I like what I'm seeing so far, but their anticipation of relying on a rev share model concerns me. AAH is not a license holder and (at least so far) does not appear to intend to be a license holder, it's essentially a pick and shovel play. In fact, on their deck slide covering potential CA projects they specifically state that the growers will provide the license.

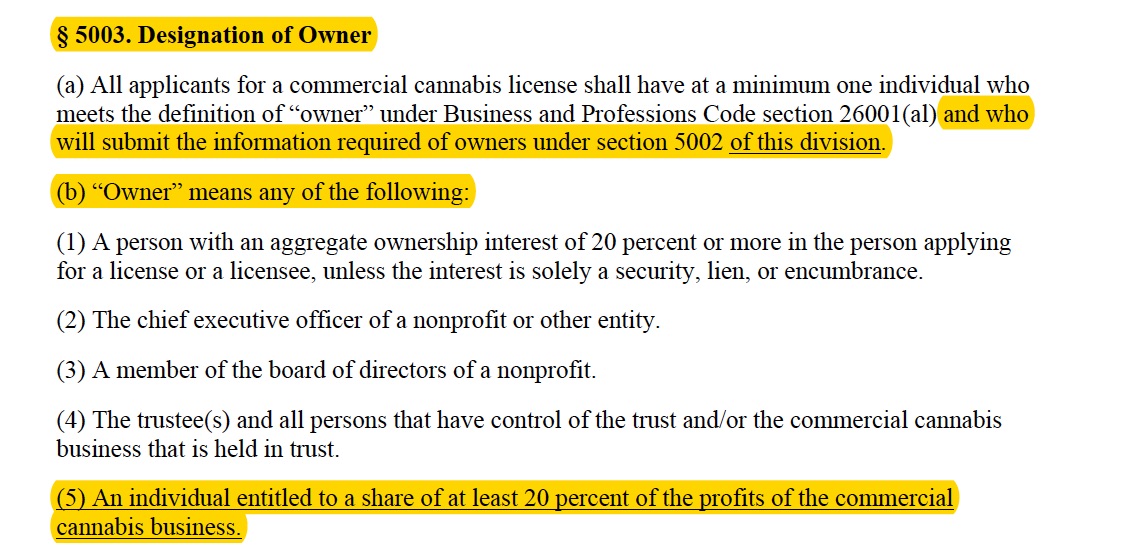

However, CA regulations may not allow for that in the future - and perhaps other jurisdictions may not allow it either. For example in the latest draft CA regs, this would qualify AAH as an "owner" of the cannabis biz and AAH would need to be listed as an applicant on the underlying cannabis license for each grower/customer. This brings up several questions for me:

1. First and foremost, would a grower actually be willing to list AAH on its cannabis license? (seems unlikely, but maybe I'm wrong)

2. If AAH would somehow get listed on a license, has it considered its potential exposure to products liability for a plant product that is not really a part of its core competency - manufacturing technological equipment (for growing plant products)

2. If revenue sharing is untenable, what's their pivot? (of the three this seems most critical to understand)

Again, these are draft regs (https://cannabis.ca.gov/cannabis-regulations/)- so they're not in play yet. And, this is only for CA (but, CA is a huge market) and the draft regs at least shine a light on where the state is headed even if the outcome will not 100% match the language in this draft.

Moreover, the address of the growing premise also must be listed on the license. And, that premise has to meet a number of other requirements - including licensure at the local level (which - depending on the locality can be difficult to obtain) prior to being granted a state-level license. AAH can't just drop a pod anywhere and start commercially growing cannabis as implied in their deck.

I can think of ways AAH could get around this - a straight subscription/lease model (w/no rev share), for example, but their lack of even acknowledging that this could be a road bump (considering how heavily they are selling this aspect to investors) gives me concern - if for no other reason than because it suggests they're either 1) unaware of their own risks and haven't fleshed out a potential pivot, or 2) not disclosing the actual foreseeable risks to investors.

Also, their benchmark for a pound of indoor is way off. They give a spread of $1300-$2600, when it's really closer to just $1,300. I haven't heard of pounds going for more than $2k for several years now.

In sum, I think the product is good - but I'm cautious about the numbers, which sound inflated and don't account for the real risks to their current business model. Most concerning though - I'm not convinced they understand the potential impact of the still-often changing regulatory environment on their current business model.

News

News  Market Data

Market Data  Discover

Discover