Wednesday, December 05, 2007 6:04:21 PM

http://www.321gold.com/editorials/banister/banister120507.html

HUI index resting before a large breakout

Juniors at fire sale prices

David Banister

Dec 5, 2007

"My favorite Junior is Southern Arc Minerals"

I've seen this movie before a few times in this gold bull market, and I already know the ending. For those contrarian investors like me, this, in my view, is your last chance to buy quality Junior gold exploration stocks at fire sale prices. Bull markets like to buck off as many investors as they can along the ride up. This one has been no different.

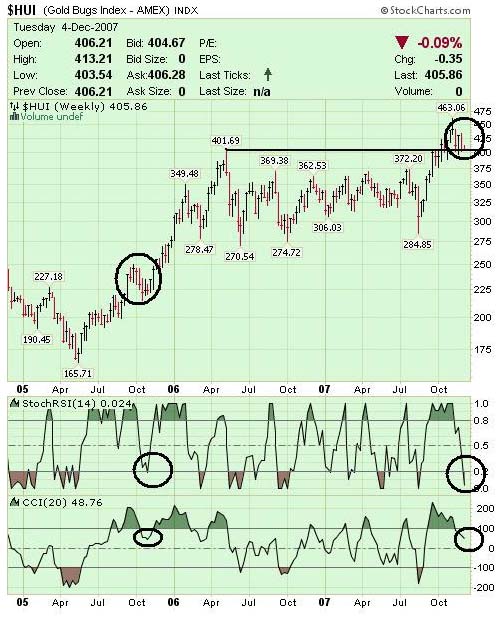

Let's start by examining the HUI index of "unhedged" gold companies. This index has always served me well by using technical analysis and "Elliott wave" theory. One thing I like to do is keep it as simple as I can. The HUI index broke out of its near 18 month base pattern this fall when it finally crept over the May 2006 highs of 401. The index rallied to 463 before recently pulling back in the October-November time window.

This particular pullback looks eerily like the fall of 2005. The HUI index then had begun to run off of extreme bottoms, and formed its first pullback. This is what I call a "wave 2" pullback. Quite simply, the herd has decided to pull their chips off the table assuming the run is over. Once again, the end of this movie will show that herd to be wrong. What we have now is the HUI index coming back to test the May 2006 levels one more time, and whilst doing so, the index has become extremely oversold. If you look at the chart I did here, you will see a strikingly similar pattern to the fall of 2005 pullback. In fact, I expect the HUI to eventually run up towards 600 from 405 today, with the intermediate peak around 525 along the way. The index is going to mimic the April 2005 to May 2006 move, only from much higher levels. Gold will be heading to about $980 per ounce US at its next pivot top.

There is not a lot of time left to enter at these fire sale levels. In a recent interview, John Embry, the Chief Investment Officer of Sprott Asset Management felt that Juniors are at their cheapest valuation levels since 2000-2001. He believes the fund he manages will return 100% or more in the next twelve months for the patient investors. The HUI index back then was at a low of 50, its now 405.

If Embry is right, and the charts that I have used successfully for this entire gold bull market are right, well, it's time to look for some Juniors to invest in at these "fire sale" prices. There are many that come to mind that are trading at 1% to 3% of inferred in situ ore valuations. The key is finding those with low capital costs to build a mine, low labor costs, and economic deposits. Many of the best Juniors are advanced in their exploration projects, are well cashed up, and have multiple drill results to review. The best of them will eventually have the opportunity to be bought out for anywhere between 10% to 40% of their proven and probable resources. Now is the time to invest aggressively in this sector while the inherent discounts to ore value are at extreme lows.

My favorite Junior is Southern Arc Minerals. SA has been written up on 321Gold.com in numerous articles from April through August of this year by Bob Moriarty, Omar Boulden, and Kevin Graham. Southern Arc has continued to drill off 600 meter deep drill holes of gold and copper intercepts all summer long. After six consecutively announced drill holes averaging 430 meters of gold and copper intercept per hole, they recently decided to secure a second drill to expand the work at the Selodong Intrusive Complex in Indonesia. They have identified fifteen - that's right, fifteen - separate porphyry style formations in the same 7km x 3km project area at Selodong. A simple trip to their website will lay it all out for you, including maps and historical drill results from Newmont Mining.

Recently, management decided to take this advanced exploration story on the road to New York, Boston, London, Zurich, Montreal, and Toronto. John Proust, CEO, and Hamish Campbell, chief geologist, conducted over thirty meetings. Following these meetings, Southern Arc announced this week a $12,000,000 brokered private placement at $1.20 per share with warrants. The offering book sold out in 48 hours, and from what I hear, John Proust was trying to find another 2,000,000 shares to help meet demand from one large fund group.

Why the interest? The stock has consolidated heady gains for the past seven months, after having gone from 20 cents in February to $2.48 in June. Southern Arc last did a private placement in March of this year at 30 cents. This offering was 400% higher only eight months later, and six times the value raised. Stocks like to consolidate big gains for many months at a time, until the volume dries up and they become "oversold". The timing for investors in the placement could not have been better, talk about an early holiday present. After completing six deep drill holes back to back all summer long, management felt "it is time to tell the story". Apparently the story was quite well received and I expect the share price to begin climbing into the new year. Once this offering officially closes, Southern Arc will have $11.3 million in the til, [till] plus current cash on hand of near 3 million, or in the neighborhood of $14.3 million. They recently added the second deep drill and now have two turning actively. They are securing a 3rd drill which will be able to drill down as far as 1,200 meters instead of the 700 meter limitations of the current drills. The company is fully cashed up for at least the next twelve to eighteen months of work at Selodong, let alone several other projects with blue sky.

Suffice to say that there will be a lot of news flow coming out of Southern Arc over the next twelve months as they expand the scope of their Selodong work and continue to prove up a potentially huge gold and copper resource deposit. John Proust, the CEO, has been an active buyer of the stock all summer long in the open markets, purchasing more as recently as November 29th. It's rare to find a quality junior with an advanced exploration project with insider buying, thirteen geologists on staff, and fast assay lab results from each drill hole. It's even more rare to find a project with the potential to equal that of the Batu Hijau deposit owned by Newmont Mining, and some are even putting Grasberg in the same sentence. Although there is quite a bit more drilling to do, the company trades at a fully diluted market cap of only about $112,000,000 as of this writing. Bob Moriarty hypothesized this summer after just four deep drill holes, that one could infer 270 million tones of ore already. They had only deep drilled four holes over just two of the fifteen porphyries identified. 270 million tones at about $25 per tonne is about 7 billion dollars of gross ore value. 10% of that figure is 700 million, or $8.50 per fully diluted share.

The stock is selling in the $1.30-$1.50 ranges of late. This calculation assumes there is no further blue sky on the project, and also assumes we are not giving Southern Arc any value for any of their other prospective properties in the prolific Indonesian arena. If we were to put a 5% inferred resource valuation on the figures above, the stock should be trading at $4.30 per fully diluted share today. To wit, Omar Boulden's piece this past June on 321Gold had a fair value of about $3.89 per share at the time, after only three deep drill holes, we now have had seven. Palmajero is good proxy to compare as well. They were acquired this summer for about $1.1 billion, or 40% of proven ore value. Southern Arc is currently trading at about 1.5% of inferred value with a lot of blue sky on this Selodong project to come.

Although this is certainly not a complete representation of all of the facts surrounding Southern Arc, it is but one example of many Juniors that are trading at severe discounts to potential takeover value. Many of the Senior Miners have publicly stated they are concerned about meeting the demand for gold and copper, but also replacing rapidly depleting reserves. I could list another ten juniors here, but Im [I'm] biased about Southern Arc and I am a shareholder. I have invested in some five and 10 baggers several times in the Junior sector, patience is usually difficult when the stock drifts for 6-7 months at a time, but when they start to move, they can really build steam.

With the HUI index ready to resume its advance, along with gold... now may be a good time to build your shopping list, but you probably shouldn't wait for much lower fire sale pricing, it's already here.

Dec 4, 2007

David Banister

email: dbanister@cox.net

David Banister is a Registered Representative with Investor's Capital Corporation and has a personal position in Southern Arc Minerals at the time of this writing. David has written for CBS Marketwatch.com in the past, has been on national radio, and has written articles for local newspapers on the topics of investing and economics. Please perform your own due diligence. All opinions expressed in this article are not the opinions of Investor's Capital, and should not be relied upon for advice.

321gold Ltd

Recent SA News

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 08/14/2024 04:28:33 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 08/14/2024 02:39:55 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 08/14/2024 10:00:40 AM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 08/07/2024 06:20:15 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 07/29/2024 08:20:47 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 07/26/2024 02:05:16 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 06/06/2024 07:38:38 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 05/30/2024 03:22:37 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 05/29/2024 07:44:09 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 05/29/2024 07:14:36 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 05/13/2024 09:24:26 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 05/13/2024 08:25:18 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 02/29/2024 03:20:59 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 02/14/2024 02:27:23 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 02/05/2024 04:59:47 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 01/24/2024 07:58:25 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 01/17/2024 03:42:26 PM

- Form 6-K/A - Report of foreign issuer [Rules 13a-16 and 15d-16]: [Amend] • Edgar (US Regulatory) • 01/16/2024 09:11:10 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 01/16/2024 03:51:40 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 01/02/2024 03:42:15 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 12/20/2023 03:18:45 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 12/14/2023 06:55:56 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 11/20/2023 04:50:15 PM

- Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16] • Edgar (US Regulatory) • 11/13/2023 10:26:52 PM

- Gold Stocks Shining on Bullion Rally as U.S. Fed Chief Hints at Rate Hike Pause, Dollar Weakens • AllPennyStocks.com • 10/27/2023 10:56:00 PM

VHAI - Vocodia Partners with Leading Political Super PACs to Revolutionize Fundraising Efforts • VHAI • Sep 19, 2024 11:48 AM

Dear Cashmere Group Holding Co. AKA Swifty Global Signs Binding Letter of Intent to be Acquired by Signing Day Sports • DRCR • Sep 19, 2024 10:26 AM

HealthLynked Launches Virtual Urgent Care Through Partnership with Lyric Health. • HLYK • Sep 19, 2024 8:00 AM

Element79 Gold Corp. Appoints Kevin Arias as Advisor to the Board of Directors, Strengthening Strategic Leadership • ELMGF • Sep 18, 2024 10:29 AM

Mawson Finland Limited Further Expands the Known Mineralized Zones at Rajapalot: Palokas step-out drills 7 metres @ 9.1 g/t gold & 706 ppm cobalt • MFL • Sep 17, 2024 9:02 AM

PickleJar Announces Integration With OptCulture to Deliver Holistic Fan Experiences at Venue Point of Sale • PKLE • Sep 17, 2024 8:00 AM