News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

You think RD may have sold all his BDCO?

The crack spread for jet fuel is expected to hold up quite well in coming months:

"Jet Fuel Cargoes CIF NWE (Platts) Crack Spread Futures - Quotes

Venue:

Auto-refresh is off

Last Updated 08 Aug 2022 10:33:12 AM CT.

Market data is delayed by at least 10 minutes.

Month Chart Last Change Prior

Settle Open High Low Volume Updated

Month Chart Last Change Prior

Settle Open High Low Volume Updated

AUG 2022

JFCQ2"

-

-

34.680

-

-

-

0

16:00:00 CT

07 Aug 2022

SEP 2022

JFCU2

-

-

34.660

-

-

-

0

16:00:00 CT

07 Aug 2022

OCT 2022

JFCV2

-

-

34.910

-

-

-

0

16:00:00 CT

07 Aug 2022

NOV 2022

JFCX2

-

-

34.000

-

-

-

0

16:00:00 CT

07 Aug 2022

DEC 2022

JFCZ2

-

-

33.790

-

-

-

0

16:00:00 CT

07 Aug 2022

JAN 2023

JFCF3

-

-

33.510

-

-

-

0

16:00:00 CT

07 Aug 2022

FEB 2023

JFCG3

-

-

32.840

-

Nice pop on VTNR and will be rolling over profits to more BDCO before next week

Time to buy a little more today

VTNR looking good earnings tomorrow

Bdco is where to be

Dutch u said the number would out already. Did u sell

shurta I guess refiners can to some extent choose if they refine the crude to gasoline or to some other alternative. If an increase in the demand for gasoline expected it is natural to increase the production of gasoline and to reduce the production of some of the alternatives. This is hardly very strange. The refiners may have had too high expectations when it comes to the demand for gasoline this summer and may therefore have produced too much.

Calling out BS on this 50 day drop in gasoline prices - How do you go from extreme gasoline shortage to demand falling off a cliff at the peak summer months

I wasn't even going to reply.

But I don't want him to wait 3 days for an answer that will never come.

Someone else can answer his questions !

For 15 years I have supported a number of companies and I have received nothing in return. That's going to change now.

I will help this company if management shows me they are worth it.

He's asking you for help, not for you to help the company.

Someone else can answer your question. I'm no longer helping out this company (in any way).

When are the BDCO results pls?

The fall in crude won't affect this Qtr margins correct? Hopefully the sellers find this out before selling on fall of crude prices? If it goes past it's lifetime highs I'm happy, 10$ tgt is just very very good.

Here you have in one view what happened to refining margins.

It all started in March.

https://www.neste.com/investors/market-data/oil-product-margins#0c0ca8d6

Gasoline has come down again but diesel is still close to $40/barrel.

It's also updated daily. So I check this frequently.

Just shaking things up a little. We are going to need it later on. lol.

Get in already. Time is running out.

There is another very large refinery in Houston that is for sale. Its about 100 years old. Rohm and Hass?

If they do not find a buyer, they may close it forever. Adding to the shortage of US refiners.

And no one is building new ones in the US

A friend of mine drives by this plant on a regular basis.

Remind me again why I should buy this?

LMAO

"The market simply won't care about earnings. You have seen DK drop 9% after they reported earnings yesterday. PKN Orlen is down today after they reported earnings.

What we need is dividends. An acquisition. Some serious debt relief. Clarity on hedging. Guidance. Uplisting. Some serious IR activity. But what we do have so far is a bunch of morons acting like they don't know anything."

At this time I think BDCO diesel has too high of a sulfur content to be used in vehicles (in the USA). However, the higher sulfur content may be usable in other countries. I also think they may be able to start producing biodiesel in the future, but don't know for sure...

Their settlement with Genesis (GEL) I think back in 2018 really hurt them. However, they hopefully won't do any more of those types of agreements anymore. All just my opinion.

Assuming that the crack spread for diesel and jet fuel will drop to $20 (a lot has to happen) then I think the company will still make EPS $1.50 next year. Multiplied by 7 is still a $10 stock.

We bought the right stock. Otherwise I wouldn't be here.

Significant advantages include

1) Higher margins for jet fuel and diesel

2) Potential acquisition and tripling of capacity

3) No taxes!

All of these are very significant.

Add to that a potential uplisting.

We are good here!

Margins are still double what is typical for this time of year.

https://www.marketplace.org/2022/08/02/u-s-oil-refiners-are-doing-well-even-though-gasoline-prices-are-down/

While refining costs have gone up due to supply chain and logistics issues, Jason Gabelman at Cowen said the current crack spread is wide enough to offset those costs, and then some.

“Even though they’ve come off, they’re still historically strong margins, double what they typically are for this time of year,” he said. “So these guys are making money hand over fist right now.”

RD What is unknown is the crack spread next year and the year after that. . Let's assume that it will be 20 dollars for a barrel. This is close to the current crack spread for gsoline. Let's assume that the p/e will be a conservative 7. What stock price does it imply?

makinezmoney It is true that the crack spread for jrt fuel is etill good but it has been falling fast DURING THE SUMMER. RD has just posted the numbers.

Blue skies next week -waiting/hard part almost over

VTNR making a nice move before earnings

Sounds reasonable. Thanks.

If they deliver on earnings, like EPS $1.62, then I expect the stock to rally to the previous high at $2.35, perhaps challenge $3. But it is really hard to say. All the rest depends on the details we mentioned.

I get that, but why not use some in-the-ballpark numbers.

They sure cared about earnings when the Q1 came out.

Is there room for more upside if they repeat or beat Q1... I think so...not to nearly $27 though Limited upside here. for the reasons you mentioned.... .

Maybe $3-5, or so

lol. I'm trying to make a point though.

I agree with these items you mentioned. But that spread was too extreme to conceive over some points you mentioned.

The market simply won't care about earnings. You have seen DK drop 9% after they reported earnings yesterday. PKN Orlen is down today after they reported earnings.

What we need is dividends. An acquisition. Some serious debt relief. Clarity on hedging. Guidance. Uplisting. Some serious IR activity. But what we do have so far is a bunch of morons acting like they don't know anything.

With all due respect that seems preposterous. If the good earnings are there as mentioned here, it won't matter who is in charge to that degree.

Then we won't get $27. Perhaps $1.

That likely won't happen.

So what SP with them until otherwise?

$27, after we replace the managers and directors.

Come off it sir.

"$27 Very Very Conservative"

Well, we won't be getting a P/E of 10, for now.

But I can see the tech stocks crash and the oil companies rally later this year.

Demanding a higher P/E than what we have now in the oil sector.

When the summer madness is over.

$BDCO: $27/share very very conservative !!!!!!!!!!!

But...... I can live with that still.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=169188727

Anything over this measley super undervalued valued of only $1.40

GO $BDCO

$BDCO: How much do they sell refined crude ...........

Refined to Jet Fuel ??????

Whats the unit price on that ?????????????????????????????????

Thats right........ put a lil thought on that one.

Take a look around and tell me how much refining capacity is out there right now

to produce something that is soooooooooo high in demand in this gangbusters travel season.

Good nite !

GO $BDCO

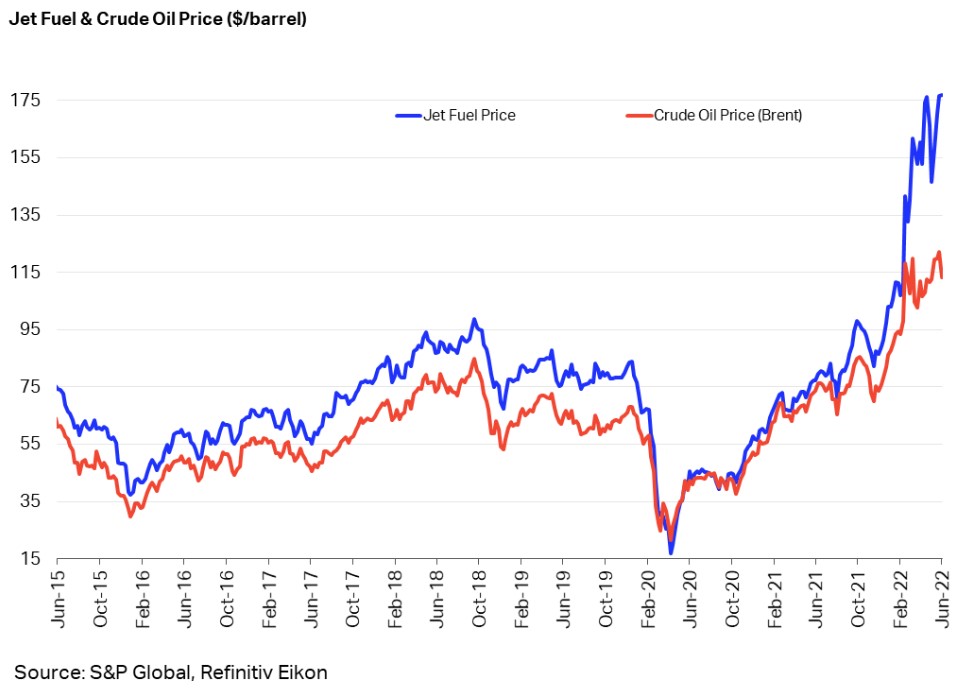

This is interesting. I can calculate the spread for jet fuel.

https://ycharts.com/indicators/gulf_coast_jet_fuel_spot_price

https://ycharts.com/indicators/wti_crude_oil_spot_price

per barrel (jet fuel price - crude price)

Aug 1 = 136.3 - 96.6 = 39.7

Jul 22 = 140.0 - 97.7 = 42.3

Jul 15 = 148.8 - 99.6 = 49.2

...Jul 01 = 158.7 - 110.3 = 48.4

.........Jun 01 = 165.2 - 115.2 = 50.0

A bit lower now as expected but still very good. And in line with diesel.

Lotos Refining Margin should be even higher than PKN Orlen.

Because Lotos has only 23% gasoline and 63% diesel. Still a big difference.

Pity. I think they stopped giving updates. As they have been acquired by PKN Orlen.

The latest was $40.48/barrel on July 29.

Very respectable indeed.

https://inwestor.lotos.pl/en/2731/investors/daily_model_refining_margin

makinezmoney "Definitely RECORD revenues thanks to Jet Fuel, Diesel and NAPHTHA prices alone." It is earnings per share that matter and not revenues.

makinzmoney T company buys crude it does not produce it1

PKN Orlen Refining results

(million PLN)

(1 PLN = 0.23 USD)

Q2/21 : 263

Q1/22 : 900

Q2/22 : 1,845

There are at least 2 major reasons why earnings aren't higher as expected

1) PLN 2.8 billion impairment. Something to do with switching from Russian oil. They already announced it yesterday, btw.

2) PLN 2.1 billion negative impact from hedging.

Hedging is something to watch for BDCO. They never mentioned hedging before in the financial reports. If they do it, they better get the timing right. So perhaps during Q2.

I think I will leave it there. Can't deduce how much of that refining margin ends up being profits. But perhaps someone else can.

Hard to interpret the results for PKN Orlen (with a similar product mix as BDCO). But here we are.

Model refining margin = revenues (93,5% Products = 36% Gasoline + 43% Diesel + 14,5% HHO) - costs (100% input: crude oil and other raw materials).

Total input calculated acc. to Brent Crude quotations. Spot market quotations.

Q1 : $6.0 per barrel

Q2 : $38.7 per barrel

Kaboom. A lot higher than what the other refineries reported (because they sell a lot more gasoline)

They were predicting $18.7 for Q2 when they reported Q1. Jokers. lol.

And they are not giving many details now in the Q2 report.

Q2

https://money2.wpcdn.pl/gielda/gpw/espi/129/6798033773340801_3.pdf

Q1

https://www.orlen.pl/content/dam/internet/orlen/pl/en/investor-relations/reports-and-publications/financial-results/2022/1q2022/Wyniki_1Q22_ENG.pdf.coredownload.pdf

Tomorrow PKN Orlen from Poland will report earnings.

As you can see here, they have roughly the same product mix as BDCO. Mostly diesel and jet fuel.

It's also the 4th largest oil company in Europe.

|

Followers

|

72

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

4325

|

|

Created

|

03/30/05

|

Type

|

Free

|

| Moderators | |||

Blue Dolphin Energy Company is a publicly traded Delaware corporation, headquartered in Houston, primarily engaged in the

refining and marketing of petroleum products to be used as jet fuel, or as "a light sweet crude."[2]

The company also provides tolling and storage terminaling services. 60 acres of assets, which are located in Nixon, Wilson County, Texas

primarily include a 15,000 bbl/d (2,400 m3/d)[3] crude distillation tower and more than 1.0 million barrels of petroleum

storage tanks (collectively the “Nixon Facility”). Pipeline transportation and oil and gas operations are no longer active.[4][5]

Since 2006 through 2014, according to the chief executive regarding this facility, in-kind with his other similar

facility at the time, “...there were some issues with the EPA (Environmental Protection Agency) that we were not made

aware of, and those issues have yet to be resolved.”[6]

As of 2014, 45 workers were employed at this facility.[7]

Lazarus ENERGY is a Subsidiary of Blue Dolphin

https://www.lazarusenergy.com/

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |