News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

MG, Thank you for your dedication and support. A person like who always stood behind the team in good as well as the hard times, you’re an irreplaceable asset to our team.

Thank you so much for all these years excellent work!

DiscoverGold

DiscoverGold

Apple $2.4 Million Call • Strike: 215 • Expiration: 01/19/24

By: Cheddar Flow | June 20, 2023

• $AAPL $2.4M OTM Call

Strike: 215

Expiration: 01/19/24

Read Full Story »»»

DiscoverGold

I see that DiscoverGold is nearing Abet's Chichi2's total posts and that is a signal for me to respectfully bow out now and make way for DG to take the board home.

Later on, readers can track DG, SkeBallLarry and myself to find us posting similar stock info elsewhere.

It has been a pleasure and honor to be part of this board, founded and sustained by selfless, tireless Abet Chichi2.

MiamiGent

The Most Upgraded Stocks In Q2

ChatGPT Is Already "Old School"

TUE., June 20, 2023|

by Thomas Hughes for MarketBeat

Key Points

Microsoft scores the top spot in Q2 for upgrades and price target revisions.

Meta Platforms falls from 1st to 2nd but is still a heavily upgraded name.

NVIDIA remains in 3rd spot and is a winner in the eyes of the analysts.

The Q2 earnings reporting season is about to be unleashed, making now an excellent time to look at which stocks the analysts are paying attention to. Among the many ways to find this information is Marketbeat’s list of the Most Upgraded Stocks. This list tracks upgrades and upward price target revisions and can be a telling indicator of where market money is flowing. While the names at the top of the list are the same as in Q1, the order is changing, and some exciting names are popping up below the top 3 spots that bear watching.

Microsoft Takes The Lead, Is Most Upgraded Stock In Q2

Microsoft NASDAQ: MSFT was the 2nd Most Upgraded stock coming out of the Q1 reporting season due to its position in the Cloud and potential dominance within the world of AI. The analysts have continued to shower praise on the company and have put it firmly in 1st position outpacing Meta NASDAQ: META by 8 revisions. Microsoft has been upgraded or had its price target raised 54 times in the last 3 months pegging its consensus rating at Moderate Buy. The 54 is significant for the volume of analysts covering and upgrading the stock and because some analysts have upped their data more than once.

The price target is a cause for concern in the near term. The price target is trending higher since the Q1 report, it’s up more than 15% since last quarter, but it is still trailing the price action. The consensus of $333.23 is about 2.5% below the price action, which is trying to break out to a new high. That may come when the company reports earnings for Q2, which is scheduled for July 27th. The analysts expect revenue to grow about 7%, consistent with Q1. Solid guidance and anything to do with AI could be the catalyst to get the consensus target above the all-time high and this market to break out.

Microsoft stock price chart

Meta Platforms: Still Getting Upgrades

Meta Platforms fell from the top spot, but this cloud-based consumer-oriented AI-powered company still gets upgrades, price target increases, and newly initiated coverage. The company has received 46 revisions in the last 3 months from 50 analysts, up 13 from last year. Some companies in the AI craze don’t have 13 analysts covering them, so that is saying something. The price target is trending higher, but, like with Microsoft; it is trailing the price action by a wider margin.

Meta is slated to report earnings the day after Microsoft and to post about 8% of top-line growth. Again, the company may provide market-beating results due to its internal efforts at efficiency and the rise of AI. Regardless, news about AI may be enough to invigorate the market and extend the rally to a new high.

NVIDIA: Still In 3rd

NVIDIA NASDAQ: NVDA is still sitting in 3rd spot. The company has garnered 44 revisions in the last month to remain solidly in its position. The analysts rate this stock a Moderate Buy with a price target trending higher but lagging the market. The caveat is that the price target is up 40% in the last month, 40% YOY and the freshest targets imply a double-digit upside. NVIDIA reports on August 23rd and may shock the market with another strong report.

Advanced Micro Devices NASDAQ: AMD and Adobe NASDAQ: ADBE are in the 4th and 5th spots. These companies have emerged as serious competition for NVIDIA (in the case of AMD) and a substantial part of the AI infrastructure (in the case of ADBE).

The surprising cyclicality of the biotech sector

By: Jay Kaeppel | June 19, 2023

• The biotech sector has shown remarkably consistent cyclicality in the past 22 years. As detailed herein, investors and traders can gain an advantage by knowing where this sector stands regarding the annual seasonal trend.

Read Full Story »»»

DiscoverGold

Hunter Biden to plead guilty to federal criminal tax charges

This is a developing news story. Please check back for updates:

https://www.cnbc.com/2023/06/20/hunter-biden-to-plead-guilty-to-federal-criminal-tax-charges.html

CNBC Morning News

1. Short but dense week ahead

U.S. equities markets face a shortened week after the three-day Juneteenth holiday weekend. Whether stocks can continue their momentum from last week, though, remains an open question. The S&P 500 and the Nasdaq, in particular, are on hot streaks. The former has posted five straight winning weeks, while the latter is on an eight-week run, something it hasn’t done since November 2019. While the Federal Reserve’s rate-hiking pause may have lifted spirits among investors, all ears will be listening for hints about the central bank’s next steps from several Fed speakers this week. New York Fed President John Williams and Fed Vice Chair for Supervision Michael Barr will appear together at an event Tuesday, while Chairman Jerome Powell is scheduled to testify before lawmakers Wednesday and Thursday. Follow live market updates.

2. Big changes at Alibaba

Alibaba, the Chinese e-commerce and tech giant, shook up its leadership structure as it embarks on a sweeping corporate restructuring into six business units. The company said Daniel Zhang will step down from his CEO role and focus more on Alibaba’s cloud operations. “Cloud Intelligence Group is now full speed ahead on its spin-off plans and we are approaching a crucial stage of the process, so it is the right time for me to dedicate my full attention and time to the business,” he said in a memo to employees. Eddie Wu will take Zhang’s spot as CEO, while Brooklyn Nets owner Joe Tsai will become chairman after previously serving as executive vice chair.

3. Bad weekend for Disney and Warner Bros.

After months of hype, it sounded like Warner Bros. Discovery had lightning in the bottle with its latest big-budget DC Comics movie, “The Flash,” but those hopes fizzled this weekend. The superhero movie, which features troubled actor Ezra Miller and a slew of live action and CGI cameos, came in well below estimates for its opening weekend, drawing only $55 million. But Warner wasn’t the only studio with issues over the weekend. Disney’s animated “Elemental” had the lowest opening of any Pixar release since the original “Toy Story” in 1995 – and that’s without taking inflation into consideration. (MG Note: In this movie, DIsney introduced its first "non-binary character. Seems movie goers are talking back to Disney). There won’t be much new competition at the box office this coming weekend, so maybe there’s a chance both movies can do OK in week 2. But it appears as though audiences are already getting their superhero and animation fixes from the dominant “Spider-Man: Across the Spider-Verse.”

4. Blinken in China

U.S. Secretary of State Antony Blinken traveled to China over the long weekend in a bid to ease escalating tensions between the two major powers. His trip included a surprise visit with Chinese President Xi Jinping, prompting positive signals from both sides. U.S. President Joe Biden said Blinken “did a hell of a job.” “We’re on the right trail here,” the president added. The Xi-Blinken meeting could also set the stage for a meeting between the two presidents later this year. Several issues remain, however, including frosty relations between the countries’ military leaders, particularly in light of growing global concern over China’s designs for Taiwan, which China claims as its own. Blinken said he repeatedly mentioned the need to restart military talks, but “China China does not agree to move forward with that.”

5. Hyundai ponders Tesla partnership

Hyundai is considering whether to join Ford and General Motors in using Tesla’s charging technology in North America. Elon Musk’s EV giant dominates the market for fast-charging stations in the U.S. Increased adoption of the tech, known as the North American Charging Standard, should be a boost to legacy automakers trying to catch up to Tesla, while Tesla should reap profits, as well. For Hyundai, it will be a matter of whether Tesla can adapt to the South Korean automaker’s higher-voltage charging demands. “That’s what we will look into from the customer’s perspective,” Hyundai CEO Jaehoon Chang said.

— CNBC’s Mike Calia wrote this newsletter. Brian Evans, Clement Tan, Arjun Kharpal, Sarah Whitten, Sheila Chiang and Evelyn Cheng contributed.

IBM and Adobe Expand Partnership With Generative AI Focus

BY PYMNTS | JUNE 19, 2023

IBM and Adobe are expanding their partnership to help brands create content with artificial intelligence (AI).

The collaboration, announced Monday (June 19), will see IBM Consulting debut a portfolio of Adobe consulting services to help customers “navigate the complex generative AI landscape, bringing together innovation, technology and design to digitally reinvent customer interactions,” IBM said in a news release.

According to the release, Adobe’s enterprise clients will gain access to IBM Consulting experts, who can help them implement generative AI models for the design and creative process.

“We’re seeing incredible momentum in AI adoption as more brands turn to generative AI to create seamless and highly personalized customer experiences to drive growth and improve productivity,” said Matt Candy, global managing partner, IBM iX Customer & Experience Transformation, IBM Consulting.

“By expanding our strategic partnership with Adobe, we can help marketers more effectively design AI-powered experiences while establishing appropriate guardrails, so the AI is built on trust and transparency principles to promote brand consistency and integrity.”

The announcement comes as more and more companies add generative AI functions into their offerings, such as last week’s debut of Meta Platforms’ generative AI model that performs speech-generation tasks such as audio editing, sampling and styling.

As PYMNTS noted recently, generative AI is bringing brands’ customer service to its next horizon, with technology that can detect emotion, offer advice and complete entire transactions.

Already, more than 60% of consumers say that voice assistants will become as smart and reliable as human assistants, while 41% project that will happen within five years, according to the PYMNTS report “How Consumers Want to Live In the Voice Economy.”

Last month saw reports that IBM was freezing or slowing hiring for roughly 26,000 back-office roles, positions that could be handled by AI.

“I could easily see 30% of that getting replaced by AI and automation over a five-year period,” CEO Arvind Krishna said at the time, though he later clarified this doesn’t necessarily mean the company’s total employment would decrease.

“That gives the ability to plow a lot more investment into value-creating activities,” said Krishna. “We hired more people than were let go because we’re hiring into areas where there is a lot more demand from our clients.”

Liquidity is Increasingly Stable as Fed Holds Rate Hikes

By: Joe Duarte | June 18, 2023

The Federal Reserve is still talking tough via its dot-plot, which forecasts two more interest rate increases before the end of 2023. But the markets are not agreeing. My money, for now, is with the markets.

In fact, we are currently in what I call a double barrel bull market, where two major groups are pulling the rest of the market higher. The one everyone knows is AI. The other, more quiet but equally bullish, is the housing sector.

Since lots of people have missed the rally and are now playing catch up, the upward momentum will keep going for a while. Of course, this rally can't, shouldn't, and won't last forever. But if history is any guide, the rest of 2023 and much of 2024 have a built in upward bias, at least based on the phenomenon known as the Presidential Cycle; whose major premise is that the Fed raises rates in the first two years of a presidential term (which it has) and lowers them in the last two years (which seems highly likely).

AI Poster Child Makes New Highs

The poster child for the AI rally is the Invesco QQQ Trust (QQQ), as it houses the large-cap tech stocks, which are moving higher based on expectations of large profits in the future from increasing automation and whatever AI eventually delivers.

Last week, QQQ made another series of new highs. But, by Friday, it looked at bit tired. Thus, it makes sense to expect some sort of consolidation. A move back to the 20-day moving average is not out of the question.

Lennar's Goldilocks Quarter

For the past several years, I've written extensively about the homebuilder stocks and related sectors. That's because this area of the market continues to move higher. Moreover, the more negative investors become on the sector, the higher it goes.

Take, for instance, the recent action in leading homebuilder Lennar (LEN), a longstanding holding in my Joe Duarte in the Money Options portfolio, and a personal holding. Its most recent earnings report blew past analysts' expectations on both earnings and revenues as the company again offered a positive outlook. Naturally, the shares broke out to a new high.

What makes Lennar's earnings most interesting is the company's management of its inventory – not too hot, not too cold. Moreover, the company's Executive Chairman Stuart Miller noted that home buyers have come to accept the "new normal" status of interest rates, adding "demand has accelerated." He concluded by noting: "Simply put, America needs more housing, particularly affordable workforce housing, and demand is strong when price and interest rates are affordable."

In other words, unless interest rates climb significantly higher, the housing sector, from the point of view of homebuilders, is in better shape than many investors may think.

And here is something else to consider. Lennar is trading at a P/E of 9.46, while Nvidia (NVDA), the biggest benefactor of the AI trend, is trading at a P/E of 54.91.

Bond Yields Hold their Ground

Bond yields remained below their recent top level of 3.8% as 262,000 Americans filed for unemployment benefits, an increase of 17,000 from the prior week. In addition to the stable inflation pictured in CPI and the rolling over of producer prices (PPI) released earlier in the week, bond traders breathed a sigh of relief.

Buried in the jobless claims number were over 7,000 new filings in Texas, the highest number of new claims in the U.S. for the week. Let's put this in some perspective. Based on recent U.S. Bureau of Labor Statistics numbers, the Lone Star State accounted for 7% of the total U.S. GDP. Moreover, in Q4 2022, Texas accounted for 9.5% of total U.S. GDP, which means the largest economy in the U.S. is starting to feel the pinch of the Fed's rate hikes.

On the other hand, Texas has received the largest number of new residents of any state in the post-COVID period. All of which means that for now, even in a slower economy, there is still a tight supply of housing combined with high demand. Texas is not alone, as the sunbelt remains attractive to many people looking to escape high taxes and challenging employment situations.

This confluence of data, rising initial jobless claims, slowing inflation, and a coincident slowing of the Chinese economy has led to an encouraging reversal in U.S. Treasury bond yields, which will likely benefit the homebuilders. That's because, with lower bond yields, we're already seeing an increase in mortgage activity, as the chart above shows.

The 3.85% yield on the U.S. Ten Year Note remains 3.85%, roughly corresponding to 7% on the average 30-year mortgage. So, if yields remain below this level, the odds favor a continuation of the steady performance of the homebuilder sector.

Incidentally, I have expanded my coverage of the housing and real estate markets in a new section for members of my Buy me a Coffee page, where you will get the inside scoop on what's happening in these important sectors. This crucial information complements the stock picks at Joe Duarte in the Money Options.com You can start by reviewing my extensive report on the outlook for the homebuilder sector here.

NYAD Improves SPX and NDX Look to Consolidate

The New York Stock Exchange Advance Decline line (NYAD) continues to improve. As long as it's above its 50-day moving average, that's signaling stocks are back in an uptrend.

The Nasdaq 100 Index (NDX) moved above 15,000 and is due for a pause. But in this market, any pause may be short-lived. ADI and OBV remain in bullish postures.

The S&P 500 (SPX) moved above 4400 and looks set to take a breather. As with NDX, any pause may not last. Both ADI and OBV look to be in good shape.

VIX Makes New Low

The CBOE Volatility Index (VIX) broke to another new low last week as call option buyers overwhelmed the market. As I noted last week, this is probably a little too much bullishness all at once, so I expect a bit of a bounce in VIX, which will likely lead to some backing and filling in the market.

When the VIX rises, stocks tend to fall, as rising put volume is a sign that market makers are selling stock index futures to hedge their put sales to the public. A fall in VIX is bullish, as it means less put option buying, and it eventually leads to call buying, which causes market makers to hedge by buying stock index futures. This raises the odds of higher stock prices.

Liquidity is Increasingly Stable as Fed Holds Rate Hikes

With the Fed on hold, the market's liquidity is starting to move sideways, which is a positive. A move below 94 on the Eurodollar Index (XED) would be very bearish, while a move above 95 will be a bullish development. Usually, a stable or rising XED is very bullish for stocks.

Read Full Story »»»

DiscoverGold

AMD Stock May Have Much Further To Go Based On Analysts' Estimates

By: Barchart | June 18, 2023

Advanced Micro Devices (AMD) stock is up over 87% YTD, including a rise of 19% in the last month alone. However, as of June 16 AMD stock is at $120.08, up just $1.87 or 1.58% since May 31 when it closed at $118.21. However, based on average analyst earnings estimates, the stock may have much further to go. That is good news for investors who short out-of-the-money (OTM) put options for income plays.

In fact, we discussed this trade last month on May 28, “High Put Premiums On Advanced Micro Devices Stock Make Shorting Them Attractive For Income.” At the time we discussed shorting the $110 strike price puts expiring on June 16 for $1.12 premium and shorting the $113 strike price puts for $1.56.

Both trades have been extremely profitable since AMD stock closed at $120.08 and the put options expired worthless. That means the investor kept all of the proceeds from the 3-week trade. In addition, had no obligation to purchase the stock at either $110 or $113.00.

Given that the stock does not appear overvalued at this point (see below) it makes sense to repeat the same trade in a new 3-week short expiration period.

AMD Stock May Still Be Undervalued

One reason the stock could have further to go is that analysts still have reasonably high price targets. For example, Morningstar's analyst says that his price target is now $130 per share. This is based on the “firm’s significant growth opportunity ahead as it capitalizes on favorable trends in data centers, artificial intelligence, and gaming.”

Moreover, the average annual P/E (price/earnings) forward multiple for the last 5 years has been 38.5x according to Morningstar data. This is higher than the average of the 2023 41.7x multiple and the 28.3 multiple for 2024 based on Seeking Alpha's survey of analysts' forecasts. That average is 35x, making it clear that the 38.5 average from Morningstar implies AMD stock could rise at least 10% from here (i.e., $38.5/35 = 1.10).

Moreover, Seeking Alpha indicates that the 5-year forward multiple has been 42.73x. That implies that AMD stock could rise 22% from here (i.e., 42.73x/35x = 1.22). The bottom line is that AMD stock could still rise from here over the next year even if it were to stay in line with its historical average multiples.

Shorting OTM AMD Put Options For Income

As mentioned above, it might make sense to short AMD puts for 3 weeks out, or that expire on July 7, 2023. For example, the $113 strike price put trades for $1.82 per put contract and the $115 strike price put is at an amazing $2.49 premium.

This means that the $113 strike price cash-secured short put investor will make 1.61% (i.e., $1.82/$113 = 0.161) immediately with a strike price that is almost 6% below today's price. The $115 strike price short put investor will make 2.165% (i.e., $2.49/$115).

AMD Puts - Expiring July 7, 2023 - Barchart - As of June 16, 2023

For example, assuming an investor secures $11,300 (i.e., 100 shares x $113) with their brokerage firm, they can enter an order to “Sell to Open” one 1 put contract at $113. The account will immediately make $182.00. That is why the immediate yield is 1.61% (i.e., $182/$11,300). Moreover, if the investor can do this every three weeks for a year, the annualized return is 27.9%, since there are 17.33 periods of 3 weeks in a year (i.e., 17.33 x 1.61% = 27.9%).

And, in addition, an investor who secures just $11,500 with their brokerage firm can make $249.00 immediately. That works to an immediate yield of 2.165% or 37.5% if done every three weeks for a year.

Moreover, keep in mind that if AMD stock falls to $115 or $113 on or before July 7, the investor's secured cash will be used to automatically purchase 100 shares of AMD stock. But at least the overall breakeven dollar points are still well below today's price. Nevertheless, at that point, the investor may or may not have an unrealized loss by purchasing AMD stock.

But all is not lost. For one, this exercised purchase may actually lower the investor's ongoing cost in the stock. Moreover, the investor can turn the situation around and sell out-of-the-money calls on a three-week basis. That will bring in more income that could allow them to allow the trade to become profitable, despite the unrealized capital loss.

The bottom line is that AMD puts that are out-of-the-money look like a good investment, especially since AMD stock may have further to rise.

Read Full Story »»»

DiscoverGold

S&P 500 Index (SPX) »» Weekly Summary Analysis

By: Marty Armstrong | June 17, 2023

S&P 500 Cash Index closed above our indicating ranges on the Daily level. It closed today at 440959 and is trading up about 14% for the year from last year's settlement of 383950. Presently, this market has been rising for 2 months going into June reflecting that this has been only still, a bullish reactionary trend. As we stand right now, this market has made a new high exceeding the previous month's high reaching thus far 444847 while it has not broken last month's low so far of 404828. Nevertheless, this market is still trading above last month's high of 423110.

ECONOMIC CONFIDENCE MODEL CORRELATION

Here in S&P 500 Cash Index, we do find that this particular market has correlated with our Economic Confidence Model in the past. Our next ECM target remains Tue. May 7, 2024. The Last turning point on the ECM cycle low to line up with this market was 2020 and 2009 and 2002. The Last turning point on the ECM cycle high to line up with this market was 2022 and 2007 and 2000.

MARKET OVERVIEW

NEAR-TERM OUTLOOK

The historical perspective in the S&P 500 Cash Index included a rally from 1974 moving into a major high for 2022, the market has pulled back for the current year. The last Yearly Reversal to be elected was a Bullish at the close of 2020 which signaled the rally would continue into 2022. However, the market has been unable to exceed that level intraday since then. This overall rally has been 2 years in the making.

This market remains in a positive position on the weekly to yearly levels of our indicating models. Nevertheless, it closed last year on the weak side down from 2021. Pay attention to the Monthly level for any serious change in long-term trend ahead.

From a perspective using the indicating ranges on the Daily level in the S&P 500 Cash Index, this market remains in a bullish position at this time with the underlying support beginning at 434013.

On the weekly level, the last important high was established the week of June 12th at 444847, which was up 13 weeks from the low made back during the week of March 13th. So far, this week is trading within last week's range of 444847 to 430437. Nevertheless, the market is still trading upward more toward resistance than support. A closing beneath last week's low would be a technical signal for a correction to retest support.

The broader perspective, this current rally into the week of June 12th reaching 444847 has exceeded the previous high of 421291 made back during the week of May 15th. Right now, the market is above momentum on our weekly models hinting this is still bullish for now as well as trend, long-term trend, and cyclical strength. Looking at this from a wider perspective, this market has been trading up for the past 13 weeks which from a timing perspective warrants concern.

INTERMEDIATE-TERM OUTLOOK

YEARLY MOMENTUM MODEL INDICATOR

Our Momentum Models are declining at this time with the previous high made 2021 while the last low formed on 2022. However, this market has rallied in price with the last cyclical high formed on 2022 and thus we have a divergence warning that this market is starting to run out of strength on the upside.

After closing above last year's low of 366271.

Interestingly, the S&P 500 Cash Index has been in a bullish phase for the past 7 months since the low established back in October 2022.

The market is trading some 4.21% percent above the last high 423110 from which we did originally obtain one sell signal from that event established during May. Long-Term critical support still underlies this market at 416430 and only a break of that level on a monthly closing basis would warn of a break of the current uptrend. At this time, the market is holding and is trading above last month's high as well.

DiscoverGold US Equity Fund Inflows $19.9 Billion; Taxable Bond Fund Inflows $6.4 Billion

By: Refinitiv | June 15, 2023

• FUND FLOW REPORTS FOR THE WEEK ENDED 06/14 ARE NOW AVAILABLE.

For the week ended 06/14/2023 ExETFs - All Equity funds report net outflows totaling -$5.295 billion, with Domestic Equity funds reporting net outflows of -$4.614 billion and Non-Domestic Equity funds reporting net outflows of -$0.682 billion...ExETFs - Emerging Markets Equity funds report net outflows of -$0.234 billion...Net inflows are reported for All Taxable Bond funds of $6.399 billion, bringing the rate of inflows for the $2.966 trillion sector to $2.291 billion/week...International & Global Debt funds posted net inflows of $0.181 billion...Net inflows of $4.003 billion were reported for Corp-Investment Grade funds while High Yield funds reported net inflows of $0.615 billion...Money Market funds reported net outflows of -$6.842 billion...ExETFs - Municipal Bond funds report net outflows of -$0.168 billion.

Read Full Story »»»

DiscoverGold

Money managers Reduced their exposure to the US Equity markets since last week...

DiscoverGold

NAAIM Exposure Index

June 15, 2023

The NAAIM Number

81.66

Last Quarter Average

63.74

»»» Read More…

Breitbart Business Digest

by John Carney - Breitbart Economics Editor

and Alex Marlow - Breitbart Editor-In-Chief

June 15, 2023

advertisement

The Market Still Doubt Fed's Inflation Resolve

Wall Street still wants to fight the Fed.

The Federal Reserve's policymakers at yesterday's meeting revised up their estimates for year-end interest rates from 5.1 percent to 5.6 percent, which would translate into a policy range of 5.50 percent to 5.75 percent. The "dot plot" shows that nine Fed officials have forecasted that level for rates and three have forecasted a higher level. Just six officials have predicted rates lower than that, and no one has predicted anything lower than the current level.

The other revisions in the Summary of Economic Projections were largely consistent with this view. The median projection for core inflation was revised up (although headline inflation was revised down slightly), as was the projection for economic growth. The projection for unemployment was revised down. So, the Fed appeared to be sending the signal that the economy is expected to continue to be resilient, making it better able to withstand further rate increases.

The bond market has consistently underestimated the Fed's rate increases for two years. Some investors have thought, as the Fed itself once did, that inflation would be "transitory" and therefore not require too many hikes. Others thought the economy would be more vulnerable to rate hikes, entering a recession late last year or early this year. And still others just doubted the determination of the Fed to bring down inflation, predicting that the Fed would not just back off from increasing rates but start cutting to fend off a downturn.

The reaction to Wednesday's announcements and Chairman Jerome Powell's press conference suggests this is still happening. Markets and analysts are no longer forecasting a series of rate cuts this year, but they do not buy the notion that the Fed will hike to a range of 5.5 to 5.75 and keep it there through the end of the year. The CME Group's metric based on prices of fed funds futures currently estimates just under a seven percent chance that we end the year at the median forecasted range, with no chance that we end higher.

The outcome most favored by the implied odds is one quarter of a point higher than the current target. The probability of that is estimated to be around 44 percent. After that is rates ending the year at their current level, with a 39 percent probability. A quarter-point cut is still getting a 10 percent probability, higher than the odds that we hit the median Fed projection.

The Bloomberg consensus forecast is based on estimates issued before the Fed's meeting, but it also suggests a skepticism that the Fed will follow the projected path. It shows rates at year's end being where they are today. When updated, it is unlikely to show more than a quarter point hike.

"Why the gap?" Bank of America's Ethan Harris asked in a note on Thursday morning. "In our view, both the markets and the consensus are under-estimating the anti-inflation resolve of the Fed. When inflation is a serious problem, the Fed will not cut at the first sign of recession. Indeed, the doves on the committee have voted for every rate hike, including lumpy 75 bp moves, a hike at the peak of bank stress and a hike in front of the debt ceiling deadline. These folks are serious."

Fed No Longer Sees 2023 Recession

When the Fed released its earlier set of projections back in March, we noted that the Fed appeared to be forecasting a recession. The Fed was projecting fourth-quarter to fourth-quarter growth of just 0.4 percent even though the economy appeared to have grown by at least one percent in the first quarter of the year. To us this signaled that the Fed believed we were in for two consecutive quarters of contraction later in the year to drag the full year down to four-tenths of a percent.

That's no longer the case. The latest projections have the economy growing 1.1 percent this year. That's below the Fed's long run estimate of 1.8 percent growth—but not that far below. More importantly, it looks achievable with sluggish growth in the third and four quarter after a surprisingly robust second quarter. So, there is no longer an assumption of contraction built into the numbers.

If you look at the range of growth estimates, it is striking how much more bullish on the economy the Fed has become. At the March meeting, estimates ranged from -0.2 percent to two percent. The new projections lift the bottom of the range all the way up to positive 0.5 percent and the top of the range to 2.2 percent. We don't get dot plots for the GDP projections, but it is striking that no one on the Fed is expecting a full-year contraction.

Americans Are Still Spending More

That bullishness on the economy got some support on Thursday from the better-than-expected retail sales numbers. Sales were expected to contract in May, with many economists doubting our Easter rally thesis and convinced that there would be pullback after April's 0.4 percent surge. Instead, consumer sales rose by 0.3 percent. If you exclude gas station sales (which were depressed by the decline in gas prices), consumer sales were up 0.6 percent.

As we said the other day on Larry Kudlow's Fox Business show, consumer sales are likely to stay strong so long as the jobs market remains strong. That, in turn, is likely to continue to prop up inflation and higher interest rates.

With the consumer price index rising just 0.1 percent and core inflation up 0.4 percent in May, a good deal of this spending looks real and not just nominal. So, Americans are actually buying more, not just paying more for the same volume of goods and services.

CNBC Morning news

1. The pause is here

The Federal Reserve on Wednesday held its benchmark rate steady after more than a year of increases, but the central bank suggested more hikes could come this year. The next Fed meeting is in six weeks, and Chairman Jerome Powell said the next rate decision is still up in the air. Markets were mixed afterward, as the Dow fell while the S&P 500 and the Nasdaq hit their highest levels since April of last year. It was also the S&P 500's fifth consecutive positive trading day, its longest such streak since November 2021. Follow live market updates.

2. An IPO on the menu

Cava, the Mediterranean fast-casual restaurant chain that’s been compared to Chipotle, is set to make its debut on public markets Thursday. The company said Wednesday night it had priced its offering at $22 a share, up from the already-increased range of $19 to $20 that Cava projected Monday. The pricing values Cava at about $2.45 billion. The stock will trade under the symbol CAVA. A successful debut for Cava could be a good sign for a moribund market for initial public offerings that has taken a hit over the past year-plus amid higher inflation and rate hikes.

3. China's economic muddle

The economic signs coming out of China aren’t great, as its post- “zero Covid” recovery stalls out. On Thursday, the country released a wave of lackluster data, including that the unemployment rate for workers aged 16 to 24 rose to a record 20.8% in May. Retail sales, industrial production and fixed asset investment all grew at slower rates than expected. While China’s statistics bureau said the data represented continued momentum for the recovery, it also acknowledged that certain international challenges could pressure the economy, but didn’t elaborate beyond that. China’s central bank, meanwhile, is in rate-cutting mode as it looks to juice growth.

4. In the rough

It was just last week that the PGA Tour and its Saudi-funded rival, LIV Golf, announced a deal that rocked the sports world. Since then, there have been plenty of twists and turns, including the sudden leave of absence taken by PGA Tour Commissioner Jay Monahan over an unspecified health matter. Senators have opened probes while urging the Justice Department to look into the agreement, which has yet to fully take shape. CNBC’s David Faber, meanwhile, reported that PGA Tour players who had previously missed out on big LIV paydays may be looking to hire a bank to advise them on compensation if the deal closes. PGA Tour players, meanwhile, are in Los Angeles for the U.S. Open, which begins Thursday.

5. Putin's mercenary problem

Russian President Vladimir Putin finds himself at odds with the country’s infamous Wagner Group of mercenaries. Until recently, Wagner’s leader, Yevgeny Prigozhin, primarily has had issues with Russia’s defense ministry over strategy in the Ukraine invasion. Now, though, Putin has endorsed the ministry’s call to have groups like Wagner sign contracts with the military, which Prigozhin has opposed. Elsewhere, U.S. Secretary of State Antony Blinken plans to attend the Ukraine Recovery Conference next week in London as allies and organizations work to devise a reconstruction plan for the war-ravaged country. Follow live war updates.

— CNBC’s Mike Calia wrote this newsletter. Hakyung Kim, Sara Salinas, Evelyn Cheng, Jihye Lee, Jessica Golden, Chelsey Cox and Holly Ellyatt contributed.

— Follow Squawk Pod for the best conversations and analysis from Squawk Box in a curated, daily podcast.

Here's how every Dow Jones stock has performed so far in 2023

By: Evan | June 14, 2023

• Here's how every Dow Jones stock has performed so far in 2023

Salesforce $CRM +57.9%

Apple $AAPL +41.6%

Microsoft $MSFT +40.7%

Intel $INTC +34.6%

American Express $AXP +18.1%

Boeing $BA +13.9%

Walmart $WMT +10.6%

McDonald's $MCD +9.5%

Visa $V +7.6%

Cisco $CSCO +7%

Disney $DIS +6.4%

JPMorgan $JPM +5.5%

$DOW +4.8%

The Dow Jones Index $DIA 2.7%

Caterpillar $CAT +1.6%

Goldman Sachs $GS -1.4%

Merck $MRK -2.1%

$IBM -2.6%

Procter & Gamble $PG -3.4%

Nike $NKE -3.6%

Coca-Cola $KO -4.3%

Home Depot $HD -5.1%

Honeywell $HON -6.4%

Travelers $TRV -7.4%

Johnson & Johnson $JNJ -8.5%

Verizon $VZ -9.3%

Chevron $CVX -12.5%

UnitedHealth $UNH -13.3%

3M $MMM -15%

Walgreens $WBA -15.4%

Amgen $AMGN -15.7%

Read Full Story »»»

DiscoverGold

S&P 500: Active investment managers are actively increasing their exposure to the equity market amidst the ongoing rally in stocks

By: Isabelnet | June 15, 2023

• S&P 500

Active investment managers are actively increasing their exposure to the equity market amidst the ongoing rally in stocks.

Read Full Story »»»

DiscoverGold

How Ray Dalio Discovered the Strategy That He Called the Holy Grail of Investing that Made Him a Multi Billionaire

Ryan Targo

Apr 18

Ray Dalio is a Billionaire “investing coach” and is famous for teaching his students what he calls, “the holy grail of investing.”

He would never tell his followers to just play only offense and not bother playing any defense. Yet, nearly all the mutual fund managers on Wall Street only play offense, always betting that stocks will go up no matter how bad the economic conditions get.

They stick with this “buy and hold” practice even when it is obvious to them that the economy is in recession or the Fed is raising interest rates drastically.

If they can convince their clients to just “hold” they can keep charging them fees non-stop.

Unfortunately, this stubborn belief cost the investors in these “offense only” funds dearly with the Nasdaq 100 Index down -32.5% for 2022.

There is Obviously a Better Way

In his book Principles, multi billionaire hedge fund manager Ray Dalio called diversification the “Holy Grail of Investing.” The diversification he is referring to is not owning a portfolio that is a one way bet on stocks going up.

If you own hundreds of stocks, and the stockmarket is down a lot, you are still down big. That isn’t diversification. That is putting all of your eggs in one basket.

Ray Dalio’s version of “real” diversification made him a fortune that exceeds 22 Billion according to Forbes. This type of diversification between equities, commodities, currencies, and bonds makes him money in bull markets and bear markets.

Ray Dalio’s Holy Grail of Investing

Below is Dalio’s explanation of the holy grail of investing that made him wealthy far beyond what he could spend in his lifetime.

That simple chart struck me with the same force I imagine Einstein must have felt when he discovered E=mc2: I saw that with fifteen to twenty good, uncorrelated return streams, I could dramatically reduce my risks without reducing my expected returns… I called it the “Holy Grail of Investing” because it showed the path to making a fortune.

Chart of BNP CASA Index II That Diversifies Between Equities, Commodities, Bonds, Credit, and Currency

Here is how the math works:

If you have 1 return stream like the S&P 500 you earn a 1x return/risk ratio

Combining 2 uncorrelated return streams like stocks and bonds earns a 1.41x return/risk ratio

Combining 4 uncorrelated return streams like stocks, commodities, currencies, and bonds can earn a 2x return/risk ratio

How Diversification Can Make Your Returns Fly Without Increasing Your Risk

Traditional investments like stocks make big money during a boom and lose big during a recession. The key to getting beyond this boom and bust cycle to create a steady path towards financial freedom is balancing offensive strategies that do well when the economy is growing with defensive strategies that generate big returns during a recession.

It should be common sense that you could easily beat something like the S&P 500 that only plays offense and gets clobbered during a downturn with a balanced strategy that makes money steadily rather than making it and giving it back.

Applying Offense and Defense to Build Dalio’s All Weather Portfolio

The key to building an all weather portfolio that can make money whether the economy is booming, in recession, inflating, or deflating is deploying a strategy that works for each of these “seasons.”

A) Economy Booming: Equities do very well

B) Economy Tanking: Trend following strategies that short markets that are tanking typically thrive during bear markets like 2022, 2008, and 2000–2002.

C) Inflation: Investments in commodities thrive when inflation is ripping

Usually there are 3 opposite market direction waves during a Federal Open Market Committee (FOMC) day. Abet Chichi2 had been able to observe and monitor this market behavior over the years.

DiscoverGold

EU charges Google with anti-competitive practices in ad tech business

This is a developing news story. Please check back for updates:

https://www.cnbc.com/2023/06/14/eu-charges-google-with-anti-competitive-practices-in-ad-tech-business.html

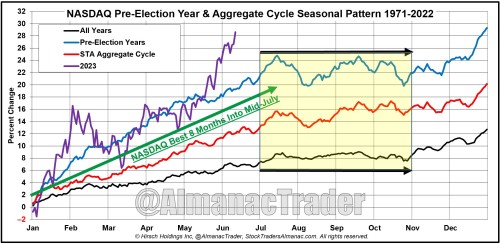

Solid Pre-Election June Gains As Expected

By: Almanac Trader | June 13, 2023

June is delivering much better than typical pre-election year strength, but NASDAQ and Russell 2000 are leading the charge as usual. R2K was up 7% for the month yesterday and NAS was up 4%, both up more today. However, June quarterly OpEx is riddled with volatility. Week after DJIA is Down 27 of the last 33 years 1990-2022. (2023 STA page 108.) S&P down 23 of 33. NASDAQ down 18/33.

So far in 2023 NASDAQ is closely tracking the pre-election pattern up 28.6% year-to-date! But remember, June ends NASDAQ’s Best 8 Months with a seasonal peak in mid-July. Enjoy this AI/Chip-driven rally for now and use it to reposition for the Worst 4 Months July-October.

The backdrop is set up for sideways action over the weak summer months, especially after mid-July into the worst two months of the year August and September. This is lining up well for our NASDAQ Best 8 Months MACD Seasonal Sell Signal that can occur anytime on or after June 1. AI (Almanac Investor) subscribers will be emailed when it triggers.

Read Full Story »»»

DiscoverGold

Breitbart Business Digest

by John Carney - Breitbart Economics Editor

and Alex Marlow - Breitbart Editor-In-Chief

June 13, 2023

Inflation Tame Enough for a Fed Pause

Federal Reserve Chairman Jerome Powell will get his pause.

The Labor Department's consumer price index (CPI) rose just one-tenth of a percentage point in May, slightly less than forecast, largely due to a fall in energy prices. Compared with a year ago, prices are up four percent, the lowest inflation read in two years. That's likely enough to make Federal Reserve officials comfortable with putting rate hikes on pause at the next meeting.

More troublingly, core inflation continues to run hot. Core CPI rose 0.4 percent in May, where it has been since December. Unrounded core inflation has actually been ticking up for two months. This suggests that the Fed has not made very much progress on bringing down inflation.

Energy prices tumbled 3.6 percent for the month and are down 11.6 percent compared with May of 2022, providing relief to households but also likely fueling spending elsewhere in the economy. Gasoline prices dropped 5.6 percent in May and are down 19.7 percent year-over-year. Energy services prices fell 1.6 percent for the month, the fourth consecutive decline. This was largely driven by a fall in piped natural gas prices.

Food inflation, on the other hand, accelerated. The prices of groceries rose by one-tenth of a percentage point, ending two straight months of falling prices. Prices of fruit and vegetables rose 1.3 percent. This was partially offset by declines in prices for meats, poultry, fish, and eggs. Bread prices climbed higher, raising their year-over-year gain to 12.5 percent.

Dining out also got pricier. The Labor Department's measure of "food away from home" jumped 0.5 percent, for a year-over-year gain of 8.3 percent. This is likely driven by restaurants passing along increased labor costs. Fast food prices rose faster than full-service restaurant prices, also likely a reflection of labor costs.

Used Car Prices and Rent Driving Inflation

Used car prices rose sharply, as telegraphed by the rise in wholesale auction used car prices earlier this year. Excluding used car prices, core CPI was flat for the month, down from a 0.6 percent increase in April. This reflects a decline in demand for goods as well as better functioning supply chains. China's reopening may also be contributing to disinflation, particularly in categories like furniture, which fell 0.7 percent, the second consecutive monthly decline.

Shelter costs are also driving inflation, although the pace is decelerating. Rent and owner’s equivalent rent increased by 0.5 percent in May compared with April. Over the last three months, these have averaged 0.5 percent month-0ver-month. The three-month annualized rate of change for rent is 6.3 percent, down from 7.4 percent. The three-month change in owners' equivalent of rent dropped 0.7 percent to 6.4 percent.

Median CPI Isn't Falling

As we've argued in the past, we think that median CPI is the best guide to forecasting where inflation is going. The Cleveland Fed said Tuesday that median CPI came in at 0.4 percent in May, exactly where it was in March and April. This suggests that underlying inflationary pressures are not easing by very much at all.

The Cleveland Fed's 16 percent trimmed mean inflation metric ticked down to 0.2 percent on a month-over-month basis, down a tenth from April and equal to the March reading.

Given the stubbornness of inflation and the extremely tight labor market, the Fed should probably stick to hiking rates. Unfortunately, the Fed is most likely going to "skip" this meeting and hold rates steady. Jason Furman's view seems right to us.

That said, a hawkish "skip" is unlikely to be very consequential. The Fed can probably afford to hold rates steady for a month or two without sending inflation higher—so long as it successfully communicates the message that there are more rate hikes ahead. If Powell falters on this, he may end up reigniting inflation.

CNBC Morning news

1. Inflation and the Fed

The Federal Reserve kicks off its two-day policy-setting meeting Tuesday, just as markets will start processing the latest consumer price index report, a key indicator of inflation. Experts expect the number to show that inflation is continuing to cool off, which should encourage the Fed’s policymakers to skip a rate hike this month, according to CNBC’s Jeff Cox. The report drops at 8:30 a.m. ET. Economists polled by Dow Jones expect monthly inflation growth to be just 0.1%, good for a 4% annual rate, still higher than the Fed’s 2% target. Investors, meanwhile, will look at whether Tuesday’s session can bounce off Monday’s positive results. Follow live market updates.

2. Boss battle

The fight between tech giant Microsoft and government regulators just leveled up. The Federal Trade Commission on Monday took legal action in an attempt to block the XBox gaming console maker’s $68.7 billion deal to buy videogame maker Activision Blizzard, saying it would be anti-competitive. Activision Blizzard produces the popular and lucrative Call of Duty series, which is also available on Microsoft rival Sony’s PlayStation consoles. The FTC, which had sued to block the acquisition in December, faced a rapidly approaching deadline for the deal. Microsoft had said it expected to close the transaction by the end of this month.

3. Oracle shines

Oracle shares enjoyed a nice bump in extended trading after the software giant posted better than expected quarterly results and upbeat sales guidance. The company’s cloud business drove much of the success. Cloud services and license support revenue rose 23% to $9.37 billion, accounting for the lion’s share of Oracle’s revenue for the quarter. Revenue from cloud licenses and on-premises did slide, but the company’s growing cloud infrastructure surged again. Oracle will also release a generative artificial intelligence cloud service that’s part of a partnership with startup Cohere, according to co-founder and Executive Chairman Larry Ellison.

4. Toyota charges forward

Toyota unveiled new plans to juice its approach to electric vehicles, sending the company's stock higher in overseas trading. The Japanese auto giant had been more cautious than some of its competitors in joining the EV fray, focusing on hybrids while also focusing on specific markets’ demands. On Tuesday, however, Toyota announced a new unit, called BEV Factory, that aims to produce a full lineup of EVs sporting extended battery range starting in 2026. Toyota aims to achieve sales of 3.5 million all-electric vehicles annually by 2030.

5. Arraignment day

Former President Donald Trump is set to be arraigned Tuesday afternoon at a federal courthouse in Miami. He stands charged with 37 felony counts over his retention of classified government documents, including top secret national security records. Trump has claimed the case is a continuation of a “witch hunt,” while special counsel Jack Smith, who led the probe, has urged Americans to grasp the gravity of the alleged crimes. Smith is still investigating Trump in a different inquiry focused on the ex-president’s attempts to keep power after Joe Biden defeated him in the 2020 election. Trump is set to return to his private club in Bedminster, New Jersey, after his arraignment. There, he’ll host a 2024 campaign fundraiser in honor of his birthday. Trump, the frontrunner for the Republican nomination, turns 77 on Wednesday.

And one more thing ...

The NBA has a new king, and his name is Nikola Jokic. The staid Serbian superstar led the deeply talented Denver Nuggets to their first NBA title Monday night, knocking off the scrappy Miami Heat in five games. Jokic, who has already won two regular season MVP awards, was named NBA Finals MVP after racking up 28 points and 16 rebounds in the deciding game. “The job is done,” Jokic said afterward. “We can go home now.”

— CNBC’s Mike Calia wrote this newsletter. Samantha Subin, Jeff Cox, Lauren Feiner, Jordan Novet, Lim Hui Jie and Christina Wilkie contributed.

It's time to keep an eye on utilities

By: Jay Kaeppel | June 12, 2023

• The utility sector is rarely an exciting place to be. However, when favorable sentiment, breadth, insider buying, and a favorable seasonal tailwind relative to the overall market converge, it may be a good place to be.

Read Full Story »»»

DiscoverGold

Breitbart Business Digest

by John Carney - Breitbart Economics Editor

and Alex Marlow - Breitbart Editor-In-Chief

June 09, 2023

The Labor Market Is Still Very Strong

While the notion that the labor market has been softening underneath the strong headline figures is increasingly popular, the evidence marshaled to support it is not very strong.

The headline labor market figures have been extremely strong. The economy added 239,000 jobs in May, according to the Labor Department. The upward revisions to March and April tacked on another 93,000 jobs. The three-month average is now 283,000, a number that would be impressive in any economy and one that is absolutely shocking in an economy already at full employment and grappling with one of the most rapid rate hike cycles in history.

To put that number in context, it would only take around 75,000 to 100,000 new jobs each month to keep up with demographic trends. So, we're running at or close to double "trend-like" payroll growth.

Meanwhile, employers were trying to fill more than 10 million job vacancies at the end of April. There were 1.8 openings for every unemployed person, a figure that was unprecedented prior to the post-pandemic labor crunch. In other words, the labor market is extraordinarily tight.

The payrolls data has been so strong that economists have not been able to keep up. Since the start of last year, payrolls have come in above the consensus estimate in 15 out of 17 months. This adds up to 1.75 million more jobs than forecast, according to Bank of America's Ethan Harris, or about 100,000 jobs a month.

The Case for Weakness Is...Weak

So, where is the weakness? The unemployment rate moved up from 3.4 percent to 3.7 percent in May. This data, however, comes from the much more volatile and smaller household survey. This showed employment dropping 310,000 in May. While this survey is long-running and has a good track record over the long term, when it conflicts with the larger establishment survey in a given month, it is probably best to look to the establishment survey for guidance.

We do think the household survey could be picking up on an important economic trend. There appears to be a slowdown in the self-employment and very small business sector in the United States. Some of this may be due to tightening financial conditions and inflation pushing up costs. Some of the self-employed are likely moving onto payrolls, which would explain where all the workers fueling payroll growth are coming from. (That was a bit of a mystery given the fact that labor force participation has not been rising.) Some may simply be declaring themselves unemployed. The good news is that with 10.1 million vacant jobs, it is unlikely that they will stay that way for long.

The dip in the average workweek is another widely cited data point supporting the softening labor market thesis.

This is overstated. The average workweek has declined from 34.6 hours in January to 34.3 hours in May. A big part of this appears to be a return to a normal amount of hours worked. In October 2019, for example, the average was also 34.3. The May number was not especially low by historical standards.

We suspect that part of what is driving down the workweek is the increasing demand that employees return to the office. Anecdotal evidence suggests that many workers are willing to work longer if they can do so from the comfort of their homes. What's more, the absence of a commute allows for more time spent on the job.

Harris at Bank of America points to a shift in the composition of the workforce. We're employing more workers in jobs in which people work fewer hours.

"This drop is mainly due to rapid hiring in industries with low average hours. For example, in the past two years 26% of job growth has been in leisure and hospitality where the average work week is only 25.4 hours compared to 34.3 hours for the private sector as a whole," Harris wrote in a recent client note.

It's also true that while average hours may be declining, total hours worked are rising because there are more people working.

The final component of the softer labor market thesis is wages. Average hourly wage growth has slowed down in the past few months to a four percent annual pace. But this, too, is largely reflecting the work force composition.

"A significant chunk of the weakness is due to high growth in low-wage jobs. Again focusing on the red-hot leisure and hospitality sector, even with some increase in pay in the last couple years these workers earn an average of $21 per hour compared to $33 for the private sector as a whole," Harris wrote.

Eventually, the labor market is likely to crack under the pressure of rising rates. There just is not much evidence that it has started to crack yet.

FOMC June 2023 Meeting: A Pause Or A Skip?

By Panos Mourdoukoutas Ph.D.Panos Mourdoukoutas Ph.D.

06/12/23 AT 4:51 AM EDT

When FOMC—the Federal Reserve's monetary policy arm—meets this week, it will likely leave interest rates unchanged.

That's according to the CME's FedWatch Tool, which analyzes the probabilities of changes in the Fed Funds Rate and U.S. monetary policy. This time, it points to a 71.2% chance of interest rates remaining unchanged and a 28.8% chance of a hike by 25 basis points.

But markets will pay close attention to the statement accompanying the FOMC decision to determine whether the Fed is pausing or skipping interest rate hikes.

That's a new dilemma the nation's bank is facing as the U.S. economy has moved closer to its dual pursuit of maximum employment and steady prices. But not close enough to provide clear signals as to whether the Fed is over with monetary tightening.

For instance, the U.S. labor market shows signs of cooling off, with job growth moderating and the unemployment rate edging higher. Nonetheless, the unemployment rate remains at a multi-year low, close to what economists call "the natural unemployment rate."

That's the unemployment rate consistent with full employment.

But further rate hikes could change the situation, push the economy into a recession and the labor market below full employment target. Thus, the case for an interest rate pause.

Still, there's inflation, which remains by most conventional measures, well above 2%, which the nation's central bank considers consistent with steady prices. Thus, the case for a skip in interest rate than a pause in interest rate hikes.

In addition, there are time lags in the transmission mechanism of monetary policy, which makes its full impact unpredictable. That's another argument for a pause, which could help policymakers figure out how the rate hikes have impacted the economy thus far.

Meanwhile, the Fed must cast a wary eye on the looming regional bank crisis and the prospect of a credit crunch that could further limit liquidity and push a slowing economy into a recession. It's another argument for a pause on rate hikes.

"Markets are ready for the Fed to take a break in June," David Russell, vice president of market intelligence at TradeStation, told International Business Times. "Nobody, including Jerome Powell, knows if it's a pause or a skip. Recent data argue in favor of a pause because we're seeing weaker inflation and weaker employment. However, policymakers have been blindsided before, so they will likely keep their options open. The Dot Plot and economic forecasts might mostly stay the same from March. "

Carlos Vaz, CEO of CONTI Capital, is with the pause camp."After hiking interest rates by a cumulative five percentage points over just 17 months, the Federal Reserve appears set to pause the June FOMC meeting," he told IBT. "The Fed is likely mindful of the lagged effects of monetary policy changes, the continued fallout from the banking crisis and some positive signs on the inflation front."

He further thinks that supporting a rate hike pause is the significant tightening in lending standards during the banking crisis. "It only compounds the tightening associated with over a year's worth of rising interest rates," he added. "From the commercial real estate side, we already see a significant downturn in commercial loan originations."

But Vaz doesn't see the pause as the prelude to monetary easing that bullish investors have been hoping for in recent months. "Having been slow to react to the persistence of inflation in late-2021 initially, we believe the Fed is in no mood to pivot to cutting interest rates through the remainder of 2023," he added. "Depending on the economic situation in 2024 — namely, unemployment and GDP growth — a steady pace of interest rate cuts could be in the cards."

Meanwhile, Russell expects this week's FOMC meeting to have little impact on markets, as a couple of committee members have already conveyed the outcome. "We could be entering a new phase when big macro items like inflation and the Fed matter less," he added. "Investors have been through many shocks in the last few years, and the next surprise could be a gradual return to normal. That could be the message from the VIX finally returning to pre-pandemic levels."

But there's an unknown that could tip the balance between skipping and pausing: The May Consumer Price Index (CPI) — a measure of retail inflation — which will be released on June 13, just as the FOMC meeting begins.

"If CPI blows out to the upside, all bets are off," Kevin Flanagan, head of fixed income strategy at WisdomTree, told IBT. "But assuming it comes in as expected, it would not surprise me to see the Fed not make a move."

Angelo Kourkafas, CFA, senior investment strategist at Edward Jones, see the Fed adopting a flexible stance.

Builders FirstSource (BLDR) Shares See Mega Inflows

By: Lucas Downey | June 12, 2023

• Builders FirstSource, Inc. (BLDR) shares are up a staggering 88% in 2023. Investing in growth stocks this year has been a great way to outperform markets. Big Money footprints tell the real story.

Builders FirstSource Attracts Big Money Inflows

Want an edge in trading? Follow the Big Money.

What’s Big Money? Said simply, it’s when a stock rises due to institutional demand. Top stocks tend to attract savvy investors.

You see, fund managers are always looking to bet on the next outperforming stocks…the best in class. They spend countless hours sizing up companies, reading reports, speaking to analysts…you name it. When they find a company firing on all cylinders, they pounce in a big way.

The YTD action tells the story. Each green bar signals unusual buying volumes in BLDR shares, pushing the stock higher:

Source: www.mapsignals.com

Very few stocks have charts this strong. Recent green bars suggest strong demand. But, what about the fundamental story?

Builders FirstSource Fundamental Analysis

Next, it’s a good idea to check under the hood. I want to make sure the fundamental story is healthy too. As you can see, BLDR has had double-digit sales and positive earnings growth the past 3 years:

• 3-year sales growth rate (+54.7%)

• 3-year EPS growth rate (+118.9%)

Source: FactSet

Marrying great fundamentals with our proprietary Big Money software has found some big winning stocks over the long-term.

Check this out. Builders FirstSource has been a top-rated stock at MAPsignals for years. That means the stock has had buy pressure and growing fundamentals. We have a ranking process that showcases stocks like this on a weekly basis.

It’s made the rare Top 20 report numerous times since 2015. The blue bars below show when BLDR was a top pick:

Source: www.mapsignals.com

Tracking unusual volumes reveals the power of the MAPsignals process.

Builders FirstSource Price Prediction

The BLDR rally has been in place for years and recently. Big Money buying in the shares is signaling to take notice. Given the historical gains in share price and strong fundamentals, this stock could be worth a spot in a diversified portfolio.

Read Full Story »»»

DiscoverGold

NYAD Remains Above Support. SPX and NDX Look to Consolidate

By: Joe Duarte | June 11, 2023

First things first. Last week, the headlines blared the S&P 500 (SPX) is in a bull market after a 20% gain from the October 2022 bottom. That's nice, but the real winner has been the tech sector, as measured by the Nasdaq 100 index (NDX), which is up some 38% over the same period.

In fact, as the chart for the Invesco QQQ Trust ETF (NSDQ: QQQ) shows, the rally started in January 2023, as the tech stocks completed a nifty triple bottom. I pointed out that this likely marked the beginning of a new uptrend in this video on January 27, 2023.

What's even more interesting is that the stealth bull market in NDX, which has now spilled over into SPX, is now six months old and has unfolded even as the Fed has been raising interest rates. All of which suggests that as the Fed's next meeting approaches, this is a great time to take inventory of one's portfolio holdings and to take some profits, as the AI/Tech fueled rally, along with the Fed, are both due for a pause.

The Fed's Date with Destiny

The Federal Reserve has a lot to ponder at its June 13-14 meeting. The stock market is booming, while the global economy is showing signs of decelerating rapidly – think China and Europe. The latter has officially slipped into recession based on recently revised data. In the U.S., there is plenty of "soft data" that confirms the softening story. As I noted last week:

• The Dallas Fed Survey crashed, falling for 13th consecutive month; one respondent noted: "There is nothing encouraging on the horizon." Other notable quotes: "orders canceled," "order volume has stalled recently," and "seeing a massive slowdown;"

• The Dallas Fed services survey fell for 12th straight month. Comments worth noting: "Businesses are preparing for a recession by looking for ways to cut back, which in some ways, works to create a self-fulfilling prophecy;"

• Chicago PMI Collapsed;

• China manufacturing PMI fell below 50, signaling contraction; and

• U.S. PMI and ISM surveys fell again.

Elsewhere, it seems that OPEC's "hold the line", combined with decreasing oil production in the U.S., are starting to squeeze oil supplies for the summer driving season. Rising gas prices at the pump are likely to reduce consumer spending in other areas.

All of this suggests there is a 50-50 case for an official pause announcement from the Fed prior to the next FOMC meeting, unless the May CPI and PPI reports, due out on June 13 and 14 as the Fed meets, throw a wrench into things. And don't forget, Mr. Powell's press conference will follow.

My guess is we'll get a pause. But don't discount another 25-basis-point rate increase just for "insurance."

OPEC Puts Floor Under Oil Prices for Now

Of late, I've suggested that shorting a dull market is not a good idea, meaning that, given the ultra-bearish sentiment in the oil market, the odds were better than even that a bottom in the price of crude, and likely oil stocks, was likely.

As it happens, after much talk, OPEC+ decided to keep its current production cuts in place (as much as 1.6 million barrels per day) while OPEC kingpin Saudi Arabia promised a "voluntary" 1 million barrel cut per day.

When dealing with OPEC investors should be aware that production cuts are just numbers. In other words, there is a fair amount of cheating that goes on. Thus, the key is to adjust expectations based on what they say, and watch what they do.

If OPEC+ is to be believed, then up to 2.6 million barrels of oil per day will be removed from the market by some point in 2023-2024 until proven otherwise.

From a market standpoint, the statement seems to have been good enough to put a bottom in West Texas Intermediate (WTIC) and Brent Crude (BRENT) around $70 per barrel.

Moreover, the oil (XOI) and oil service stocks (OSX) seem to have put in a bottom, which is bullish since, traditionally, the stocks bottom out before the commodity. Already, out in the field, I've noticed gasoline prices firming in my neck of the woods.

So, here's a review of what we know as we head into the fullness of driving season:

• OPEC+ is promising to cut production;

• The U.S active rig count is falling, which means the shale belt is following suit;

• Oil and gasoline prices seem to be firming.

It all add up to one thing: oil prices seem to have bottomed until proven otherwise.

I've recently recommended several energy sector picks. You can have a look at them with a free trial to my service. In addition, I've posted a Special Report on the oil market, which you can gain access to here.

Bond Yields Remain Below Important Yield Level

The bond market is reaching a decision point, as it sorts out the state of the economy and inflation. An important data point under consideration is the steadily rising jobless claims numbers released on 6/9/23. In fact, jobless claims have been quietly edging up over the last few weeks as employers reduce new hiring, suggesting a continuation of the economy's slowing.

As a result, the relationship between bond yields, mortgage rates, and the homebuilder stocks remains operational. Note the reversal in mortgage rates (MORTGAGE) leading to a rally in the homebuilders index (SPHB)

The crucial yield point on the U.S. Ten Year Note is 3.85%. If yields remain below this level, the odds favor a continuation of the steady performance of the homebuilder sector.

I have recently written an extensive report on the outlook for the homebuilder sector, which is accessible at my Buy me A Coffee page. To review it, click here.

NYAD Remains Above Support. SPX and NDX Look to Consolidate

As I noted above, the headline of the week was that the S&P 500 (SPX) rose over 20% since its 10/22 market bottom. This puts in a bull market, by definition. I have no problem with that concept, other than to say that I'm expecting the market to consolidate in the short term, which is not a bad thing.

The New York Stock Exchange Advance Decline line (NYAD) remained above its 50-day moving average, signaling stocks are back in an uptrend.

The Nasdaq 100 Index (NDX) remained above 14,500 and is starting to move sideways as it consolidates its AI-related gains. ADI and OBV remain in bullish postures.

The S&P 500 (SPX) moved above 4300 and looks set to take a breather. Both ADI and OBV look to be in good shape.

VIX Looks Set to Bottom Out in the Short Term

The CBOE Volatility Index (VIX) broke to a new low last week as call option buyers overwhelmed the market. This is probably a little too much bullishness all at once, so I expect a bit of a bounce in VIX, which will likely lead to some backing and filling in the market.

When the VIX rises, stocks tend to fall, as rising put volume is a sign that market makers are selling stock index futures to hedge their put sales to the public. A fall in VIX is bullish, as it means less put option buying, and it eventually leads to call buying, which causes market makers to hedge by buying stock index futures. This raises the odds of higher stock prices.

Liquidity is Still Limited but Stable

The market's liquidity may have bottomed out, but it's not particularly bullish or bearish. However, as long as it stays in the current posture, it will pose little danger. With the Eurodollar Index (XED), a move below 94 would be very bearish, while a move above 95 will be a bullish development. Usually, a stable or rising XED is very bullish for stocks.

Read Full Story »»»

DiscoverGold

Microsoft Corp. (MSFT) May just be starting to go into digestion mode...

By: Options Mike | June 11, 2023

• $MSFT Above the 21D still, but some of the air came out of this trade and other big tech names last Wednesday

May just be starting to go into digestion mode...

Read Full Story »»»

DiscoverGold

S&P 500 Index (SPX) »» Weekly Summary Analysis

By: Marty Armstrong | June 10, 2023

S&P 500 Cash Index opened above the previous high and closed above it as well warning of a bullish posture right now. This market is above all our indicators at this time reflecting it is moving higher over recent activity. It closed today at 429886 and is trading up about 11% for the year from last year's settlement of 383950.

As of now, this market has been rising for 2 months going into June reflecting that this has been only still, a bullish reactionary trend. As we stand right now, this market has made a new high exceeding the previous month's high reaching thus far 432262 while it has not broken last month's low so far of 404828. Nevertheless, this market is still trading above last month's high of 423110.

ECONOMIC CONFIDENCE MODEL CORRELATION

Here in S&P 500 Cash Index, we do find that this particular market has correlated with our Economic Confidence Model in the past. Our next ECM target remains Tue. May 7, 2024. The Last turning point on the ECM cycle low to line up with this market was 2020 and 2009 and 2002. The Last turning point on the ECM cycle high to line up with this market was 2022 and 2007 and 2000.

MARKET OVERVIEW

NEAR-TERM OUTLOOK

The historical perspective in the S&P 500 Cash Index included a rally from 1974 moving into a major high for 2022, the market has pulled back for the current year. The last Yearly Reversal to be elected was a Bullish at the close of 2020 which signaled the rally would continue into 2022. However, the market has been unable to exceed that level intraday since then. This overall rally has been 2 years in the making.

This market remains in a positive position on the weekly to yearly levels of our indicating models. Nevertheless, it closed last year on the weak side down from 2021. Pay attention to the Monthly level for any serious change in long-term trend ahead.

The perspective using the indicating ranges on the Daily level in the S&P 500 Cash Index, this market remains moderately bullish currently with underlying support beginning at 426682 and overhead resistance forming above at 429928. The market is trading closer to the resistance level at this time. An opening above this level in the next session will imply that a bounce is unfolding.

On the weekly level, the last important high was established the week of June 5th at 432262, which was up 12 weeks from the low made back during the week of March 13th. So far, this week is trading within last week's range of 432262 to 426107. Nevertheless, the market is still trading upward more toward resistance than support. A closing beneath last week's low would be a technical signal for a correction to retest support.

The broader perspective, this current rally into the week of June 5th reaching 432262 has exceeded the previous high of 421291 made back during the week of May 15th. Right now, the market is above momentum on our weekly models hinting this is still bullish for now as well as trend, long-term trend, and cyclical strength. Looking at this from a wider perspective, this market has been trading up for the past 12 weeks overall.

INTERMEDIATE-TERM OUTLOOK

YEARLY MOMENTUM MODEL INDICATOR

Our Momentum Models are declining at this time with the previous high made 2021 while the last low formed on 2022. However, this market has rallied in price with the last cyclical high formed on 2022 and thus we have a divergence warning that this market is starting to run out of strength on the upside.

After closing above last year's low of 366271.

Interestingly, the S&P 500 Cash Index has been in a bullish phase for the past 7 months since the low established back in October 2022.

The market is trading some 1.60% percent above the last high 423110 from which we did originally obtain one sell signal from that event established during May. Long-Term critical support still underlies this market at 416430 and only a break of that level on a monthly closing basis would warn of a break of the current uptrend. At this time, the market is holding and is trading above last month's high as well.

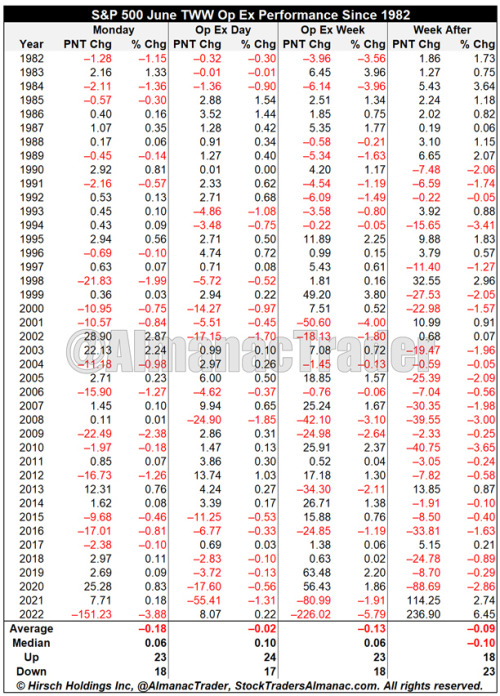

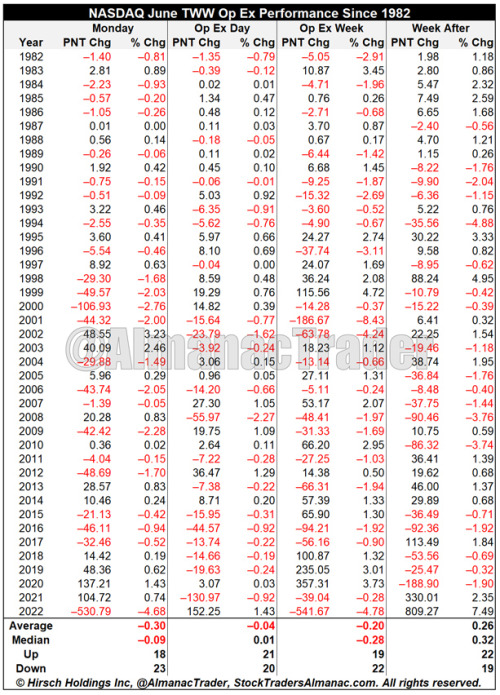

DiscoverGold June’s Quad Witching Options Expiration Riddled With Volatility

By: Almanac Trader | June 9, 2023

The second Triple Witching Week (Quadruple Witching if you prefer) of the year brings on some volatile trading with losses frequently exceeding gains. NASDAQ has the weakest record on the first trading day of the week. Triple-Witching Friday is usually better, S&P 500 has been up 12 of the last 20 years, but down 6 of the last 8.

Full-week performance is choppy as well, littered with greater than 1% moves in both directions. The week after June’s Triple-Witching Day is horrendous. This week has experienced DJIA losses in 27 of the last 33 years with an average performance of –0.81%. S&P 500 and NASDAQ have fared better during the week after over the same 33-year span. S&P 500’s averaged –0.46%. NASDAQ has averaged +0.03%. 2022’s sizable gains during the week after improve historical average performance notably.