| Followers | 928 |

| Posts | 48631 |

| Boards Moderated | 0 |

| Alias Born | 07/22/2008 |

Wednesday, April 26, 2023 8:36:39 PM

Well, we lost 7.09¢ from our 20 day-closing-average convert-strike-point...the past couple days...

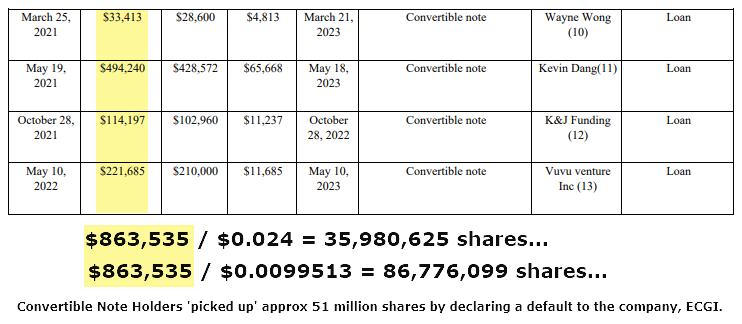

There are 5 convertible notes. #1 converts @ $3 and the holders seem oblivious (in AU) of even holding a note. All 5 notes are in default which from my DD indicates that they are not fixed conversions (@ 2.4¢, 60% of 4¢ ) any longer and, since default, are now calculated by taking 60% of the average closing price for the 20 days prior to conversion.

So, add up the closes for the past 20 days. Ex: .01025 + .01 + .0074 + .009 + .01, etc...divide that total by 20 (days). Then take 60% of that.

I got .33171 total for the 20 days including today. We lost .0379 (day 21, 3/28) and .033 (day 22, 3/27) from the 20-day-sum-calculation. That hurt.

.33171 / 20 days = average weighted price of .0165855.

60% of .0165855 = .0099513.

This is today's Conversion Price for the 4 convertible notes >> $0.0099513

Tomorrow we lose an .03 (day 20, 3/29) from our total and pick up perhaps an .01 for a net loss of .02 which would put us around .31171 / 20 days = average weighted price of .0155855. 60% of equals .0093513...

I had originally calculated the 4 convertibles using 60% of .04 (.024) to calculate the convertibles' conversion totals (all have the same terms). Now we have a variable conversion price. It's now (today, changes daily) 87 million shares if all were converted tonight or early tomorrow.

I believe this is accurate. CEO Wong can correct it if it's not...

Looks like a lot of shares but can easily be eaten up with a couple/few rally monkeys... :)

$ECGI

There are 5 convertible notes. #1 converts @ $3 and the holders seem oblivious (in AU) of even holding a note. All 5 notes are in default which from my DD indicates that they are not fixed conversions (@ 2.4¢, 60% of 4¢ ) any longer and, since default, are now calculated by taking 60% of the average closing price for the 20 days prior to conversion.

So, add up the closes for the past 20 days. Ex: .01025 + .01 + .0074 + .009 + .01, etc...divide that total by 20 (days). Then take 60% of that.

I got .33171 total for the 20 days including today. We lost .0379 (day 21, 3/28) and .033 (day 22, 3/27) from the 20-day-sum-calculation. That hurt.

.33171 / 20 days = average weighted price of .0165855.

60% of .0165855 = .0099513.

This is today's Conversion Price for the 4 convertible notes >> $0.0099513

Tomorrow we lose an .03 (day 20, 3/29) from our total and pick up perhaps an .01 for a net loss of .02 which would put us around .31171 / 20 days = average weighted price of .0155855. 60% of equals .0093513...

I had originally calculated the 4 convertibles using 60% of .04 (.024) to calculate the convertibles' conversion totals (all have the same terms). Now we have a variable conversion price. It's now (today, changes daily) 87 million shares if all were converted tonight or early tomorrow.

I believe this is accurate. CEO Wong can correct it if it's not...

Looks like a lot of shares but can easily be eaten up with a couple/few rally monkeys... :)

$ECGI

Recent ECGI News

- ECGI's Rezy.Fi Opens Investor Onboarding for Tokenized Mortgages on Avalanche; Nomyx Issuance Engine Powers Platform • ACCESS Newswire • 05/19/2026 12:30:00 PM

- ECGI Launches Rezy.Fi, Engages Axion OnChain as Consulting Advisor, and Validates Core Mortgage RWA Workflows • ACCESS Newswire • 04/09/2026 12:30:00 PM

- ECGI Signs Definitive $25 Million Agreement to Acquire RezyFi • InvestorsHub NewsWire • 03/24/2026 12:30:00 PM

- ECGI Signs Definitive $25 Million Agreement to Acquire RezyFi • ACCESS Newswire • 03/24/2026 12:30:00 PM

- ECGI Signs Definitive $25 Million Agreement to Acquire RezyFi • GlobeNewswire Inc. • 03/24/2026 12:30:00 PM

- UPDATE -- ECGI Building in Crypto's Top-Performing Sector as Tokenized Real-World Assets Surge Past $26 Billion • GlobeNewswire Inc. • 03/19/2026 01:39:51 PM

- ECGI Building in Crypto's Top-Performing Sector as Tokenized Real-World Assets Surge Past $26 Billion • InvestorsHub NewsWire • 03/19/2026 12:30:00 PM

- ECGI Building in Crypto's Top-Performing Sector as Tokenized Real-World Assets Surge Past $26 Billion • GlobeNewswire Inc. • 03/19/2026 12:30:00 PM

- ECGI Advances $10M Mortgage Tokenization Pilot as SEC Interpretation Adds Clarity • GlobeNewswire Inc. • 03/18/2026 01:11:07 PM

- ECGI Advances $10M Mortgage Tokenization Pilot as SEC Interpretation Adds Clarity • InvestorsHub NewsWire • 03/18/2026 12:45:50 PM

- ECGI Advances Mortgage Tokenization Pilot as Institutional Market Rails Continue to Develop • GlobeNewswire Inc. • 03/17/2026 12:39:33 PM

- ECGI Advances Mortgage Tokenization Pilot as Institutional Market Rails Continue to Develop • InvestorsHub NewsWire • 03/17/2026 12:30:00 PM

- ECGI Highlights RezyFi Live Pilot Progress in CEO Interview Update • GlobeNewswire Inc. • 03/03/2026 01:30:00 PM

- ECGI Highlights RezyFi Live Pilot Progress in CEO Interview Update • InvestorsHub NewsWire • 03/03/2026 01:30:00 PM

- ECGI Holdings and Nomyx Begin Live Pilot to Tokenize Up to $10 Million in Mortgage Loans on RezyFi • InvestorsHub NewsWire • 02/24/2026 01:30:00 PM

- ECGI Holdings and Nomyx Begin Live Pilot to Tokenize Up to $10 Million in Mortgage Loans on RezyFi • GlobeNewswire Inc. • 02/24/2026 01:30:00 PM

- ECGI Discusses Advancing Mortgage AI and Tokenization Strategy as RezyFi Definitive Agreement Nears Completion in Shareholder Letter • GlobeNewswire Inc. • 12/02/2025 01:30:00 PM

- ECGI Discusses Advancing Mortgage AI and Tokenization Strategy as RezyFi Definitive Agreement Nears Completion in Shareholder Letter • InvestorsHub NewsWire • 12/02/2025 01:30:00 PM

- ECGI Appoints AI Platform Architect as CTO to Build Mortgage Tokenization Infrastructure • GlobeNewswire Inc. • 11/13/2025 01:30:00 PM

- ECGI Appoints AI Platform Architect as CTO to Build Mortgage Tokenization Infrastructure • InvestorsHub NewsWire • 11/13/2025 01:30:00 PM

- ECGI Highlights Fintech Expansion Through RezyFi Acquisition and Tokenized Mortgage Platform in Shareholder Letter • InvestorsHub NewsWire • 11/11/2025 01:30:00 PM

- ECGI Highlights Fintech Expansion Through RezyFi Acquisition and Tokenized Mortgage Platform in Shareholder Letter • GlobeNewswire Inc. • 11/11/2025 01:30:00 PM

- ECGI Holdings Signs Binding $30 Million LOI to Acquire Licensed Mortgage Lender RezyFi • InvestorsHub NewsWire • 11/03/2025 01:30:00 PM

- ECGI Holdings Signs Binding $30 Million LOI to Acquire Licensed Mortgage Lender RezyFi • GlobeNewswire Inc. • 11/03/2025 01:30:00 PM

- ECGI Holdings Joins Entrepreneur Ventures to Expand Institutional Deal Flow • GlobeNewswire Inc. • 10/30/2025 12:30:00 PM