Wednesday, February 19, 2020 12:08:49 PM

>>> Massive 2020s Gold And Gold Stock Bull Market Is Just Beginning

Seeking Alpha

Feb. 16, 2020

Kirk Spano

https://seekingalpha.com/article/4324632-massive-2020s-gold-and-gold-stock-bull-market-is-just-beginning

Summary

After a period of fixing balance sheets, right sizing and de-risking, gold companies are poised to expand profits in the intermediate to long term.

Mergers have tightened exploration spending and consolidated operations to impose new discipline on the gold mining industry which will constrain production.

A toxic mix of global debt, aging demographics and poor fiscal policy by governments will lead to competitive currency devaluations leading to inflation.

Perpetual monetary stimulus and eventual "helicopter money" or MMT will cause a flight to safety that drives gold prices higher in the 2020s.

Low cost gold producers stand to benefit greatly as they gradually raise production into an inflating gold market in the 2020s.

This idea was discussed in more depth with members of my private investing community, Margin of Safety Investing. Get started today »

A combination of factors are leading to a secular bull market in gold and gold stocks. First, the gold industry is coming off a period of cleaning up balance sheets and right sizing operations. Further, industry consolidation via M&A is causing a more balanced gold supply and demand equation. Finally, QE for longer, government policy and potential other easy money policies are being used to offset demographically driven deflation. The inevitable outcome is inflation that devalues currencies and overwhelming government debts that drives gold to as high as $3000 per ounce.

My recommendation today is that investors buy or expand their holdings in the Van Eck Gold Miners ETF (GDX) on all pullbacks, making gold stocks a core 10-15% position in a portfolio for the 2020s, not just a satellite position.

I discussed the coming gold bull market in my most recent free Friday "Investing 2020s" webinar:

A Gold Bear Turns Buggy

I am neither a gold bear nor a gold bug. I am just letting the data take me where it leads. The data today screams for firm and rising gold prices, as well as, significant profits falling to the bottom lines of the top low cost gold producers.

In an April 2012 article, I discussed why the dollar would remain relatively strong for decades and at least partially, the global reserve currency. I also stated that "gold was done leading after a decade long rally." Commenters were sure to tell me that I was wrong in very colorful ways.

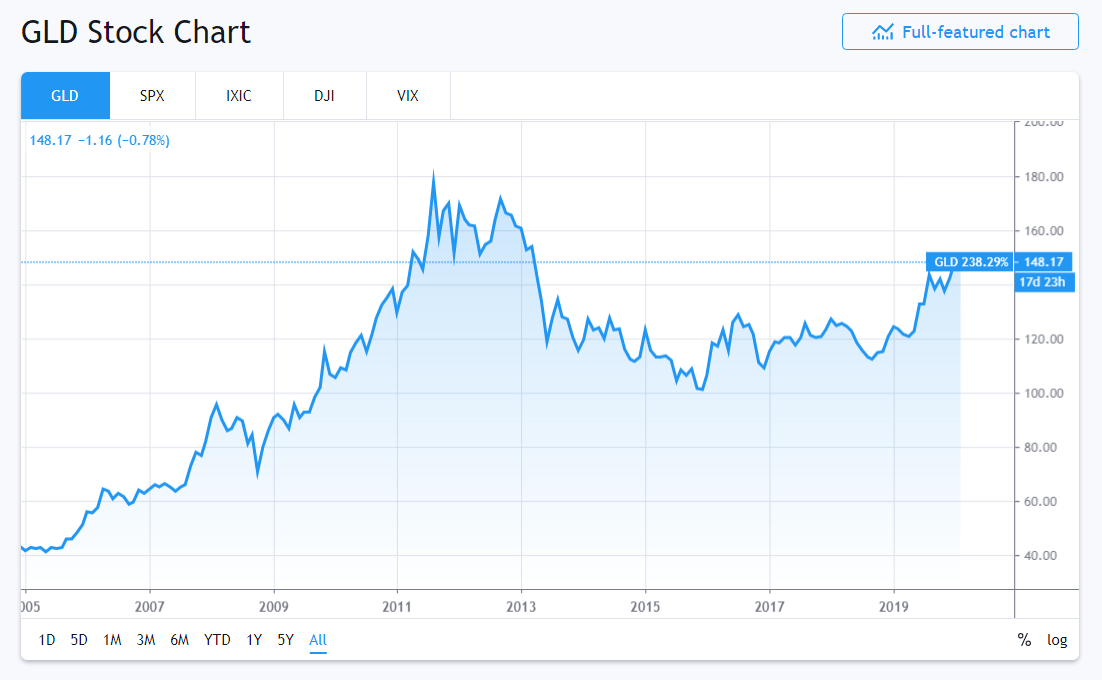

After my call on gold, from September 2012 through December 2015, the SPDR Gold Trust ETF (GLD) tracking the price of gold plunged over 40%.

GLD

In late 2018, I told clients of my firm and subscribers to Margin of Safety Investing that I was constructive on gold again. We made a few investments over then next few months on that thought. We are again looking to expand gold holdings as mentioned described and justified today.

Gold Industry M&A

The gold industry has seen massive consolidation in the past couple years and there appears to be another wave set to hit. Two massive deals creating the two largest gold miners, with about 30% of global production, happened in the past two years.

In autumn of 2018, Barrick (GOLD) bought Randgold in an $18 billion tie-up at the time creating the largest gold miner. By summer of 2019, Newmont (NEM) and GoldCorp merged to take the largest miner mantle by a nugget.

The creation of two powerhouses in precious metals mining has increased the oligopolistic qualities of the industry. Further, those companies are cooperating on a joint venture in Nevada that will save up to $5 billion for those companies over 20 years, with half of that savings in the first five years.

According to Kitco, M&A activity in 2019 rose to the highest levels since 2010. The Newmont deal accounted for two-thirds of that volume.

The expectation in 2020 is that smaller companies will merge in order to optimize their operations and expenses. The first big deal is Kirkland Gold (KL) buying Detour Gold for $3.5 billion.

The impact of the mergers is largely to combine assets to become more efficient and to further improve balance sheets. The typical result of large scale mergers in a sector is to slightly reduce competition and constrain supply which is obviously bullish for gold.

I expect the industry consolidation to continue with at least a few juniors with specific strategic assets being acquired.

Supply And Demand For Gold

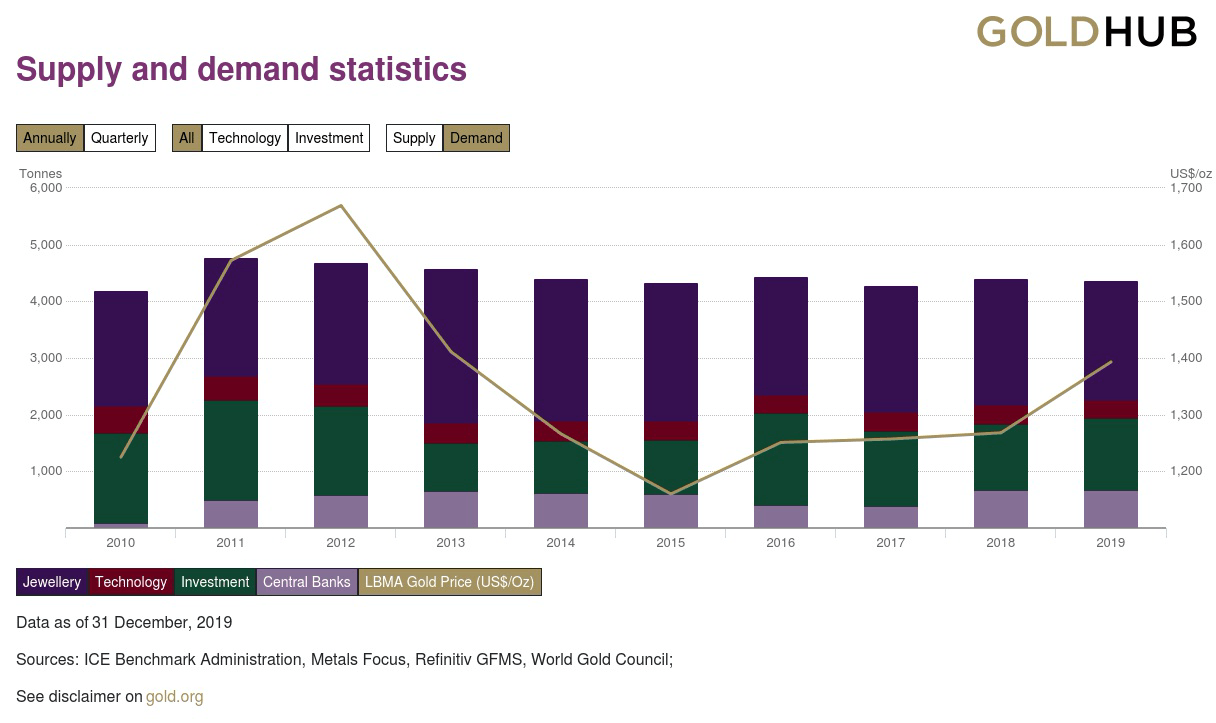

The World Gold Council provides excellent data on gold demand and supply. The following charts shows that gold demand has slightly fallen from the massive rally 8 to 10 years ago.

Gold Demand

The next chart shows that supply has edged up since the last gold bull market, but just barely.

Gold Supply

If the M&A activity described above, combined with more scarce economic resources in general, even prevents an increase of supply, that will be bullish for gold. If supply starts to drift down, even slowly, that will be extremely bullish for gold.

On the demand front, if we should see any catalysts for higher gold demand that will be bullish for gold. We know that demand is likely to slowly rise simply on the expansion of the global middle class. If other catalysts manifest, that will be extremely bullish for gold. Following are some of those potential "other catalysts."

A Word About Junior Gold Miners

The key for juniors are strong management, simplified business plans and solid balance sheets. In my opinion, they must also have some transformational asset already being developed, i.e. past the permitting stage, and on the cusp of dropping profits to the bottom line after the initial spending phases.

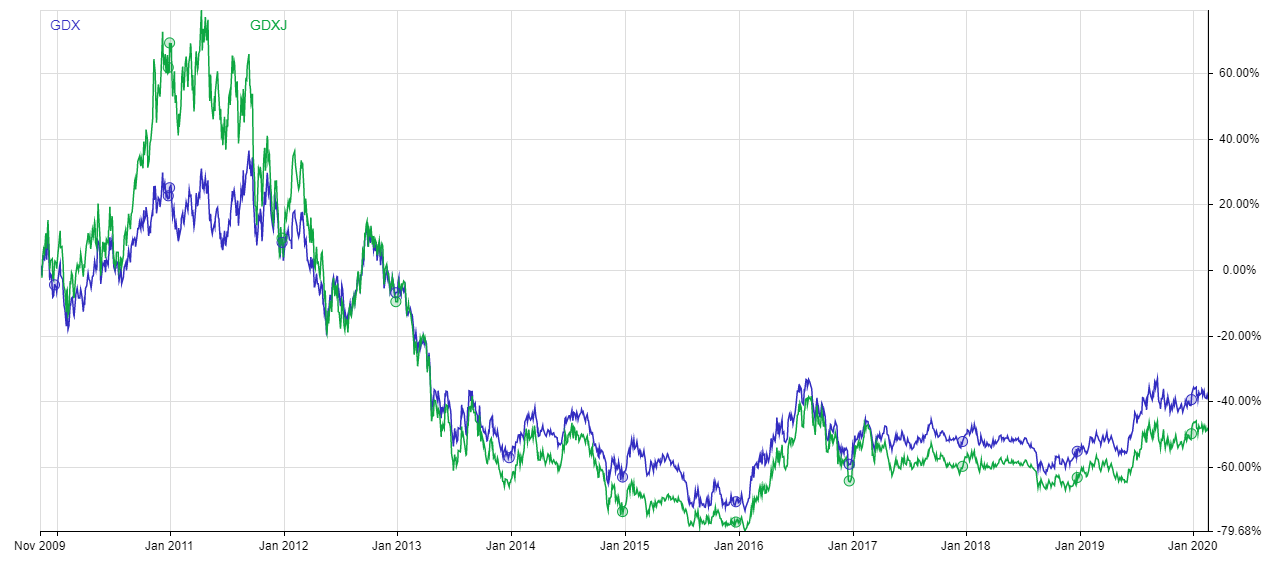

Too many people believe that the junior miners as a group are a strong investment in a rising gold environment. Since the inception of the Van Eck Junior Gold Miners ETF (GDXJ), it has trailed the mid and large cap focused GDX adjusted for dividends. I recommend GDXJ only for those inclined to trade technically.

Gold Miners ETFs GDX vs GDXJ

Members of MoSI are long Coeur Mining (CDE) and have been for over a year now. It is a buy at the moment under $6 per share. It can represent 1-4% of a portfolio depending on your risk level. We are long Coeur due to the company's move to be a fully North American company. The Silvertip mine is the transformational asset we are focused on. More information is available within MoSI with a search.

Aging Demographics, Government Budgets And Stagflation

Aging demographics are increasing the expenses of government and also slowing down the economy. The following chart shows the rising "over-65" age curve in the U.S. and falling velocity of money.

Older & Slower

What you are seeing is the inverse relationship of an aging population and the economic activity. While the Millennials entering peak earnings and household support years will offset this a bit, the damage is largely already being done. Consider the subdued GDP numbers the past decade.

Aging demographics are also driving national budgets as healthcare needs rise and pension programs payout. In the United States, while Medicare is very efficient, it is simply becoming overwhelmed with new beneficiaries as payroll taxes begin to fall short. Social Security was never meant to support people for decades, yet, that is what it is being asked to do.

Some estimates put outstanding, but unfunded, obligations at around $100 trillion. Social Security projects a $15 trillion shortfall over the next 75 years. This can largely be overcome by raising the full retirement age to 70 for most job classes (ex-heavy physical labor categories) and a cash infusion, i.e. the so-called "lock box" of Al Gore.

Medicare is the larger problem that government will have to deal with. As we have learned, there is no easy solution.

Greater healthcare competition does not work fully in an industry with monopoly pricing power, that is, anything that cannot be substituted, such as healthcare, is going to exhibit massive pricing power. Cutting healthcare benefits is a non-starter. Restricting compensation for providers, hospitals and pharma could lead to less innovation and access. Bottom line, it's complicated and as the Baby Boomers mature, is going to become even more expensive.

In my client letter describing the "Slow Growth Forever" global economy, I discuss aging demographics more in depth and allude to the distinct possibility that the 2020s could see a period of "stagflation." The 1970s proved that the relationship between inflation and unemployment is not always inverse. Outside factors can complicate the relationship.

In the 1970s, the oil embargos were the complicating factor. In the 2020s and 2030s, it will be the aging of the population and the onset of machine learning impacting the jobs market.

If we get stagflation, which I think is likely in the absence of structural reform of the economy, then we should look to the 1970s for what a good investment looks like. The period of stagflation ran from 1973 to 1982.

At the start of 1973 the price of gold was $64 per troy ounce. By the end of 1982 it was $447.

Central Bank QE For Longer

With aging demographics putting pressure on federal budgets and organic economic growth pressured, the likelihood for ongoing bouts of central bank quantitative easing are extremely high. We have seen it in Japan for decades.

While not announced as QE, an example is that the Federal Reserve has expanded its balance sheet by $800 billion since September to bailout and support the repo market. I believe the bailout was primarily done to prevent at least one and likely two or three financial institutions (hedge funds or banks that lend to hedge funds) from having a Long Term Capital moment. The cash was likely needed to allow at least one hedge fund to wind down leveraged bets and a possibly a bank to recapitalize losses on hedge fund lending. I do have an idea of who these institutions were through sources in Connecticut and New York, however, without further confirmation would be speculating.

Further, more U.S. Treasuries and less cash on the balance sheets of the four banks that do most of the lending in the repo markets will continue to put pressure on repo or overnight lending. This of course speaks to a broader problem of less cash on the balance sheets of banks due to absorbing more U.S. government debt.

In this environment of rising debt, competitive devaluations are likely to occur. What one central bank does to fix domestic budget problems, other central banks will follow with corresponding policies.

As the economy struggles with debt issues brought about by aging demographics, central banks, especially in the absence of smart fiscal policy, will need to continue with easy money operations to allow governments to continue creating debt. Quantitative easing and possibly other more experimental means of easy money, such as Modern Monetary Theory or MMT, ultimately will lead to inflation.

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output... Milton Friedman

Helicopter Money Is Inevitable

In order to "fix" the growth, inflation and unemployment problems coming to the economy, politicians will resort to more exotic measures. We are seeing right now that tax cuts primarily to the wealthy raise debt without raising growth rates.

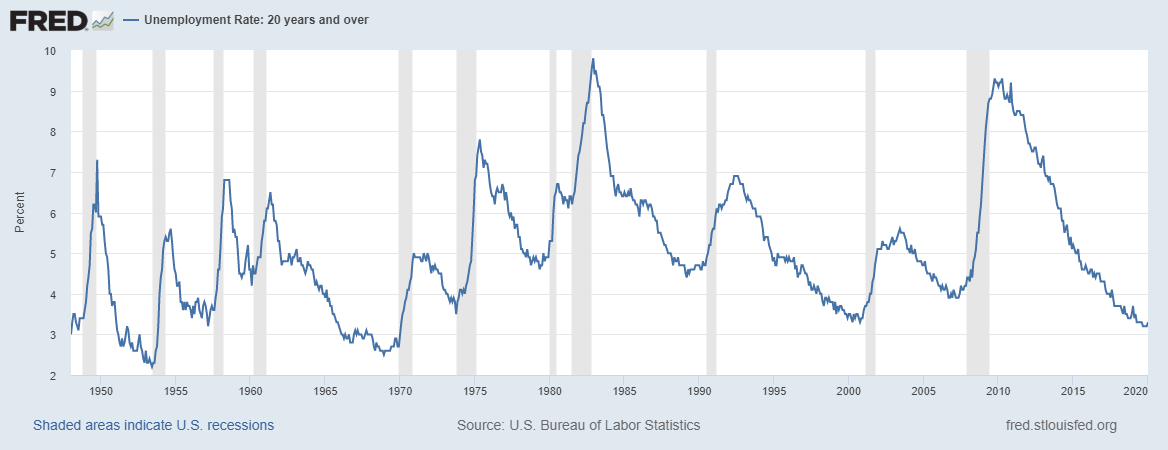

Currently, we are in a low unemployment economy, but that is more a result of a long recovery, than anything else. Without more organic economic growth brought about by smart fiscal policy, unemployment is likely to reverse soon.

Unemployment

With any dramatic rise in unemployment, a recession will follow. I believe this will be the first step to implementing "helicopter money" to try to fix the structural economic problems that we face.

Milton Friedman's quote above points out that excessive money creation will unlock inflation. We have seen that in asset prices. The reason we do not see it in all of our everyday prices is that economic growth is slow and we the velocity of money has plummeted due to an aging population.

These are unique ideas I am discussing. But, let's follow to the logical conclusion, even if we do not get there in a straight line via our political process.

Eventually, "helicopter money," another Friedman idea will be employed. This is the large and sudden introduction of actual "printed money" into the economy. This is different than QE as that creates a debit on the other side of the balance sheet that theoretically means it will have to be paid off - it won't be.

The fear with "helicopter money" is that it will create hyperinflation. The "banana republic" effect or Weimar Republic impact. If money is simply rained from the skies to spend by the public as it sees fit, then yes, the Austrian economists will be right and we will see hyperinflation. In that case, gold is king.

Ultimately, the goal of "helicopter money" should be to "fix" structural problems. My fear is we simply paper over the problems described above, much in the same way that MMT would do. We will see what transpires.

My guess is that our political process lets us down at least once and we see "helicopter money" more than once. Eventually, I believe the money would be printed and placed into a "lock box" for the retirement system. In this case, the money would trickle money out for decades via Social Security and pension payments creating a small offsetting inflationary impact versus the deflationary pressures of aging demographics.

That last paragraph is vitally important. I do not have faith that most of our representatives understand the economics I am pointing to. For certain, those who champion MMT do not understand. Neither do those who believe "tax cutting" our way to prosperity works for more than a hot minute.

For investors, whether we see better or worse policy, and, once or several times creating money, the outcome is clear. There will be inflationary monetary policy in the face of deflationary economic pressures.

The argument for gold is not bullish or bearish, but bullish or more bullish.

Buy The Dips On Gold And Gold Stocks

Investors at my firm and investment letters bought Newmont Mining (NEM) at the merger with Gold Corp. We simultaneously wrote covered calls which expired because we understood the mathematical implications of the merger. We also sold cash-secured puts. We own Newmont Goldcorp today and would buy more on technical corrections as we believe it to be the best gold company in the world.

Barrick Gold (GOLD) is also under consideration and we are in the process of a deep dive. Kirkland Gold recently made our radar after a member discussed the company in the MoSI chat. As mentioned own Coeur Mining which we are also buying on technical dips.

I recommend expanding your gold stock holdings as the companies are likely to benefit from stable to higher gold prices. The easy solution is to buy the Van Eck Gold Miners ETF (GDX) to a very low double digit percentage of your overall asset allocation, inclusive of any stocks held individually. I would not exceed 20% of allocation to gold stocks or gold proper, and closer to the low to middle teens is a better allocation.

I am not buying physical gold ETFs at this time, Gold ETFs, such as the SPDR Gold Trust (GLD) and IShares Gold (IAU). I consider these swing trading vehicles to be used in conjunction with technical analysis. In general, the leverage with the best miners will outperform the actual price of gold.

GDX v GLD

I do think owning some pretty gold coins that you might pass on is a fun approach to wealth accumulation. I say fun, because we will never use those as currency and if we devolve into barter, I want food and fuel. I don't want Bitcoin either, which is the topic of an upcoming discussion.

We believe the 2020s are going to be more volatile than the last decade. With that in mind, you must build a margin of safety into all of your investment decisions. Our focus is to help you do that whether you focus on growth or growth & income.

Kirk Spano and the MoSI analysts offer deep research and a 4-step approach to finding great opportunities and managing risk. Join us today and get your first year of Margin of Safety Investing for 20% off.

Disclosure: I am/we are long GDX, NEM, CDE.

<<<

Seeking Alpha

Feb. 16, 2020

Kirk Spano

https://seekingalpha.com/article/4324632-massive-2020s-gold-and-gold-stock-bull-market-is-just-beginning

Summary

After a period of fixing balance sheets, right sizing and de-risking, gold companies are poised to expand profits in the intermediate to long term.

Mergers have tightened exploration spending and consolidated operations to impose new discipline on the gold mining industry which will constrain production.

A toxic mix of global debt, aging demographics and poor fiscal policy by governments will lead to competitive currency devaluations leading to inflation.

Perpetual monetary stimulus and eventual "helicopter money" or MMT will cause a flight to safety that drives gold prices higher in the 2020s.

Low cost gold producers stand to benefit greatly as they gradually raise production into an inflating gold market in the 2020s.

This idea was discussed in more depth with members of my private investing community, Margin of Safety Investing. Get started today »

A combination of factors are leading to a secular bull market in gold and gold stocks. First, the gold industry is coming off a period of cleaning up balance sheets and right sizing operations. Further, industry consolidation via M&A is causing a more balanced gold supply and demand equation. Finally, QE for longer, government policy and potential other easy money policies are being used to offset demographically driven deflation. The inevitable outcome is inflation that devalues currencies and overwhelming government debts that drives gold to as high as $3000 per ounce.

My recommendation today is that investors buy or expand their holdings in the Van Eck Gold Miners ETF (GDX) on all pullbacks, making gold stocks a core 10-15% position in a portfolio for the 2020s, not just a satellite position.

I discussed the coming gold bull market in my most recent free Friday "Investing 2020s" webinar:

A Gold Bear Turns Buggy

I am neither a gold bear nor a gold bug. I am just letting the data take me where it leads. The data today screams for firm and rising gold prices, as well as, significant profits falling to the bottom lines of the top low cost gold producers.

In an April 2012 article, I discussed why the dollar would remain relatively strong for decades and at least partially, the global reserve currency. I also stated that "gold was done leading after a decade long rally." Commenters were sure to tell me that I was wrong in very colorful ways.

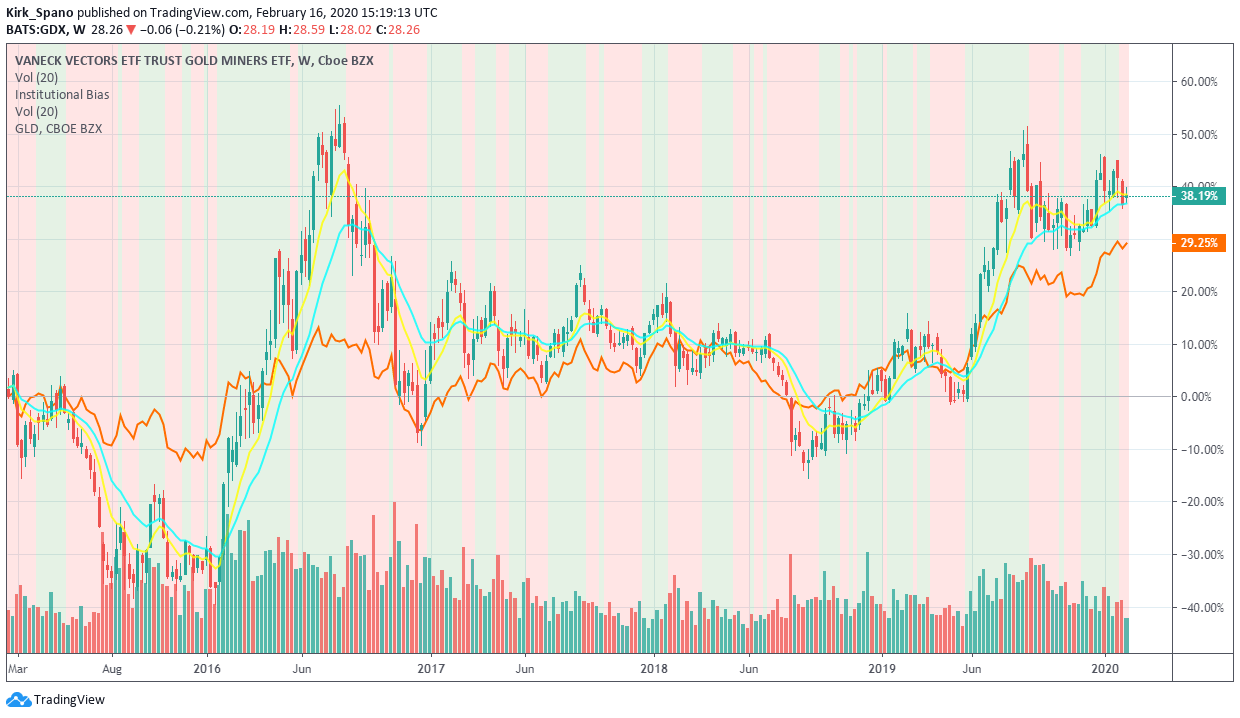

After my call on gold, from September 2012 through December 2015, the SPDR Gold Trust ETF (GLD) tracking the price of gold plunged over 40%.

GLD

In late 2018, I told clients of my firm and subscribers to Margin of Safety Investing that I was constructive on gold again. We made a few investments over then next few months on that thought. We are again looking to expand gold holdings as mentioned described and justified today.

Gold Industry M&A

The gold industry has seen massive consolidation in the past couple years and there appears to be another wave set to hit. Two massive deals creating the two largest gold miners, with about 30% of global production, happened in the past two years.

In autumn of 2018, Barrick (GOLD) bought Randgold in an $18 billion tie-up at the time creating the largest gold miner. By summer of 2019, Newmont (NEM) and GoldCorp merged to take the largest miner mantle by a nugget.

The creation of two powerhouses in precious metals mining has increased the oligopolistic qualities of the industry. Further, those companies are cooperating on a joint venture in Nevada that will save up to $5 billion for those companies over 20 years, with half of that savings in the first five years.

According to Kitco, M&A activity in 2019 rose to the highest levels since 2010. The Newmont deal accounted for two-thirds of that volume.

The expectation in 2020 is that smaller companies will merge in order to optimize their operations and expenses. The first big deal is Kirkland Gold (KL) buying Detour Gold for $3.5 billion.

The impact of the mergers is largely to combine assets to become more efficient and to further improve balance sheets. The typical result of large scale mergers in a sector is to slightly reduce competition and constrain supply which is obviously bullish for gold.

I expect the industry consolidation to continue with at least a few juniors with specific strategic assets being acquired.

Supply And Demand For Gold

The World Gold Council provides excellent data on gold demand and supply. The following charts shows that gold demand has slightly fallen from the massive rally 8 to 10 years ago.

Gold Demand

The next chart shows that supply has edged up since the last gold bull market, but just barely.

Gold Supply

If the M&A activity described above, combined with more scarce economic resources in general, even prevents an increase of supply, that will be bullish for gold. If supply starts to drift down, even slowly, that will be extremely bullish for gold.

On the demand front, if we should see any catalysts for higher gold demand that will be bullish for gold. We know that demand is likely to slowly rise simply on the expansion of the global middle class. If other catalysts manifest, that will be extremely bullish for gold. Following are some of those potential "other catalysts."

A Word About Junior Gold Miners

The key for juniors are strong management, simplified business plans and solid balance sheets. In my opinion, they must also have some transformational asset already being developed, i.e. past the permitting stage, and on the cusp of dropping profits to the bottom line after the initial spending phases.

Too many people believe that the junior miners as a group are a strong investment in a rising gold environment. Since the inception of the Van Eck Junior Gold Miners ETF (GDXJ), it has trailed the mid and large cap focused GDX adjusted for dividends. I recommend GDXJ only for those inclined to trade technically.

Gold Miners ETFs GDX vs GDXJ

Members of MoSI are long Coeur Mining (CDE) and have been for over a year now. It is a buy at the moment under $6 per share. It can represent 1-4% of a portfolio depending on your risk level. We are long Coeur due to the company's move to be a fully North American company. The Silvertip mine is the transformational asset we are focused on. More information is available within MoSI with a search.

Aging Demographics, Government Budgets And Stagflation

Aging demographics are increasing the expenses of government and also slowing down the economy. The following chart shows the rising "over-65" age curve in the U.S. and falling velocity of money.

Older & Slower

What you are seeing is the inverse relationship of an aging population and the economic activity. While the Millennials entering peak earnings and household support years will offset this a bit, the damage is largely already being done. Consider the subdued GDP numbers the past decade.

Aging demographics are also driving national budgets as healthcare needs rise and pension programs payout. In the United States, while Medicare is very efficient, it is simply becoming overwhelmed with new beneficiaries as payroll taxes begin to fall short. Social Security was never meant to support people for decades, yet, that is what it is being asked to do.

Some estimates put outstanding, but unfunded, obligations at around $100 trillion. Social Security projects a $15 trillion shortfall over the next 75 years. This can largely be overcome by raising the full retirement age to 70 for most job classes (ex-heavy physical labor categories) and a cash infusion, i.e. the so-called "lock box" of Al Gore.

Medicare is the larger problem that government will have to deal with. As we have learned, there is no easy solution.

Greater healthcare competition does not work fully in an industry with monopoly pricing power, that is, anything that cannot be substituted, such as healthcare, is going to exhibit massive pricing power. Cutting healthcare benefits is a non-starter. Restricting compensation for providers, hospitals and pharma could lead to less innovation and access. Bottom line, it's complicated and as the Baby Boomers mature, is going to become even more expensive.

In my client letter describing the "Slow Growth Forever" global economy, I discuss aging demographics more in depth and allude to the distinct possibility that the 2020s could see a period of "stagflation." The 1970s proved that the relationship between inflation and unemployment is not always inverse. Outside factors can complicate the relationship.

In the 1970s, the oil embargos were the complicating factor. In the 2020s and 2030s, it will be the aging of the population and the onset of machine learning impacting the jobs market.

If we get stagflation, which I think is likely in the absence of structural reform of the economy, then we should look to the 1970s for what a good investment looks like. The period of stagflation ran from 1973 to 1982.

At the start of 1973 the price of gold was $64 per troy ounce. By the end of 1982 it was $447.

Central Bank QE For Longer

With aging demographics putting pressure on federal budgets and organic economic growth pressured, the likelihood for ongoing bouts of central bank quantitative easing are extremely high. We have seen it in Japan for decades.

While not announced as QE, an example is that the Federal Reserve has expanded its balance sheet by $800 billion since September to bailout and support the repo market. I believe the bailout was primarily done to prevent at least one and likely two or three financial institutions (hedge funds or banks that lend to hedge funds) from having a Long Term Capital moment. The cash was likely needed to allow at least one hedge fund to wind down leveraged bets and a possibly a bank to recapitalize losses on hedge fund lending. I do have an idea of who these institutions were through sources in Connecticut and New York, however, without further confirmation would be speculating.

Further, more U.S. Treasuries and less cash on the balance sheets of the four banks that do most of the lending in the repo markets will continue to put pressure on repo or overnight lending. This of course speaks to a broader problem of less cash on the balance sheets of banks due to absorbing more U.S. government debt.

In this environment of rising debt, competitive devaluations are likely to occur. What one central bank does to fix domestic budget problems, other central banks will follow with corresponding policies.

As the economy struggles with debt issues brought about by aging demographics, central banks, especially in the absence of smart fiscal policy, will need to continue with easy money operations to allow governments to continue creating debt. Quantitative easing and possibly other more experimental means of easy money, such as Modern Monetary Theory or MMT, ultimately will lead to inflation.

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output... Milton Friedman

Helicopter Money Is Inevitable

In order to "fix" the growth, inflation and unemployment problems coming to the economy, politicians will resort to more exotic measures. We are seeing right now that tax cuts primarily to the wealthy raise debt without raising growth rates.

Currently, we are in a low unemployment economy, but that is more a result of a long recovery, than anything else. Without more organic economic growth brought about by smart fiscal policy, unemployment is likely to reverse soon.

Unemployment

With any dramatic rise in unemployment, a recession will follow. I believe this will be the first step to implementing "helicopter money" to try to fix the structural economic problems that we face.

Milton Friedman's quote above points out that excessive money creation will unlock inflation. We have seen that in asset prices. The reason we do not see it in all of our everyday prices is that economic growth is slow and we the velocity of money has plummeted due to an aging population.

These are unique ideas I am discussing. But, let's follow to the logical conclusion, even if we do not get there in a straight line via our political process.

Eventually, "helicopter money," another Friedman idea will be employed. This is the large and sudden introduction of actual "printed money" into the economy. This is different than QE as that creates a debit on the other side of the balance sheet that theoretically means it will have to be paid off - it won't be.

The fear with "helicopter money" is that it will create hyperinflation. The "banana republic" effect or Weimar Republic impact. If money is simply rained from the skies to spend by the public as it sees fit, then yes, the Austrian economists will be right and we will see hyperinflation. In that case, gold is king.

Ultimately, the goal of "helicopter money" should be to "fix" structural problems. My fear is we simply paper over the problems described above, much in the same way that MMT would do. We will see what transpires.

My guess is that our political process lets us down at least once and we see "helicopter money" more than once. Eventually, I believe the money would be printed and placed into a "lock box" for the retirement system. In this case, the money would trickle money out for decades via Social Security and pension payments creating a small offsetting inflationary impact versus the deflationary pressures of aging demographics.

That last paragraph is vitally important. I do not have faith that most of our representatives understand the economics I am pointing to. For certain, those who champion MMT do not understand. Neither do those who believe "tax cutting" our way to prosperity works for more than a hot minute.

For investors, whether we see better or worse policy, and, once or several times creating money, the outcome is clear. There will be inflationary monetary policy in the face of deflationary economic pressures.

The argument for gold is not bullish or bearish, but bullish or more bullish.

Buy The Dips On Gold And Gold Stocks

Investors at my firm and investment letters bought Newmont Mining (NEM) at the merger with Gold Corp. We simultaneously wrote covered calls which expired because we understood the mathematical implications of the merger. We also sold cash-secured puts. We own Newmont Goldcorp today and would buy more on technical corrections as we believe it to be the best gold company in the world.

Barrick Gold (GOLD) is also under consideration and we are in the process of a deep dive. Kirkland Gold recently made our radar after a member discussed the company in the MoSI chat. As mentioned own Coeur Mining which we are also buying on technical dips.

I recommend expanding your gold stock holdings as the companies are likely to benefit from stable to higher gold prices. The easy solution is to buy the Van Eck Gold Miners ETF (GDX) to a very low double digit percentage of your overall asset allocation, inclusive of any stocks held individually. I would not exceed 20% of allocation to gold stocks or gold proper, and closer to the low to middle teens is a better allocation.

I am not buying physical gold ETFs at this time, Gold ETFs, such as the SPDR Gold Trust (GLD) and IShares Gold (IAU). I consider these swing trading vehicles to be used in conjunction with technical analysis. In general, the leverage with the best miners will outperform the actual price of gold.

GDX v GLD

I do think owning some pretty gold coins that you might pass on is a fun approach to wealth accumulation. I say fun, because we will never use those as currency and if we devolve into barter, I want food and fuel. I don't want Bitcoin either, which is the topic of an upcoming discussion.

We believe the 2020s are going to be more volatile than the last decade. With that in mind, you must build a margin of safety into all of your investment decisions. Our focus is to help you do that whether you focus on growth or growth & income.

Kirk Spano and the MoSI analysts offer deep research and a 4-step approach to finding great opportunities and managing risk. Join us today and get your first year of Margin of Safety Investing for 20% off.

Disclosure: I am/we are long GDX, NEM, CDE.

<<<

Join the InvestorsHub Community

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.