News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Walmart raises full-year guidance, as earnings beat on boost from grocery and online businesses

This is a developing news story. Please check back for updates:

https://www.cnbc.com/2023/05/18/walmart-wmt-q1-2024.html

Breitbart business News

by John Carney - Breitbart Economics Editor and Alex Marlow - Breitbart Editor-In-Chief

March 14, 2023

Silicon Valley Bet It Could Avoid the Costs of Managing Banking Risk. It Won That Bet.

Silicon Valley essentially put the cost of ordinary corporate treasury prudence onto the banking system and got rewarded for it when the government broke its own rules and agreed to back even the largest deposits at Silicon Valley Bank (SVB).

In a joint statement, the Treasury, Federal Reserve, and the FDIC announced that all deposits at SVB and Signature Bank would be made whole. To accomplish this, the regulators declared that the failure of the banks posed "systemic risk" and therefore qualified for an exception to the usual limits on deposit insurance.

Does this qualify as a bailout? The official statement was clear in saying that “shareholders and certain unsecured debtholders” would not be protected and that senior management would be removed. The shareholders are likely to lose all of their investment, and holders of bonds issued by the banks may be zeroed out as well. It's possible they could be in for some recovery if the banks' assets prove to be more than enough to pay off depositors, but that is likely a long way off and will certainly involve some losses.

So, this is not quite a 2008-style bailout. In that instance, equity holders were heavily diluted when the government used the TARP funds to buy preferred equity stakes. But they did not see the value of their stock go to zero. They were allowed to participate in the recovery of the companies. Holders of debts issued by the financial institutions were almost universally made whole.

On the other hand, the move definitely bails out depositors who had more than $250,000 at the banks. In the ordinary course, these depositors would have received an emergency dividend payment sometime this week and certificates entitling them to funds from the sales of assets of the bank. If a bank's assets can be sold quickly and for a price that exceeds the deposit liabilities, there might not be any impairment beyond a small delay. So far as can be seen from public disclosures, it is likely that Silicon Valley Bank's depositors would have eventually been made whole—or nearly so.

Where Are the Buyers for Silicon Valley Bank?

As we've seen, however, the banking authorities have not yet succeeded in finding a buyer for the bank or its assets. The auction held over the weekend apparently failed, although the reasons are not known. Charlie Gasparino of Fox Business Network has raised questions about the quality of SVB's loan book. The Wall Street Journal's editorial page said that some regulators were trying to keep the biggest banks from getting even bigger by buying Silicon Valley Bank.

It's more than likely that some of our largest banks have looked back at what happened after 2008 and decided it is not worth the risk of buying a large, failed bank's assets even at fire sale prices. Jamie Dimon, the chief executive and chairman of JPMorgan Chase, has said he regretted buying Bear Stearns and Washington Mutual in 2008 because the liabilities associated with those two banks were responsible for something like 70 percent of the $19 billion in fines, penalties, and buybacks his bank was forced to make.

“We did not anticipate that we would have to pay the penalties we ultimately were required to pay,” Jamie Dimon wrote in a 2015 letter to JPMorgan shareholders. He went on to say that he doubts if his board would allow him to make similar acquisitions given that experience.

Transferring Costs of Risk Management from Venture Capitalists to the Banking System

As a result, many of those with officially uninsured deposits at Silicon Valley Bank may have faced significant delays in recovering their funds. The media reported that many Silicon Valley start-ups were "scrambling" over the weekend to find money to pay their bills. Some companies reportedly had tens of millions or even hundreds of millions of dollars in Silicon Valley Bank. BuzzFeed, for example, reportedly had over $50 million. Roku said it had $487 million on deposit at Silicon Valley Bank.

In Roku's case, this amounted to just 26 percent of the company's cash or cash equivalents. So, it had diversified away some of the risk it faced by exposure to Silicon Valley Bank. Others appear to have put all of their cash in one bank, leaving them vulnerable to potentially being unable to make payments to employees and vendors if their deposits were not immediately released. This is an admission of an abdication of basic risk management and an indictment of both the management of these companies and their venture capital investors.

But turned out to be a good wager on the part of Silicon Valley. The venture capital community was able to avoid paying the costs of managing treasury risk by concentrating deposits in a single institution. When the bank went belly up because those same depositors rushed to withdraw their funds en masse last week, the costs were absorbed by the broader banking system.

Small speculators are loaded for bear

By: Jay Kaeppel | May 17, 2023

• According to our Small Spec Index Position indicator, small speculators in stock index futures have been bearish recently. Whether they are speculating for profit, hedging existing stock positions, or some combination thereof, the implication is clear - "the Little Guy" is betting on a near-term decline. This type of action is typically considered to be a bullish contrarian sign.

Read Full Story »»»

DiscoverGold

DiscoverGold

NASDAQ Outperforming DJIA By Most since 1991

By: Almanac Trader | May 16, 2023

After being the best performing index last year (by declining the least), DJIA’s laggard performance in 2023 continued today. Home Depot’s disappointing forecast earlier today only added further pressure on DJIA. As of today’s close, the 12th trading day of May, DJIA is negative for the year, down 0.41%. NASDAQ, however, is up 17.93% thus far this year. This gives NASDAQ an 18.34% advantage, it’s second biggest lead at this point of the year since 1991 when it was ahead by 18.99%. We would not be surprised to see NASDAQ to continue to lead the way as it still has the rest of May and June remaining in its “Best Eight Months,” November through June.

Read Full Story »»»

DiscoverGold

CNBC Morning news..

1. Looking for action

We might see some real action from stocks Tuesday after a fairly ho-hum session Monday that nonetheless ended with all three major indices slightly higher. There weren’t any meaningful developments out of Washington on the debt ceiling (see below), earnings have slowed to a trickle, and it appears the Federal Reserve is likely going to keep rates in place for a while. The nation’s top banking regulators, including Fed Vice Chair Michael Barr, are set to appear before the House Financial Services Committee on Tuesday, a hearing that could provide further clues on the state of the regional banking sector after recent failures. Fed Presidents Raphael Bostic of Atlanta, John Williams of New York and Austan Goolsbee of Chicago are slated to speak elsewhere Tuesday. Follow live market updates.

2. Debt ceiling update

President Joe Biden might be optimistic about the direction of talks to raise or suspend the debt ceiling, but his Republican foil, House Speaker Kevin McCarthy, doesn’t think things have gotten better since they met last week. While White House and congressional staff have met daily in a bid to hammer out a deal to avoid a debt default, on the surface, at least, it doesn’t look like there’s been much progress ahead of Tuesday afternoon’s planned meeting between Biden, McCarthy, House Minority Leader Hakeem Jeffries, Senate Majority Leader Chuck Schumer and Senate Minority Leader Mitch McConnell. Time is running short. Treasury Secretary Janet Yellen on Monday reaffirmed that the U.S. is on track to run out of money to pay its bills as soon as June 1.

3. Gloomy report from Home Depot

Home Depot’s earnings report is out, and it’s not great. While the bottom line barely beat Wall Street’s expectations, revenue came up short. In fact, it was the home improvement retailer’s second consecutive revenue miss after previously posting 12 consecutive beats. Home Depot also lowered its same-store sales estimate for the year to a decline of 2% to 5%. Before, it had expected the metric to stay effectively flat. The company’s lackluster results and outlook come as the retail stage of earnings season kicks off. Target reports Wednesday, Walmart posts its results Thursday, and Home Depot rival Lowe’s is up a week from now.

4. Musk faces subpoena in Epstein case

The U.S. Virgin Islands has issued a subpoena to billionaire Tesla CEO Elon Musk in its lawsuit against JPMorgan Chase for the bank’s ties to the dead sex trafficker and predator Jeffrey Epstein. Specifically, the USVI government is seeking documents from Musk that show any communication involving him, Epstein and JPMorgan. The islands’ government issued the subpoena out of suspicion that Epstein, who had relationships with rich and powerful men including Bill Gates and Prince Andrew, may have referred Musk to JPMorgan. The USVI has so far failed to serve Musk with the subpoena and is seeking the judge’s OK to to do so through Tesla’s registered agent. Musk, on Twitter, called the subpoena “idiotic on so many levels.” Be sure to tune in to CNBC at 6 p.m. ET tonight, when David Faber will interview Musk live.

5. Russia hammers Kyiv

Ukraine’s capital, Kyiv, faced a massive overnight strike from Russian forces that Ukrainian officials called “exceptional” in its ferocity. The blitz included drone strikes and missiles, starting fires and damaging property through the city. The intense barrage came as Ukraine prepares for a much-anticipated counteroffensive in a bid to drive Russia back from its occupied positions. Additionally, China’s special representative on Eurasian affairs, Li Hui, is slated to visit Ukraine on Tuesday in an attempt to broker a peace deal. The diplomat also plans to visit Poland, France, Germany and Russia. Follow live war updates.

— CNBC’s Mike Calia wrote this newsletter. Brian Evans, Christina Wilkie, Emma Kinery, Melissa Repko, Robert Hum, Dan Mangan and Holly Ellyatt contributed.

Severe Silver Cross Index Negative Divergence a Tip Off to Severe Decline?

By: Erin Swenlin | May 15, 2023

Over the weekend, Carl decided to put together the chart below. We often make comparisons between the SPY and its equal-weight sibling, RSP. By determining divergences between the two ETFs, we can see whether the mega-cap stocks are leading the charge or whether a rally is supported by the rest of the index.

Currently we have rising tops on the SPY, but declining tops on RSP. This alone tells us that market participation is far from broad. The Apples of the world are leading the index. And, at this point, those Apples of the world are barely holding the market together right now as the SPY is looking very toppy.

Now let's add the Silver Cross Index (SCI) which in and of itself is equally weighted. Each stock is looked at to see whether it has a "Silver Cross" or not. A Silver Cross is a 20-day EMA moving above the 50-day EMA. Typically those stocks are intermediate-term bullish.

Notice at the previous price top in February, the SCI was reading at about 80%. On this higher price top, only about 55% were on Silver Crosses. That's roughly a 30% decrease in the reading and sets up a massive negative divergence. RSP is confirming the problem as it has a much lower April price top.

Conclusion: Our question is how is the SPX going to start another bull leg when the rally isn't broad? If the Apples of the world slip, there is no one there to pick up the slack. At this point, we see this as an ominous set up that will likely lead to a severe decline.

Read Full Story »»»

DiscoverGold

Midway through May, DJIA Logs its Second Daily Gain

By: Almanac Trader | May 15, 2023

As of today’s close, May has been trading consistent with it historical seasonal pattern, weak and choppy. DJIA, S&P 500, Russell 1000 and 2000 are all in the red. Today’s modest 0.14% gain by DJIA was just the second daily gain this month and it is now down 2.20% for May. NASAQ is up 1.13% and is the only index with a gain in May. With no progress being made on the debt ceiling, the market is likely to continue to trade sideways. Historical strength over the last four trading days in May is the lone bright spot over the last 21-years.

Read Full Story »»»

DiscoverGold

Home Depot misses revenue expectations, lowers forecast as consumers take on smaller projects

This is a developing news story. Please check back for updates:

https://www.cnbc.com/2023/05/16/home-depot-hd-earnings-q1-2023.html

Bill Ackman's Pershing Square accumulates massive $1.2 billion position in Google

By: Investing.com | May 15, 2023

Shares of Alphabet Inc. (NASDAQ:GOOGL) (NASDAQ:GOOG) gained fractionally after-hours Monday following news that Bill Ackman's Pershing Square Capital hedge fund has amassed a more than 10 million share stake in the mega-cap.

A 13F filing with the SEC after the close of trading showed that Pershing Square now owns 8,069,770 C shares (GOOG) and 2,185,000 (GOOGL) A shares.

The shares were owned as of the quarter ended March 31, 2023. At some point between the end of 2022 and March 31, the fund accumulated the stock.

The value of the position as of Monday's close was nearly $1.2 billion.

Read Full Story »»»

DiscoverGold

SPY Opening OTM sweeper in to 05/19/23 $419 CALLS ~ $365K premium

By: FLOWrensics | May 15, 2023

• $SPY Opening OTM sweeper in to 05/19/23 $419 CALLS ~ $365K premium.

Read Full Story »»»

DiscoverGold

EU approves Microsoft's $69 billion acquisition of Activision Blizzard, clearing major hurdle

This is a developing news story. Please check back for updates:

https://www.cnbc.com/2023/05/15/microsoft-activision-deal-eu-approves-takeover-of-call-of-duty-maker.html

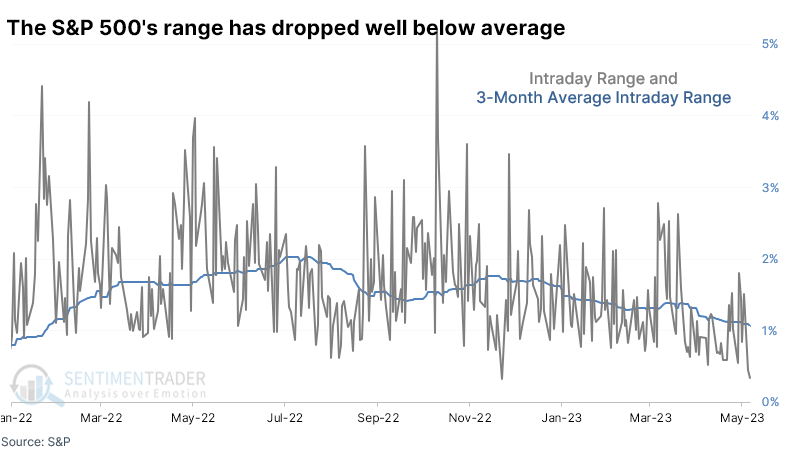

Stocks are swinging by half as much as volatility ebbs

By: Jason Goepfert | May 15, 2023

• Ahead of widely anticipated inflation reports, the S&P 500 barely moved for a couple of days last week. The S&P's intraday range was less than half the 3-month average, and that 3-month average has itself fallen by half. While contrarians consider low volatility to be a negative, historical behavior shows the opposite.

Read Full Story »»»

DiscoverGold

Paul Tudor Jones says the Fed is done raising rates, stocks to finish the year higher from here

Mon, May 15 2023

Yun Li for CNBC

Paul Tudor Jones says the Fed is done raising rates, stocks to finish the year higher from

Billionaire hedge fund manager Paul Tudor Jones believes the Federal Reserve has finished raising interest rates in its fight against inflation, and the stock market could grind higher this year.

“I definitely think they are done,” Jones said Monday on CNBC’s “Squawk Box” of the Fed’s rate-hiking campaign. “They could probably declare victory now because if you look at CPI, it’s been declining 12 straight months. ... That’s never happened before in history.”

The central bank has raised interest rates 10 times since March 2022, taking the fed funds rate to a target range of 5%-5.25%, the highest since August 2007. The consumer price index has cooled considerably since peaking out around 9% in June 2022. The gauge eased to 4.9% in April.

The longtime investor said the market setup right now is similar to mid-2006 before the global financial crisis, where stocks moved higher for over a year after the Fed stopped tightening monetary policy.

“Equity prices ... I think they’re going to continue to go up this year,” Jones said. “I’m not rampantly bullish because I think it’ll be a slow grind.”

For the near term, the investor said there would be some indigestion because of the fight to raise the U.S. debt ceiling, and he would buy the dip on the political volatility.

Jones shot to fame after he predicted and profited from the 1987 stock market crash. He is also the chairman of nonprofit Just Capital, which ranks public U.S. companies based on social and environmental metrics.

He believes that there’s plenty of dry powder that’s ready to be put to work after a particularly dull period for deal-making activities.

“We have no IPOs, no calendar, no secondaries, valuations are at 19 but nobody’s rushing to offer so clearly, something is going on internally in the stock market,” Jones said. “From a flow standpoint, that’s constructive.”

0

CNBC Morning news...

1. Market malaise

The Dow Jones Industrial Average and S&P 500 have fallen for two straight weeks. A flurry of data that will hint at the health of the economy — along with debt ceiling talks in Washington — will help to determine if stocks can break the losing streak. A survey that tracks manufacturing sentiment in New York will hit Monday, followed by retail sales Tuesday and weekly initial jobless claims Thursday. Earnings from Home Depot, Target and Walmart will paint a picture of how consumers are spending. A string of remarks from regional Federal Reserve Bank presidents will also offer a window into whether the central bank plans to suspend interest rate hikes. Follow live market updates.

2. Debt ceiling clock is ticking

The window for the U.S. to avoid a debt default is shrinking. Congress and the White House now have as few as 2½ weeks to break an impasse and avoid a calamity that would upend the economy and jeopardize government benefits. Staff for President Joe Biden and congressional leaders met over the weekend, and the highest-ranking ranking officials in Washington are expected to huddle Tuesday for the second straight week. Biden said Saturday that the talks are “moving along” but have not yet reached a “crunch point.”

3. Retail earnings rush

Retail will dominate the slate of corporate earnings this week. Reports from Home Depot, Target and Walmart on consecutive days will give more clues about how high prices have affected discretionary spending — and how companies are adapting to more cost-conscious consumers. Investors will also watch for hints the companies offer about the health of the economy moving forward. Here’s the earnings schedule this week:

Tuesday: Home Depot (before the bell)

Wednesday: Target (before the bell)

Thursday: Walmart (before the bell)

4. Vice bankruptcy

Vice Media was once valued at $5.7 billion, as a digital upstart that drew attention and money from legacy companies. Vice filed Monday for Chapter 11 bankruptcy protection. The brand is one of a handful of digital outlets that have taken a hit this year as economic concerns mount. A consortium that includes Fortress Investment, Soros Fund Management and Monroe Capital has made a $225 million credit bid for Vice, including $20 million to fund its operations during the sale process.

5. Turkey election could go to runoff

Turkey’s high-stakes presidential election appears headed to a runoff. With nearly all votes counted, neither incumbent President Recep Tayyip Erdogan nor challenger Kemal Kilicdaroglu had secured the 50% of votes needed to win the race outright. Kilicdaroglu has run as a reform candidate after Erdogan increasingly consolidated power during his two decades as the country’s leader. Turkey’s economy has struggled, and Erdogan has come under scrutiny for his skepticism about expanding NATO during Russia’s war in Ukraine.

— CNBC’s Jacob Pramuk wrote this newsletter. Sarah Min, Elliott Smith and Natasha Turak contributed.

Americans are keeping their cars longer >

https://www.cnbc.com/2023/05/15/americans-are-keeping-their-cars-longer-amid-rising-interest-rates.html

Interest Rate-Sensitive Sectors and Big Tech See Positive Money Flows

By: Joe Duarte | May 14, 2023

Interest rate-sensitive and big tech stocks are seeing positive money flows. but the market's breadth is suddenly crashing as bond yields test their recent lows.

You know trading is dull when stock traders talk about the bond market. But that's where the action is these days, other than the Nasdaq 100, which no one pays much attention to anymore. So as the sell in May and go away crowd starts chanting their usual seasonal song, the contrarian in me is slugging more coffee then ever in order to home in on whatever is working, which is limited these days.

On the macro end, even perma-bulls (are there any left?), along with those who don't look at bond charts, can see the economy is slowing. Last week's data was clear enough:

• A slowing rate of rise in CPI

• A similar slowing rate of rise in PPI, with the processed good for intermediate demand component posting a negative growth rate for the year

• Jobless claims hitting the highest level since they bottomed out in September 2022

Moreover, jobless claims rose the most, with California, Massachusetts, Missouri, Texas, and New York. Tennessee and North Carolina, two other sunbelt states, joined Texas, coming in at 15 and 16 on the list. California, Massachusetts, and Texas all have heavy tech company presences.

Watching the Sunbelt

Of course, I'm keeping a close eye on the sunbelt for two reasons. First, the sunbelt's economy has done well over the last few years, as the migration to them has bolstered housing-related industries. Second, this is where the job creation has been of late. Thus, if jobs start to falter in the sunbelt, the odds of a recession will rise.

In Texas, the Austin area has been hit hard as the layoffs in the tech sector have extended there. Even big players like 3M (MMM) are shedding real estate in the city to go along with the phasing out of 500 jobs. MMM's woes are not difficult to understand, as its global strategy and heavy presence in China, where the post-COVID economy is still having some problems, have become its Achilles' heel.

The stock continues to hover near its recent lows and is showing little sign of perking up. All of which adds up to bond traders licking their chops as they see inflation slowing, rising jobless claims, and a Federal Reserve which may be forced to stop its rate hikes, once and for all.

From a trading standpoint, it's useful to keep some money in bonds and related areas of the market. I've recommended several ways to do that on my service. You can have a look with a free trial.

Bonds Holds Near New Yield Lows

The bond market is betting on a slowing economy. And last week's data helped that viewpoint. On the other hand, bond traders aren't fully convinced yet, as the 3.3% yield continues to be the floor on yields for now. A decisive move below 3.3% would likely lead to a further decline in yields.

Certainly, that would be a positive for the bond market, but the weak data that would push yields to those levels would be significant, almost certainly weak enough to strongly suggest a recession.

As I've noted here for several weeks, the long-term relationship between the U.S. Ten Year Note yield (TNX), mortgage rates (MORTGAGE), and the Homebuilder sector (SPHB) remains intact, as the recent fall in yields and mortgage rates has again led to a rise in the homebuilder sector.

For an in-depth comprehensive outlook on the homebuilder sector, click here.

Interest Rate-Sensitive Sectors and Big Tech See Positive Money Flows

Meanwhile, traditional interest rate-sensitive sectors in the stock market are confirming the currently falling bond yields, and are waiting for a break below that key 3.3% yield in TNX.

In addition to the move into interest rate-sensitive areas, you can see selective money into big tech. The Invesco QQQ Trust (QQQ), home to Microsoft (MSFT), Apple (AAPL), and the rest of the big tech posse, is near a major breakout, with investors pricing in layoffs and cost-cutting measures as potential profit boosters for the companies. Moreover, there is the current AI-related buzz that is also fueling interest in the sector.

The traditionally interest rate-sensitive utility sector (XLU) is also answering the bond market's siren call. XLU is trading well off of its lows and is on the verge of a breakout as it tests the key resistance level near $70. This is where the 200-day moving average and a large Volume-by-Price bar (VBP) are hunkered down. A move above this area would be bullish, and would likely happen if TNX breaks below 3.3%.

On Balance Volume (OBV) and Accumulation Distribution (ADI) are both trending higher, confirming the bullish money flow.

NYAD Breaks Down

The New York Stock Exchange Advance=Decline line (NYAD) rolled over at the end of last week with a nasty-looking break below its 50-day moving average. It looks headed for a test of its 200-day moving average. A sustained break below the 200-day line would be very negative for the market.

In contrast, the S&P 500 (SPX) went nowhere. The index has remained in what has become a familiar trading range, between 4100 and 4200 for several weeks as the heavily weighted big-tech stocks, which are also in the Nasdaq 100 index (see below) are holding things up. On Balance Volume (OBV), however, looks to be turning lower, which means sellers are starting to increase in number. Accumulation Distribution (ADI) remain very constructive for SPX as short sellers pare positions.

The Nasdaq 100 Index (NDX) remains in an uptrend. The index closed above 13,400, extending its breakout above 13,200. I'm watching what happens to OBV and ADI in the short term, however. If they both turn lower, this rally may be ending as well.

VIX Holds Steady

The CBOE Volatility Index (VIX) has been stable lately trading well below 20. This is a positive for the markets, as it shows short sellers are staying away.

When VIX rises, stocks tend to fall, as rising put volume is a sign that market makers are selling stock index futures in order to hedge their put sales to the public. A fall in VIX is bullish, as it means less put option buying, and it eventually leads to call buying, which causes market makers to hedge by buying stock index futures. This raises the odds of higher stock prices.

Liquidity Remains Stable Despite Rate Hike

The market's liquidity is moving sideways as the Eurodollar Index (XED) remains below 94.75, but did not make a new low after the Fed's rate hike. That's a positive for now.

A move above 95 will be a bullish development. Usually, a stable or rising XED is very bullish for stocks. On the other hand, in the current environment, it's more of a sign that fear is rising and investors are raising cash.

Read Full Story »»»

DiscoverGold

S&P 500 Index (SPX) »» Weekly Summary Analysis

By: Marty Armstrong | May 13, 2023

S&P 500 Cash Index closed today at 412408 and is trading up about 7.41% for the year from last year's settlement of 383950. Factually, this market has been rising for this month going into May reflecting that this has been only still, a bullish reactionary trend. As we stand right now, this market has made a new low breaking beneath the previous month's low reaching thus far 404828 yet it is trading below last month's close of 416948.

Up to now, we still have only a 1 month reaction rally from the low established during March. We must exceed the 3 month mark in order to imply that a trend is developing.

ECONOMIC CONFIDENCE MODEL CORRELATION

Here in S&P 500 Cash Index, we do find that this particular market has correlated with our Economic Confidence Model in the past. Our next ECM target remains Tue. May 7, 2024. The Last turning point on the ECM cycle low to line up with this market was 2020 and 2009 and 2002. The Last turning point on the ECM cycle high to line up with this market was 2022 and 2007 and 2000.

MARKET OVERVIEW

NEAR-TERM OUTLOOK

The historical perspective in the S&P 500 Cash Index included a rally from 1974 moving into a major high for 2022, the market has pulled back for the current year. The last Yearly Reversal to be elected was a Bullish at the close of 2020 which signaled the rally would continue into 2022. However, the market has been unable to exceed that level intraday since then. This overall rally has been 2 years in the making.

This market remains in a positive position on the weekly to yearly levels of our indicating models. Nevertheless, it closed last year on the weak side down from 2021. Pay attention to the Monthly level for any serious change in long-term trend ahead.

The perspective using the indicating ranges on the Daily level in the S&P 500 Cash Index, this market remains neutral with resistance standing at 412426 and support forming below at 412381. The market is trading closer to the resistance level at this time. An opening above this level in the next session will imply that a bounce is unfolding.

On the weekly level, the last important low was established the week of March 13th at 380886, which was down 6 weeks from the high made back during the week of January 30th. We have been generally trading down to sideways for the past week, which has been a very dramatic move of 2.101% in a stark panic type decline.

Looking at this from a broader perspective, this last rally into the week of May 1st reaching 418692 failed to exceed the previous high of 419544 made back during the week of January 30th. That rally amounted to only seven weeks. Right now, the market is neutral on our weekly Momentum Models warning we have overhead resistance forming and support in the general vacinity of 407255. Additional support is to be found at 380886. Looking at this from a wider perspective, this market has been trading up for the past 6 weeks overall.

INTERMEDIATE-TERM OUTLOOK

YEARLY MOMENTUM MODEL INDICATOR

Our Momentum Models are declining at this time with the previous high made 2021 while the last low formed on 2022. However, this market has rallied in price with the last cyclical high formed on 2022 and thus we have a divergence warning that this market is starting to run out of strength on the upside.

After closing above last year's low of 366271.

Some caution is necessary since the last high 419544 was important given we did obtain one sell signal from that event established during February. That high was still lower than the previous high established at 432528 back during August 2022. Critical support still underlies this market at 372320 and a break of that level on a monthly closing basis would warn of a further decline ahead becomes possible.

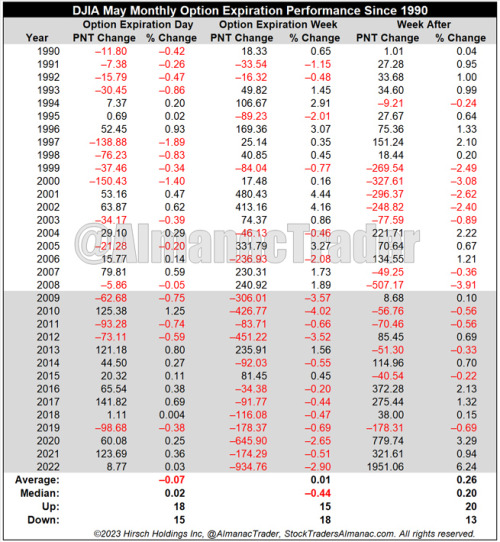

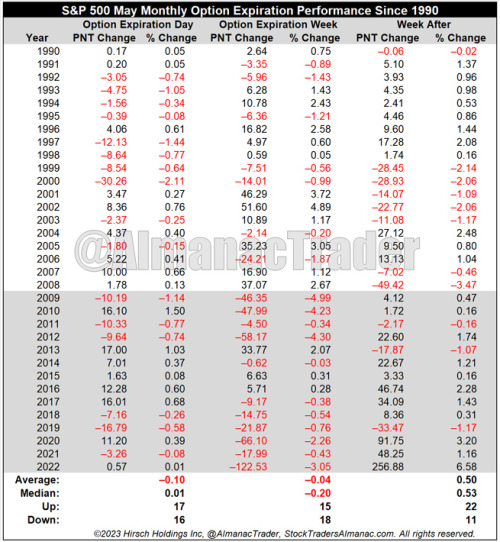

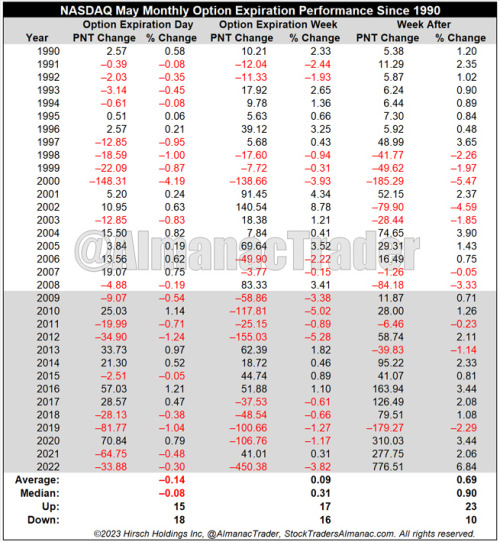

DiscoverGold May Monthly OpEx Week Weak - DJIA Down 12 of Last 14

By: Almanac Trader | May 12, 2023

May’s monthly option expiration has been mixed over the longer-term since 1990. DJIA has been up eighteen of the last thirty-three May monthly expiration days with an average loss of 0.07%. Monthly OpEx week has a slight bearish bias with DJIA and S&P 500 down 18 and up 15.

More recently, DJIA has suffered declines in 12 of the last 14, monthly expiration weeks. S&P 500 has one additional weekly gain since 2009, down 11 of the last 14. NASDAQ has declined in 9 of the last 14. The week after has been best for S&P 500 and NASDAQ.

The week after options expiration is more bullish with S&P and NASDAQ up 11 of 14. Last year DJIA, S&P 500 and NASDAQ all gained over 6% in the week after.

Read Full Story »»»

DiscoverGold

Weekly Market Guide | Markets and Investing

By: Raymond James Financial | May 12, 2023

Market resiliency, albeit on weak participation, remains the theme with recent performance still dominated by mega-cap Technology-oriented and defensive areas. While narrow leadership is not an ideal backdrop for short-term trends, rotation is more positive than broad-based weakness. Fed actions are likely playing into the mixed market signals, as the Committee both tightens (rate hikes) and loosens (supports bank liquidity issues) at the same time. On the one hand, we do not believe that equities are ready for a sustainable climb higher yet. But on the other hand, we believe a mild recession was likely priced in at the October lows. In our opinion, choppiness is the highest probability for short-term trends and we have a range-bound bias for the S&P 500 (potentially between ~3600-4200).

Technically, the S&P 500 is still hung in the same range, as investors wait on inflation, the economy (what sort of damage will be done), and whether there is another shoe to drop. The market grind requires patience for investors, as we may be stuck in this range for a while. Nonetheless, there are plenty of things to do for the active investor. The overall playbook remains to not chase the rallies and buy the pullbacks- and they are out there at the individual stock level. Headwinds leave equities not ready to get back to highs soon- have to let time pass and the data to get out there. In the meantime, we expect back-and-forth economic data, sentiment, and markets. We see this as the process of a market in a waiting game to learn more about the issues at hand, which include:

• Inflation- leading indicators point to inflation coming down, but we need to see it do

• Economy- the lag effect of higher interest rates puts high odds on weakness

• Fed policy- bond market indicating that Fed hikes are done, and the Fed should be lowering rates late this year or early next year as a recession takes place and inflation recedes.

• Debt ceiling- headline volatility can impact markets, but both sides know something has to get done. Our base case is a deal or extension after plenty of political posturing.

We believe the market has likely priced in a mild recession. If more severe, equities will probably move to the October lows (or worse) but it may not do too much damage to long-term investor portfolios. We can make the case for limited losses by the time earnings hit lows, which will be a precursor before the market eventually prints a new high. It is important to keep this bear market in perspective- it is already 16 months long and -27% at the lows (vs. recessionary bear markets -33% over 13 months historically). The bottom line is investors need to exercise patience a bit longer, deal with back-and-forth motion that probably occurs for a while, and pick opportunities to accumulate favored stocks along the way.

Read Full Story »»»

DiscoverGold

Elon Musk hires ex-NBCUniversal ad chief Linda Yaccarino to be Twitter’s CEO

FRI, MAY 12 2023 9:04 AM

Lillian Rizzo for CNBC

KEY POINTS

Former NBCUniversal advertising chief Linda Yaccarino will be Twitter’s next CEO.

Elon Musk, who owns the social media platform, confirmed the hire in a tweet.

Yaccarino resigned from NBCUniversal effective immediately Friday.

In this article

NBCUniversal global advertising chief Linda Yaccarino has resigned to join Twitter as its next chief executive.

Twitter owner Elon Musk confirmed the hire in a tweet Friday.

“I am excited to welcome Linda Yaccarino as the new CEO of Twitter!” Musk tweeted. He said she “will focus primarily on business operations, while I focus on product design & new technology.”

He added: “Looking forward to working with Linda to transform this platform into X, the everything app.”

The announcement comes a day after Musk said via Twitter he would step down from the role and that there would be a new CEO of the social media website, although he didn’t name the new person. Musk said in his tweet the person would start in about six weeks.

Yaccarino joined NBCUniversal in 2011 and had risen to the top of the company’s global advertising business. On Monday, the ad chief was slated to take part in NBCUniversal’s Upfront event at Radio City in New York – the sales presentation the company, along with its media peers, makes to the advertising industry every year in May.

The longtime ad executive brings a wealth of relationships with top chief marketing officers and other advertising executives to Twitter at a time when the platform has seen advertisers flee – therefore losing billions of dollars – after Musk’s takeover last year.

Musk completed his $44 billion acquisition of Twitter in October of last year. Soon after, he fired the company’s top brass and laid off thousands of employees.

Many companies halted their ad spending on the platform since Twitter has seen an increase in offensive speech and rhetoric, as several advocacy groups have documented. In an attempt to make up for the loss of ad revenue, Musk created a new subscription service, Twitter Blue, which offers features such as the ability to compose longer tweets.

Yaccarino and Musk sat together in a keynote interview at a marketing conference in Florida in mid-April. During the conversation, the two discussed the role marketers play in the future of Twitter, as well as its position in the cultural conversation.

During the conference, Musk reportedly tried to reassure advertisers that Twitter was a respectable place for their brands.

Yaccarino’s exit from NBCUniversal comes weeks after Jeff Shell was ousted as the company’s CEO after admitting to an inappropriate relationship with an employee. Rather than replacing Shell, NBCUniversal’s top executives will report to Mike Cavanagh, president of parent company Comcast.

On Friday, NBCUniversal said Yaccarino would leave the company, effective immediately, and Mark Marshall, the current president of advertising sales and client partnerships would become interim chairman of the company’s advertising and partnerships group.

Marshall will report to Mark Lazarus, chairman of NBCUniversal Television and Streaming. Lazarus and Marshall are likely to take part in NBCUniversal’s Upfront presentation on Monday, CNBC’s David Faber and Julia Boorstin reported Friday.

Disclosure: NBCUniversal is the parent company of CNBC.

CNBC Morning news..

1. Looking for a rebound

The Nasdaq is humming along, and it’s on track to post its third consecutive winning week. The Dow and the S&P 500, however, are heading into Friday headed for their second straight week of losses. Investors are chewing over potential signs of an economic slowdown while also contending with the aftermath of the major part of earnings season. (Disney, which posted a middling report Wednesday, was a drag on the Dow Thursday – more below.) Then there’s renewed worry about regional banks, which fell after PacWest reported a sharp decline in deposits. Follow live market updates.

2. A new leader for Twitter

Elon Musk announced Thursday that he would be stepping down as Twitter’s chief executive in about six weeks. He didn’t name his successor publicly, but referred to this person as “she.” CNBC’s Julia Boorstin later confirmed that Twitter was in talks with NBCUniversal advertising chief Linda Yaccarino for the CEO role. While Musk would inevitably retain much control over Twitter – he owns it, and he plans to keep overseeing its product development – Yaccarino, a seasoned operator in the advertising world, could help Twitter beef up its flagging ad business. Tesla investors, man of whom are eager to have Musk spend more time on his EV company. seemed to like the news, sending shares up 2% Thursday and another 1.5% in extended trading.

3. Disney drops

Disney had been riding pretty high in the market since Bob Iger returned as CEO in November. He reorganized the entertainment giant and rolled out a cost-cutting plan that includes 7,000 layoffs, while focusing the company’s content creators on core brands. Then came Wednesday’s after hours earnings report, which, in turn, pushed Disney’s stock down nearly 9% Thursday. Now the shares are up only 6% for the year. While the company’s streaming losses improved, it still showed it had a long way to go before making a profit in that segment. Also, by folding Hulu into the Disney+ app, Iger seemed to acknowledge that Disney might need a bit more than its core, family-friendly content to make its streaming venture work.

4. Debt ceiling meeting delayed

President Joe Biden was set to meet Friday with the big four congressional leaders as they try to hammer out an agreement that would lift the debt ceiling and prevent the United States from defaulting on its debt. The sitdown is delayed until early next week, however, as White House and congressional staff work behind the scenes. The Treasury Department has said the U.S. could run out of cash to pay its bills as soon as June 1 unless Congress raises the debt limit. House Republicans, led by Speaker Kevin McCarthy, have insisted on pairing spending cuts with a debt ceiling increase. Biden has said he will only negotiate spending reductions as part of a separate bill. Treasury Secretary Janet Yellen, meanwhile, is slated to meet with top banking leaders about the matter early next week, as well.

5. The end of the Covid emergency

The United States ended its public health emergency for Covid on Thursday after three years, more than a million deaths, and a bevy of sweeping, still-developing societal and economic changes. Deaths and hospitalizations from the disease have fallen dramatically thanks largely to the vaccines and antiviral medicines on the market. While some worry the end of the emergency will leave the U.S. vulnerable to future Covid surges, others say we’re past the worst of it. Meanwhile, uninsured Americans can still get Covid shots for free, at least for now, CNBC’s Annika Kim Constantino reports.

— CNBC’s Mike Calia wrote this newsletter. Sarah Min, Jonathan Vanian, Julia Boorstin, Noah Sheidlower, Emma Kinery, Spencer Kimball and Annika Kim Constantino contributed.

Money managers Reduced their exposure to the US Equity markets since last week...

DiscoverGold

NAAIM Exposure Index

May 2, 2023

The NAAIM Number

65.22

Last Quarter Average

63.74

»»» Read More…

US Equity Fund Outflows -$3.7 Billion; Taxable Bond Fund Inflows $726 Million

By: Refinitiv | May 11, 2023

• FUND FLOW REPORTS FOR THE WEEK ENDED 05/10 ARE NOW AVAILABLE.

For the week ended 05/10/2023 ExETFs - All Equity funds report net outflows totaling -$6.219 billion, with Domestic Equity funds reporting net outflows of -$5.639 billion and Non-Domestic Equity funds reporting net outflows of -$0.581 billion...ExETFs - Emerging Markets Equity funds report net inflows of $0.049 billion...Net inflows are reported for All Taxable Bond funds of $0.726 billion, bringing the rate of outflows for the $3.583 trillion sector to -$0.101 billion/week...International & Global Debt funds posted net outflows of -$0.559 billion...Net inflows of $1.428 billion were reported for Corp-Investment Grade funds while High Yield funds reported net outflows of -$1.202 billion...Money Market funds reported net inflows of $16.405 billion...ExETFs - Municipal Bond funds report net outflows of -$0.249 billion.

Read Full Story »»»

DiscoverGold

NBCUniversal ad chief Linda Yaccarino in talks to >

succeed Elon Musk as Twitter CEO ..

https://www.cnbc.com/2023/05/11/elon-musk-says-hes-stepping-down-as-twitter-ceo-will-oversee-product.html

TSN (link back) is in recovery mode today.

Classic 3 down days.

https://stockcharts.com/h-sc/ui?s=TSN

Quote as of 5/11/2023 10:36AM ET

$48.648 +$1.368 (+2.893%)

Volume

1,801,396

90 Day Avg. Vol.

3,388,727

Day Range

Low$47.48

High$48.66

CNBC Morning news

1. More muddling

Wednesday was another mixed day for stocks. The Dow closed slightly down, while the Nasdaq and the S&P 500 finished a little higher as investors chewed over April’s consumer price index. That data showed inflation is indeed slowing down, but at the expected pace, which means we’re like a ways off from the Federal Reserve cutting rates after hiking them 10 times since last year. On Thursday, markets will process April’s producer price index, which measures inflation at the wholesale level. Economists surveyed by Dow Jones estimate that it rose 0.3% month to month. Follow live market updates.

2. The new frontier

Investors didn’t care for what they saw out of Disney earnings Wednesday, sending the stock down more than 5% in off-hours trading. The company’s streaming operations posted a loss, albeit a smaller one than expected, as Disney pushes to make that business profitable. Disney+ actually lost subscribers during the most recent quarter, but revenue per user was higher thanks in large part to recent price increases. Taking all of that together, along with other media companies’ recent results, it’s clear the streaming wars are over, at least in the sense of a growth narrative, according to CNBC’s Alex Sherman. That means the industry needs to look elsewhere for growth – and gaming might be the way.

3. 'Unthinkable'

Treasury Secretary Janet Yellen is in Japan for meetings with fellow finance ministers from G-7 countries, but the debt ceiling remains front and center for her given that the United States’ credibility in global markets is at stake. Yellen again warned of economic catastrophe if Congress fails to address the debt limit. “The notion of defaulting on our debt is something that would so badly undermine the U.S. and global economy that I think it should be regarded by everyone as unthinkable,” she said. “America should never default.” Yellen said this in response to a question about leading GOP presidential contender Donald Trump urging Republicans to let the U.S. default if Democrats don’t agree to sweeping spending cuts in exchange for raising the debt limit.

4. Microsoft pauses pay hikes

Microsoft is putting pay raises on hold for salaried employees as the tech giant continues its cost-cutting efforts. The move comes after Microsoft said earlier this year it would cut nearly 5% of its workforce. Last year, the company beefed up its budget for merit pay increases and stock awards as inflation surged. “We will maintain our bonus and stock award budget again this year, however, we will not overfund to the extent we did last year, bringing it closer to our historical averages,” CEO Satya Nadella said in an email to employees. Performance bonuses for executives will also come down significantly, he said. Big tech companies in general are trimming costs and jobs after a year of share price declines that followed a period of rapid growth during the earlier days of the pandemic.

5. Showing cracks

The division between the pro-Russia mercenary Wagner Group and Russia’s defense ministry has grown more severe in recent days. Wagner’s leader has threatened to pull out of the protracted fight for Ukraine’s Bakhmut due to a lack of supplies. Russian forces, likewise, have pulled back somewhat in that fight, as Ukrainian fighters reclaim ground. All of this comes as Ukraine is expected to launch a new counteroffensive backed by western money and weaponry. Russia, meanwhile, is accelerating its efforts to recruit prisoners to fight. Follow live war updates.

— CNBC’s Mike Calia wrote this newsletter. Hakyung Kim, Sarah Whitten, Alex Sherman, Jihye Lee, Jordan Novet and Holly Ellyatt contributed.

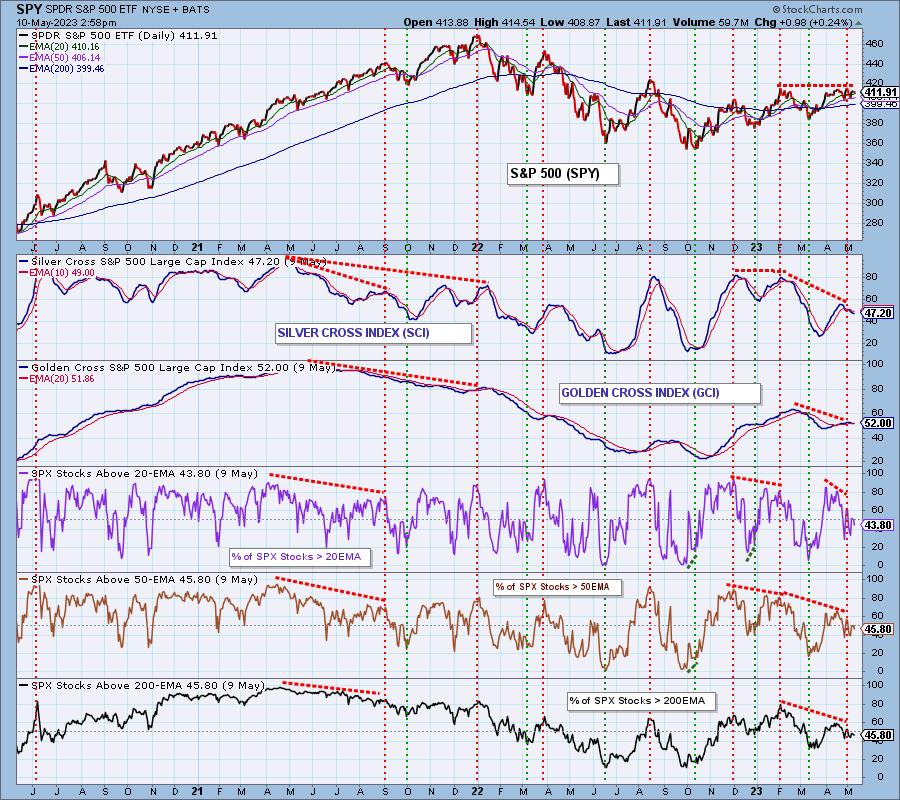

Market Participation Is Dismal

By: Carl Swenlin | May 10, 2023

When we talk about "participation," we are referring to the number of stocks actually taking part in a given market move. Presently, we are looking at the rally from the October lows and the indicators we use to assess it. First, we have our Silver Cross Index (SCI), which shows the percentage of stocks in the S&P 500 that have their 20-day EMA above their 50-day EMA. This configuration is an intermediate-term BUY Signal, and we can see that the SCI currently reads 47 percent. Note that the SCI reading at the February price top was about 80 percent, so we have a double price top with a severe SCI negative divergence.

We have a similar situation with the Golden Cross Index (GCI), which shows the percent of stocks with the 50-day EMA above the 200-day EMA, a long-term BUY Signal. At 52 percent, it reads a bit higher than the SCI, but it is a slower moving indicator. Nevertheless, it too has negative divergence against the two price tops.

The remaining three panels show the percent of stocks in the index with price above their 20-, 50-, and 200-day EMAs. They are all reading in the 40 percent range, and are all displaying negative divergences. All this evidence tells us that participation is narrowing with fewer stocks supporting the price advance.

Conclusion: Last Friday's rally fueled hopes that the rally from the October lows would be continuing, but fading participation shows severe erosion of the technical foundation, and a rally continuation seems highly unlikely.

Read Full Story »»»

DiscoverGold

Trump urges GOP to let catastrophic debt default happen >

Trump urges GOP to let catastrophic debt default happen if Dems don’t accept cuts ...

https://www.cnbc.com/2023/05/11/trump-endorses-debt-ceiling-default.html

SoftBank posts record $32 billion loss at its Vision Fund tech investment arm

This is a developing news story. Please check back for updates:

https://www.cnbc.com/2023/05/11/softbank-full-year-2022-earnings-vision-fund-posts-32-billion-loss.html

Contagion worries return

Stock market update: May 5, 2023

Fidelity Viewpoints

Market sentiment was clouded last week by fresh fears of an imminent banking crisis. Here's a look at what happened, and what to expect in the coming week.

WHAT HAPPENED LAST WEEK

On Monday, the FDIC seized First Republic Bank (FRC), an event that marked the second-largest bank failure in US history. Just one week before, the bank disclosed that customers had withdrawn $100 billion following the panic over Silicon Valley Bank's collapse in March. The seizure added to growing worries that the banking sector could be in trouble. On Wednesday, PacWest Bancorp (PACW) noted that it's currently exploring options to reinforce its finances, including the potential of a sale. The stock closed the week down 43%. A positive-leaning Apple (AAPL) earnings report helped the market bounce on Friday, but it remains to be seen whether the bounce will hold. Health care, utilities, and consumer staples were the best-performing sectors, while energy, financials, and comm services were the worst-performing sectors.

Last week Year-to-date 5-year

S&P 500 –0.8% 7.7% 52.9%

Dow Jones –1.3% 1.6% 38.4%

Nasdaq 0.07% 16.9% 64.0%

Oil (WTI crude) –5.3% –4.5% 2.1%

Gold (New York) 0.8% 10.6% 53.9%

Bitcoin 1.0%

77.8%

216.8%

Source: Fidelity.com, CNBC, as of May 5, 2023.

KEY THINGS TO WATCH THIS WEEK

Another busy week for earnings is on deck, featuring a mix of biotech, pharma, and former growth stocks. Investors will watch to see if any good news can help buoy the market.

Riot Platforms (RIOT) CPI – Wednesday

Rivian Automotive (

RIVN) EIA Petroleum Status Report – Wednesday

Airbnb (ABNB) Jobless claims – Thursday

GrowGeneration (GRWG) PPI final demand – Thursday

Fiverr International (

FVRR) Fed balance sheet – Thursday

Electronic Arts (EA) Consumer sentiment – Friday

See the full earnings calendar (login required). See the full economic calendar.

Source: Fidelity.com, as of May 5, 2023.

Orders by Fidelity customers

Rank is based on the total of buy and sell orders for the security.

Information shown below in the table is based on the aggregate number of orders entered by Fidelity Brokerage Services LLC self-directed retail customers “as of” the date and time shown.

As of May-10-2023 12:12 PM ET

Symbol % Change # Buy orders Buy/sell ratio # Sell orders Sector

TSLA -0.06% 7,520

Buy 50.12%

Sell 49.88%

7,484 Consumer Discretionary

SQQQ -1.90% 4,206

Buy 52.58%

Sell 47.42%

3,793

TQQQ +1.94% 3,977

Buy 50.11%

Sell 49.89%

3,960

ABNB -9.53% 4,879

Buy 66.5%

Sell 33.5%

2,458 Consumer Discretionary

AMD +4.27% 3,149

Buy 44.93%

Sell 55.07%

3,859 Information Technology

SOXL +3.41% 2,661

Buy 49.41%

Sell 50.59%

2,725

AMZN +2.83% 2,069

Buy 41.36%

Sell 58.64%

2,934 Consumer Discretionary

NVDA +1.14% 2,273

Buy 47.37%

Sell 52.63%

2,525 Information Technology

PYPL -3.77% 3,515

Buy 74.57%

Sell 25.43%

1,199 Financials

UPST +32.97% 1,909

Buy 42.9%

Sell 57.1%

2,541 Financials

PLTR +3.66% 1,772

Buy 46.35%

Sell 53.65%

2,051 Information Technology

RIVN +4.62% 1,817

Buy 47.77%

Sell 52.23%

1,987 Consumer Discretionary

AAPL +0.78% 1,829

Buy 51.83%

Sell 48.17%

1,700 Information Technology

TWLO -15.86% 2,112

Buy 74.39%

Sell 25.61%

727 Information Technology

SPY +0.01% 1,390

Buy 53.88%

Sell 46.12%

1,190

MSFT +1.27% 1,049

Buy 40.94%

Sell 59.06%

1,513 Information Technology

QQQ +0.64% 1,148

Buy 48.85%

Sell 51.15%

1,202

STSS +22.25% 1,074

Buy 46.11%

Sell 53.89%

1,255 Health Care

HCDI +136.64% 1,111

Buy 48.33%

Sell 51.67%

1,188 Consumer Discretionary

SOXS -3.62% 1,235

Buy 54.45%

Sell 45.55%

1,033

TNA +0.51% 1,104

Buy 53.99%

Sell 46.01%

941

GOOGL +1.45% 999

Buy 53.03%

Sell 46.97%

885 Communication Services

OXY -3.70% 1,386

Buy 76.41%

Sell 23.59%

428 Energy

META -0.16% 893

Buy 50.88%

Sell 49.12%

862 Communication Services

UVXY -1.36% 991

Buy 57.15%

Sell 42.85%

743

CVNA +12.15% 791

Buy 46.2%

Sell 53.8%

921 Consumer Discretionary

MVST +84.73% 735

Buy 44.2%

Sell 55.8%

928 Industrials

BAC -1.14% 1,015

Buy 61.4%

Sell 38.6%

638 Financials

BBBYQ +2.82% 1,434

Buy 90.36%

Sell 9.64%

153 Consumer Discretionary

UPRO -0.03% 807

Buy 53.23%

Sell 46.77%

709

OXY Occidental Petroleum: Will Buffet Buy More?

Wednesday, May 10, 2023 by Thomas Hughes for MarketWatch

https://stockcharts.com/h-sc/ui?s=OXY

Warren Buffet has said he and Berkshire Hathaway would not take a controlling interest in Occidental Petroleum (NYSE: OXY), and that’s smart. Oxy has a capable CEO who has the company on the right track. That is evidenced by Buffet’s remarks, specifically his comments about preferred stock.

Oxy began redeeming Berkshire’s preferred stock holdings, reducing its income payments, but the move is good for the company. Reducing its debt load and freeing up the capital structure and cash flow is the right thing to do and one that will generate more value for Buffet and his Oxy shares down the road.

"In the first quarter of 2023, our shareholder return framework reached a significant milestone as we began redeeming the preferred equity, further advancing the transfer of enterprise value to our common shareholders,” said President and Chief Executive Officer Vicki Hollub.

So, no controlling interest, but that means more than 50%. Berkshire owns about 23% of the stock now and is approved to buy up to 50%, so it could purchase another 27% of the company and leave Mr. Buffet true to his word. Will he do it? Berkshire last bought Oxy in March when share prices fell below $60. He and they bought the stock several times below $60 with a low of $56.70 on March 15th. That marked the bottom for the price action, and the price action in Oxy shares is back to that level. If Mr. Buffet and his crew at Berkshire were going to up their stake, now is the time they’d do it.

Occidental Falls On Weak Results

Occidental had a relatively good quarter, but the revenue and earnings fell short of expectations and are weighing on the market. The company reported $7.26 billion in net revenue, a decline of 14.9% driven by the decline in oil prices. This is 150 basis points short of the consensus, and there was weakness on the bottom line. Oil & Gas was the worst-performing sector due primarily to lower oil prices. The OxyChem segment was flattish compared to last year, and midstream saw gains.

CNBC Morning news

1. Where do we go from here?

Markets haven’t had much of a direction this week as investors prepare to parse the latest inflation reports from the government. The consumer price index for April is due out Wednesday morning. Wall Street expects a 0.4% increase in prices month over month, and 5% year over year. The Federal Reserve has been trying to cram down the pace of inflation with a steady regimen of interest rate hikes. But while the Fed’s policymakers have signaled they are likely to pause the increases, we’re still a far way off from rate cuts. So it’s unlikely the CPI report, or Thursday’s producer price index, will change the Fed’s thinking. Follow live market updates.

2. Push it to the limit

The big meeting between President Joe Biden and the four main leaders in Congress didn’t yield any progress on the debt ceiling, which, going by the Treasury Department’s calculations, is rapidly approaching. Still, the sides plan to meet again Friday, which indicates the gears are at least turning. Republicans, led by House Speaker Kevin McCarthy, have said they would only address the debt limit if there are spending cuts attached. Biden has refused to negotiate over the debt ceiling itself and would rather negotiate over spending as a separate issue. Even with the United States’ credit and reputation on the line, markets haven’t reacted all that much to the brewing crisis. We’ll see whether that changes if we go a few more days without a deal.

3. Disney on deck

It’s been a busy week for earnings, but Disney is the biggest dog on the block this time around. The entertainment and media giant is slated to report its quarterly results after the closing bell Wednesday. Analysts polled by Refinitiv expect Disney to report per share earnings of 93 cents and revenue of $21.79 billion. Investors will be paying close attention to what the company says about the next stage of CEO Bob Iger’s restructuring plan. Disney has said it plans to wrap up its third round of job cuts by summer. Disney watchers will also be looking out for any updates on the company’s battle with Florida Gov. Ron DeSantis over the special district that governs Walt Disney World.

4. Decent report for Rivian

Electric vehicle maker Rivian’s stock jumped in off-hours trading after the company posted a narrower-than-expected quarterly loss after the close Tuesday. The company, known mainly for its R1 pickups and SUVs, also said it is on track to meet its production outlook of 50,000 vehicles this year, which would about double what it produced last year. It also intends to continue its focus on keeping costs in check. “Our core priorities for 2023 are unchanged,” CEO RJ Scaringe said in Rivian’s earnings release. “The team remains focused on ramping production, driving cost reductions, developing the R2 platform and future technologies and delivering an outstanding end-to-end customer experience.”

5. Not worth conveying

— CNBC’s Mike Calia wrote this newsletter. Samantha Subin, Christina Wilkie, Emma Kinery, John Rosevear and Dan Mangan contributed.

ECONOMY Inflation rate eases to 4.9% in April, less than expectations

MAY 10 2023

by Jeff Cox for CNBC

Key Points

The consumer price index rose 0.4% last month, pushed higher by rising shelter, used vehicle and gas prices. The increase was in line with Wall Street expectations.

On an annual basis, the inflation rate was 4.9%, slightly less than the estimate and providing some hope that the trend is lower.

For workers, real average hourly earnings, adjusted for inflation, rose 0.1% for the month but were still down 0.5% from a year ago.

Inflation rose 4.9% in April from a year ago, less than expectations

A widely followed measure of inflation rose in April, though the pace of the annual increase provided some hope that the cost of living will head lower later this year.

The consumer price index, which measures the cost of a broad swath of goods and services, increased 0.4% for the month, in line with the Dow Jones estimate, according to a Labor Department report Wednesday.

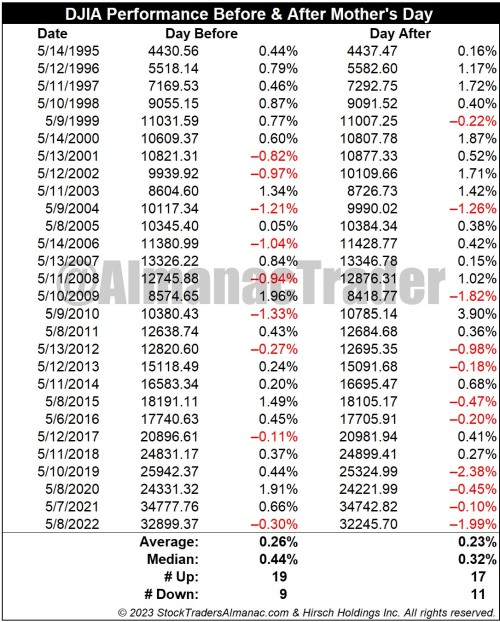

Stocks Love Day Before Mother’s Day Better

By: Almanac Trader | May 9, 2023

With just a few days until Mother’s Day, this is also a reminder. Always used to plant flowers with mom and pick the fresh blooming lilacs. Over the last 28 years on the Friday before Mother’s Day Dow has gained ground 19 times. On Monday after, DJIA has advanced 17 times. Average gain on Friday has been 0.26% and 0.23% on Monday. However, Monday following Mother’s Day has been down 8 of the last 11 years. In 2019, DJIA suffered its worst post Mother’s Day loss going back to 1995, off 2.38%.

Read Full Story »»»

DiscoverGold

This is a great link.

Breitbart Business Digest

by John Carney - Breitbart Economics Editor

and Alex Marlow - Breitbart Editor-In-Chief

March 27, 2023

Why Silicon Valley Bank Was Exposed to Monetary Policy Changes from the Fed

The run on Silicon Valley Bank was triggered by depositor concerns over losses the bank had suffered due to rising interest rates. Which raises the question: why was the bank so exposed to interest rate risk?

Silicon Valley Bank was flooded with deposits during the pandemic and the initial phases of the recovery when its tech industry clients prospered and venture capitalists poured money into startups, creating new clients for the bank. It bought lots of U.S. Treasuries and government-backed mortgage bonds, securities that are considered safe assets because there is essentially no risk of default. As a result, the bank's deposits and assets roughly doubled in 2021.

When interest rates rise, however, the fixed interest payments on these securities do not keep up with the prevailing rate. An older government bond that pays two percent drops in value when the latest bonds pay twice that. The price of the older bond falls enough so that the yield more or less equals the yield on the newer bond.

This does not necessarily mean that the bank actually loses money on those bonds. If the bank holds the bonds until maturity, the bonds will pay off exactly as the bank expected when they purchased them. This is why they are considered "safe assets." In fact, banks are allowed to declare that bonds they buy are going to be "held-to-maturity," which means they do not have to mark them to market prices and can go on reporting them as being worth their face value on their balance sheet and for the purposes of regulatory capital.

The rules do not let banks entirely conceal these mark-to-market losses. Somewhere in the financial statements, usually in a footnote or appendix, banks are required to explain the difference between the market value of their bond holdings and the value listed on their balance sheet.

What's more, if a bank ever sells any of the bonds that it has declared as "held-to-maturity," all of the rest of its holdings get disqualified from this treatment. Which means they all have to be marked to the market value, potentially triggering a huge accounting loss. To avoid doing this, banks also hold bonds that they do mark-to-market, labeled "available for sale." These can be sold without disqualifying other bonds from being treated as held-to-maturity.

Even the unrealized losses on those available-for-sale bonds do not hurt a bank's net income. They get tracked under a balance sheet line called “accumulated other comprehensive income.” It's only when a bond is actually sold at a loss that it hits the bank's income.

Silicon Valley Investors and Depositors' Panic

A week or so before it collapsed, Silicon Valley disclosed that it had sold some investments at a $1.8 billion after-tax loss and would seek to raise $2.25 billion in new capital by selling common and preferred stock. The price of the banks shares plunged by 60 percent. Investors and customers began to pay attention to the fact that the bank was sitting on $17 billion of unrealized losses. Spooked investors began pulling deposits, attempting to withdraw as much as $42 billion in a single day, cratering the bank.

Of course, Silicon Valley Bank is not alone in sitting on a mountain of unrealized losses. The Federal Deposit Insurance Corporation (FDIC) said in February that across the U.S. banking system, unrealized losses on available-for-sale and held-to-maturity securities totaled $620 billion as of December 31. A year earlier, before the Fed began hiking rates, unrealized losses were just $8 billion.

So, why were banks so exposed to the risk of rising rates? One unsatisfactory answer is that banks were just caught off guard by the speed of interest rate hikes. While it is true that banks probably were caught off guard—so was the Fed itself—this does not really answer the question of why banks were taking interest rate risk in the first place. Why did banks leave themselves vulnerable to a change in monetary policy?

Bond Portfolios as a Hedge

Fortunately, there happens to be a paper published in the American Economic Journal: Macroeconomics that takes this question head-on. It is titled "Why Are Banks Exposed to Monetary Policy" and is authored by Sebastian Di Tella of Stanford University and Pablo Kurlat of the University of Southern California. It was published in October 2021 but was circulating as a working paper for a few years before that.

Di Tella and Kurlat argue that banks take interest rate risk as a hedging strategy. When prevailing interest rates are very low—as they have been in recent years—banks earn very little income from deposits. When rates rise, banks do not pass on all of the benefit of higher rates to depositors. Especially in the beginning, banks raise the rates they charge on loans but keep deposits rates low. Even when deposit rates start to climb, banks still earn a larger spread from higher rates. In an interview, Kurlat estimated that banks keep about two-thirds of the benefit of higher rates and depositors get only one-third.

How do banks get away with this? Why don't depositors just instantly move deposits to higher-interest mutual funds that own U.S. Treasuries and other safe assets? This is a bit of a mystery that the economics profession is still trying to work out, Kurlat told us. Most likely, it is a combination of complacency and convenience. Banks offer lots of services—like ATM cards, direct bill payments, and direct deposits—that a money market mutual fund typically does not. And trying to figure out whether it makes sense to move money out of the bank takes some work that might not be worthwhile for bank customers without all that much money in the bank.

As a result, the basic business of taking deposits and making loans is itself exposed to interest rate risk. If rates fall, the deposit side becomes less profitable. If rates rise, it becomes more profitable.

The bond portfolio is a natural hedge against this. If rates fall, the bond portfolio gains while the other part of the business declines. If rates rise, basic banking business becomes more profitable, and the bond portfolio loses value. So, Di Tella and Kurlat's paper argues that banks intentionally expose themselves to interest rate risk as a hedge against the interest rate sensitivity of the deposit business.

"The trick is to find the right amount of risk that does the job of hedging for the other business," Kurlat explained. He said that for the typical bank, around a four-year mismatch between deposits and liabilities is probably the right level of hedging.

Silicon Valley, however, might have needed to be more conservative than most in this because of the unusual nature of its deposit funding. Its depositors were unusually wealthy and held incredibly large deposits at the bank. If you have $1 million in the bank, earning four hundred extra basis points on your savings is more likely to prompt you to relocate your funds. If you have $100 million, well, then we're talking serious money. Trying to keep deposit rates low just will not work.

A bright side for consumers may be that a broad range of banks may now be compelled to raise rates to stem deposit outflows. On the downside for banks and their investors, this will diminish bank profits.

Earnings pick a Ticker or a Date:

By: Chichi2 | May 9, 2023

• You can change the date or pick a ticker on most of these.

One may not have your Ticker Info, another may.

CHOOSE Your Info Gatherer BELOW

http://biz.yahoo.com/research/earncal/today.html

http://www.earningswhispers.com/?advert=g4cal&gclid=COr-mNP1m7QCFQ2znQodqWgAbw

http://www.thestreet.com/event-calendar/index.html

http://www.nasdaq.com/earnings/earnings-calendar.aspx

DiscoverGold

CNBC Morning news

1. Slow going

Stocks got off to a muddled start this week, with the S&P 500 and Nasdaq finishing a smidge higher Monday and the Dow ending the day slightly down. Investors will have a lot to chew over Tuesday, between speeches from Fed Governor Philip Jefferson and New York Fed President John Williams, the latest spate of earnings, and debt ceiling developments out of Washington. Two big inflation data points will come later, with the latest consumer price index set for release Wednesday and the producer price index slated for Thursday. Follow live market updates.

Just in: ChatGPT developer OpenAI leads CNBC's Disruptor 50 list for 2023

2. Another batch of earnings

There are several notable names on the earnings schedule for Tuesday, and from a mix of industries, at that. Before the bell, investors will hear from Fox Corp., which may further address its defamation settlement with Dominion Voting Systems and potentially its ongoing battle with another voting tech company, Smartmatic. Electric truck maker Nikola is also on tap Tuesday morning. After the close, we’ll hear from Airbnb as well as EV company Rivian and a couple of space names, Virgin Galactic and Rocket Lab.

3. Biden and the 'big four'

The battle over the debt limit enters a new stage Tuesday as leaders in Washington work to avoid the first sovereign debt default in U.S. history and the ensuing “financial chaos,” to use Treasury Secretary Janet Yellen’s words. President Joe Biden is scheduled to meet with the top four lawmakers in Congress: Senate Majority Leader Chuck Schumer and House Minority Leader Hakeem Jeffries, both New York Democrats; and House Speaker Kevin McCarthy, R-Calif., and Senate Minority Leader Mitch McConnell, R-Ky. Biden is expected to stick to his stance that the debt ceiling should be raised cleanly, without any corresponding spending cuts. The president, however, is open to discussing Republicans’ push for spending cuts as a separate matter. The Treasury Department has warned the U.S. could run out of money to pay its bills as soon as June 1.

4. Saudi Aramco profit slides

Aramco, Saudi Arabia’s state-owned oil giant, posted a 19% decline in first quarter earnings from a year ago. The decline reflects a drop in prices as the global economy reacts to high inflation and the potential for a slowdown. Still, Aramco’s profit beat lower expectations, coming in at $31.9 billion vs. an estimated $30.5 billion. The company, which is the world’s largest oil exporter, is coming off a blockbuster 2022, when it posted a profit gain of more than 46%. Aramco aims to proceed with its plans to expand capacity, and its “long-term outlook remains unchanged,” CEO Amin Nasser said.

5. Not-so-super Nintendo

These days, the big money Nintendo action isn’t at home. It’s at movie theaters, where “The Super Mario Bros. Movie” has dominated with more than $1.1 billion in global grosses. (Disclosure: The movie was produced by Universal Pictures, CNBC’s fellow NBCUniversal subsidiary.) Nintendo itself, however, has hit a rough patch for its Switch consoles. The Japanese company sold nearly 18 million of the gadgets during the fiscal year that ended in March, just a touch below estimates and 22% lower than during the previous year. And it doesn’t look like the “Mario” movie is going to give Switch sales the power-up they need. Nintendo said it expects to sell 15 million of the consoles during the current fiscal year.

— CNBC’s Mike Calia wrote this newsletter. Alex Harring, Emma Kinery, Christina Wilkie, Natasha Turak and Arjun Kharpal contributed.

0

CNBC Morning news

1. Markets look to rebound

U.S. stock indexes are coming off their worst week since March. A regional bank stock rebound and strong Apple earnings boosted the market Friday, and April jobs data came in better than expected despite recession concerns. This week, the focus will turn to monthly inflation data after the Federal Reserve hiked interest rates again to try to cool off stubbornly high prices. The consumer price index will come Wednesday, while the producer price index is due Thursday. Inflation has started to ease, and the central bank has signaled it may pause rate increases amid concerns about an economic slowdown and the health of the banking system. Follow live market updates.

2. Buffett dishes

Warren Buffett and his right-hand man Charlie Munger weighed in on everything from regional banks to artificial intelligence during Berkshire Hathaway’s annual shareholders meeting Saturday. While Buffett said banks may not be out of the woods yet, he said he believes deposits are safe. The Oracle of Omaha said he has also seen slowing activity at some of Berkshire’s businesses. The conglomerate does not plan to take full control of oil giant Occidental Petroleum, Buffett said.

3. Debt ceiling drama

The coming days could prove pivotal for efforts in Washington to raise the debt ceiling and prevent a first-ever default on U.S. sovereign debt. President Joe Biden will meet Tuesday with the top four congressional leaders as lawmakers try to break a stalemate over how to increase the borrowing limit. Treasury Secretary Janet Yellen warned Sunday that a “steep economic downturn” would follow if Congress fails to act in the next few weeks. The Treasury Department has estimated the U.S. could run out of money to pay its bills as soon as early June.

4. Regionals rise

Regional bank stocks appeared poised to climb for a second straight day Monday, after the failure of First Republic sent their shares plunging early last week. The third failure of a regional bank since March put more scrutiny on the sector — and names like PacWest Bancorp in particular. Shares of the lender spiked in premarket trading Monday, after PacWest announced Friday evening that it would slash its dividend. The bank’s rise helped to fuel a broader rally in the sector, as the SPDR S&P Regional Banking ETF advanced in premarket trading.

5. Disney on deck

Walt Disney will headline the quarterly earnings slate expected this week. Other results will shine a light on the health of the consumer. Here are some of the reports expected this week:

Tuesday: Fox, Nikola (before the bell); Airbnb, Rivian (after the bell)

Wednesday: Roblox (before the bell); Disney (after the bell)

— CNBC’s Jacob Pramuk wrote this newsletter. Samantha Subin, Jeff Cox, Yun Li, Sarah Min, Tanaya Macheel, Alex Harring, Hakyung Kim, Christina Cheddar-Berk and Ashley Capoot contributed.

US Futures Tick Up Ahead Of Earnings

By: Barchart | May 8, 2023

Wall Street pointed higher early Monday as markets gear up for another busy week of earnings and two inflation reports from the U.S. government, all while monitoring the regional banking crisis.

Futures for the Dow Jones Industrial Average and futures for the S&P 500 each rose about 0.2% before the bell.

Companies this earnings season have largely reported better-than-expected results, injecting some optimism into what's been mostly gloomy economic outlook. Stubborn inflation, the war in Ukraine and the recent collapse of three regional banks have combined to paint a grim economic forecast, with many experts expecting a recession late this year or early next year.

Shares in PacWest Bancorp surged about 35% in premarket trading Monday, following Friday's gain of more than 80%. PacWest shares lost nearly half their value last week before Friday's turnaround as anxiety persists over the stability of smaller banks amid the Federal Reserve's cranking up of interest rates. Shares of Western Alliance, which also got pummeled last week, rose more than 15% before the bell.

PacWest share are still about 75% lower than they were before the bank collapses began in mid-March. Western Alliance shares are off about 64% in the same period.

Meat producer Tyson Foods, owner of the Jimmy Dean and Ball Park brands, posted its first quarterly loss since the Great Recession and its shares tumbled more than 9% in premarket trading Monday.

Also this week, PayPal, Under Armour, Rivian, Wendy's and The Walt Disney Co. are among the slew companies scheduled to report quarterly results.

On Wednesday, the government releases its monthly report on consumer inflation, followed Thursday by its report on inflation at the wholesale level. Both reports are closely monitored by analysts and investors, but more importantly by the Federal Reserve, which has been raising interest rates for more than a year to combat four-decade-high inflation.

A report Friday showed hiring accelerated across the economy by much more than expected last month. The government’s jobs report also showed workers won bigger pay raises than expected.