether in retirement or otherwise, while others reinvest the money to boost long-term returns. Dividend stocks have generally outperformed their non-dividend-paying peers over long periods.

Clearly, this mode of investing has advantages, but if there's one thing better than investing in dividend stocks, it's investing in cheap dividend stocks. Let's consider two companies that fit the bill: Pfizer (NYSE: PFE) and Viatris (NASDAQ: VTRS).

1. Pfizer

Last year, Pfizer's revenue dropped by 42% year over year to $58.5 billion. The decline was due to the receding pandemic. Demand for Pfizer's COVID-19 vaccine, Comirnaty, and its related medicine, Paxlovid, dropped off a cliff. Still, the drugmaker's current slump won't last forever.

Pfizer already has a plan to turn over a new leaf. Last year, it earned approval in the U.S. for seven brand-new products, more than double any of its competitors' total for 2023.These products will eventually help Pfizer's revenue start moving in the right direction.

It's also worth noting that Pfizer's underlying business, excluding its coronavirus portfolio, isn't performing that badly: Revenue increased by a solid 7% year over year in 2023. Pfizer's decision to join the COVID-19 market has been a net positive despite its current declining top-line. It became the company in the pharmaceutical industry to hit $100 billion in sales in 2023 thanks to it. The money it generated allowed it to invest in the future.

Pfizer made important acquisitions, including that of cancer specialist Seagen, for $43 billion. Seagen was already a successful oncology-focused biotech before having access to the kinds of funds Pfizer has. The newly formed entity under Pfizer should speed up innovation compared with what it would have been able to accomplish by itself. Pfizer plans on increasing the number of blockbuster cancer medicines in its portfolio to eight by 2030, up from five today.

Of course, Pfizer is also active in many other areas, from immunology to infectious diseases. It's developing an influenza vaccine to help address the low efficacy of currently available options. The drugmaker is also working on a combined COVID/flu vaccine. Both are in late-stage studies. Pfizer boasts 112 candidates in its pipeline. The company should significantly improve its lineup in the next few years, even more than it already has.

As for the dividend, the company has increased its payouts by just under 17% in the past five years. It offers a forward dividend yield of 6.18%. Lastly, Pfizer's forward price-to-earnings (P/E) ratio is just 12, compared with a forward P/E of 18.4 for the pharmaceutical industry. So Pfizer looks like an attractively valued dividend stock by this popular metric.

2. Viatris

Viatris hasn't been a standalone, publicly traded corporation for very long. The company was created when Pfizer's former subsidiary, off-patent drug specialist Upjohn, merged with the corporation then known as Mylan N.V., which focused on developing and marketing generic drugs, back in late 2020.

The company's position in the market for generic and branded pharmaceutical products is enviable. It owns several popular brands that should continue attracting customers for a long time. These include Viagra, Xanax, Lipitor, and more. This business creates a somewhat stable source of revenue for the company.

Viatris has also significantly changed its operations recently by shedding lower-growth opportunity segments. For instance, it got rid of its biosimilar and women's healthcare units. Besides cutting off low-growth opportunities, Viatris planned to pay off debt while investing in more potentially lucrative avenues.

The company created a new eye care division through acquisitions and announced a research and development partnership with Switzerland-based pharmaceutical company Idorsia. Viatris added two potential blockbuster candidates to its late-stage pipeline through the Idorsia deal, while it expects its new eye care unit to add more than $1 billion in annual sales by 2028.

Viatris has struggled with top-line growth. Last year, its net sales of $15.4 billion remained flat on an adjusted basis (that is, taking into account acquisitions and divestitures). However, thanks to recent business changes, the company could make significant progress on that front in the years ahead. Meanwhile, Viatris offers a forward yield of 3.89%, though it has increased its dividend just once since it became a standalone company.

Viatris' forward P/E ratio of 4.4 looks more than reasonable. For income seekers willing to stay the course for a while, Viatris looks like a good option.

<<<

---

Yeah, Woolworth's was a turnaround story.....there are many companies that were a turnaround....until they weren't. Sears, K-Mart, JCP....

I just find it a better strategy to wait.

Derf, >> stocks on the way up <<

Yes, owning something that's already in an established uptrend has the best odds for success. Trying to guess a bottom is dicey at best. But within the broader 'turnaround' category, there are relatively safer situations when the stock has had a long history as a solid long term stock, has formed a convincing bottom, etc. Something like Pepsico being down 15% would be a great bet on an eventual recovery, but it's not really a turnaround, more of a 'contrarian value'. HSY down 30% would be closer to a 'turnaround', and NEE down 50% would be even closer.

But either way, better to not go overboard with these contrarian value plays. As Buffett said - 'the trouble with turnarounds is that they never turn around'. I was surprised to hear Buffett say that though, considering he originally came from the Ben Graham 'cigar butt' school of extreme value investing.

---

Nope, it was DUK and I still can't explain it.

As to NEE, I prefer to buy my stocks on the way up vs the way down. I'd rather miss a little profit more often than be wrong by a lot too early.

I used to know a guy who was great at picking stocks.....but always 4 months too early.

So I started saving his picks on the calendar. Worked out much better

Derf, >> DUK <<

Just a guess, but you might be thinking of Duke Realty (DRE) (?) I remember my dad had some DRE, and after it was bought out by Prologis there may have been a hassle at tax time. Not sure though. DUK is Duke Energy, so a regular utility stock as far as I know.

With NEE, while it's still early, I'm thinking it could be forming a bottom. With the higher % rates the utility sector has been hit pretty hard, and NEE also has the close connection with clean energy, so it got hit even harder. But I stuck my neck out recently and got a little NEE, and a tiny amount of solar exposure via FSLR and ENPH. Just small positions, but having % rates coming down should help revive the utility sector, and solar is reportedly very sensitive to % rates.

So a few small 'contrarian' positions. I figure with the techs and broader market no longer the bargains they were, it could be time to look at the lagging sectors like REITS and utilities.

---

NEE has been correcting for two years now! No real support until maybe $44.

I can recall having to file something extra when I owned DUK, which is why I sold it.

Derf, >> extra forms to file <<

With TRP, I owned it in the past and don't remember having any problems, but it's probably best to do more research, especially if you are getting a sizable position. In the past I had problems 'staying the course' with stocks, so may not have owned TRP long enough to get a dividend distribution.

Other out of favor sectors with high yields include the utilities, and I recently picked up a little DUK and SO, plus NEE as a turnaround. These have nice dividends over 4%, with NEE at around 3.5%.

With dividends, I usually avoid the really high div stocks, and look more for good long term holdings, with the dividend yield as secondary.

---

TRP looks like a winner. Are you sure, since it's Canadian, there are no extra forms to file?

Derf, >> to find a high yielding dividend paying stock with a low P/E <<

Here are some dividend stocks ideas (link below), with yields of 2% or more. I recently added some additional REITS figuring that these should benefit as % rates come down over the next several years. As a sector, the REITS got hit by the Fed tightening, and also from the commercial / office real estate problems. I figure that sub-sector should probably still be avoided, but the other REIT areas should gradually recover and most have nice dividend yields --> data center REITS, industrial warehouse REITS, wireless tower REITS, and the storage REITS. There's also a roadside ad / billboard REIT (LAMR) that has done well over time and has a dividend yield over 4%.

Another high dividend area I recently added are several pipeline stocks - ENB, TRP, which are yielding over 7%. These are a lot less volatile than regular energy stocks, and I figure even if they don't go up, the 7% dividend by itself is a good enough reason to own them for the long term. I only have small positions though. Owning these (ENB, TRP) also avoids the tax reporting problems of the pipeline LPs.

Dividend Stock Ideas -

https://investorshub.advfn.com/Dividend-Stocks-28771

---

I bought some CCI back in December. Still flat as it failed to break through, but still holding hope.

I've owned AMT during the huge run up, fortunately got out in 4/22, when it broke below support.

I also still own NXST. Bought and sold it in 2021, but back back a half position in 2022, which so far is flat. It is a decent dividend though. In the last 4 years they've tripled the dividend.

OK, so this is the reason I've started reading your posts. I've never even heard of EME, FIX, and MEDP and here I've missed them all!

From your other posts, the one I liked the best is $ADI. A bit overextended here, but I like that they've raised their dividend yet again. Although, reading a tad further, it looks like projected earnings are dropping. I'll have to keep an eye on it.

At the moment, I need to find a high yielding dividend paying stock with a low P/E.

Wireless tower REITS - AMT, CCI, SBAC -

>>> American Tower(AMT), one of the largest global REITs, is a leading independent owner, operator and developer of multitenant communications real estate with a portfolio of over 224,000 communications sites and a highly interconnected footprint of U.S. data center facilities. <<<

>>> Crown Castle owns (CCI), operates and leases more than 40,000 cell towers and approximately 90,000 route miles of fiber supporting small cells and fiber solutions across every major U.S. market. This nationwide portfolio of communications infrastructure connects cities and communities to essential data, technology and wireless service - bringing information, ideas and innovations to the people and businesses that need them. <<<

>>> SBA Communications Corporation (SBAC) is a leading independent owner and operator of wireless communications infrastructure including towers, buildings, rooftops, distributed antenna systems (DAS) and small cells. With a portfolio of more than 39,000 communications sites throughout the Americas, Africa and in Asia, SBA is listed on NASDAQ under the symbol SBAC. Our organization is part of the S&P 500 and is one of the top Real Estate Investment Trusts (REITs) by market capitalization. <<<

---

Signs of a bubble --> Single stock leveraged ETFs -

>>> Inflows into bullish Nvidia ETF hit record on AI frenzy

Reuters

Mar 7, 2024

By Bansari Mayur Kamdar

https://finance.yahoo.com/news/inflows-bullish-nvidia-etf-hit-155124143.html

(Reuters) - Investors have piled into Nvidia-focused exchange-traded funds (ETFs) this year on the frenzy around AI, with inflows into a bullish fund that tracks the shares of the chip designer hitting an all-time high on Wednesday.

Net daily inflows into the GraniteShares 2x Long NVDA Daily ETF hit a record of $197 million, according to LSEG Lipper data. The assets managed by the ETF have grown to $1.41 billion from $213.75 million at the start of the year.

WHY IT'S IMPORTANT

Risk-averse investors have largely stayed away from leveraged ETFs tracking single stocks that aim to provide returns over extremely short periods.

These ETFs, which made their U.S. debut in 2022, have become popular among speculators looking to bet on the most volatile shares based on earnings and other news.

CONTEXT

Nvidia, which controls about 80% of the high-end AI chip market, has surged nearly 82% since the start of the year after a stellar forecast and amid renewed euphoria around AI.

Leveraged single-stock ETFs seek to amplify the returns of an underlying stock for a single day, generally by two or three times, using financial derivatives and debt as leverage.

KEY QUOTES

"Nvidia has been the hottest stock in 2024 and many investors are eager to seek out higher returns in exchange for added risk," said Todd Rosenbluth, chief ETF strategist at VettaFi.

"We expect to see continued demand for single stock leveraged ETFs as a new wave of must-own companies emerge."

THE NUMBERS

Net monthly inflows into leveraged ETFs tracking Nvidia such as the GraniteShares 2x Long NVDA ETF, the Direxion Daily NVDA Bull 1.5X Shares ETF and the T-Rex 2X Long Nvidia Daily Target ETF hit a record in February.

The GraniteShares ETF has already crossed its net monthly flow record within the first six days of the month.

Assets of the three Nvidia-linked ETFs jumped between five and 11 times since the start of 2024, while their prices are up between 143% and 218% year-to-date, outperforming other ETFs.

<<<

---

>>> NextEra Energy is a growth and income gem

https://finance.yahoo.com/news/3-utility-stocks-buy-hand-101100971.html

NextEra Energy's 3.7% dividend yield is modest compared to the other two utilities on this list. In fact, it is only 10 basis points above the average of the broader utility sector. But the yield is near a 10-year high for NextEra Energy, suggesting the stock is cheap today.

However, the real linchpin in the story is the average annualized dividend growth of around 10% over the past decade, extremely high by utility standards. Management expects to raise the dividend by that much again in 2024.

The story here comes in two parts. First, NextEra Energy owns the largest utility in Florida, which is a state with a growing population. That's the solid foundation. On top of that, NextEra Energy owns one of the world's largest portfolios of solar and wind power assets. This is a growth business, with management hoping to double its clean energy capacity by 2026.

The combination of these two businesses is expected to produce earnings growth of between 6% and 8% a year through 2026. Even if dividend growth only tracks along with earnings growth after 2024, that's still a great outcome for a growth- and income-oriented utility. Investors should look at this stock, which has increased its dividend annually for nearly three decades and is still on sale.

<<<

---

Derf, >> LLY <<

Yes, a lot of overextended stocks right now in need of a consolidation. Fwiw, I inventoried my own holdings this week and some are so near-term overbought it's not funny --> EME, FIX, MEDP . But since these have great long term charts, and are only small positions, I'm figuring it's best to just hang with them long term.

Btw, SMG continues to move cautiously higher. Looks like a test of 70 soon, and then a move up to 80 (Feb 2023 high) might be possible. But just a guess based on the chart. I always liked SMG's lawn + garden business, but the Hawthorne / cannabis side has been holding the stock back. If they would announce plans to spin off Hawthorne --> a fast recovery for SMG stock.

---

Derf, Good point about the class action suits, which will be a thorn in ADM's side for quite a while. That said, the chart looks like it might bounce up to the 50 MA, even if it's only a short term trade. It's a dominant company at a 30% discount, so I was thinking about a small position for the longer haul, but may just watch from the sidelines.

With Broadcom, a pullback will probably be healthy since the semis and Ai stocks have had such a big run. Along with AVGO, I have a little in KLAC, MPWR, ADI, MCHP, and NVDA. Only small positions, but I figure this makes it easier to 'stay the course' :o)

>>> Why Broadcom Stock Was Sliding Today

by Jeremy Bowman

Motley Fool

March 8, 2024

https://finance.yahoo.com/news/why-broadcom-stock-sliding-today-170211445.html

Shares of Broadcom (NASDAQ: AVGO) were moving lower Friday after the diversified semiconductor company posted solid results in its fiscal 2024 first-quarter earnings report after the market closed Thursday, but failed to raise its guidance.

High expectations were also baked into the stock. The company is viewed as a beneficiary of the AI boom, and as its shares have risen in recent months in consequence.

As of 11:59 a.m. ET, the stock was down by about 6%.

A good -- but not good enough -- quarter

Broadcom, which also just completed its purchase of VMware, said that revenue jumped by 34% in the quarter (which ended Feb. 4) to $12 billion, edging past the consensus estimate of $11.72 billion. Organic revenue, which excludes the impact of the VMware acquisition, was up 11%, accelerating from just 4% growth in the previous quarter, and the company said it was seeing strong demand for AI-related products.

In its semiconductor solutions segment, it reported 4% growth to $7.4 billion, while VMware drove a 153% jump in infrastructure software revenues to $4.6 billion.

Further down the income statement, adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) increased by 26% to $7.16 billion, and adjusted earnings per share rose 6.4% to $10.99, which beat the consensus estimate of $10.29.

CEO Hock Tan noted the strengthening tailwind in AI, saying, "Strong demand for our networking products in AI data centers, as well as custom AI accelerators from hyperscalers, are driving growth in our semiconductor segment."

Guidance falls a bit short

Friday's share price pullback seems to be driven by the company's decision to maintain its full-year guidance at $50 billion in revenue and $30 billion in adjusted EBITDA. It kept that steady forecast even as it has had one quarter to integrate VMware and as it's seeing increased demand for AI products.

Even with Friday's slide, Broadcom shares are still up 18% year to date and have more than doubled in the last year, showing the stock is benefiting from AI tailwinds. While this session's dip may be disappointing for investors, it shouldn't change anyone's long-term thesis on the stock.

<<<

---

YIKERS!!! Why in the world would you ever try to play a stock with so many class action suits against it?

I've told you before, I'm not the bottom fisher guy.

Looks to me like their projected earnings are dropping and projected FP/E may not be accurate.

Not saying it won't bounce back, it's just not a play for me.

I did buy some $AVGO today. I took a half position with about $40k worth so not totally convinced its not still overvalued. But it seems like one of the long term plays you will want to hold onto.

Meanwhile, SMCI keeps going and going like the Energizer Bunny.

FWIW, I'm starting to get a bit close to feeling like I've got too little cash on hand. When you think you've got this all figured out, a correction comes. Glad I sold half my $LLY the other day. ...I think.

Any ideas on ADM as a value play?

The chart is starting to look interesting for a rebound, but with the investigation going on, I'm thinking it might turn out to be 'value trap'. The company's comments try to minimalize the risk of earnings revisions, etc, but it looks like they finagled their numbers in order to boost management's bonuses. The big question is whether this will somehow get glossed over with minimal repercussions, or is it just the beginning of trouble for the company? The CFO is reportedly on administrative leave, pending an internal probe, and Bloomberg reports that "the US Attorney’s Office in Manhattan has launched an investigation into the reporting of inter-segment transactions", which sounds pretty serious.

The chart suggests a bounce to the 50 MA might be in the cards (58.7 area), but beyond that may require a resolution to the investigation uncertainty. Just a guess though..

---

Bausch Health -

>>> 5 Best Marijuana Stocks To Invest In

Insider Monkey

February 22, 2024

https://www.insidermonkey.com/blog/5-best-marijuana-stocks-to-invest-in-2-1263318/3/

2. Bausch Health Companies Inc. (NYSE:BHC)

Number of Hedge Fund Holders: 31

Bausch Health Companies Inc. (NYSE:BHC) is a pharmaceutical company that develops, manufactures, and markets products in various medical fields, including gastroenterology, hepatology, neurology, dermatology, international pharmaceuticals, and eye health. Bausch Health Companies Inc. (NYSE:BHC) is also involved in the medical marijuana market. Bausch’s Q4 2023 revenue rose 9.5% year-over-year to $2.41 billion, beating Wall Street estimates by $120 million.

According to Insider Monkey’s fourth quarter database, 31 hedge funds were bullish on Bausch Health Companies Inc. (NYSE:BHC), same as the prior quarter. GoldenTree Asset Management is the largest stakeholder of the company, with 27.6 million shares worth $221.7 million.

Here is what Miller Value Partners Opportunity Trust Fund has to say about Bausch Health Companies Inc. (NYSE:BHC) in its Q2 2022 investor letter:

“Bausch Health Companies Inc. (NYSE:BHC) declined during the quarter as the company consummated its Bausch+Lomb IPO at valuations far below expectations, reported disappointing Q1 2022 results, and delayed its plan to spin out its Solta (aesthetics) business due to difficult market conditions. While the company spun off 10% of Bausch+Lomb (BCLO) they retained 90% of the company which they intend to distribute once they have met their target leverage ratio of 6.5-6.7x. The future spin-off value of the Bausch+Lomb piece represents a value of $12.55 per share, 39% above where Bausch Health is currently trading. The company recently appointed John Paulsen as Chair of the Board, which should accelerate value realization.”

<<<

---

Derf, >> Absolutely no one wants this board to be on any sort of Hot! list <<

Lol, that's like a corporation saying that they don't want increasing revenues this quarter. With I-Hub, overall posting activity is way down, so they resort to inflating the numbers to maintain their ad revenues. What makes 'Latoria' suspicious is that there is no other apparent explanation for her posts. What is her motivation? She isn't pumping specific stocks, and isn't hyping her supposed business ('!F Cash Advance LLC'). Her posts are just vacuous robotic fluff, so the goal is to pad I-Hub's flagging numbers? It's one explanation anyway, especially if more 'Latorias' start showing up on I-Hub.

Btw, the SMG chart you mentioned still looks interesting. I've been watching it for several years as a deep value play, but the cannabis related side of their business (Hawthorne) is what has tanked the stock so bad. Another otherwise 'normal' stock that has an unfortunate pot connection is Bausch Health (BHC).

>>> 5 Best Marijuana Stocks To Invest In

Insider Monkey

February 22, 2024

https://www.insidermonkey.com/blog/5-best-marijuana-stocks-to-invest-in-2-1263318/3/

3. The Scotts Miracle-Gro Company (NYSE:SMG)

Number of Hedge Fund Holders: 30

The Scotts Miracle-Gro Company (NYSE:SMG) manufactures and sells lawn, garden care, and indoor/hydroponic gardening products globally. It operates through three segments – U.S. Consumer, Hawthorne, and Other. The company offers a range of lawn care and gardening products, including fertilizers, seeds, plant foods, pest control, and hydroponic equipment. The Scotts Miracle-Gro Company (NYSE:SMG) is one of the best marijuana stocks to invest in. On January 22, the company declared a quarterly dividend of $0.66 per share, in line with previous. The dividend is payable on March 8, to shareholders on record as of February 23.

According to Insider Monkey’s fourth quarter database, 30 hedge funds were bullish on The Scotts Miracle-Gro Company (NYSE:SMG), compared to 17 funds in the prior quarter. Schonfeld Strategic Advisors is the leading stakeholder of the company, with 444,336 shares worth $28.3 million.

Madison Funds made the following comment about The Scotts Miracle-Gro Company (NYSE:SMG) in its Q4 2022 investor letter:

“Stock selection was the poorest for us in this sector. Two stocks in particular – Hain Celestial (HAIN) and The Scotts Miracle-Gro Company (NYSE:SMG) – while big winners for us in 2020 and 2021, hurt the portfolio in 2022.

While both companies were so-called COVID beneficiaries (businesses that benefited from consumers staying home and spending on their homes during COVID), we felt they possessed certain additional drivers that would maintain their fundamentals into 2022 and beyond.

Scott’s Miracle-Gro is arguably one of the great American franchises. The brand is synonymous with lawn care and pest control, has a dominant market share (~60%) with historically-impressive ~30% cash flow margins, and has the country’s largest Cannabis supply business. Scotts’ core business saw a significant windfall during COVID lockdowns. Lawn and garden care is not a growth business, and SMG dominance does not allow for much incremental gain in market share. However, our thesis was that even in a reopening scenario where lawn and garden businesses would revert to the mean, the cannabis market was poised for years of growth as more states legalized recreational use.

What we missed was the highly inefficient structure of the U.S. cannabis market. Currently, California, Colorado, and Michigan have the biggest and most mature markets. However, over the course of the last few years, several very large states and regions have voted to legalize recreational use, including New York, New Jersey, and Connecticut. The fly in the ointment has been Oklahoma, which is a medical marijuana state. Although recreational use is still prohibited, licenses to grow the crop were granted in Laissez Faire fashion to anyone willing to buy one. Oklahoma began to grow and cultivate the crop far in excess of their medical marijuana demand. That excess supply bled into gray markets across the country, devastating pricing for growers in other states. This glut put a near complete stop to capital spending on grow operations. With no new or incremental facilities coming on, Scotts’ Hawthorne business was cut in half from its peak in F21. This, of course, had a devastating effect on the stock.”

<<<

---

IH Admin [Shelly]

Member Level

Re: Zardiw post# 213369

Wednesday, September 13, 2023 8:23:22 PM

Post#

213374

of 216077

I can confidently and 100% say that I have never heard of or been privy to anything that suggests any aspect of our company manipulates or inflates stats in anyway.

I do seem to recall there was a point, many, many years ago, there was an idea thrown out that bots could be used to boost posting. That was pretty much quickly shut down by the iHub team from my recollection. From memory, they don't improve engagement in any way as their content is typically negligible and mostly ignored. Sure, it could artificially inflate post counts, but, so? It wouldn't increase dialog which would actually be meaningful.

Just for some perspective, I was on a call today and we were talking about some metric with Google. That specific # was in the 14 million range for something I believe was being analyzed on a daily basis. That's sort of mind boggling.

58k reads isn't really very high in the big scheme of things. And, truly, think about it. If iHub decided to "cook" any numbers - Q&A reads would be the silliest to manipulate. As far as I know, there's zero SEO value in this board. Absolutely no one wants this board to be on any sort of Hot! list. So, while it may look like that to you, I can't believe there's any validity to that theory.

Sirius XM -- Buffett -

https://finance.yahoo.com/news/warren-buffetts-latest-2-1-100600894.html

>>> Beyond Occidental, we've also seen Warren Buffett and his team piling back into satellite-radio operator Sirius XM Holdings (NASDAQ: SIRI). Though radio operators are often highly dependent on advertising revenue to keep the lights on, Sirius XM has an assortment of competitive advantages working in its favor that should help it navigate any economic climate better than terrestrial and online radio companies.

To start with the obvious, Sirius XM is the only licensed satellite-radio operator. While this doesn't mean it's free of competition for listeners, it does give the company reasonably strong subscription-pricing power.

What's arguably even more important with Sirius XM is how the company generates revenue. Whereas terrestrial and online radio providers are reliant on advertising revenue, only 20% of Sirius XM's sales came from advertising in 2023. Meanwhile, a whopping 77% of Sirius XM's revenue can be traced to subscriptions. Subscribers are less likely to cancel their service during an economic downturn than businesses are to meaningfully pare back their advertising budgets.

Sirius XM is also historically cheap. Shares are currently trading for a multiple of 13 times forward-year earnings, which is a 32% discount to its average forward-year earnings multiple over the trailing five-year period.

<<<

---

>>> Why C3.ai Stock Rocketed Higher Thursday Morning

by Danny Vena

Motley Fool

Feb 29, 2024

https://finance.yahoo.com/news/why-c3-ai-stock-rocketed-162410723.html

Shares of C3.ai (NYSE: AI) moved sharply higher Thursday morning, soaring by as much as 26.4%. As of 10:40 a.m. ET, the stock was still up by 24.3%.

The catalyst for that surge was the quarterly report it delivered after the close Wednesday, which revealed that the artificial intelligence (AI) specialist may finally be tapping into the widening adoption of AI.

The beginnings of a turnaround?

For its fiscal 2024 third quarter, which ended Jan 31, C3.ai generated revenue of $78.4 million, up 18% year over year. Subscription revenue grew even faster, up 23% to $70.4 million, accounting for 90% of the total. The results were further aided by the company's expanding gross profit margin of 58%, which edged higher from 56% in fiscal Q2.

Profits continued to be elusive. C3.ai booked a net loss of $72.6 million, resulting in an adjusted loss of $0.13 per share -- more than double its loss of $0.06 per share in the prior-year quarter.

To put those results into context, analysts' consensus estimates were calling for revenue of $76.1 million and a loss of $0.28 per share, so the company beat on both top and bottom lines.

Better days to come

C3.ai's results might not seem like much to celebrate, particularly given its worsening bottom-line losses. However, there are indications that better days could be coming as management increased its full-year guidance and investors let out a collective cheer.

The company cited the increasing number of new agreements it has signed with customers -- it inked 50 during the quarter, up 85% year over year. Of those, 29 were new pilots. Management expects these deals will translate into commercial revenue in the months and years to come.

For its fiscal 2024 fourth quarter, management forecasts revenue of between $82 million and $86 million, which would amount to growth of roughly 10% at the midpoint. For the full year, C3 is forecasting revenue of $306 million to $310 million, a year-over-year increase of about 15% at the midpoint. Most of that range tops analysts' consensus expectation for revenue of $306.2 million. However, as a result of its increasing investments, the company said its losses will continue, and it no longer expects to be profitable by the fiscal fourth quarter.

C3.ai still needs to show it can capitalize on the AI boom and turn a profit.

<<<

---

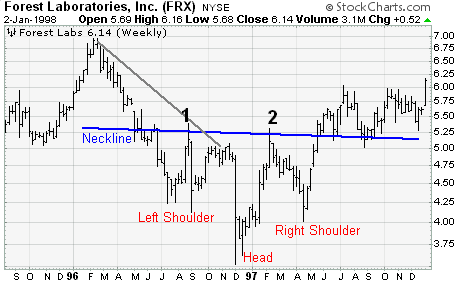

Derf, Likewise, the inverse head + shoulders below is also seen in the GLD chart from 2020-2024. This is basic 'Chart Patterns 101' stuff -

https://school.stockcharts.com/doku.php?id=chart_analysis:chart_patterns:head_and_shoulders_bottom_reversal

---

Derf, The chart pattern below is nearly identical to the GLD chart from 2010-2024, except for the breakout, which hasn't happened yet -

Cup With Handle Pattern -

https://school.stockcharts.com/doku.php?id=chart_analysis:chart_patterns:cup_with_handle_continuation

---

Gone to it? I've taught it!

I'm not going to debate something with you that I've done and taught for 30 years.

I guess, like clouds in the sky, you can see in it whatever you wish. You want it to be a cup and handle, it's a cup and handle.

Derf, >> neither a cup nor handle there <<

It sounds like you haven't been to chart school. Compare the chart below with the GLD chart from 2010-2024 -

https://school.stockcharts.com/doku.php?id=chart_analysis:chart_patterns:cup_with_handle_continuation

---

Gold fell below support back in April 2013. Didn't really rebound until Jan 2019. But it fell back and retested until Nov. 2022, when it broke out.

I see neither a cup nor handle there.

I think buying gold as a hedge is now dumb (not that you're dumb, but the idea of gold is)

Gold is no longer a currency worthy of trade.

In a disaster, what is really more valuable....a chunk of gold or a cup of water?

And buying a gold stock or ETF or whatever, isn't really buying gold! It's not like you can show someone your investment portfolio and say...."See this here gold!"

Many years ago, I had a buddy who loaded up on silver quarters for safety. His thinking was, in a worst case scenario, at least he could buy himself a Coke.

Funny thing, this guy was very conservative. Would always take months to evaluate an investment. Then invariably, choose the wrong one. Don't know if he still has silver, but if so, it has been awful.

Also bought houses as an investment......which his soon to be ex-wife took from him in the settlement.

Derf, >> breakout in gold was back in November <<

Btw, that was a bottom or reversal, not a breakout. A breakout is when a stock gets through a resistance level.

---

Derf, >> cup and handle <<

Check the chart going back to 2011 and the 'cup' is classic. The 'handle' has been forming since 2020, but has actually taken 3 dips to form, so is a 'quasi handle', but close enough. The inverted head + shoulders since 2020 is fairly classic -- the left shoulder was deeper than the right, but the neckline is classic.

Can't blame you for being anti-gold though, especially now with cash and bonds paying 4-5%. But I figure a modest gold position makes sense as disaster insurance. With the US debt at 34 trillion and climbing by several trillion / year, and global de-dollarization, the crumbling Petrodollar system, etc, a dollar crisis is inevitable at some point. But tough to say when. I'd say residential real estate is the better inflation hedge, but probably best to have some of both.

---

The breakout in gold was back in November of '22. I'm not seeing a cup and handle.

I owned some GLD a while back, but took my profits and ran. Historically gold has been a terrible investment, but I do have to admit the last 20 years has been better than most. Just doesn't pay a dividend and I like too many other areas better.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |