News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Lululemon shares surge after reporting 24% sales growth, raising full-year guidance >

https://www.cnbc.com/2023/06/01/lululemon-lulu-earnings-q1-2023.html

CNBC Morning News

1. New month

Stocks are set to kick off June trading with modest gains, as investors remain wary of debt ceiling deal progress in Washington and potential Federal Reserve rate hikes later this month. Dow Jones Industrial Average futures were about flat Thursday, while S&P 500 futures gained 0.2% and Nasdaq futures rose about 0.1%. “We have been impressed by the resilience of this market since the March low, absorbing a relentless onslaught of negative sentiment and headlines,” said Piper Sandler Chief Market Technician Craig Johnson. Follow live market updates.

2. Debt drama defused ... for now

It took a late-night vote and arm twisting, but a bill to raise the U.S. debt ceiling passed the House on Wednesday, mere days before the country risks its first-ever default on June 5. The chamber approved the measure in a 314-117 vote — a more overwhelming result than expected for a plan that included spending provisions that many Democrats and Republicans opposed. The Senate will forge ahead with the bill Thursday morning, and aims to send it to President Joe Biden’s desk as soon as Friday. It remains to be seen how quickly Majority Leader Chuck Schumer can push the bill through the famously slow-moving upper chamber, where one senator’s opposition can slow down swift passage of legislation. If the Treasury dries up, it would roil global financial markets, cost jobs and jeopardize vital government benefits for millions.

3. Mixed bag for retail

A slate of retail earnings reports has stocks swinging before the market opens Thursday, as some companies noted consumer weakness entering the spring season. Macy’s shares dropped as much as 10% after the department store operator slashed its full-year earnings and sales guidance. The company said it saw weaker discretionary spending starting in March and has had to mark down seasonal merchandise. Nordstrom’s stock, however, rose more than 3% after the company beat expectations on the top and bottom lines on Wednesday. While the retailer expects sales to fall this year, it reported sales improvements in April after a slow March. Shares of Chewy, meanwhile, soared more than 15% after the digital pet care retailer topped earnings and revenue estimates.

4. Alexa, pay up

Amazon has agreed to hand over more than $30 million to the Federal Trade Commission to settle allegations of privacy violations involving its Alexa and Ring products, according to filings out Wednesday. The FTC claimed in separate lawsuits that Amazon was improperly securing or holding onto video recordings and profile data of users, including children. In addition to the settlement charges, Amazon will be required to delete scores of data. And because, according to the FTC, “Ring failed to implement basic measures to monitor and detect inappropriate access before February 2019, Ring has no idea how many instances of inappropriate access to customers’ sensitive video data actually occurred.”

5. Coming home

More and more companies are looking to bring manufacturing operations home, pulling out of longstanding production powerhouses like China, in a trend called “reshoring” that could have massive implications for the global supply chain. According to Bank of America analysis, mentions of “reshoring” during S&P 500 earnings transcripts in the first quarter were up 128% over the same quarter last year, outpacing even the growth in mentions of “AI.” There’s a host of factors at play here: the Russia-Ukraine war, the aftereffects of the Covid-19 pandemic, U.S. and EU incentives for at-home production, and shifting demand due in part to the rise of TikTok. Still, remapping the global supply chain wouldn’t happen overnight.

— CNBC’s Jacob Pramuk and Sara Salinas wrote this newsletter. Yun Li, Christina Wilkie, Melissa Repko, Gabrielle Fonrouge, Lauren Feiner, Annie Palmer and Lucy Handley contributed.

DJIA Up Nine of Last Ten Years on June’s First Trading Day

By: Almanac Trader | May 31, 2023

According to the Stock Trader’s Almanac 2023 (page 90), the first trading day of June is the fifth weakest first trading day of all twelve months with DJIA gaining just 442.36 total points since 1998. Over the past 28 years, DJIA’s first trading day of June has produced gains 74.1% of the time with an average gain of 0.04% in all years. Sizable losses in 2002, 2011 and 2012 limit overall performance. S&P 500 has advanced 60.7% of the time. NASDAQ has been slightly weaker at 53.6%. Russell 2000 has advanced 64.3% with the best average performance of 0.20%. Following three straight losses from 2010 to 2012, DJIA has advanced on nine of the last ten first trading days of June.

Read Full Story »»»

DiscoverGold

DiscoverGold

Yesterday's CNBC Morning News

1. Mixed-up May

The major U.S. stock indices are in a mixed state as May ends. The tech-heavy Nasdaq, on one hand, is up more than 6% heading into the final session of the month, driven in large part by the explosion of artificial intelligence. The Dow, on the other, is down more than 3%. And the broad S&P 500 has risen only slightly in May. The end of the month also brings the U.S. closer to a potential debt default, if Congress doesn’t act (more on that below). Follow live market updates.

2. Moot

3. Dimon goes to China

JPMorgan Chase CEO Jamie Dimon, speaking in Shanghai, called on the U.S. and Chinese governments to cool it and find a way to better work together. “You’re not going to fix these things if you are just sitting across the Pacific yelling at each other, so I’m hoping we have real engagement,” Dimon said, referring to trade and security issues, as he spoke at the JPMorgan Global China Summit. The banker isn’t the only major U.S. CEO who visited China this week against the backdrop of intensifying tension between the countries. Tesla boss Elon Musk met several top officials and executives during his trip.

4. One sentence to warn the world

Warnings about artificial intelligence are coming almost as rapidly as advancements in the technology. The most recent one, coming in at just one sentence long, might be the starkest yet, however. “Mitigating the risk of extinction from AI should be a global priority alongside other societal-scale risks such as pandemics and nuclear war,” reads an open letter posted by the Center for AI Safety. It’s signed by a slew of top scientists and executives, including Sam Altman, the head of ChatGPT creator OpenAI. Even as ChatGPT explodes in popularity, reaching more than 100 million users and prompting several competitors to join the race, Altman has been one of the voices calling for regulation to keep AI from becoming something more than a mere tool for humanity. And that seems pretty serious.

5. Mortgage demand slumps

Mortgage demand is at its lowest point in three months, according to the Mortgage Bankers Association. Rates shot up again recently, nearly hitting 7% by some measures, as it became clear that the Federal Reserve wasn’t going to cut its benchmark rate any time soon. The supply of homes remains tight, as well, and prices look like they’re going higher again. “While refinance demand is almost entirely driven by the level of rates, purchase volume continues to be constrained by the lack of homes on the market,” Michael Fratantoni, the Mortgage Bankers Association’s chief economist, said in a release.

— CNBC’s Mike Calia wrote this newsletter. Jesse Pound, Christina Wilkie, Emma Kinery, Elliot Smith, Sheila Chiang and Diana Olick contributed.

Nasdaq Triggers A New Volatility Correlation Sell Signal

By: Jesse Felder | May 30, 2023

A few years ago, I was studying the relationship between the major stock market indexes and their volatility indexes and I came across and an intriguing phenomenon. The vast majority of the time these indexes move in opposite directions from one another. If stock prices are rising, volatility indexes are usually falling and vice versa. It’s when this relationship inverts that things get interesting. And that’s exactly what happened again last week.

A new Nasdaq Volatility Correlation sell signal triggered last week when the 10-day correlation (the bottom panel in the chart below) of the NDX and VXN turned positive because both had risen together over that span. Previous sell signals are marked on the chart below by a vertical red line. Buy signals occur when the 10-day correlation turns positive because both the index and its volatility index are falling together. These are marked by vertical green lines in the chart.

Why these signals are, at times, effective is anyone’s guess but it’s clear that disconnects like this between equities and options markets can be important signals of impending trend reversals. The two previous buy signals late last year proved to be effective in that regard. The last sell signal in early-February also proved effective as stocks struggled over the following month or so.

Time will tell if this most recent sell signal will also prove effective in this way. It’s interesting to note, however, that it also culminated in an even more rare signal on Friday when both the NDX and VXN rose more than 2% on the day (last seen on 2/2). This is a pretty strong indication that the options market is not nearly as sanguine as the equities market at this stage of the rally. And that in itself may be an important development to pay attention to.

Read Full Story »»»

DiscoverGold

Breitbart Business Digest

by John Carney - Breitbart Economics Editor

Alex Marlow - Breitbart Editor-In-Chief

May 30, 2023

Debt Ceiling Deal Paves Road for Fed Hike

The deal to suspend the limit on federal government debt until 2025 removes one of the obstacles to another Federal Reserve rate increase.

It was highly unlikely that the Fed would have decided to raise rates without a deal. Federal Reserve officials regarded the possibility of crossing the "x-date"—the point at which the government would no longer have enough available funds to pay bills as they come due—with sufficient alarm to forestall a hike even if other economic data were supportive of higher rates. Monetary policy, in other words, would have become a captive of fiscal policy.

This is one of the unheralded risks posed by the debt limit. It threatened to push the central bank away from further tightening even if that is what the data were to prescribe. The result might have been an acceleration or prolonging of inflation. The debt deal clears the road for Fed officials to pursue monetary policy according to economic fundamentals instead of navigating around a battle over fiscal policy.

That's one reason the Fed's decision to absent itself from the discussion over the debt ceiling—and particularly the need for fiscal restraint—was so regrettable. The question of how much debt and how large a deficit the economy can support very much impacts the Fed's statutory mandate to pursue full employment and price stability. At the very least, Fed Chair Jerome Powell could have stated the likely consequences for interest rates if the country continues on the spending path charted by the Biden administration.

A Tricky Question of Timing

The deal brokered by House Speaker Kevin McCarthy (R-CA) suspends the current $31.4 trillion debt limit into 2025. Many on the right, including several members of the House Republican Caucus, would have preferred a one-year suspension, which would have set the stage for another debt ceiling fight next year. Many of these critics believe that forcing Biden to defend another debt ceiling increase in an election year would hurt his chances for re-election and bolster those of Republicans to regain the White House and the Senate and maintain control of the House.

Perhaps. As Yogi Berra might have said, events are hard to predict, especially if they haven't happened yet. A year from now it seems very likely that the economy will be in a recession or close to one (perhaps entering into it or perhaps coming out of it). Unemployment is likely to be higher in June of 2024 than it is today. The public may be less concerned about government debt levels and inflation if the economy is shedding jobs, incomes are plunging, and output is falling. Instead of a better deal or a political win next year, the debt ceiling could become a political liability for Republicans.

There is at least as plausible a case to be made that Republicans would do better in next year's elections by fighting on the issues they choose based on the mood of voters rather than on an issue dictated by the fiscal calendar. As our friend Larry Kudlow of Fox Business has argued, it's very likely that next year's election will turn on "kitchen table" issues. Playing the role of budgetary bean counters is not going to inspire many votes. It risks distracting from a more important agenda centered around economic nationalism and growth.

What the Deal Means for the Economy

The most direct macroeconomic impact of the debt deal is likely to come from the agreement to resume student debt payments this summer. The average monthly bill before the pandemic was $393 per borrower, according to data from the Federal Reserve. Some 40 million Americans have student loans. Many of those with student debt have a relatively high propensity to spend any additional discretionary income, which means that a large part of that $393 was finding its way into consumer spending. As a result, the resumption of payments will mean a decline in overall demand in the economy and relief from some inflationary pressures.

This might be somewhat offset, however, by a boost in consumer confidence. According to the University of Michigan's Joanne Hsu, the debt ceiling debate has likely been weighing on consumer confidence. Although this has not shown up in spending restraint on the part of households, the lifting of this worry could propel some additional spending. To the extent that business investment has been held back by the uncertainty around the debt ceiling, that could also improve.

Would it have been better if McCarthy's team could have wrung deeper spending cuts out of the Biden administration? Certainly. The deal agrees to cap discretionary non-military spending at $704 billion, down from the projected 2024 baseline of $757 billion. The House bill would have reduced it to $689 billion. Even that, however, would only bring us back to 2022 levels, which would not be going far enough for an economy at full employment and very high inflation.

It's still too early to say whether the Fed will hike at the June meeting. The CME's FedWatch tool, which is based on fed funds futures prices, now gives a 70 percent chance of a hike in June, up from less than 30 percent last week. A lot will likely turn on the jobs report this Friday. A weak jobs report will likely allow the Fed to at least skip the June meeting and put it into a holding pattern for the July meeting. A strong jobs report should guarantee another hike, either in June or July.

Why an interest rate hike is still on the table for June

BY Megan Cassella, BARRON'S – 05/19/2023

The fire hose of commentary from the Federal Reserve this past week made one thing clear: Central-bank officials are fiercely split on how to navigate the policy path forward and whether to raise interest rates or hold them steady when the Fed’s policy-making committee next meets in June.

Officials laid the groundwork at their May meeting for the Fed to pause next month, although they stopped short of committing to specific next steps. But since then, a series of economic surveys and data releases have appeared to show an economy that looks increasingly stable.

That has emboldened the central bank’s hawks to publicly endorse the idea of at least one more rate boost in June, given that the pace of inflation remains more than double the Fed’s target. Dallas Fed President Lorie Logan, a voting member of the Federal Open Market Committee, was perhaps the most explicit, saying Thursday that while the data “could yet show” it is appropriate to skip a rate hike, the current environment suggests that “we aren’t there yet.”

The economic case for further policy tightening centers on fresh optimism that the U.S. will be able to stave off a recession, at least until sometime next year. A new working paper from economists at the San Francisco Fed shows that, despite years of strong demand and high inflation, U.S. households across the income spectrum still hold an estimated half-trillion dollars in excess savings—enough to fuel consumer spending at least into the fourth quarter of 2023.

At the same time, some of the more interest-rate-sensitive sectors of the economy that had been impacted by monetary-policy tightening—namely, housing and manufacturing—could be reaccelerating.

Skanda Amarnath, executive director at Employ America and a former research analyst with the New York Fed, notes that growth in multifamily residential units under construction and resilience in mortgage demand both are helping to paint an “encouraging picture” for the housing market. Manufacturing data out this past week from the Philadelphia Fed, he added, suggest that the most contractionary months for that sector could be behind us.

Buoyancy in housing and manufacturing isn’t “a typical thing you see right before a recession,” Amarnath said.

(con't)

Nasdaq boosted by Nvidia, tentative debt deal cheer

REUTERS - 10:30 AM ET 5/30/2023

By Shreyashi Sanyal

(Reuters) - The Nasdaq led gains among Wall Street's main indexes on Tuesday, boosted by shares of Nvidia ( NVDA ), amid optimism about lawmakers tentatively agreeing to raise the nation's debt limit to avert a default.

U.S. President Joe Biden and Republican House of Representatives Speaker Kevin McCarthy on Sunday signed off on an agreement to temporarily suspend the debt ceiling and cap some federal spending.

(con't)

Volume movers

2-day

Symbol Last % Change Volume

VSTM $1.04 +2.98% 15.5M

VMW $135.23 +1.49% 2.9M

AVGO $854.73 +5.17% 6.4M

LXRX $2.94 -7.63% 7.7M

NVDS $8.81 -7.46% 15.0M

Most actives

Symbol Last % Change Volume

PLTR $14.98 +9.74% 90.8M

TQQQ $35.96 +2.80% 79.5M

SQQQ $22.27 -2.79% 74.8M

TSLA $200.88 +3.99% 72.6M

SOXL $23.81 +4.04% 68.0M

1. Short week, high stakes

Investors are back from their three-day holiday weekend, facing a world with no more new “Succession” episodes, as well as a shortened week that will nonetheless be loaded with consequential twists and turns. There’s a decent slate of earnings ahead, as well as major economic data points, including the job openings report Wednesday and the April jobs report due Friday. Markets will also have their mind on what’s going on in Washington with the debt ceiling (more below), while Tesla investors will keep a keen on eye on what CEO Elon Musk does during his visit to China. Follow live market updates.

2. Now for the hard part

President Joe Biden and House Speaker Kevin McCarthy reached a deal over the weekend to raise the debt ceiling, avoid the first-ever U.S. default and cap some government spending. But there's still a lot of work to be done. Treasury Secretary Janet Yellen said the U.S. government could run out of cash to pay its bills June 5, which is just six days away. In that time, the Biden-McCarthy agreement will have to pass through Congress. It’s already shaping up to be dicey, with progressive Democrats and conservative Republicans airing their gripes. McCarthy wants the House to vote on the bill Wednesday. We’ll see.

3. Still plenty of earnings

Earnings season is just about wrapped up, but there are still several notable companies set to report this week. Salesforce and Broadcom lead the tech stragglers, while Macy’s and Nordstrom are on tap as the retail earnings extravaganza tapers off. Here’s a look at which companies are reporting this week:

Tuesday: HP (after the bell)

Wednesday: Salesforce, Nordstrom, Okta, CrowdStrike, Chewy (after the bell)

Thursday: Macy’s, Dollar General (before the bell); Lululemon, Broadcom (after the bell)

4. Drones attack Moscow

Moscow itself is now feeling the impact of Russia’s war on Ukraine. Drones hit several buildings in the Russian capital early Tuesday. The strikes caused some damage but no casualties, officials said. It wasn’t immediately clear where the drones came from, although Russian officials blamed Ukraine. While the Ukrainian government didn’t claim credit, a top advisor to President Volodomyr Zelenskyy’s office said Ukraine “has nothing directly to do” with the Moscow attacks, although it’s “pleased to observe and predict an increase in the number of attacks.” Follow live war updates.

5. Final showdowns

The NBA Finals are set: The Miami Heat will take on the Denver Nuggets. The Heat, led by star Jimmy Butler, took game 7 of the Eastern Conference finals in convincing fashion, holding off the Boston Celtics’ bid for a historic comeback from an 0-3 series deficit. The finals matchup is intriguing for several reasons, including the fact that the Heat barely even made the playoffs, while the Nikola Jokic-led Nuggets are making their first-ever finals appearance. The series begins Thursday on Disney’s ABC. The Stanley Cup Finals are also ready to go in the NHL, with the Vegas Golden Knights set to take on another surprising Florida team, the Panthers. The puck drops in that series Saturday on Warner Bros. Discovery’s TNT.

— CNBC’s Mike Calia wrote this newsletter. Brian Evans, Christina Wilkie and Natasha Turak contributed.

US Futures Mostly Higher Ahead Of Debt Ceiling Vote, Oil Falls Again

By: Barchart | May 30, 2023

Wall Street pointed mostly higher early Tuesday after President Joe Biden and House Speaker Kevin McCarthy reached an agreement on a deal to raise the U.S. national debt ceiling.

Futures for the Dow were flat the S&P 500 rose 0.7% before the bell.

Biden and McCarthy are now working to gather votes needed to gain congressional approval in time to avert a default.

Biden spent part of the Memorial Day holiday working the phones, calling lawmakers in both parties, as the president worked to deliver the votes. A number of hard right conservatives are criticizing the deal as falling short of the deep spending cuts they wanted, while liberals decry policy changes such as new work requirements for older Americans in the food aid program.

A key test comes Tuesday afternoon when the House Rules Committee is scheduled to consider the package and vote on sending it to the full House for a vote expected Wednesday.

“I feel very good about it,” Biden told reporters Monday as he left Washington for his home in Delaware.

There are other concerns on top of the threat of the U.S. defaulting on its debt. A key measure of inflation that is closely watched by the Federal Reserve ticked higher than economists expected in April. The persistent pressure from inflation complicates the Fed's fight against high prices. The central bank has been aggressively raising interest rates since 2022, but recently signaled it will likely forgo a rate hike when it meets in mid-June.

Shares of chipmakers are still rising after Marvell and Nvidia last week posted very strong sales forecasts for AI-related products. Most chipmakers were up more than 3% early Tuesday, lifting the tech-heavy Nasdaq 1.5%.

Markets are also waiting for U.S. consumer confidence data set to be released later Tuesday.

In Europe at midday, Germany’s DAX rose 0.5%, Britain's FTSE 100 fell 0.5% and France’s CAC 40 shed 0.4%.

In Asian trading, Japan’s benchmark Nikkei 225 rose 0.3% to 31,328.16. Australia’s S&P/ASX 200 edged down 0.1% to 7,209.30. South Korea’s Kospi jumped 1.0% to 2,585.52.

Hong Kong’s Hang Seng gained 0.2% to 18,595.78. The Shanghai Composite gained less than 0.1%, to 3,224.21.

Analysts say investors remain concerned about the a possible “second wave” of COVID-19 cases in China, although the economic impact is expected to be more limited than from the earlier pandemic wave.

China’s recovery from virus-related disruptions during the past several years appears to be faltering, adding to worries over the regional economy.

“To say China’s economic opening has been a disappointment could be an understatement, especially as reflected in local stocks that are now on the cusp of a bear market,” Stephen Innes of SPI Asset Management said in a commentary.

In other trading, U.S. benchmark crude fell 73 cents to $71.94 a barrel in electronic trading on the New York Mercantile Exchange. Brent crude, the international standard, declined $1.05 to $76.05 per barrel.

The U.S. dollar slipped to 139.62 Japanese yen from 140.44 yen. The euro cost $1.0744, up from $1.0711.

Read Full Story »»»

DiscoverGold

Nvidia on track to hit $1 trillion market cap when market opens

This is a developing news story. Please check back for updates:

https://www.cnbc.com/2023/05/30/nvidia-on-track-to-hit-1-trillion-market-cap-when-market-opens.html

$DIA Not participating. Held just above the 200D this week. Again if they want to rotate nothing heated here...

By: Options Mike | May 29, 2023

• $DIA Also not participating. Held just above the 200D this week. Again if they want to rotate nothing heated here...

Read Full Story »»»

DiscoverGold

The Weekend Rip

by StockTwits

May 28, 2023

It was a turbulent week in markets as the debt ceiling deadline loomed, but U.S. tech stocks and foreign markets helped keep the major indices inching higher.

Let’s recap and prep you for the four-day week ahead.

What Happened

Technology stocks helped push the market to new heights, driven by artificial intelligence (AI) hype. Nvidia’s earnings outlook propelled the stock and its peers to new heights, with it nearing a $1 trillion market cap.

Foreign stocks continued to show strength, with Greece’s stock market breaking out. Speaking of Greece, global shipping companies signaled a continued slowdown in demand and pricing amid economic uncertainty.

The median price of new homes sold in the U.S. declined YoY for the first time since April 2020. Constrained existing home inventories and low affordability continued to weigh on housing demand.

Retailers across the spectrum continue to paint a cautious picture of U.S. consumers, though many expect a rebound in the year’s second half. We recapped Dollar Tree, Best Buy, Big Lots’, Gap, several mall retailers, and many others.

Many tech stocks reported earnings this week, including Snowflake and Intuit. Chinese tech giants showed mixed results.

It was a big Monday of mergers and acquisition news, which we recapped early in the week.

Several names were on the Stocktwits trending tab for most of the week, including $HEPA, $OMH, $TRKA, $MULN, $IEP, $SPCE, and $PLTR.

Here are the closing prices:

S&P 500 4,205 +0.32%

Nasdaq 12,976 +2.51%

Russell 2000 1,773 -0.04%

Dow Jones 33,093 -1.00%

Bullets

Bullets From The Weekend

Meta’s making changes to avoid more U.K. antitrust troubles. Facebook’s parent company is giving assurances to the country’s regulators that it will allow advertisers to opt out of their advertising data being used to develop Facebook Marketplace. The change will come through new technical systems. Still, the company will also train staff to ensure that they don’t use advertiser data when developing new products for use in the U.K. market that may be in direct competition with advertisers. TechCrunch has more.

Realtor numbers pull back amid market slump. Thousands of real estate agents are giving up on the profession, with over 60,000 exiting over the last six months. The number of U.S. realtors peaked at 1.6 million in October and began to trend lower after nearly a year of a significant slowdown in the housing market, where sales of existing single-family homes fell 43% from their 2021 peak. Additionally, average annualized realtor commissions fell from a peak of $84,355 in January 2021 to $56,632 in April 2023. More from Axios.

U.S. debt ceiling debate reaches “an agreement in principle.” U.S. President Joe Biden and top congressional Republican Kevin McCarthy reached a tentative deal to suspend the federal government’s $31.4 trillion debt ceiling after a months-long debate. The deal would include suspending the debt limit through January 2025, capping spending in the 2024 and 2025 budgets, clawing back unused COVID funds, speeding up energy project permitting, and expanding work requirements for food aid programs. The compromises give the deal a slight majority in the Republic House and Democratic Senate, though we’ll have to wait and see if it’s finalized successfully before the June 5th deadline. Reuters has more.

The Brief

Need a concise summary of what’s going on this week? Look no further. Here’s an overview of important earnings and economic data for the trading week ahead.

Economic Calendar

It’s a short but busy week on the economic data front. Investors and the Fed will be watching U.S. employment data later in the week. In addition to the above, check out this week’s complete list of economic releases.

Earnings This Week

Earnings season is nearing its last legs, with 86 companies reporting. Some tickers you may recognize are $CRM, $AI, $AVGO, $CHPT, $EH, $TIGR, $LULU, $M, $DG, $JWN, $CHWY, and more.

NYAD Holds Above 200-Day Moving Average. Liquidity is Shrinking

By: Joe Duarte | May 28, 2023

There's an old adage of Wall Street, which says: "never short a dull market." And while AI is getting all the press these days, the oil market is about as dull as it gets. This, of course, brings the energy sector to the top of my contrarian alert list.

This is not to say that I'm buying oil-related assets with both hands. It just means that, at this point, it makes more sense to look at energy as a value asset, as it is oversold and ripe for a move up whenever the right set of variables required to deliver such a move line up just right.

In the current world, the variables could line up just right as early as today.

There are No Oil Bulls Left

Nobody loves oil.

The level of bearishness expressed by futures traders is at least equal to where it was during the pandemic, and after the Silicon Valley Bank (SIVB) collapse. The International Energy Agency (IEA), forecasts that, of the expected $2.8 trillion in energy investments for 2023, roughly $1.7 trillion will be allocated to low carbon energy sources, including nuclear, solar, and other potential sources. Only $1.1 trillion will be invested in fossil fuels.

And according to the Financial Times, auctioneers in Texas are trying to unload two brand new fracking rigs, which together cost $70 million, for a starting combined bid of just below $17 million.

Supply is the Primary Influence on Oil Prices

Meanwhile, oil companies are quietly merging with competitors, and exploration outside the United States is continuing aggressively, with new discoveries being frequently announced.

Simultaneously, the U.S. active rig count is slowly falling, led by natural gas. The price of gasoline is steadily rising, as the market begins to price in future supply reductions. Just in my neck of the woods, regular unleaded is up some $0.32 in the last week alone.

That doesn't sound like an industry that's planning on fading away. It sounds like an industry that's hunkering down and waiting for better times and preparing to squeeze supply in order to boost prices.

Charting the Oil Sector

The price chart for West Texas Intermediate Crude, the U.S. benchmark (WTIC), shows the depressed price picture which has led investors to walk away. And, until proven otherwise, there are plenty of sellers at the $75-$80 price area, where a sizeable Volume by Price bar highlights the point of resistance.

At first glance, there little difference in the general price behavior for Brent Crude, the European benchmark. (BRENT) where there is a resistance band defined by VBP bars between $80 and $90. A closer look reveals an uptick in Accumulation Distribution (ADI) and the semblance of some nibbling in On Balance Volume (OBV). It's subtle, but it's there.

The oil stocks are far from a bull trend. The Energy Select Sector SPDR ETF (XLE) is trading below its 200-day moving average, facing resistance put from $78 to $90 (VBP bars).

So why bother? Simply stated, OPEC has an upcoming meeting on June 3-4. The cartel is not happy about the prices and the way things are evolving. The Saudi oil minister recently warned bearish speculators to "watch out." And my gut is doing flips when I think about oil, as I see gasoline prices creep up when I drive to work.

But mostly, it's because there are no oil bulls left. This is what we saw in the technology sector a few months ago before its current rally. In early 2023, the tech sector was pronounced dead. The stories were all about the technology sector shuddering as the economy slowed. How about this one, from March 2023, which breathlessly announced a 5.2% decrease in semiconductor sales on a month to month basis and an 18.5% year to year drop?

Yet, as validated by the recent AI-fueled rally, the bad news first marked a bottom, while preceding a significant move up in tech shares.

Never short a dull market.

I've recently recommended several energy sector picks. You can have a look at them with a free trial to my service. In addition, I've posted a Special Report on the oil market which you can gain access to here.

Bond and Mortgage Roller Coaster Reverses Course

Expect negative news about the effect of rising mortgage rates on the homebuilder industry. That's because, as the chart below illustrates, there is a tight and very close correlation between rising bond yields, mortgage rates, and the homebuilder stocks (SPHB).

Moreover, the rise above 3.75% on the U.S. Ten Year Note yield (TNX) has triggered headlines about mortgage rates climbing above 7%. What the news isn't reporting is that, once bond yields roll over, which they are likely to do at some point in the future when the economy shows more signs of slowing and the Fed finally admits that they must pause, is that mortgage rates will drop and demand for new homes will once again pick up. Thus, we will see the homebuilders pick up where they left off.

As things stood last week, SPHB seems to have made a short term bottom.

For now, expect a continuation of the backing and filling in the homebuilder stocks. But, if I'm right and bond yields reverse course, the homebuilders are likely to rally again.

For an in-depth comprehensive outlook on the homebuilder sector click here.

NYAD Holds Above 200-Day Moving Average. SPX Joins NDX in Breaking Out. Liquidity is Shrinking.

The New York Stock Exchange Advance Decline line (NYAD) tested its 200-day moving average on an intra-week basis but did not break below the key technical level. On the other hand, NYAD remained below its 50-day moving average, which is still an intermediate-term negative.

Moreover, with the major indexes (see below) breaking out to new highs, we remain in a technical divergence as the market's breadth is lagging the action in the indexes. This is of some concern, given the fade in the market's liquidity, as I point out below.

The Nasdaq 100 Index (NDX) extended its recent breakout, closing the week well above 14,200. The current move is unsustainable, so some sort of pullback and consolidation are likely over the next few days to weeks. Both ADI and OBV remain encouraging.

What's more bullish is that the S&P 500 (SPX) finally broke out above the 4100–4200 trading range on 5/24/23. On Balance Volume (OBV) is perking up while the Accumulation Distribution (ADI) indicator is very encouraging.

We may be seeing a shift from a short-covering rally to a fear-of-missing-out buyer's rally.

VIX Holds Steady

The CBOE Volatility Index (VIX) remained below 20, as it has since March 2023. This remains a positive for the markets, as it shows short sellers are staying away at the moment.

When the VIX rises, stocks tend to fall, as rising put volume is a sign that market makers are selling stock index futures to hedge their put sales to the public. A fall in VIX is bullish, as it means less put option buying, and it eventually leads to call buying, which causes market makers to hedge by buying stock index futures. This raises the odds of higher stock prices.

Liquidity is Getting Squeezed

The market's liquidity is now in a downtrend. The Eurodollar Index (XED) is now below 94.5, and looks weak. A move above 95 will be a bullish development. Usually, a stable or rising XED is very bullish for stocks.

Read Full Story »»»

DiscoverGold

2023 S&P Sector Returns...

By: Charlie Bilello | May 27, 2023

• 2023 S&P Sector Returns...

Tech $XLK: +33%

Communications $XLC: +30%

Consumer Discretionary $XLY: +18%

Industrials $XLI: +1%

Consumer Staples $XLP: -1%

Materials $XLB: -1%

Real Estate $XLRE: -3%

Health Care $XLV: -6%

Financials $XLF: -6%

Utilities $XLU: -8%

Energy $XLE: -9%

Read Full Story »»»

DiscoverGold

S&P 500 Index (SPX) »» Weekly Summary Analysis

By: Marty Armstrong | May 27, 2023

The S&P 500 Cash Index has been in an uptrend for the past 2 days closing above the previous session's high by 0.95%. The broader rally has peaked with the last high established at 421291 back on 05/19 5 days ago. We did elect 2 Bearish Reversals from this high. Clearly, this high was formed after a rally of 11 days.

Currently, the market is trading somewhat bullish on our indicators still showing overhead resistance but it is trading strongly higher up some 2.01% from the previous session low. Our projected target for closing resistance for the next session stands at 426731, we need to close above that target to imply a further advance. Failure to even exceed this intraday warns that the upward momentum is starting to decline. Nevertheless, this session closed below our ideal projection for closing resistance warning that the market which stood at 422750 is forming a high. A break of this session's low of 415616 will warn that we have a potential temporary high in place.

Up to now, we still have only a 1 month reaction rally from the low established during March. We must exceed the 3 month mark in order to imply that a trend is developing.

ECONOMIC CONFIDENCE MODEL CORRELATION

Here in S&P 500 Cash Index, we do find that this particular market has correlated with our Economic Confidence Model in the past. Our next ECM target remains Tue. May 7, 2024. The Last turning point on the ECM cycle low to line up with this market was 2020 and 2009 and 2002. The Last turning point on the ECM cycle high to line up with this market was 2022 and 2007 and 2000.

MARKET OVERVIEW

NEAR-TERM OUTLOOK

The historical perspective in the S&P 500 Cash Index included a rally from 1974 moving into a major high for 2022, the market has pulled back for the current year. The last Yearly Reversal to be elected was a Bullish at the close of 2020 which signaled the rally would continue into 2022. However, the market has been unable to exceed that level intraday since then. This overall rally has been 2 years in the making.

This market remains in a positive position on the weekly to yearly levels of our indicating models. Nevertheless, it closed last year on the weak side down from 2021. Pay attention to the Monthly level for any serious change in long-term trend ahead.

Looking at the indicating ranges on the Daily level in the S&P 500 Cash Index, this market remains moderately bullish currently with underlying support beginning at 417968 and overhead resistance forming above at 420922. The market is trading closer to the resistance level at this time. An opening above this level in the next session will imply that a bounce is unfolding.

On the weekly level, the last important high was established the week of May 15th at 421291, which was up 31 weeks from the low made back during the week of October 10th. This was a key week for at least a temporary high on the Pi cycle. We have seen the market drop sharply for the past week penetrating the previous week's low and yet it recovered to close above the previous week's close of 419198. We are still trading above the Weekly Momentum Indicators so we have not undermined critical support as of yet.

INTERMEDIATE-TERM OUTLOOK

YEARLY MOMENTUM MODEL INDICATOR

Our Momentum Models are declining at this time with the previous high made 2021 while the last low formed on 2022. However, this market has rallied in price with the last cyclical high formed on 2022 and thus we have a divergence warning that this market is starting to run out of strength on the upside.

After closing above last year's low of 366271.

The market is trading some 0.23% percent above the last high 419544 from which we did originally obtain one sell signal from that event established during February. Long-Term critical support still underlies this market at 372320 and only a break of that level on a monthly closing basis would warn of a break of the current uptrend. At this time, the market is holding and is trading above last month's high as well.

DiscoverGold Breitbart Business News

May 26, 2023

Inflation Is Still Stuck on Us

It is getting harder and harder to justify not raising rates at the next meeting of the Federal Open Market Committee.

The Bureau of Economic Analysis on Friday released its personal-consumption expenditures (PCE) price index for April. Wall Street had been expecting the price index to climb 0.3 percent after inching up by just 0.1 percent in March. Since this index comes out weeks after the Labor Department's consumer price and producer price index, it should be fairly predictable based on similar data already received.

Yet we got an upside surprise. PCE inflation rose by four-tenths of a percentage point. Over the past 12 months, PCE inflation is up 4.4 percent, also a tenth of a point higher than expected and up two-tenths from the March reading.

Core PCE inflation, which excludes food and energy prices, were likewise up 0.4 percent from the prior month. From a year ago, core prices are 4.7 percent. Both were higher than the March. numbers and higher than Wall Street expected.

Core PCE inflation has been in a tight range of 4.6 to 4.7 for five months. This suggests that the Fed has not made much progress at all when it comes to inflation.

Watching What the Fed Watches

The Federal Reserve uses PCE inflation for its two percent target as well as in the Summary of Economic Projections (SEP) that gets released every other FOMC meeting. Fed officials also forecast core PCE inflation in the SEP. While Fed Chair Jerome Powell and others have emphasized that they also look at other measures of inflation, PCE inflation is certainly viewed as the Fed's "favored" metric. So, it gets a lot of attention from anyone trying to figure out where rates are heading.

The last SEP was released at the March meeting. It showed that the median expectation for headline PCE inflation for 2023 was 3.3 percent, up from 3.1 percent in the prior summary from December. The range of projections was for between 2.8 percent and 4.1 percent. Core PCE was expected to come in at 3.6 percent for the year, up from 3.5 percent.

Those projections now look unrealistic. It would take a very severe downturn in inflation in the last eight months of the year to bring headline down to 3.3 percent and core down to 3.6 percent. Getting there would require a large pullback in consumer spending and a big uptick in unemployment. This means it is likely that Fed officials will raise their forecasts for inflation at the next meeting.

One alternative metric that has been singled out by Powell several times is PCE core services inflation excluding housing. This rose 0.42 percent in April, which amounts to a 5.2 percent annualized rate. Powell would probably look at the last three month annualized rate, which comes out to 4.4 percent. The six month annualized rate is 4.9 percent, and the 12 month is 4.9 percent. As Nick Timiraos of the Wall Street Journal pointed out, this measure has basically gone sideways for several months.

The second point Timiraos makes is also worth highlighting. The disinflation in core goods prices has slowed, offsetting the leveling out of housing inflation. Many economists had been expecting outright deflation—meaning falling prices—in goods after last year's huge increases. That has not happened.

In his speech earlier this week, Fed Governor Christopher Waller warned about this exact dynamic:

We're hoping there will be a continued slowdown in goods price increases, but we aren't seeing deflation in this category like we had pre-pandemic. A second concern is rent increases, which accounts for most of a category called housing services and is a sizable component of inflation. Lower rent increases from lease renewals last year are slowly making their way into the inflation data, but most recently, a rebound in the housing market is raising questions about how sustained those lower rent increases will be. While housing prices actually have less of a short-term effect on rents than one might think, this upturn in the housing market, which comes even with significantly higher mortgage rates, has raised questions about whether the benefit from the slowing in rent increases will last as long as we have been expecting.

The Median Is the Message

That is where inflation has been. Where is it going? For that we return to our old friends, median and trimmed mean inflation.

The Cleveland Fed calculates median PCE inflation each month, and we consider it a reasonably reliable guide to underlying inflationary forces that can allow for predictions about where inflation is likely to be in the months ahead. This was also up 0.4 percent for the month, exactly the same as headline and core. That's a signal that inflation is no longer being pushed around by outlying factors but is now broad-based.

The only trend detectable in median PCE inflation is sideways. It has been 0.4 percent in five out of the last six months. The exception was in January, when it rose 0.6 percent. The message from this is that PCE inflation probably cannot be expected to move down much. It's certainly not on a reliable path to two percent.

The Dallas Fed calculates 16 percent trimmed mean PCE inflation, which excludes eight percent on both ends of the basket of goods and services that goes into calculation of the PCE price index. This is another measure intended to reveal underlying inflation and provide a ground for forecasts of inflation's trend. It is reported on an annualized basis for one month, six months, and 12 months. The one-month annualized figure for April was 4.4 percent, up from 3.8 percent in March and tied with February as the second-highest reading over the past six months. The six-month annualized trimmed mean is also 4.4 percent, exactly where it was in March. The 12-month annualized trimmed mean increased to 4.8 percent, up from 4.7 percent.

Like median inflation, trimmed mean is pointing toward inflation not coming down by much at all.

It is still possible that the Fed will decide to keep policy rates unchanged at its June meeting. A strong jobs report next Friday, however, could extinguish that possibility. The market is looking for around 180,000 jobs. Anything above 200,000 will create a lot of pressure for the Fed to hike. And even if the Fed does opt to hold rates unchanged, it is likely to send the message that this is a "skip" until the July meeting rather than the beginning of a long-term pause.

As Cleveland Federal Reserve President Loretta Mester said in an interview on Friday: “The data coming in this morning suggest we have more work to do."

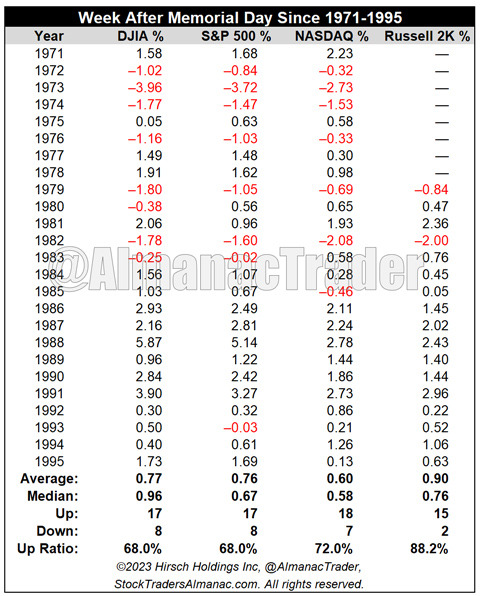

Market Weaker After Memorial Day Recent Years

By: Almanac Trader | May 26, 2023

The week after Memorial Day performed quite well 1971-95. DJIA & S&P up 68% of the time, averaging 0.8% – DJIA up 12 in a row 1984-95. NAS was up 72% of the time, average 0.6%, up 10 straight 1986-95. Since 1979 R2K was up 88.2% of the time, average 0.9%, up 13 straight 1983-95.

Starting in 1996 the week after Memorial Day performance diminished. DJIA was up only 40.7% of times, average loss 0.02%, down 9 of last 13. S&P, NAS & R2K all gained ground less than 56% of the time, down 7 of last 13. Huge gains during the week in 2000 do skew the averages.

2023 Stock Trader’s Almanac page 100 tracks behavior before & after holidays since 1980. Days after Memorial Day show positivity. But weakness has increased the last 22-years the 3 days after Memorial Day. Day after Memorial Day DJIA & NAS down 6 of last 8, S&P down 7 of last 8.

Read Full Story »»»

DiscoverGold

All major U.S. stock markets will be closed on Monday May 29, 2023, in observance of Memorial Day.

Iconic Chicago Company Threatens to Leave >

https://theblacksphere.net/2023/05/iconic-chicago-company-threatens-to-leave/

US Equity Fund Outflows -$513 Million; Taxable Bond Fund Inflows $5.5 Billion

By: Refinitiv | May 25, 2023

• FUND FLOW REPORTS FOR THE WEEK ENDED 05/24 ARE NOW AVAILABLE.

For the week ended 05/24/2023 ExETFs - All Equity funds report net outflows totaling -$7.716 billion, with Domestic Equity funds reporting net outflows of -$6.476 billion and Non-Domestic Equity funds reporting net outflows of -$1.240 billion...ExETFs - Emerging Markets Equity funds report net outflows of -$0.727 billion...Net inflows are reported for All Taxable Bond funds of $5.474 billion, bringing the rate of inflows for the $3.548 trillion sector to $1.645 billion/week...International & Global Debt funds posted net outflows of -$0.434 billion...Net inflows of $3.015 billion were reported for Corp-Investment Grade funds while High Yield funds reported net inflows of $1.399 billion...Money Market funds reported net inflows of $43.112 billion...ExETFs - Municipal Bond funds report net outflows of -$0.847 billion.

Read Full Story »»»

DiscoverGold

Money managers Increased their exposure to the US Equity markets since last week...

DiscoverGold

NAAIM Exposure Index

May 25, 2023

The NAAIM Number

65.51

Last Quarter Average

63.74

»»» Read More…

2023 S&P Sector Returns...

By: Charlie Bilello | May 25, 2023

• 2023 S&P Sector Returns...

Tech $XLK: +29%

Communications $XLC: +27%

Consumer Discretionary $XLY: +15%

Industrials $XLI: -0.2%

Consumer Staples $XLP: -1%

Materials $XLB: -2%

Real Estate $XLRE: -4%

Health Care $XLV: -6%

Financials $XLF: -6%

Utilities $XLU: -8%

Energy $XLE: -9%

Read Full Story »»»

DiscoverGold

Wall Street's Year End Targets for the S&P 500

By: Barchart | May 25, 2023

• Wall Street's Year End Targets for the S&P 500.

Read Full Story »»»

DiscoverGold

Orders by Fidelity customers - Expanded Listing

Rank is based on the total of buy and sell orders for the security.

Information shown below in the table is based on the aggregate number of orders entered by Fidelity Brokerage Services LLC self-directed retail customers “as of” the date and time shown.

Symbol % Change # Buy orders Buy/sell ratio # Sell orders Sector

NVDA +25.66% 14,500

Buy 38.44%

Sell 61.56%

23,225 Information Technology

TSLA +0.89% 4,023

Buy 46.89%

Sell 53.11%

4,556 Consumer Discretionary

AMD +10.13% 2,778

Buy 34.25%

Sell 65.75%

5,333 Information Technology

SQQQ -6.97% 3,587

Buy 60.63%

Sell 39.37%

2,329

SNOW -16.58% 3,563

Buy 71.02%

Sell 28.98%

1,454 Information Technology

BMR +115.72% 2,238

Buy 52.13%

Sell 47.87%

2,055 Information Technology

SOXL +17.16% 1,216

Buy 30.75%

Sell 69.25%

2,738

TQQQ +7.10% 1,527

Buy 38.74%

Sell 61.26%

2,415

MSFT +3.54% 1,355

Buy 35.88%

Sell 64.12%

2,422 Information Technology

SOXS -17.13% 2,657

Buy 75.59%

Sell 24.41%

858

AMZN -1.42% 1,832

Buy 54.8%

Sell 45.2%

1,511 Consumer Discretionary

PLTR +1.88% 1,876

Buy 57.37%

Sell 42.63%

1,394 Information Technology

NVDS -32.25% 2,154

Buy 74.48%

Sell 25.52%

738

WLDS +258.96% 1,271

Buy 46.9%

Sell 53.1%

1,439 Information Technology

AI -2.01% 1,270

Buy 49.11%

Sell 50.89%

1,316 Information Technology

T -5.17% 2,211

Buy 87.39%

Sell 12.61%

319 Communication Services

AAPL +0.59% 1,324

Buy 57.74%

Sell 42.26%

969 Information Technology

QQQ +2.40% 1,155

Buy 50.88%

Sell 49.12%

1,115

INTC -6.42% 1,827

Buy 83.5%

Sell 16.5%

361 Information Technology

VZ -2.56% 1,934

Buy 92.1%

Sell 7.9%

166 Communication Services

TNA -3.28% 1,180

Buy 57.37%

Sell 42.63%

877

BBBYQ +12.78% 1,487

Buy 86.1%

Sell 13.9%

240 Consumer Discretionary

TSM +12.38% 579

Buy 33.66%

Sell 66.34%

1,141 Information Technology

SPY +0.72% 911

Buy 53.94%

Sell 46.06%

778

META +2.20% 743

Buy 44.6%

Sell 55.4%

923 Communication Services

GOOGL +2.93% 790

Buy 50.74%

Sell 49.26%

767 Communication Services

TCEHY -2.61% 828

Buy 54.01%

Sell 45.99%

705 Communication Services

DIS -1.04% 1,133

Buy 78.52%

Sell 21.48%

310 Communication Services

UPRO +1.97% 685

Buy 48.21%

Sell 51.79%

736

NA +51.12% 572

Buy 44.48%

Sell 55.52%

714 Information Technology

0

CNBC News

1. Plodding along

Stocks are coming off a rough day. All three major indices took a dive Wednesday after debt ceiling negotiations yet again yielded no deal. We could be in for a jumbled Thursday, however, after both Fitch’s warning about the U.S. debt rating and Nvidia’s blowout earnings report (more on both below). Investors will also chew over a new slate of retail earnings, including Best Buy and Dollar Tree, as well as pending home sales data and weekly jobless claims. Follow live market updates.

2. One week to get it done

The Treasury Department has warned the U.S. could run out of money to pay its bills as soon as June 1, which is exactly one week from Thursday. So, what’s the status of negotiations between the White House and House Speaker Kevin McCarthy’s team? Improving, but still not where they need to be. The House, in fact, will be allowed to go home for Memorial Day weekend, although they’re on call to come back for a vote. Meanwhile, the possibility of an unprecedented default on U.S. debt is ratcheting up the external pressure on Congress to raise the debt ceiling. Fitch put the U.S.’s triple-A status on rating watch negative, citing the tense debt talks.

3. Blowout report from Nvidia

Nvidia shares soared after the chip maker posted a big earnings beat and offered sales guidance way above Wall Street’s estimates. The stock was already up 109% this year going into the earnings report after the bell Wednesday. The company is riding an artificial intelligence-driven wave of demand for chips. Its data center business posted a 14% increase in quarterly revenue. As CNBC’s Kif Leswing points out, this robust result shows how important AI chips are becoming for cloud vendors and other companies running a lot of servers.

4. Ups and downs at the mall

It’s a tale of two mall retailers. American Eagle Outfitters’ shares plunged 19% in off-hours trading after the company said Wednesday afternoon it lowered its outlook for revenue and operating income for the year, citing a slowdown in sales heading into the current quarter. American Eagle also had a tough act to follow. Before the bell Wednesday, rival Abercrombie & Fitch posted a surprise profit and raised its guidance for the year. That, in turn, sparked a monster rally in the stock. Shares surged 31%, accounting for nearly all of Abercrombie’s gains this year.

5. Awkward ...

In Twitter Spaces, no one can hear you stream. At least that was the case Wednesday night for Florida Gov. Ron DeSantis, Twitter owner and Tesla CEO Elon Musk and conservative tech investor David Sacks. DeSantis was set to announce his (already established and widely known) candidacy for presidency at 6 p.m. ET, but numerous glitches and crashes forced the men to shut down the livestream after about 25 minutes. They blamed server issues because more than 500,000 people piled into the stream. They started a second one, which went much more smoothly from a tech perspective and drew about 300,000 listeners. DeSantis supporters spun the disastrous rollout as a positive, saying it was a sign that DeSantis was generating excitement. But, as CNBC’s Kevin Breuninger noted, an audience of that size would be considered a ratings disappointment on primetime cable news.

— CNBC’s Mike Calia wrote this newsletter. Sarah Min, Christina Wilkie, Emma Kinery, Darla Mercado, Kif Leswing, Gabrielle Fonrouge, Melissa Repko and Kevin Breuninger contributed.

Nvidia shares spike 26% on huge forecast beat driven by A.I. chip demand >

https://www.cnbc.com/2023/05/24/nvidia-nvda-earnings-report-q1-2024.html

Deteriorating liquidity may be a significant headwind for the S&P 500

By: Isabelnet | May 24, 2023

• Valuation

Deteriorating liquidity may be a significant headwind for the S&P 500.

Read Full Story »»»

DiscoverGold

CNBC

1. Gloom grows

This week isn’t looking so hot for stocks. After a mixed session Monday, the three major U.S. stock indices all fell Tuesday, with the Nasdaq and the S&P 500 each declining by more than 1%. And each day without a debt ceiling deal in Washington (see below for more) ratchets up the tension as investors dwell more on what could be the United States’ first sovereign default. Retailers’ earnings haven’t been so strong, either, as companies warn of a slowdown in consumer spending. Kohl’s and mall retailers Abercrombie & Fitch and American Eagle are next up to report Wednesday. In the afternoon, the Federal Reserve is slated to release the minutes from its meeting earlier this month. Follow live market updates.

2. What's the deal?

The United States could run out of money to pay its debts as soon as June 1 – eight days from now – and there still isn’t a deal in Washington. Some Republicans questioned whether the deadline is actually so soon, suggesting there’s more wiggle room for talks. Negotiations have been heating up, however, as the White House and House Speaker Kevin McCarthy’s team tightened their focus for compromise on a handful of issues. Wednesday’s talks could be pivotal, especially with lawmakers itching to get out of town for Memorial Day weekend.

3. Netflix cracks down

It took a little longer than expected, but Netflix’s password-sharing crackdown has come to the U.S. after rolling out in other countries. On Tuesday, the streaming giant said it started emailing subscribers to lay down the law on passwords. “Your Netflix account is for you and the people you live with — your household,” the emails read. Each account user outside of a household will cost an extra $7.99 a month. These users can also transfer their Netflix profile if they want to start their own account. Netflix, like other streamers, is in a profitability push as subscriber growth slows. Company executives have said the new password-sharing policy will probably result in fewer viewers at first, with many eventually coming back to start their own accounts.

4. It's over

Virgin Orbit, the once-promising rocket company founded by Richard Branson, is now fully dead after selling off the bulk of its assets to aerospace companies Rocket Lab, Stratolaunch and Launcher. The company’s six remaining rockets, which are in various states of development, have yet to be sold, nor has the company’s intellectual property. Virgin Orbit once reached a multibillion-dollar valuation as its novel concept – launching space rockets from refitted airliners mid-flight – turned heads, but the company had problems executing quickly and raising money, eventually leading to its bankruptcy and liquidation.

5. The Ron and Elon Show

This is the day we stop calling Ron DeSantis a potential presidential candidate. The Florida governor is expected to announce his run 6 p.m. ET Wednesday on Twitter Spaces, in a discussion with the social platform’s owner and Tesla CEO Elon Musk, as well as Musk supporter and investor David Sacks. The political world has been eager to see DeSantis jump into the Republican primary after months of hype. While he’s widely seen as the strongest challenger to former President Donald Trump for the GOP nomination in 2024, he’s nonetheless a distant second in the polls. DeSantis, though, will be banking on a strong network of donors to help him convince Republican voters that he should be the one to take on President Joe Biden next year.

— CNBC’s Mike Calia wrote this newsletter. Hakyung Kim, Christina Wilkie, Lillian Rizzo, Michael Sheetz and Brian Schwartz contributed.

Small Caps Russell 2000 (IWM) Are Ready To Launch!

By: Tom Bowley | May 23, 2023

There are many who have given up on the small cap community, but I'm not one of them. The long-term 15-year chart remains in a solid uptrend. Yes, the group has been underperforming the S&P 500 for quite awhile, but that's been the standard since this bull market began. Admittedly, its relative strength has been poor. Its absolute performance, however, remains in an uptrend and we could be on the verge of a major breakout today. Check out this daily chart:

While the IWM has been floundering, check out that bottom panel. Money has been steadily rotating from small cap value ($DJUSVS) to small cap growth ($DJUSGS). I've been discussing this with our EarningsBeats.com members for the last several weeks. This bottoming formation (blue circles), though a bit longer in duration, is quite similar to previous bottoms. The MAJOR difference this time is the shift to small cap growth, which I believe is a signal that this breakout won't simply be short-term, and the simultaneous bullish PPO crossover (black circle). I'm looking for a small cap explosion on this breakout, IF it confirms into today's close! I'm betting it will.

Read Full Story »»»

DiscoverGold

CNBC Morning news

1. Looking for a way forward

Stocks kicked off the week with a jumbled session Monday, as investors work to get a grasp on the state of the economy and what could come next, especially with the debt ceiling negotiations (more on that below). The Nasdaq finished higher, giving the index its best close since August, while the Dow fell slightly and the S&P 500 was effectively flat. Tuesday brings a fresh slate of earnings for markets to pick over, including from retailers Lowe’s and Dick’s Sporting Goods before the bell. Follow live market updates.

2. Debt limit dealings

We are a little over a week from when the United States could run out of money to pay its bills, and there’s still no deal in Washington. However, President Joe Biden and House Speaker Kevin McCarthy both said after their meeting Monday evening that they’re cautiously optimistic they can agree on a way to address the debt limit as their sides also sort out a budget compromise. Tuesday and Wednesday will be especially important for a deal to come together. Lawmakers are also up against Memorial Day weekend in a few days, and Congress hates to miss a holiday.

3. TikTok sues Montana

In what’s sure to be a preview of cases to come, TikTok sued Montana to overturn the state’s ban on the app. Last week, Montana became the first state to ban TikTok, saying it posed a security risk due to its parent company, ByteDance, being Chinese-owned. “Yet the State cites nothing to support these allegations,” lawyers for ByteDance wrote. The lawyers argue that Montana’s law is unconstitutional, saying it violates the First Amendment’s freedom of speech while also preempting federal law. TikTok is facing heat from politicians on both sides of the aisle, in Washington and at the state level, as the popular app’s owners try to distance it from perceptions it’s controlled by the Chinese government. The Montana ban goes into effect Jan. 1.

4. Lowe's cuts guidance

Home improvement chain Lowe’s lowered its revenue outlook for the year, as lumber prices have fallen and customers pared back spending on do-it-yourself projects. As we’ve seen from retail earnings so far, shoppers are spending less on things they don’t need while focusing more on necessities. Last week, Lowe’s rival Home Depot said its shoppers were spending less on renovation projects. Spring is typically the big season for hardware and home improvement stores, but it doesn’t appear that way this year. Lowe’s same-store sales for the period ended May 5 fell more than Wall Street expected, and the company lowered its same-store-sales expectations for the year.

5. Dimon on commercial real estate

The CEO of the largest bank in America sees more trouble ahead for the financial system, thanks to commercial real estate. “There’s always an off-sides,” JPMorgan Chase CEO Jamie Dimon said during the company’s investor conference Monday. “The off-sides in this case will probably be real estate. It’ll be certain locations, certain office properties, certain construction loans. It could be very isolated; it won’t be every bank.” Dimon joins a growing chorus of business leaders and experts who say commercial real estate could be the next big problem for the financial industry after the recent regional bank crisis. Earlier this month, Warren Buffett and Charlie Munger said commercial real estate is starting to see consequences from too many people borrowing at low rates.

— CNBC’s Mike Calia wrote this newsletter. Alex Harring, Christina Wilkie, Melissa Repko, Jonathan Vanian and Hugh Son contributed.

Another investor survey moves into favorable territory

By: Jay Kaeppel | May 22, 2023

• Investor surveys tend to be contrary in nature. But not all surveys are created equal, it would appear. One measure of sentiment among active money managers seems to add weight to the bullish case for stocks presently.

Read Full Story »»»

DiscoverGold

CNBC Morning news..

1. Another winning week?

Stock futures were flat Monday as Wall Street watches debt ceiling negotiations in Washington. The three major U.S. indexes climbed last week, and the borrowing limit talks, earnings and a couple of economic data points will help to determine whether they post a second straight winning week. The minutes from the last Federal Reserve meeting, which could illuminate future interest rate policy, will come out Wednesday. The government will offer a second read on first-quarter GDP on Thursday. The personal consumption expenditures price index, a key inflation gauge the Fed watches closely while making its interest rate decisions, is due Friday. Follow live market updates here.

2. Debt deadline draws close

Policymakers in Washington have only 10 days to raise or suspend the debt ceiling before they risk a first-ever U.S. default as early as June 1. Talks between the White House and House Republicans kicked back into gear Sunday as President Joe Biden returned from the G-7 summit in Japan. Biden and House Speaker Kevin McCarthy, R-Calif., plan to meet Monday afternoon in a positive sign for the discussions, which moved markets throughout last week. The time of their huddle was unclear as of Monday morning. A U.S. default would damage the U.S. and global economies – and force the Treasury to make “hard choices” about which bills to pay, Treasury Secretary Janet Yellen said Sunday. Raising the debt ceiling does not authorize new spending, but Republicans have pushed Democrats to slash fresh outlays as part of a deal to increase the borrowing limit.

3. Retail has more to say

As first-quarter earnings season winds down, retail will again dominate the slate of companies reporting this week. The biggest names posting results include Lowe’s and Best Buy. But other retailers from Kohl’s to Gap will also offer more information about how consumers are spending their money, and what businesses are doing to keep shoppers buying. Last week’s reports that included Home Depot, Target and Walmart suggested inflation is still hampering households, and some companies indicated sales slowed as the first quarter went on. Here are some of the key companies reporting this week:

Tuesday: Lowe’s (before the bell)

Wednesday: Kohl’s (before the bell); Nvidia (after the bell)

Thursday: Best Buy (before the bell); Gap (after the bell)

4. Meta hit with record fine

European regulators handed Meta a 1.2 billion euro ($1.3 billion) fine for allegedly sending EU user data to the U.S. The penalty is the largest handed out for alleged violations of the landmark digital privacy rule known as the General Data Protection Regulation, which took effect in 2018. Regulators ordered the Facebook owner to suspend future data transfers to the U.S. Meta plans to appeal the decision.

5. Chip clashes continue

Shares of Micron slid in premarket trading after China said it would bar some purchases of the U.S. chipmaker’s products. Chinese semiconductor stocks popped on the news. The ban, sparked by a review from China’s Cyberspace Administration, extends to operators of “critical information infrastructure.” The administration said in a statement that Micron’s chips “have serious network security risks, which pose significant security risks to China’s critical information infrastructure supply chain, affecting China’s national security.” Increasing economic and political tensions between the U.S. and China have extended to the supply of semiconductors, which is critical for a range of industries. Micron said it would continue to engage with Chinese authorities, according to Reuters.

— CNBC’s Jacob Pramuk wrote this newsletter. Jesse Pound, Ashley Capoot, Melissa Repko, Arjun Kharpal, Lim Hui Jie and Jihye Lee contributed.

Ryanair reports bumper profit on ‘favorable’ fuel hedges, sees major industry consolidation >

https://www.cnbc.com/2023/05/22/ryanair-reports-bumper-profit-on-favorable-fuel-hedges-sees-major-industry-consolidation.html

Meta fined a record $1.3 billion over EU user data transfers to the U.S.

This is a developing news story. Please check back for updates:

https://www.cnbc.com/2023/05/22/meta-fined-record-1point3-billion-over-eu-user-data-transfers-to-the-us-.html

NYAD Dances on Tightrope as Potential Divergence Develops

By: Joe Duarte | May 21, 2023

Here is a bullish thought. The Federal Reserve seems to have lost its consensus about higher interest rates. Consider the following:

On the day the Nasdaq 100 Index (NDX) broke out to a new high, 5/18/23, the Federal Reserve's recently anointed Dallas Fed president, Lorie Logan, noted the Fed had "made progress" against inflation. However, she clarified that unless the data changes – whatever that means – "we aren't there yet."

Here are some numbers released around her speech:

• Leading economic indicators dropped 0.6%, the 13th straight monthly decline;

• Existing home sales dropped in April – the 14th drop in 15 months;

• Foot Locker (FL) shares crashed as they missed earnings expectations and commented on slowing consumer spending; and

• Regional bank shares sold off once again on remarks by Treasury Secretary Yellen, suggesting that more bank failures may be on the way.

On 5/19/23, Fed Chair Powell noted rate hikes may end sooner rather than later as the banking crisis persists. Stocks sold off on Powell's remarks, but, again, no major damage was done to the indexes, although the market's breadth, as I discuss below, remained troubling.

Meanwhile, the debt ceiling kabuki theater continued, although the odds of some sort of deal are better than even. They always make a deal when the market starts rumbling. No one wants to be blamed for a preventable economic crash.

All in all, when the Fed starts arguing about the future of rates in public, the odds that the worst is over are likely on the rise.

Trade What You See. The New Buzzword is A.I.

Perhaps the most telling sign as to what the stock market thinks of the Fed and the general state of affairs was the sharp breakout on the Nasdaq 100 index (NDX), which came despite a move above 3.6% on the U.S. Ten Year Note yield (TNX). I'll have more on both these markets below.

But suffice it to say, that the new buzz in tech is all about A.I. If that feels familiar, think about the dotcom boom, and its close relative Y2K. Both of those "buzz-driven" rallies made fortunes for those who were able to ride them and get off the train early enough.

We may be entering one of those periods.

Playing the AI Megatrend

If nothing else, Wall Street is good at creating buzz over technology trends. And this one's no different than any of the past ones. Thus, when ChatGPT started to gather steam, so too did the Nasdaq 100 bottom out. I detail the recent action in the index below. But, as I noted last week, owning the Invesco QQQ Trust (QQQ), or stocks which are housed in the ETF, has paid off from an investment standpoint.

Note that QQQ, along with NDX, started to bottom out in November 2022, just as ChatGPT started making headlines. Specifically, the big tech bottom began in late 2022, while ChatGPT was "born" on November 30. Since then, NDX, led by a handful of the usual-suspects mega-cap tech stocks, has been on a tear, which culminated with a breakout above 13,300 on 5/18/23.

Microsoft (MSFT), Alphabet (GOOGL), and Apple (AAPL), among others, have broken out to new highs, because of their association or potential association with A.I. Of the three, the most reliable as a bellwether for what's likely to happen in the A.I. segment is Microsoft. That's because an increasing percentage of its earnings is coming from its cloud services division.

Another high flyer on the A.I. whirlwind has been Nvidia (NVDA), long known for its next generation gaming chips and more recently for its association with A.I. via its graphics processing unit heavy lifting data processing chips (GPU).

My point is that it's clear A.I. is going to be something to deal with as an investor for the next few years. At the same time, it's a bit mindboggling that the biggest beneficiaries of what should be a breakthrough technology are stodgy old tech companies like Microsoft, instead of a startup or two who delivered the technology and are making it available.

For the record, the creator of ChatGPT, Open AI, is still described as a Unicorn and is not publicly traded. Of course, knowing Wall Street, that could change sooner rather than later, unless of course someone buys the company out before it goes public.

Moreover, the big tech stocks have come a long way over the last six months and are due for some sort of pause. At the same time, there are still lots of well-run fundamentally sound tech stocks which have yet to pop. In other words, it is not out of the realm of possibilities that, even as the current crop of tech giants consolidate after their heady gains, the next tier will start to pick up steam.

Bond and Mortgage Roller Coaster Reverses Course

Stock traders weren't listening to Dallas Fed president Logan, but it seems as if bond traders were, which would explain a move above 3.6% for the U.S. Ten Year note (TNX). Of course, mortgage rates followed. Thus, we may see a bit of a pullback in the homebuilder stocks in the short term.

I expect that, once bond yields roll over, we will see the homebuilders pick up where they left off.

As I've noted here for several weeks, the long-term relationship between the U.S. Ten Year Note yield (TNX), mortgage rates (MORTGAGE), and the Homebuilder sector (SPHB) remains intact, as the recent fall in yields and mortgage rates has again led to a rise in the homebuilder sector.

I'm seeing quite a bit of traffic in my usual homebuilder kick the tires haunts, which tells me buyers are picking potential places to make a move on when mortgage rates fall.

For an in-depth comprehensive outlook on the homebuilder sector click here.

NYAD Dances on Tightrope as Potential Divergence Develops

The New York Stock Exchange Advance Decline line (NYAD) continues to walk along the tightrope provided by its 50-day moving average. It recovered from the prior week's nasty-looking break below its 50-day moving average and remains above its 200-day moving average.

At the same time, however, it's hard to ignore the fact that NDX, see below, made a new high and NYAD has been lagging. This divergence is concerning.

The Nasdaq 100 Index (NDX) broke out, closing well above the previous resistance level of 13,400, which now becomes support. Both ADI and OBV are moving higher here, as new buyers are causing short sellers to leave at a faster pace.

As with NDX, the S&P 500 (SPX) broke out above the 4100–4200 trading range on 5/18/23, although it did not hold above the key resistance level. On Balance Volume (OBV) is again flattening out as sellers pull back. Accumulation Distribution (ADI) remain very constructive for SPX as short sellers continue to leave.

VIX Holds Steady

The CBOE Volatility Index (VIX) has been stable lately, trading well below 20 since March 2023. This is a positive for the markets, as it shows short sellers are staying away at the moment.