This subsidiary has had a tremendous impact on the financial statements since Fiscal Q2 2017. While the net income of $248,679 may not appear significant, the sales of $6,630,973 allowed the company to execute its expansion plan for each subsidiary and continue to run at a profit.Snakes & Lattes Inc. has been operating with an increased staffing cost since Q4 due to the training of staff members for the new location. All of the new managers and some new staff members have been hired and have been training in the existing locations for the past few weeks, working towards the approximately 70 additional employees which will be required to staff the 3rd and largest location opening first week of September, dubbed 'Midtown'. Staff totals for the Snakes & Lagers Inc. / Snakes & Lattes Inc. subsidiary are now at 126 members. These costs, as well as costs for professional fees and construction, have been injected into the location to ensure that the opening of 'Midtown' proceeds as planned and immediately begins generating revenue. In addition, the subsidiary has been adding strength to the distribution and fulfillment division in preparation for further expansion into Fiscal 2018, with large revenue increases projected as a result.

(repost)Snakes DD: I fully expect margins to improve as they grow... The 2 Snakes locations + distribution have been supporting a good amount of overhead (including the EcoPr03 sub), for stuff like web design/maintaining thousands of products on the site, sales people that were getting the distribution segment going, accountants, lawyers, warehouses, etc, etc... but all of this infrastructure is in place now and capable of handling much more growth...

...and they are STILL turning a NET profit, after all of these startup/expansion expenses... Of course there will be additional expansion costs down the road, but for them to be able to support everything + turn a net profit, is impressive for the stage they are in... Frankly, i would not mind a small loss at this stage, even minor dilution, if it was used for rapid expansion.

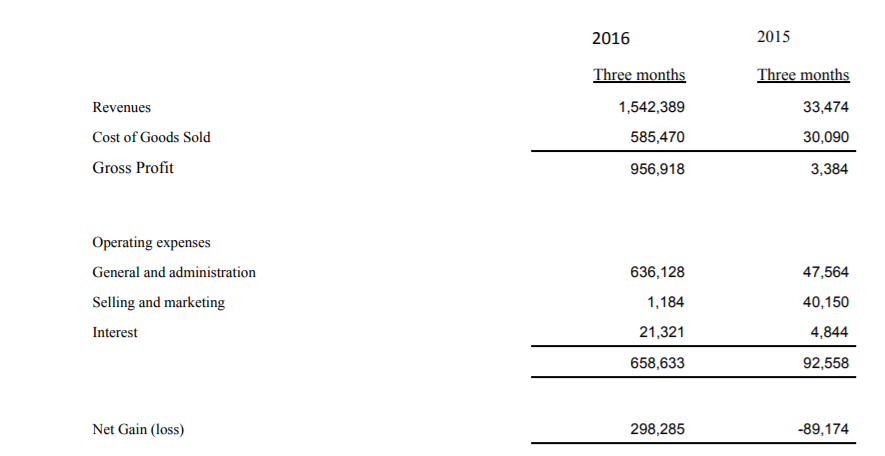

2 Q's ago they collected $300,000 in NET profits on $1,500,000 in revenues... and now we are landing single orders that almost match that entire quarters revs.

A stready flow of sold financial reports are coming. This is the best time to find an emerging growth stock. All ya gotta do is be patient...

Video tour of Snakes & Lattes:

The way the place is designed, its hard to see the size in a photo, but this video shows it well... and they pack this place often...

... and the new location will be even bigger/nicer/with more amenities, near the busiest foot traffic area in Canada...

Supported speculation: With July revenues ALONE approaching $2 million, you'll want to buy this dip imo

...because we will likely hit new all time highs heading into the next report, based on speculation. We could see $5+ million in Q1! We did $3+ million last Q and we are on a blistering growth pace during the first month of the fiscal year/Q1.

Its setup to be a perfect swing trade from now until the next Q, at a minimum.

The potential is .50+ in just months, with relatively low risk for a penny stock... cause when you start doing the math on GRO3, speculation can run wild. ONLY 10-15 large growers can equate to 8 figures and we have the best salesman = government(s)

Add a hot self published title into the mix + location #4 + BvB launch + Nintendo, etc and we are looking at a .01+ EPS potential by next year

If they can do $300K NET profits on $1.5 million revs when they are not investing heavy in expansion (like we witnessed in Q2), what does it equate to when they are making $25+ million? Am i crazy, or does the math work out?!

... and at THAT growth rate, a 100+ p/e would be in the cards imo. $1.00+ PPS

News

News  Market Data

Market Data  Discover

Discover